Financial Accounting: Problem Questions and Solutions, RMIT University

VerifiedAdded on 2023/06/04

|25

|2479

|273

Homework Assignment

AI Summary

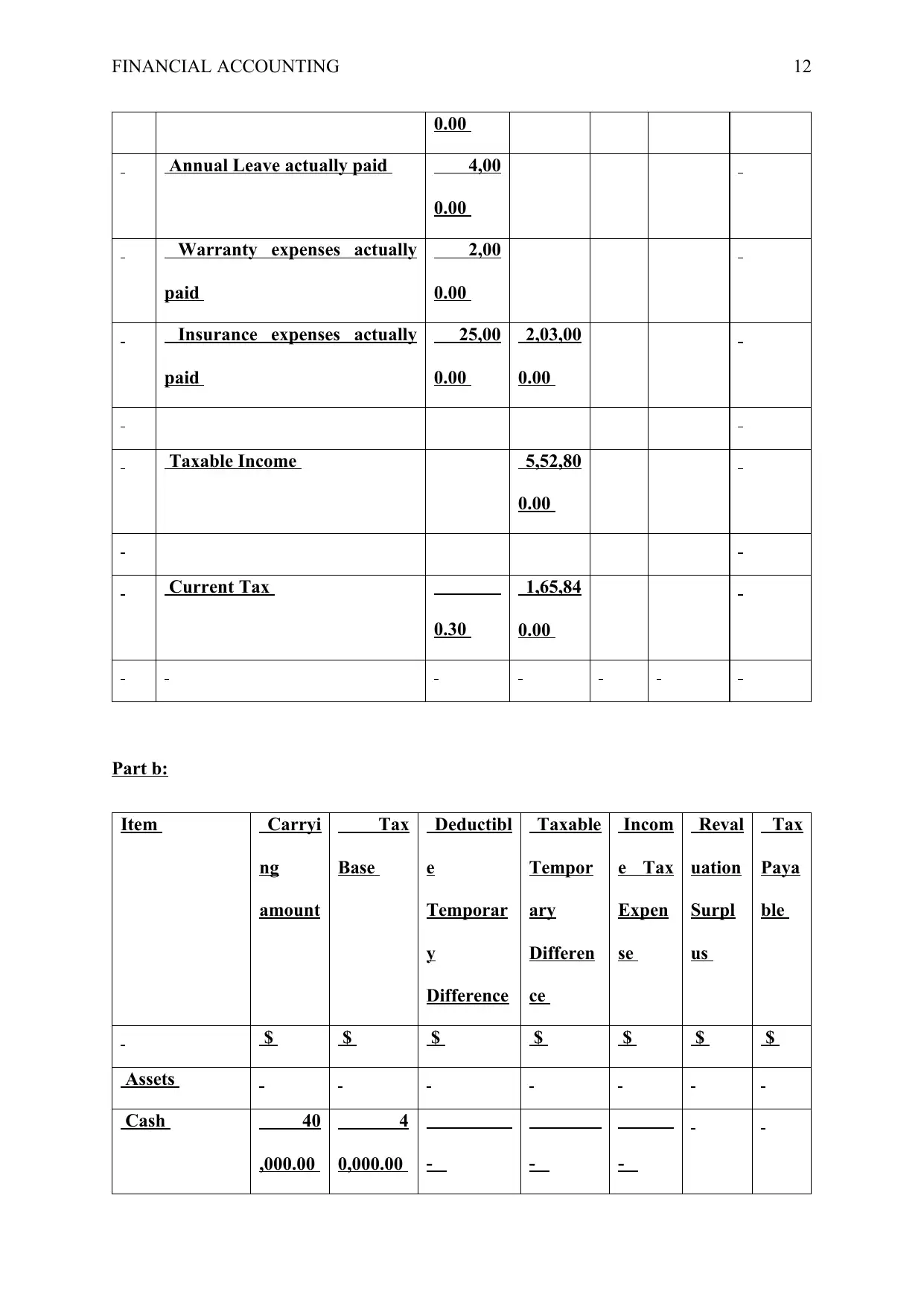

This document presents a comprehensive solution to a financial accounting assignment, addressing a variety of accounting problems. The solution covers several key areas including the application of IAS 8, IFRS 13, and AASB 108. It includes detailed journal entries for share capital transactions, depreciation calculations, tax computations, and impairment analysis. The assignment also delves into the measurement of fair values and the treatment of errors in financial statements. The solutions provide step-by-step explanations, calculations, and financial statement disclosures, providing a valuable resource for students studying financial accounting. Furthermore, the assignment incorporates real-world scenarios such as fraudulent activities, and guides the reader on how to handle such events within the accounting framework.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.