Financial Accounting Process Analysis Report - Course Name

VerifiedAdded on 2023/01/23

|10

|886

|26

Report

AI Summary

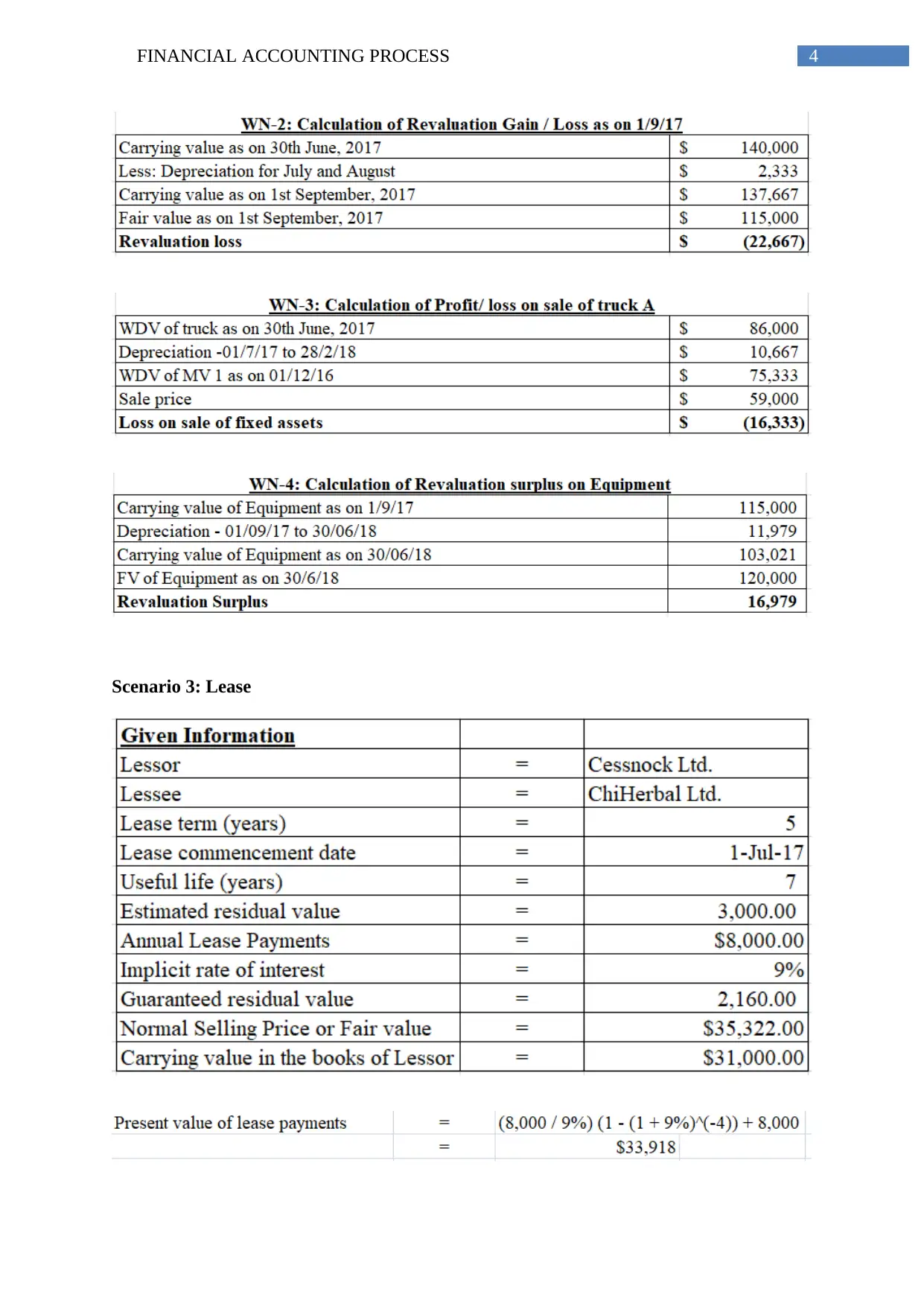

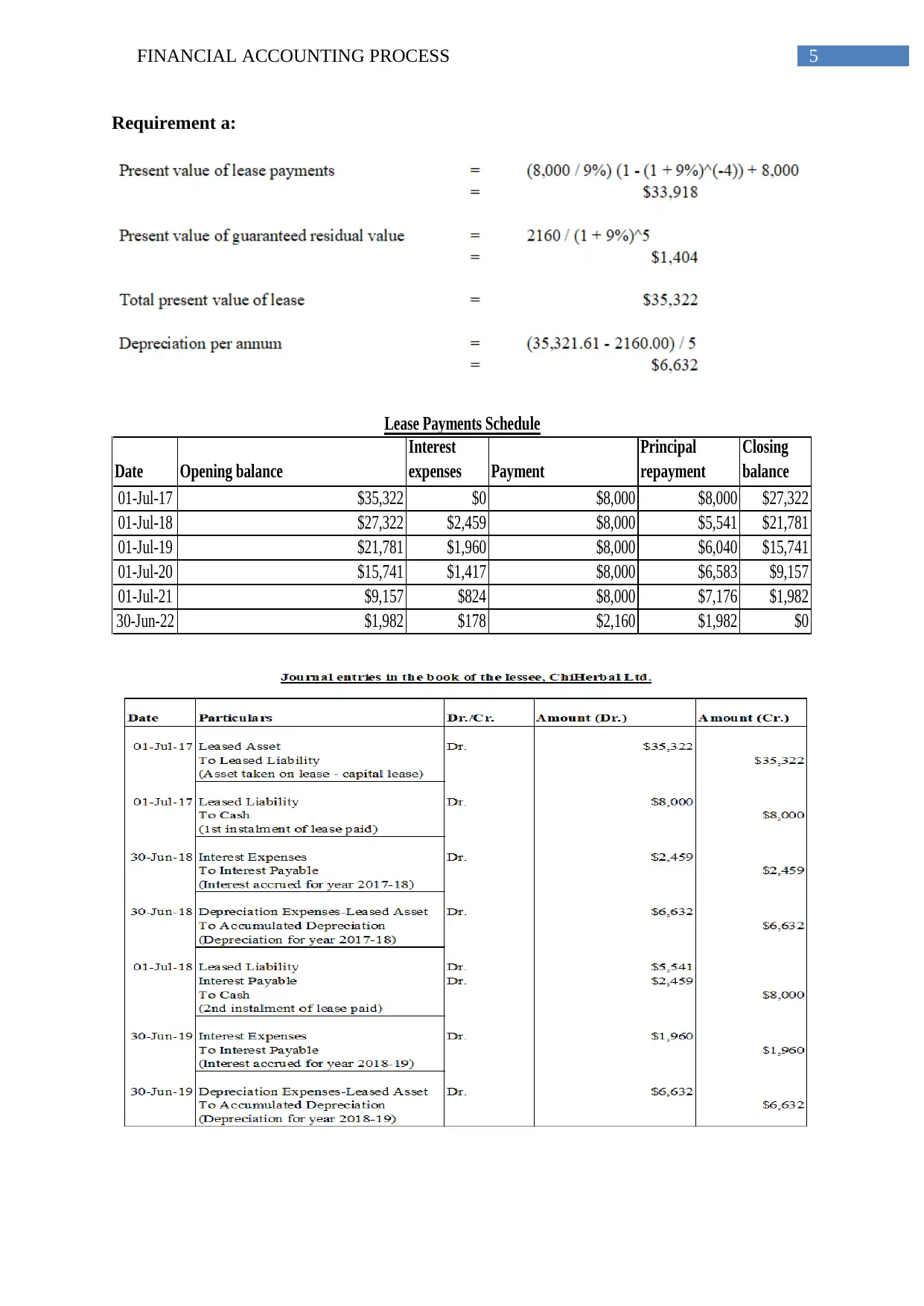

This report delves into the intricacies of financial accounting through a series of scenarios. It begins by examining the financing of company operations, followed by an analysis of property, plant, and equipment, and then explores the accounting treatment of leases. A significant portion of the report focuses on intangible assets, specifically addressing the development of an online sales team equipped with hologram-projecting equipment. The report discusses the relevant accounting standards, particularly AASB 138, and determines whether the development costs should be expensed or capitalized based on specific criteria. It includes calculations related to depreciation and amortization, and provides references to support its analysis. The report offers a comprehensive understanding of financial accounting principles and their application in various business contexts.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.