Financial Accounting Principles and Practical Application Report

VerifiedAdded on 2023/01/06

|22

|4660

|22

Report

AI Summary

This report delves into the core principles of financial accounting, emphasizing its role in monitoring a business's financial activities. It begins by defining financial accounting and its purpose, highlighting the significance of financial reporting, including income statements and balance sheets. The report then explores both internal and external stakeholders of a large organization, explaining their interests in financial information. The practical section focuses on understanding the dual-entry accounting system and the preparation of final accounts, supported by examples from multiple clients. Key topics such as bank reconciliation statements and suspense accounts are also explained. The report provides detailed financial statements for several clients, including profit and loss statements, statements of changes in equity, and statements of financial position, along with supporting schedules and notes. The assignment concludes with a comprehensive overview of financial accounting's importance and its practical applications in business decision-making.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION............2

MAIN BODY..................................................................................................................................2

TASK 1............................................................................................................................................2

1. Define financial accounting and its purpose............................................................................2

2. Explain two internal stakeholders and four external stakeholder of a large organization.......5

TASK 2............................................................................................................................................6

CLIENT 1........................................................................................................................................6

CLIENT 2......................................................................................................................................11

CLIENT 3......................................................................................................................................15

CLIENT 4......................................................................................................................................17

CLIENT 5......................................................................................................................................18

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

1

MAIN BODY..................................................................................................................................2

TASK 1............................................................................................................................................2

1. Define financial accounting and its purpose............................................................................2

2. Explain two internal stakeholders and four external stakeholder of a large organization.......5

TASK 2............................................................................................................................................6

CLIENT 1........................................................................................................................................6

CLIENT 2......................................................................................................................................11

CLIENT 3......................................................................................................................................15

CLIENT 4......................................................................................................................................17

CLIENT 5......................................................................................................................................18

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

1

INTRODUCTION

Financial accounting is a specialist accounting division whose focus is on monitoring

financial activities of the business (Baker and Burlaud, 2015). It is a standard schedule for any

company. It is a very critical field of management as merely doing trade is not enough for a

company to see whether, or not, actions are focused in the correct direction. This control over the

activities of the company and its workers is carried out by the use of financial reporting. This

involves the preparation of financial reports, such as the income statement for the assessment of

income earned by the firm in the fiscal year and also the balance sheet, which is a detailed

statement of the financial status of the company. The analysis is divided into two sections. The

first section outlines the principle of financial accounting and its purpose. It also focuses on the

stakeholders of a large organisation. The second section is focuses on practical aspect of gaining

an understanding of the dual-entry accounting system and preparation of the final accounts.

Further explanation of the bank reconciliation statement and the suspense account is given in this

report.

MAIN BODY

TASK 1

1. Define financial accounting and its purpose

It is characterised as the process of documenting, classifying, summarising, analysis and

interpreting the monetary data of a company. This method is focused on the several accounting

standards defined by the regulatory authorities. The use of financial accounting is popular among

each and every company in the world. The information used during financial accounting are

classified as revenue, expenditure, assets, liabilities and capital (or equity) under five separate

headings. There is various financial treatments for each object in compliance with defined

accounting standards and policies adopted in the organisation. The basic aim of financial

accounting is to assess the gains or losses of the stated period and to assess the financial

condition of the corporation. The following features of financial accounting could be extracted

from the description below:

Recording: It is the basic feature of financial accounting and where financial transection

of the business recorded (Drew and Dollery, 2015). It can be calculated in monetary

2

Financial accounting is a specialist accounting division whose focus is on monitoring

financial activities of the business (Baker and Burlaud, 2015). It is a standard schedule for any

company. It is a very critical field of management as merely doing trade is not enough for a

company to see whether, or not, actions are focused in the correct direction. This control over the

activities of the company and its workers is carried out by the use of financial reporting. This

involves the preparation of financial reports, such as the income statement for the assessment of

income earned by the firm in the fiscal year and also the balance sheet, which is a detailed

statement of the financial status of the company. The analysis is divided into two sections. The

first section outlines the principle of financial accounting and its purpose. It also focuses on the

stakeholders of a large organisation. The second section is focuses on practical aspect of gaining

an understanding of the dual-entry accounting system and preparation of the final accounts.

Further explanation of the bank reconciliation statement and the suspense account is given in this

report.

MAIN BODY

TASK 1

1. Define financial accounting and its purpose

It is characterised as the process of documenting, classifying, summarising, analysis and

interpreting the monetary data of a company. This method is focused on the several accounting

standards defined by the regulatory authorities. The use of financial accounting is popular among

each and every company in the world. The information used during financial accounting are

classified as revenue, expenditure, assets, liabilities and capital (or equity) under five separate

headings. There is various financial treatments for each object in compliance with defined

accounting standards and policies adopted in the organisation. The basic aim of financial

accounting is to assess the gains or losses of the stated period and to assess the financial

condition of the corporation. The following features of financial accounting could be extracted

from the description below:

Recording: It is the basic feature of financial accounting and where financial transection

of the business recorded (Drew and Dollery, 2015). It can be calculated in monetary

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

terms, shortly after they have been recorded in the books of accounts. Transactions shall

be reported in the financial report.

Classification: It further classifies the data into related nature of the business transactions

under the same heading. Basically, with the help of ledger accounts, accountants separate

the amount of the basis of their nature such as profit, expenses etc.

Summarizing: it presents a detailed analysis of sensitive data in a way that is beneficial

to users. This stage of financial accounting includes the financial reporting, such as profit

and loss reports, balance sheets, cash flow statements, etc.

Interpreting: since all the functions listed above have been completed, analysing comes

into play, which implies the transmission of results to management after analysing them.

It is an art and a science as well: Accounting is an art for financial experts because they

have to make some decisions which are based on the personal opinion of the accountant

after analysing financial results. In general, books of accounts are produced in a similar

manner on the basis of accounting standards that are practiced by any accountant.

Purpose of financial accounting:

Financial accounting plays essential role in the organization and it also has several

purposes which are defined below:

Keeping systematic records: financial accounting is carried out with the basic intention

of preserving systematic records. If accounting is not carried out, it will impose an enormous

burden on the administration head. In this situations, organization lead to a breakdown of

business processes. That is why; maintaining financial record is very essential and organization

need to focus on it at initial stage because any error or omission can lead to change the final

results. Any mistake can increase the complexity among books of accounts, so accountant need

to be more focused while recording business transections.

Protecting business resources: Financial accounting provides protections for business

resources from unreasonable usage. This is important because management keep a tab on data

such as the amount of capital invested in companies, the level of debt and credit to the company ,

different information such as the amount of fixed assets, cash, W-I-P, the number of finished

goods, the stock of raw materials, the activities that produce higher income, etc. All this

information allows managers to ensure that the resources are not held idle or under utilities.

3

be reported in the financial report.

Classification: It further classifies the data into related nature of the business transactions

under the same heading. Basically, with the help of ledger accounts, accountants separate

the amount of the basis of their nature such as profit, expenses etc.

Summarizing: it presents a detailed analysis of sensitive data in a way that is beneficial

to users. This stage of financial accounting includes the financial reporting, such as profit

and loss reports, balance sheets, cash flow statements, etc.

Interpreting: since all the functions listed above have been completed, analysing comes

into play, which implies the transmission of results to management after analysing them.

It is an art and a science as well: Accounting is an art for financial experts because they

have to make some decisions which are based on the personal opinion of the accountant

after analysing financial results. In general, books of accounts are produced in a similar

manner on the basis of accounting standards that are practiced by any accountant.

Purpose of financial accounting:

Financial accounting plays essential role in the organization and it also has several

purposes which are defined below:

Keeping systematic records: financial accounting is carried out with the basic intention

of preserving systematic records. If accounting is not carried out, it will impose an enormous

burden on the administration head. In this situations, organization lead to a breakdown of

business processes. That is why; maintaining financial record is very essential and organization

need to focus on it at initial stage because any error or omission can lead to change the final

results. Any mistake can increase the complexity among books of accounts, so accountant need

to be more focused while recording business transections.

Protecting business resources: Financial accounting provides protections for business

resources from unreasonable usage. This is important because management keep a tab on data

such as the amount of capital invested in companies, the level of debt and credit to the company ,

different information such as the amount of fixed assets, cash, W-I-P, the number of finished

goods, the stock of raw materials, the activities that produce higher income, etc. All this

information allows managers to ensure that the resources are not held idle or under utilities.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Determining the amount of profit or loss: It is one of the main purposes of financial

accounting is to assess the income and losses of the company. This role is carried out by having a

consistent record of revenue and expenses for a particular duration. If revenue exceeds

from expenditure then it means organization gaining and in the opposite case, company facing

loss. This work is done by preparing an income statements and this account allows management,

investors and all stakeholders to understand the profitability of a company. In the event of losses

for consecutive years, managers can take the appropriate steps to investigate the reasons for such

losses.

Financial condition: Another purpose of financial accounting is to identify the financial

position of organization in terms of total assets and total liabilities. It will be possible through

making balance sheet which serves this purpose. It is a comprehensive statement of the assets

and liabilities of the company for the fixed period of time. It serves as a leading indicator for the

financial health of the organisation. Various research tests are carried out on the basis of this

statement (Flower and Ebbers, 2018). It further contributes to the production of knowledge that

is useful for formulating the strategy. This is a vital activity to undertake, as the simple

measurement of income is not enough, as it can create an unclear image, which can only become

apparent when preparing the Balance sheet.

Promote sound decision making process: With the help of financial accounting, it will

helps accountants and other stakeholders to make effective decision as the results produced by

the final reports are being used as information for comparing company's output with other

businesses in the market. This analogy makes it easier for management to decide about the

potential course of action. If the assessment is not carried out correctly, the findings obtained

would be ambiguous and thus judgments will not be made in the proper way. These decisions

apply to issues such as depreciation strategy, disposition of obsolete assets, etc.

Information system: One of the main purposes of financial accounting is to make

people aware about their operational performances. It helps in processing and communication

of organizational information. This collected information allows the administration to make the

effective and relevant decisions. By disclosing financial information, organization and other

potential interested parties can show their interest regarding investment in business.

4

accounting is to assess the income and losses of the company. This role is carried out by having a

consistent record of revenue and expenses for a particular duration. If revenue exceeds

from expenditure then it means organization gaining and in the opposite case, company facing

loss. This work is done by preparing an income statements and this account allows management,

investors and all stakeholders to understand the profitability of a company. In the event of losses

for consecutive years, managers can take the appropriate steps to investigate the reasons for such

losses.

Financial condition: Another purpose of financial accounting is to identify the financial

position of organization in terms of total assets and total liabilities. It will be possible through

making balance sheet which serves this purpose. It is a comprehensive statement of the assets

and liabilities of the company for the fixed period of time. It serves as a leading indicator for the

financial health of the organisation. Various research tests are carried out on the basis of this

statement (Flower and Ebbers, 2018). It further contributes to the production of knowledge that

is useful for formulating the strategy. This is a vital activity to undertake, as the simple

measurement of income is not enough, as it can create an unclear image, which can only become

apparent when preparing the Balance sheet.

Promote sound decision making process: With the help of financial accounting, it will

helps accountants and other stakeholders to make effective decision as the results produced by

the final reports are being used as information for comparing company's output with other

businesses in the market. This analogy makes it easier for management to decide about the

potential course of action. If the assessment is not carried out correctly, the findings obtained

would be ambiguous and thus judgments will not be made in the proper way. These decisions

apply to issues such as depreciation strategy, disposition of obsolete assets, etc.

Information system: One of the main purposes of financial accounting is to make

people aware about their operational performances. It helps in processing and communication

of organizational information. This collected information allows the administration to make the

effective and relevant decisions. By disclosing financial information, organization and other

potential interested parties can show their interest regarding investment in business.

4

2. Explain two internal stakeholders and four external stakeholder of a large organization

The primary objective of financial accounting is to provide business information to the

interested parties (users). Users of this financial accounting can be divided into two groups, i.e.

internal and external users (Keil, 2016). These consumers are also referred to as stakeholders

who are interested in the financial statements of the organisations which shows profit and loss

position and financial health of the firm.

Internal stakeholders: these are the individuals or groups who've been

working within company. This data is used for separate purposes, some of which are described

below:

Owners: It is one main user of financial information, since they only provide funding for

the organisation's activities, so they'll have to know whether or not their funding is being

used correctly. They are keen to learn about the operational and liquidity position of the

company. As has already been addressed, the key goal of financial accounting is to create

final accounts of the company that produce the relevant results.

Management: The key role of management should be to get work done by someone else

such as employees and to determine that the juniors are working effectively or not.

Financial accounting shall provide assistance in this subject by supplying them with

reporting of the results of employees. Management functions include planning and

monitoring. Planning is carried out with the aid of the planning of different budgets.

Controlling is carried out with the aid of estimating the variances between the real figures

and the budgeted figures (Kwan and et.al., 2016).

External stakeholders: these people are from outside of the organisation but are indirectly

involved with organisation and they are interest in financial information in detail. There are some

external stakeholders which are as follows:

Investors: these people who invested in the company and who are interested in

examining the financial status of the organisation to know if their investment is in safe

hands or not. They are curious to know if the profits are in line with what they planned or

not. Anticipated financial decisions depend on the accounting results of financial reports

such as EPS, net profit, etc.

Government: Both federal and state governments are concerned about accounting

information because of their own purposes. Tax documents are some of the reasons for

5

The primary objective of financial accounting is to provide business information to the

interested parties (users). Users of this financial accounting can be divided into two groups, i.e.

internal and external users (Keil, 2016). These consumers are also referred to as stakeholders

who are interested in the financial statements of the organisations which shows profit and loss

position and financial health of the firm.

Internal stakeholders: these are the individuals or groups who've been

working within company. This data is used for separate purposes, some of which are described

below:

Owners: It is one main user of financial information, since they only provide funding for

the organisation's activities, so they'll have to know whether or not their funding is being

used correctly. They are keen to learn about the operational and liquidity position of the

company. As has already been addressed, the key goal of financial accounting is to create

final accounts of the company that produce the relevant results.

Management: The key role of management should be to get work done by someone else

such as employees and to determine that the juniors are working effectively or not.

Financial accounting shall provide assistance in this subject by supplying them with

reporting of the results of employees. Management functions include planning and

monitoring. Planning is carried out with the aid of the planning of different budgets.

Controlling is carried out with the aid of estimating the variances between the real figures

and the budgeted figures (Kwan and et.al., 2016).

External stakeholders: these people are from outside of the organisation but are indirectly

involved with organisation and they are interest in financial information in detail. There are some

external stakeholders which are as follows:

Investors: these people who invested in the company and who are interested in

examining the financial status of the organisation to know if their investment is in safe

hands or not. They are curious to know if the profits are in line with what they planned or

not. Anticipated financial decisions depend on the accounting results of financial reports

such as EPS, net profit, etc.

Government: Both federal and state governments are concerned about accounting

information because of their own purposes. Tax documents are some of the reasons for

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

interest. They will need financial information on the basis of the collection of business-

related statistics used to compile national accounts.

Creditors: Company owes some funds to certain parties such as suppliers who provide

raw material, money lending etc. They are concerned in accounting details on the

grounds that they'd like to maintain the financial health of the company (Mook and et.al.,

2015). If previous estimates and audits are not carried out by creditors, they which

contribute to their bad debts, as the business does not occupy the role in which it will be

sufficient to reimburse debts.

Society: Community as a whole needs to check the company's financial details, so it

needed to understand whether or not the company fulfils its obligation towards society

for example CSR. It will be an effective tool for maintaining a good place between

society and target audience.

6

related statistics used to compile national accounts.

Creditors: Company owes some funds to certain parties such as suppliers who provide

raw material, money lending etc. They are concerned in accounting details on the

grounds that they'd like to maintain the financial health of the company (Mook and et.al.,

2015). If previous estimates and audits are not carried out by creditors, they which

contribute to their bad debts, as the business does not occupy the role in which it will be

sufficient to reimburse debts.

Society: Community as a whole needs to check the company's financial details, so it

needed to understand whether or not the company fulfils its obligation towards society

for example CSR. It will be an effective tool for maintaining a good place between

society and target audience.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

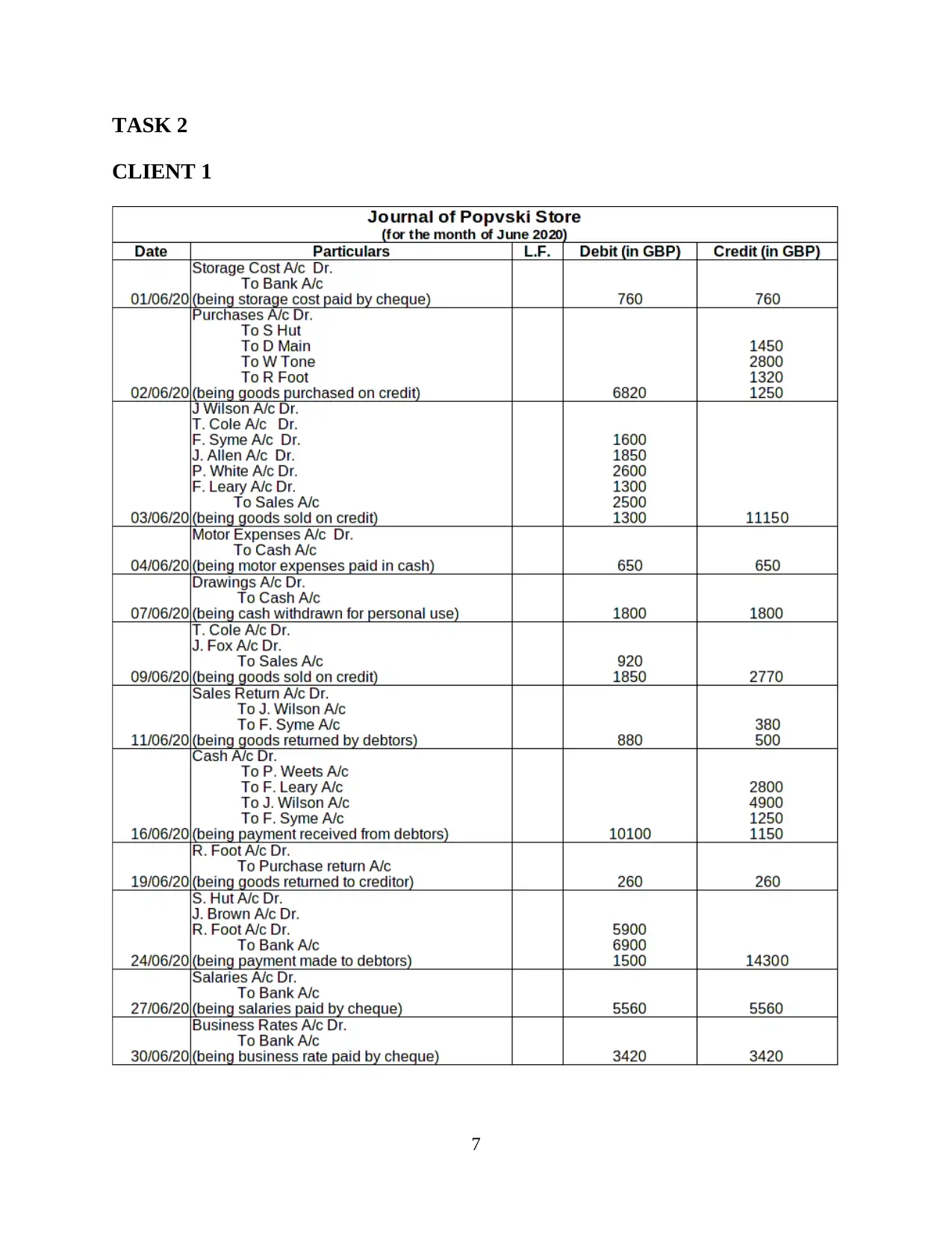

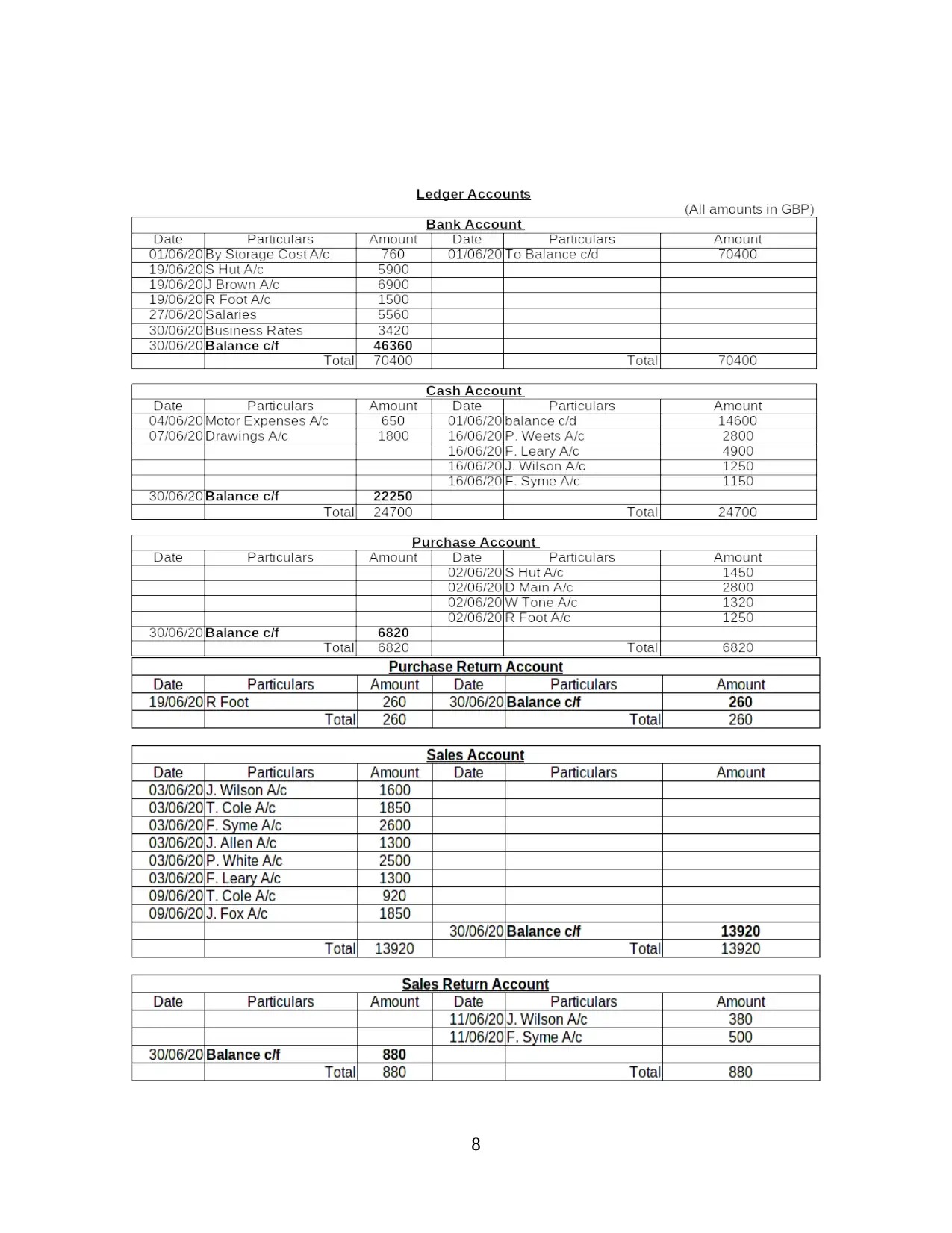

TASK 2

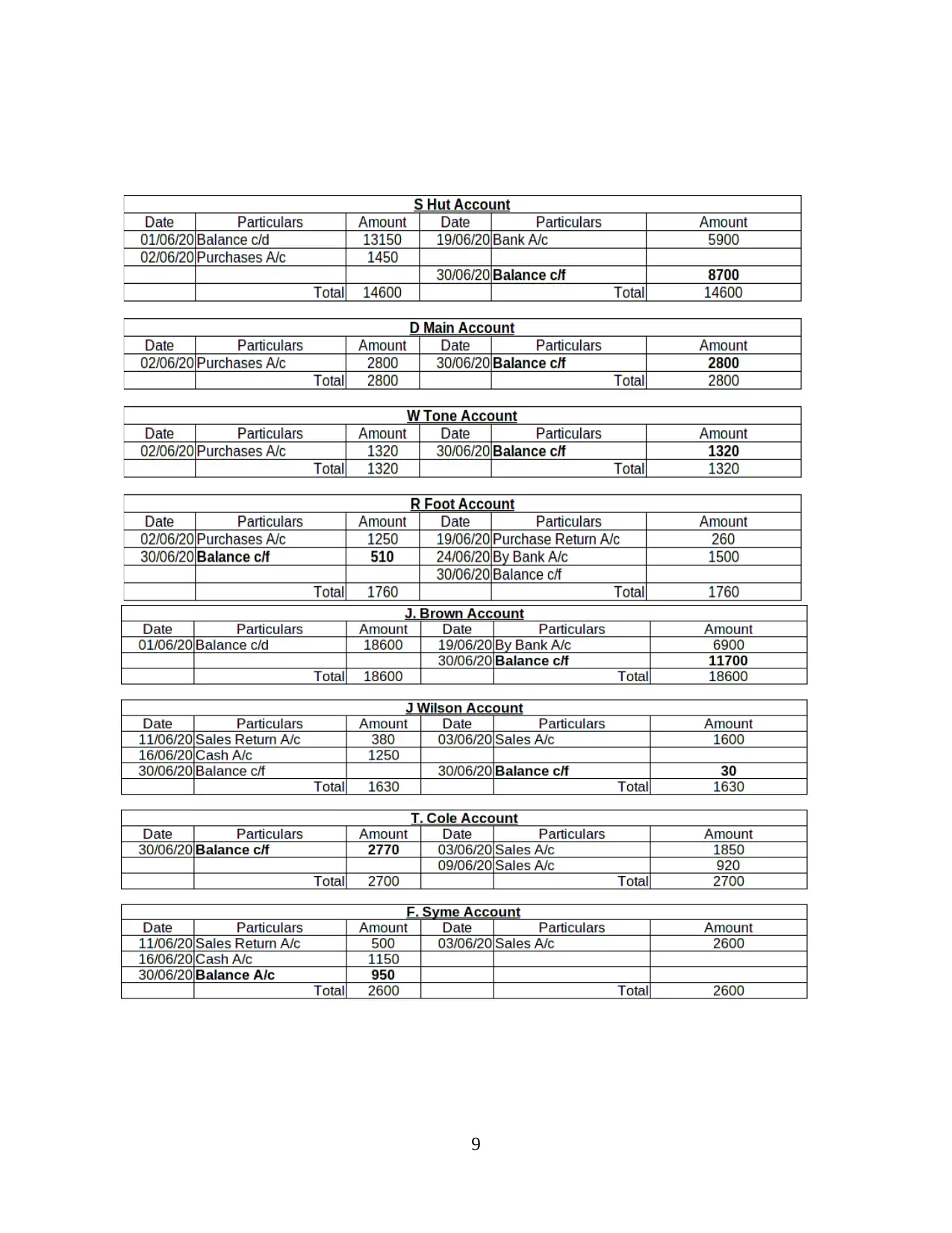

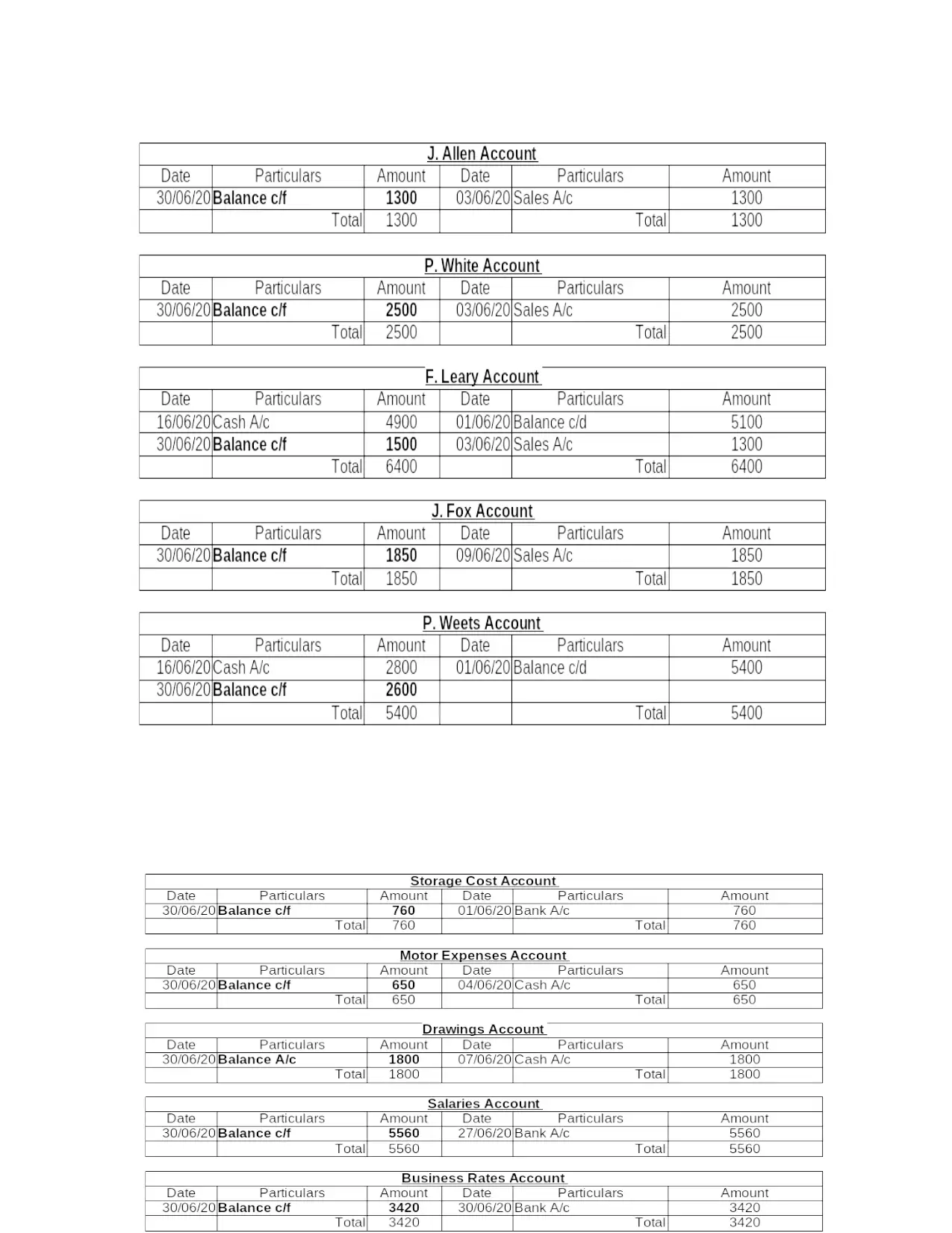

CLIENT 1

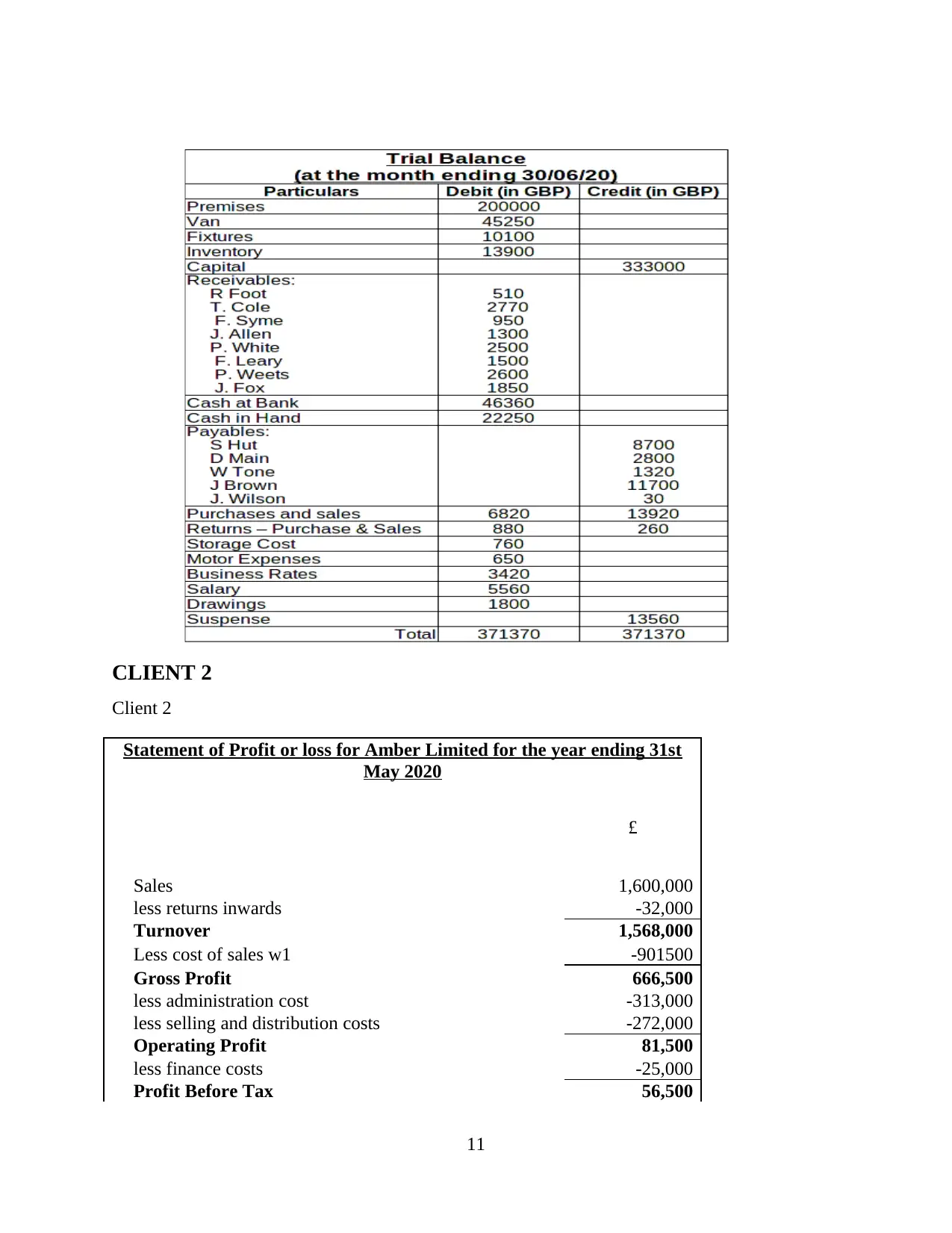

7

CLIENT 1

7

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CLIENT 2

Client 2

Statement of Profit or loss for Amber Limited for the year ending 31st

May 2020

£

Sales 1,600,000

less returns inwards -32,000

Turnover 1,568,000

Less cost of sales w1 -901500

Gross Profit 666,500

less administration cost -313,000

less selling and distribution costs -272,000

Operating Profit 81,500

less finance costs -25,000

Profit Before Tax 56,500

11

Client 2

Statement of Profit or loss for Amber Limited for the year ending 31st

May 2020

£

Sales 1,600,000

less returns inwards -32,000

Turnover 1,568,000

Less cost of sales w1 -901500

Gross Profit 666,500

less administration cost -313,000

less selling and distribution costs -272,000

Operating Profit 81,500

less finance costs -25,000

Profit Before Tax 56,500

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.