Financial Accounting Principles Report

VerifiedAdded on 2020/10/23

|20

|4019

|483

Report

AI Summary

This report delves into the principles of financial accounting, outlining its purpose, regulations, and essential accounting rules. It discusses various financial statements, including cash flow statements, income statements, and balance sheets, while also addressing the importance of adhering to accounting standards such as IFRS and IASB. The report includes practical examples and client case studies to illustrate the application of these principles in real-world scenarios.

Financial accounting

principles

principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

(A) REPORT....................................................................................................................................1

1. Financial accounting and its purpose......................................................................................1

2: The regulations relating to financial accounting.....................................................................2

3: Accounting rules and principles..............................................................................................3

4: Conventions and concepts related to consistency and materiel disclosure.............................5

CLIENT 1........................................................................................................................................5

CLIENT 2........................................................................................................................................8

CLIENT 3........................................................................................................................................9

CLIENT 4......................................................................................................................................13

CLIENT 5......................................................................................................................................14

CLIENT 6......................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

(A) REPORT....................................................................................................................................1

1. Financial accounting and its purpose......................................................................................1

2: The regulations relating to financial accounting.....................................................................2

3: Accounting rules and principles..............................................................................................3

4: Conventions and concepts related to consistency and materiel disclosure.............................5

CLIENT 1........................................................................................................................................5

CLIENT 2........................................................................................................................................8

CLIENT 3........................................................................................................................................9

CLIENT 4......................................................................................................................................13

CLIENT 5......................................................................................................................................14

CLIENT 6......................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is a process of preparing financial statements using few principles

and concepts. These principles are generally accepted by every organisation regardless of its

size, scope and nature of the business operations. In this project report, various financial

concepts and conventions are discussed along with the rules and regulations which needs to be

followed by the organisation. The main aim of this report is to incorporate all accounting

techniques and principles along with providing solutions for the issues of various clients

mentioned below. Journal entries, trial balance and financial statements are prepared along with

suspense account and bank reconciliation statement to provide an answer for all the clients

questions. Bank reconciliation statement is a rectification account where deviation between cash

and pass book are resolved by stating reason of there deviation. Book keeping system and

suspense accounts are also defined in this report.

(A) REPORT

1. Financial accounting and its purpose

Financial accounting:

Financial management plays a crucial role in an organization by preparing an effective

financial accounting plans and managing as well as allocating funds to different business

functions with an expectation of getting profitable outcomes in near future. It defines the

important elements related with financial accounting concepts and accounting rules. Financial

accounting represents the actual financial position of company which enable finance manager to

make further corrective actions and plans for the purpose of improving financial growth of

business organisation. There is a need for company to analyse their financial stability on

particular time period. The main purpose of using financial accounting is to manage and control

financial information in an appropriate manner so as to utilise financial resources in profitable

manner. There are different types of financial accounts which need to be prepared by an

organisation so as to identify their true and fair financial position of company (Baker, 2012).

Such types of financial accounts are briefly described under the below:

Cash flow statement: In this statement, all the cash transactions are recorded on regular

basis so as to know cash inflow and outflow of an organisation. There are mainly three types of

cash expenditure and income which includes cash flow operations, cash flow from investing and

1

Financial accounting is a process of preparing financial statements using few principles

and concepts. These principles are generally accepted by every organisation regardless of its

size, scope and nature of the business operations. In this project report, various financial

concepts and conventions are discussed along with the rules and regulations which needs to be

followed by the organisation. The main aim of this report is to incorporate all accounting

techniques and principles along with providing solutions for the issues of various clients

mentioned below. Journal entries, trial balance and financial statements are prepared along with

suspense account and bank reconciliation statement to provide an answer for all the clients

questions. Bank reconciliation statement is a rectification account where deviation between cash

and pass book are resolved by stating reason of there deviation. Book keeping system and

suspense accounts are also defined in this report.

(A) REPORT

1. Financial accounting and its purpose

Financial accounting:

Financial management plays a crucial role in an organization by preparing an effective

financial accounting plans and managing as well as allocating funds to different business

functions with an expectation of getting profitable outcomes in near future. It defines the

important elements related with financial accounting concepts and accounting rules. Financial

accounting represents the actual financial position of company which enable finance manager to

make further corrective actions and plans for the purpose of improving financial growth of

business organisation. There is a need for company to analyse their financial stability on

particular time period. The main purpose of using financial accounting is to manage and control

financial information in an appropriate manner so as to utilise financial resources in profitable

manner. There are different types of financial accounts which need to be prepared by an

organisation so as to identify their true and fair financial position of company (Baker, 2012).

Such types of financial accounts are briefly described under the below:

Cash flow statement: In this statement, all the cash transactions are recorded on regular

basis so as to know cash inflow and outflow of an organisation. There are mainly three types of

cash expenditure and income which includes cash flow operations, cash flow from investing and

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cash flow from financial activity. The transactions which are made in monetary terms are only

recorded in cash flow statement.

Income and expenditure account: It is an account which is essential to prepare in order

to calculate net profit and loss of organisation. All the expenses incurred and income earned are

recorded in such statement. It enables manager to determine the actual profitability of an

organisation through preparing profit and loss account. It is prepared on annual basis which

clearly shows the net financial position of company (Bayou, 2011).

Financial position statement: This statement is also called as balance sheet which

includes all assets and liabilities of an organisation. It shows the direct relation found in of assets

and liabilities within an organisation due to which the value of an organisation are easily

identified and determined. Fixed asset, liabilities, non-current liabilities, capital expenditure and

current liabilities are the parts of financial position statement.

Change in equity statement: It is another effective statement which helps in managing

the financial accounts and information associated with capital structure of an organisation. There

is a overall capital equity structure of an organisation. There are different types of financial

components and management functions which are remain attached with the fluctuations in

equities and share capital of an organisation (Brown, 2011).

2: The regulations relating to financial accounting

There are specific regulations and standards which are essential to follow while making

an accounting report for an organisation. Finance managers are held liable to overview the rules

and regulations associated with financial accounting. There are several financial accounting

regulations which help in analysing and controlling the procedure of financial reporting. Such

financial accounting regulations are given as below:

IASB

It is an international body which is established in order to control and manage framework

of financial reporting and recording for an companies, individuals and group of associations.

Such authority contains the rules and structure to record and retain the data in more systematic

and informative manner (Donelson, 2012).

IFRS

It is also another regulatory body which provides financial plans and procedures for the

purpose of retaining financial detail and maximum utilisation of financial rules so as to make

2

recorded in cash flow statement.

Income and expenditure account: It is an account which is essential to prepare in order

to calculate net profit and loss of organisation. All the expenses incurred and income earned are

recorded in such statement. It enables manager to determine the actual profitability of an

organisation through preparing profit and loss account. It is prepared on annual basis which

clearly shows the net financial position of company (Bayou, 2011).

Financial position statement: This statement is also called as balance sheet which

includes all assets and liabilities of an organisation. It shows the direct relation found in of assets

and liabilities within an organisation due to which the value of an organisation are easily

identified and determined. Fixed asset, liabilities, non-current liabilities, capital expenditure and

current liabilities are the parts of financial position statement.

Change in equity statement: It is another effective statement which helps in managing

the financial accounts and information associated with capital structure of an organisation. There

is a overall capital equity structure of an organisation. There are different types of financial

components and management functions which are remain attached with the fluctuations in

equities and share capital of an organisation (Brown, 2011).

2: The regulations relating to financial accounting

There are specific regulations and standards which are essential to follow while making

an accounting report for an organisation. Finance managers are held liable to overview the rules

and regulations associated with financial accounting. There are several financial accounting

regulations which help in analysing and controlling the procedure of financial reporting. Such

financial accounting regulations are given as below:

IASB

It is an international body which is established in order to control and manage framework

of financial reporting and recording for an companies, individuals and group of associations.

Such authority contains the rules and structure to record and retain the data in more systematic

and informative manner (Donelson, 2012).

IFRS

It is also another regulatory body which provides financial plans and procedures for the

purpose of retaining financial detail and maximum utilisation of financial rules so as to make

2

better formation and control. It is also known as quality management tool which assist finance

manager to organise department in such an effective manner that will help in utilising financial

resources in particular areas of department. Rules of IFRS are given as under:

FRS 1: This rule contains rules and standard regarding preparation of cash flows from

three activities which includes operating, investing and financial activities. It also provides a

systematic structure for tax treatment.

FRS 3: Such rule produces information regarding the treatment made related with loss

and profits for future period of time. The financial performance of company are properly

evaluated on the basis of various components which are determined as under:

Records associated with analysing the revenue from discontinued business operations.

Results which are considered for exchanging the information within operations (Fourie, 2015).

3: Accounting rules and principles

Accounting rules:

Accounting is the activity which is done with the following of certain standards and rules

so as to prepare accurate and reliable financial statements. Such rules are listed under the below:

Debit the receiver, credit the giver: Such rule is mainly applied in case of personal

account which deals with an person or an individual.. As per the rule, when one party provide

resources to another party on credit then such given party is called as debtor and the receiver of

resources is called as creditor.

Debit all expenses and losses, credit all income and gains: Such rule is mainly follow

din case of nominal accounts which are related with fictions accounts associated with various

expenditures, losses, revenues, income etc. As per the rule, all the expenses incurred by an

organisation are recorded as debits transaction whereas all the income earned on particular

transactions are recorded as credit.

Debit what comes in, credit what goes out: This is the rule which is mainly used in case

of real accounts. Such account is related with the assets such as building, goodwill, machinery

account etc. As per the rule, if the assets of an organisation are increased or acquired then it will

recorded as debit transactions. Same wise if the assets are sold or decreased then it will be treated

as credit transactions (Francis, 2015).

Accounting Principles

3

manager to organise department in such an effective manner that will help in utilising financial

resources in particular areas of department. Rules of IFRS are given as under:

FRS 1: This rule contains rules and standard regarding preparation of cash flows from

three activities which includes operating, investing and financial activities. It also provides a

systematic structure for tax treatment.

FRS 3: Such rule produces information regarding the treatment made related with loss

and profits for future period of time. The financial performance of company are properly

evaluated on the basis of various components which are determined as under:

Records associated with analysing the revenue from discontinued business operations.

Results which are considered for exchanging the information within operations (Fourie, 2015).

3: Accounting rules and principles

Accounting rules:

Accounting is the activity which is done with the following of certain standards and rules

so as to prepare accurate and reliable financial statements. Such rules are listed under the below:

Debit the receiver, credit the giver: Such rule is mainly applied in case of personal

account which deals with an person or an individual.. As per the rule, when one party provide

resources to another party on credit then such given party is called as debtor and the receiver of

resources is called as creditor.

Debit all expenses and losses, credit all income and gains: Such rule is mainly follow

din case of nominal accounts which are related with fictions accounts associated with various

expenditures, losses, revenues, income etc. As per the rule, all the expenses incurred by an

organisation are recorded as debits transaction whereas all the income earned on particular

transactions are recorded as credit.

Debit what comes in, credit what goes out: This is the rule which is mainly used in case

of real accounts. Such account is related with the assets such as building, goodwill, machinery

account etc. As per the rule, if the assets of an organisation are increased or acquired then it will

recorded as debit transactions. Same wise if the assets are sold or decreased then it will be treated

as credit transactions (Francis, 2015).

Accounting Principles

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principle of conservatism: It is the concept which states that the expenses and liabilities

are recognised as soon as possible even there is uncertainty about receiving outcomes but the

revenues and assets are recognised when the company are assured of bring received.

Cost principle: It refers to such accounting principle which states that the all the assets,

liabilities and equity investment of an organisation should required to be recorded at their

original or acquisition cost in financial statements. It is also known as historical cost principle

due to recording at historical cost instead of incremental cost.

Going concern: As per such principle, accountants makes assumptions that an

organisation will continue its business operations for nest accounting period despite of any issues

or policies. On the basis of such assumptions, the company can able to buy inventory o0n credit

with an intention of repay in future time period (Hale, 2011).

Monetary Unit: According to this principle, all the transactions must be recorded in

monetary terms. For example, purchasing of raw materiel must required to be recorded with their

monetary amount and should not on the basis of barter system or any other exchange method.

Full disclosure: Such accounting principle states that all the transactions made by an

organisation are properly recoded under financial statement will full descriptions associated with

such transaction. If information are nit disclosed with the recorded transactions then it be

mentioned under head of foot note of financial statements.

Matching principle: Such principle states that income statement should required to be

prepared under financial statements which includes revenues and expenses and these both should

be equal. All the expenses and income must be match with each other so as to gain or bear profit

or loss.

Revenue recognition principle: Such principle is mainly used in accrue transactions in

which the transaction has been recorded when it is made not when the outcome has been

received. For example, revenue is recorded when the goods are sold or service is rendered

regardless that a payment is not received yet (McEnroe, 2013).

Materiality: As per such principle, all the relevant and useful information should required

to be recorded. The irrelevant and immaterial information should be ignored.

Time period and assumption principle: It states that all the transactions are recorded in

financial statement with the time allotted to complete such transactions. Such financial statement

is prepared on annual basis.

4

are recognised as soon as possible even there is uncertainty about receiving outcomes but the

revenues and assets are recognised when the company are assured of bring received.

Cost principle: It refers to such accounting principle which states that the all the assets,

liabilities and equity investment of an organisation should required to be recorded at their

original or acquisition cost in financial statements. It is also known as historical cost principle

due to recording at historical cost instead of incremental cost.

Going concern: As per such principle, accountants makes assumptions that an

organisation will continue its business operations for nest accounting period despite of any issues

or policies. On the basis of such assumptions, the company can able to buy inventory o0n credit

with an intention of repay in future time period (Hale, 2011).

Monetary Unit: According to this principle, all the transactions must be recorded in

monetary terms. For example, purchasing of raw materiel must required to be recorded with their

monetary amount and should not on the basis of barter system or any other exchange method.

Full disclosure: Such accounting principle states that all the transactions made by an

organisation are properly recoded under financial statement will full descriptions associated with

such transaction. If information are nit disclosed with the recorded transactions then it be

mentioned under head of foot note of financial statements.

Matching principle: Such principle states that income statement should required to be

prepared under financial statements which includes revenues and expenses and these both should

be equal. All the expenses and income must be match with each other so as to gain or bear profit

or loss.

Revenue recognition principle: Such principle is mainly used in accrue transactions in

which the transaction has been recorded when it is made not when the outcome has been

received. For example, revenue is recorded when the goods are sold or service is rendered

regardless that a payment is not received yet (McEnroe, 2013).

Materiality: As per such principle, all the relevant and useful information should required

to be recorded. The irrelevant and immaterial information should be ignored.

Time period and assumption principle: It states that all the transactions are recorded in

financial statement with the time allotted to complete such transactions. Such financial statement

is prepared on annual basis.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Economic entity assumption: Such principle states to assume that an organisation has

different identify from their owner. It is most suitable principle for company due to having lots

of owners which are called as shareholders (Muller, 2011).

4: Conventions and concepts related to consistency and materiel disclosure

Accounting is an important activity which is essential to be done in order to identify true

and fair financial position of company. It can be done through preparing financial statements

such as profit & loss account, cash floe statement, balance sheet etc. In these, transactions are

recorded on the basis of various concepts and conventions which are given as below:

Consistency concept: Such concept is based on an assumptions that the business are

operated in market on consistent basis regardless of different policies and issues which are based

by them. On the basis of such assumptions, the company can transfer goods to other parties on

credit with an expectation of getting repayment in near future (Narayanaswamy, 2017).

Material Disclosure: According to such concept, all the material or important transaction

s should be recorded in brief description and should ignore irrelevant or immaterial information.

Accrual concept: It is another fundamental concept which states that all the revenues are

recorded when they are actually received in cash and all the expenses to be recorded when

actually paid in cash.

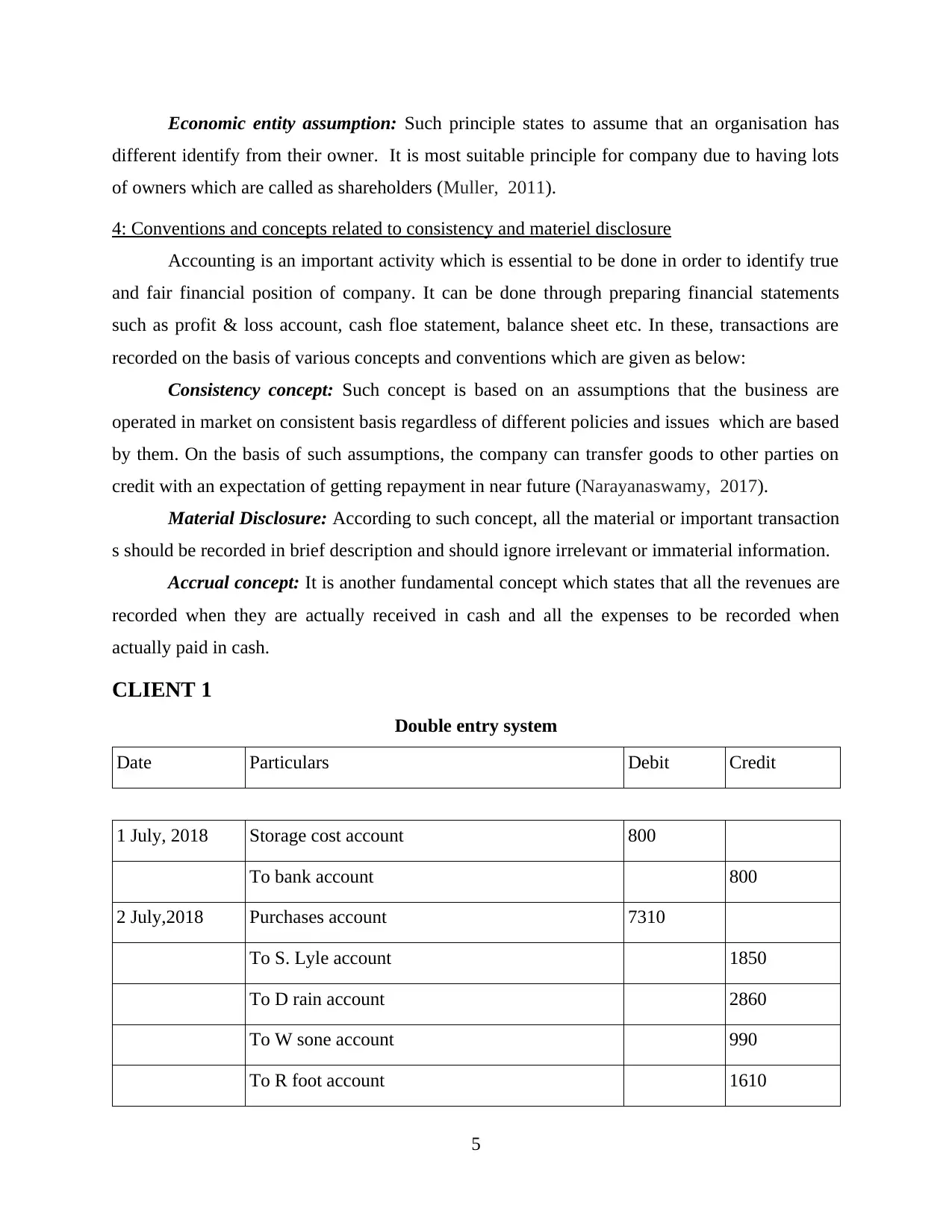

CLIENT 1

Double entry system

Date Particulars Debit Credit

1 July, 2018 Storage cost account 800

To bank account 800

2 July,2018 Purchases account 7310

To S. Lyle account 1850

To D rain account 2860

To W sone account 990

To R foot account 1610

5

different identify from their owner. It is most suitable principle for company due to having lots

of owners which are called as shareholders (Muller, 2011).

4: Conventions and concepts related to consistency and materiel disclosure

Accounting is an important activity which is essential to be done in order to identify true

and fair financial position of company. It can be done through preparing financial statements

such as profit & loss account, cash floe statement, balance sheet etc. In these, transactions are

recorded on the basis of various concepts and conventions which are given as below:

Consistency concept: Such concept is based on an assumptions that the business are

operated in market on consistent basis regardless of different policies and issues which are based

by them. On the basis of such assumptions, the company can transfer goods to other parties on

credit with an expectation of getting repayment in near future (Narayanaswamy, 2017).

Material Disclosure: According to such concept, all the material or important transaction

s should be recorded in brief description and should ignore irrelevant or immaterial information.

Accrual concept: It is another fundamental concept which states that all the revenues are

recorded when they are actually received in cash and all the expenses to be recorded when

actually paid in cash.

CLIENT 1

Double entry system

Date Particulars Debit Credit

1 July, 2018 Storage cost account 800

To bank account 800

2 July,2018 Purchases account 7310

To S. Lyle account 1850

To D rain account 2860

To W sone account 990

To R foot account 1610

5

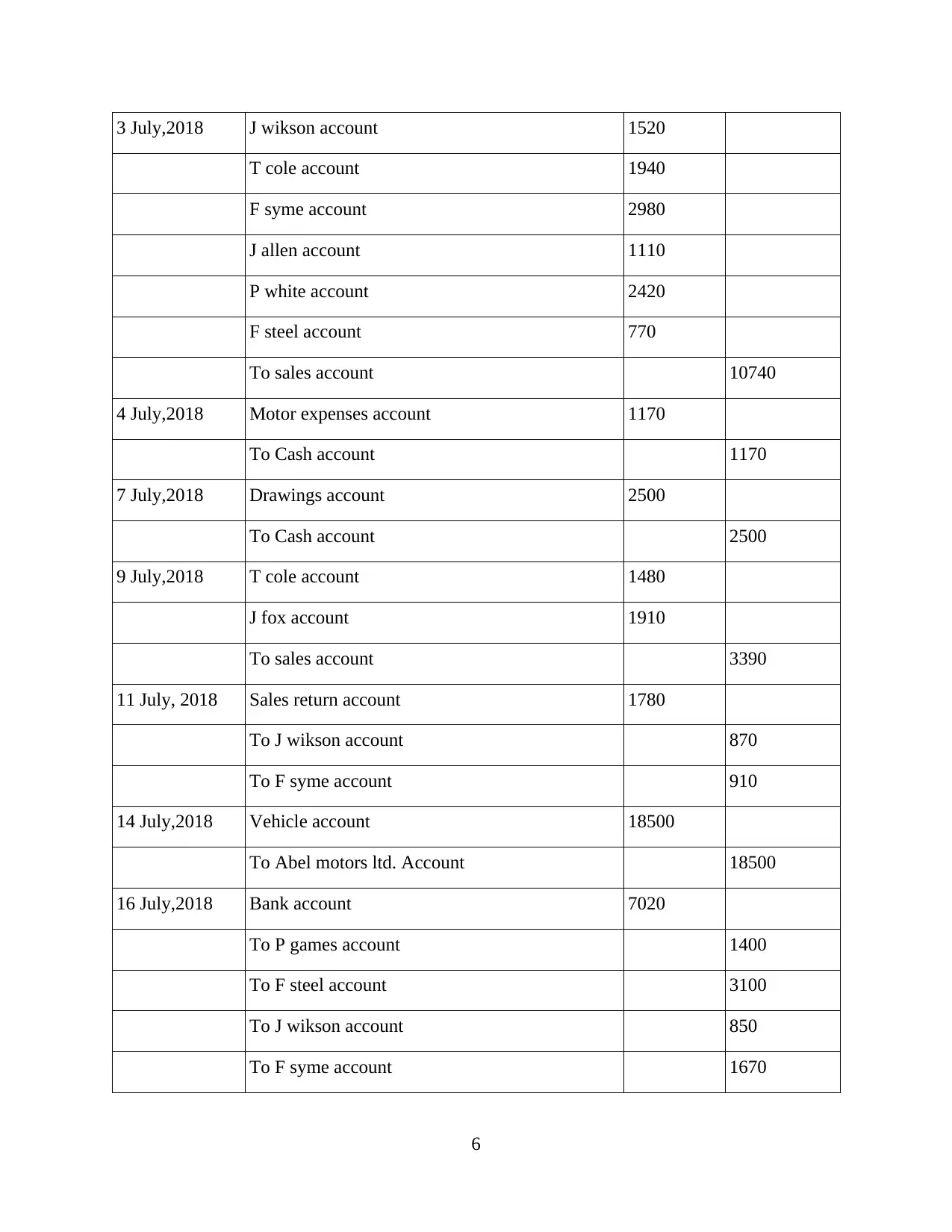

3 July,2018 J wikson account 1520

T cole account 1940

F syme account 2980

J allen account 1110

P white account 2420

F steel account 770

To sales account 10740

4 July,2018 Motor expenses account 1170

To Cash account 1170

7 July,2018 Drawings account 2500

To Cash account 2500

9 July,2018 T cole account 1480

J fox account 1910

To sales account 3390

11 July, 2018 Sales return account 1780

To J wikson account 870

To F syme account 910

14 July,2018 Vehicle account 18500

To Abel motors ltd. Account 18500

16 July,2018 Bank account 7020

To P games account 1400

To F steel account 3100

To J wikson account 850

To F syme account 1670

6

T cole account 1940

F syme account 2980

J allen account 1110

P white account 2420

F steel account 770

To sales account 10740

4 July,2018 Motor expenses account 1170

To Cash account 1170

7 July,2018 Drawings account 2500

To Cash account 2500

9 July,2018 T cole account 1480

J fox account 1910

To sales account 3390

11 July, 2018 Sales return account 1780

To J wikson account 870

To F syme account 910

14 July,2018 Vehicle account 18500

To Abel motors ltd. Account 18500

16 July,2018 Bank account 7020

To P games account 1400

To F steel account 3100

To J wikson account 850

To F syme account 1670

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

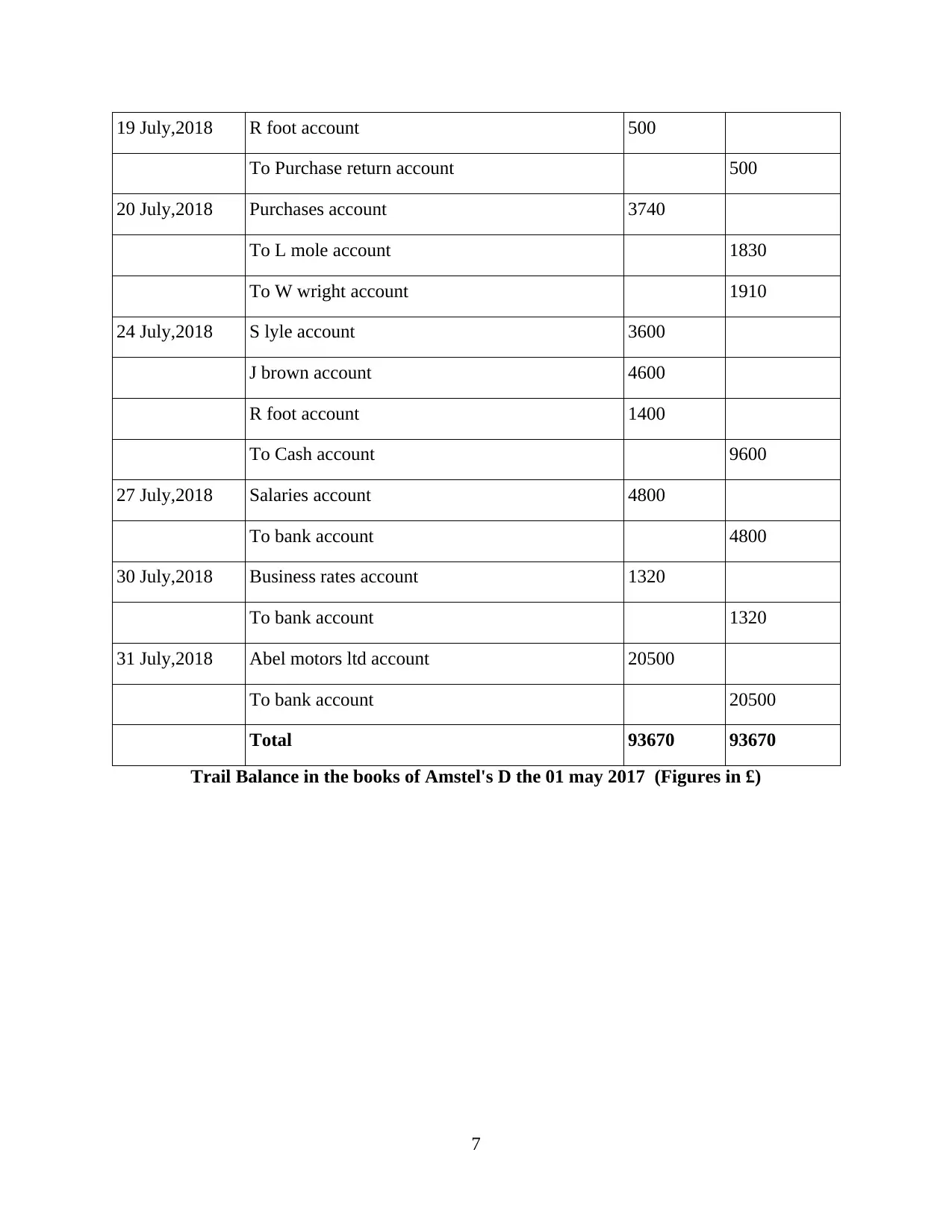

19 July,2018 R foot account 500

To Purchase return account 500

20 July,2018 Purchases account 3740

To L mole account 1830

To W wright account 1910

24 July,2018 S lyle account 3600

J brown account 4600

R foot account 1400

To Cash account 9600

27 July,2018 Salaries account 4800

To bank account 4800

30 July,2018 Business rates account 1320

To bank account 1320

31 July,2018 Abel motors ltd account 20500

To bank account 20500

Total 93670 93670

Trail Balance in the books of Amstel's D the 01 may 2017 (Figures in £)

7

To Purchase return account 500

20 July,2018 Purchases account 3740

To L mole account 1830

To W wright account 1910

24 July,2018 S lyle account 3600

J brown account 4600

R foot account 1400

To Cash account 9600

27 July,2018 Salaries account 4800

To bank account 4800

30 July,2018 Business rates account 1320

To bank account 1320

31 July,2018 Abel motors ltd account 20500

To bank account 20500

Total 93670 93670

Trail Balance in the books of Amstel's D the 01 may 2017 (Figures in £)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

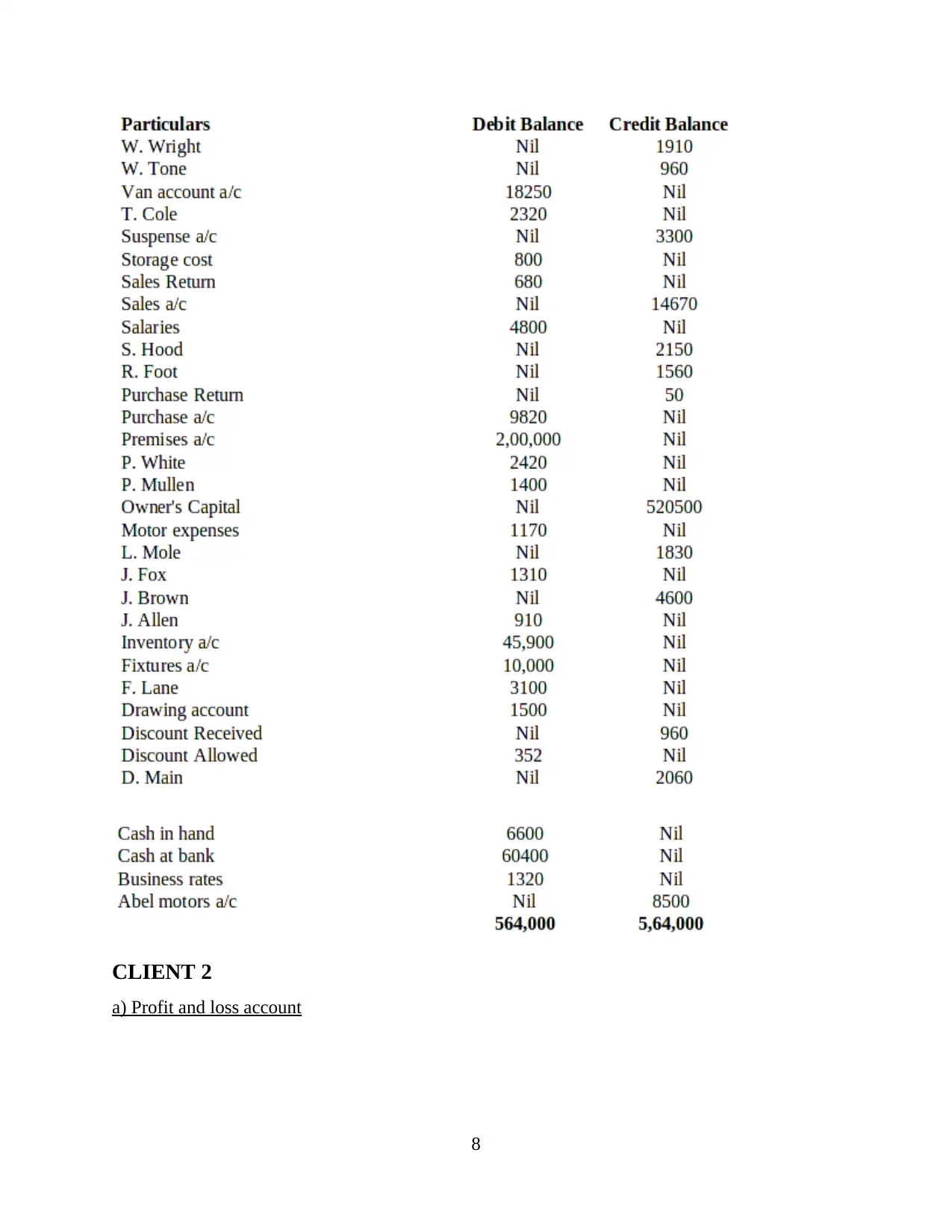

CLIENT 2

a) Profit and loss account

8

a) Profit and loss account

8

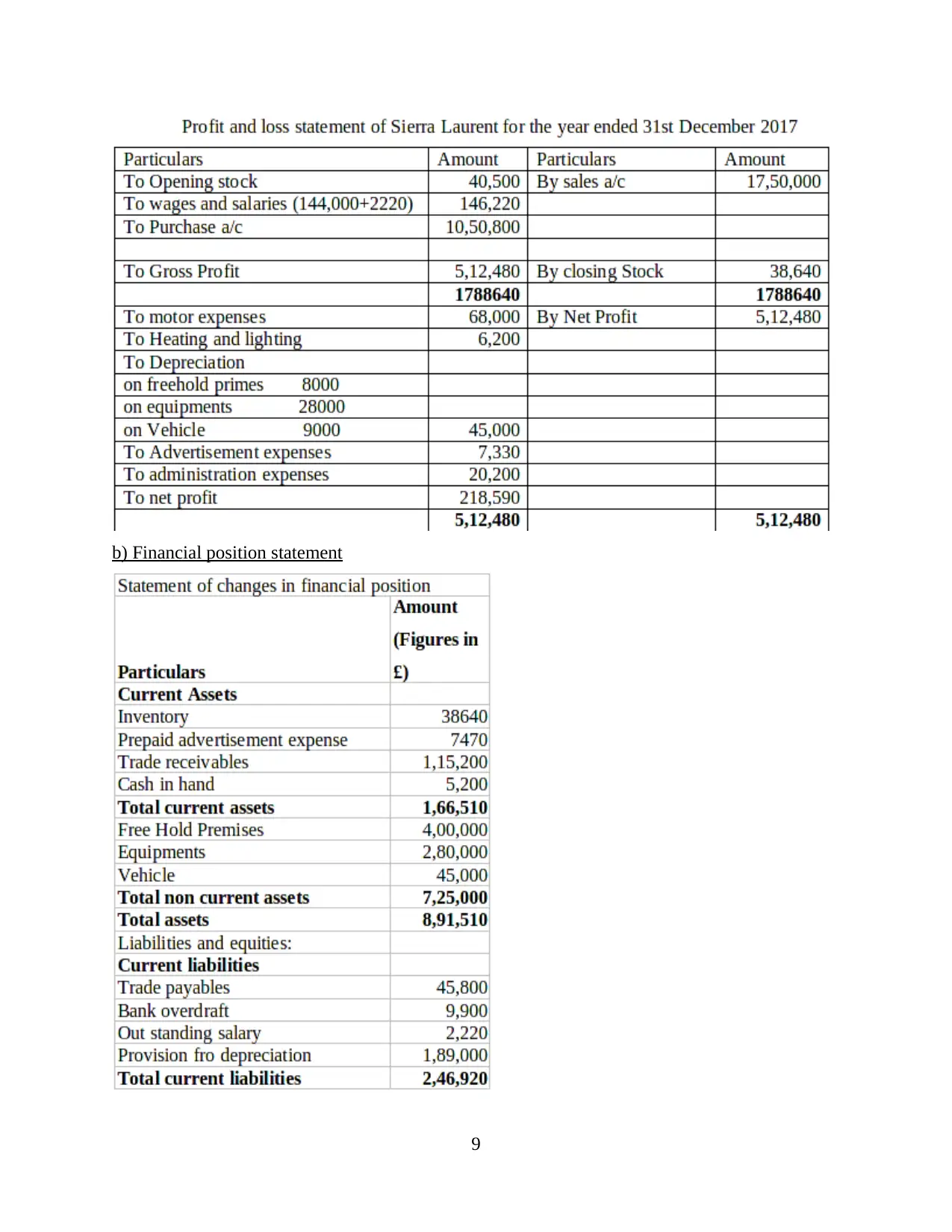

b) Financial position statement

9

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.