Report on Financial Accounting Principles, Rules, and Regulations

VerifiedAdded on 2024/06/11

|28

|2807

|301

Report

AI Summary

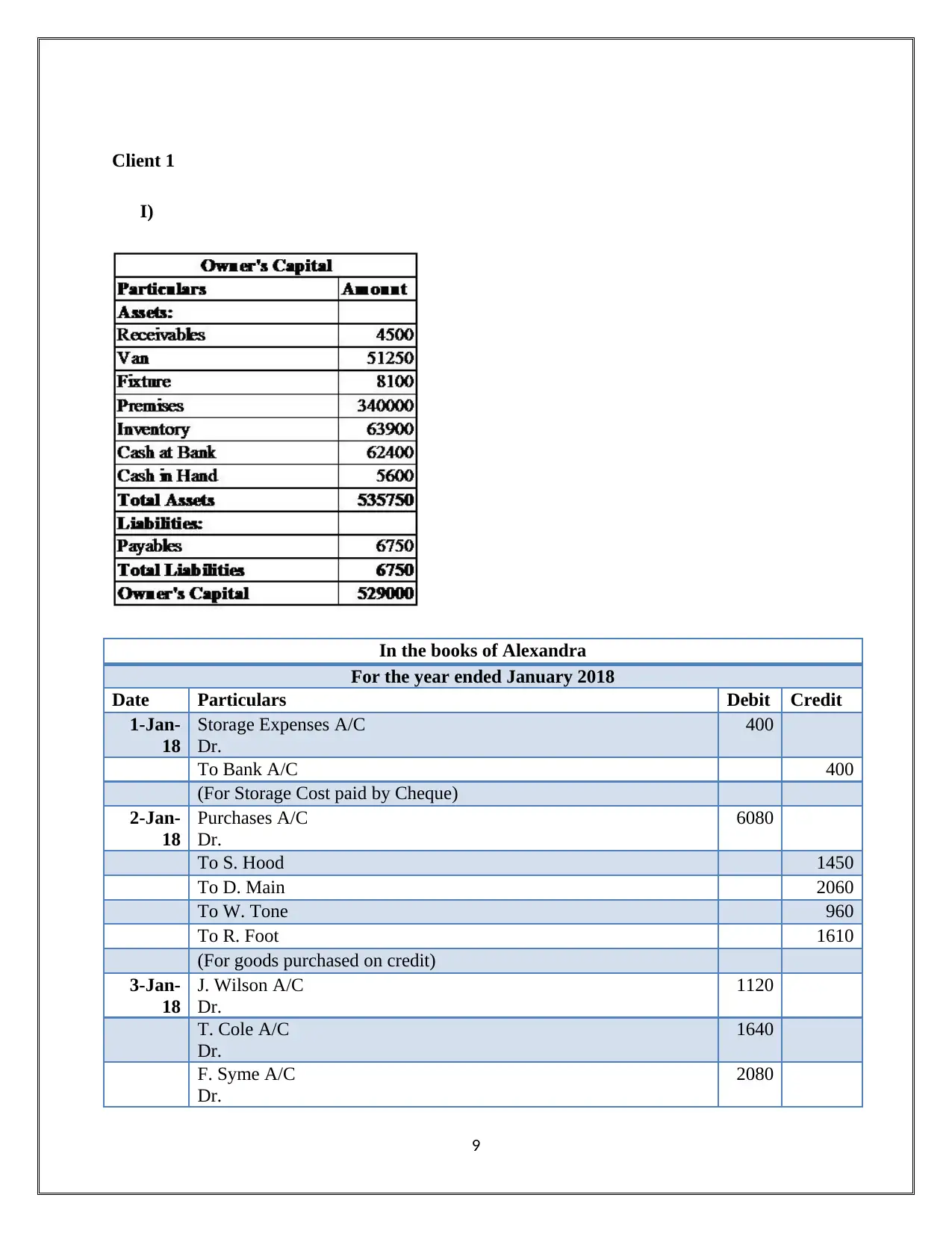

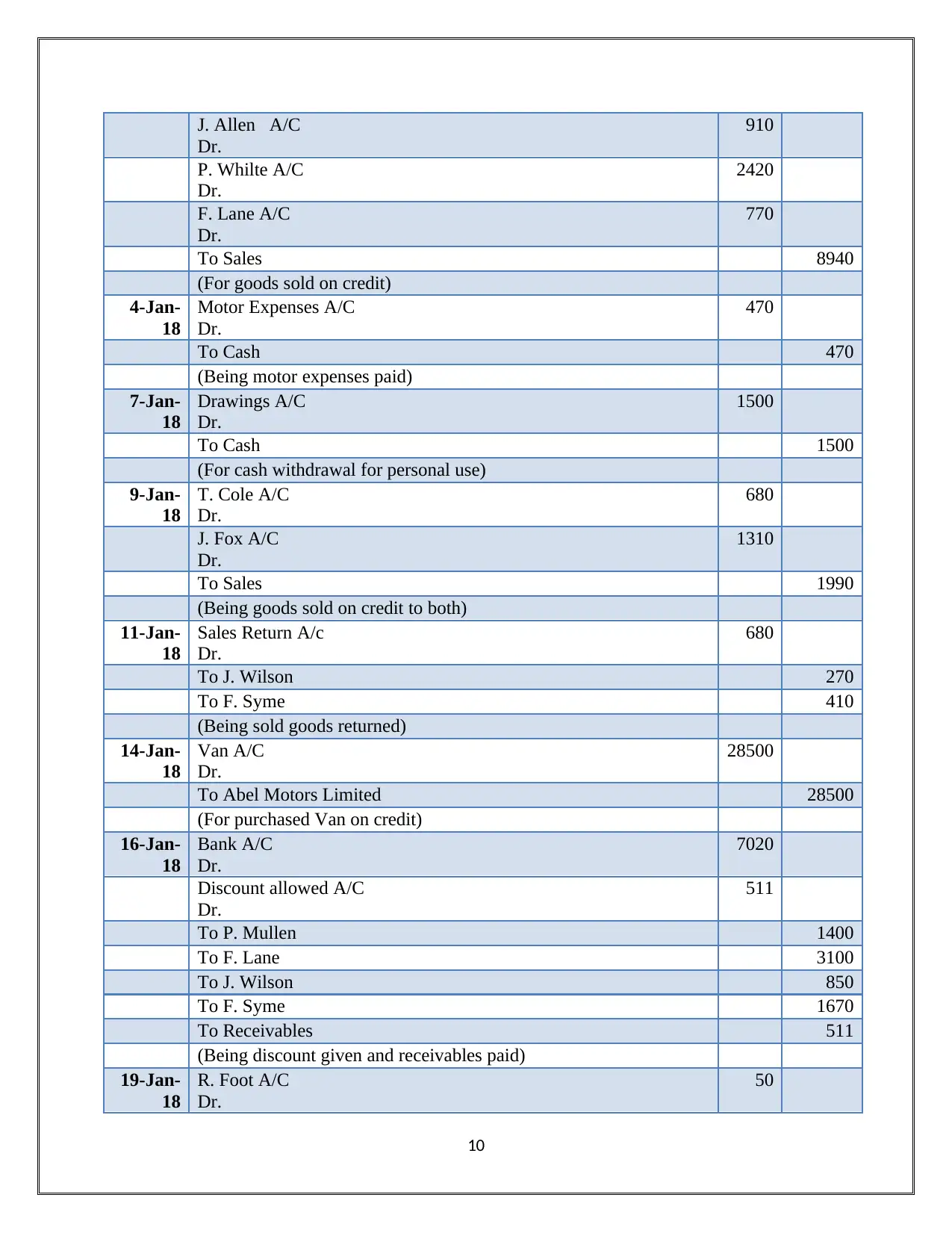

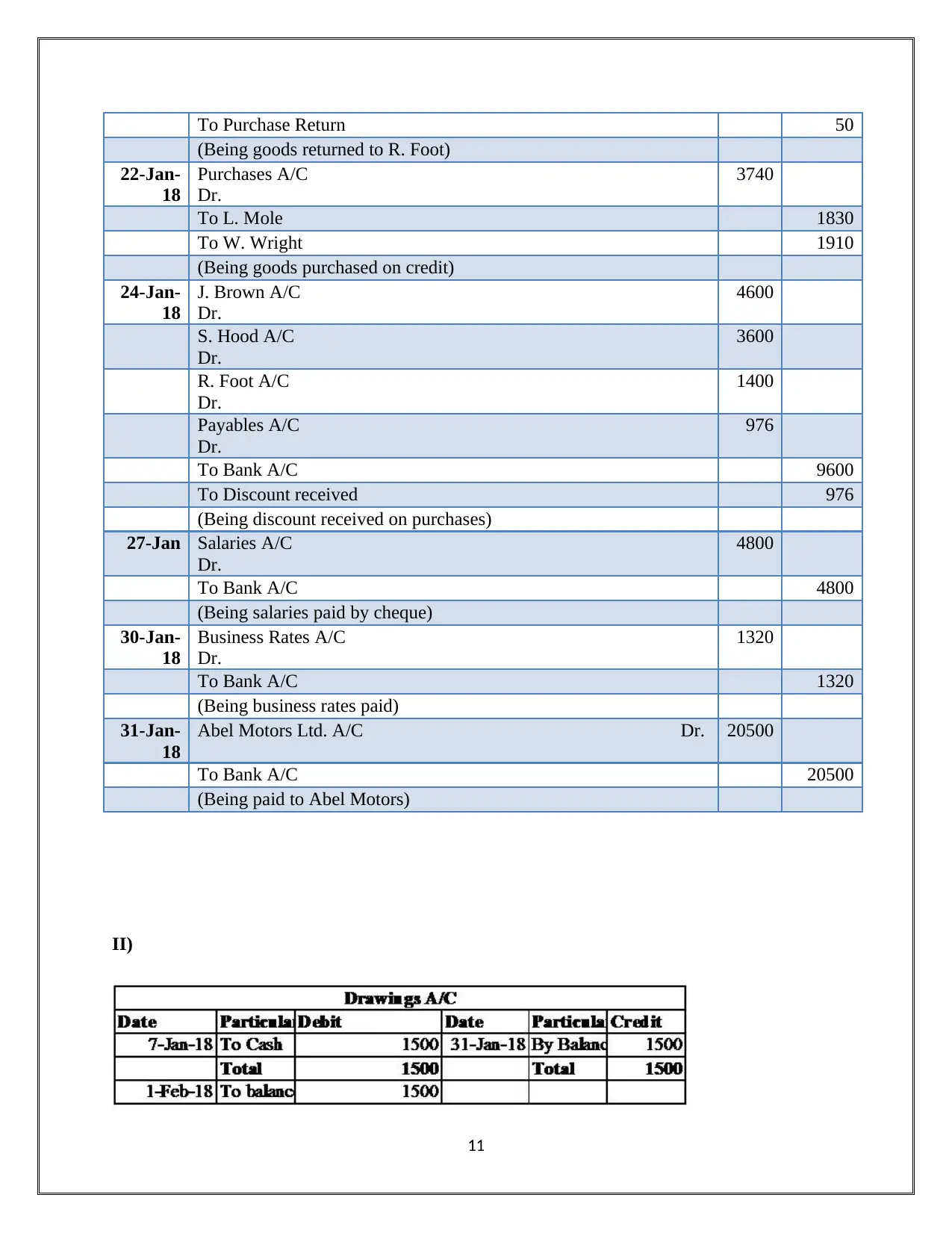

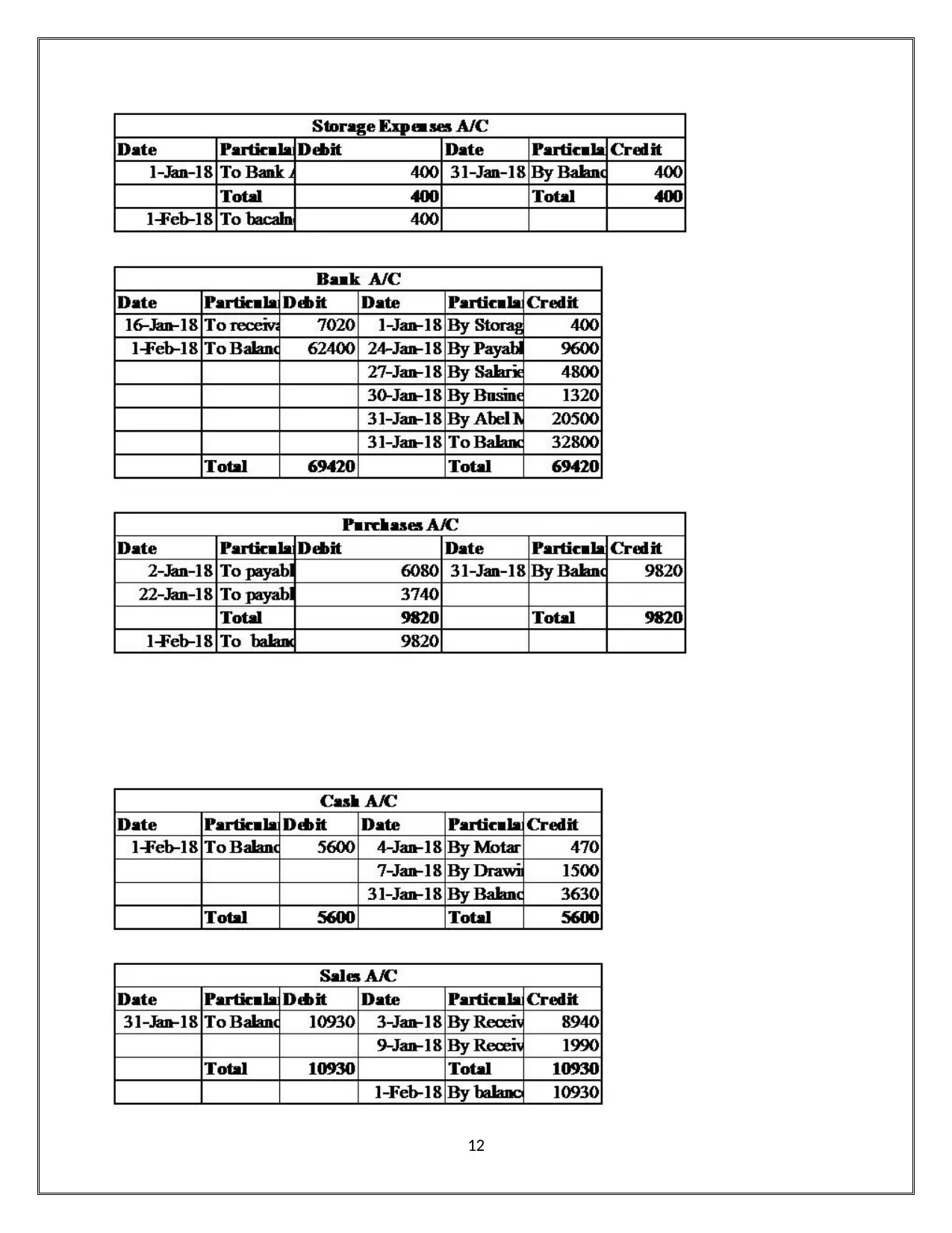

This report provides a detailed explanation of financial accounting principles, covering various concepts, rules, and regulations. It highlights the debit and credit rules, consistency, and material disclosure concepts. The report includes practical applications through financial statements like profit & loss statements, bank reconciliation statements, and trial balances for multiple clients. It discusses the role of the International Accounting Standard Board, the Statement of Principles, and specific accounting rules like debiting the receiver and crediting the giver. Furthermore, it delves into accounting principles such as the matching principle and historic cost principle, alongside conventions like consistency and materiality disclosure. The report also addresses the purpose of depreciation and methods for calculating it, ending with the importance of bank reconciliation statements and areas causing differences in cash and bank books.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.