Financial Accounting Principles Report - Semester 1, University

VerifiedAdded on 2020/12/09

|23

|2809

|163

Report

AI Summary

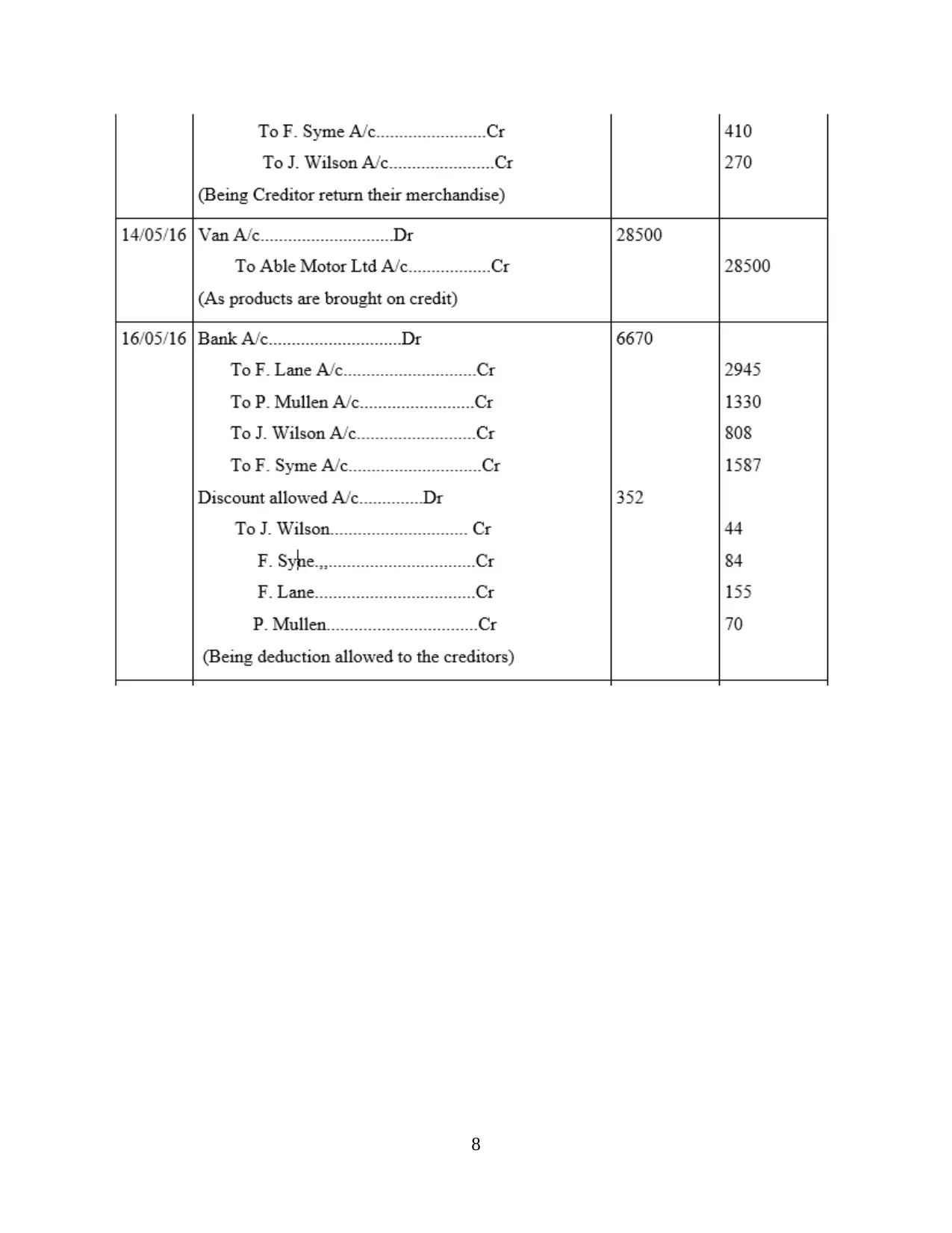

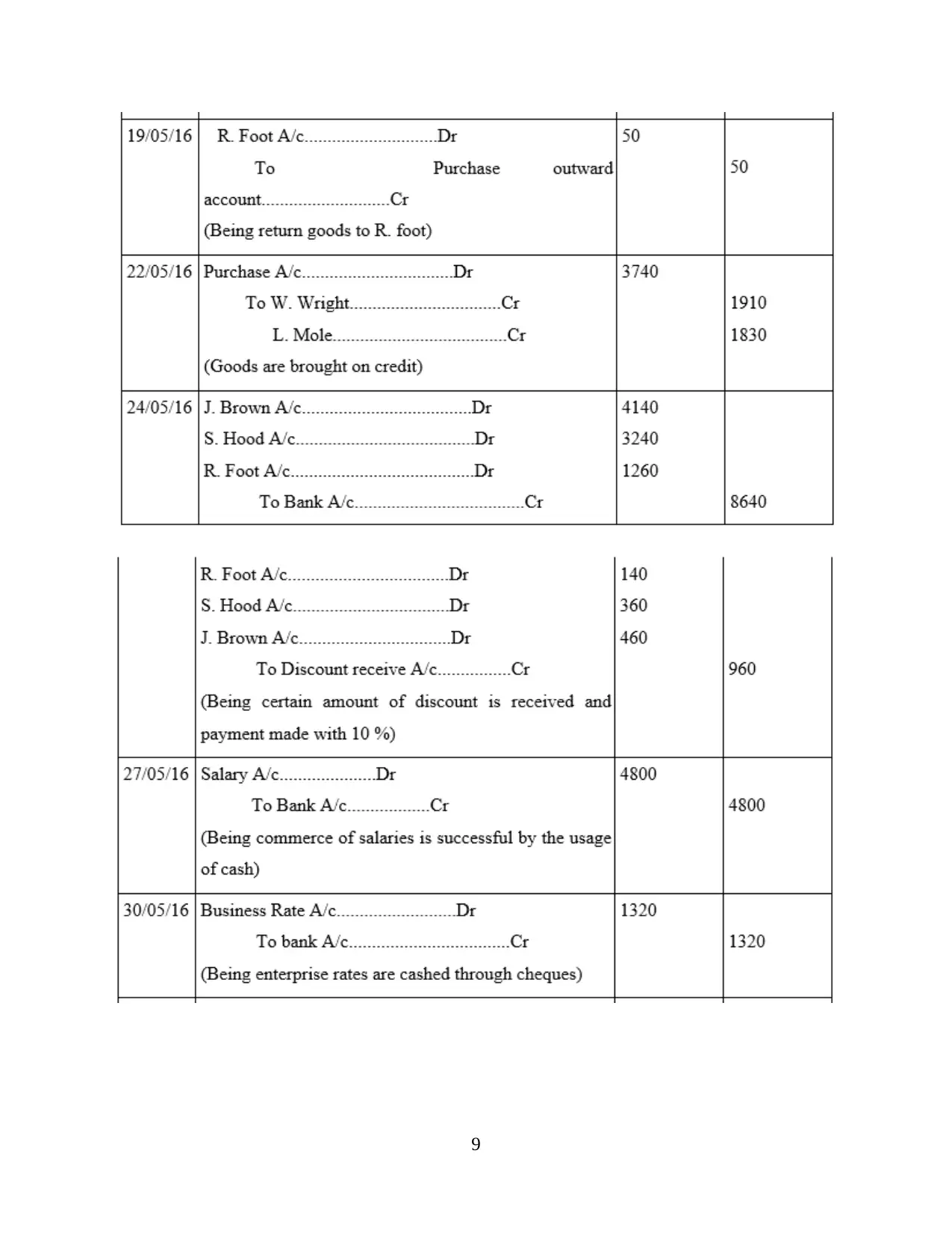

This report provides a detailed overview of financial accounting principles. It begins with an introduction to financial accounting, defining its role in summarizing, analyzing, and interpreting business transactions, and explaining the preparation of financial statements like the statement of profit and loss, balance sheet, and cash flow statement. The report then explores the regulations and regulatory bodies such as IASB and FASB that govern financial accounting, emphasizing the importance of standards like IFRS and US-GAAP in ensuring reliable and fair financial reporting. It also covers key accounting rules, including double-entry principles (debit and credit), and accounting principles such as revenue recognition, historical cost, and matching principles. Furthermore, the report discusses accounting conventions like material disclosure and consistency, highlighting their significance in preparing financial statements. Part B of the report demonstrates practical application of double-entry recording and accounting concepts like consistency and prudence. This report is a valuable resource for students studying finance and accounting. Desklib provides past papers and solved assignments for students.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.