Financial Accounting Principles Report: Cartex Accounting, London

VerifiedAdded on 2020/12/09

|28

|5605

|500

Report

AI Summary

This report, prepared by a Jr. Accountant at Cartex Accounting, provides a comprehensive overview of financial accounting principles. It begins with an introduction to financial accounting, its purposes, and the importance of adhering to established rules and guidelines. The report then delves into the roles of internal and external stakeholders in a large business organization, highlighting their interests in financial information. Practical applications are demonstrated through the preparation of financial statements for various clients, including sole traders and limited companies, along with explanations of accounting concepts, depreciation methods, and bank reconciliation statements. Furthermore, the report covers the preparation of sales and purchase ledger control accounts and the use of suspense accounts in financial statement preparation, concluding with journal entries. The report underscores the significance of financial accounting in maintaining accuracy, measuring performance, and meeting legal and stakeholder requirements.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A Report To The Line Manager ......................................................................................................1

1. Financial accounting and its purposes.....................................................................................1

2. Explaining Internal and External stakeholders of a large business organisation....................3

Client 1.............................................................................................................................................5

Preparation of financial statements of the Alexandra.................................................................5

Client 2...........................................................................................................................................13

A) Preparation of profit and loss statement ..............................................................................13

B) Preparation of statement of financial position.....................................................................14

C) Explaining the accounting concepts.....................................................................................15

D) Describing purpose of depreciation in formulation of accounting statements and methods

of depreciation...........................................................................................................................16

E) Critical evaluation of difference between financial statements prepared by the sole traders

and limited companies..............................................................................................................17

Client 3...........................................................................................................................................18

A) Purpose of preparing the bank reconciliation statements....................................................18

B) explaining the areas that may cause the variation in the companies records with the bank

records.......................................................................................................................................19

C) Explaining the term “imprest” in the context of petty cash system.....................................19

D) Preparation of bank reconciliation statements for Burcu Ltd..............................................19

Client 4...........................................................................................................................................20

A) Preparation of sales ledger control account and purchase ledger control account .............20

B) Need of preparing control accounts.....................................................................................21

Client 5...........................................................................................................................................21

A) Explaining the term suspense accounts and its features......................................................21

B) Preparing trial balance with the help of control ledger accounts.........................................22

C) Showing journal entries of the company..............................................................................23

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

INTRODUCTION...........................................................................................................................1

A Report To The Line Manager ......................................................................................................1

1. Financial accounting and its purposes.....................................................................................1

2. Explaining Internal and External stakeholders of a large business organisation....................3

Client 1.............................................................................................................................................5

Preparation of financial statements of the Alexandra.................................................................5

Client 2...........................................................................................................................................13

A) Preparation of profit and loss statement ..............................................................................13

B) Preparation of statement of financial position.....................................................................14

C) Explaining the accounting concepts.....................................................................................15

D) Describing purpose of depreciation in formulation of accounting statements and methods

of depreciation...........................................................................................................................16

E) Critical evaluation of difference between financial statements prepared by the sole traders

and limited companies..............................................................................................................17

Client 3...........................................................................................................................................18

A) Purpose of preparing the bank reconciliation statements....................................................18

B) explaining the areas that may cause the variation in the companies records with the bank

records.......................................................................................................................................19

C) Explaining the term “imprest” in the context of petty cash system.....................................19

D) Preparation of bank reconciliation statements for Burcu Ltd..............................................19

Client 4...........................................................................................................................................20

A) Preparation of sales ledger control account and purchase ledger control account .............20

B) Need of preparing control accounts.....................................................................................21

Client 5...........................................................................................................................................21

A) Explaining the term suspense accounts and its features......................................................21

B) Preparing trial balance with the help of control ledger accounts.........................................22

C) Showing journal entries of the company..............................................................................23

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

INTRODUCTION

Financial accounting principles refers to those rules that are need to be followed by each

of the business organisation while preparing their books of accounts and recording their financial

data in the books. They can also be defined as the guidelines to taken into account while

preparing financial reports of the company. Cartex Accounting firm is a business organisation of

London that provides professional accounting services to its clients. The firm also provides tax

advisory services to its customers. The present study shows a report of Jr Accountant of Cartex

Accounting to its line manager. The reports provide details about various rules, principles of

accountancy, purpose of financial accounting and its various users. Including internal and

external stakeholders. Further, the study also shows various calculations relating to preparation

of financial statements of sole traders, company and partnership firm, and calculations as to

prepare the bank reconciliation statement along with its purposes. In addition, it also shows

preparation of sales ledger and purchase ledger control accounts preparation of financial

statements with the help of suspense account.

A Report To The Line Manager

Cartex Accounting

To,

The line manager.

From,

Jr. Accountant

Subject: A report providing information about financial accounting, its purposes and usage.

1. Financial accounting and its purposes

Financial accounting

“Financial accounting can be defines as a branch of accounting that helps the business in

providing professional and specialised services to the organisation in order to maintain a

standard in the books of accounts of the company” (Financial Accounting .2019) .

Preparation of financial accounting is based on some basic principles, rules and

guidelines, that helps the professionals in recording the financial data in the books and

preparation of various financial reports of the company.

In other words, it can be evaluated that “financial accounting is a process that includes,

Financial accounting principles refers to those rules that are need to be followed by each

of the business organisation while preparing their books of accounts and recording their financial

data in the books. They can also be defined as the guidelines to taken into account while

preparing financial reports of the company. Cartex Accounting firm is a business organisation of

London that provides professional accounting services to its clients. The firm also provides tax

advisory services to its customers. The present study shows a report of Jr Accountant of Cartex

Accounting to its line manager. The reports provide details about various rules, principles of

accountancy, purpose of financial accounting and its various users. Including internal and

external stakeholders. Further, the study also shows various calculations relating to preparation

of financial statements of sole traders, company and partnership firm, and calculations as to

prepare the bank reconciliation statement along with its purposes. In addition, it also shows

preparation of sales ledger and purchase ledger control accounts preparation of financial

statements with the help of suspense account.

A Report To The Line Manager

Cartex Accounting

To,

The line manager.

From,

Jr. Accountant

Subject: A report providing information about financial accounting, its purposes and usage.

1. Financial accounting and its purposes

Financial accounting

“Financial accounting can be defines as a branch of accounting that helps the business in

providing professional and specialised services to the organisation in order to maintain a

standard in the books of accounts of the company” (Financial Accounting .2019) .

Preparation of financial accounting is based on some basic principles, rules and

guidelines, that helps the professionals in recording the financial data in the books and

preparation of various financial reports of the company.

In other words, it can be evaluated that “financial accounting is a process that includes,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

evaluation, recording and summarisation of the financial data for the purpose of providing all

the material data of the company at a single place.”

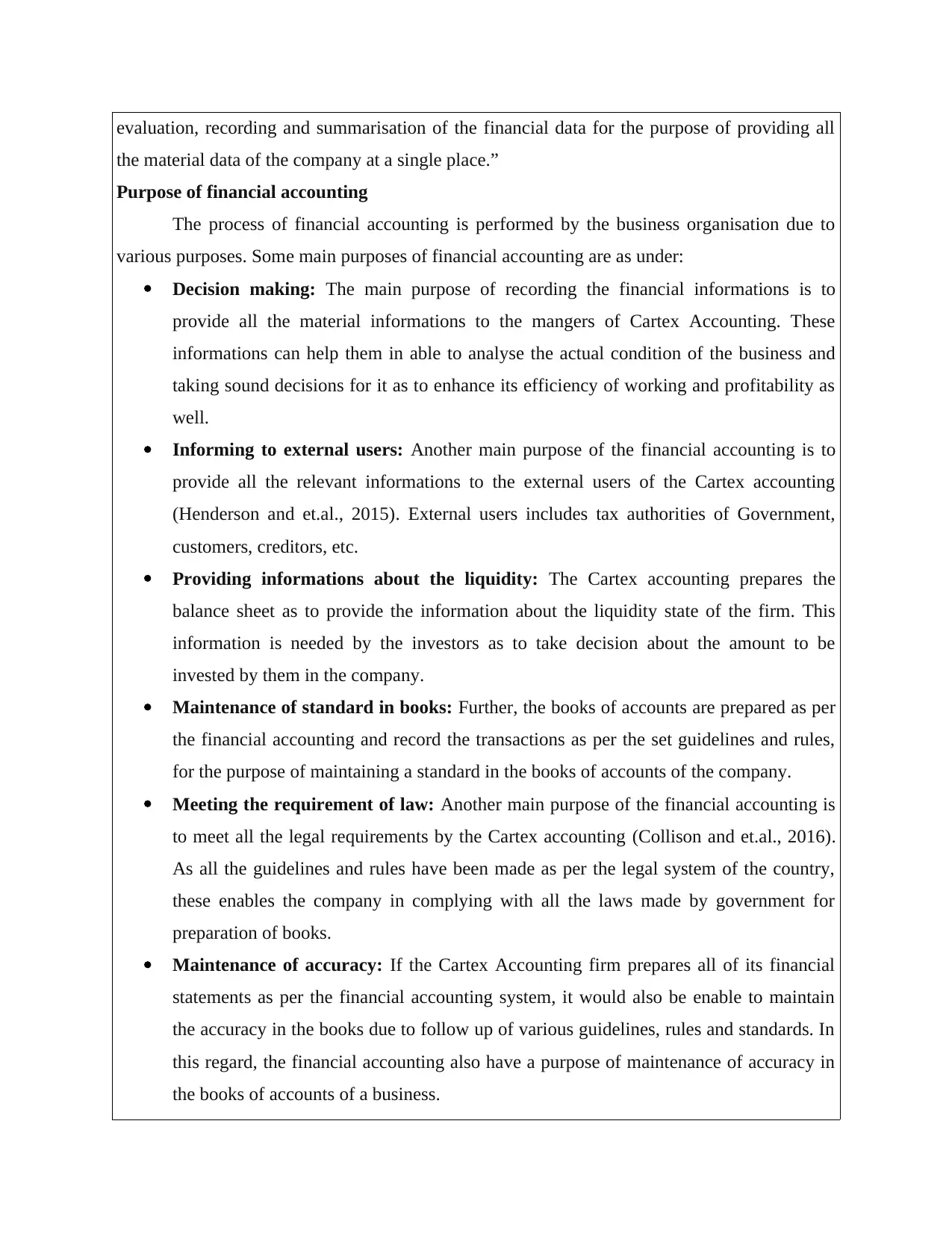

Purpose of financial accounting

The process of financial accounting is performed by the business organisation due to

various purposes. Some main purposes of financial accounting are as under:

Decision making: The main purpose of recording the financial informations is to

provide all the material informations to the mangers of Cartex Accounting. These

informations can help them in able to analyse the actual condition of the business and

taking sound decisions for it as to enhance its efficiency of working and profitability as

well.

Informing to external users: Another main purpose of the financial accounting is to

provide all the relevant informations to the external users of the Cartex accounting

(Henderson and et.al., 2015). External users includes tax authorities of Government,

customers, creditors, etc.

Providing informations about the liquidity: The Cartex accounting prepares the

balance sheet as to provide the information about the liquidity state of the firm. This

information is needed by the investors as to take decision about the amount to be

invested by them in the company.

Maintenance of standard in books: Further, the books of accounts are prepared as per

the financial accounting and record the transactions as per the set guidelines and rules,

for the purpose of maintaining a standard in the books of accounts of the company.

Meeting the requirement of law: Another main purpose of the financial accounting is

to meet all the legal requirements by the Cartex accounting (Collison and et.al., 2016).

As all the guidelines and rules have been made as per the legal system of the country,

these enables the company in complying with all the laws made by government for

preparation of books.

Maintenance of accuracy: If the Cartex Accounting firm prepares all of its financial

statements as per the financial accounting system, it would also be enable to maintain

the accuracy in the books due to follow up of various guidelines, rules and standards. In

this regard, the financial accounting also have a purpose of maintenance of accuracy in

the books of accounts of a business.

the material data of the company at a single place.”

Purpose of financial accounting

The process of financial accounting is performed by the business organisation due to

various purposes. Some main purposes of financial accounting are as under:

Decision making: The main purpose of recording the financial informations is to

provide all the material informations to the mangers of Cartex Accounting. These

informations can help them in able to analyse the actual condition of the business and

taking sound decisions for it as to enhance its efficiency of working and profitability as

well.

Informing to external users: Another main purpose of the financial accounting is to

provide all the relevant informations to the external users of the Cartex accounting

(Henderson and et.al., 2015). External users includes tax authorities of Government,

customers, creditors, etc.

Providing informations about the liquidity: The Cartex accounting prepares the

balance sheet as to provide the information about the liquidity state of the firm. This

information is needed by the investors as to take decision about the amount to be

invested by them in the company.

Maintenance of standard in books: Further, the books of accounts are prepared as per

the financial accounting and record the transactions as per the set guidelines and rules,

for the purpose of maintaining a standard in the books of accounts of the company.

Meeting the requirement of law: Another main purpose of the financial accounting is

to meet all the legal requirements by the Cartex accounting (Collison and et.al., 2016).

As all the guidelines and rules have been made as per the legal system of the country,

these enables the company in complying with all the laws made by government for

preparation of books.

Maintenance of accuracy: If the Cartex Accounting firm prepares all of its financial

statements as per the financial accounting system, it would also be enable to maintain

the accuracy in the books due to follow up of various guidelines, rules and standards. In

this regard, the financial accounting also have a purpose of maintenance of accuracy in

the books of accounts of a business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

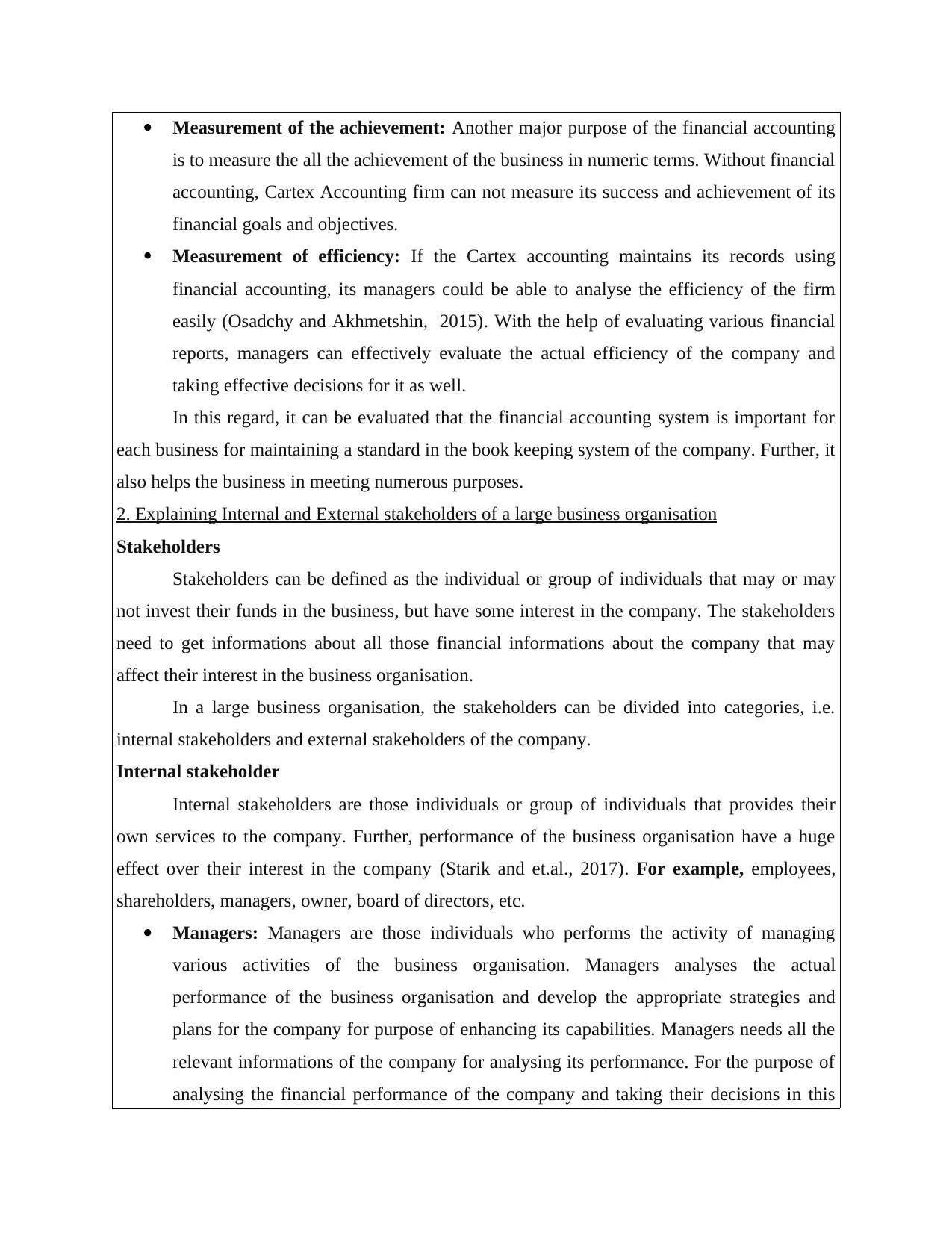

Measurement of the achievement: Another major purpose of the financial accounting

is to measure the all the achievement of the business in numeric terms. Without financial

accounting, Cartex Accounting firm can not measure its success and achievement of its

financial goals and objectives.

Measurement of efficiency: If the Cartex accounting maintains its records using

financial accounting, its managers could be able to analyse the efficiency of the firm

easily (Osadchy and Akhmetshin, 2015). With the help of evaluating various financial

reports, managers can effectively evaluate the actual efficiency of the company and

taking effective decisions for it as well.

In this regard, it can be evaluated that the financial accounting system is important for

each business for maintaining a standard in the book keeping system of the company. Further, it

also helps the business in meeting numerous purposes.

2. Explaining Internal and External stakeholders of a large business organisation

Stakeholders

Stakeholders can be defined as the individual or group of individuals that may or may

not invest their funds in the business, but have some interest in the company. The stakeholders

need to get informations about all those financial informations about the company that may

affect their interest in the business organisation.

In a large business organisation, the stakeholders can be divided into categories, i.e.

internal stakeholders and external stakeholders of the company.

Internal stakeholder

Internal stakeholders are those individuals or group of individuals that provides their

own services to the company. Further, performance of the business organisation have a huge

effect over their interest in the company (Starik and et.al., 2017). For example, employees,

shareholders, managers, owner, board of directors, etc.

Managers: Managers are those individuals who performs the activity of managing

various activities of the business organisation. Managers analyses the actual

performance of the business organisation and develop the appropriate strategies and

plans for the company for purpose of enhancing its capabilities. Managers needs all the

relevant informations of the company for analysing its performance. For the purpose of

analysing the financial performance of the company and taking their decisions in this

is to measure the all the achievement of the business in numeric terms. Without financial

accounting, Cartex Accounting firm can not measure its success and achievement of its

financial goals and objectives.

Measurement of efficiency: If the Cartex accounting maintains its records using

financial accounting, its managers could be able to analyse the efficiency of the firm

easily (Osadchy and Akhmetshin, 2015). With the help of evaluating various financial

reports, managers can effectively evaluate the actual efficiency of the company and

taking effective decisions for it as well.

In this regard, it can be evaluated that the financial accounting system is important for

each business for maintaining a standard in the book keeping system of the company. Further, it

also helps the business in meeting numerous purposes.

2. Explaining Internal and External stakeholders of a large business organisation

Stakeholders

Stakeholders can be defined as the individual or group of individuals that may or may

not invest their funds in the business, but have some interest in the company. The stakeholders

need to get informations about all those financial informations about the company that may

affect their interest in the business organisation.

In a large business organisation, the stakeholders can be divided into categories, i.e.

internal stakeholders and external stakeholders of the company.

Internal stakeholder

Internal stakeholders are those individuals or group of individuals that provides their

own services to the company. Further, performance of the business organisation have a huge

effect over their interest in the company (Starik and et.al., 2017). For example, employees,

shareholders, managers, owner, board of directors, etc.

Managers: Managers are those individuals who performs the activity of managing

various activities of the business organisation. Managers analyses the actual

performance of the business organisation and develop the appropriate strategies and

plans for the company for purpose of enhancing its capabilities. Managers needs all the

relevant informations of the company for analysing its performance. For the purpose of

analysing the financial performance of the company and taking their decisions in this

regard, the managers need the financial reports as to gain informations about the

financial activities of the company. Therefore, managers have interest in the financial

informations of the company.

Shareholders: In a large organisation like companies, the shareholders are the actual

owners of the company. Shareholders are those individuals that invests their funds in the

company, which is used by it as a part of equity for running its normal course of

business activities and expanding its business as well (Boesso, Favotto and Michelon,

2015). Shareholders also needs the financial reports of the company as to analyse the

financial capacity and profitability of the company. Profitability of the company affects

the amount of dividend of the shareholders. Therefore, for the purpose of taking

decisions for maintaining, enhancing or reducing their shareholding in the company,

shareholders needs to analyse the financial reports of the company. In this regard, they

also have interest in the financial informations of the company.

External stakeholders

External shareholders can defined as those individuals that does not provide their

services to the company, and also are not the part of management of the business organisation,

but the financial performance of the company indirectly affects the interest of these

stakeholders. For example, Investors, creditors, suppliers, customers, Government authorities,

competitors, etc.

Investors: Investors are one of the major external stakeholders of a business

organisation. They invest their funds in the business for the purpose of providing

financial help to the company and enabling it to run its normal course of business

activities smoothly. They need to determine the financial performance of the firm for

the purpose of analysing the capacity of the company in paying their interest and the risk

involved in making investment in the company as well.

In this way, the investors are interested in the financial informations of the business

organisation. Further, financial performance of the business directly effects their decision of

making investment in the company.

Creditors: In a business organisation, creditors can be defined as those individuals or

firm or any other business, from which a company has purchased goods, raw materials,

assets or any other thing on credit for the purpose of using it in the business operations

financial activities of the company. Therefore, managers have interest in the financial

informations of the company.

Shareholders: In a large organisation like companies, the shareholders are the actual

owners of the company. Shareholders are those individuals that invests their funds in the

company, which is used by it as a part of equity for running its normal course of

business activities and expanding its business as well (Boesso, Favotto and Michelon,

2015). Shareholders also needs the financial reports of the company as to analyse the

financial capacity and profitability of the company. Profitability of the company affects

the amount of dividend of the shareholders. Therefore, for the purpose of taking

decisions for maintaining, enhancing or reducing their shareholding in the company,

shareholders needs to analyse the financial reports of the company. In this regard, they

also have interest in the financial informations of the company.

External stakeholders

External shareholders can defined as those individuals that does not provide their

services to the company, and also are not the part of management of the business organisation,

but the financial performance of the company indirectly affects the interest of these

stakeholders. For example, Investors, creditors, suppliers, customers, Government authorities,

competitors, etc.

Investors: Investors are one of the major external stakeholders of a business

organisation. They invest their funds in the business for the purpose of providing

financial help to the company and enabling it to run its normal course of business

activities smoothly. They need to determine the financial performance of the firm for

the purpose of analysing the capacity of the company in paying their interest and the risk

involved in making investment in the company as well.

In this way, the investors are interested in the financial informations of the business

organisation. Further, financial performance of the business directly effects their decision of

making investment in the company.

Creditors: In a business organisation, creditors can be defined as those individuals or

firm or any other business, from which a company has purchased goods, raw materials,

assets or any other thing on credit for the purpose of using it in the business operations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Diouf and Boiral, 2017).

Creditors also have interest in the financial performance of a business as the creditworthiness of

the organisation affects their decision of providing their goods or services on credit of the

company.

Auditors: Auditors are the professionals that examines the financial reports of the

company. They ensure the compliance of all guidelines, rules and standards of

preparation of financial statements of the company. Reports prepared by them showing

all the details about their examination are being relied by the suppliers, investors and

other individuals in their decision making process.

Auditors needs all the financial reports for the purpose of performing all the activities of

auditing procedures efficiently and developing the examination reports with accuracy. In this

regard, auditors also have interest in the financial reports of the business.

Government authorities: Government authorities also have vital interest in the books

of a business organisation. Government have interest in the financial informations of the

company for the purpose of determining tax liability of the firm (Del Giudice,

Manganelli and De Paola, 2016). Further, they also need the information for ensuring

the compliance of all the laws by the company and ensuring the disclosure of all the

material informations of the company.

In this regard, it can be analysed that there are numerous stakeholders of a large business

organisation. Each stakeholder has directly or indirectly interest in various financial

informations of the firm.

Client 1

Preparation of financial statements of the Alexandra

Journal entries in the books of Alexandra for January are as follows

Date Particulars Debit Credit

1st jan 2019 Storage expense a/c dr 450

To bank a/c

2nd jan 2019 Purchase a/c dr 6080

To s. hood a/c 1450

Creditors also have interest in the financial performance of a business as the creditworthiness of

the organisation affects their decision of providing their goods or services on credit of the

company.

Auditors: Auditors are the professionals that examines the financial reports of the

company. They ensure the compliance of all guidelines, rules and standards of

preparation of financial statements of the company. Reports prepared by them showing

all the details about their examination are being relied by the suppliers, investors and

other individuals in their decision making process.

Auditors needs all the financial reports for the purpose of performing all the activities of

auditing procedures efficiently and developing the examination reports with accuracy. In this

regard, auditors also have interest in the financial reports of the business.

Government authorities: Government authorities also have vital interest in the books

of a business organisation. Government have interest in the financial informations of the

company for the purpose of determining tax liability of the firm (Del Giudice,

Manganelli and De Paola, 2016). Further, they also need the information for ensuring

the compliance of all the laws by the company and ensuring the disclosure of all the

material informations of the company.

In this regard, it can be analysed that there are numerous stakeholders of a large business

organisation. Each stakeholder has directly or indirectly interest in various financial

informations of the firm.

Client 1

Preparation of financial statements of the Alexandra

Journal entries in the books of Alexandra for January are as follows

Date Particulars Debit Credit

1st jan 2019 Storage expense a/c dr 450

To bank a/c

2nd jan 2019 Purchase a/c dr 6080

To s. hood a/c 1450

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

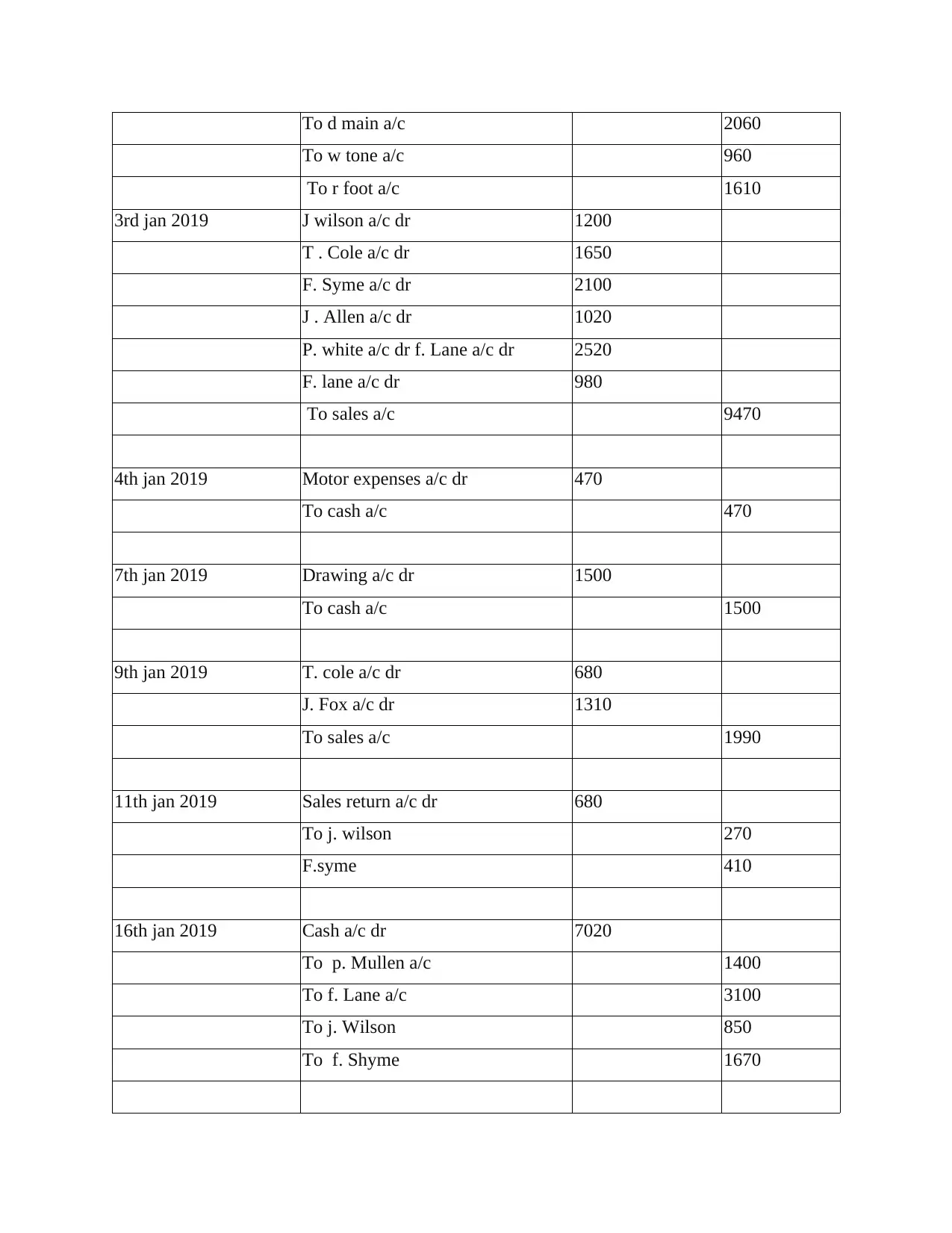

To d main a/c 2060

To w tone a/c 960

To r foot a/c 1610

3rd jan 2019 J wilson a/c dr 1200

T . Cole a/c dr 1650

F. Syme a/c dr 2100

J . Allen a/c dr 1020

P. white a/c dr f. Lane a/c dr 2520

F. lane a/c dr 980

To sales a/c 9470

4th jan 2019 Motor expenses a/c dr 470

To cash a/c 470

7th jan 2019 Drawing a/c dr 1500

To cash a/c 1500

9th jan 2019 T. cole a/c dr 680

J. Fox a/c dr 1310

To sales a/c 1990

11th jan 2019 Sales return a/c dr 680

To j. wilson 270

F.syme 410

16th jan 2019 Cash a/c dr 7020

To p. Mullen a/c 1400

To f. Lane a/c 3100

To j. Wilson 850

To f. Shyme 1670

To w tone a/c 960

To r foot a/c 1610

3rd jan 2019 J wilson a/c dr 1200

T . Cole a/c dr 1650

F. Syme a/c dr 2100

J . Allen a/c dr 1020

P. white a/c dr f. Lane a/c dr 2520

F. lane a/c dr 980

To sales a/c 9470

4th jan 2019 Motor expenses a/c dr 470

To cash a/c 470

7th jan 2019 Drawing a/c dr 1500

To cash a/c 1500

9th jan 2019 T. cole a/c dr 680

J. Fox a/c dr 1310

To sales a/c 1990

11th jan 2019 Sales return a/c dr 680

To j. wilson 270

F.syme 410

16th jan 2019 Cash a/c dr 7020

To p. Mullen a/c 1400

To f. Lane a/c 3100

To j. Wilson 850

To f. Shyme 1670

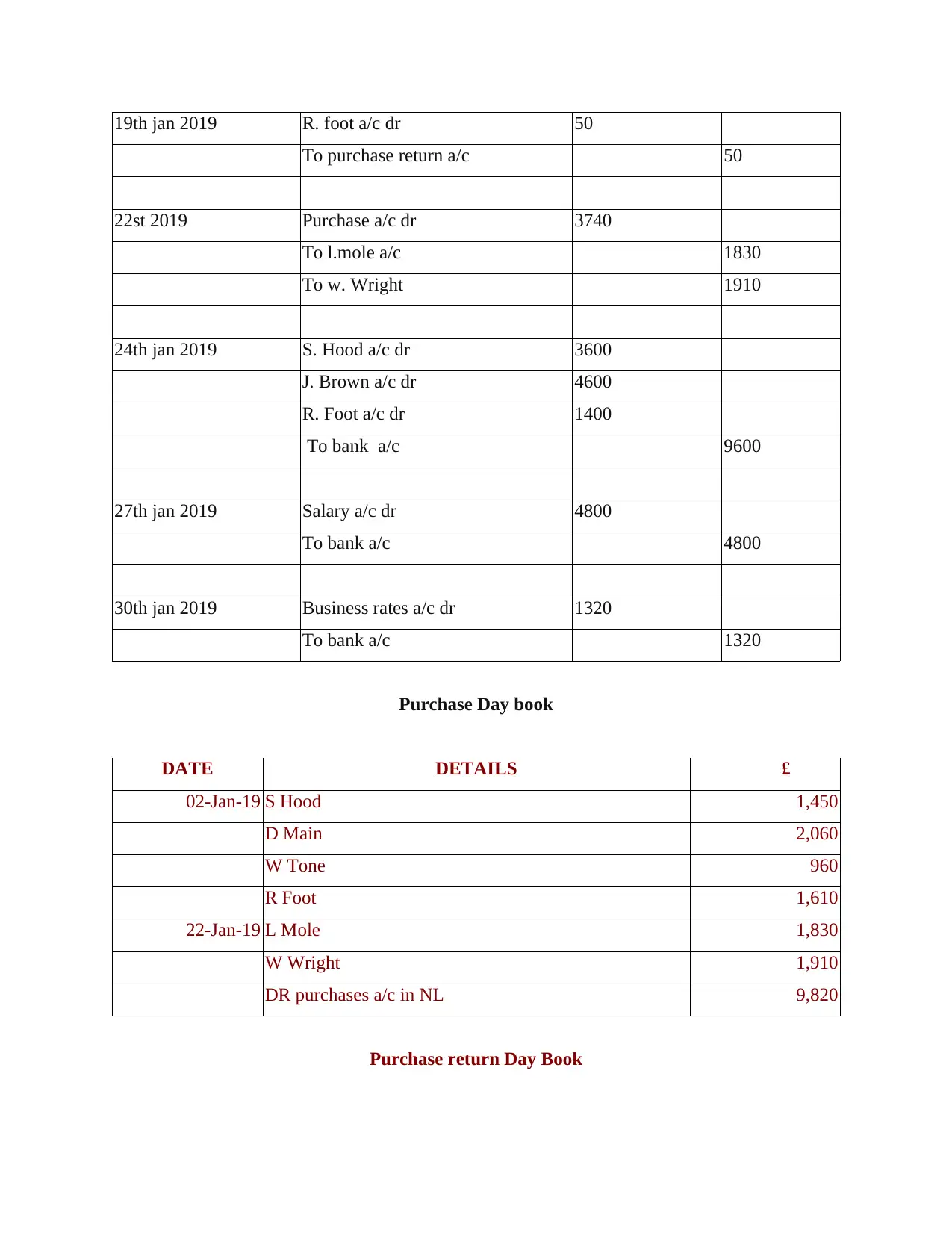

19th jan 2019 R. foot a/c dr 50

To purchase return a/c 50

22st 2019 Purchase a/c dr 3740

To l.mole a/c 1830

To w. Wright 1910

24th jan 2019 S. Hood a/c dr 3600

J. Brown a/c dr 4600

R. Foot a/c dr 1400

To bank a/c 9600

27th jan 2019 Salary a/c dr 4800

To bank a/c 4800

30th jan 2019 Business rates a/c dr 1320

To bank a/c 1320

Purchase Day book

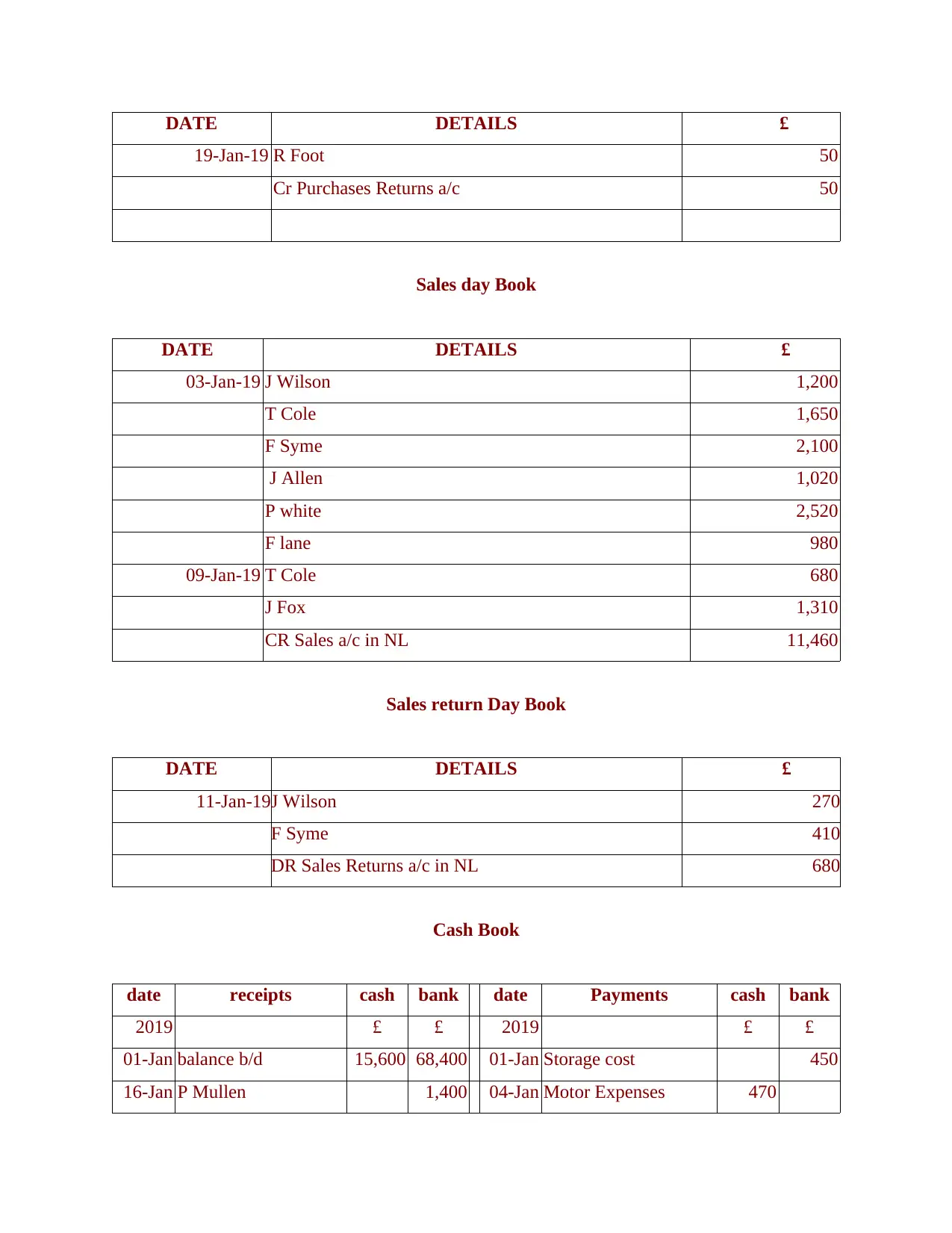

DATE DETAILS £

02-Jan-19 S Hood 1,450

D Main 2,060

W Tone 960

R Foot 1,610

22-Jan-19 L Mole 1,830

W Wright 1,910

DR purchases a/c in NL 9,820

Purchase return Day Book

To purchase return a/c 50

22st 2019 Purchase a/c dr 3740

To l.mole a/c 1830

To w. Wright 1910

24th jan 2019 S. Hood a/c dr 3600

J. Brown a/c dr 4600

R. Foot a/c dr 1400

To bank a/c 9600

27th jan 2019 Salary a/c dr 4800

To bank a/c 4800

30th jan 2019 Business rates a/c dr 1320

To bank a/c 1320

Purchase Day book

DATE DETAILS £

02-Jan-19 S Hood 1,450

D Main 2,060

W Tone 960

R Foot 1,610

22-Jan-19 L Mole 1,830

W Wright 1,910

DR purchases a/c in NL 9,820

Purchase return Day Book

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DATE DETAILS £

19-Jan-19 R Foot 50

Cr Purchases Returns a/c 50

Sales day Book

DATE DETAILS £

03-Jan-19 J Wilson 1,200

T Cole 1,650

F Syme 2,100

J Allen 1,020

P white 2,520

F lane 980

09-Jan-19 T Cole 680

J Fox 1,310

CR Sales a/c in NL 11,460

Sales return Day Book

DATE DETAILS £

11-Jan-19J Wilson 270

F Syme 410

DR Sales Returns a/c in NL 680

Cash Book

date receipts cash bank date Payments cash bank

2019 £ £ 2019 £ £

01-Jan balance b/d 15,600 68,400 01-Jan Storage cost 450

16-Jan P Mullen 1,400 04-Jan Motor Expenses 470

19-Jan-19 R Foot 50

Cr Purchases Returns a/c 50

Sales day Book

DATE DETAILS £

03-Jan-19 J Wilson 1,200

T Cole 1,650

F Syme 2,100

J Allen 1,020

P white 2,520

F lane 980

09-Jan-19 T Cole 680

J Fox 1,310

CR Sales a/c in NL 11,460

Sales return Day Book

DATE DETAILS £

11-Jan-19J Wilson 270

F Syme 410

DR Sales Returns a/c in NL 680

Cash Book

date receipts cash bank date Payments cash bank

2019 £ £ 2019 £ £

01-Jan balance b/d 15,600 68,400 01-Jan Storage cost 450

16-Jan P Mullen 1,400 04-Jan Motor Expenses 470

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

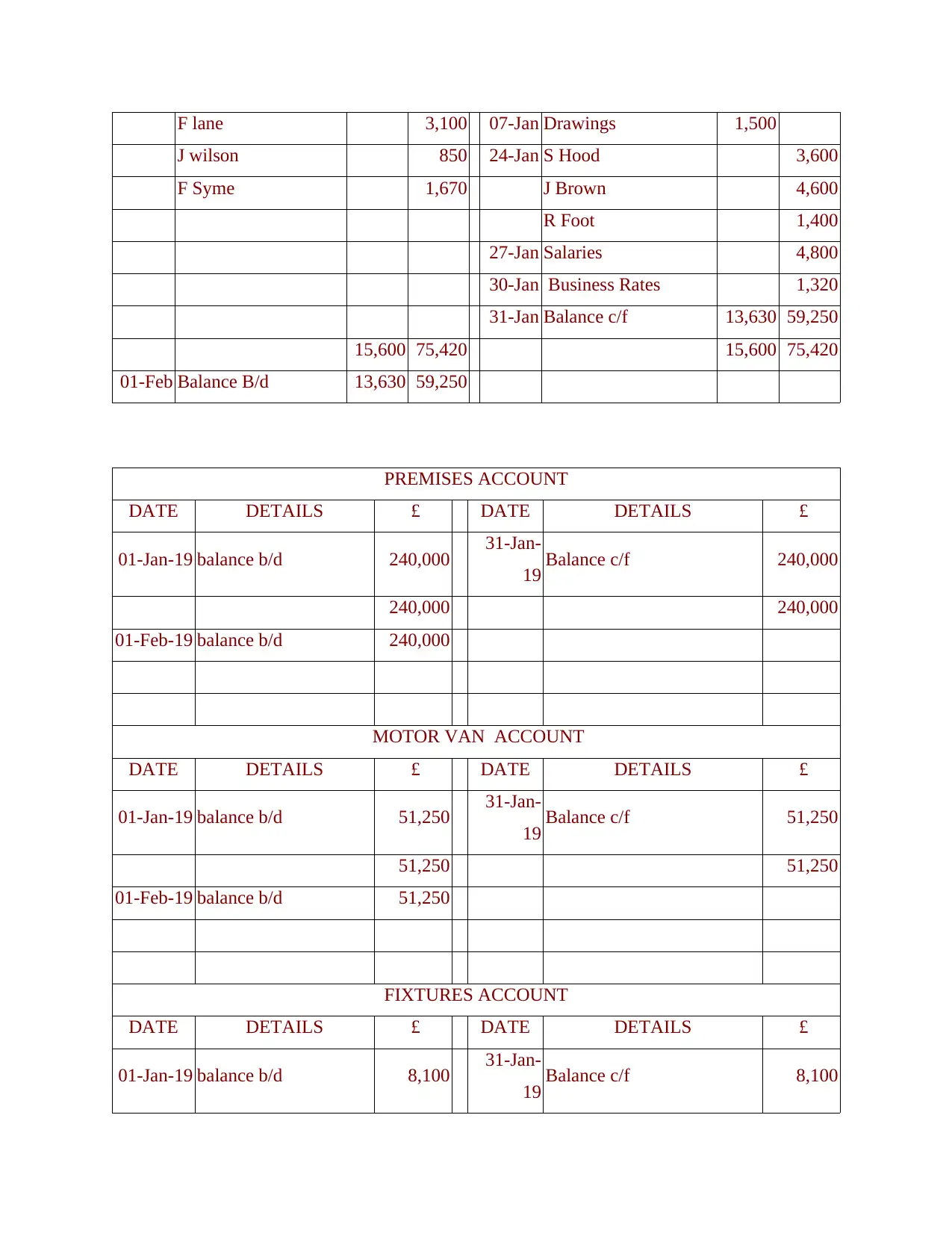

F lane 3,100 07-Jan Drawings 1,500

J wilson 850 24-Jan S Hood 3,600

F Syme 1,670 J Brown 4,600

R Foot 1,400

27-Jan Salaries 4,800

30-Jan Business Rates 1,320

31-Jan Balance c/f 13,630 59,250

15,600 75,420 15,600 75,420

01-Feb Balance B/d 13,630 59,250

PREMISES ACCOUNT

DATE DETAILS £ DATE DETAILS £

01-Jan-19 balance b/d 240,000 31-Jan-

19 Balance c/f 240,000

240,000 240,000

01-Feb-19 balance b/d 240,000

MOTOR VAN ACCOUNT

DATE DETAILS £ DATE DETAILS £

01-Jan-19 balance b/d 51,250 31-Jan-

19 Balance c/f 51,250

51,250 51,250

01-Feb-19 balance b/d 51,250

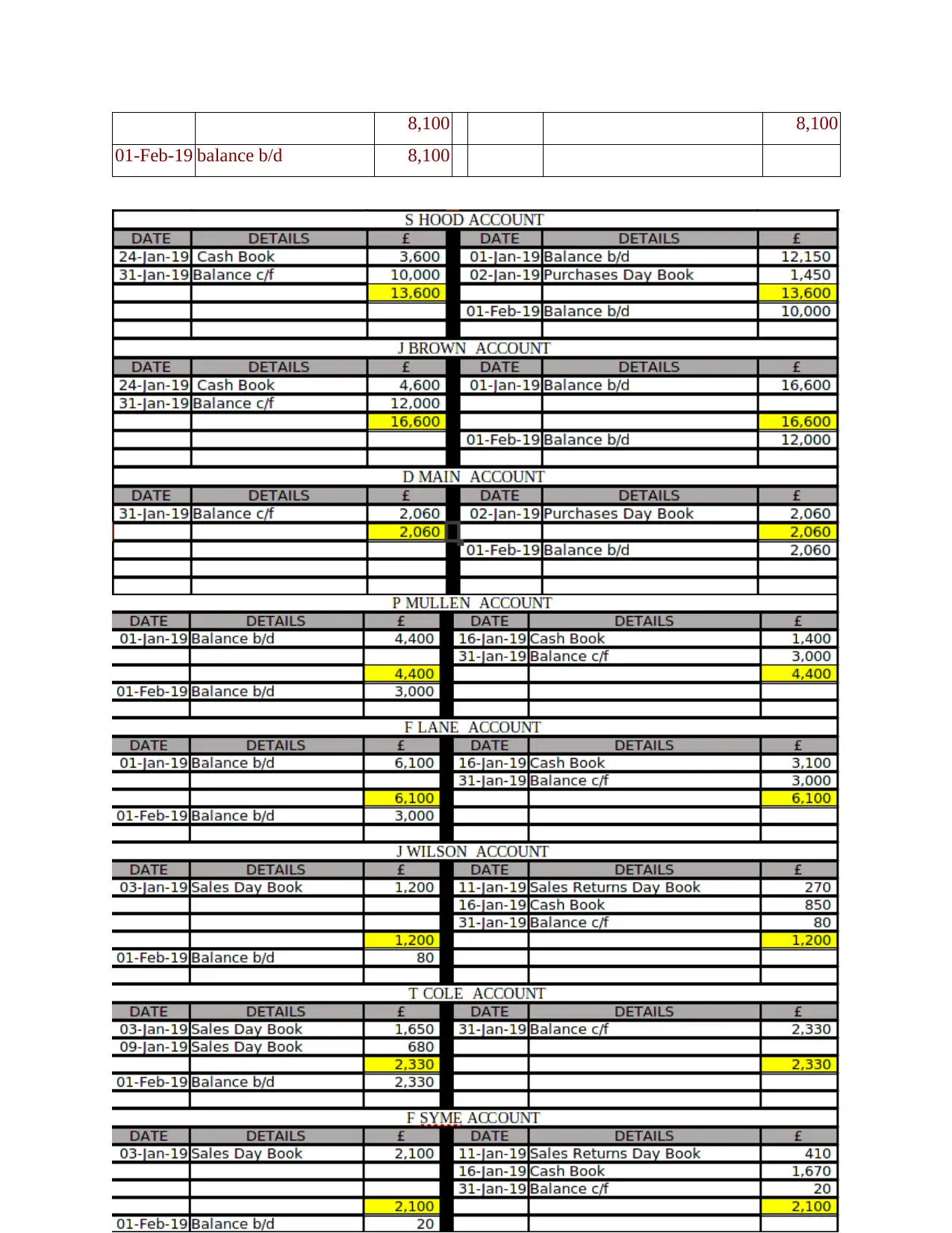

FIXTURES ACCOUNT

DATE DETAILS £ DATE DETAILS £

01-Jan-19 balance b/d 8,100 31-Jan-

19 Balance c/f 8,100

J wilson 850 24-Jan S Hood 3,600

F Syme 1,670 J Brown 4,600

R Foot 1,400

27-Jan Salaries 4,800

30-Jan Business Rates 1,320

31-Jan Balance c/f 13,630 59,250

15,600 75,420 15,600 75,420

01-Feb Balance B/d 13,630 59,250

PREMISES ACCOUNT

DATE DETAILS £ DATE DETAILS £

01-Jan-19 balance b/d 240,000 31-Jan-

19 Balance c/f 240,000

240,000 240,000

01-Feb-19 balance b/d 240,000

MOTOR VAN ACCOUNT

DATE DETAILS £ DATE DETAILS £

01-Jan-19 balance b/d 51,250 31-Jan-

19 Balance c/f 51,250

51,250 51,250

01-Feb-19 balance b/d 51,250

FIXTURES ACCOUNT

DATE DETAILS £ DATE DETAILS £

01-Jan-19 balance b/d 8,100 31-Jan-

19 Balance c/f 8,100

8,100 8,100

01-Feb-19 balance b/d 8,100

01-Feb-19 balance b/d 8,100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.