Financial Accounting Principles Report - Practical Applications

VerifiedAdded on 2021/01/02

|41

|5398

|84

Report

AI Summary

This report offers a comprehensive exploration of financial accounting principles, encompassing key concepts and practical applications. It begins with an introduction to financial accounting, its purpose, and the regulations that govern it, including GAAP, IFRS, and IASB. The report then delves into accounting rules and principles, such as the economic entity assumption, monetary unit assumption, and the matching principle. Conventions like materiality and consistency are also discussed. The core of the report involves practical examples and case studies, including drafting journal entries, double-entry recordings with ledgers, and trial balances. The report then proceeds to the preparation of financial statements, including profit and loss accounts and statements of financial position for various clients. Furthermore, it addresses bank reconciliation statements, control accounts, and depreciation methods. The report concludes with a discussion of the consistency and prudence concepts, and the purpose of depreciation in framing accounting statements, providing a well-rounded understanding of financial accounting principles and their real-world application.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A.1 Financial accounting and its purpose...................................................................................1

A.2 Regulations relating to financial accounting........................................................................2

A.3 Accounting rules and principles...........................................................................................3

A.4 Conventions and concepts relating to consistency and material disclosure.........................4

CLIENT 1........................................................................................................................................4

1. Drafting journal entries...........................................................................................................4

2. Drafting double entry recording with context of ledger..........................................................6

3. Drafting accuracy level with context of trial balance...........................................................22

CLIENT 2......................................................................................................................................23

A. Drafting Statement of Profit and Loss account (Sierra Laurent).........................................23

B. Drafting Statement of Financial Position (Sierra Laurent)...................................................24

CLIENT 3......................................................................................................................................26

A. Drafting statement of Profit and loss statement of LMS Limited........................................26

B. Drafting Statement of Financial position of LMS Limited..................................................27

C. Drafting concept of Consistence and Prudence....................................................................27

D. Drafting purpose of depreciation for framing accounting statements along with its two

methods.....................................................................................................................................28

CLIENT 4......................................................................................................................................29

A. Drafting objective of preparing Bank Reconciliation Statement.........................................29

B. Drafting areas which creates variations in transaction from bank records...........................29

C.1 Draft Kendal's Cash-book as per July 2018.......................................................................30

C.2 Drafting Bank Reconciliation statement as per July 2018.................................................31

CLIENT 5......................................................................................................................................31

A.1 Draft Sales ledger control account for Henderson for year 2018 (July)............................31

A.2 Draft Purchase ledger control account for Henderson for year 2018 (July)......................32

B. Draft the definition of control account.................................................................................32

CLIENT 6......................................................................................................................................33

A. Suspense Account................................................................................................................33

B and C Draft trial balance........................................................................................................34

D Draft comparison between clearing and suspense account...................................................35

CONCLUSION..............................................................................................................................37

REFERENCES..............................................................................................................................38

INTRODUCTION...........................................................................................................................1

A.1 Financial accounting and its purpose...................................................................................1

A.2 Regulations relating to financial accounting........................................................................2

A.3 Accounting rules and principles...........................................................................................3

A.4 Conventions and concepts relating to consistency and material disclosure.........................4

CLIENT 1........................................................................................................................................4

1. Drafting journal entries...........................................................................................................4

2. Drafting double entry recording with context of ledger..........................................................6

3. Drafting accuracy level with context of trial balance...........................................................22

CLIENT 2......................................................................................................................................23

A. Drafting Statement of Profit and Loss account (Sierra Laurent).........................................23

B. Drafting Statement of Financial Position (Sierra Laurent)...................................................24

CLIENT 3......................................................................................................................................26

A. Drafting statement of Profit and loss statement of LMS Limited........................................26

B. Drafting Statement of Financial position of LMS Limited..................................................27

C. Drafting concept of Consistence and Prudence....................................................................27

D. Drafting purpose of depreciation for framing accounting statements along with its two

methods.....................................................................................................................................28

CLIENT 4......................................................................................................................................29

A. Drafting objective of preparing Bank Reconciliation Statement.........................................29

B. Drafting areas which creates variations in transaction from bank records...........................29

C.1 Draft Kendal's Cash-book as per July 2018.......................................................................30

C.2 Drafting Bank Reconciliation statement as per July 2018.................................................31

CLIENT 5......................................................................................................................................31

A.1 Draft Sales ledger control account for Henderson for year 2018 (July)............................31

A.2 Draft Purchase ledger control account for Henderson for year 2018 (July)......................32

B. Draft the definition of control account.................................................................................32

CLIENT 6......................................................................................................................................33

A. Suspense Account................................................................................................................33

B and C Draft trial balance........................................................................................................34

D Draft comparison between clearing and suspense account...................................................35

CONCLUSION..............................................................................................................................37

REFERENCES..............................................................................................................................38

INTRODUCTION

Financial Accounting is a field which is concerned about summarising, recording and

analysing fiscal transactions which occur daily in an organization. This present report file is a

brief study of principles of financial accounting with solved practical examples denoting

operations of its fiscal statements. In this project report guidelines and regulations that govern

financial accounting in UK are explained briefly, like GAAP, IFRS, IASB. Moreover, this

assignment gives a brief study of accounting rules and principle that needs to be considered

while recording transactions in accountancy books. Further, a mini- research is conducted to

describe purpose of financial accounting to determine objectives and needs for maintaining its

books. Conventions and concepts relating to materiality and consistency are also highlighted

carefully. In addition to this, double entry recording would be drafted in context with ledger.

A.1 Financial accounting and its purpose

Financial Accounting is the base of accountancy in any organisation concerned about

summary, analysis, and recording of fiscal transactions of that business. This process of

recording of financial transactions involves preparation of fiscal statements, which are available

for public consumption (Renz, 2016). It is governed by both local and international accounting

standards, like GAAP, IFRS and IASB. It is used to show financial situation of company to any

outsider or the one who is interested in daily functioning of business. Most basic accounting

principle is "The Measuring Unit principle". Knowing the purpose of financial accounting make

differences between just being a bean-counter and really knowing what business in doing. So,

some objectives or purpose of financial that every business should know are as follows:

Relevance: The information provided should be relevant to be useful for users.

Moreover, it should help the statement readers to make decisions about the financial

wellness of an organization. To satisfy this objective, any company reports its financial

results either quarterly or annually.

Reliability: Any organization should provide investors with reliable information of

financial statements in order to enable them to gain understanding of fiscal position of

company to make any decision. Any reliable information is free from biases, misleading

and should be verified.

1

Financial Accounting is a field which is concerned about summarising, recording and

analysing fiscal transactions which occur daily in an organization. This present report file is a

brief study of principles of financial accounting with solved practical examples denoting

operations of its fiscal statements. In this project report guidelines and regulations that govern

financial accounting in UK are explained briefly, like GAAP, IFRS, IASB. Moreover, this

assignment gives a brief study of accounting rules and principle that needs to be considered

while recording transactions in accountancy books. Further, a mini- research is conducted to

describe purpose of financial accounting to determine objectives and needs for maintaining its

books. Conventions and concepts relating to materiality and consistency are also highlighted

carefully. In addition to this, double entry recording would be drafted in context with ledger.

A.1 Financial accounting and its purpose

Financial Accounting is the base of accountancy in any organisation concerned about

summary, analysis, and recording of fiscal transactions of that business. This process of

recording of financial transactions involves preparation of fiscal statements, which are available

for public consumption (Renz, 2016). It is governed by both local and international accounting

standards, like GAAP, IFRS and IASB. It is used to show financial situation of company to any

outsider or the one who is interested in daily functioning of business. Most basic accounting

principle is "The Measuring Unit principle". Knowing the purpose of financial accounting make

differences between just being a bean-counter and really knowing what business in doing. So,

some objectives or purpose of financial that every business should know are as follows:

Relevance: The information provided should be relevant to be useful for users.

Moreover, it should help the statement readers to make decisions about the financial

wellness of an organization. To satisfy this objective, any company reports its financial

results either quarterly or annually.

Reliability: Any organization should provide investors with reliable information of

financial statements in order to enable them to gain understanding of fiscal position of

company to make any decision. Any reliable information is free from biases, misleading

and should be verified.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Comparability: There is an established system of recording transactions and reporting

accounting information in order to verify comparability. It benefits and helps investors to

make judgemental decisions about their investment opportunities.

Consistency: It is a secondary quality of financial information because users are mostly

provided with financial information that spans various periods of time. As everything like

standards, business changes, it is not possible every time to have consistent information.

A.2 Regulations relating to financial accounting

Financial accounting of UK is governed and regulated by GAAP, IFRS, IASB. Following

is a brief study of these regulations:

GAAP (Generally Accepted Accounting Principles): It is a collection or set of

commonly followed and used accounting rules and standards for reporting any financial

transaction. These regulations are followed to ensure consistency and transparency of

financial reporting from one organization to another. GAAP is not universal it differs

from one country to another or from one geographic location to another. It should be

followed while distributing financial statements outside a company. Financial Accounting

Standards Board regulates GAAP for the state government and local government (Petty

and et. al., 2015). It also includes signified amount of accounting guidance, which is

often issued to explain accounting convections used by specialised industries. These are

termed as Statements of Recommended Practice and in addition to that ASB issues

Urgent Task Force Statements.

IFRS (International Financial Reporting Standards): It is a collection or set of

accounting standards which states how a particular transaction and other financial events

should be reported in financial statements. IFRS are issued by IASB to specify exactly

how accounts of a company are to be maintained and reported. It ensures common

language so that business and accounts could be understood from one company and

country to another.

IASB (International Accounting Standards Board): These are older accounting

standards which were replaced by 2001 by IFRS. Earlier it had fifteen members around

the world then the number extended to sixteen (Morden, 2016). IASB has full control

over developing and setting up of its own agenda, IFRS considers this agenda but don’t

have power to determine it. It aims to establish a thorough due process; engagement of

2

accounting information in order to verify comparability. It benefits and helps investors to

make judgemental decisions about their investment opportunities.

Consistency: It is a secondary quality of financial information because users are mostly

provided with financial information that spans various periods of time. As everything like

standards, business changes, it is not possible every time to have consistent information.

A.2 Regulations relating to financial accounting

Financial accounting of UK is governed and regulated by GAAP, IFRS, IASB. Following

is a brief study of these regulations:

GAAP (Generally Accepted Accounting Principles): It is a collection or set of

commonly followed and used accounting rules and standards for reporting any financial

transaction. These regulations are followed to ensure consistency and transparency of

financial reporting from one organization to another. GAAP is not universal it differs

from one country to another or from one geographic location to another. It should be

followed while distributing financial statements outside a company. Financial Accounting

Standards Board regulates GAAP for the state government and local government (Petty

and et. al., 2015). It also includes signified amount of accounting guidance, which is

often issued to explain accounting convections used by specialised industries. These are

termed as Statements of Recommended Practice and in addition to that ASB issues

Urgent Task Force Statements.

IFRS (International Financial Reporting Standards): It is a collection or set of

accounting standards which states how a particular transaction and other financial events

should be reported in financial statements. IFRS are issued by IASB to specify exactly

how accounts of a company are to be maintained and reported. It ensures common

language so that business and accounts could be understood from one company and

country to another.

IASB (International Accounting Standards Board): These are older accounting

standards which were replaced by 2001 by IFRS. Earlier it had fifteen members around

the world then the number extended to sixteen (Morden, 2016). IASB has full control

over developing and setting up of its own agenda, IFRS considers this agenda but don’t

have power to determine it. It aims to establish a thorough due process; engagement of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investors, regulators at every stage of the process and collaborative efforts with world-

wide standard setting community.

A.3 Accounting rules and principles

General rules and concepts that governs the field of accounting are referred to as

principles and guidelines. Following is a list of 10 main accounting principles and guidelines:

Economic Entity Assumption: This principle states that all the business transactions

should be kept aside or separate from the business owner's personal transactions. As sole

proprietor and business are considered as two separate entities for the purpose of

accounting (Zeff, 2016).

Monetary Unit Assumption: According to basic accounting principle, it is assumed that

the purchasing power of any currency is not changed over time. Hence, effects of

inflation should be avoided on recorded amounts.

Time Period Assumption: This principle assumes that it is possible to report complex

and ongoing activities of a business in relatively short intervals to determine more likely

need for the accountant to estimate amounts relevant to that period.

Cost Principle: This accounting principle does not allow assets to be adjusted upward

for inflation.

Full disclosure Principle: This principle states that every information should be

disclosed within the statement in order to facilitate investors with honesty and loyalty.

Going Concern Principle: This accounting principle assumes that a company will exist

long enough to carry out its objectives and commitment and will not get liquidated in

future.

Matching Principle: This principle requires that expenses should be matched with

revenues.

Revenue Recognition Principle: This principle guides accountant to record all cash

basis accounting as soon as product has been sold or a service is given irrespective of

when money is actually received.

Materiality: This accounting principle give rights to accountant to violate another

accounting principle in case of insignificant amount (Schaltegger and Burritt, 2017).

3

wide standard setting community.

A.3 Accounting rules and principles

General rules and concepts that governs the field of accounting are referred to as

principles and guidelines. Following is a list of 10 main accounting principles and guidelines:

Economic Entity Assumption: This principle states that all the business transactions

should be kept aside or separate from the business owner's personal transactions. As sole

proprietor and business are considered as two separate entities for the purpose of

accounting (Zeff, 2016).

Monetary Unit Assumption: According to basic accounting principle, it is assumed that

the purchasing power of any currency is not changed over time. Hence, effects of

inflation should be avoided on recorded amounts.

Time Period Assumption: This principle assumes that it is possible to report complex

and ongoing activities of a business in relatively short intervals to determine more likely

need for the accountant to estimate amounts relevant to that period.

Cost Principle: This accounting principle does not allow assets to be adjusted upward

for inflation.

Full disclosure Principle: This principle states that every information should be

disclosed within the statement in order to facilitate investors with honesty and loyalty.

Going Concern Principle: This accounting principle assumes that a company will exist

long enough to carry out its objectives and commitment and will not get liquidated in

future.

Matching Principle: This principle requires that expenses should be matched with

revenues.

Revenue Recognition Principle: This principle guides accountant to record all cash

basis accounting as soon as product has been sold or a service is given irrespective of

when money is actually received.

Materiality: This accounting principle give rights to accountant to violate another

accounting principle in case of insignificant amount (Schaltegger and Burritt, 2017).

3

Conservatism: This allows accountant to choose the alternative that will result in less net

income or less asset amount. It happens in a situation where there are two acceptable

alternatives for reporting any transaction.

A.4 Conventions and concepts relating to consistency and material disclosure

Materiality Concept: This concept ensures disclosure of all materials from which

decisions of the user of financial statement may affect. It is defined as the characteristics

attaching to a statement, fact or item where its disclosure can influence judgement of a

reasonable person. So, if the event is material it should be disclosed but if it is not a material then

it may not be disclosed (Bobryshev and et. al., 2015).

Consistency Concept: The consistency concept requires that the basis of income

measurement and financial statement preparation should remain consistent for intra firm

comparison. GAAP allows more than one method of describing identical looking operating

situations. Accounting Standards also assumes that these policies are consistent from one-time

period to another. Thus, it is recommended to use same accounting methods each year by firm.

Convention of Materiality: This convention says that only those item should be

recorded in the books which have significant bearing and other insignificant items should be

avoided. This is done to prevent burden of minute things which are unnecessarily recorded on the

reader of accounting books. It is a matter of judgement of accountant to take a decision of

material and immaterial events and only those should be noted.

Convention of Consistency: This convention signifies that accounting practices should

be unchanged from one year to another. It is also necessary for the purpose of comparison and it

does not mean inflexibility of accounting practices. It can consider a new introduction of

improved accounting techniques. If any change is necessary than it should be stated clearly

denoting its effects and reasons for change.

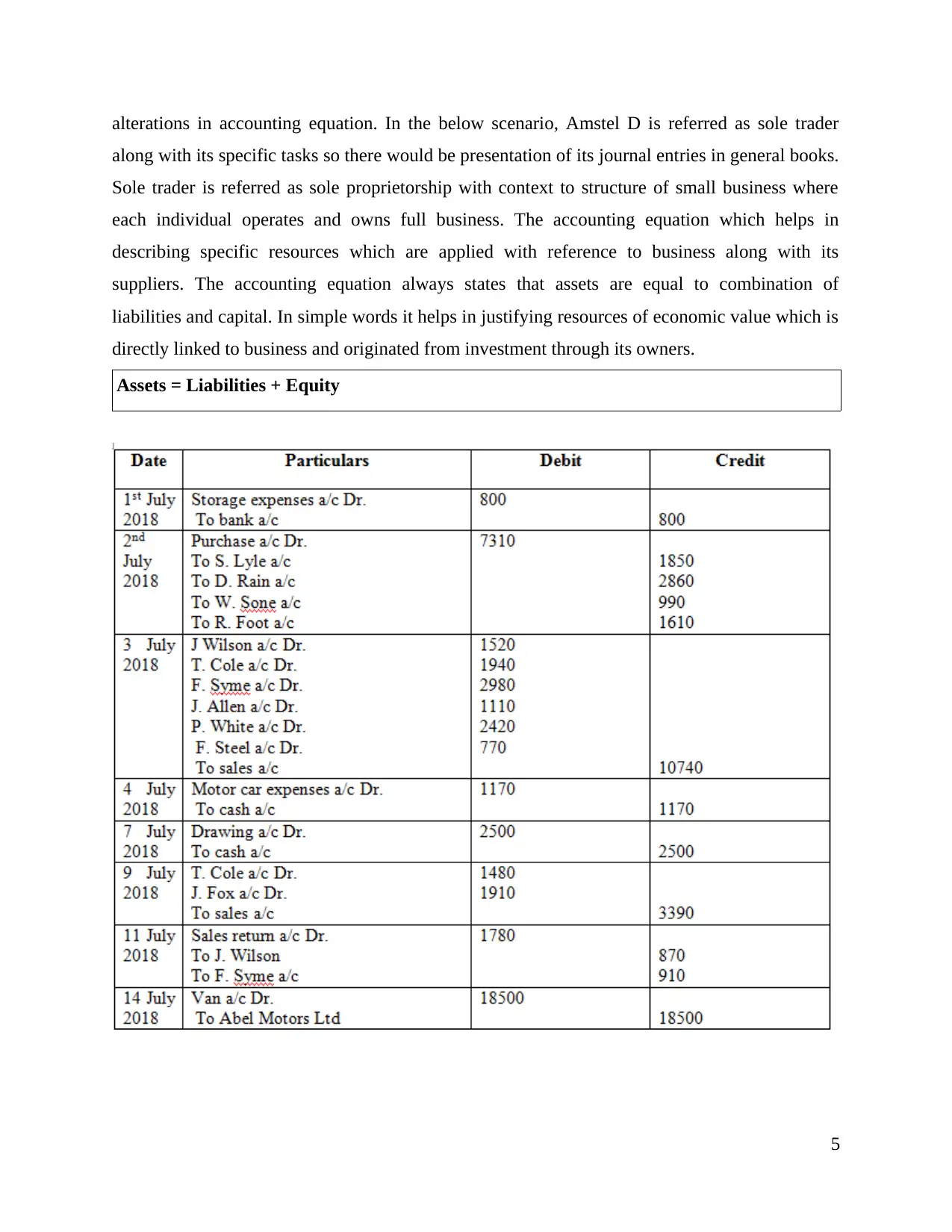

CLIENT 1

1. Drafting journal entries

Journal entries are referred as initial step with reference to accounting cycle which is used

for tracing each business transactions along with specific events with context to this system

(Maskell, Baggaley and Grasso, 2016). The events with context to business occurs in particular

accounting period, journal entries would be recorded in that specific journal for reflecting

4

income or less asset amount. It happens in a situation where there are two acceptable

alternatives for reporting any transaction.

A.4 Conventions and concepts relating to consistency and material disclosure

Materiality Concept: This concept ensures disclosure of all materials from which

decisions of the user of financial statement may affect. It is defined as the characteristics

attaching to a statement, fact or item where its disclosure can influence judgement of a

reasonable person. So, if the event is material it should be disclosed but if it is not a material then

it may not be disclosed (Bobryshev and et. al., 2015).

Consistency Concept: The consistency concept requires that the basis of income

measurement and financial statement preparation should remain consistent for intra firm

comparison. GAAP allows more than one method of describing identical looking operating

situations. Accounting Standards also assumes that these policies are consistent from one-time

period to another. Thus, it is recommended to use same accounting methods each year by firm.

Convention of Materiality: This convention says that only those item should be

recorded in the books which have significant bearing and other insignificant items should be

avoided. This is done to prevent burden of minute things which are unnecessarily recorded on the

reader of accounting books. It is a matter of judgement of accountant to take a decision of

material and immaterial events and only those should be noted.

Convention of Consistency: This convention signifies that accounting practices should

be unchanged from one year to another. It is also necessary for the purpose of comparison and it

does not mean inflexibility of accounting practices. It can consider a new introduction of

improved accounting techniques. If any change is necessary than it should be stated clearly

denoting its effects and reasons for change.

CLIENT 1

1. Drafting journal entries

Journal entries are referred as initial step with reference to accounting cycle which is used

for tracing each business transactions along with specific events with context to this system

(Maskell, Baggaley and Grasso, 2016). The events with context to business occurs in particular

accounting period, journal entries would be recorded in that specific journal for reflecting

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

alterations in accounting equation. In the below scenario, Amstel D is referred as sole trader

along with its specific tasks so there would be presentation of its journal entries in general books.

Sole trader is referred as sole proprietorship with context to structure of small business where

each individual operates and owns full business. The accounting equation which helps in

describing specific resources which are applied with reference to business along with its

suppliers. The accounting equation always states that assets are equal to combination of

liabilities and capital. In simple words it helps in justifying resources of economic value which is

directly linked to business and originated from investment through its owners.

Assets = Liabilities + Equity

5

along with its specific tasks so there would be presentation of its journal entries in general books.

Sole trader is referred as sole proprietorship with context to structure of small business where

each individual operates and owns full business. The accounting equation which helps in

describing specific resources which are applied with reference to business along with its

suppliers. The accounting equation always states that assets are equal to combination of

liabilities and capital. In simple words it helps in justifying resources of economic value which is

directly linked to business and originated from investment through its owners.

Assets = Liabilities + Equity

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

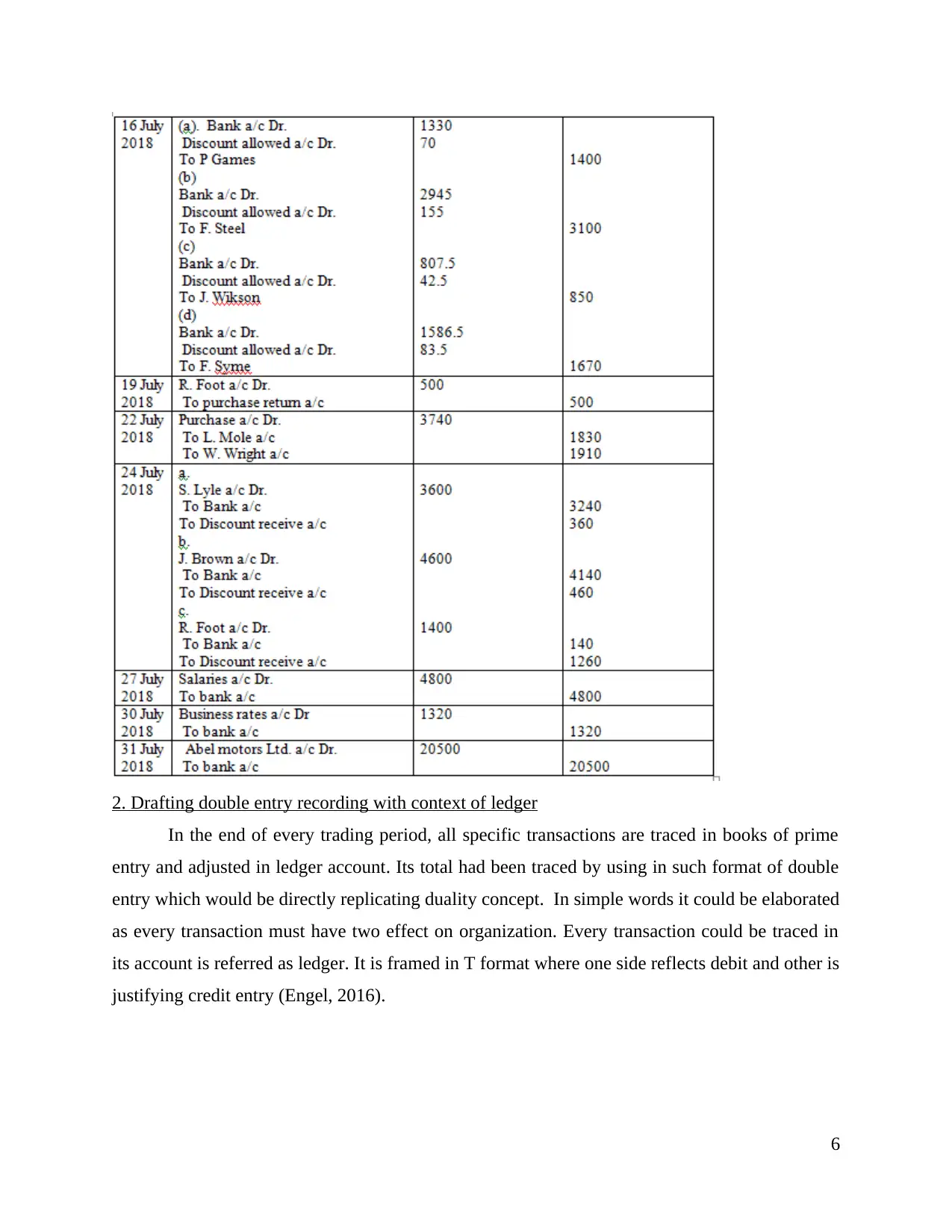

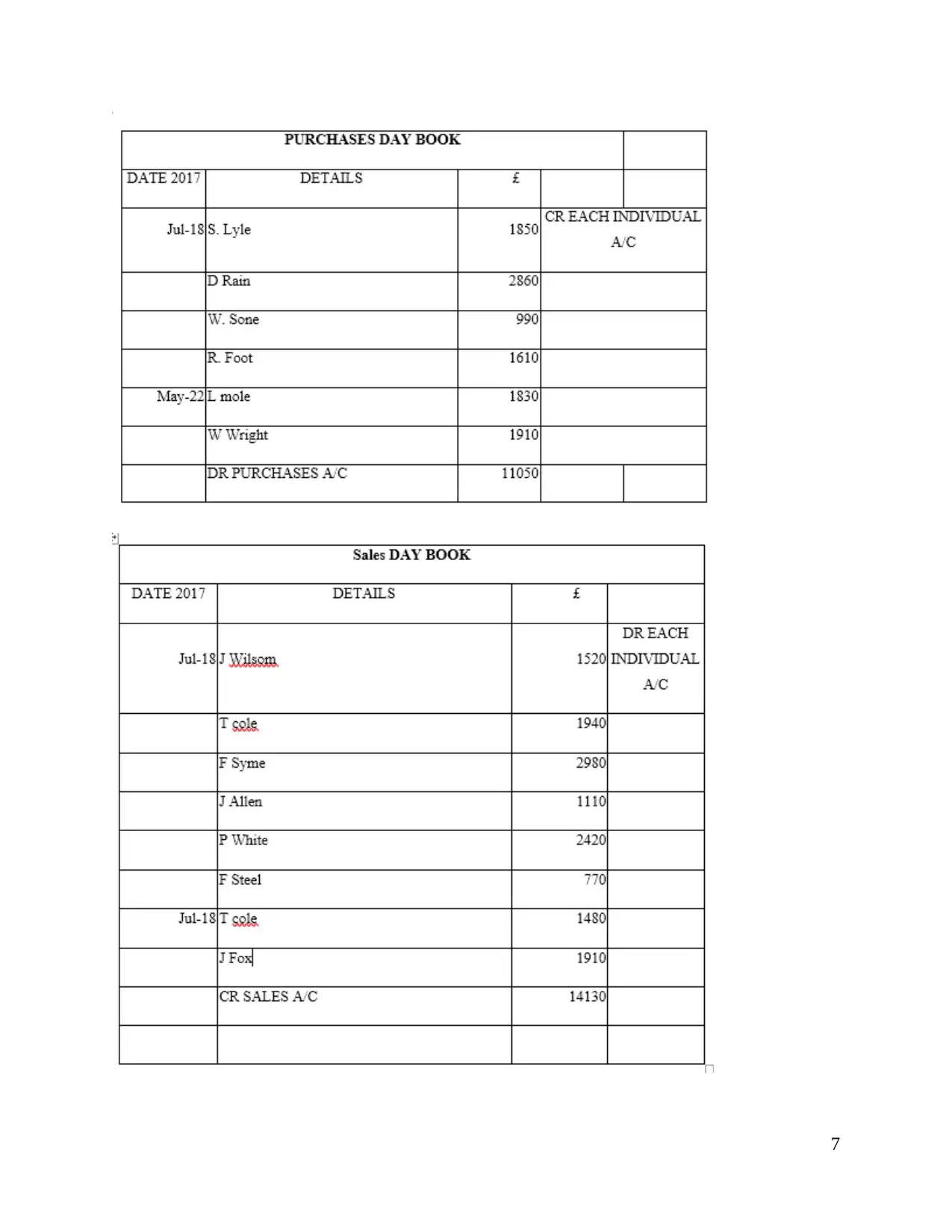

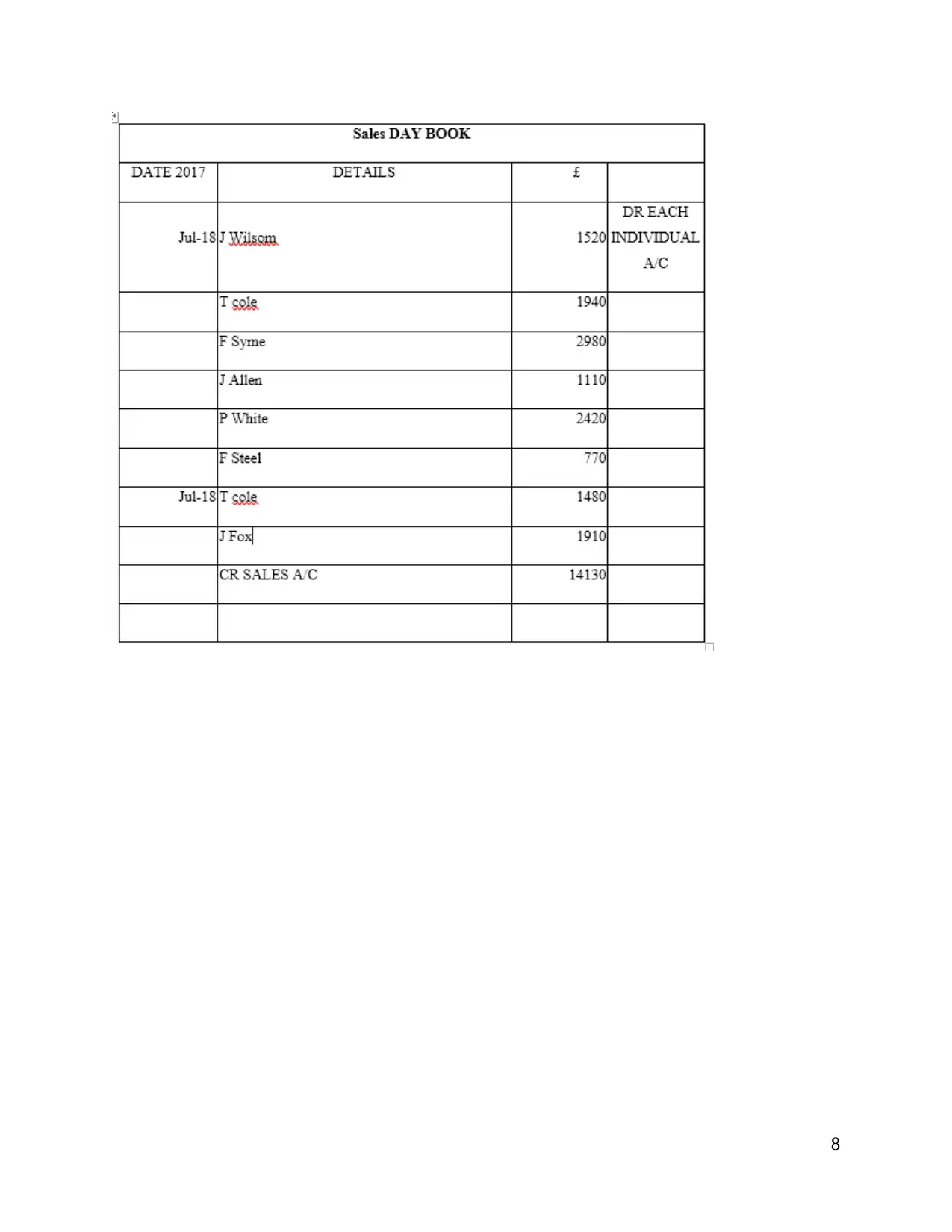

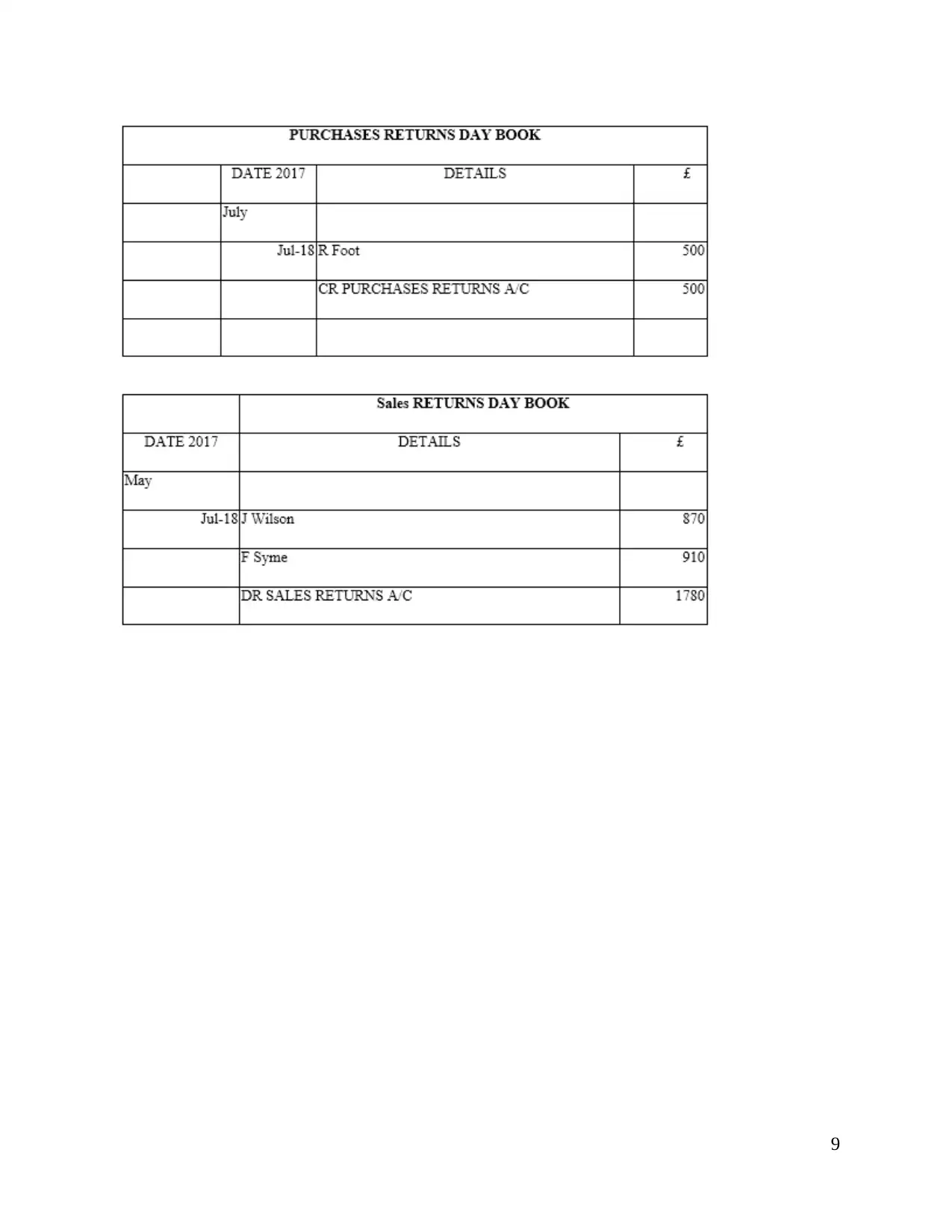

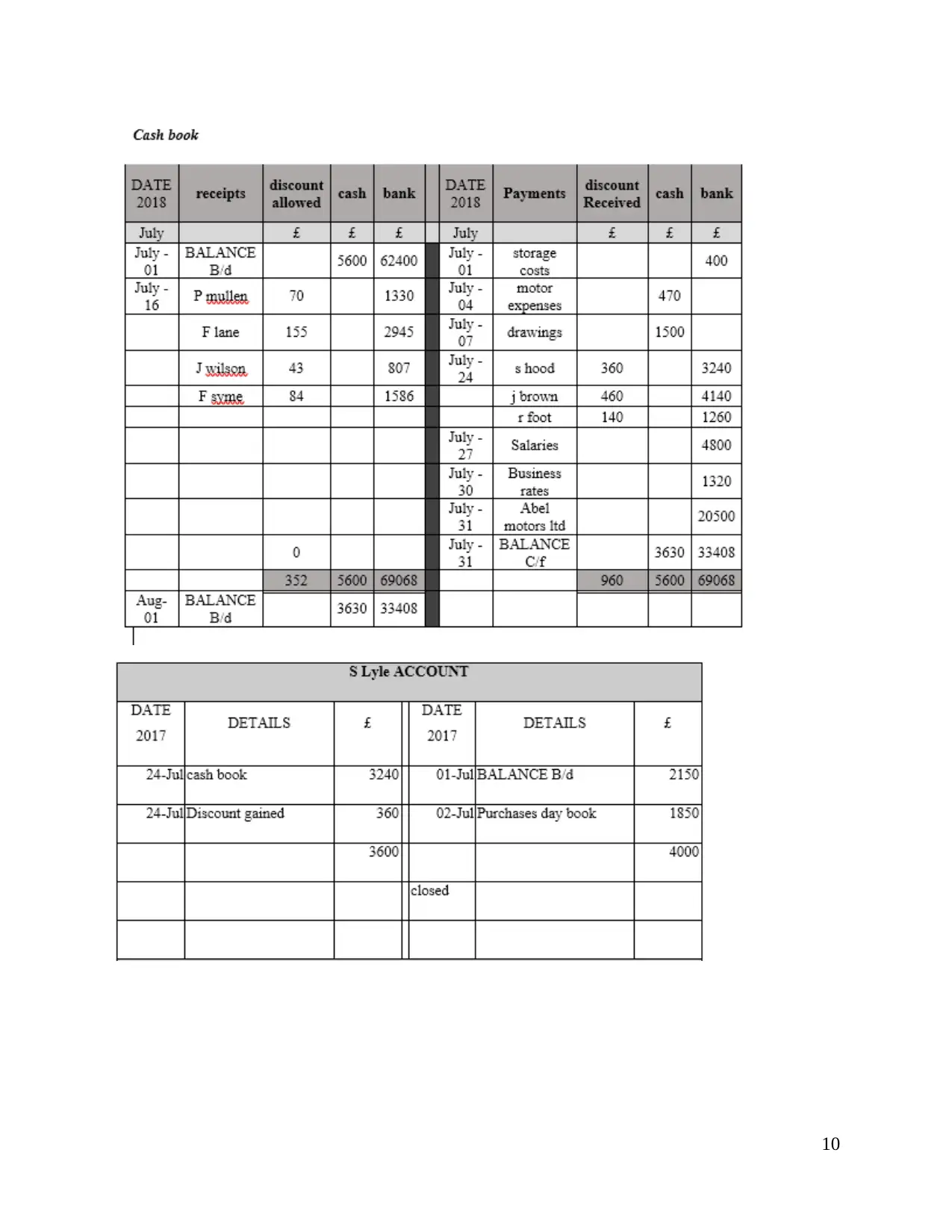

2. Drafting double entry recording with context of ledger

In the end of every trading period, all specific transactions are traced in books of prime

entry and adjusted in ledger account. Its total had been traced by using in such format of double

entry which would be directly replicating duality concept. In simple words it could be elaborated

as every transaction must have two effect on organization. Every transaction could be traced in

its account is referred as ledger. It is framed in T format where one side reflects debit and other is

justifying credit entry (Engel, 2016).

6

In the end of every trading period, all specific transactions are traced in books of prime

entry and adjusted in ledger account. Its total had been traced by using in such format of double

entry which would be directly replicating duality concept. In simple words it could be elaborated

as every transaction must have two effect on organization. Every transaction could be traced in

its account is referred as ledger. It is framed in T format where one side reflects debit and other is

justifying credit entry (Engel, 2016).

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 41

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.