Financial Accounting Principles Assignment - Comprehensive Solution

VerifiedAdded on 2020/01/07

|37

|6580

|173

Homework Assignment

AI Summary

This assignment solution provides a comprehensive overview of financial accounting principles. It covers key concepts such as financial accounting regulations, accounting rules and principles, and conventions. The solution includes detailed examples and practical applications through various client scenarios. These scenarios involve the preparation of books of prime entry, double-entry recordings in ledgers, trial balances, statements of profit and loss, statements of financial position, bank reconciliation statements, sales and purchase ledger control accounts, and suspense accounts. The document also explains accounting concepts like consistency and prudence, and methods of depreciation. Furthermore, it includes journal entries for rectifying errors and clarifying the use of control accounts. The assignment aims to provide a thorough understanding of financial accounting and its practical applications.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................5

A. (i) Financial accounting...........................................................................................................5

A. (ii) Explain the regulation relating to financial accounting....................................................6

A. (iii). Describe accounting rules and principles........................................................................8

A. (iv) Explain the conventions and concepts relating to consistency and material disclosure...8

B. CLIENT 1...................................................................................................................................9

(i) Books of prime entry...............................................................................................................9

(ii) Complete double entry recording in ledgers........................................................................11

(iii) Trial balance to check arithmetical accuracy......................................................................25

CLIENT 2......................................................................................................................................26

(A). Preparation of Statement of profit and loss acount............................................................26

(B). Preparation of Statement of Financial Position..................................................................27

CLIENT 3......................................................................................................................................28

(A). Preparation of statement of profit & Loss..........................................................................28

(B). Preparation of statement of SOFP, balance sheet...............................................................29

(C). Explaining the consistency and prudence accounting concepts.........................................30

(D). Briefly presenting the aim of depreication and two depreciation methods........................30

CLIENT 4......................................................................................................................................31

(A). Explaining the purpose of bank reconcilation statement....................................................31

(B). Listing several areas which may vary Cash book (bank column) & pass book balances. .31

(C). (i) Preparation of bank reconcilation statements on 1st December 2016............................32

(ii). Preparation of Kendal Ltd’s updated cash book for December 2016.................................32

(iii) Preparation of bank reconcilations statement as at December 2016...................................32

CLIENT 5......................................................................................................................................33

INTRODUCTION...........................................................................................................................5

A. (i) Financial accounting...........................................................................................................5

A. (ii) Explain the regulation relating to financial accounting....................................................6

A. (iii). Describe accounting rules and principles........................................................................8

A. (iv) Explain the conventions and concepts relating to consistency and material disclosure...8

B. CLIENT 1...................................................................................................................................9

(i) Books of prime entry...............................................................................................................9

(ii) Complete double entry recording in ledgers........................................................................11

(iii) Trial balance to check arithmetical accuracy......................................................................25

CLIENT 2......................................................................................................................................26

(A). Preparation of Statement of profit and loss acount............................................................26

(B). Preparation of Statement of Financial Position..................................................................27

CLIENT 3......................................................................................................................................28

(A). Preparation of statement of profit & Loss..........................................................................28

(B). Preparation of statement of SOFP, balance sheet...............................................................29

(C). Explaining the consistency and prudence accounting concepts.........................................30

(D). Briefly presenting the aim of depreication and two depreciation methods........................30

CLIENT 4......................................................................................................................................31

(A). Explaining the purpose of bank reconcilation statement....................................................31

(B). Listing several areas which may vary Cash book (bank column) & pass book balances. .31

(C). (i) Preparation of bank reconcilation statements on 1st December 2016............................32

(ii). Preparation of Kendal Ltd’s updated cash book for December 2016.................................32

(iii) Preparation of bank reconcilations statement as at December 2016...................................32

CLIENT 5......................................................................................................................................33

(A). (i). Preparation of Sales Ledger Control Account..............................................................33

(A). (ii). Preparation of purchase Ledger Control Account.......................................................33

(B). Explaining the term “control Account” & its uses.............................................................34

CLIENT 6......................................................................................................................................34

(A). Describing the term “suspense account” & its main features.............................................34

(B) Drafting a trial balance........................................................................................................35

(C). Prepration of Journal entries to show corrections & clear the suspense account...............35

(D). Differentiate between Suspense account and Clearing Account........................................36

CONCLUSION..............................................................................................................................37

REFERENCES..............................................................................................................................37

(A). (ii). Preparation of purchase Ledger Control Account.......................................................33

(B). Explaining the term “control Account” & its uses.............................................................34

CLIENT 6......................................................................................................................................34

(A). Describing the term “suspense account” & its main features.............................................34

(B) Drafting a trial balance........................................................................................................35

(C). Prepration of Journal entries to show corrections & clear the suspense account...............35

(D). Differentiate between Suspense account and Clearing Account........................................36

CONCLUSION..............................................................................................................................37

REFERENCES..............................................................................................................................37

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

List of Tables

Table 1 Journal entry in Books of Alex for Month of May 2016...............................................................11

Table 2 Trial Balance of Alex...................................................................................................................25

Table 3 Statement of profit and loss acount of Peter Piper for the year ended 31st December 2016..........27

Table 4 Calculation of cost of goods sold..................................................................................................27

Table 5 Statement of financial position of Peter Piper as on 31st December 2016....................................27

Table 6 Statement of P&L of Raintree ltd for the year ended 30th September 2016.................................28

Table 7 Statement of SOFP of Raintree ltd as on 30th September 2016....................................................29

Table 8 Bank reconcilation statement of Kendal Ltd on 1st December 2016............................................32

Table 9 Kendal Ltd’s updated cash book for December 2016...................................................................32

Table 10 Bank reconcilations statement of Kendal Ltd as at December 2016...........................................32

Table 11 Sales Ledger control a/c of Henderson.......................................................................................33

Table 12 purchase Ledger Control Account of Henderson........................................................................33

Table 13 Trial balance...............................................................................................................................35

Table 14 Journal entries for rectifying errors.............................................................................................35

Table 15 Preparation of Suspense a/c........................................................................................................36

Table of Figures

Figure 1 Regulatory framework of financial accounting................................................................6

Figure 2 International standards of accounting..............................................................................7

Table 1 Journal entry in Books of Alex for Month of May 2016...............................................................11

Table 2 Trial Balance of Alex...................................................................................................................25

Table 3 Statement of profit and loss acount of Peter Piper for the year ended 31st December 2016..........27

Table 4 Calculation of cost of goods sold..................................................................................................27

Table 5 Statement of financial position of Peter Piper as on 31st December 2016....................................27

Table 6 Statement of P&L of Raintree ltd for the year ended 30th September 2016.................................28

Table 7 Statement of SOFP of Raintree ltd as on 30th September 2016....................................................29

Table 8 Bank reconcilation statement of Kendal Ltd on 1st December 2016............................................32

Table 9 Kendal Ltd’s updated cash book for December 2016...................................................................32

Table 10 Bank reconcilations statement of Kendal Ltd as at December 2016...........................................32

Table 11 Sales Ledger control a/c of Henderson.......................................................................................33

Table 12 purchase Ledger Control Account of Henderson........................................................................33

Table 13 Trial balance...............................................................................................................................35

Table 14 Journal entries for rectifying errors.............................................................................................35

Table 15 Preparation of Suspense a/c........................................................................................................36

Table of Figures

Figure 1 Regulatory framework of financial accounting................................................................6

Figure 2 International standards of accounting..............................................................................7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Businesses carry out number of transactions in a given reporting year, such activities held

during a year is recorded in a coherent and logical manner in the financial statements of the

enterprise. Financial Accounting (FA) is a process whereby accountant record the monetary

activities in the annual accounts, such as profit and loss statement, balance sheet and cash flow

statement to examine their return and financial health. It follows various concepts like accural,

double-entry, consistency, matching, monetary measurements and accounting standards i.e. UK

GAAP, IAS & IFRS. The current project mainly targeted at the preparation of various accounts

like P&L a/c, balance sheet, trial balance, rectification entries, control account & Bank

reconcilation statement (BRS) as well following the relevant accounting standards and

guidelines.

A. (i) Financial accounting

Financial accounting is the field of accounting that is concerned with the analysis,

examination, summarizing and reporting of the financial transactions conducted during the

business operations. It involves the construction of annual accounts, also called financial

statements i.e. statement of comprehensive income (SOCI), statement of financial position

(SOFP, balance/sheet), statement of cash flow (SOCF), statement of changes in retained earnings

along with the necessary notes representing the adopted accounting standards, conventions and

revenues and expendiure recognition principles (Deegan, 2013). The key aim behind the

financial accouting is to determine the net profitability and the financial status at te end of every

financial year. Such statements are created adopting accounting rules and standards such as UK

GAAP, IAS (International Accounting standards) & in the globalized era, multinational

companies publish their accounts in harmonized manner through following IFRS. Double entry

book-keeping system is followed by the establishments to prepare their accounts, wherein every

accounting activity is recorded in both the sides, credit and debit. It is essential to prepare

accounts because without arranging a proper record of the monetary activities held in the daily

operations, enterprise cannot examine their financial position i.e. solvency and liquidity as well

as organizational performance (Pratt, 2013). It not only helps the internal stakeholders such as

managers and employees but also assists outsiders such as government, shareholders, lenders,

Businesses carry out number of transactions in a given reporting year, such activities held

during a year is recorded in a coherent and logical manner in the financial statements of the

enterprise. Financial Accounting (FA) is a process whereby accountant record the monetary

activities in the annual accounts, such as profit and loss statement, balance sheet and cash flow

statement to examine their return and financial health. It follows various concepts like accural,

double-entry, consistency, matching, monetary measurements and accounting standards i.e. UK

GAAP, IAS & IFRS. The current project mainly targeted at the preparation of various accounts

like P&L a/c, balance sheet, trial balance, rectification entries, control account & Bank

reconcilation statement (BRS) as well following the relevant accounting standards and

guidelines.

A. (i) Financial accounting

Financial accounting is the field of accounting that is concerned with the analysis,

examination, summarizing and reporting of the financial transactions conducted during the

business operations. It involves the construction of annual accounts, also called financial

statements i.e. statement of comprehensive income (SOCI), statement of financial position

(SOFP, balance/sheet), statement of cash flow (SOCF), statement of changes in retained earnings

along with the necessary notes representing the adopted accounting standards, conventions and

revenues and expendiure recognition principles (Deegan, 2013). The key aim behind the

financial accouting is to determine the net profitability and the financial status at te end of every

financial year. Such statements are created adopting accounting rules and standards such as UK

GAAP, IAS (International Accounting standards) & in the globalized era, multinational

companies publish their accounts in harmonized manner through following IFRS. Double entry

book-keeping system is followed by the establishments to prepare their accounts, wherein every

accounting activity is recorded in both the sides, credit and debit. It is essential to prepare

accounts because without arranging a proper record of the monetary activities held in the daily

operations, enterprise cannot examine their financial position i.e. solvency and liquidity as well

as organizational performance (Pratt, 2013). It not only helps the internal stakeholders such as

managers and employees but also assists outsiders such as government, shareholders, lenders,

creditors and other regulatory authority to gather required information for the rationalized

decision-making purpose. In UK, as per the Company Act, 2006, all the private as well as public

limited organizations are legally required to report their financial transactions in annual accounts

and publish it to communicate external users.

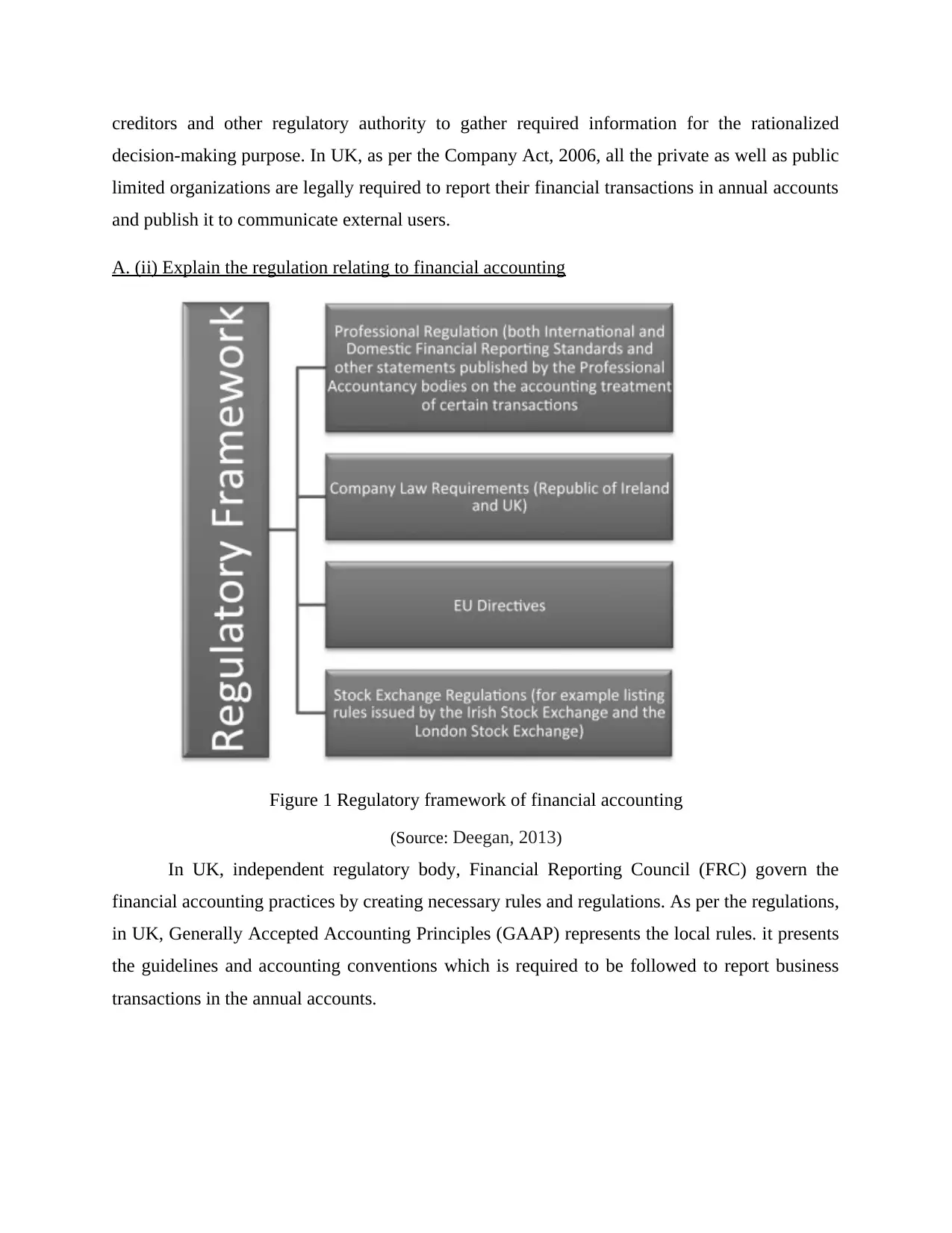

A. (ii) Explain the regulation relating to financial accounting

Figure 1 Regulatory framework of financial accounting

(Source: Deegan, 2013)

In UK, independent regulatory body, Financial Reporting Council (FRC) govern the

financial accounting practices by creating necessary rules and regulations. As per the regulations,

in UK, Generally Accepted Accounting Principles (GAAP) represents the local rules. it presents

the guidelines and accounting conventions which is required to be followed to report business

transactions in the annual accounts.

decision-making purpose. In UK, as per the Company Act, 2006, all the private as well as public

limited organizations are legally required to report their financial transactions in annual accounts

and publish it to communicate external users.

A. (ii) Explain the regulation relating to financial accounting

Figure 1 Regulatory framework of financial accounting

(Source: Deegan, 2013)

In UK, independent regulatory body, Financial Reporting Council (FRC) govern the

financial accounting practices by creating necessary rules and regulations. As per the regulations,

in UK, Generally Accepted Accounting Principles (GAAP) represents the local rules. it presents

the guidelines and accounting conventions which is required to be followed to report business

transactions in the annual accounts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

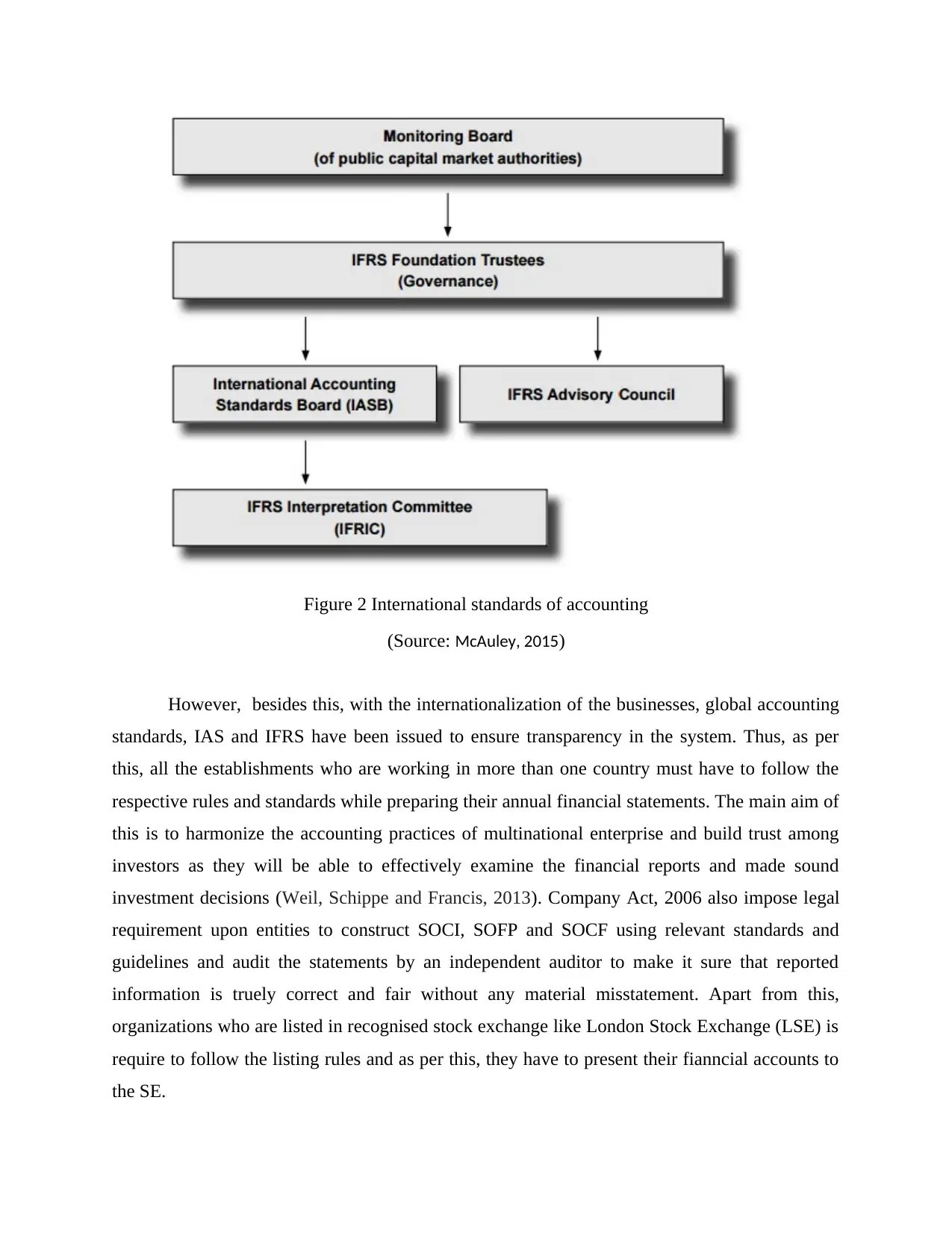

Figure 2 International standards of accounting

(Source: McAuley, 2015)

However, besides this, with the internationalization of the businesses, global accounting

standards, IAS and IFRS have been issued to ensure transparency in the system. Thus, as per

this, all the establishments who are working in more than one country must have to follow the

respective rules and standards while preparing their annual financial statements. The main aim of

this is to harmonize the accounting practices of multinational enterprise and build trust among

investors as they will be able to effectively examine the financial reports and made sound

investment decisions (Weil, Schippe and Francis, 2013). Company Act, 2006 also impose legal

requirement upon entities to construct SOCI, SOFP and SOCF using relevant standards and

guidelines and audit the statements by an independent auditor to make it sure that reported

information is truely correct and fair without any material misstatement. Apart from this,

organizations who are listed in recognised stock exchange like London Stock Exchange (LSE) is

require to follow the listing rules and as per this, they have to present their fianncial accounts to

the SE.

(Source: McAuley, 2015)

However, besides this, with the internationalization of the businesses, global accounting

standards, IAS and IFRS have been issued to ensure transparency in the system. Thus, as per

this, all the establishments who are working in more than one country must have to follow the

respective rules and standards while preparing their annual financial statements. The main aim of

this is to harmonize the accounting practices of multinational enterprise and build trust among

investors as they will be able to effectively examine the financial reports and made sound

investment decisions (Weil, Schippe and Francis, 2013). Company Act, 2006 also impose legal

requirement upon entities to construct SOCI, SOFP and SOCF using relevant standards and

guidelines and audit the statements by an independent auditor to make it sure that reported

information is truely correct and fair without any material misstatement. Apart from this,

organizations who are listed in recognised stock exchange like London Stock Exchange (LSE) is

require to follow the listing rules and as per this, they have to present their fianncial accounts to

the SE.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A. (iii). Describe accounting rules and principles

As said earlier that UK GAAP presents the conventions, principles and accounting rules

to guide accountatnts how the regular transactions will be reported in their financial statements.

The necessary rules and principles concerned with the accounting are mentioned here as follows:

Accural concept: This principles states that in the annual reports, transactions will be

record at the time of their occurence. There will be no effect of its cash generation or expenditure

occurence on the financial reporting. In other words, activities will be recorded when they held

irregardless of whether cash is received/paid or not (Saunders and Cornett, 2014).

Going concern: It assumes that business will continue its functions for long duration to

complete its committments and there is no probability of its liquidiation in foreseeable future.

This accounting principle allow the enterprise to defer several transactions like prepaid expense

and also amortize depreciation and others over a given period (Jollands and Quinn, 2017).

Matching principle: It matches the expenses incurred with the revenues because of

double-entry book keeping and accural accounting basis. For instance, sales commission must be

recorded at the time of sales instead of when the commission is actually paid to sales personnel.

Full disclosure: Corporations must record each and every information in their accounts

which are important for the stakeholders like lenders and investors in any way. Moreover, notes

also must be shown disclosing all the relevant principles and standards in footnotes to final

accounts, so that, investors can make better decisions (Gregory, Uys and Gregory, 2014).

Disclosing all the material statements or information is necessary otherwise, default person will

be penalised by fine and other lawsuit.

Monetary principle: In the financial statements, only those transactions are reported that

can be measured in monetary terms, GBP. Thus, it only provide quantitative results i.e. sales, and

cost and do not disclose any qualitative results and performance i.e. environmental performance

and others.

A. (iv) Explain the conventions and concepts relating to consistency and material disclosure

Accounting concepts postulates necessary assumptions upon which the entire accounting

and reporting is based. However, conventions represents customs that enable accountant to deal

with the practical accounting issue and problems. The consistency and material disclosure

concepts & conceptions are analyzed here as under:

As said earlier that UK GAAP presents the conventions, principles and accounting rules

to guide accountatnts how the regular transactions will be reported in their financial statements.

The necessary rules and principles concerned with the accounting are mentioned here as follows:

Accural concept: This principles states that in the annual reports, transactions will be

record at the time of their occurence. There will be no effect of its cash generation or expenditure

occurence on the financial reporting. In other words, activities will be recorded when they held

irregardless of whether cash is received/paid or not (Saunders and Cornett, 2014).

Going concern: It assumes that business will continue its functions for long duration to

complete its committments and there is no probability of its liquidiation in foreseeable future.

This accounting principle allow the enterprise to defer several transactions like prepaid expense

and also amortize depreciation and others over a given period (Jollands and Quinn, 2017).

Matching principle: It matches the expenses incurred with the revenues because of

double-entry book keeping and accural accounting basis. For instance, sales commission must be

recorded at the time of sales instead of when the commission is actually paid to sales personnel.

Full disclosure: Corporations must record each and every information in their accounts

which are important for the stakeholders like lenders and investors in any way. Moreover, notes

also must be shown disclosing all the relevant principles and standards in footnotes to final

accounts, so that, investors can make better decisions (Gregory, Uys and Gregory, 2014).

Disclosing all the material statements or information is necessary otherwise, default person will

be penalised by fine and other lawsuit.

Monetary principle: In the financial statements, only those transactions are reported that

can be measured in monetary terms, GBP. Thus, it only provide quantitative results i.e. sales, and

cost and do not disclose any qualitative results and performance i.e. environmental performance

and others.

A. (iv) Explain the conventions and concepts relating to consistency and material disclosure

Accounting concepts postulates necessary assumptions upon which the entire accounting

and reporting is based. However, conventions represents customs that enable accountant to deal

with the practical accounting issue and problems. The consistency and material disclosure

concepts & conceptions are analyzed here as under:

Consistency: This principle state that the adopted accounting principles and methods will

be followed continually over the different finacial years untill and unless there is a sound reason

to use other standards and principles that will bring improvement in the current reporting system

(Giles, 2014). The most important benefit of this standard is it helps to compare performance

over the years.

Material disclosure: Accountants are allowed to exclude those items that are

insignificant, in this regards, whether an amount is material or immaterial will be decided on the

basis of professional judgement (Beatty and Liao, 2014). For instance, if a multinational entity

buys a printer costing 150GBP, as per the matching principle, it will be expensed over 5 year.

However, materiality principle here allows the accounatnt to violate the matching accounting

principle and charge thee entire cost in the same year instead of 5 year.

B. CLIENT 1

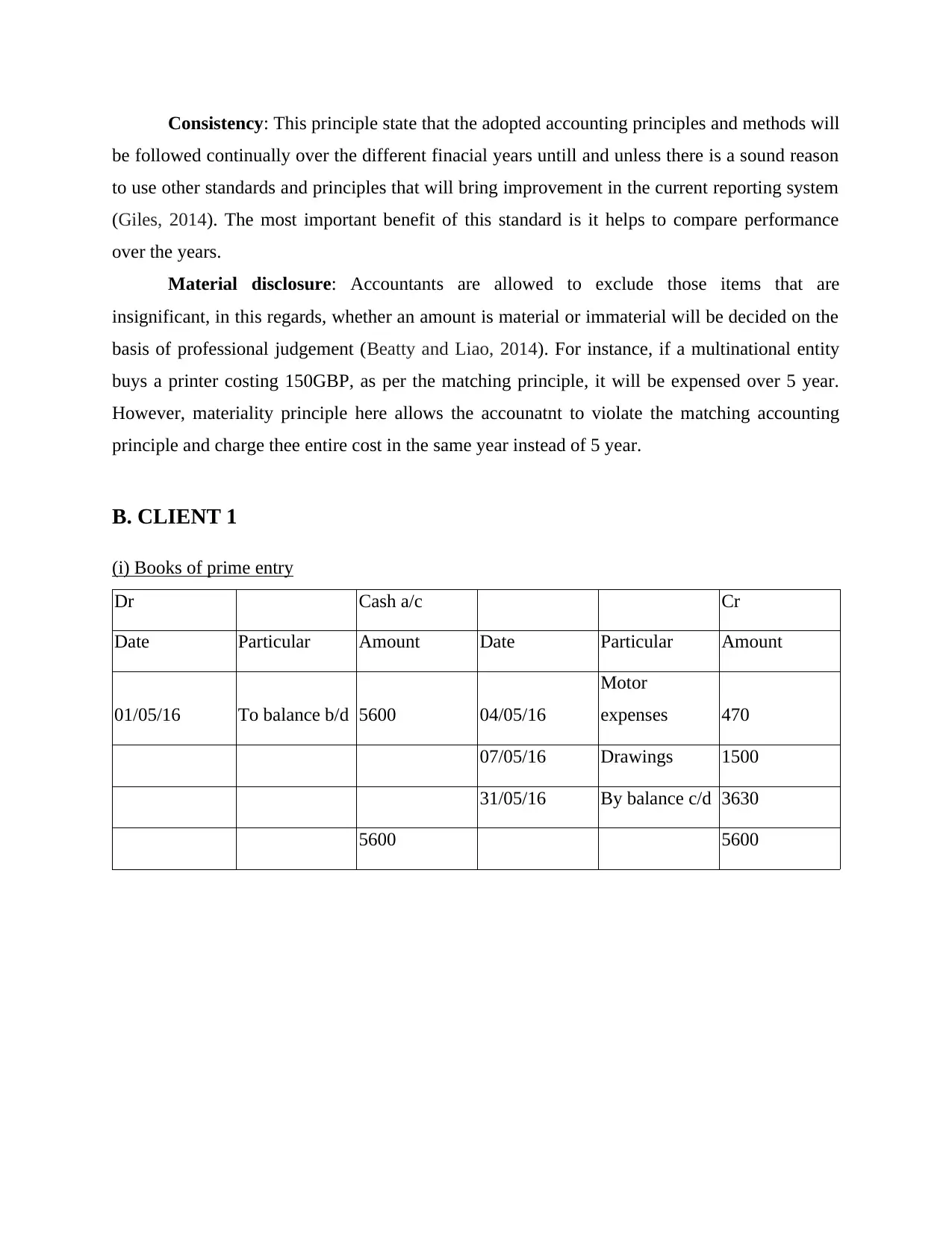

(i) Books of prime entry

Dr Cash a/c Cr

Date Particular Amount Date Particular Amount

01/05/16 To balance b/d 5600 04/05/16

Motor

expenses 470

07/05/16 Drawings 1500

31/05/16 By balance c/d 3630

5600 5600

be followed continually over the different finacial years untill and unless there is a sound reason

to use other standards and principles that will bring improvement in the current reporting system

(Giles, 2014). The most important benefit of this standard is it helps to compare performance

over the years.

Material disclosure: Accountants are allowed to exclude those items that are

insignificant, in this regards, whether an amount is material or immaterial will be decided on the

basis of professional judgement (Beatty and Liao, 2014). For instance, if a multinational entity

buys a printer costing 150GBP, as per the matching principle, it will be expensed over 5 year.

However, materiality principle here allows the accounatnt to violate the matching accounting

principle and charge thee entire cost in the same year instead of 5 year.

B. CLIENT 1

(i) Books of prime entry

Dr Cash a/c Cr

Date Particular Amount Date Particular Amount

01/05/16 To balance b/d 5600 04/05/16

Motor

expenses 470

07/05/16 Drawings 1500

31/05/16 By balance c/d 3630

5600 5600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

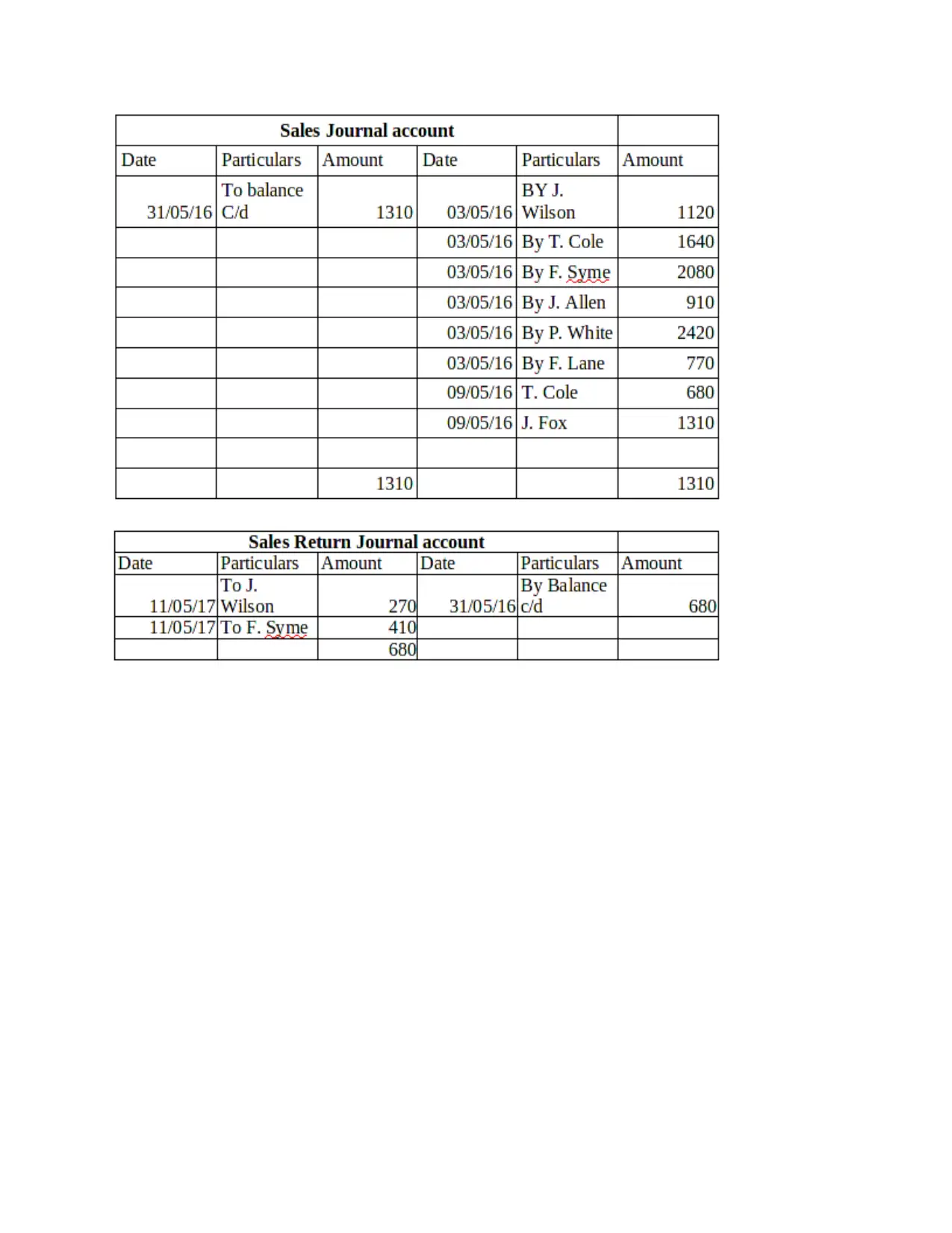

Prime book entries shows the daily routine expenditures or income incurred in an entity

as this gives the actual expenses and income to be incurred in the business in a particular

financial year. Role of an entity gets increases when they prepare this compulsory kind of books

as this shows the overall performance of an entity within a given span of time (Beatty and Liao,

2014). The primary book entry includes sale ledger that records each and every sales in an entity

along with the purchases made by the firm. All these expenditures are managed with the help of

cash that maintains liquidity in the business in order to meet all kinds of problems imposed on an

entity.

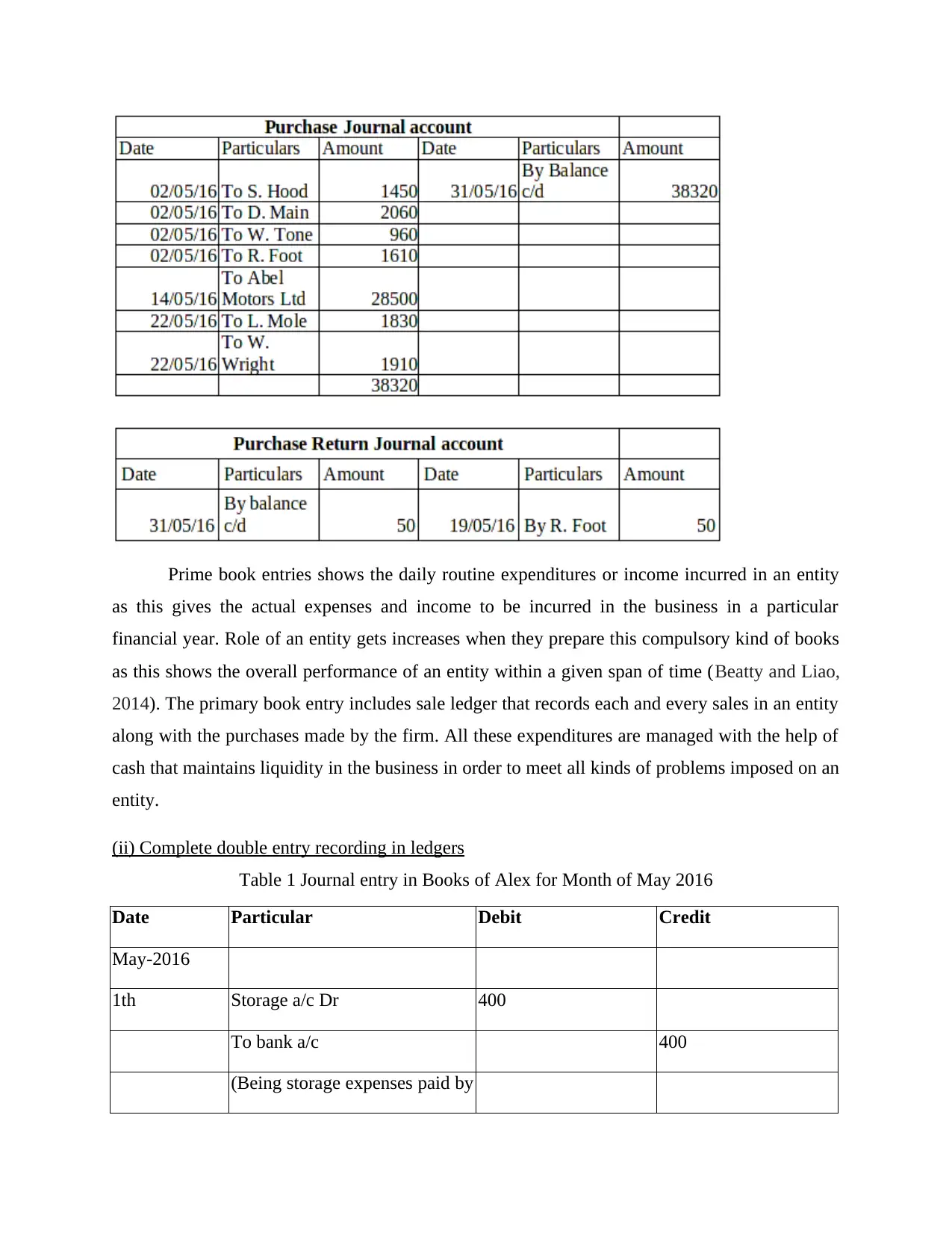

(ii) Complete double entry recording in ledgers

Table 1 Journal entry in Books of Alex for Month of May 2016

Date Particular Debit Credit

May-2016

1th Storage a/c Dr 400

To bank a/c 400

(Being storage expenses paid by

as this gives the actual expenses and income to be incurred in the business in a particular

financial year. Role of an entity gets increases when they prepare this compulsory kind of books

as this shows the overall performance of an entity within a given span of time (Beatty and Liao,

2014). The primary book entry includes sale ledger that records each and every sales in an entity

along with the purchases made by the firm. All these expenditures are managed with the help of

cash that maintains liquidity in the business in order to meet all kinds of problems imposed on an

entity.

(ii) Complete double entry recording in ledgers

Table 1 Journal entry in Books of Alex for Month of May 2016

Date Particular Debit Credit

May-2016

1th Storage a/c Dr 400

To bank a/c 400

(Being storage expenses paid by

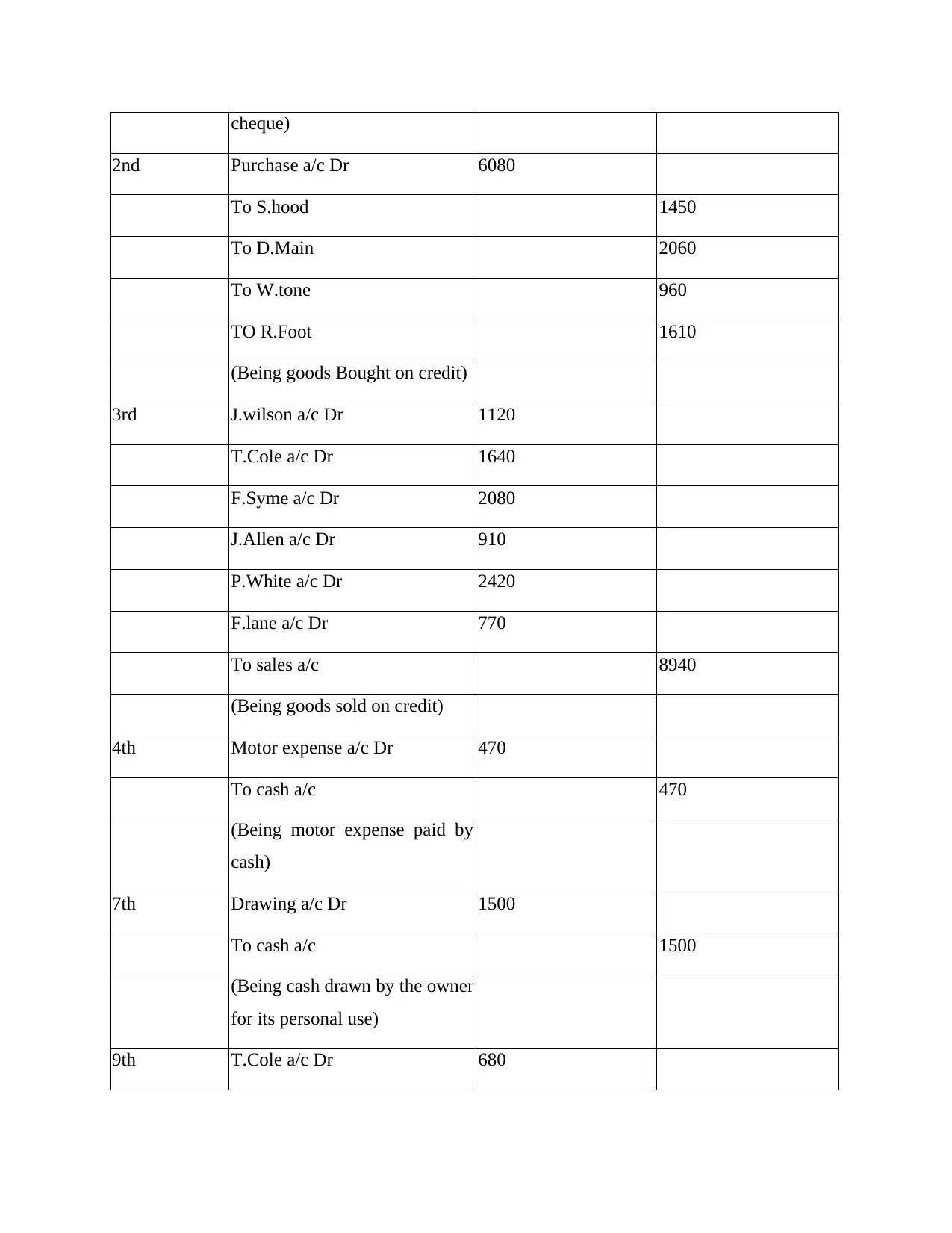

cheque)

2nd Purchase a/c Dr 6080

To S.hood 1450

To D.Main 2060

To W.tone 960

TO R.Foot 1610

(Being goods Bought on credit)

3rd J.wilson a/c Dr 1120

T.Cole a/c Dr 1640

F.Syme a/c Dr 2080

J.Allen a/c Dr 910

P.White a/c Dr 2420

F.lane a/c Dr 770

To sales a/c 8940

(Being goods sold on credit)

4th Motor expense a/c Dr 470

To cash a/c 470

(Being motor expense paid by

cash)

7th Drawing a/c Dr 1500

To cash a/c 1500

(Being cash drawn by the owner

for its personal use)

9th T.Cole a/c Dr 680

2nd Purchase a/c Dr 6080

To S.hood 1450

To D.Main 2060

To W.tone 960

TO R.Foot 1610

(Being goods Bought on credit)

3rd J.wilson a/c Dr 1120

T.Cole a/c Dr 1640

F.Syme a/c Dr 2080

J.Allen a/c Dr 910

P.White a/c Dr 2420

F.lane a/c Dr 770

To sales a/c 8940

(Being goods sold on credit)

4th Motor expense a/c Dr 470

To cash a/c 470

(Being motor expense paid by

cash)

7th Drawing a/c Dr 1500

To cash a/c 1500

(Being cash drawn by the owner

for its personal use)

9th T.Cole a/c Dr 680

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 37

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.