Financial Accounting Report: Analysis and Practical Applications

VerifiedAdded on 2020/11/12

|24

|4569

|479

Report

AI Summary

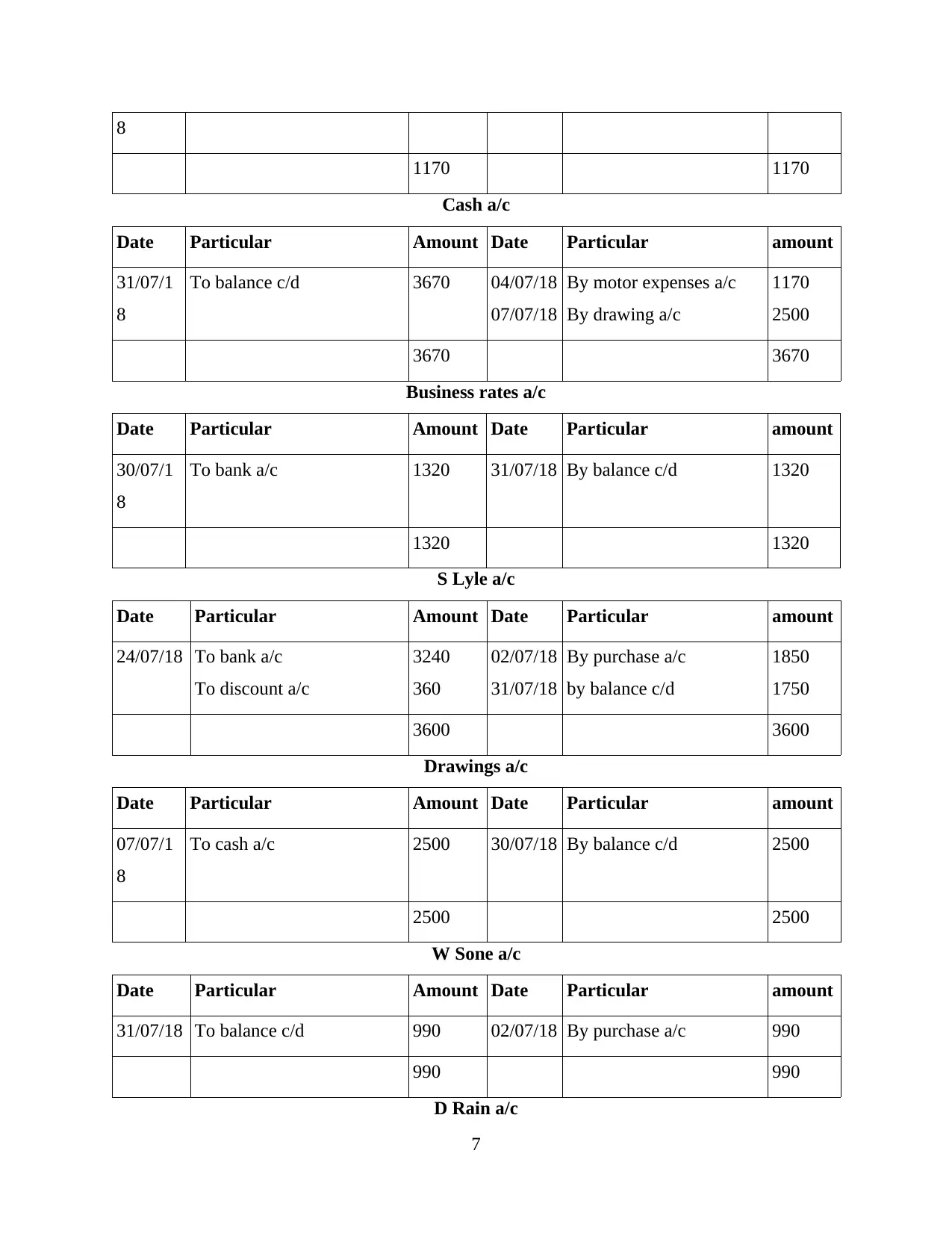

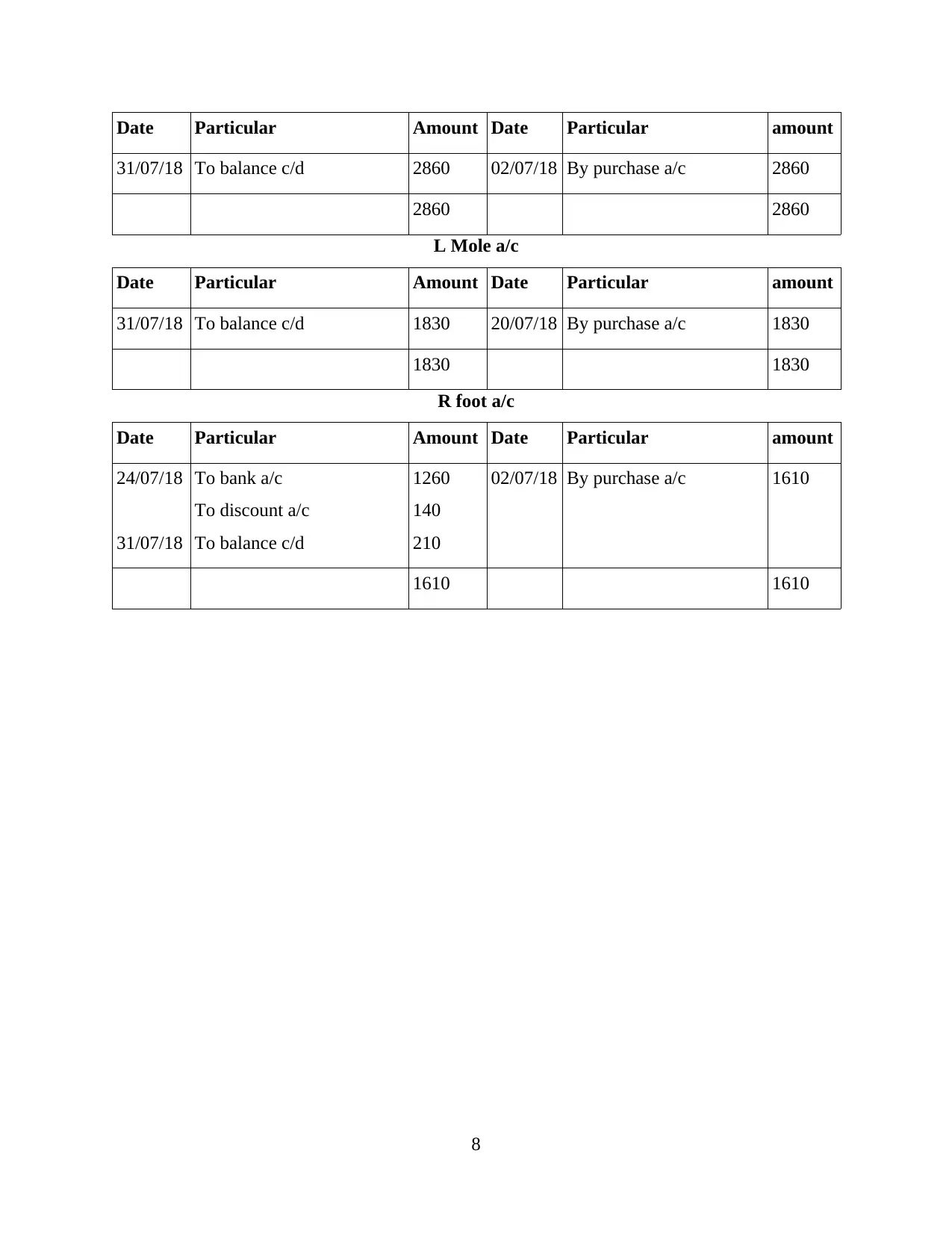

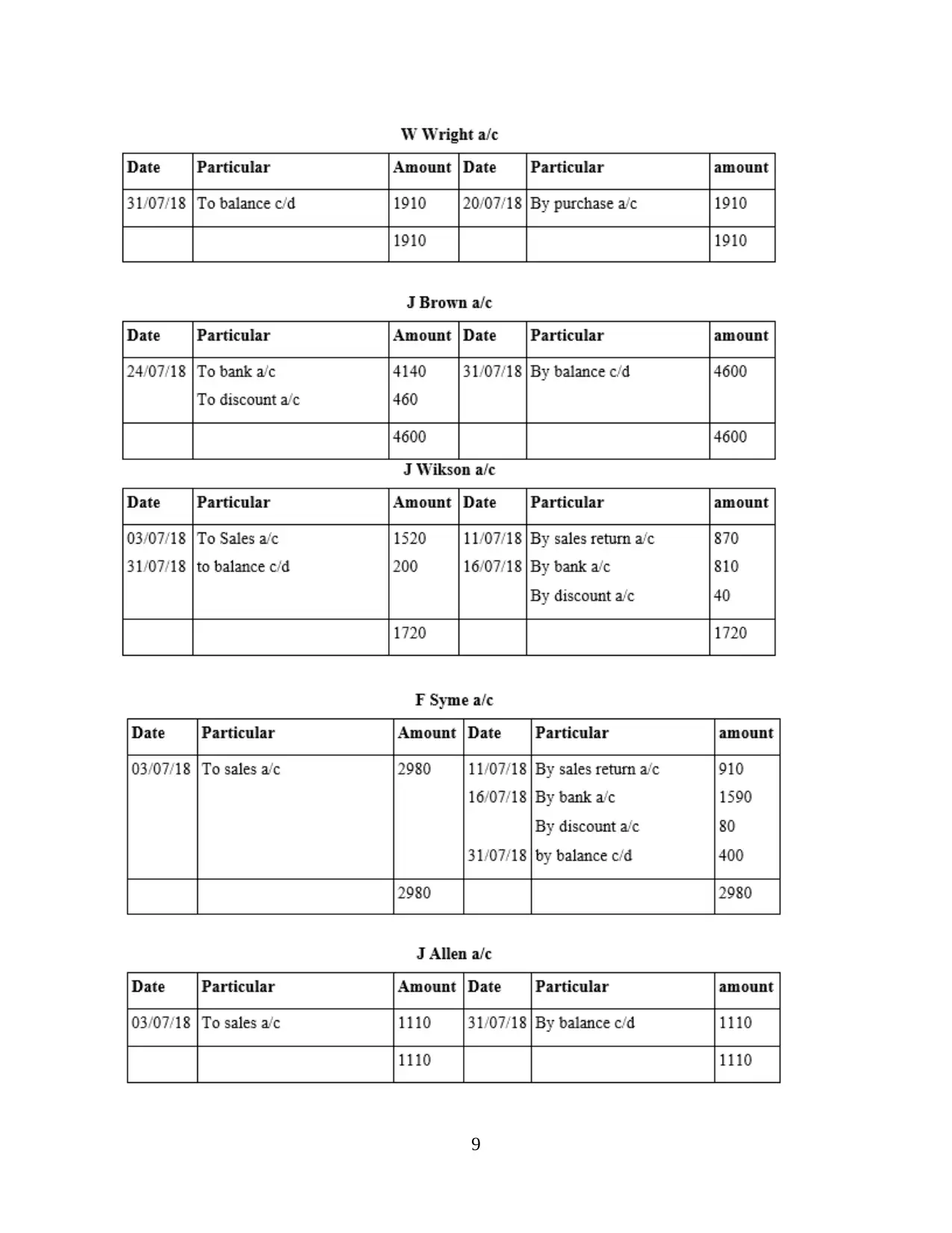

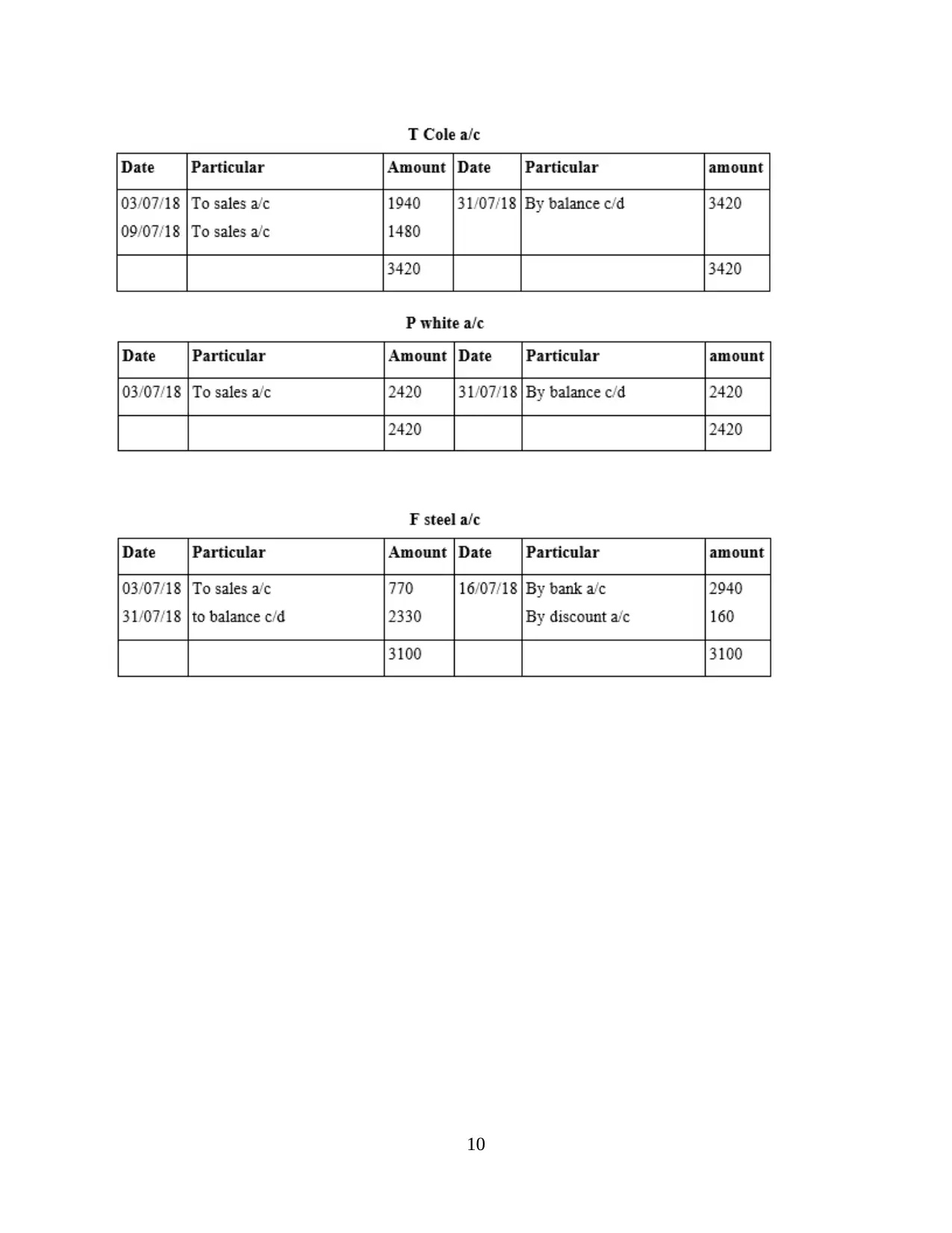

This report delves into the realm of financial accounting, elucidating its significance in business operations and management. It initiates with an introduction to financial accounting, its purpose, and its benefits for both governmental and private organizations in maintaining financial discipline. The report then navigates through the regulations governing financial accounting, emphasizing the role of IASB and IFRS. A detailed exploration of accounting rules and principles follows, encompassing debit/credit principles, economic entity assumptions, and principles like cost, full disclosure, going concern, matching, revenue recognition, accrual, consistency, time period, reliability, and monetary unit. Furthermore, the report examines conventions and concepts related to consistency and material disclosure. The practical application of accounting principles is demonstrated through journal entries and ledger postings for a specific client, illustrating real-world financial accounting practices. The report includes a comprehensive financial accounting analysis of client accounts, providing practical examples of journal entries, ledger postings, and financial statement preparation, which can be used for decision-making.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.