Financial Accounting Principles Report: Client Analysis and Accounting

VerifiedAdded on 2020/10/22

|30

|7212

|286

Report

AI Summary

This comprehensive report delves into the core principles of financial accounting, exploring its purpose, relevant regulations, and the Generally Accepted Accounting Principles (GAAP) that govern financial statement preparation. The report examines accounting rules, conventions, and concepts such as consistency and material disclosure. It includes detailed analyses of various client scenarios, encompassing journal entries, ledger accounts, trial balances, profit and loss statements, balance sheets, bank reconciliation statements, and control accounts. The report also addresses key accounting concepts like the dual aspect concept, cost principle, and matching concept, providing a thorough understanding of financial accounting practices. Furthermore, it discusses the importance of accounting conventions, particularly consistency and material disclosure, and their impact on financial reporting. The report offers practical examples and explanations, making it a valuable resource for students studying financial accounting.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

1. Financial accounting and it's purpose......................................................................................1

2. Explain regulations related to Financial accounting................................................................2

3. Describe accounting rules and principles................................................................................3

4. Explain conventions and it's concept consistency & material disclosure................................4

CLIENT 1........................................................................................................................................4

(a) Preparation of Journal Entries in books of David Study........................................................4

(b) Ledger Accounts of David Study's financial statements........................................................7

(c) Trial balance of David Study as on 31st January 2018........................................................14

CLIENT 2 .....................................................................................................................................16

(a) Statement of profit and loss account....................................................................................16

(b) Statement of financial position of Peter Hampau as at 31st July 2018................................16

CLIENT 3......................................................................................................................................18

(a) Profit and loss account of Bowling Limited.........................................................................18

(b) Balance sheet of Bowling Limited.......................................................................................18

....................................................................................................................................................19

(c) Accounting concepts of Consistency and Prudency.............................................................19

(d) Purpose of depreciation and its methods..............................................................................20

CLIENT 4......................................................................................................................................21

(A) Bank Reconciliation Statement...........................................................................................21

(B) Prepare Durrell Ltd's updated cash book for December 2017.............................................21

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

1. Financial accounting and it's purpose......................................................................................1

2. Explain regulations related to Financial accounting................................................................2

3. Describe accounting rules and principles................................................................................3

4. Explain conventions and it's concept consistency & material disclosure................................4

CLIENT 1........................................................................................................................................4

(a) Preparation of Journal Entries in books of David Study........................................................4

(b) Ledger Accounts of David Study's financial statements........................................................7

(c) Trial balance of David Study as on 31st January 2018........................................................14

CLIENT 2 .....................................................................................................................................16

(a) Statement of profit and loss account....................................................................................16

(b) Statement of financial position of Peter Hampau as at 31st July 2018................................16

CLIENT 3......................................................................................................................................18

(a) Profit and loss account of Bowling Limited.........................................................................18

(b) Balance sheet of Bowling Limited.......................................................................................18

....................................................................................................................................................19

(c) Accounting concepts of Consistency and Prudency.............................................................19

(d) Purpose of depreciation and its methods..............................................................................20

CLIENT 4......................................................................................................................................21

(A) Bank Reconciliation Statement...........................................................................................21

(B) Prepare Durrell Ltd's updated cash book for December 2017.............................................21

(C) Bank Reconciliation Statement as on 31st December 2017................................................22

CLIENT 5......................................................................................................................................22

(a) Books of Henderson.............................................................................................................22

(b) Control account and its need................................................................................................23

CLIENT 6......................................................................................................................................24

(a) Suspense account..................................................................................................................24

(b) Trial Balance........................................................................................................................25

(c) Trial balance have credit balance of £ 330 as suspense account..........................................25

(d) Difference between Clearing and Suspense account............................................................26

CONCLUSION..............................................................................................................................26

REFERENCES .............................................................................................................................28

Books & Journals...........................................................................................................................28

CLIENT 5......................................................................................................................................22

(a) Books of Henderson.............................................................................................................22

(b) Control account and its need................................................................................................23

CLIENT 6......................................................................................................................................24

(a) Suspense account..................................................................................................................24

(b) Trial Balance........................................................................................................................25

(c) Trial balance have credit balance of £ 330 as suspense account..........................................25

(d) Difference between Clearing and Suspense account............................................................26

CONCLUSION..............................................................................................................................26

REFERENCES .............................................................................................................................28

Books & Journals...........................................................................................................................28

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting principle provide some rules and regulations to the organisation

which help them to make financial statements. These standard and guidelines should be follow

by the every business. Generally accepted accounting principle (GAAP) provide general

guidelines for the company that is helpful at the time of preparing financial accounts such as

balance sheet or profit and loss accounts. As a junior accountant it is very important to use these

standard that provide accurate information to prepare statements. Further report is about financial

accounting, it's purpose and regulation (Agasisti and Catalano, 2013). Along with this, they also

discussed about accounting principle, conventions, it's concept such as consistency or material

disclosure. It is also included that double entry book keeping system, trial balance and final

accounts in respect of sole proprietor, limited company or partnership. Rest of the topic is about

bank reconciliation statement, it's process, suspense account with the relevant example and it

also include the sales and purchase control account. These statement help the accountant take

necessary decision and it provide the help to achieve business objectives and goals.

BUSINESS REPORT

1. Financial accounting and it's purpose

Financial accounting: It is a process of recording business transactions, summarised and

analyse these data provide a accurate information to the organisation. Financial accounting is the

specialised branch of accounting which help the organisation to create income statement and

financial position. This accounting system follow the some guidelines which provide them

proper guidelines. It is also prepared for further use such as decision making process, record data

for future budget and for analysing. It is prepared for it's users such as shareholders and

stakeholders of the company. Accounting system helps the organisation to record it's daily

activities that further helpful in manager's decision making process (Akenbor and Ibanichuka,

2012). There are various purpose of financial accounting such as:

Identify the performance of the company through it's financial activities.

It is helpful for the identification of true position of business in respect of income

statement and balance sheet.

It provide helps to the manager to take decision on the basis of financial information.

Helpful for the analysis of accounting fundamentals.

1

Financial accounting principle provide some rules and regulations to the organisation

which help them to make financial statements. These standard and guidelines should be follow

by the every business. Generally accepted accounting principle (GAAP) provide general

guidelines for the company that is helpful at the time of preparing financial accounts such as

balance sheet or profit and loss accounts. As a junior accountant it is very important to use these

standard that provide accurate information to prepare statements. Further report is about financial

accounting, it's purpose and regulation (Agasisti and Catalano, 2013). Along with this, they also

discussed about accounting principle, conventions, it's concept such as consistency or material

disclosure. It is also included that double entry book keeping system, trial balance and final

accounts in respect of sole proprietor, limited company or partnership. Rest of the topic is about

bank reconciliation statement, it's process, suspense account with the relevant example and it

also include the sales and purchase control account. These statement help the accountant take

necessary decision and it provide the help to achieve business objectives and goals.

BUSINESS REPORT

1. Financial accounting and it's purpose

Financial accounting: It is a process of recording business transactions, summarised and

analyse these data provide a accurate information to the organisation. Financial accounting is the

specialised branch of accounting which help the organisation to create income statement and

financial position. This accounting system follow the some guidelines which provide them

proper guidelines. It is also prepared for further use such as decision making process, record data

for future budget and for analysing. It is prepared for it's users such as shareholders and

stakeholders of the company. Accounting system helps the organisation to record it's daily

activities that further helpful in manager's decision making process (Akenbor and Ibanichuka,

2012). There are various purpose of financial accounting such as:

Identify the performance of the company through it's financial activities.

It is helpful for the identification of true position of business in respect of income

statement and balance sheet.

It provide helps to the manager to take decision on the basis of financial information.

Helpful for the analysis of accounting fundamentals.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

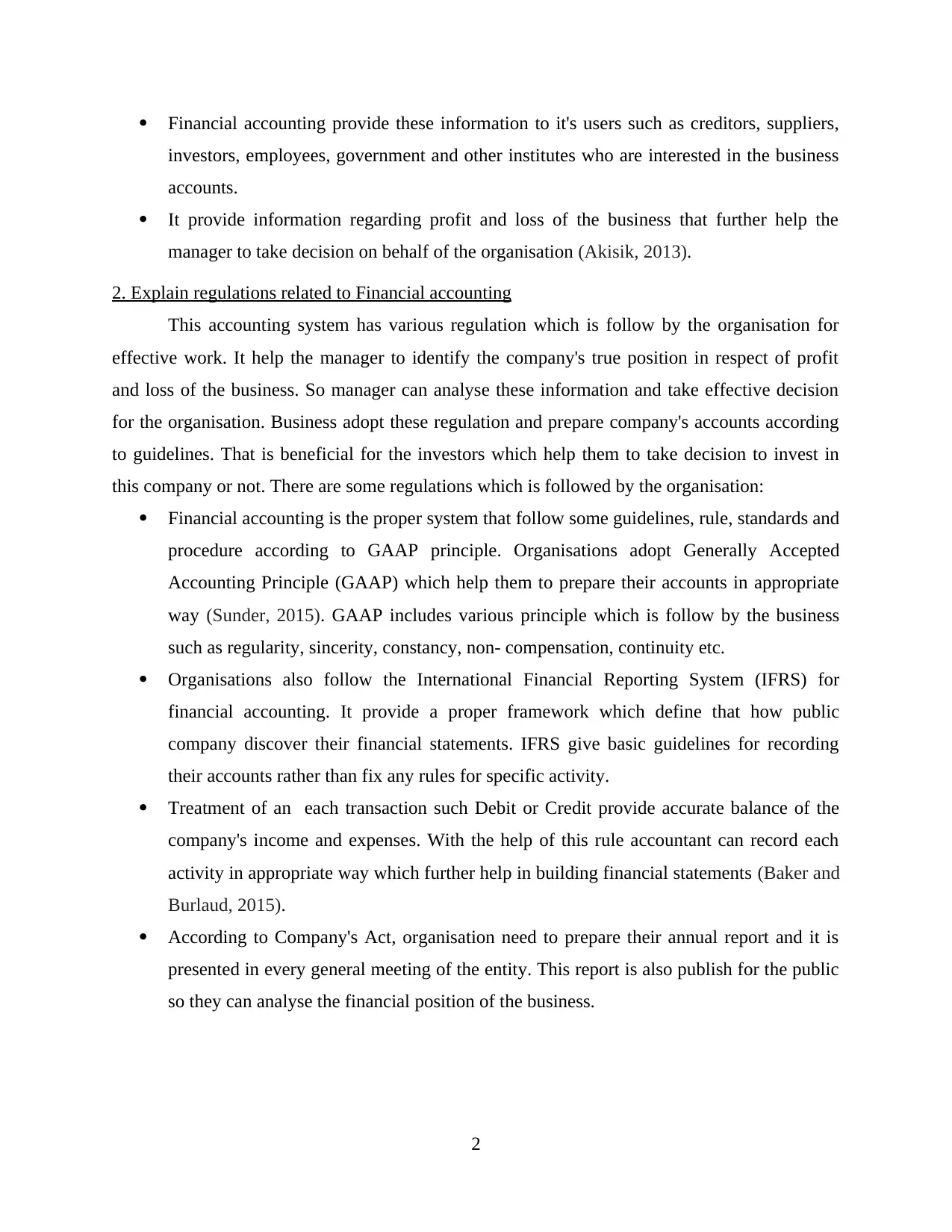

Financial accounting provide these information to it's users such as creditors, suppliers,

investors, employees, government and other institutes who are interested in the business

accounts.

It provide information regarding profit and loss of the business that further help the

manager to take decision on behalf of the organisation (Akisik, 2013).

2. Explain regulations related to Financial accounting

This accounting system has various regulation which is follow by the organisation for

effective work. It help the manager to identify the company's true position in respect of profit

and loss of the business. So manager can analyse these information and take effective decision

for the organisation. Business adopt these regulation and prepare company's accounts according

to guidelines. That is beneficial for the investors which help them to take decision to invest in

this company or not. There are some regulations which is followed by the organisation:

Financial accounting is the proper system that follow some guidelines, rule, standards and

procedure according to GAAP principle. Organisations adopt Generally Accepted

Accounting Principle (GAAP) which help them to prepare their accounts in appropriate

way (Sunder, 2015). GAAP includes various principle which is follow by the business

such as regularity, sincerity, constancy, non- compensation, continuity etc.

Organisations also follow the International Financial Reporting System (IFRS) for

financial accounting. It provide a proper framework which define that how public

company discover their financial statements. IFRS give basic guidelines for recording

their accounts rather than fix any rules for specific activity.

Treatment of an each transaction such Debit or Credit provide accurate balance of the

company's income and expenses. With the help of this rule accountant can record each

activity in appropriate way which further help in building financial statements (Baker and

Burlaud, 2015).

According to Company's Act, organisation need to prepare their annual report and it is

presented in every general meeting of the entity. This report is also publish for the public

so they can analyse the financial position of the business.

2

investors, employees, government and other institutes who are interested in the business

accounts.

It provide information regarding profit and loss of the business that further help the

manager to take decision on behalf of the organisation (Akisik, 2013).

2. Explain regulations related to Financial accounting

This accounting system has various regulation which is follow by the organisation for

effective work. It help the manager to identify the company's true position in respect of profit

and loss of the business. So manager can analyse these information and take effective decision

for the organisation. Business adopt these regulation and prepare company's accounts according

to guidelines. That is beneficial for the investors which help them to take decision to invest in

this company or not. There are some regulations which is followed by the organisation:

Financial accounting is the proper system that follow some guidelines, rule, standards and

procedure according to GAAP principle. Organisations adopt Generally Accepted

Accounting Principle (GAAP) which help them to prepare their accounts in appropriate

way (Sunder, 2015). GAAP includes various principle which is follow by the business

such as regularity, sincerity, constancy, non- compensation, continuity etc.

Organisations also follow the International Financial Reporting System (IFRS) for

financial accounting. It provide a proper framework which define that how public

company discover their financial statements. IFRS give basic guidelines for recording

their accounts rather than fix any rules for specific activity.

Treatment of an each transaction such Debit or Credit provide accurate balance of the

company's income and expenses. With the help of this rule accountant can record each

activity in appropriate way which further help in building financial statements (Baker and

Burlaud, 2015).

According to Company's Act, organisation need to prepare their annual report and it is

presented in every general meeting of the entity. This report is also publish for the public

so they can analyse the financial position of the business.

2

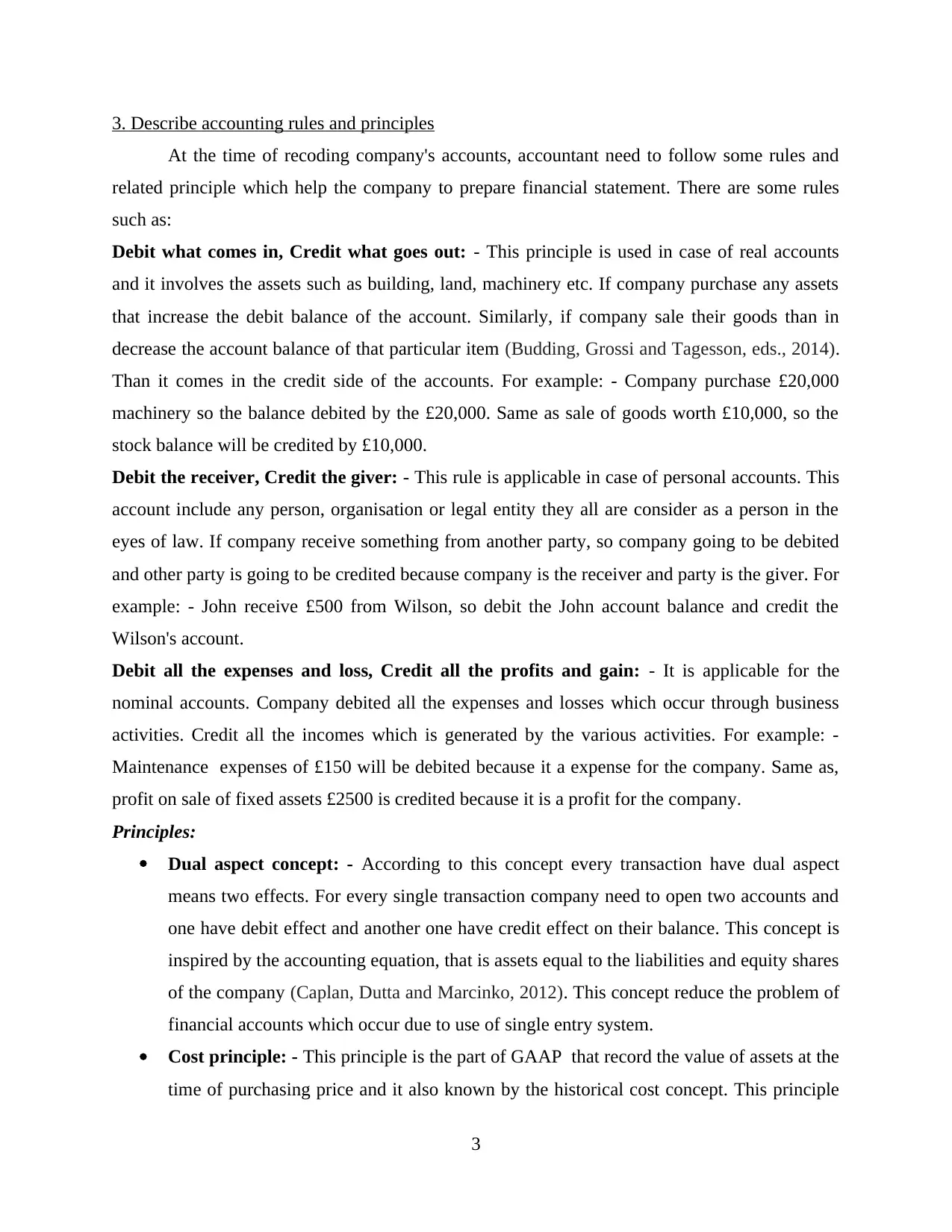

3. Describe accounting rules and principles

At the time of recoding company's accounts, accountant need to follow some rules and

related principle which help the company to prepare financial statement. There are some rules

such as:

Debit what comes in, Credit what goes out: - This principle is used in case of real accounts

and it involves the assets such as building, land, machinery etc. If company purchase any assets

that increase the debit balance of the account. Similarly, if company sale their goods than in

decrease the account balance of that particular item (Budding, Grossi and Tagesson, eds., 2014).

Than it comes in the credit side of the accounts. For example: - Company purchase £20,000

machinery so the balance debited by the £20,000. Same as sale of goods worth £10,000, so the

stock balance will be credited by £10,000.

Debit the receiver, Credit the giver: - This rule is applicable in case of personal accounts. This

account include any person, organisation or legal entity they all are consider as a person in the

eyes of law. If company receive something from another party, so company going to be debited

and other party is going to be credited because company is the receiver and party is the giver. For

example: - John receive £500 from Wilson, so debit the John account balance and credit the

Wilson's account.

Debit all the expenses and loss, Credit all the profits and gain: - It is applicable for the

nominal accounts. Company debited all the expenses and losses which occur through business

activities. Credit all the incomes which is generated by the various activities. For example: -

Maintenance expenses of £150 will be debited because it a expense for the company. Same as,

profit on sale of fixed assets £2500 is credited because it is a profit for the company.

Principles:

Dual aspect concept: - According to this concept every transaction have dual aspect

means two effects. For every single transaction company need to open two accounts and

one have debit effect and another one have credit effect on their balance. This concept is

inspired by the accounting equation, that is assets equal to the liabilities and equity shares

of the company (Caplan, Dutta and Marcinko, 2012). This concept reduce the problem of

financial accounts which occur due to use of single entry system.

Cost principle: - This principle is the part of GAAP that record the value of assets at the

time of purchasing price and it also known by the historical cost concept. This principle

3

At the time of recoding company's accounts, accountant need to follow some rules and

related principle which help the company to prepare financial statement. There are some rules

such as:

Debit what comes in, Credit what goes out: - This principle is used in case of real accounts

and it involves the assets such as building, land, machinery etc. If company purchase any assets

that increase the debit balance of the account. Similarly, if company sale their goods than in

decrease the account balance of that particular item (Budding, Grossi and Tagesson, eds., 2014).

Than it comes in the credit side of the accounts. For example: - Company purchase £20,000

machinery so the balance debited by the £20,000. Same as sale of goods worth £10,000, so the

stock balance will be credited by £10,000.

Debit the receiver, Credit the giver: - This rule is applicable in case of personal accounts. This

account include any person, organisation or legal entity they all are consider as a person in the

eyes of law. If company receive something from another party, so company going to be debited

and other party is going to be credited because company is the receiver and party is the giver. For

example: - John receive £500 from Wilson, so debit the John account balance and credit the

Wilson's account.

Debit all the expenses and loss, Credit all the profits and gain: - It is applicable for the

nominal accounts. Company debited all the expenses and losses which occur through business

activities. Credit all the incomes which is generated by the various activities. For example: -

Maintenance expenses of £150 will be debited because it a expense for the company. Same as,

profit on sale of fixed assets £2500 is credited because it is a profit for the company.

Principles:

Dual aspect concept: - According to this concept every transaction have dual aspect

means two effects. For every single transaction company need to open two accounts and

one have debit effect and another one have credit effect on their balance. This concept is

inspired by the accounting equation, that is assets equal to the liabilities and equity shares

of the company (Caplan, Dutta and Marcinko, 2012). This concept reduce the problem of

financial accounts which occur due to use of single entry system.

Cost principle: - This principle is the part of GAAP that record the value of assets at the

time of purchasing price and it also known by the historical cost concept. This principle

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

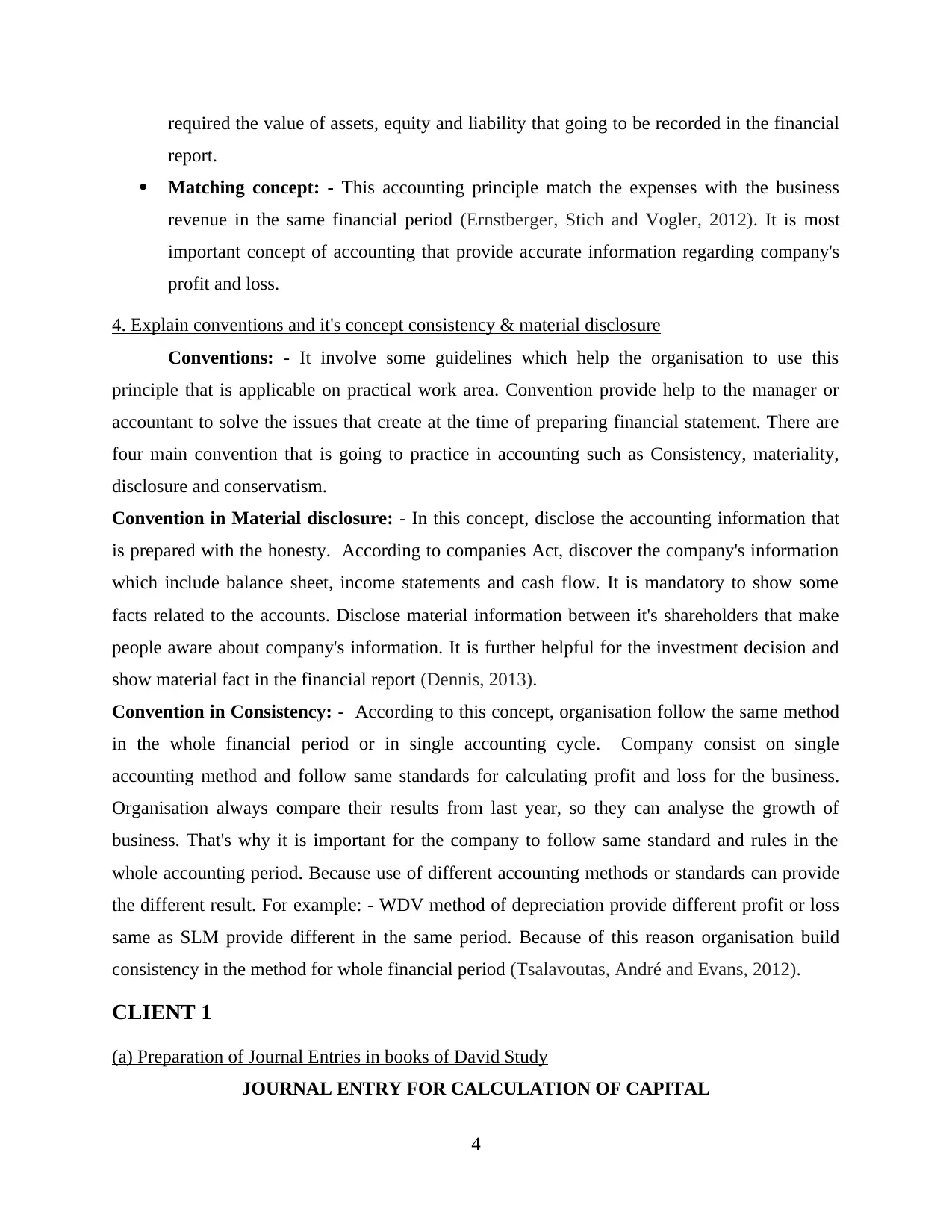

required the value of assets, equity and liability that going to be recorded in the financial

report.

Matching concept: - This accounting principle match the expenses with the business

revenue in the same financial period (Ernstberger, Stich and Vogler, 2012). It is most

important concept of accounting that provide accurate information regarding company's

profit and loss.

4. Explain conventions and it's concept consistency & material disclosure

Conventions: - It involve some guidelines which help the organisation to use this

principle that is applicable on practical work area. Convention provide help to the manager or

accountant to solve the issues that create at the time of preparing financial statement. There are

four main convention that is going to practice in accounting such as Consistency, materiality,

disclosure and conservatism.

Convention in Material disclosure: - In this concept, disclose the accounting information that

is prepared with the honesty. According to companies Act, discover the company's information

which include balance sheet, income statements and cash flow. It is mandatory to show some

facts related to the accounts. Disclose material information between it's shareholders that make

people aware about company's information. It is further helpful for the investment decision and

show material fact in the financial report (Dennis, 2013).

Convention in Consistency: - According to this concept, organisation follow the same method

in the whole financial period or in single accounting cycle. Company consist on single

accounting method and follow same standards for calculating profit and loss for the business.

Organisation always compare their results from last year, so they can analyse the growth of

business. That's why it is important for the company to follow same standard and rules in the

whole accounting period. Because use of different accounting methods or standards can provide

the different result. For example: - WDV method of depreciation provide different profit or loss

same as SLM provide different in the same period. Because of this reason organisation build

consistency in the method for whole financial period (Tsalavoutas, André and Evans, 2012).

CLIENT 1

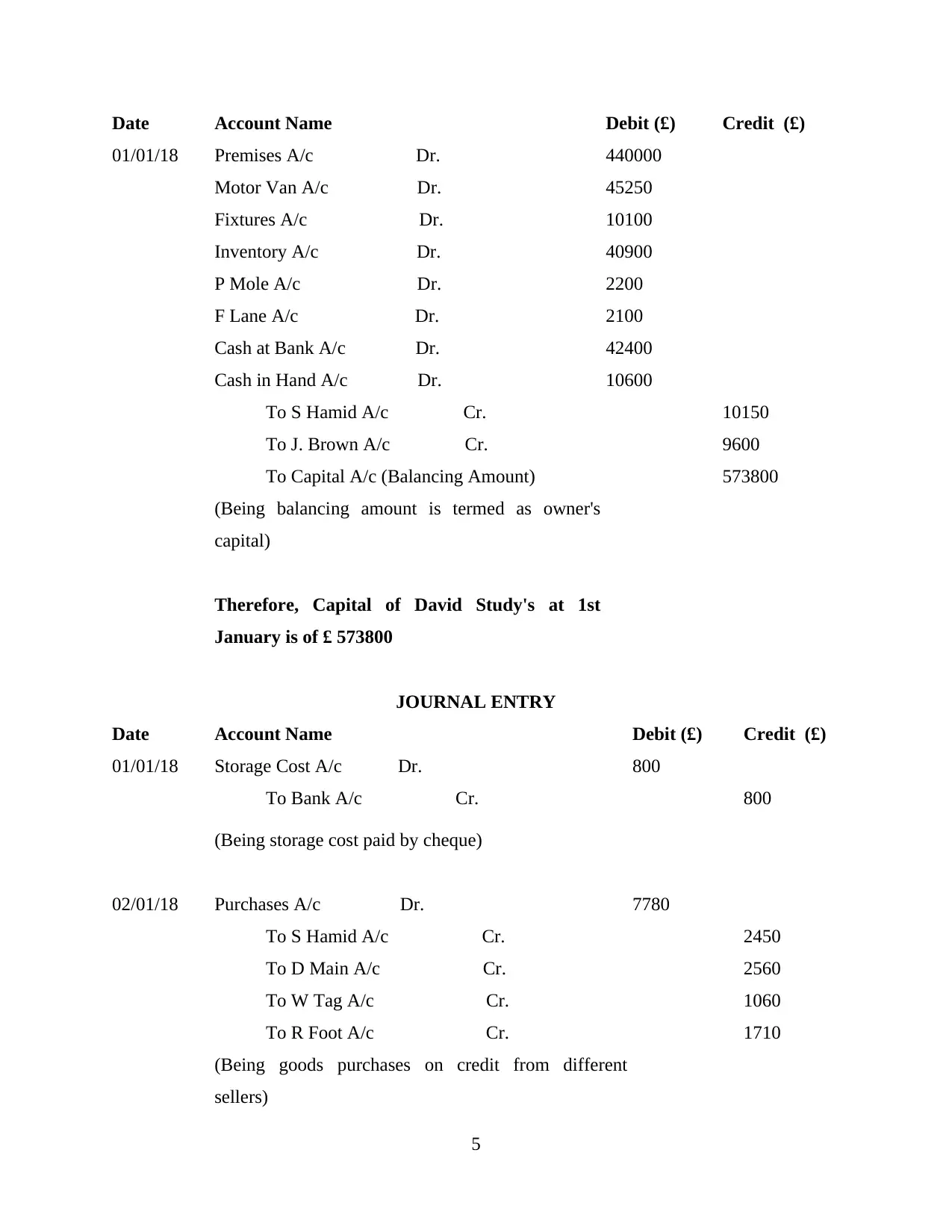

(a) Preparation of Journal Entries in books of David Study

JOURNAL ENTRY FOR CALCULATION OF CAPITAL

4

report.

Matching concept: - This accounting principle match the expenses with the business

revenue in the same financial period (Ernstberger, Stich and Vogler, 2012). It is most

important concept of accounting that provide accurate information regarding company's

profit and loss.

4. Explain conventions and it's concept consistency & material disclosure

Conventions: - It involve some guidelines which help the organisation to use this

principle that is applicable on practical work area. Convention provide help to the manager or

accountant to solve the issues that create at the time of preparing financial statement. There are

four main convention that is going to practice in accounting such as Consistency, materiality,

disclosure and conservatism.

Convention in Material disclosure: - In this concept, disclose the accounting information that

is prepared with the honesty. According to companies Act, discover the company's information

which include balance sheet, income statements and cash flow. It is mandatory to show some

facts related to the accounts. Disclose material information between it's shareholders that make

people aware about company's information. It is further helpful for the investment decision and

show material fact in the financial report (Dennis, 2013).

Convention in Consistency: - According to this concept, organisation follow the same method

in the whole financial period or in single accounting cycle. Company consist on single

accounting method and follow same standards for calculating profit and loss for the business.

Organisation always compare their results from last year, so they can analyse the growth of

business. That's why it is important for the company to follow same standard and rules in the

whole accounting period. Because use of different accounting methods or standards can provide

the different result. For example: - WDV method of depreciation provide different profit or loss

same as SLM provide different in the same period. Because of this reason organisation build

consistency in the method for whole financial period (Tsalavoutas, André and Evans, 2012).

CLIENT 1

(a) Preparation of Journal Entries in books of David Study

JOURNAL ENTRY FOR CALCULATION OF CAPITAL

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Account Name Debit (£) Credit (£)

01/01/18 Premises A/c Dr. 440000

Motor Van A/c Dr. 45250

Fixtures A/c Dr. 10100

Inventory A/c Dr. 40900

P Mole A/c Dr. 2200

F Lane A/c Dr. 2100

Cash at Bank A/c Dr. 42400

Cash in Hand A/c Dr. 10600

To S Hamid A/c Cr. 10150

To J. Brown A/c Cr. 9600

To Capital A/c (Balancing Amount) 573800

(Being balancing amount is termed as owner's

capital)

Therefore, Capital of David Study's at 1st

January is of £ 573800

JOURNAL ENTRY

Date Account Name Debit (£) Credit (£)

01/01/18 Storage Cost A/c Dr. 800

To Bank A/c Cr. 800

(Being storage cost paid by cheque)

02/01/18 Purchases A/c Dr. 7780

To S Hamid A/c Cr. 2450

To D Main A/c Cr. 2560

To W Tag A/c Cr. 1060

To R Foot A/c Cr. 1710

(Being goods purchases on credit from different

sellers)

5

01/01/18 Premises A/c Dr. 440000

Motor Van A/c Dr. 45250

Fixtures A/c Dr. 10100

Inventory A/c Dr. 40900

P Mole A/c Dr. 2200

F Lane A/c Dr. 2100

Cash at Bank A/c Dr. 42400

Cash in Hand A/c Dr. 10600

To S Hamid A/c Cr. 10150

To J. Brown A/c Cr. 9600

To Capital A/c (Balancing Amount) 573800

(Being balancing amount is termed as owner's

capital)

Therefore, Capital of David Study's at 1st

January is of £ 573800

JOURNAL ENTRY

Date Account Name Debit (£) Credit (£)

01/01/18 Storage Cost A/c Dr. 800

To Bank A/c Cr. 800

(Being storage cost paid by cheque)

02/01/18 Purchases A/c Dr. 7780

To S Hamid A/c Cr. 2450

To D Main A/c Cr. 2560

To W Tag A/c Cr. 1060

To R Foot A/c Cr. 1710

(Being goods purchases on credit from different

sellers)

5

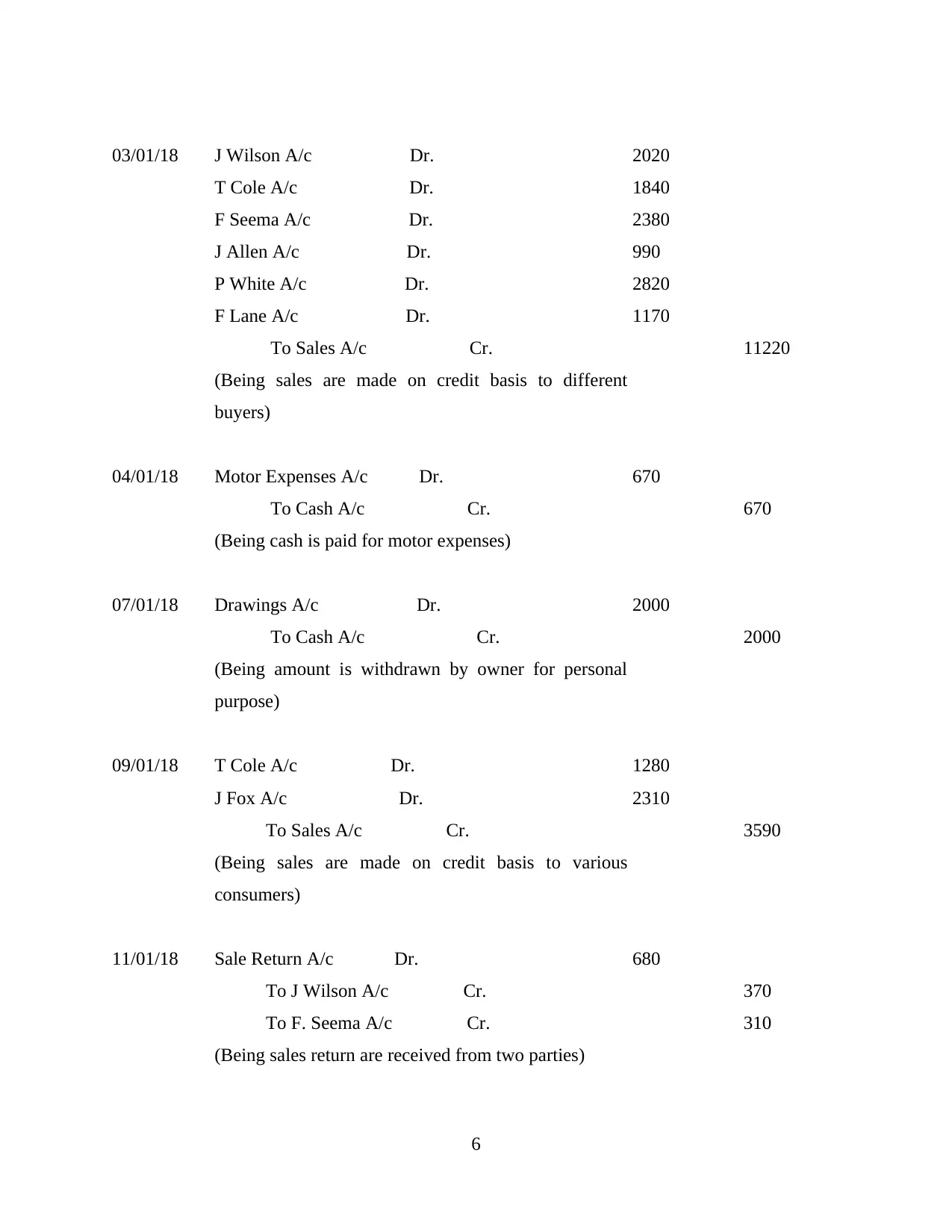

03/01/18 J Wilson A/c Dr. 2020

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

J Allen A/c Dr. 990

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c Cr. 11220

(Being sales are made on credit basis to different

buyers)

04/01/18 Motor Expenses A/c Dr. 670

To Cash A/c Cr. 670

(Being cash is paid for motor expenses)

07/01/18 Drawings A/c Dr. 2000

To Cash A/c Cr. 2000

(Being amount is withdrawn by owner for personal

purpose)

09/01/18 T Cole A/c Dr. 1280

J Fox A/c Dr. 2310

To Sales A/c Cr. 3590

(Being sales are made on credit basis to various

consumers)

11/01/18 Sale Return A/c Dr. 680

To J Wilson A/c Cr. 370

To F. Seema A/c Cr. 310

(Being sales return are received from two parties)

6

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

J Allen A/c Dr. 990

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c Cr. 11220

(Being sales are made on credit basis to different

buyers)

04/01/18 Motor Expenses A/c Dr. 670

To Cash A/c Cr. 670

(Being cash is paid for motor expenses)

07/01/18 Drawings A/c Dr. 2000

To Cash A/c Cr. 2000

(Being amount is withdrawn by owner for personal

purpose)

09/01/18 T Cole A/c Dr. 1280

J Fox A/c Dr. 2310

To Sales A/c Cr. 3590

(Being sales are made on credit basis to various

consumers)

11/01/18 Sale Return A/c Dr. 680

To J Wilson A/c Cr. 370

To F. Seema A/c Cr. 310

(Being sales return are received from two parties)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

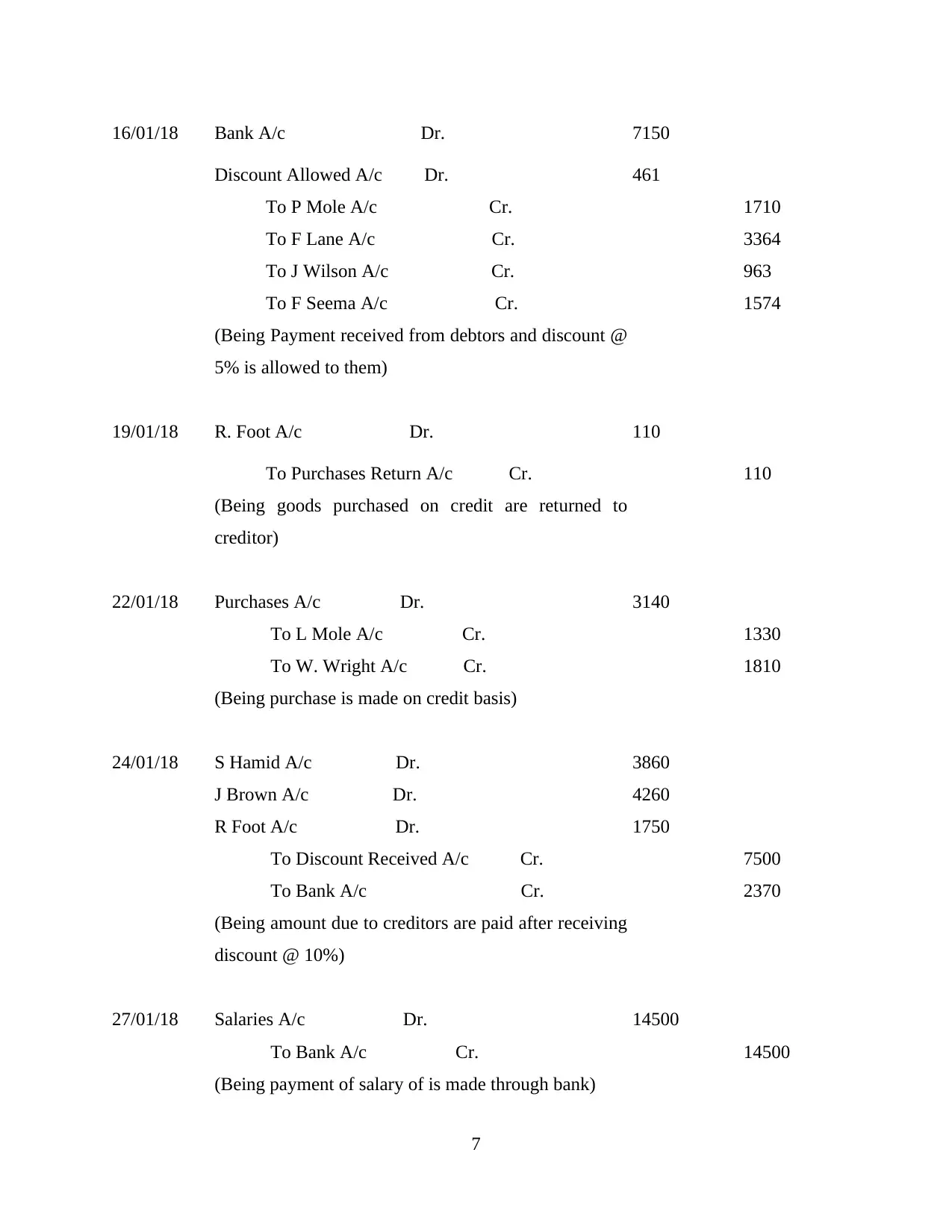

16/01/18 Bank A/c Dr. 7150

Discount Allowed A/c Dr. 461

To P Mole A/c Cr. 1710

To F Lane A/c Cr. 3364

To J Wilson A/c Cr. 963

To F Seema A/c Cr. 1574

(Being Payment received from debtors and discount @

5% is allowed to them)

19/01/18 R. Foot A/c Dr. 110

To Purchases Return A/c Cr. 110

(Being goods purchased on credit are returned to

creditor)

22/01/18 Purchases A/c Dr. 3140

To L Mole A/c Cr. 1330

To W. Wright A/c Cr. 1810

(Being purchase is made on credit basis)

24/01/18 S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Discount Received A/c Cr. 7500

To Bank A/c Cr. 2370

(Being amount due to creditors are paid after receiving

discount @ 10%)

27/01/18 Salaries A/c Dr. 14500

To Bank A/c Cr. 14500

(Being payment of salary of is made through bank)

7

Discount Allowed A/c Dr. 461

To P Mole A/c Cr. 1710

To F Lane A/c Cr. 3364

To J Wilson A/c Cr. 963

To F Seema A/c Cr. 1574

(Being Payment received from debtors and discount @

5% is allowed to them)

19/01/18 R. Foot A/c Dr. 110

To Purchases Return A/c Cr. 110

(Being goods purchased on credit are returned to

creditor)

22/01/18 Purchases A/c Dr. 3140

To L Mole A/c Cr. 1330

To W. Wright A/c Cr. 1810

(Being purchase is made on credit basis)

24/01/18 S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Discount Received A/c Cr. 7500

To Bank A/c Cr. 2370

(Being amount due to creditors are paid after receiving

discount @ 10%)

27/01/18 Salaries A/c Dr. 14500

To Bank A/c Cr. 14500

(Being payment of salary of is made through bank)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

30/01/18 Business Rates A/c Dr. 2220

To Bank A/c Cr. 2220

(Being expense of business rates are made through

cheque)

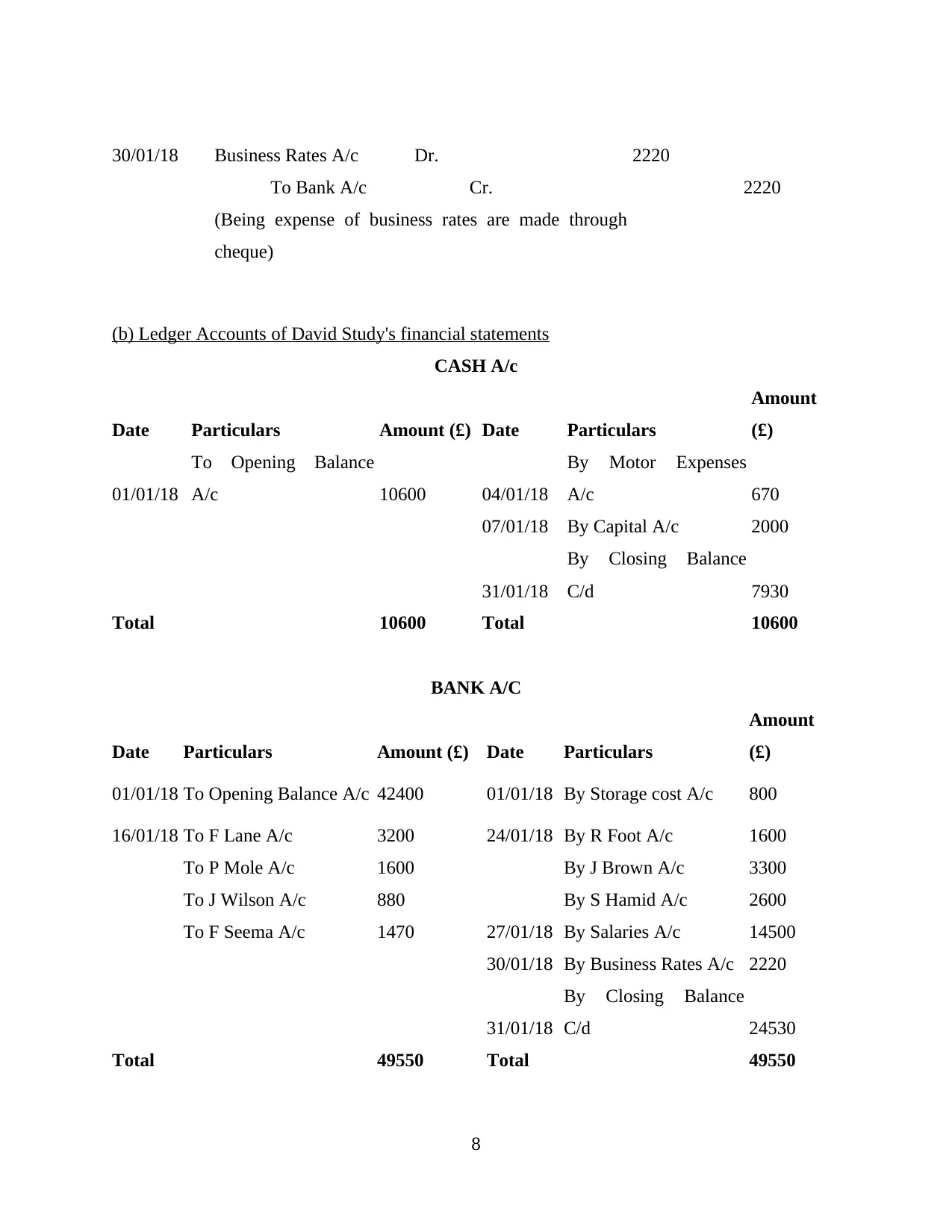

(b) Ledger Accounts of David Study's financial statements

CASH A/c

Date Particulars Amount (£) Date Particulars

Amount

(£)

01/01/18

To Opening Balance

A/c 10600 04/01/18

By Motor Expenses

A/c 670

07/01/18 By Capital A/c 2000

31/01/18

By Closing Balance

C/d 7930

Total 10600 Total 10600

BANK A/C

Date Particulars Amount (£) Date Particulars

Amount

(£)

01/01/18 To Opening Balance A/c 42400 01/01/18 By Storage cost A/c 800

16/01/18 To F Lane A/c 3200 24/01/18 By R Foot A/c 1600

To P Mole A/c 1600 By J Brown A/c 3300

To J Wilson A/c 880 By S Hamid A/c 2600

To F Seema A/c 1470 27/01/18 By Salaries A/c 14500

30/01/18 By Business Rates A/c 2220

31/01/18

By Closing Balance

C/d 24530

Total 49550 Total 49550

8

To Bank A/c Cr. 2220

(Being expense of business rates are made through

cheque)

(b) Ledger Accounts of David Study's financial statements

CASH A/c

Date Particulars Amount (£) Date Particulars

Amount

(£)

01/01/18

To Opening Balance

A/c 10600 04/01/18

By Motor Expenses

A/c 670

07/01/18 By Capital A/c 2000

31/01/18

By Closing Balance

C/d 7930

Total 10600 Total 10600

BANK A/C

Date Particulars Amount (£) Date Particulars

Amount

(£)

01/01/18 To Opening Balance A/c 42400 01/01/18 By Storage cost A/c 800

16/01/18 To F Lane A/c 3200 24/01/18 By R Foot A/c 1600

To P Mole A/c 1600 By J Brown A/c 3300

To J Wilson A/c 880 By S Hamid A/c 2600

To F Seema A/c 1470 27/01/18 By Salaries A/c 14500

30/01/18 By Business Rates A/c 2220

31/01/18

By Closing Balance

C/d 24530

Total 49550 Total 49550

8

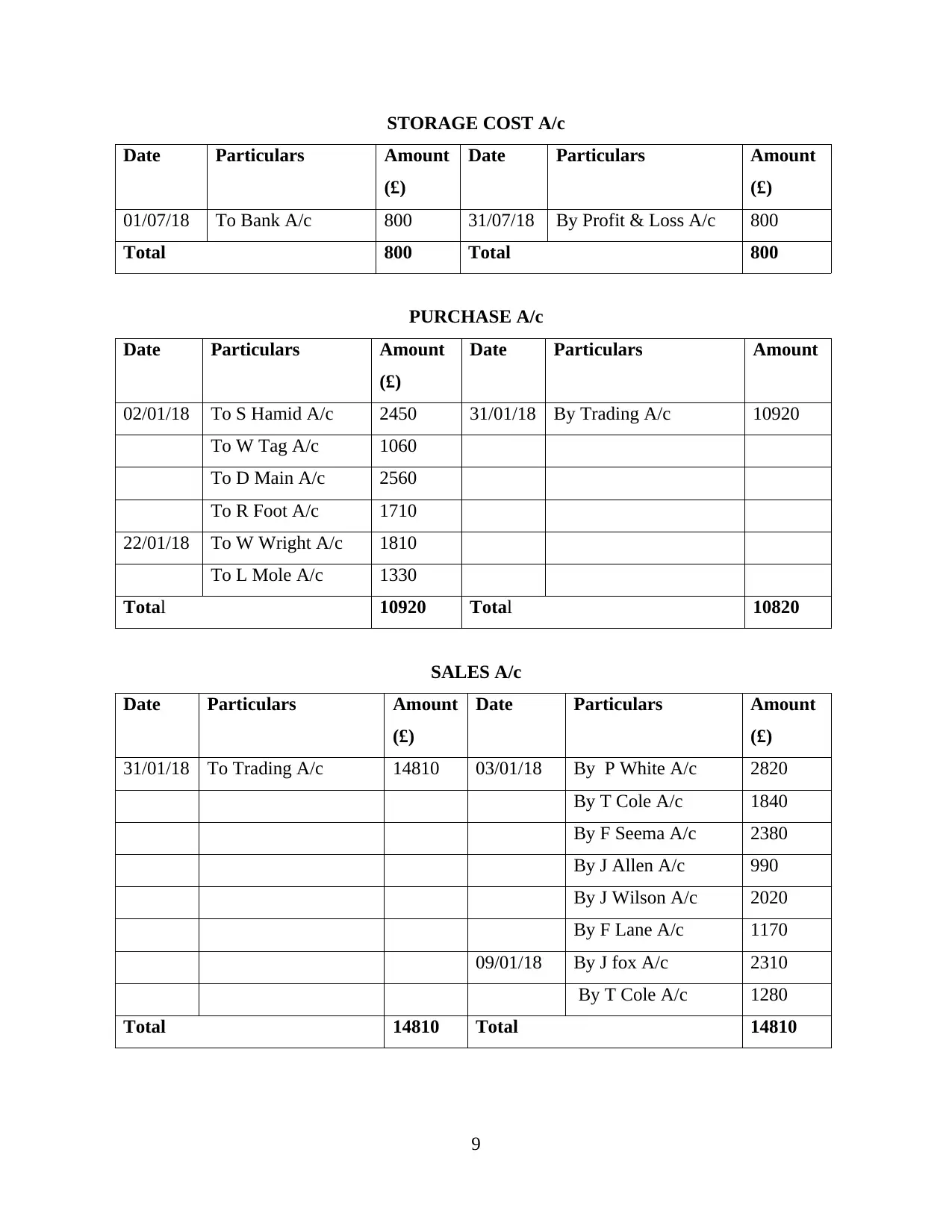

STORAGE COST A/c

Date Particulars Amount

(£)

Date Particulars Amount

(£)

01/07/18 To Bank A/c 800 31/07/18 By Profit & Loss A/c 800

Total 800 Total 800

PURCHASE A/c

Date Particulars Amount

(£)

Date Particulars Amount

02/01/18 To S Hamid A/c 2450 31/01/18 By Trading A/c 10920

To W Tag A/c 1060

To D Main A/c 2560

To R Foot A/c 1710

22/01/18 To W Wright A/c 1810

To L Mole A/c 1330

Total 10920 Total 10820

SALES A/c

Date Particulars Amount

(£)

Date Particulars Amount

(£)

31/01/18 To Trading A/c 14810 03/01/18 By P White A/c 2820

By T Cole A/c 1840

By F Seema A/c 2380

By J Allen A/c 990

By J Wilson A/c 2020

By F Lane A/c 1170

09/01/18 By J fox A/c 2310

By T Cole A/c 1280

Total 14810 Total 14810

9

Date Particulars Amount

(£)

Date Particulars Amount

(£)

01/07/18 To Bank A/c 800 31/07/18 By Profit & Loss A/c 800

Total 800 Total 800

PURCHASE A/c

Date Particulars Amount

(£)

Date Particulars Amount

02/01/18 To S Hamid A/c 2450 31/01/18 By Trading A/c 10920

To W Tag A/c 1060

To D Main A/c 2560

To R Foot A/c 1710

22/01/18 To W Wright A/c 1810

To L Mole A/c 1330

Total 10920 Total 10820

SALES A/c

Date Particulars Amount

(£)

Date Particulars Amount

(£)

31/01/18 To Trading A/c 14810 03/01/18 By P White A/c 2820

By T Cole A/c 1840

By F Seema A/c 2380

By J Allen A/c 990

By J Wilson A/c 2020

By F Lane A/c 1170

09/01/18 By J fox A/c 2310

By T Cole A/c 1280

Total 14810 Total 14810

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.