Financial Accounting Principles Report: Regulations and Principles

VerifiedAdded on 2021/01/03

|27

|6978

|29

Report

AI Summary

This report comprehensively addresses financial accounting principles, regulations, and their practical application. It begins with an introduction to financial accounting, its purpose, and the regulations governing it. The main body of the report delves into key accounting principles, including the golden rules, economic entity assumption, and cost principle. It also explores conventions such as consistency and material disclosure. The report includes several client-based examples that cover the books of prime entries, balance sheets, profit and loss statements, and cash flow statements, along with explanations of depreciation and bank reconciliation. Furthermore, the report provides a detailed examination of sales and purchase ledgers, control accounts, suspense accounts, and trial balances. The conclusion summarizes the key findings, and a reference list is included for further study. The report is designed to provide a comprehensive overview of financial accounting practices and concepts, offering valuable insights into the preparation and interpretation of financial statements.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

1. Describing financial accounting and purpose.........................................................................1

2. Explaining regulations which relates to financial accounting.................................................2

3. Description of accounting rules and principles.......................................................................3

4. Explaining conventions and concepts which related to consistency and material disclosure.4

CLIENT 1........................................................................................................................................5

I.) Books of prime entries............................................................................................................5

CLIENT 2......................................................................................................................................12

Balance sheet for the year ended 31 July 2018.........................................................................12

CLIENT 3......................................................................................................................................14

A.) Profit and Loss statement....................................................................................................14

b.) statement of financial position.............................................................................................16

c.) Explanation on following concepts......................................................................................17

D.) purpose of depreciation with its two methods....................................................................17

CLIENT 4......................................................................................................................................17

A.) Purpose of preparing bank reconciliation statement...........................................................17

B.) Explaining areas which cause records vary with bank records...........................................17

C.) Preparation of accounts through cash flow statement.........................................................17

CLIENT 5......................................................................................................................................19

(A.) Preparation of sales ledge and purchase ledge account.....................................................19

(B.) Explanation on need for preparing control account...........................................................20

CLIENT 6......................................................................................................................................20

A.) Explanation of the term suspense account..........................................................................20

B.) Drafting of trial balance......................................................................................................21

C.) Trial balance suspense account...........................................................................................21

D.) Difference between suspense account and clearing account..............................................22

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

1. Describing financial accounting and purpose.........................................................................1

2. Explaining regulations which relates to financial accounting.................................................2

3. Description of accounting rules and principles.......................................................................3

4. Explaining conventions and concepts which related to consistency and material disclosure.4

CLIENT 1........................................................................................................................................5

I.) Books of prime entries............................................................................................................5

CLIENT 2......................................................................................................................................12

Balance sheet for the year ended 31 July 2018.........................................................................12

CLIENT 3......................................................................................................................................14

A.) Profit and Loss statement....................................................................................................14

b.) statement of financial position.............................................................................................16

c.) Explanation on following concepts......................................................................................17

D.) purpose of depreciation with its two methods....................................................................17

CLIENT 4......................................................................................................................................17

A.) Purpose of preparing bank reconciliation statement...........................................................17

B.) Explaining areas which cause records vary with bank records...........................................17

C.) Preparation of accounts through cash flow statement.........................................................17

CLIENT 5......................................................................................................................................19

(A.) Preparation of sales ledge and purchase ledge account.....................................................19

(B.) Explanation on need for preparing control account...........................................................20

CLIENT 6......................................................................................................................................20

A.) Explanation of the term suspense account..........................................................................20

B.) Drafting of trial balance......................................................................................................21

C.) Trial balance suspense account...........................................................................................21

D.) Difference between suspense account and clearing account..............................................22

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION

Financial accounting principles are rules and guidelines which every company must have

to follow while preparing its financial statements (Trotman and Carson, 2018). These set of

accounting principles differ from country to country. Chosen organisation in this report is DNS

Associates which provides services in consultation relates to finance. In this assessment,

financial accounting and its purpose will be discussed with its regulations. Further, explanation

will be provided on accounting principles and rules with the conventions and concepts relates to

consistency and material disclosing. Moreover, proper calculation with description will also be

evaluated in this report.

MAIN BODY

1. Describing financial accounting and purpose

Financial accounting is a special branch of accounting which provides rules and

guidelines to companies in order to maintain their financial transactions (Freedman, 2018). With

these guidelines, transactions in income statement and in financial positions are recorded,

summarized and presented in proper way. This is the process by which company show its

financial performance and position to its users which includes investors, suppliers, creditors and

customers. Its objective is to show fair and accurate picture of company's financial capability

with its business affairs.

Its main purpose is not to report value of financial transactions of the company. Rather,

its purpose is to provide information and analysis to its users by which they will able to assess

the value themselves. It is also developed by company for sound economic decision-making

process. There are three main statements which prepared by the company which include income

Statements, financial position and cash flow statement (Weygandt, Kimmel and Kieso, 2015).

Main purpose of preparing income statement is to inform its reader business ability for earn

business profit. It also provides information which relates to volume sales, types of expenditures

and incomes which company incurred during financial year.

Purpose of financial accounting is to provide information which relates to business activities of

owners, stakeholder, investors and creditors which facilitate them to take investment decision

and lending decision. By providing such analysis and proper information, entity will able to gain

Financial accounting principles are rules and guidelines which every company must have

to follow while preparing its financial statements (Trotman and Carson, 2018). These set of

accounting principles differ from country to country. Chosen organisation in this report is DNS

Associates which provides services in consultation relates to finance. In this assessment,

financial accounting and its purpose will be discussed with its regulations. Further, explanation

will be provided on accounting principles and rules with the conventions and concepts relates to

consistency and material disclosing. Moreover, proper calculation with description will also be

evaluated in this report.

MAIN BODY

1. Describing financial accounting and purpose

Financial accounting is a special branch of accounting which provides rules and

guidelines to companies in order to maintain their financial transactions (Freedman, 2018). With

these guidelines, transactions in income statement and in financial positions are recorded,

summarized and presented in proper way. This is the process by which company show its

financial performance and position to its users which includes investors, suppliers, creditors and

customers. Its objective is to show fair and accurate picture of company's financial capability

with its business affairs.

Its main purpose is not to report value of financial transactions of the company. Rather,

its purpose is to provide information and analysis to its users by which they will able to assess

the value themselves. It is also developed by company for sound economic decision-making

process. There are three main statements which prepared by the company which include income

Statements, financial position and cash flow statement (Weygandt, Kimmel and Kieso, 2015).

Main purpose of preparing income statement is to inform its reader business ability for earn

business profit. It also provides information which relates to volume sales, types of expenditures

and incomes which company incurred during financial year.

Purpose of financial accounting is to provide information which relates to business activities of

owners, stakeholder, investors and creditors which facilitate them to take investment decision

and lending decision. By providing such analysis and proper information, entity will able to gain

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

trust and support of its users where they will remain in company for long term perspectives.

Several additional purpose of using financial accounting includes-

Credit decision: entire set of financial statements are used by lenders for determining

their decision that whether it should be extended to credit business or not. Financial statement are

provided by organisation to show its financial capability to such lenders.

Investment decision: financial statements of company are also analysed by investor of

the company in order to determine whether to invest on price per share at which they are offered

for buying business (Warren and Jones, 2018). In order to run smooth business operations, it is

necessary that organisation will have support of its investors. By showing regular financial

performance, company will able to gain trust of its investors.

Taxation decision: government use entire set of information to determine whether

imposition of tax on company on the basis of its income and assets. Proper information to

government will help in gaining government support by which brand image of company among

customer get increases.

Union bargaining decision: Unions also need financial statement of company in order to

develop base of bargaining position according to ability of business to pay. This will help entity

to gain trust of its employee by which they will develop the best efforts for gaining

organisational objectives.

2. Explaining regulations which relates to financial accounting

Financial accounting regulations are the proper guidelines which set up by particular

bodies in order to prepare their financial statement. Motive of developing these regulations is to

provide a common and understandable language to users which across the world (Habib,

Ranasinghe and Huang, 2018). Financial accounting is the process which includes identification

and recording of financial information, measurement of financial performance through which

proper communication between users and company get developed. Following are the regulations

of financial accounting:

Regulatory bodies (IASB, FRC) : Financial reporting council is the UK's independent

body which is responsible to promote high quality of corporate governance and reporting. This

body has set up proper code of conduct and standards which needs to follow by organisation's for

preparing their financial statements. This body supported by two businesses which includes

Several additional purpose of using financial accounting includes-

Credit decision: entire set of financial statements are used by lenders for determining

their decision that whether it should be extended to credit business or not. Financial statement are

provided by organisation to show its financial capability to such lenders.

Investment decision: financial statements of company are also analysed by investor of

the company in order to determine whether to invest on price per share at which they are offered

for buying business (Warren and Jones, 2018). In order to run smooth business operations, it is

necessary that organisation will have support of its investors. By showing regular financial

performance, company will able to gain trust of its investors.

Taxation decision: government use entire set of information to determine whether

imposition of tax on company on the basis of its income and assets. Proper information to

government will help in gaining government support by which brand image of company among

customer get increases.

Union bargaining decision: Unions also need financial statement of company in order to

develop base of bargaining position according to ability of business to pay. This will help entity

to gain trust of its employee by which they will develop the best efforts for gaining

organisational objectives.

2. Explaining regulations which relates to financial accounting

Financial accounting regulations are the proper guidelines which set up by particular

bodies in order to prepare their financial statement. Motive of developing these regulations is to

provide a common and understandable language to users which across the world (Habib,

Ranasinghe and Huang, 2018). Financial accounting is the process which includes identification

and recording of financial information, measurement of financial performance through which

proper communication between users and company get developed. Following are the regulations

of financial accounting:

Regulatory bodies (IASB, FRC) : Financial reporting council is the UK's independent

body which is responsible to promote high quality of corporate governance and reporting. This

body has set up proper code of conduct and standards which needs to follow by organisation's for

preparing their financial statements. This body supported by two businesses which includes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Codes and Standards Committee and Conduct Committee. This helps organisation to maintain

their financial statements with transparency and honesty.

IFRS: these are the set of international accounting standards which provide a proper

guideline to companies for particular type of transaction and events which needs to be recorded

in books of accounts. These set of standards helps organisations to provide high quality,

internationally recognised set of accounting which brings transparency, accountability and

efficiency to financial market across the nation. Main goal of developing such reporting method

is to develop transparency and reliability in financial statements of company (Jayaram and et.al.,

2018).

IASB: this is the independent, non-profit and private sector organisation which working

for the public interest in order to develop advanced quality, enforceable and globally accepted

accounting principles by which entity maintain their financial statements in proper format with

effective disclosures.

3. Description of accounting rules and principles

Accounting rules are the proper statements which establish to provide proper guidance to

companies and accountant in order to record every transaction.

Golden rules of accounting (Traditional approach):

Personal account: golden rule which relates to personal account states that debit the

receiver and credit the giver. It means that if person receive something then it must be recorded

where receiver account shall be debited and person who give something must be credited.

Real account: rules which relates to real account states that debit what comes in and

credit what goes out. It means that if something come in business shall be debited and if

something goes out from business must be credited (Madhavi, 2017.).

Nominal account: golden rule which related to nominal account states that debit all the

expenses and losses and credit all the incomes and gains. This means that if business incur any

expense and loss then this account must be debited and income receive by business must be

credited.

Accounting principles:

Economic Entity Assumption: which means that accountant keep business transaction

separate from personal transaction of owner.

their financial statements with transparency and honesty.

IFRS: these are the set of international accounting standards which provide a proper

guideline to companies for particular type of transaction and events which needs to be recorded

in books of accounts. These set of standards helps organisations to provide high quality,

internationally recognised set of accounting which brings transparency, accountability and

efficiency to financial market across the nation. Main goal of developing such reporting method

is to develop transparency and reliability in financial statements of company (Jayaram and et.al.,

2018).

IASB: this is the independent, non-profit and private sector organisation which working

for the public interest in order to develop advanced quality, enforceable and globally accepted

accounting principles by which entity maintain their financial statements in proper format with

effective disclosures.

3. Description of accounting rules and principles

Accounting rules are the proper statements which establish to provide proper guidance to

companies and accountant in order to record every transaction.

Golden rules of accounting (Traditional approach):

Personal account: golden rule which relates to personal account states that debit the

receiver and credit the giver. It means that if person receive something then it must be recorded

where receiver account shall be debited and person who give something must be credited.

Real account: rules which relates to real account states that debit what comes in and

credit what goes out. It means that if something come in business shall be debited and if

something goes out from business must be credited (Madhavi, 2017.).

Nominal account: golden rule which related to nominal account states that debit all the

expenses and losses and credit all the incomes and gains. This means that if business incur any

expense and loss then this account must be debited and income receive by business must be

credited.

Accounting principles:

Economic Entity Assumption: which means that accountant keep business transaction

separate from personal transaction of owner.

Monetary Unit Assumption: the concept of such principle assumes that business

transactions and events must be prepared and expressed in terms of monetary units only which

are stable and dependable.

Time Period Assumption: principle assume that it is possible for businesses to record

complex and ongoing transactions in a very short time interval.

Cost principle: the concept of cost principle states that financial transaction related to

business needs to be record at actual cost rather than on current value.

Full disclosure principle: according to this principle if certain information is useful for

investor then in financial statement it must be disclosed within statement or in notes because of

basic accounting principle.

Going Concern Principle: principle states that company will carry out its business

operations of long term perspective and will not liquidate in the future.

Matching Principle: this principle requires companies to maintain financial statements

with accrual basis of accounting where expenses will be matched with revenues.

Revenue Recognition Principle: concept of such principle revenue are recognised as

soon as product been sold or service been performed.

Materiality: This principle states that all the material information must be disclosed by

organisation.

Conservatism: This is the general principle of recognising expenses and liabilities when

there is uncertainty about its outcome (Jeppson, Ruddy and Salerno, 2016).

4. Explaining conventions and concepts which related to consistency and material disclosure

Consistency-

This is the accounting principles which states that company must use same accounting

policies and methods in order to record similar nature of events and transactions which is from

one accounting period to another. It means that once the method has been selected to prepare

financial statements of organisation, then all such method will consistently be followed in

accounting periods. If entity wants to change such methods and procedures in maintaining their

financial reports, reasons of such will must have to disclose by company. According to financial

accounting standard board the consistency method is one of the characteristics and qualities

which makes accounting information more useful (Barker, 2015).

transactions and events must be prepared and expressed in terms of monetary units only which

are stable and dependable.

Time Period Assumption: principle assume that it is possible for businesses to record

complex and ongoing transactions in a very short time interval.

Cost principle: the concept of cost principle states that financial transaction related to

business needs to be record at actual cost rather than on current value.

Full disclosure principle: according to this principle if certain information is useful for

investor then in financial statement it must be disclosed within statement or in notes because of

basic accounting principle.

Going Concern Principle: principle states that company will carry out its business

operations of long term perspective and will not liquidate in the future.

Matching Principle: this principle requires companies to maintain financial statements

with accrual basis of accounting where expenses will be matched with revenues.

Revenue Recognition Principle: concept of such principle revenue are recognised as

soon as product been sold or service been performed.

Materiality: This principle states that all the material information must be disclosed by

organisation.

Conservatism: This is the general principle of recognising expenses and liabilities when

there is uncertainty about its outcome (Jeppson, Ruddy and Salerno, 2016).

4. Explaining conventions and concepts which related to consistency and material disclosure

Consistency-

This is the accounting principles which states that company must use same accounting

policies and methods in order to record similar nature of events and transactions which is from

one accounting period to another. It means that once the method has been selected to prepare

financial statements of organisation, then all such method will consistently be followed in

accounting periods. If entity wants to change such methods and procedures in maintaining their

financial reports, reasons of such will must have to disclose by company. According to financial

accounting standard board the consistency method is one of the characteristics and qualities

which makes accounting information more useful (Barker, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is the approach which does not prohibit companies to change accounting principles

and methods, infect entities are free to change method to prepare their financial statements. Only

reason is that company needs to provide logical reason for adopting such change. If valid reason

has been found for changing accounting principle than business must have to disclose nature of

change, its reason and effect on financial statements. It is an important concept because it

provides effective comparability by which investors and other users of company will easily able

to analyse and compare financial statements of company.

Material disclosure-

It is an accounting principle which require that management must have to report all the

relevant information regarding operations of the company to their creditors and investors in

financial statements and footnotes. It is necessary that each and every information which related

to company's business operations must be informed to creditors and investors so that they will

able to develop and analysis their investment decision of company. Material disclosure need to

be disclosed with financial statements including any supplementary footnotes and schedules.

Information also get disclosed though annual reports or with quarterly earning reports, press

releases or with any other communication technique (Clark, 2016).

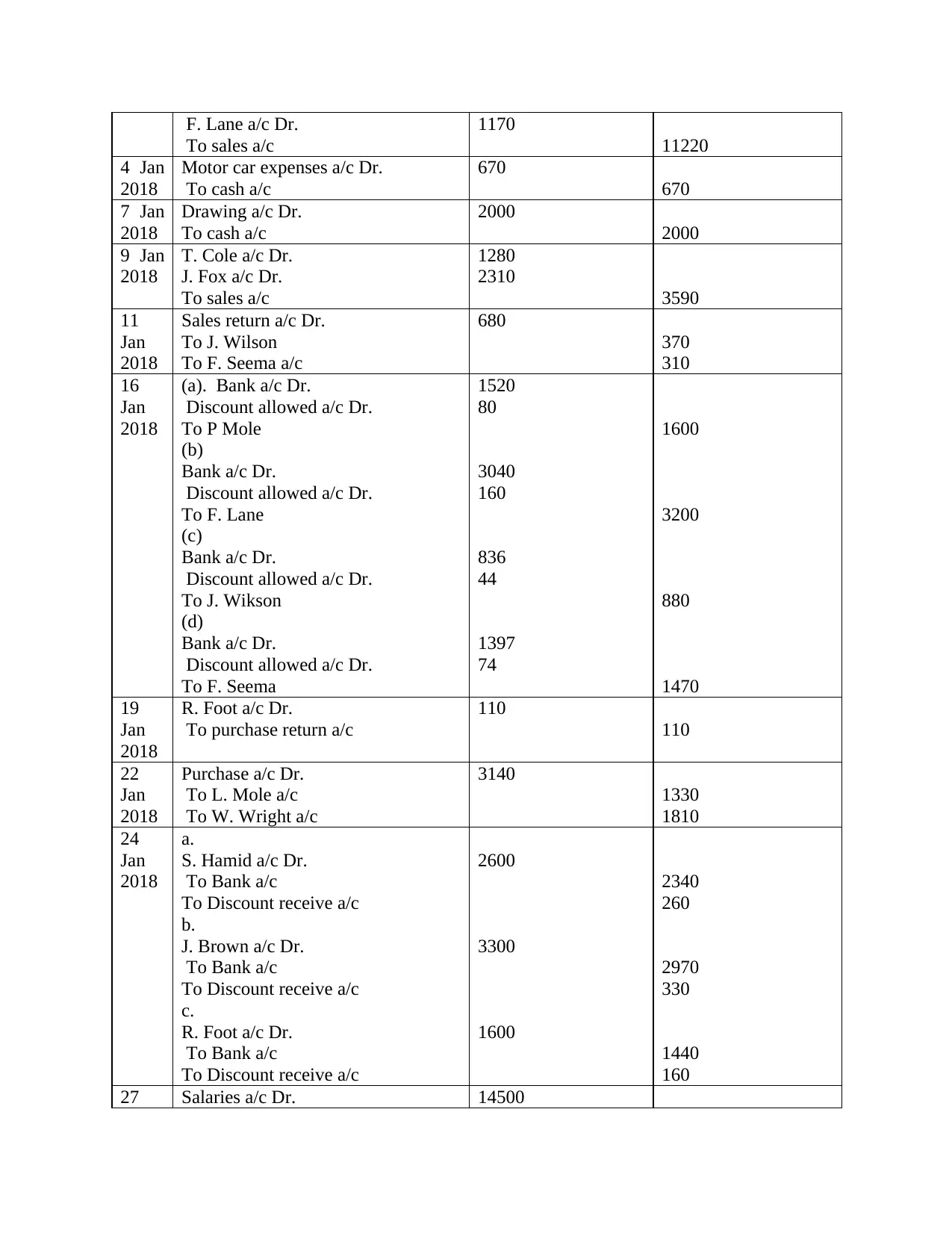

CLIENT 1

I.) Books of prime entries

Journal entries in the books of David study's for the month January is as follows-

Date Particulars Debit Credit

1st

Jan

2018

Storage expenses a/c Dr.

To bank a/c

800

800

2nd

Jan

2018

Purchase a/c Dr.

To D. Main a/c

To S. Hamid a/c

To W. Tag a/c

To R. Foot a/c

7680

2560

2450

1060

1610

3 Jan

2018

T. Cole a/c Dr.

J Wilson a/c Dr.

J. Allen a/c Dr.

F. Seema a/c Dr.

P. White a/c Dr.

2020

1840

990

2380

2820

and methods, infect entities are free to change method to prepare their financial statements. Only

reason is that company needs to provide logical reason for adopting such change. If valid reason

has been found for changing accounting principle than business must have to disclose nature of

change, its reason and effect on financial statements. It is an important concept because it

provides effective comparability by which investors and other users of company will easily able

to analyse and compare financial statements of company.

Material disclosure-

It is an accounting principle which require that management must have to report all the

relevant information regarding operations of the company to their creditors and investors in

financial statements and footnotes. It is necessary that each and every information which related

to company's business operations must be informed to creditors and investors so that they will

able to develop and analysis their investment decision of company. Material disclosure need to

be disclosed with financial statements including any supplementary footnotes and schedules.

Information also get disclosed though annual reports or with quarterly earning reports, press

releases or with any other communication technique (Clark, 2016).

CLIENT 1

I.) Books of prime entries

Journal entries in the books of David study's for the month January is as follows-

Date Particulars Debit Credit

1st

Jan

2018

Storage expenses a/c Dr.

To bank a/c

800

800

2nd

Jan

2018

Purchase a/c Dr.

To D. Main a/c

To S. Hamid a/c

To W. Tag a/c

To R. Foot a/c

7680

2560

2450

1060

1610

3 Jan

2018

T. Cole a/c Dr.

J Wilson a/c Dr.

J. Allen a/c Dr.

F. Seema a/c Dr.

P. White a/c Dr.

2020

1840

990

2380

2820

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

F. Lane a/c Dr.

To sales a/c

1170

11220

4 Jan

2018

Motor car expenses a/c Dr.

To cash a/c

670

670

7 Jan

2018

Drawing a/c Dr.

To cash a/c

2000

2000

9 Jan

2018

T. Cole a/c Dr.

J. Fox a/c Dr.

To sales a/c

1280

2310

3590

11

Jan

2018

Sales return a/c Dr.

To J. Wilson

To F. Seema a/c

680

370

310

16

Jan

2018

(a). Bank a/c Dr.

Discount allowed a/c Dr.

To P Mole

(b)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Lane

(c)

Bank a/c Dr.

Discount allowed a/c Dr.

To J. Wikson

(d)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Seema

1520

80

3040

160

836

44

1397

74

1600

3200

880

1470

19

Jan

2018

R. Foot a/c Dr.

To purchase return a/c

110

110

22

Jan

2018

Purchase a/c Dr.

To L. Mole a/c

To W. Wright a/c

3140

1330

1810

24

Jan

2018

a.

S. Hamid a/c Dr.

To Bank a/c

To Discount receive a/c

b.

J. Brown a/c Dr.

To Bank a/c

To Discount receive a/c

c.

R. Foot a/c Dr.

To Bank a/c

To Discount receive a/c

2600

3300

1600

2340

260

2970

330

1440

160

27 Salaries a/c Dr. 14500

To sales a/c

1170

11220

4 Jan

2018

Motor car expenses a/c Dr.

To cash a/c

670

670

7 Jan

2018

Drawing a/c Dr.

To cash a/c

2000

2000

9 Jan

2018

T. Cole a/c Dr.

J. Fox a/c Dr.

To sales a/c

1280

2310

3590

11

Jan

2018

Sales return a/c Dr.

To J. Wilson

To F. Seema a/c

680

370

310

16

Jan

2018

(a). Bank a/c Dr.

Discount allowed a/c Dr.

To P Mole

(b)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Lane

(c)

Bank a/c Dr.

Discount allowed a/c Dr.

To J. Wikson

(d)

Bank a/c Dr.

Discount allowed a/c Dr.

To F. Seema

1520

80

3040

160

836

44

1397

74

1600

3200

880

1470

19

Jan

2018

R. Foot a/c Dr.

To purchase return a/c

110

110

22

Jan

2018

Purchase a/c Dr.

To L. Mole a/c

To W. Wright a/c

3140

1330

1810

24

Jan

2018

a.

S. Hamid a/c Dr.

To Bank a/c

To Discount receive a/c

b.

J. Brown a/c Dr.

To Bank a/c

To Discount receive a/c

c.

R. Foot a/c Dr.

To Bank a/c

To Discount receive a/c

2600

3300

1600

2340

260

2970

330

1440

160

27 Salaries a/c Dr. 14500

Jan

2018

To bank a/c 14500

30

Jan

2018

Business rates a/c Dr

To bank a/c

2220

2220

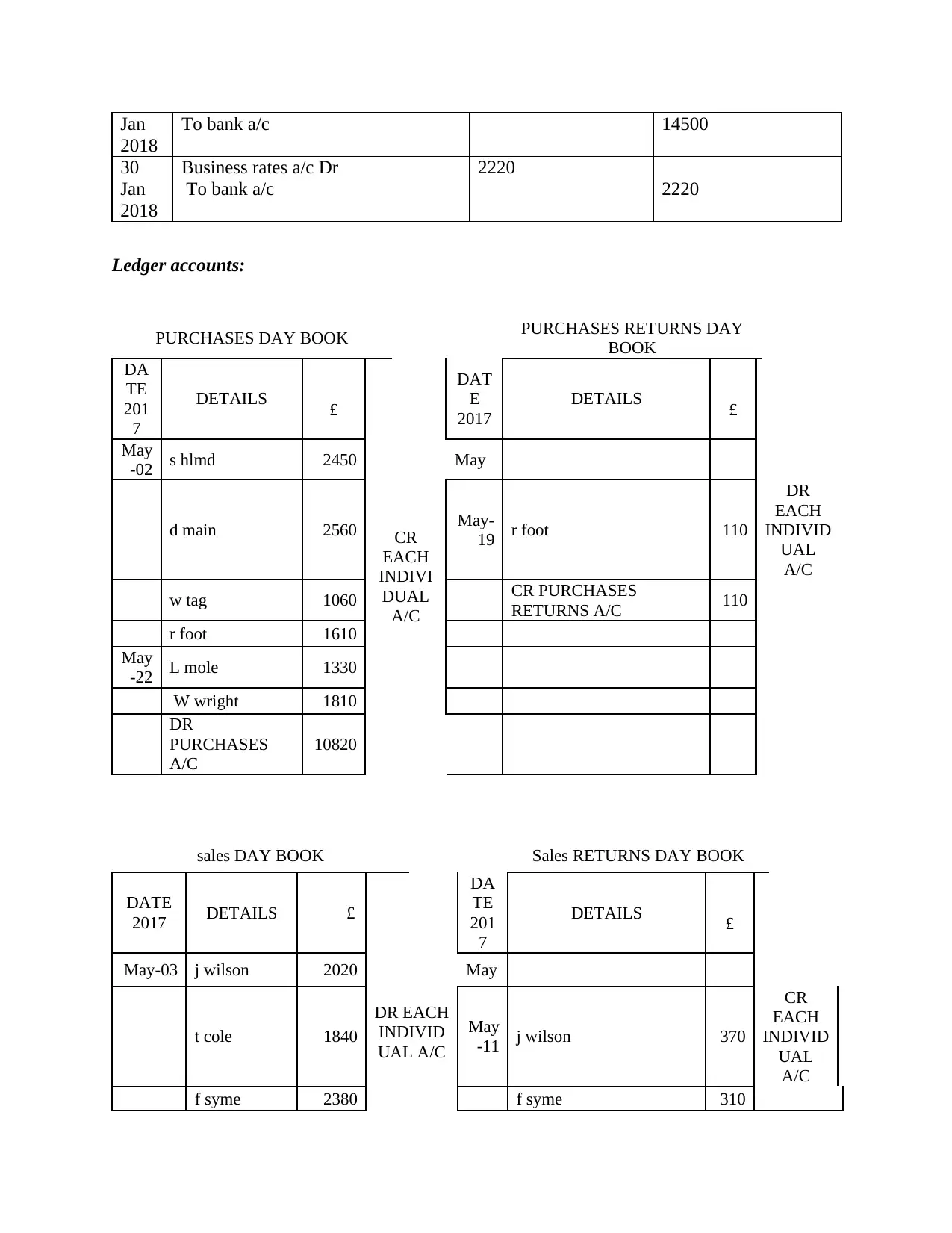

Ledger accounts:

PURCHASES DAY BOOK PURCHASES RETURNS DAY

BOOK

DA

TE

201

7

DETAILS £

DAT

E

2017

DETAILS £

May

-02 s hlmd 2450

CR

EACH

INDIVI

DUAL

A/C

May

d main 2560 May-

19 r foot 110

DR

EACH

INDIVID

UAL

A/C

w tag 1060 CR PURCHASES

RETURNS A/C 110

r foot 1610

May

-22 L mole 1330

W wright 1810

DR

PURCHASES

A/C

10820

sales DAY BOOK Sales RETURNS DAY BOOK

DATE

2017 DETAILS £

DA

TE

201

7

DETAILS £

May-03 j wilson 2020

DR EACH

INDIVID

UAL A/C

May

t cole 1840 May

-11 j wilson 370

CR

EACH

INDIVID

UAL

A/C

f syme 2380 f syme 310

2018

To bank a/c 14500

30

Jan

2018

Business rates a/c Dr

To bank a/c

2220

2220

Ledger accounts:

PURCHASES DAY BOOK PURCHASES RETURNS DAY

BOOK

DA

TE

201

7

DETAILS £

DAT

E

2017

DETAILS £

May

-02 s hlmd 2450

CR

EACH

INDIVI

DUAL

A/C

May

d main 2560 May-

19 r foot 110

DR

EACH

INDIVID

UAL

A/C

w tag 1060 CR PURCHASES

RETURNS A/C 110

r foot 1610

May

-22 L mole 1330

W wright 1810

DR

PURCHASES

A/C

10820

sales DAY BOOK Sales RETURNS DAY BOOK

DATE

2017 DETAILS £

DA

TE

201

7

DETAILS £

May-03 j wilson 2020

DR EACH

INDIVID

UAL A/C

May

t cole 1840 May

-11 j wilson 370

CR

EACH

INDIVID

UAL

A/C

f syme 2380 f syme 310

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

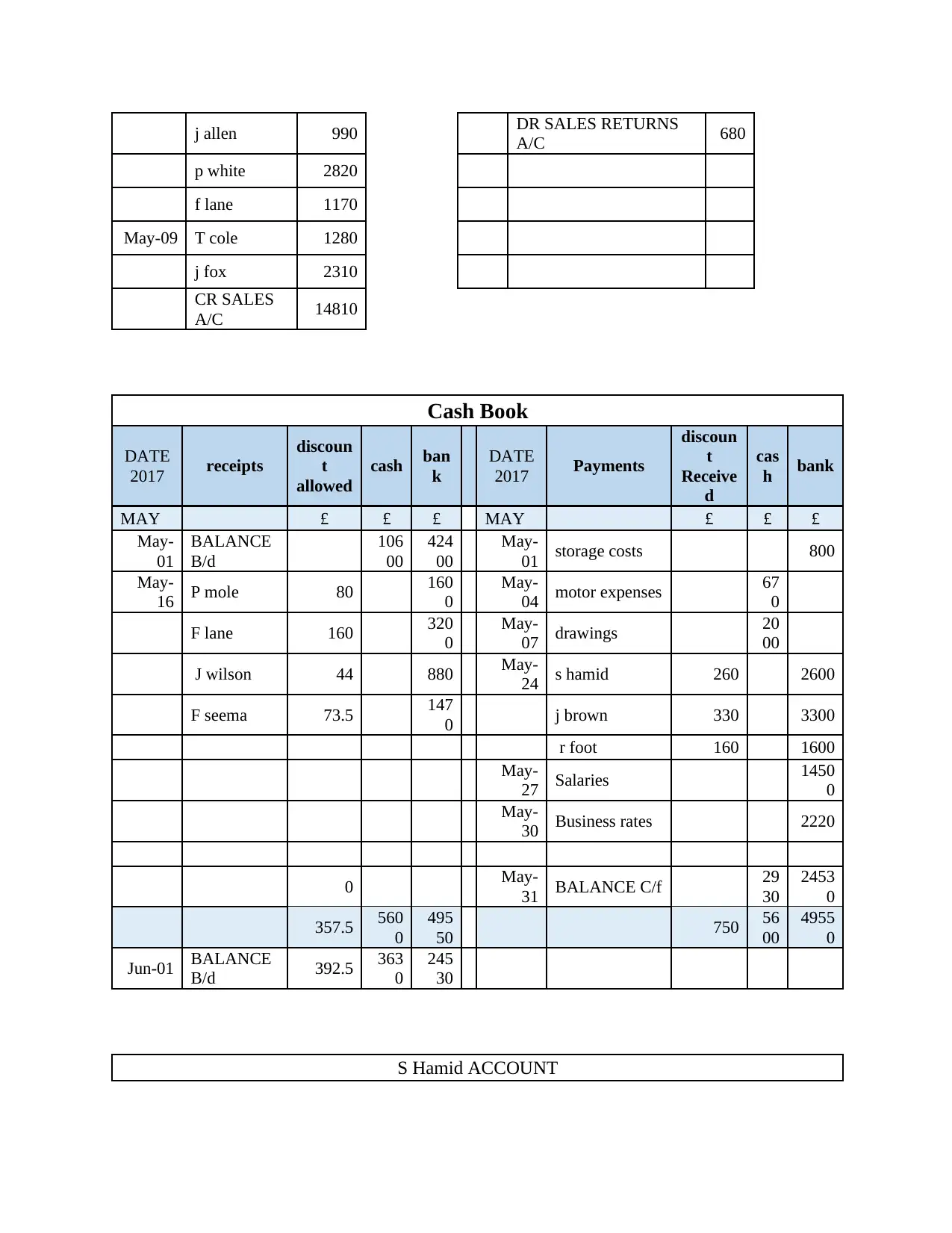

j allen 990 DR SALES RETURNS

A/C 680

p white 2820

f lane 1170

May-09 T cole 1280

j fox 2310

CR SALES

A/C 14810

Cash Book

DATE

2017 receipts

discoun

t

allowed

cash ban

k

DATE

2017 Payments

discoun

t

Receive

d

cas

h bank

MAY £ £ £ MAY £ £ £

May-

01

BALANCE

B/d

106

00

424

00

May-

01 storage costs 800

May-

16 P mole 80 160

0

May-

04 motor expenses 67

0

F lane 160 320

0

May-

07 drawings 20

00

J wilson 44 880 May-

24 s hamid 260 2600

F seema 73.5 147

0 j brown 330 3300

r foot 160 1600

May-

27 Salaries 1450

0

May-

30 Business rates 2220

0 May-

31 BALANCE C/f 29

30

2453

0

357.5 560

0

495

50 750 56

00

4955

0

Jun-01 BALANCE

B/d 392.5 363

0

245

30

S Hamid ACCOUNT

A/C 680

p white 2820

f lane 1170

May-09 T cole 1280

j fox 2310

CR SALES

A/C 14810

Cash Book

DATE

2017 receipts

discoun

t

allowed

cash ban

k

DATE

2017 Payments

discoun

t

Receive

d

cas

h bank

MAY £ £ £ MAY £ £ £

May-

01

BALANCE

B/d

106

00

424

00

May-

01 storage costs 800

May-

16 P mole 80 160

0

May-

04 motor expenses 67

0

F lane 160 320

0

May-

07 drawings 20

00

J wilson 44 880 May-

24 s hamid 260 2600

F seema 73.5 147

0 j brown 330 3300

r foot 160 1600

May-

27 Salaries 1450

0

May-

30 Business rates 2220

0 May-

31 BALANCE C/f 29

30

2453

0

357.5 560

0

495

50 750 56

00

4955

0

Jun-01 BALANCE

B/d 392.5 363

0

245

30

S Hamid ACCOUNT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

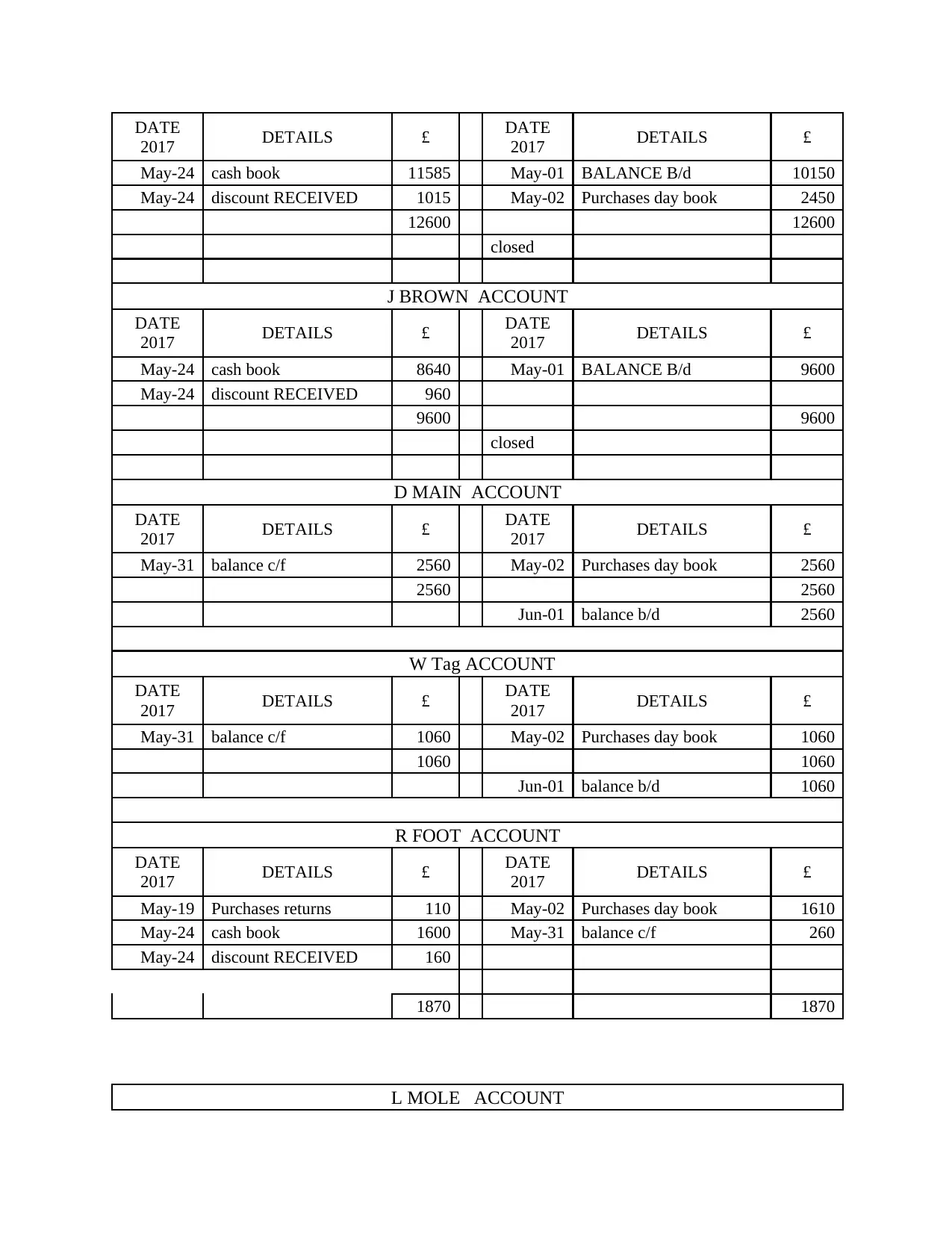

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-24 cash book 11585 May-01 BALANCE B/d 10150

May-24 discount RECEIVED 1015 May-02 Purchases day book 2450

12600 12600

closed

J BROWN ACCOUNT

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-24 cash book 8640 May-01 BALANCE B/d 9600

May-24 discount RECEIVED 960

9600 9600

closed

D MAIN ACCOUNT

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-31 balance c/f 2560 May-02 Purchases day book 2560

2560 2560

Jun-01 balance b/d 2560

W Tag ACCOUNT

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-31 balance c/f 1060 May-02 Purchases day book 1060

1060 1060

Jun-01 balance b/d 1060

R FOOT ACCOUNT

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-19 Purchases returns 110 May-02 Purchases day book 1610

May-24 cash book 1600 May-31 balance c/f 260

May-24 discount RECEIVED 160

1870 1870

L MOLE ACCOUNT

2017 DETAILS £ DATE

2017 DETAILS £

May-24 cash book 11585 May-01 BALANCE B/d 10150

May-24 discount RECEIVED 1015 May-02 Purchases day book 2450

12600 12600

closed

J BROWN ACCOUNT

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-24 cash book 8640 May-01 BALANCE B/d 9600

May-24 discount RECEIVED 960

9600 9600

closed

D MAIN ACCOUNT

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-31 balance c/f 2560 May-02 Purchases day book 2560

2560 2560

Jun-01 balance b/d 2560

W Tag ACCOUNT

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-31 balance c/f 1060 May-02 Purchases day book 1060

1060 1060

Jun-01 balance b/d 1060

R FOOT ACCOUNT

DATE

2017 DETAILS £ DATE

2017 DETAILS £

May-19 Purchases returns 110 May-02 Purchases day book 1610

May-24 cash book 1600 May-31 balance c/f 260

May-24 discount RECEIVED 160

1870 1870

L MOLE ACCOUNT

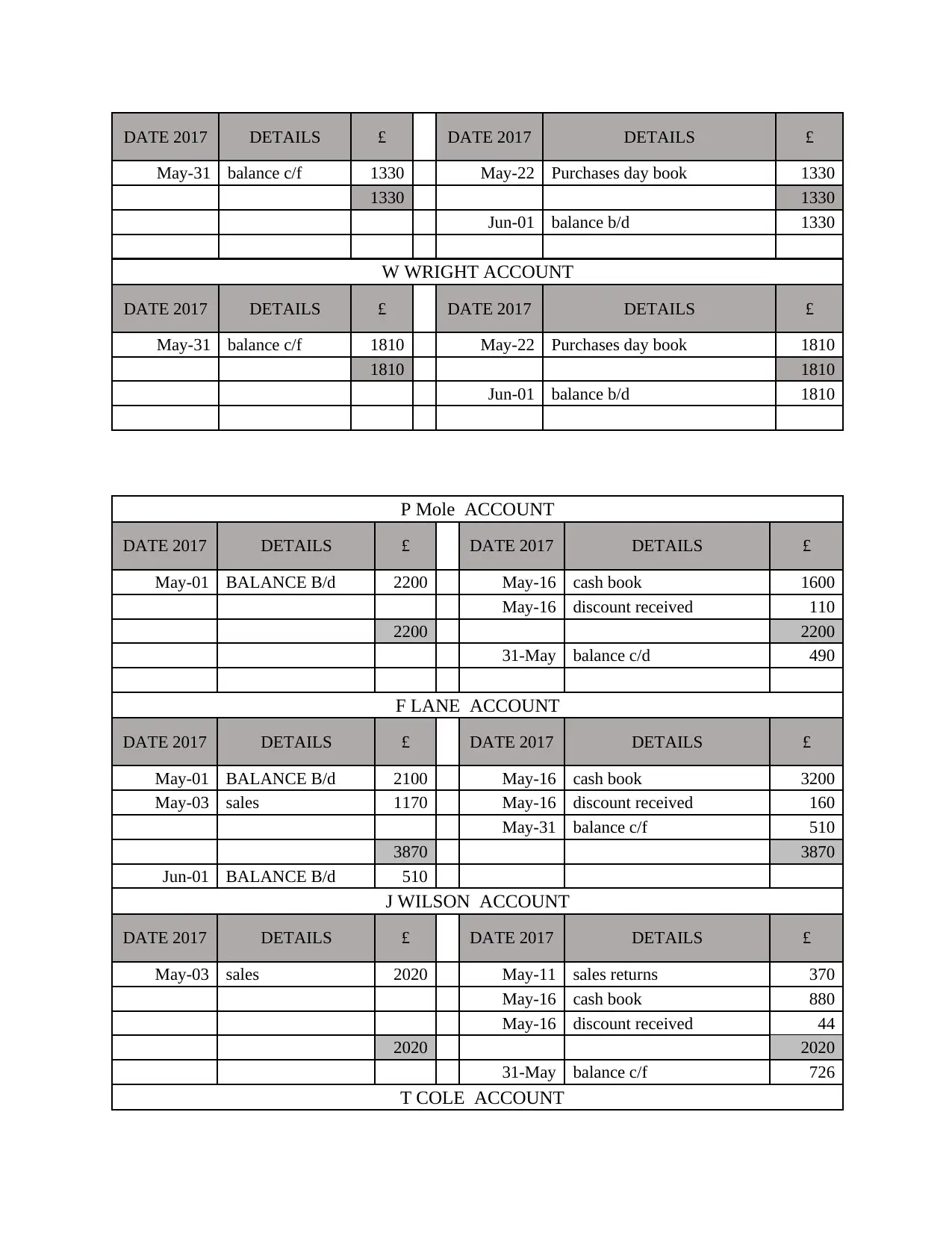

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-31 balance c/f 1330 May-22 Purchases day book 1330

1330 1330

Jun-01 balance b/d 1330

W WRIGHT ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-31 balance c/f 1810 May-22 Purchases day book 1810

1810 1810

Jun-01 balance b/d 1810

P Mole ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-01 BALANCE B/d 2200 May-16 cash book 1600

May-16 discount received 110

2200 2200

31-May balance c/d 490

F LANE ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-01 BALANCE B/d 2100 May-16 cash book 3200

May-03 sales 1170 May-16 discount received 160

May-31 balance c/f 510

3870 3870

Jun-01 BALANCE B/d 510

J WILSON ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-03 sales 2020 May-11 sales returns 370

May-16 cash book 880

May-16 discount received 44

2020 2020

31-May balance c/f 726

T COLE ACCOUNT

May-31 balance c/f 1330 May-22 Purchases day book 1330

1330 1330

Jun-01 balance b/d 1330

W WRIGHT ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-31 balance c/f 1810 May-22 Purchases day book 1810

1810 1810

Jun-01 balance b/d 1810

P Mole ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-01 BALANCE B/d 2200 May-16 cash book 1600

May-16 discount received 110

2200 2200

31-May balance c/d 490

F LANE ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-01 BALANCE B/d 2100 May-16 cash book 3200

May-03 sales 1170 May-16 discount received 160

May-31 balance c/f 510

3870 3870

Jun-01 BALANCE B/d 510

J WILSON ACCOUNT

DATE 2017 DETAILS £ DATE 2017 DETAILS £

May-03 sales 2020 May-11 sales returns 370

May-16 cash book 880

May-16 discount received 44

2020 2020

31-May balance c/f 726

T COLE ACCOUNT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.