Financial Accounting Principles: Regulations, Rules, and Statements

VerifiedAdded on 2024/06/04

|27

|4011

|468

Practical Assignment

AI Summary

This assignment provides a detailed overview of financial accounting principles, regulations, rules, and concepts. It begins by defining financial accounting and its role in reporting and analyzing financial transactions, emphasizing the importance of GAAP and IFRS. The assignment then explores various regulations, including the Accounting Standard Board and Statements of Principles, highlighting their impact on financial reporting. It describes fundamental accounting rules and principles like the Full Disclosure Principle, Going Concern Principle, Matching Principle, and Cost Principle. Additionally, the assignment discusses key accounting conventions such as consistency and materiality disclosure. Task B includes practical examples of prime entry bookkeeping and double-entry recording with relevant ledgers for multiple clients, demonstrating the application of these principles in real-world scenarios. Desklib offers a wealth of similar solved assignments and past papers for students seeking further assistance.

Financial Accounting Principles

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................3

PART A.......................................................................................................................................................4

Introduction.............................................................................................................................................4

1. Financial accounting Meaning.........................................................................................................5

2. Regulations related to Financial Accounting...................................................................................5

3. Description about accounting rules and principles...........................................................................6

4. Conventions and Concepts...............................................................................................................7

Conclusion...............................................................................................................................................8

TASK B.......................................................................................................................................................9

Client 1....................................................................................................................................................9

Client 2..................................................................................................................................................17

Client 3..................................................................................................................................................19

Client 4..................................................................................................................................................21

Client 5..................................................................................................................................................23

Client 6..................................................................................................................................................24

Conclusion.................................................................................................................................................26

Bibliography...............................................................................................................................................27

2

Introduction.................................................................................................................................................3

PART A.......................................................................................................................................................4

Introduction.............................................................................................................................................4

1. Financial accounting Meaning.........................................................................................................5

2. Regulations related to Financial Accounting...................................................................................5

3. Description about accounting rules and principles...........................................................................6

4. Conventions and Concepts...............................................................................................................7

Conclusion...............................................................................................................................................8

TASK B.......................................................................................................................................................9

Client 1....................................................................................................................................................9

Client 2..................................................................................................................................................17

Client 3..................................................................................................................................................19

Client 4..................................................................................................................................................21

Client 5..................................................................................................................................................23

Client 6..................................................................................................................................................24

Conclusion.................................................................................................................................................26

Bibliography...............................................................................................................................................27

2

Introduction

The main aim of the report is to understand about the various management accounting principles

with the explanation about the financial accounting, and the rules as well as principles of

financial management. The profit and loss statements are also prepared so that the understanding

of the financial accounts can be gained in the better way. These are the accounts which will help

the manager for the strategic decision making and in turn the profitability will be attained.

3

The main aim of the report is to understand about the various management accounting principles

with the explanation about the financial accounting, and the rules as well as principles of

financial management. The profit and loss statements are also prepared so that the understanding

of the financial accounts can be gained in the better way. These are the accounts which will help

the manager for the strategic decision making and in turn the profitability will be attained.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART A

Introduction

This part of the report deals with the understanding about the financial accounting and what are

the rules and regulations which are used in the financial accounting by the organization. With

this the concepts and the conventions are also heighted which are related to materiality disclosure

and consistency.

4

Introduction

This part of the report deals with the understanding about the financial accounting and what are

the rules and regulations which are used in the financial accounting by the organization. With

this the concepts and the conventions are also heighted which are related to materiality disclosure

and consistency.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Financial accounting Meaning

Financial accounting can be defined as one of the field of accounting which can be used for the

reporting and the analysis of the financial transactions. It is also used in the preparation of the

financial accounts (Onuoha, 2012). The various statements are prepared and then summarization

is done according to that which can be done in balance sheets, profit and loss accounts/income

statement or the cash flow statement. These statements are used to evaluate the performance of

the business operations within the organization. It is governed with the International Financial

Reporting Standards as well as the local standards which are used in the country. But the main

standard which is given in the jurisdiction is the Generally Accepted accounting Principles

(GAAP). These are the standards which define the rules as well as regulations which should be

considered by the organization so that the financial statements can be prepared in accordance

with those standards. These financial statements should be prepared accordingly as they helps to

take the strategic decisions for the long term objectives of the organization (Ramamoorti, 2017).

The statements available in the financial accounts are recorded so that the outsiders can get the

information related to the organization so that they can take decisions related to the investment

purposes. The main objective of the financial accounting is to maintain the capital of the various

objectives of the financial reporting.

2. Regulations related to Financial Accounting

There are various regulations which are related to the financial accounting so that the reporting

of the financial accounting can provide the clear and fair view of the financial statements of the

organization (Tool, 2018). But the main of the regulations which are used by most of the

organizations are:

Accounting Standard Board

The accounting standard board was taken in 1990 from the Accounting Standard Committee. The

main aim of the accounting standard board was to solve the problem of the financial reporting

and corporate accounting by providing the accurate framework (Ramamoorti, 2017). The

accounting standards determines that how the particular transaction should be reported in the

financial statements so that the true and the fair view of the financial accounts can be provided.

5

Financial accounting can be defined as one of the field of accounting which can be used for the

reporting and the analysis of the financial transactions. It is also used in the preparation of the

financial accounts (Onuoha, 2012). The various statements are prepared and then summarization

is done according to that which can be done in balance sheets, profit and loss accounts/income

statement or the cash flow statement. These statements are used to evaluate the performance of

the business operations within the organization. It is governed with the International Financial

Reporting Standards as well as the local standards which are used in the country. But the main

standard which is given in the jurisdiction is the Generally Accepted accounting Principles

(GAAP). These are the standards which define the rules as well as regulations which should be

considered by the organization so that the financial statements can be prepared in accordance

with those standards. These financial statements should be prepared accordingly as they helps to

take the strategic decisions for the long term objectives of the organization (Ramamoorti, 2017).

The statements available in the financial accounts are recorded so that the outsiders can get the

information related to the organization so that they can take decisions related to the investment

purposes. The main objective of the financial accounting is to maintain the capital of the various

objectives of the financial reporting.

2. Regulations related to Financial Accounting

There are various regulations which are related to the financial accounting so that the reporting

of the financial accounting can provide the clear and fair view of the financial statements of the

organization (Tool, 2018). But the main of the regulations which are used by most of the

organizations are:

Accounting Standard Board

The accounting standard board was taken in 1990 from the Accounting Standard Committee. The

main aim of the accounting standard board was to solve the problem of the financial reporting

and corporate accounting by providing the accurate framework (Ramamoorti, 2017). The

accounting standards determines that how the particular transaction should be reported in the

financial statements so that the true and the fair view of the financial accounts can be provided.

5

These standards can be applied to all kinds of the organization irrespective of their nature. But

the initial aim of developing the accounting standards was to properly define the practices of

accounting so that better understanding can be created between the users and the managers of the

organization who are involved in the preparation of financial accounts (Onuoha, 2012).

Statement of Principles

The statement of principle for the financial reporting was published by the accounting standards

board in 1999. It was believed that the statement of the principle helps in assisting the areas of

issues and rethinking on them so that the judgment regarding sufficiency of the disclosures can

be facilitated (Onuoha, 2012). These statements describe the setters of standards on the view that

the activities should be reported and highlighted in the financial statements. The main motive of

these are to provide the framework which will helps in resolving the issues which are faced by

the accountants (Jones, 2012).

3. Description about accounting rules and principles

The accounting rules and the principles are the basic mechanism through which the financial

transactions are recorded in the financial accounts (Jones, 2012). The set of rules are established

so that the recording can be done according to the set rules and the principles are the common set

of the principles which are to be followed so as to comply with financial statements. There are

basically three rules which are:

Type Debit Credit

Personal The receiver The giver

Real What comes in What goes out

Nominal All expenses and losses All income and gains

The principles of accounting are as follows:

Full Disclosure Principle: It states that all the information should be disclosed by the

organization in their financial statements as all the information is important to the investor and

any other lender and the explanation about each entity should also be provided (Jones, 2012).

6

the initial aim of developing the accounting standards was to properly define the practices of

accounting so that better understanding can be created between the users and the managers of the

organization who are involved in the preparation of financial accounts (Onuoha, 2012).

Statement of Principles

The statement of principle for the financial reporting was published by the accounting standards

board in 1999. It was believed that the statement of the principle helps in assisting the areas of

issues and rethinking on them so that the judgment regarding sufficiency of the disclosures can

be facilitated (Onuoha, 2012). These statements describe the setters of standards on the view that

the activities should be reported and highlighted in the financial statements. The main motive of

these are to provide the framework which will helps in resolving the issues which are faced by

the accountants (Jones, 2012).

3. Description about accounting rules and principles

The accounting rules and the principles are the basic mechanism through which the financial

transactions are recorded in the financial accounts (Jones, 2012). The set of rules are established

so that the recording can be done according to the set rules and the principles are the common set

of the principles which are to be followed so as to comply with financial statements. There are

basically three rules which are:

Type Debit Credit

Personal The receiver The giver

Real What comes in What goes out

Nominal All expenses and losses All income and gains

The principles of accounting are as follows:

Full Disclosure Principle: It states that all the information should be disclosed by the

organization in their financial statements as all the information is important to the investor and

any other lender and the explanation about each entity should also be provided (Jones, 2012).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Going Concern Principle: It believes that the organization will continue to operate in the long run

and will not liquidate in any of the unforeseen situations (Jones, 2012). It defers some its prepaid

expenses until the accounting period in future.

Matching Principle: The matching principle says that the expenses of the company should match

its revenues. It is done so that the misreporting of the earnings for the particular period can be

avoided.

Cost Principle: It is the principle which states that the all the assets are to be recorded in the cash

amount when they are acquired not when the settlement is made. This principle is also known as

the historic cost principle (Onuoha, 2012).

4. Conventions and Concepts

The conventions and the concepts are recorded so as to ensure that information related to

accounting in presented in the accurate and the consistent manner (Onuoha, 2012). The

materiality disclosure and the consistency are majorly explained:

Consistency Concept: The consistency concept states that once the accounting principles are

adopted that should be consistency followed in the future accounting periods (Adkins, 2018).

The change can only be made if that changes in leading to the improvement in the financial

results.

Convention of Materiality Disclosure: It is the convention which states that all the materials in

the financial statements should be recorded in proper manner. This will help the investors and the

shareholders to take the decisions accordingly by actually analyzing the financial performance

(Onuoha, 2012).

7

and will not liquidate in any of the unforeseen situations (Jones, 2012). It defers some its prepaid

expenses until the accounting period in future.

Matching Principle: The matching principle says that the expenses of the company should match

its revenues. It is done so that the misreporting of the earnings for the particular period can be

avoided.

Cost Principle: It is the principle which states that the all the assets are to be recorded in the cash

amount when they are acquired not when the settlement is made. This principle is also known as

the historic cost principle (Onuoha, 2012).

4. Conventions and Concepts

The conventions and the concepts are recorded so as to ensure that information related to

accounting in presented in the accurate and the consistent manner (Onuoha, 2012). The

materiality disclosure and the consistency are majorly explained:

Consistency Concept: The consistency concept states that once the accounting principles are

adopted that should be consistency followed in the future accounting periods (Adkins, 2018).

The change can only be made if that changes in leading to the improvement in the financial

results.

Convention of Materiality Disclosure: It is the convention which states that all the materials in

the financial statements should be recorded in proper manner. This will help the investors and the

shareholders to take the decisions accordingly by actually analyzing the financial performance

(Onuoha, 2012).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

It can be concluded that the proper rules and regulations should be followed by the organization

so that transparency can be maintained in the financial accounts and the investment decisions can

be taken accordingly. The financial accounting provides the accurate framework so that the

compliance can be reduced.

8

It can be concluded that the proper rules and regulations should be followed by the organization

so that transparency can be maintained in the financial accounts and the investment decisions can

be taken accordingly. The financial accounting provides the accurate framework so that the

compliance can be reduced.

8

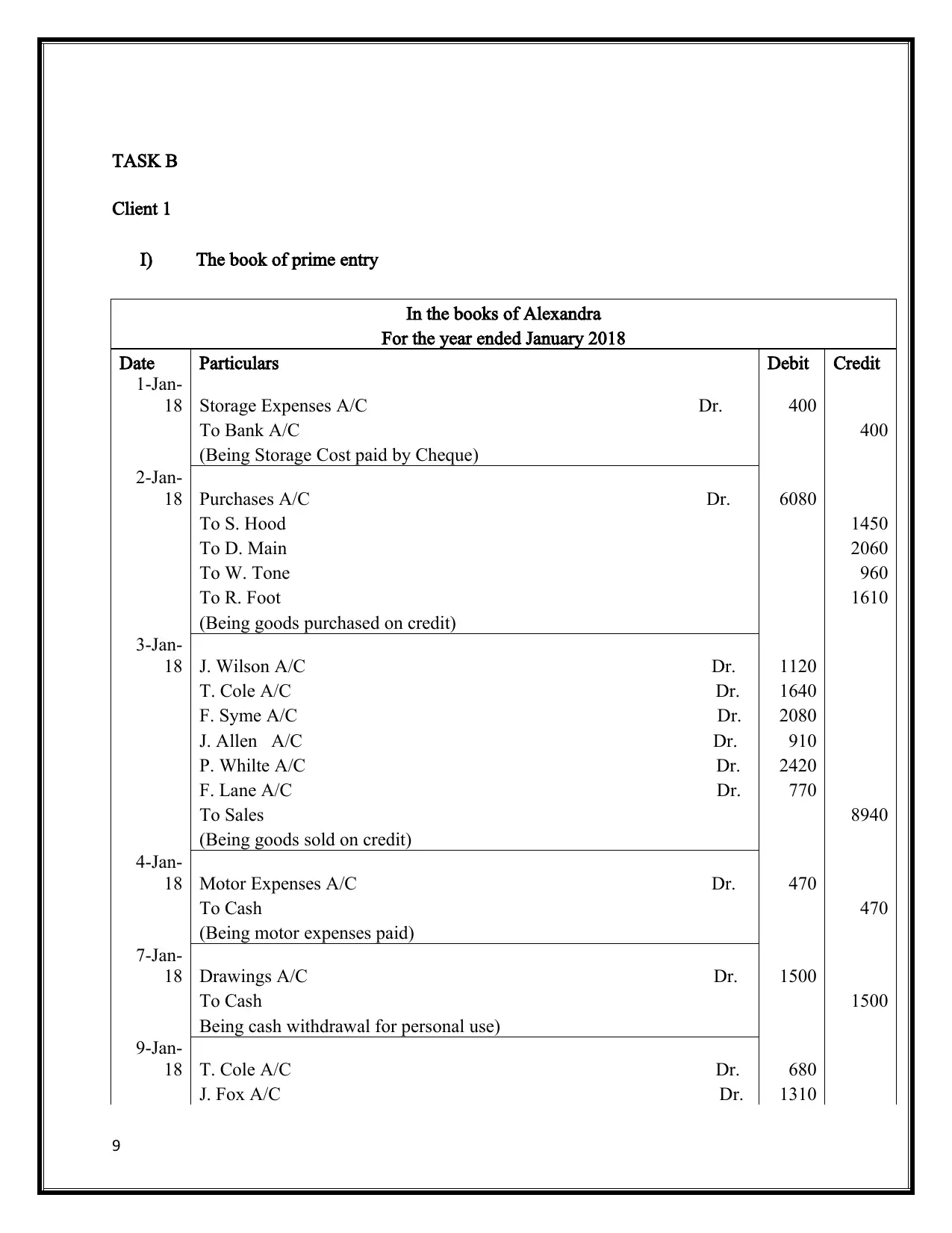

TASK B

Client 1

I) The book of prime entry

In the books of Alexandra

For the year ended January 2018

Date Particulars Debit Credit

1-Jan-

18 Storage Expenses A/C Dr. 400

To Bank A/C 400

(Being Storage Cost paid by Cheque)

2-Jan-

18 Purchases A/C Dr. 6080

To S. Hood 1450

To D. Main 2060

To W. Tone 960

To R. Foot 1610

(Being goods purchased on credit)

3-Jan-

18 J. Wilson A/C Dr. 1120

T. Cole A/C Dr. 1640

F. Syme A/C Dr. 2080

J. Allen A/C Dr. 910

P. Whilte A/C Dr. 2420

F. Lane A/C Dr. 770

To Sales 8940

(Being goods sold on credit)

4-Jan-

18 Motor Expenses A/C Dr. 470

To Cash 470

(Being motor expenses paid)

7-Jan-

18 Drawings A/C Dr. 1500

To Cash 1500

Being cash withdrawal for personal use)

9-Jan-

18 T. Cole A/C Dr. 680

J. Fox A/C Dr. 1310

9

Client 1

I) The book of prime entry

In the books of Alexandra

For the year ended January 2018

Date Particulars Debit Credit

1-Jan-

18 Storage Expenses A/C Dr. 400

To Bank A/C 400

(Being Storage Cost paid by Cheque)

2-Jan-

18 Purchases A/C Dr. 6080

To S. Hood 1450

To D. Main 2060

To W. Tone 960

To R. Foot 1610

(Being goods purchased on credit)

3-Jan-

18 J. Wilson A/C Dr. 1120

T. Cole A/C Dr. 1640

F. Syme A/C Dr. 2080

J. Allen A/C Dr. 910

P. Whilte A/C Dr. 2420

F. Lane A/C Dr. 770

To Sales 8940

(Being goods sold on credit)

4-Jan-

18 Motor Expenses A/C Dr. 470

To Cash 470

(Being motor expenses paid)

7-Jan-

18 Drawings A/C Dr. 1500

To Cash 1500

Being cash withdrawal for personal use)

9-Jan-

18 T. Cole A/C Dr. 680

J. Fox A/C Dr. 1310

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

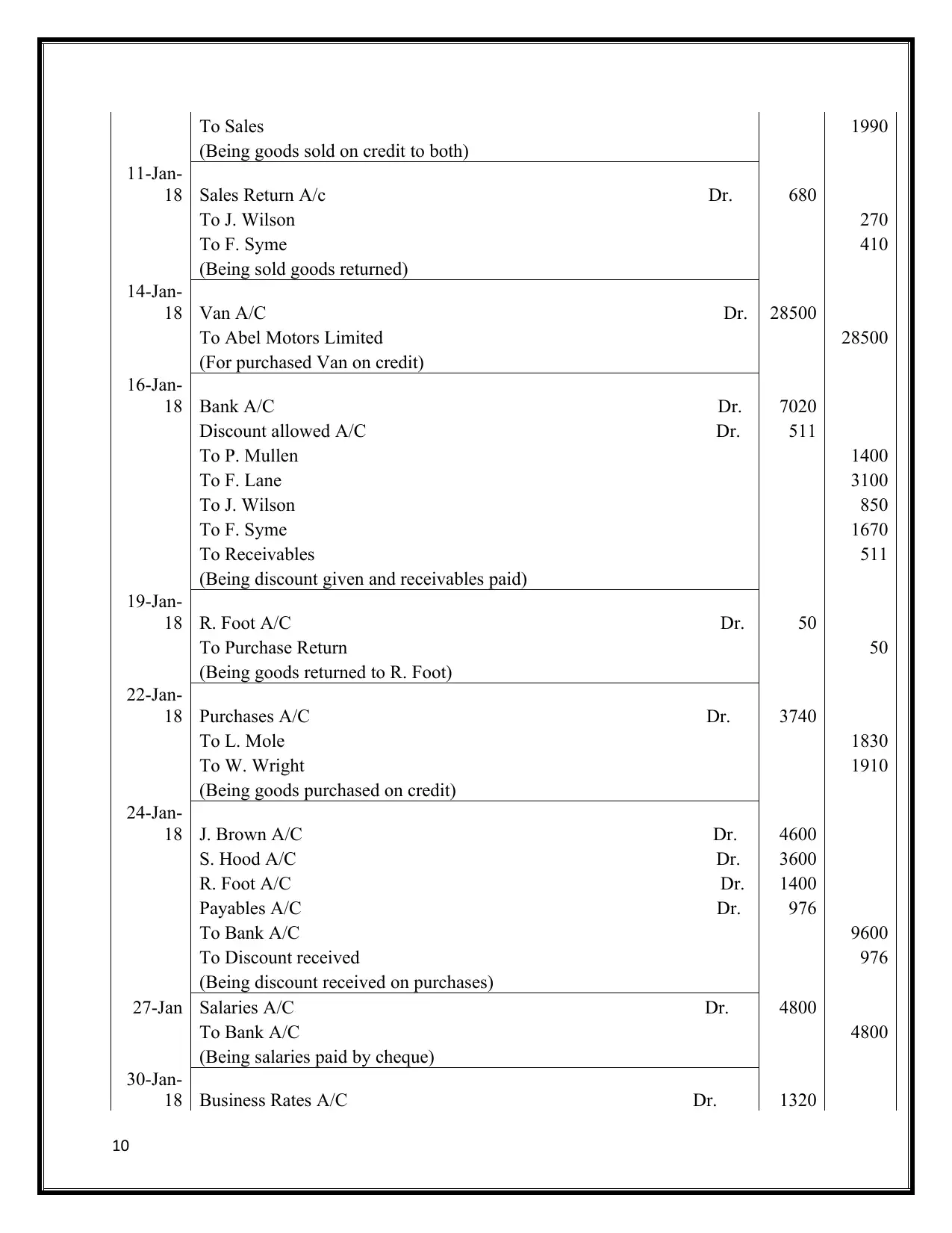

Trusted by 1+ million students worldwide

To Sales 1990

(Being goods sold on credit to both)

11-Jan-

18 Sales Return A/c Dr. 680

To J. Wilson 270

To F. Syme 410

(Being sold goods returned)

14-Jan-

18 Van A/C Dr. 28500

To Abel Motors Limited 28500

(For purchased Van on credit)

16-Jan-

18 Bank A/C Dr. 7020

Discount allowed A/C Dr. 511

To P. Mullen 1400

To F. Lane 3100

To J. Wilson 850

To F. Syme 1670

To Receivables 511

(Being discount given and receivables paid)

19-Jan-

18 R. Foot A/C Dr. 50

To Purchase Return 50

(Being goods returned to R. Foot)

22-Jan-

18 Purchases A/C Dr. 3740

To L. Mole 1830

To W. Wright 1910

(Being goods purchased on credit)

24-Jan-

18 J. Brown A/C Dr. 4600

S. Hood A/C Dr. 3600

R. Foot A/C Dr. 1400

Payables A/C Dr. 976

To Bank A/C 9600

To Discount received 976

(Being discount received on purchases)

27-Jan Salaries A/C Dr. 4800

To Bank A/C 4800

(Being salaries paid by cheque)

30-Jan-

18 Business Rates A/C Dr. 1320

10

(Being goods sold on credit to both)

11-Jan-

18 Sales Return A/c Dr. 680

To J. Wilson 270

To F. Syme 410

(Being sold goods returned)

14-Jan-

18 Van A/C Dr. 28500

To Abel Motors Limited 28500

(For purchased Van on credit)

16-Jan-

18 Bank A/C Dr. 7020

Discount allowed A/C Dr. 511

To P. Mullen 1400

To F. Lane 3100

To J. Wilson 850

To F. Syme 1670

To Receivables 511

(Being discount given and receivables paid)

19-Jan-

18 R. Foot A/C Dr. 50

To Purchase Return 50

(Being goods returned to R. Foot)

22-Jan-

18 Purchases A/C Dr. 3740

To L. Mole 1830

To W. Wright 1910

(Being goods purchased on credit)

24-Jan-

18 J. Brown A/C Dr. 4600

S. Hood A/C Dr. 3600

R. Foot A/C Dr. 1400

Payables A/C Dr. 976

To Bank A/C 9600

To Discount received 976

(Being discount received on purchases)

27-Jan Salaries A/C Dr. 4800

To Bank A/C 4800

(Being salaries paid by cheque)

30-Jan-

18 Business Rates A/C Dr. 1320

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

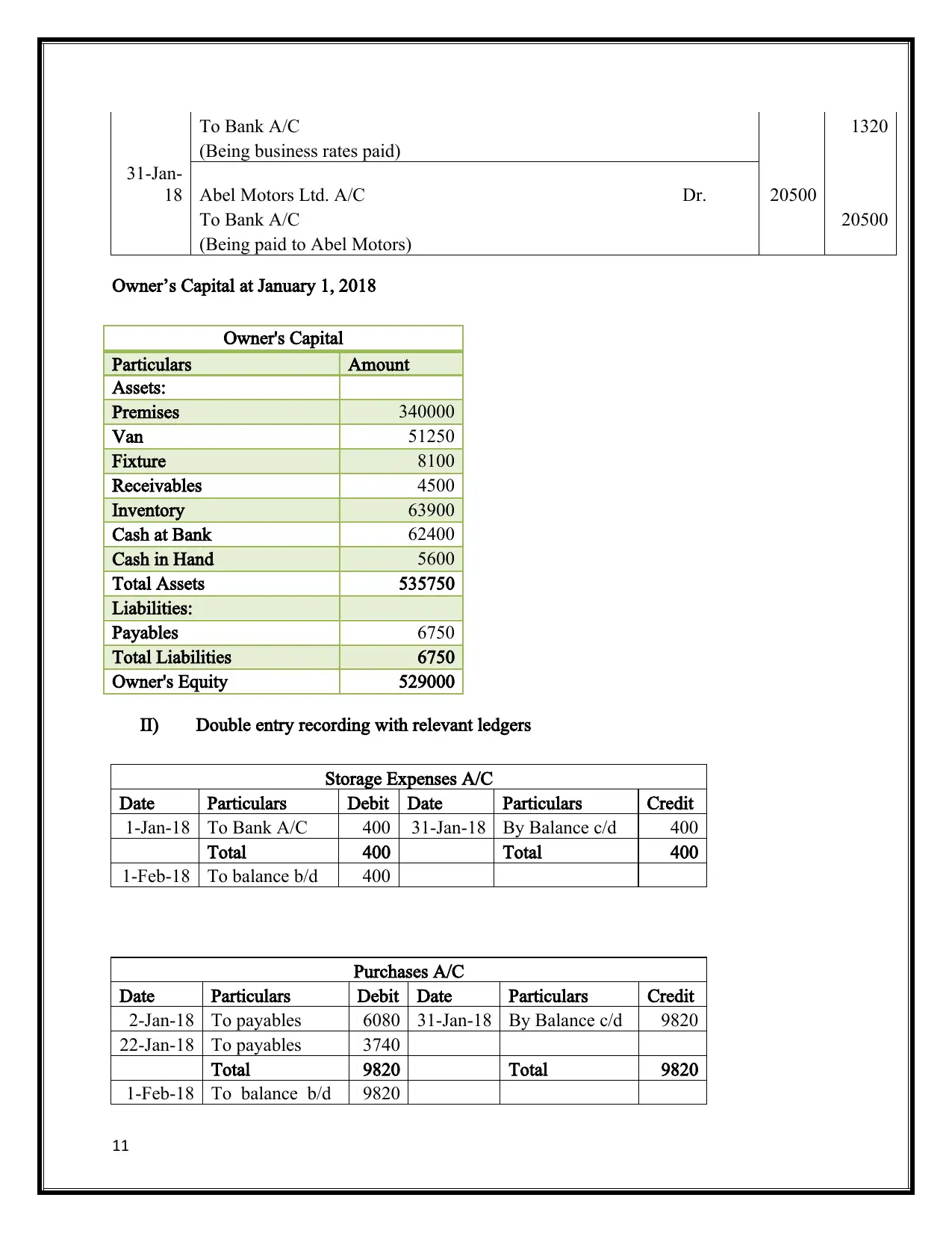

To Bank A/C 1320

(Being business rates paid)

31-Jan-

18 Abel Motors Ltd. A/C Dr. 20500

To Bank A/C 20500

(Being paid to Abel Motors)

Owner’s Capital at January 1, 2018

Owner's Capital

Particulars Amount

Assets:

Premises 340000

Van 51250

Fixture 8100

Receivables 4500

Inventory 63900

Cash at Bank 62400

Cash in Hand 5600

Total Assets 535750

Liabilities:

Payables 6750

Total Liabilities 6750

Owner's Equity 529000

II) Double entry recording with relevant ledgers

Storage Expenses A/C

Date Particulars Debit Date Particulars Credit

1-Jan-18 To Bank A/C 400 31-Jan-18 By Balance c/d 400

Total 400 Total 400

1-Feb-18 To balance b/d 400

Purchases A/C

Date Particulars Debit Date Particulars Credit

2-Jan-18 To payables 6080 31-Jan-18 By Balance c/d 9820

22-Jan-18 To payables 3740

Total 9820 Total 9820

1-Feb-18 To balance b/d 9820

11

(Being business rates paid)

31-Jan-

18 Abel Motors Ltd. A/C Dr. 20500

To Bank A/C 20500

(Being paid to Abel Motors)

Owner’s Capital at January 1, 2018

Owner's Capital

Particulars Amount

Assets:

Premises 340000

Van 51250

Fixture 8100

Receivables 4500

Inventory 63900

Cash at Bank 62400

Cash in Hand 5600

Total Assets 535750

Liabilities:

Payables 6750

Total Liabilities 6750

Owner's Equity 529000

II) Double entry recording with relevant ledgers

Storage Expenses A/C

Date Particulars Debit Date Particulars Credit

1-Jan-18 To Bank A/C 400 31-Jan-18 By Balance c/d 400

Total 400 Total 400

1-Feb-18 To balance b/d 400

Purchases A/C

Date Particulars Debit Date Particulars Credit

2-Jan-18 To payables 6080 31-Jan-18 By Balance c/d 9820

22-Jan-18 To payables 3740

Total 9820 Total 9820

1-Feb-18 To balance b/d 9820

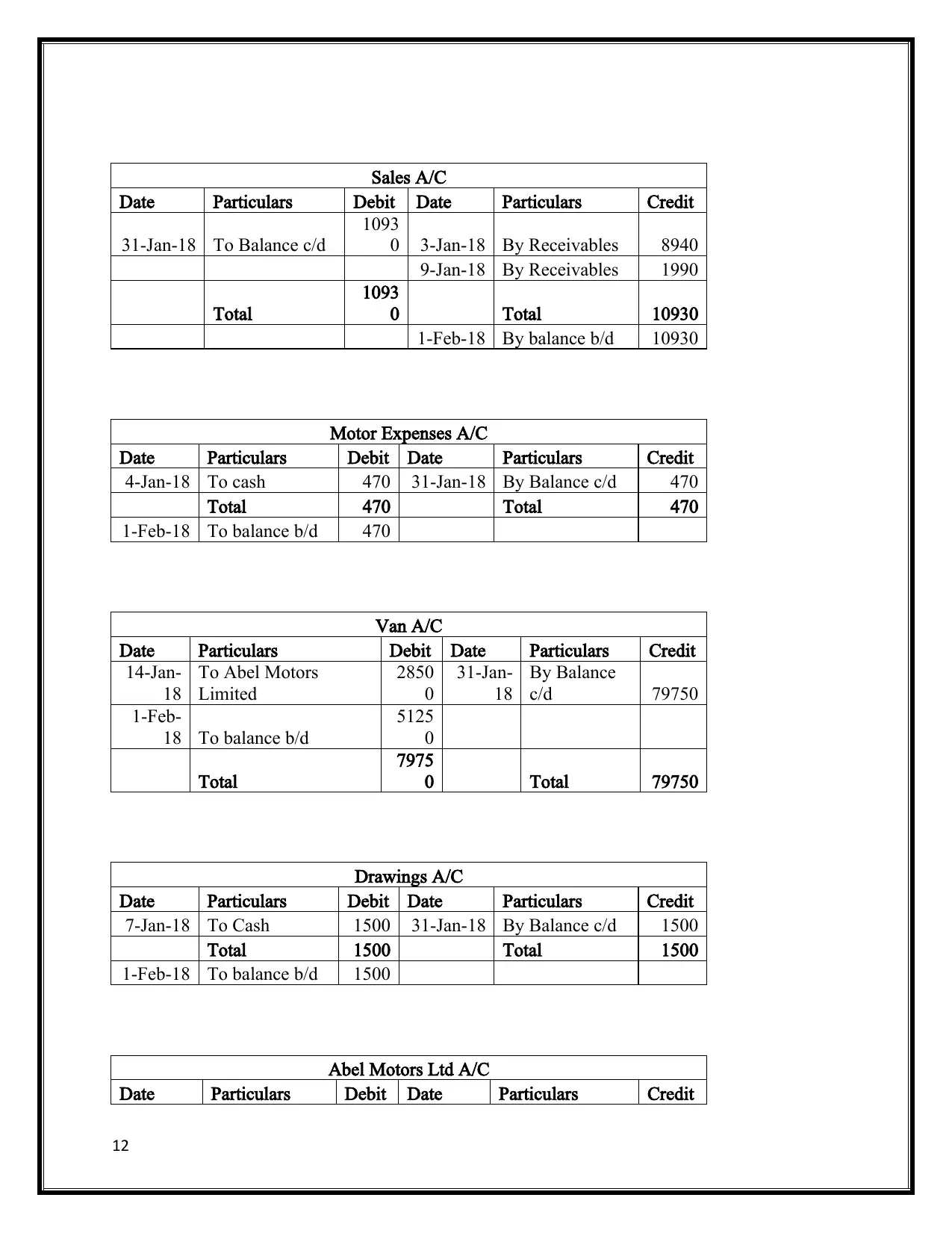

11

Sales A/C

Date Particulars Debit Date Particulars Credit

31-Jan-18 To Balance c/d

1093

0 3-Jan-18 By Receivables 8940

9-Jan-18 By Receivables 1990

Total

1093

0 Total 10930

1-Feb-18 By balance b/d 10930

Motor Expenses A/C

Date Particulars Debit Date Particulars Credit

4-Jan-18 To cash 470 31-Jan-18 By Balance c/d 470

Total 470 Total 470

1-Feb-18 To balance b/d 470

Van A/C

Date Particulars Debit Date Particulars Credit

14-Jan-

18

To Abel Motors

Limited

2850

0

31-Jan-

18

By Balance

c/d 79750

1-Feb-

18 To balance b/d

5125

0

Total

7975

0 Total 79750

Drawings A/C

Date Particulars Debit Date Particulars Credit

7-Jan-18 To Cash 1500 31-Jan-18 By Balance c/d 1500

Total 1500 Total 1500

1-Feb-18 To balance b/d 1500

Abel Motors Ltd A/C

Date Particulars Debit Date Particulars Credit

12

Date Particulars Debit Date Particulars Credit

31-Jan-18 To Balance c/d

1093

0 3-Jan-18 By Receivables 8940

9-Jan-18 By Receivables 1990

Total

1093

0 Total 10930

1-Feb-18 By balance b/d 10930

Motor Expenses A/C

Date Particulars Debit Date Particulars Credit

4-Jan-18 To cash 470 31-Jan-18 By Balance c/d 470

Total 470 Total 470

1-Feb-18 To balance b/d 470

Van A/C

Date Particulars Debit Date Particulars Credit

14-Jan-

18

To Abel Motors

Limited

2850

0

31-Jan-

18

By Balance

c/d 79750

1-Feb-

18 To balance b/d

5125

0

Total

7975

0 Total 79750

Drawings A/C

Date Particulars Debit Date Particulars Credit

7-Jan-18 To Cash 1500 31-Jan-18 By Balance c/d 1500

Total 1500 Total 1500

1-Feb-18 To balance b/d 1500

Abel Motors Ltd A/C

Date Particulars Debit Date Particulars Credit

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.