Financial Accounting Principles: Regulations, Statements & Analysis

VerifiedAdded on 2024/06/04

|15

|2236

|349

Report

AI Summary

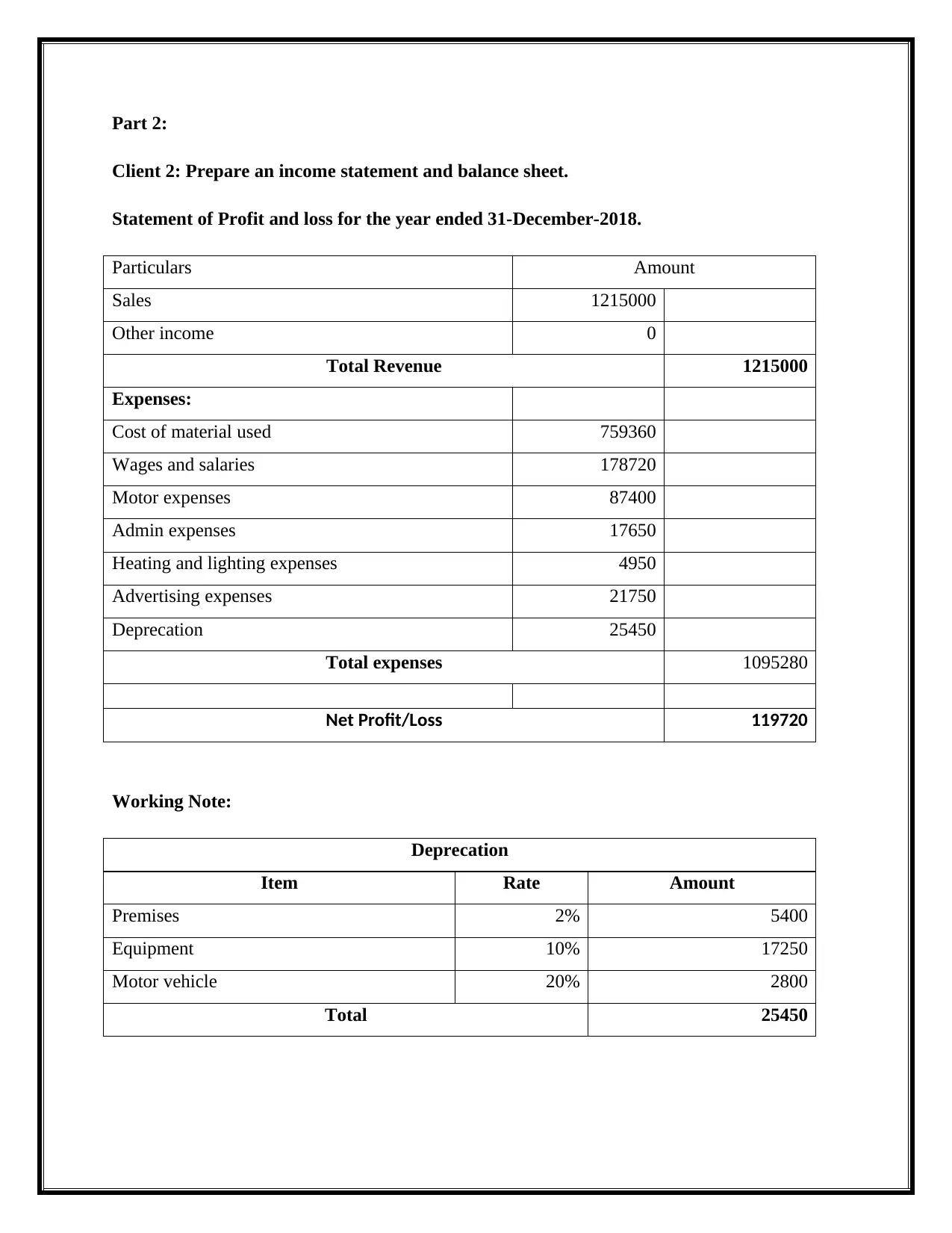

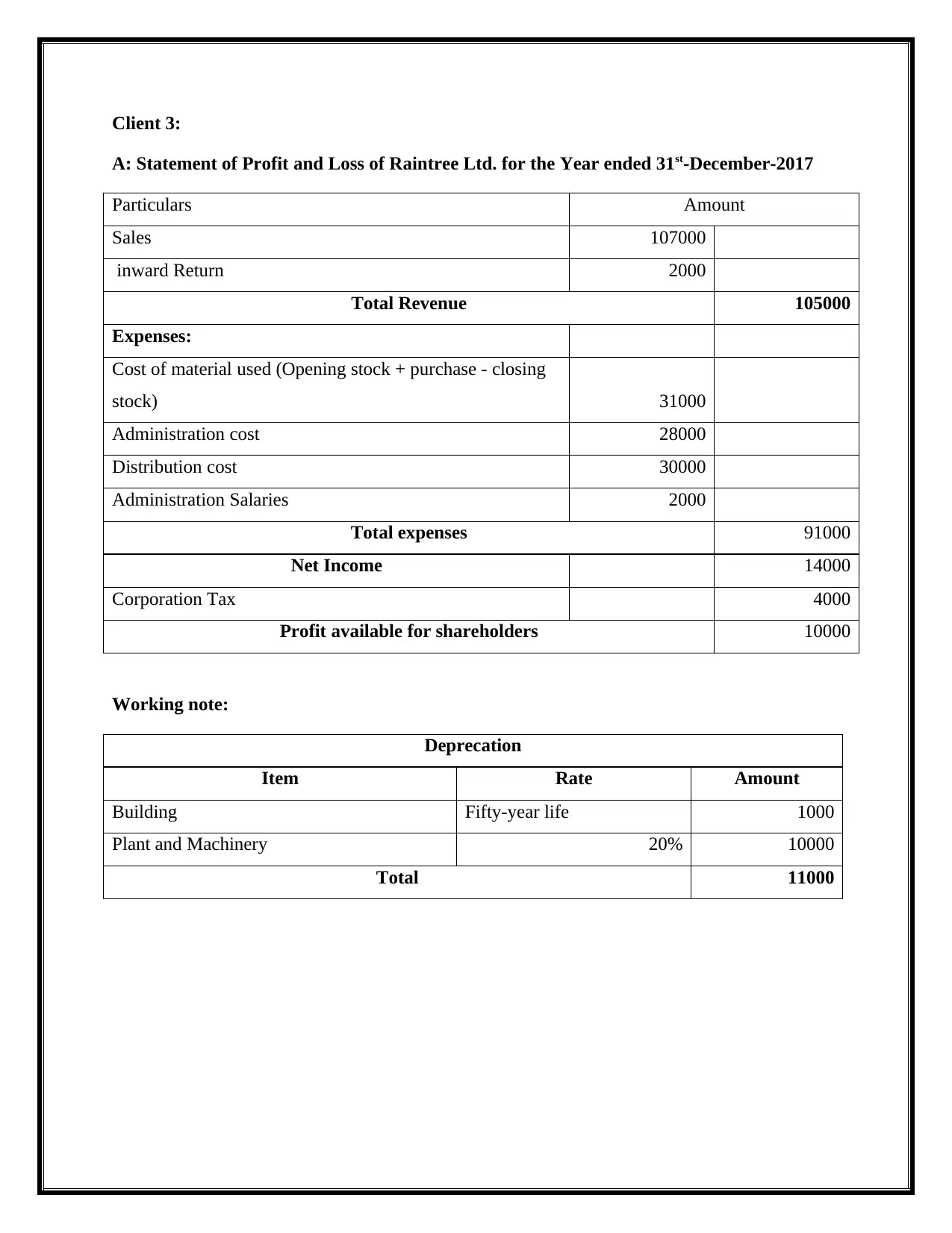

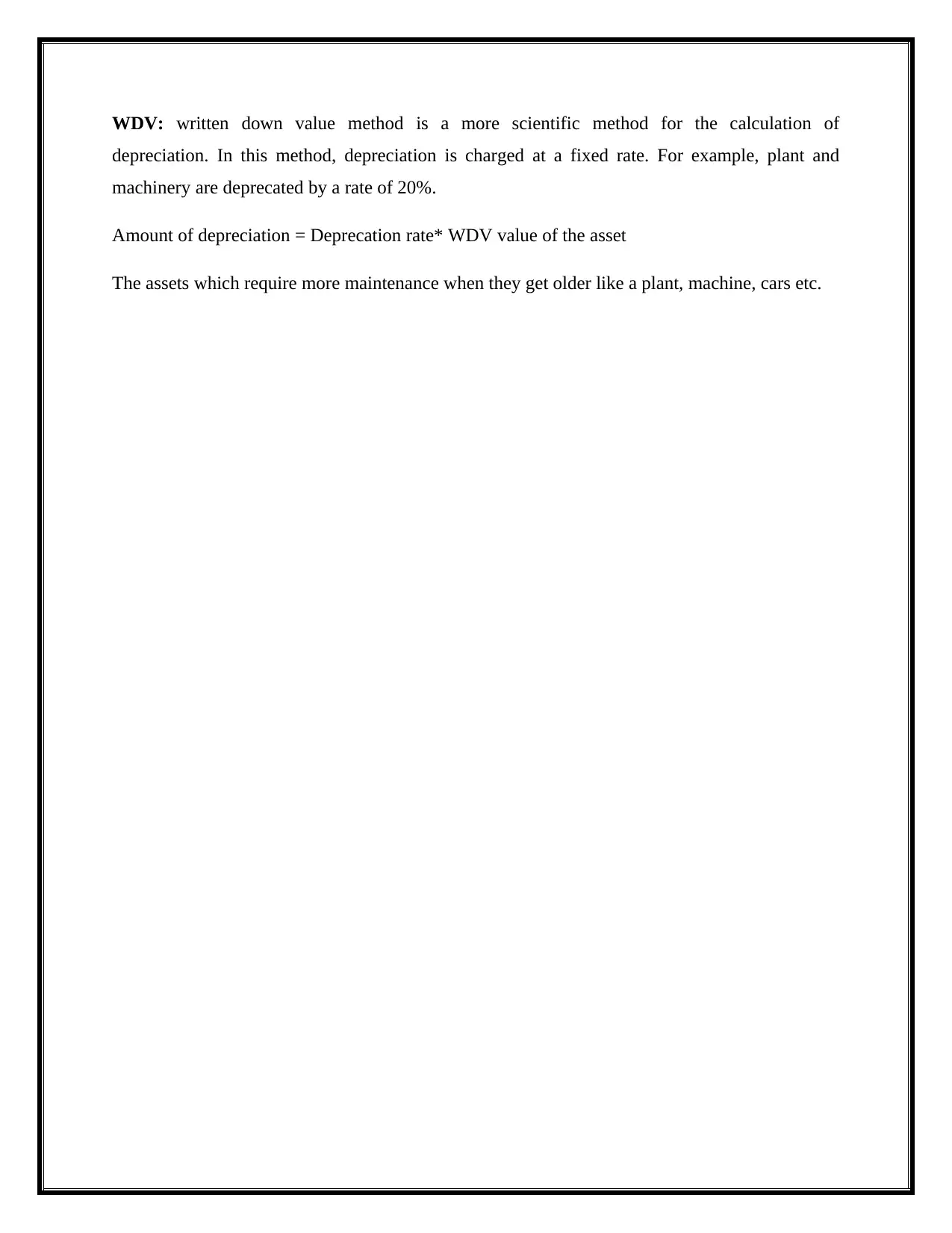

This report provides a comprehensive overview of financial accounting principles, beginning with a definition of financial accounting and its role in reporting a business's financial position to external users. It explains the regulations relating to financial accounting, focusing on GAAP and IASB, and describes essential accounting rules such as debiting the receiver and crediting the giver, alongside core principles like accrual, cost, matching, and conservatism. The report further elaborates on the concepts of consistency and material disclosure, emphasizing their importance in ensuring uniformity and comparability in financial statements. Practical application is demonstrated through the preparation of income statements and balance sheets for Clients 2 and 3, including detailed working notes for depreciation calculations. Additionally, the report discusses the concept of consistency and prudence with respect to Raintree Ltd., and it explains the purpose and methods of depreciation. The report also mentions control accounts. Desklib provides this document along with a wealth of resources for students.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.