Financial Accounting: Principles, Regulations, and Client Cases

VerifiedAdded on 2021/01/02

|35

|6213

|120

Homework Assignment

AI Summary

This assignment delves into the core principles of financial accounting, exploring its purpose, regulations (GAAP, IFRS, IASB), and fundamental concepts. It defines financial accounting as the process of recording, summarizing, and reporting financial transactions to external users, such as investors and creditors. The assignment details accounting rules and principles, including the economic entity, monetary unit, and going concern assumptions, emphasizing the importance of consistency and material disclosure. The document then applies these principles to analyze journal entries, ledgers, and financial statements for six different clients, including calculations and explanations related to purchases, sales, and various financial transactions. It covers topics like depreciation, bank reconciliation, control accounts, and suspense accounts, providing a comprehensive overview of financial accounting applications. The assignment also highlights the importance of full disclosure and consistent accounting practices for accurate financial reporting.

FINANCIAL ACCOUNTING PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Main Body.......................................................................................................................................3

A. Defining financial Accounting and its purpose......................................................................3

B. Explaining the regulation relating to the financial accounting...............................................4

C. Describing accounting rules and principles............................................................................4

D. Explaining the conventions and concepts relating to consistency and material disclosure.. .5

CLIENT 1........................................................................................................................................6

CLIENT 2........................................................................................................................................8

CLIENT 3......................................................................................................................................10

C) Explaining concepts of consistency and prudence...............................................................13

D) Purpose of depreciation and methods of calculating depreciation.......................................13

CLIENT 4......................................................................................................................................14

Purpose of preparing bank reconciliation statement.................................................................14

Explaining areas which cause record vary with bank records..................................................14

Preparing accounts through cash flow statement......................................................................14

CLIENT 5......................................................................................................................................15

A). Preparing control accounts..................................................................................................15

B) Explaining need of preparation of control account..............................................................16

CLIENT 6......................................................................................................................................16

A) Meaning of suspense account and highlighting features.....................................................16

INTRODUCTION...........................................................................................................................3

Main Body.......................................................................................................................................3

A. Defining financial Accounting and its purpose......................................................................3

B. Explaining the regulation relating to the financial accounting...............................................4

C. Describing accounting rules and principles............................................................................4

D. Explaining the conventions and concepts relating to consistency and material disclosure.. .5

CLIENT 1........................................................................................................................................6

CLIENT 2........................................................................................................................................8

CLIENT 3......................................................................................................................................10

C) Explaining concepts of consistency and prudence...............................................................13

D) Purpose of depreciation and methods of calculating depreciation.......................................13

CLIENT 4......................................................................................................................................14

Purpose of preparing bank reconciliation statement.................................................................14

Explaining areas which cause record vary with bank records..................................................14

Preparing accounts through cash flow statement......................................................................14

CLIENT 5......................................................................................................................................15

A). Preparing control accounts..................................................................................................15

B) Explaining need of preparation of control account..............................................................16

CLIENT 6......................................................................................................................................16

A) Meaning of suspense account and highlighting features.....................................................16

B. Drafting a trail balance.........................................................................................................17

C Trial balance suspense account.............................................................................................17

D) Differentiate between suspense and clearing account.........................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

C Trial balance suspense account.............................................................................................17

D) Differentiate between suspense and clearing account.........................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is an important field for ant organisation. It helps in in recording and summarising the financial

transaction of a company that helps in preparing the financial statements and financial reporting of the company for the external users .

This statements are very helpful for the external users in order to make their decisions regarding the investment in the company. The

present report will help in understanding the financial accounting and the purpose of preparing it. The report will also discuss the

various regulations and standard related to the financial accounting. Further the report will include the accounting rules and principles.

The report will include the consistency and full disclosure principle of accounting. Furthermore, the report will include calculations of

the financial statement for the different clients.

Main Body

A. Defining financial Accounting and its purpose.

It is the process of tracking all the financial transaction of a company. With the help of a specialised guidelines, financial

accounting helps the transaction to be properly recorded, summarised and presented is well manner form of a report which are known

as financial statements or reports. Financial accounting focus on providing the information of the financial performance and the

business activities of the company to the external users of the company like shareholders, investors and other people outside the

business organisation (Edwards, 2013). Financial information of the company are summarised in the form of the financial statements,

which are balance sheet, income statements, profit and loss statements etc.

Financial statesman are being prepared on the routine schedules that is quarterly, half-yearly or annually. These statements are

important to external users of the business organisation that helps them to make decisions regarding investing in the company or not.

The financial reporting is also very helpful for the management also in order to make decisions and strategies for further growth and

development of the company.

The main purpose of the financial accounting are as follows:

Financial accounting is an important field for ant organisation. It helps in in recording and summarising the financial

transaction of a company that helps in preparing the financial statements and financial reporting of the company for the external users .

This statements are very helpful for the external users in order to make their decisions regarding the investment in the company. The

present report will help in understanding the financial accounting and the purpose of preparing it. The report will also discuss the

various regulations and standard related to the financial accounting. Further the report will include the accounting rules and principles.

The report will include the consistency and full disclosure principle of accounting. Furthermore, the report will include calculations of

the financial statement for the different clients.

Main Body

A. Defining financial Accounting and its purpose.

It is the process of tracking all the financial transaction of a company. With the help of a specialised guidelines, financial

accounting helps the transaction to be properly recorded, summarised and presented is well manner form of a report which are known

as financial statements or reports. Financial accounting focus on providing the information of the financial performance and the

business activities of the company to the external users of the company like shareholders, investors and other people outside the

business organisation (Edwards, 2013). Financial information of the company are summarised in the form of the financial statements,

which are balance sheet, income statements, profit and loss statements etc.

Financial statesman are being prepared on the routine schedules that is quarterly, half-yearly or annually. These statements are

important to external users of the business organisation that helps them to make decisions regarding investing in the company or not.

The financial reporting is also very helpful for the management also in order to make decisions and strategies for further growth and

development of the company.

The main purpose of the financial accounting are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The main purpose of the financial accounting is to create information of the financial performance of the company in a form of

financial statements.

The financial statement should be in a form that can be understand by the external users which helps them in making the

decisions regarding the investment purpose in company.

B. Explaining the regulation relating to the financial accounting.

Financial accounting is the preparation of financial statements by analysing, summarising and reporting all the financial data.

It helps the external users to understand the financial performance of the company.

Financial accounting is governed by by local as well as the international accounting standard for financial reporting. Following

are the regulations related to the financial accounting

GAAP: Generally Accepted Accounting Principles are the commonly followed accounting rules and standards for financial reporting

(Horngren and et.al., 2012). This regulation helps in ensuring that the financial reporting is transparent and consist of relevant

information of financial performance.

IFRS: International Financial Reporting Standard is a set of the standard that provide a frameworks to the companies the way to

prepare and disclose their financial statements. IFRS helps in providing the general guidance for the preparation of the financial

statements . It is important for the companies to adopt a global level standard that will help them to simply the procedures by allowing

a company to use one type of accounting all over thee world.

IASB: International Accounting Standard Board is the organisation that established the IFRS all over the world. This organisation is

consist of the 14 members from all over the world that helps in setting the accounting standard, preparing the accounting reports and

accounting educations.

financial statements.

The financial statement should be in a form that can be understand by the external users which helps them in making the

decisions regarding the investment purpose in company.

B. Explaining the regulation relating to the financial accounting.

Financial accounting is the preparation of financial statements by analysing, summarising and reporting all the financial data.

It helps the external users to understand the financial performance of the company.

Financial accounting is governed by by local as well as the international accounting standard for financial reporting. Following

are the regulations related to the financial accounting

GAAP: Generally Accepted Accounting Principles are the commonly followed accounting rules and standards for financial reporting

(Horngren and et.al., 2012). This regulation helps in ensuring that the financial reporting is transparent and consist of relevant

information of financial performance.

IFRS: International Financial Reporting Standard is a set of the standard that provide a frameworks to the companies the way to

prepare and disclose their financial statements. IFRS helps in providing the general guidance for the preparation of the financial

statements . It is important for the companies to adopt a global level standard that will help them to simply the procedures by allowing

a company to use one type of accounting all over thee world.

IASB: International Accounting Standard Board is the organisation that established the IFRS all over the world. This organisation is

consist of the 14 members from all over the world that helps in setting the accounting standard, preparing the accounting reports and

accounting educations.

C. Describing accounting rules and principles.

Accounting is the process of summarizing, organising and recording in a terms of money, transactions which helps in

understanding the business activities of the organisation (May, 2013). Accounting not just record the financial transactions of the

company but also helps in analysing and converting them in the manner that can be understandable to both company and to the

external users. It can be presented in the form of the financial information.

There are general rules and concepts which govern the field of accounting. The rules of accounting refereed to as basic

accounting principles and guidelines. The Financial Accounting Standard Board(FASB) are using the basic accounting standard and

guidelines as basis of the set of accounting rules and guidelines.

The basic rules of accounting as per the FASB , that if a company is distributed its financial statements to the public, it

required to follow the guidelines by GAAP (Henderson and et.al., 2015). It is an important regulation as it helps in regulate

accounting definitions, assumptions and ,method of accounting. Following are some accounting principles which are widely used in

accounting:

Economy Entity assumptions

Monetary unit Assumptions

Time period assumptions

Cost principles

Full disclosure principles

Going concern principles

Matching principles (What are Accounting Principles | List of Top Accounting Principles , 2019).

Revenue recognition

Accounting is the process of summarizing, organising and recording in a terms of money, transactions which helps in

understanding the business activities of the organisation (May, 2013). Accounting not just record the financial transactions of the

company but also helps in analysing and converting them in the manner that can be understandable to both company and to the

external users. It can be presented in the form of the financial information.

There are general rules and concepts which govern the field of accounting. The rules of accounting refereed to as basic

accounting principles and guidelines. The Financial Accounting Standard Board(FASB) are using the basic accounting standard and

guidelines as basis of the set of accounting rules and guidelines.

The basic rules of accounting as per the FASB , that if a company is distributed its financial statements to the public, it

required to follow the guidelines by GAAP (Henderson and et.al., 2015). It is an important regulation as it helps in regulate

accounting definitions, assumptions and ,method of accounting. Following are some accounting principles which are widely used in

accounting:

Economy Entity assumptions

Monetary unit Assumptions

Time period assumptions

Cost principles

Full disclosure principles

Going concern principles

Matching principles (What are Accounting Principles | List of Top Accounting Principles , 2019).

Revenue recognition

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Materiality

Conservatism

D. Explaining the conventions and concepts relating to consistency and material disclosure.

Consistency:

It is the concept of the accounting principles which states that the company should follow the same accounting method for

over and over again. Consistency concept assumes that an accounting procedure or method once adopted should be applied

consistently in future also (Macve, 2015). If a company is using a method this year and changes subsequently to another method the

very next year it will be difficult for the users to compare the financial statements of different year.

The principles also implies that a business can change its method of accounting treatment but only when there are sound and

valid reasonable grounds. The company has to make sure that the reason for changing the method and the detail of treatment of the

new method should be be disclose in its annual financial reports and statements. This concept is important because of the need of

comparability of the financial statements by the external users.

Material Disclosure:

According to this conventions of the accounting principles, the company while preparing the income statement should disclose

each relevant information in the footnote of the statements. The information can be related to the function of its financial statements or

the business activity. This principles helps to ensure the stockholders and investors are not misguided with any aspects of the financial

report (Barth, 2015). The management of the company has to report all the information about the company's operations to creditors

and investors in their accounting reports.

The relevant information can be anything that could change the decisions of the outside users of the accounting reports

external user can analyse such information and interpret these financial statements to make informed and detailed decisions. Thus full

Conservatism

D. Explaining the conventions and concepts relating to consistency and material disclosure.

Consistency:

It is the concept of the accounting principles which states that the company should follow the same accounting method for

over and over again. Consistency concept assumes that an accounting procedure or method once adopted should be applied

consistently in future also (Macve, 2015). If a company is using a method this year and changes subsequently to another method the

very next year it will be difficult for the users to compare the financial statements of different year.

The principles also implies that a business can change its method of accounting treatment but only when there are sound and

valid reasonable grounds. The company has to make sure that the reason for changing the method and the detail of treatment of the

new method should be be disclose in its annual financial reports and statements. This concept is important because of the need of

comparability of the financial statements by the external users.

Material Disclosure:

According to this conventions of the accounting principles, the company while preparing the income statement should disclose

each relevant information in the footnote of the statements. The information can be related to the function of its financial statements or

the business activity. This principles helps to ensure the stockholders and investors are not misguided with any aspects of the financial

report (Barth, 2015). The management of the company has to report all the information about the company's operations to creditors

and investors in their accounting reports.

The relevant information can be anything that could change the decisions of the outside users of the accounting reports

external user can analyse such information and interpret these financial statements to make informed and detailed decisions. Thus full

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

disclosure principle of accounting emphasizes that any piece of data that can change the decisions of the external users should be

included in the report.

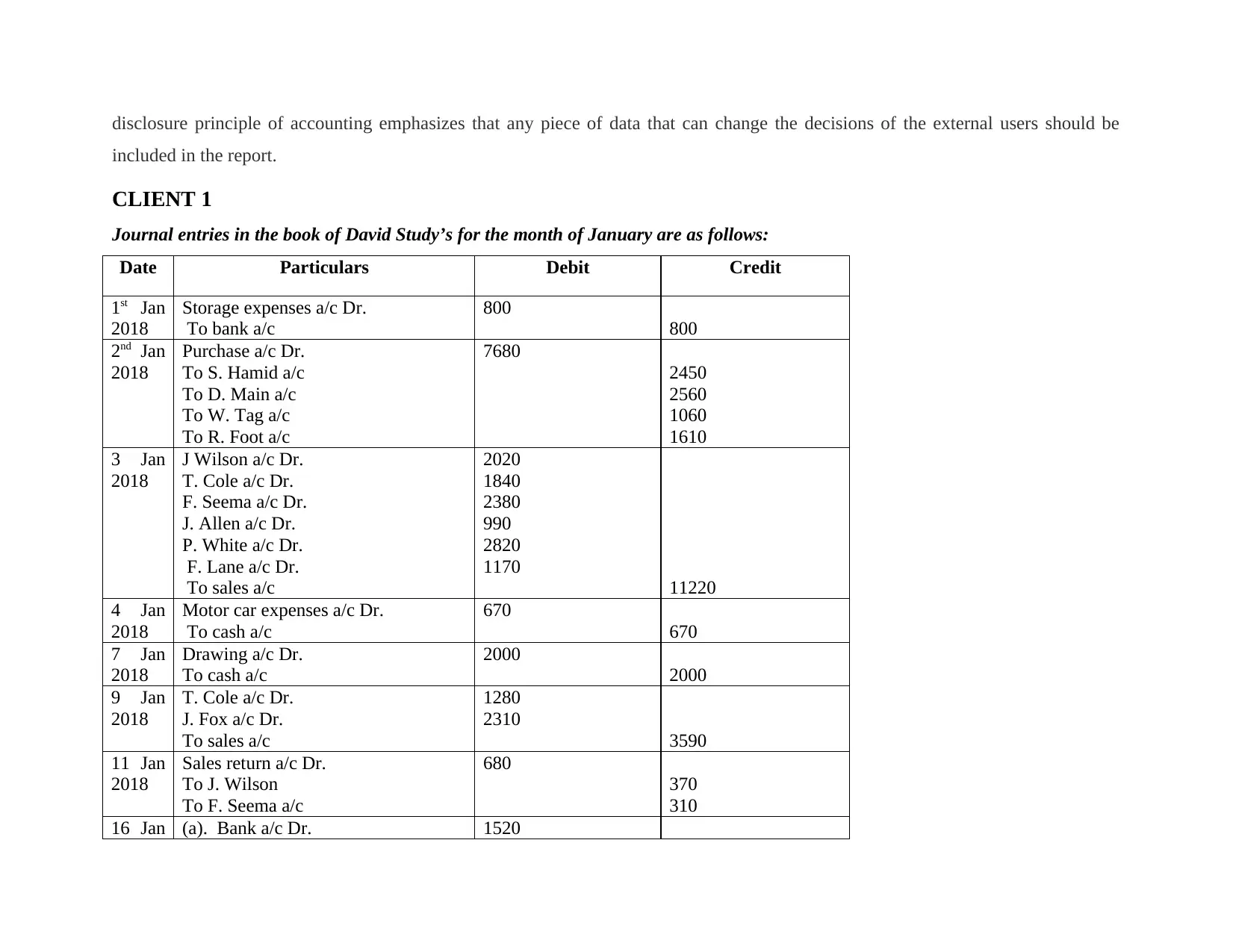

CLIENT 1

Journal entries in the book of David Study’s for the month of January are as follows:

Date Particulars Debit Credit

1st Jan

2018

Storage expenses a/c Dr.

To bank a/c

800

800

2nd Jan

2018

Purchase a/c Dr.

To S. Hamid a/c

To D. Main a/c

To W. Tag a/c

To R. Foot a/c

7680

2450

2560

1060

1610

3 Jan

2018

J Wilson a/c Dr.

T. Cole a/c Dr.

F. Seema a/c Dr.

J. Allen a/c Dr.

P. White a/c Dr.

F. Lane a/c Dr.

To sales a/c

2020

1840

2380

990

2820

1170

11220

4 Jan

2018

Motor car expenses a/c Dr.

To cash a/c

670

670

7 Jan

2018

Drawing a/c Dr.

To cash a/c

2000

2000

9 Jan

2018

T. Cole a/c Dr.

J. Fox a/c Dr.

To sales a/c

1280

2310

3590

11 Jan

2018

Sales return a/c Dr.

To J. Wilson

To F. Seema a/c

680

370

310

16 Jan (a). Bank a/c Dr. 1520

included in the report.

CLIENT 1

Journal entries in the book of David Study’s for the month of January are as follows:

Date Particulars Debit Credit

1st Jan

2018

Storage expenses a/c Dr.

To bank a/c

800

800

2nd Jan

2018

Purchase a/c Dr.

To S. Hamid a/c

To D. Main a/c

To W. Tag a/c

To R. Foot a/c

7680

2450

2560

1060

1610

3 Jan

2018

J Wilson a/c Dr.

T. Cole a/c Dr.

F. Seema a/c Dr.

J. Allen a/c Dr.

P. White a/c Dr.

F. Lane a/c Dr.

To sales a/c

2020

1840

2380

990

2820

1170

11220

4 Jan

2018

Motor car expenses a/c Dr.

To cash a/c

670

670

7 Jan

2018

Drawing a/c Dr.

To cash a/c

2000

2000

9 Jan

2018

T. Cole a/c Dr.

J. Fox a/c Dr.

To sales a/c

1280

2310

3590

11 Jan

2018

Sales return a/c Dr.

To J. Wilson

To F. Seema a/c

680

370

310

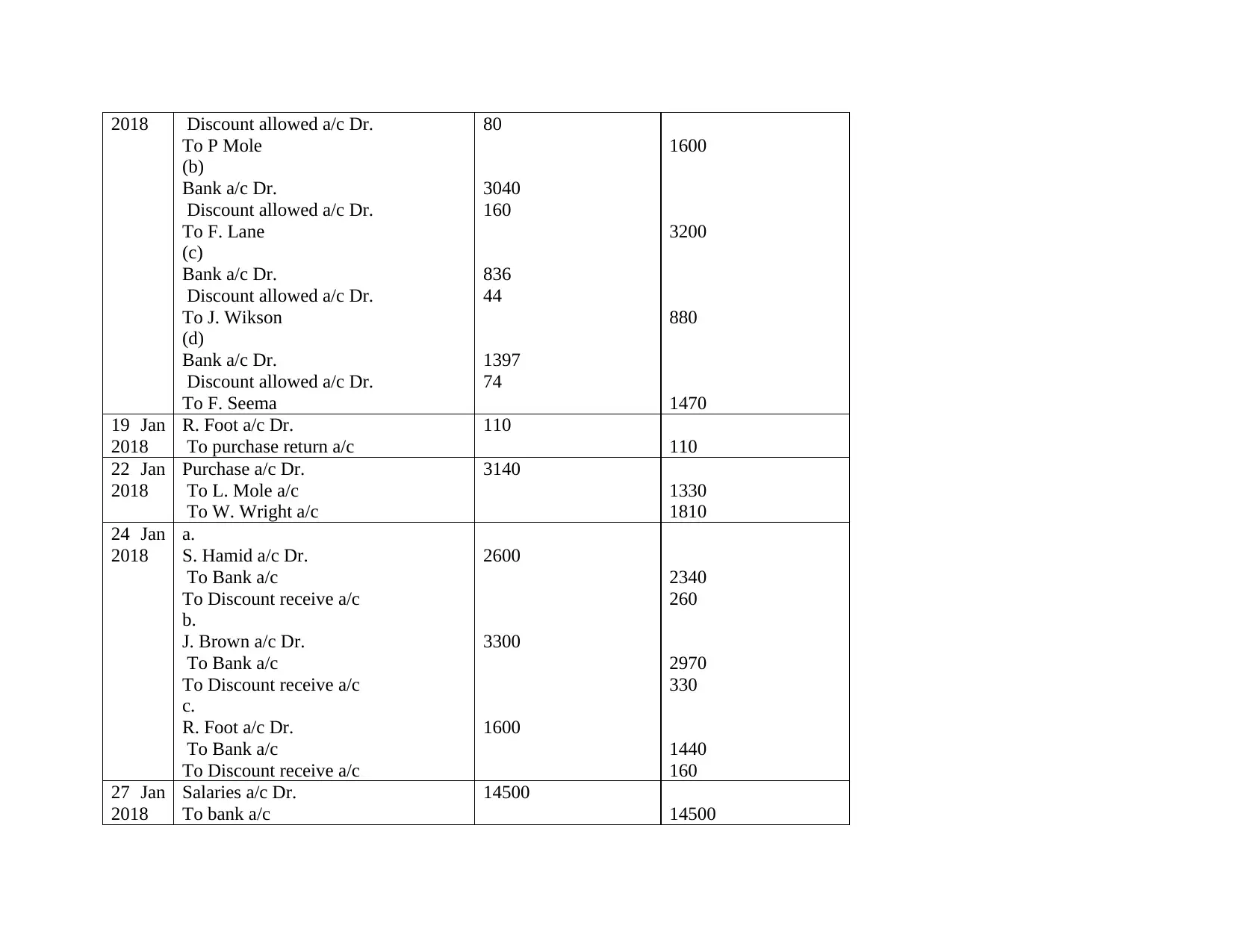

16 Jan (a). Bank a/c Dr. 1520

2018 Discount allowed a/c Dr.

To P Mole

(b)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Lane

(c)

Bank a/c Dr.

Discount allowed a/c Dr.

To J. Wikson

(d)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Seema

80

3040

160

836

44

1397

74

1600

3200

880

1470

19 Jan

2018

R. Foot a/c Dr.

To purchase return a/c

110

110

22 Jan

2018

Purchase a/c Dr.

To L. Mole a/c

To W. Wright a/c

3140

1330

1810

24 Jan

2018

a.

S. Hamid a/c Dr.

To Bank a/c

To Discount receive a/c

b.

J. Brown a/c Dr.

To Bank a/c

To Discount receive a/c

c.

R. Foot a/c Dr.

To Bank a/c

To Discount receive a/c

2600

3300

1600

2340

260

2970

330

1440

160

27 Jan

2018

Salaries a/c Dr.

To bank a/c

14500

14500

To P Mole

(b)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Lane

(c)

Bank a/c Dr.

Discount allowed a/c Dr.

To J. Wikson

(d)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Seema

80

3040

160

836

44

1397

74

1600

3200

880

1470

19 Jan

2018

R. Foot a/c Dr.

To purchase return a/c

110

110

22 Jan

2018

Purchase a/c Dr.

To L. Mole a/c

To W. Wright a/c

3140

1330

1810

24 Jan

2018

a.

S. Hamid a/c Dr.

To Bank a/c

To Discount receive a/c

b.

J. Brown a/c Dr.

To Bank a/c

To Discount receive a/c

c.

R. Foot a/c Dr.

To Bank a/c

To Discount receive a/c

2600

3300

1600

2340

260

2970

330

1440

160

27 Jan

2018

Salaries a/c Dr.

To bank a/c

14500

14500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

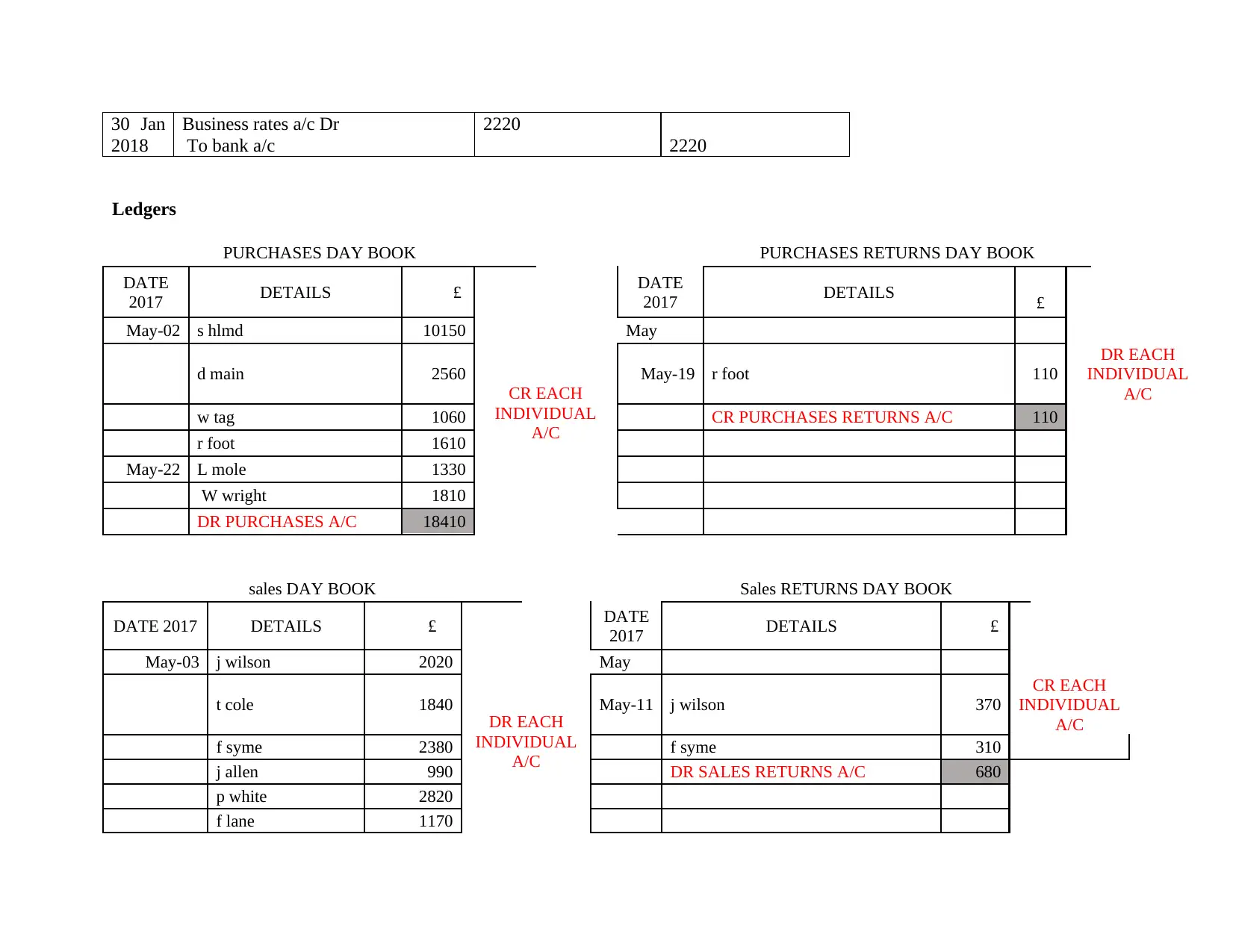

30 Jan

2018

Business rates a/c Dr

To bank a/c

2220

2220

Ledgers

PURCHASES DAY BOOK PURCHASES RETURNS DAY BOOK

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-02 s hlmd 10150

CR EACH

INDIVIDUAL

A/C

May

d main 2560 May-19 r foot 110

DR EACH

INDIVIDUAL

A/C

w tag 1060 CR PURCHASES RETURNS A/C 110

r foot 1610

May-22 L mole 1330

W wright 1810

DR PURCHASES A/C 18410

sales DAY BOOK Sales RETURNS DAY BOOK

DATE 2017 DETAILS £ DATE

2017 DETAILS £

May-03 j wilson 2020

DR EACH

INDIVIDUAL

A/C

May

t cole 1840 May-11 j wilson 370

CR EACH

INDIVIDUAL

A/C

f syme 2380 f syme 310

j allen 990 DR SALES RETURNS A/C 680

p white 2820

f lane 1170

2018

Business rates a/c Dr

To bank a/c

2220

2220

Ledgers

PURCHASES DAY BOOK PURCHASES RETURNS DAY BOOK

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-02 s hlmd 10150

CR EACH

INDIVIDUAL

A/C

May

d main 2560 May-19 r foot 110

DR EACH

INDIVIDUAL

A/C

w tag 1060 CR PURCHASES RETURNS A/C 110

r foot 1610

May-22 L mole 1330

W wright 1810

DR PURCHASES A/C 18410

sales DAY BOOK Sales RETURNS DAY BOOK

DATE 2017 DETAILS £ DATE

2017 DETAILS £

May-03 j wilson 2020

DR EACH

INDIVIDUAL

A/C

May

t cole 1840 May-11 j wilson 370

CR EACH

INDIVIDUAL

A/C

f syme 2380 f syme 310

j allen 990 DR SALES RETURNS A/C 680

p white 2820

f lane 1170

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

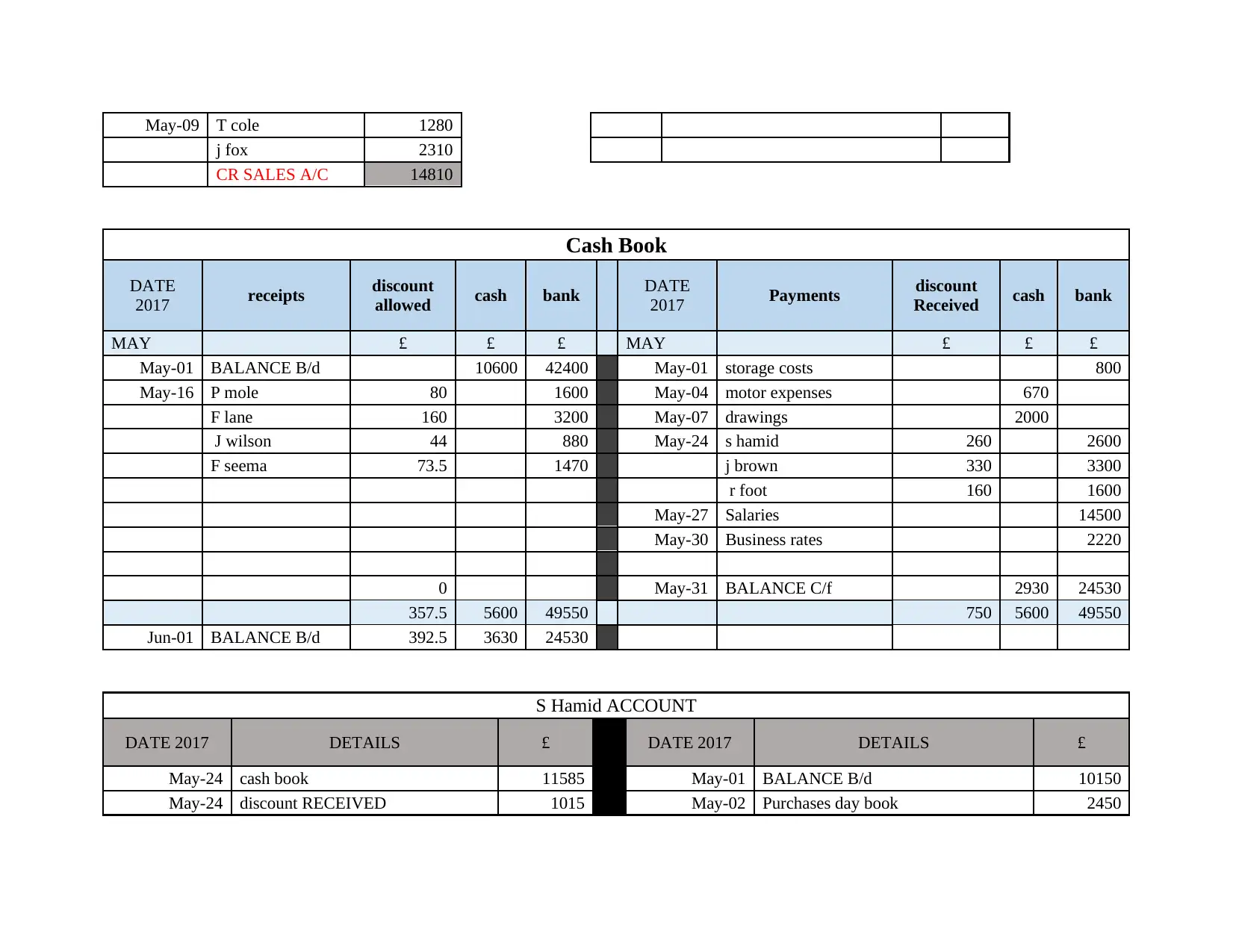

May-09 T cole 1280

j fox 2310

CR SALES A/C 14810

Cash Book

DATE

2017 receipts discount

allowed cash bank DATE

2017 Payments discount

Received cash bank

MAY £ £ £ MAY £ £ £

May-01 BALANCE B/d 10600 42400 May-01 storage costs 800

May-16 P mole 80 1600 May-04 motor expenses 670

F lane 160 3200 May-07 drawings 2000

J wilson 44 880 May-24 s hamid 260 2600

F seema 73.5 1470 j brown 330 3300

r foot 160 1600

May-27 Salaries 14500

May-30 Business rates 2220

0 May-31 BALANCE C/f 2930 24530

357.5 5600 49550 750 5600 49550

Jun-01 BALANCE B/d 392.5 3630 24530

S Hamid ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-24 cash book 11585 May-01 BALANCE B/d 10150

May-24 discount RECEIVED 1015 May-02 Purchases day book 2450

j fox 2310

CR SALES A/C 14810

Cash Book

DATE

2017 receipts discount

allowed cash bank DATE

2017 Payments discount

Received cash bank

MAY £ £ £ MAY £ £ £

May-01 BALANCE B/d 10600 42400 May-01 storage costs 800

May-16 P mole 80 1600 May-04 motor expenses 670

F lane 160 3200 May-07 drawings 2000

J wilson 44 880 May-24 s hamid 260 2600

F seema 73.5 1470 j brown 330 3300

r foot 160 1600

May-27 Salaries 14500

May-30 Business rates 2220

0 May-31 BALANCE C/f 2930 24530

357.5 5600 49550 750 5600 49550

Jun-01 BALANCE B/d 392.5 3630 24530

S Hamid ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-24 cash book 11585 May-01 BALANCE B/d 10150

May-24 discount RECEIVED 1015 May-02 Purchases day book 2450

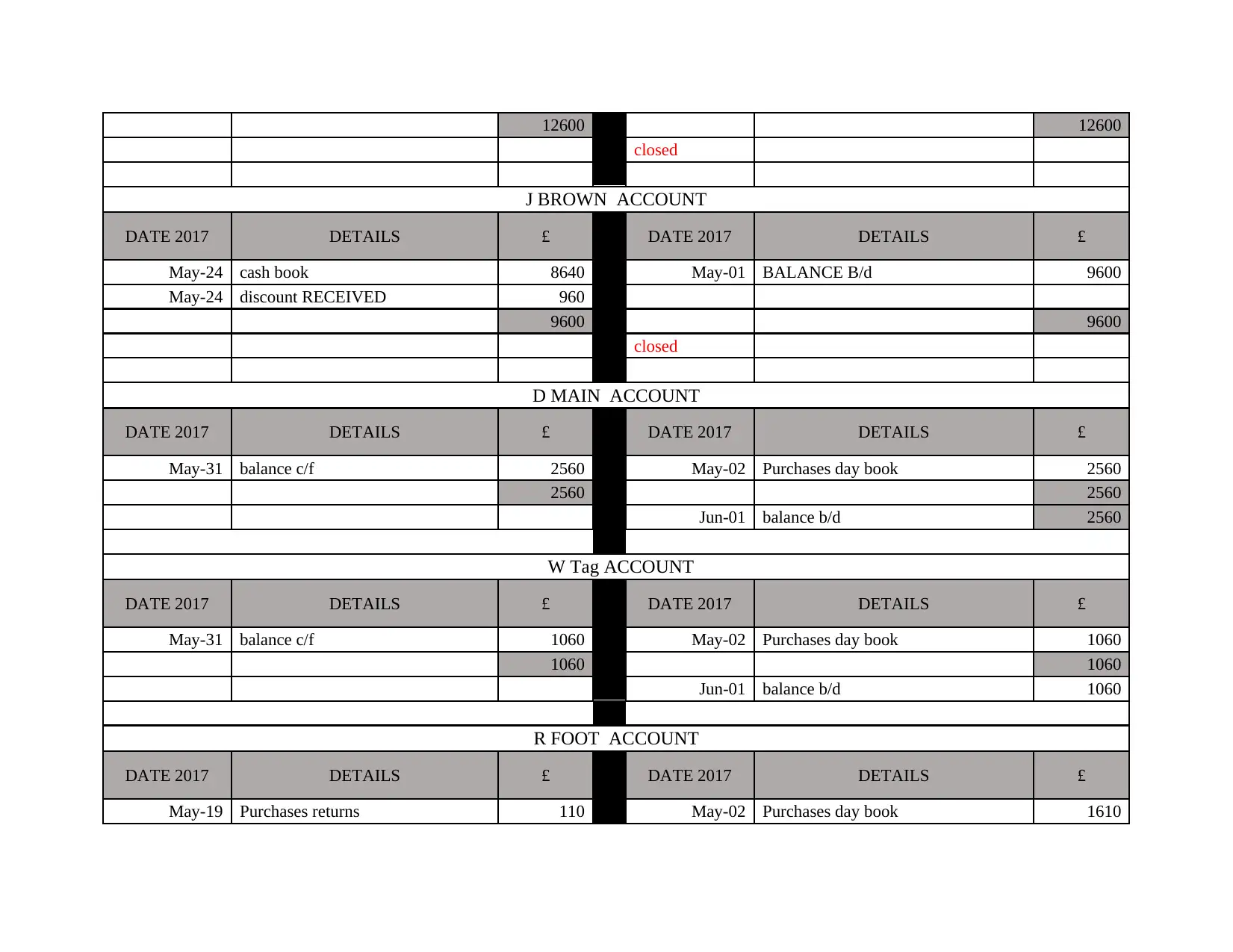

12600 12600

closed

J BROWN ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-24 cash book 8640 May-01 BALANCE B/d 9600

May-24 discount RECEIVED 960

9600 9600

closed

D MAIN ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-31 balance c/f 2560 May-02 Purchases day book 2560

2560 2560

Jun-01 balance b/d 2560

W Tag ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-31 balance c/f 1060 May-02 Purchases day book 1060

1060 1060

Jun-01 balance b/d 1060

R FOOT ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-19 Purchases returns 110 May-02 Purchases day book 1610

closed

J BROWN ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-24 cash book 8640 May-01 BALANCE B/d 9600

May-24 discount RECEIVED 960

9600 9600

closed

D MAIN ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-31 balance c/f 2560 May-02 Purchases day book 2560

2560 2560

Jun-01 balance b/d 2560

W Tag ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-31 balance c/f 1060 May-02 Purchases day book 1060

1060 1060

Jun-01 balance b/d 1060

R FOOT ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-19 Purchases returns 110 May-02 Purchases day book 1610

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 35

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.