Financial Accounting Principles: Client Cases and Analysis

VerifiedAdded on 2020/12/29

|38

|4119

|242

Homework Assignment

AI Summary

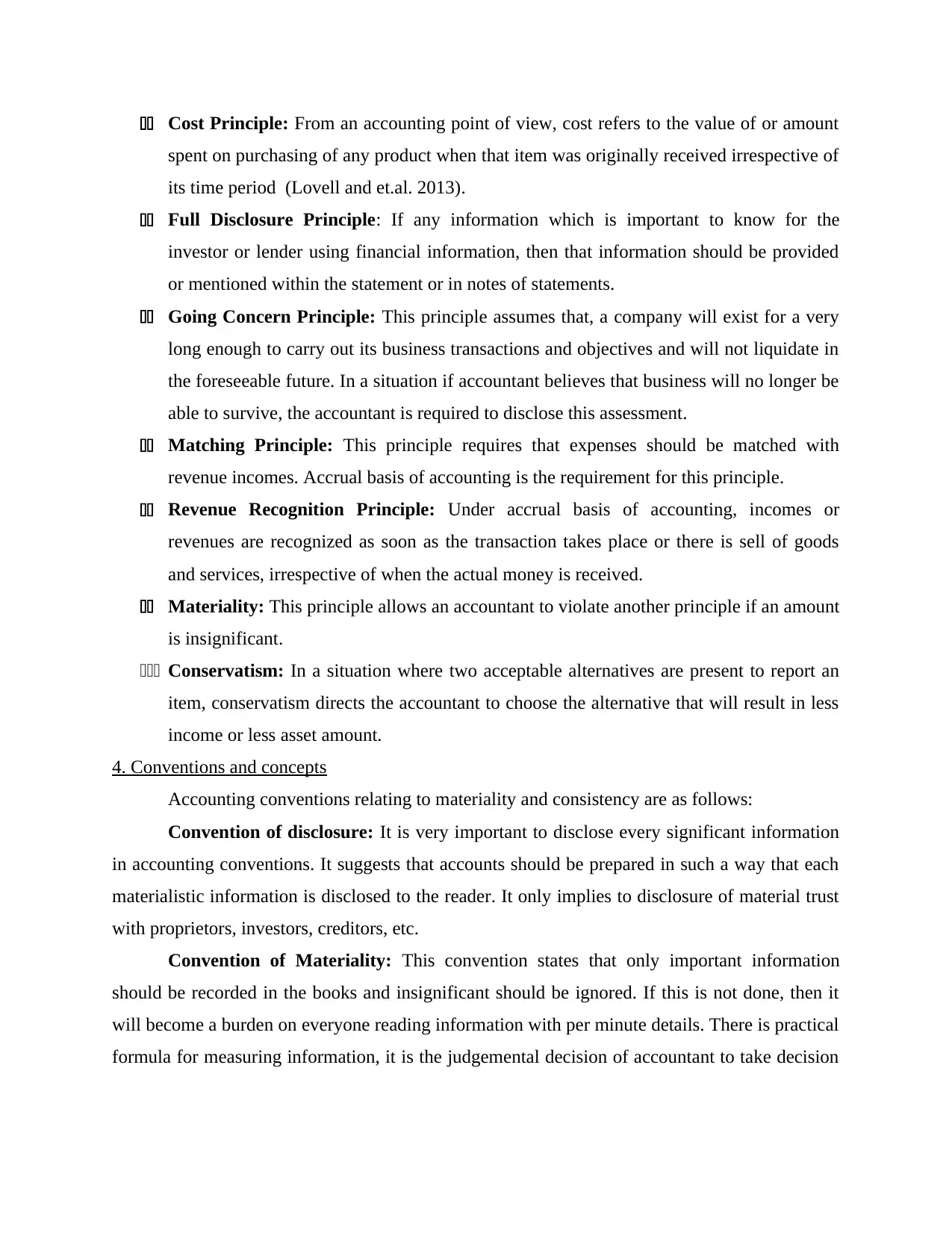

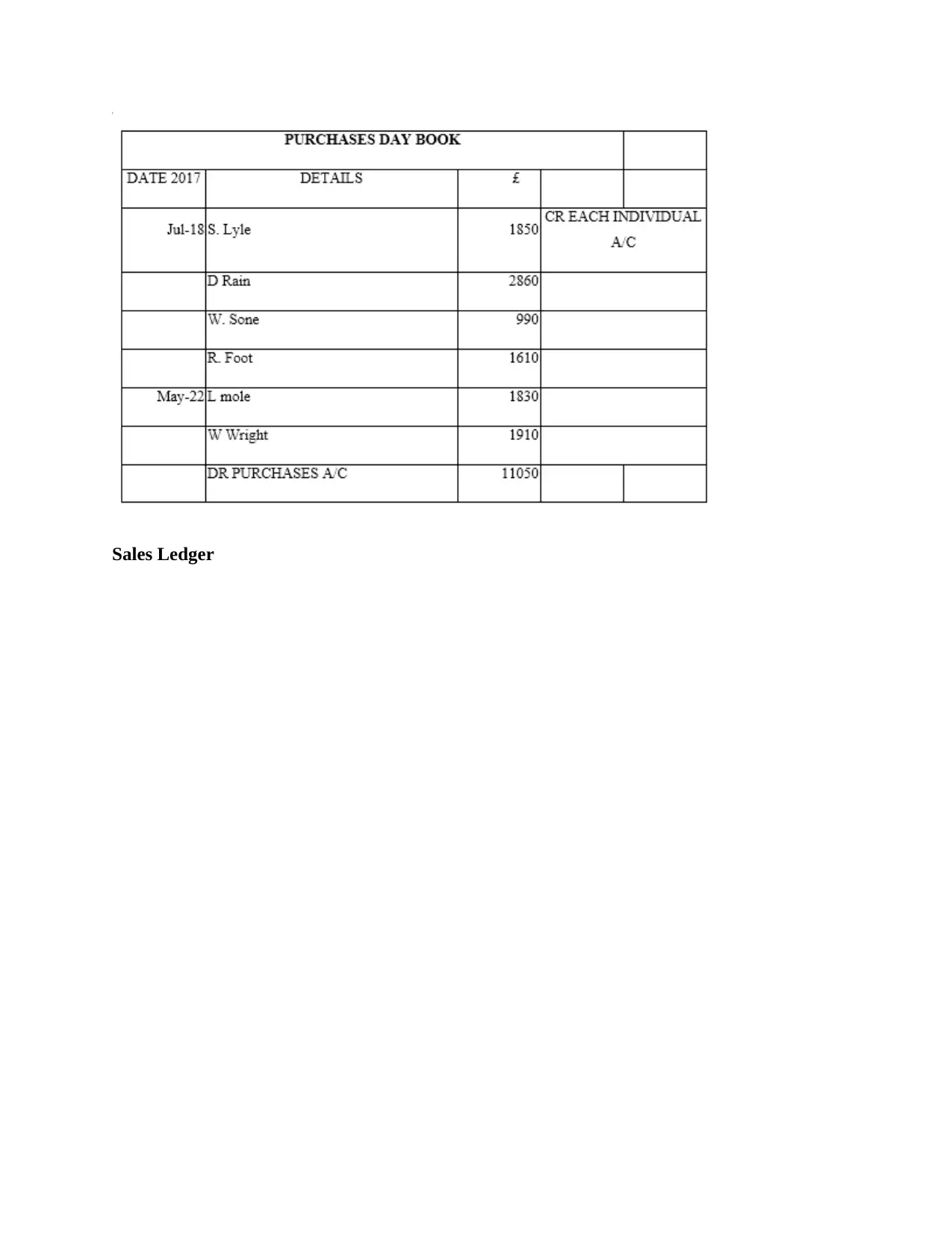

This comprehensive report delves into the core principles of financial accounting, providing a clear understanding of its purpose and regulatory framework, including GAAP, IFRS, and IASB. It explores fundamental accounting concepts, such as the economic entity, monetary unit, time period assumptions, and the cost principle, alongside conventions like disclosure, materiality, and consistency. The report presents practical applications through detailed examples and solutions for various client cases, covering journal entries, ledger accounts, income statements, statements of financial position, bank reconciliation, and depreciation methods. It also analyzes the significance of consistency and prudence in financial reporting, alongside the purpose and methods of depreciation. The report concludes with a discussion of suspense accounts and trial balance preparation, offering a complete guide to financial accounting practices.

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.