Financial Accounting Process Report - Finance Accounting Principles

VerifiedAdded on 2023/06/05

|6

|1200

|395

Report

AI Summary

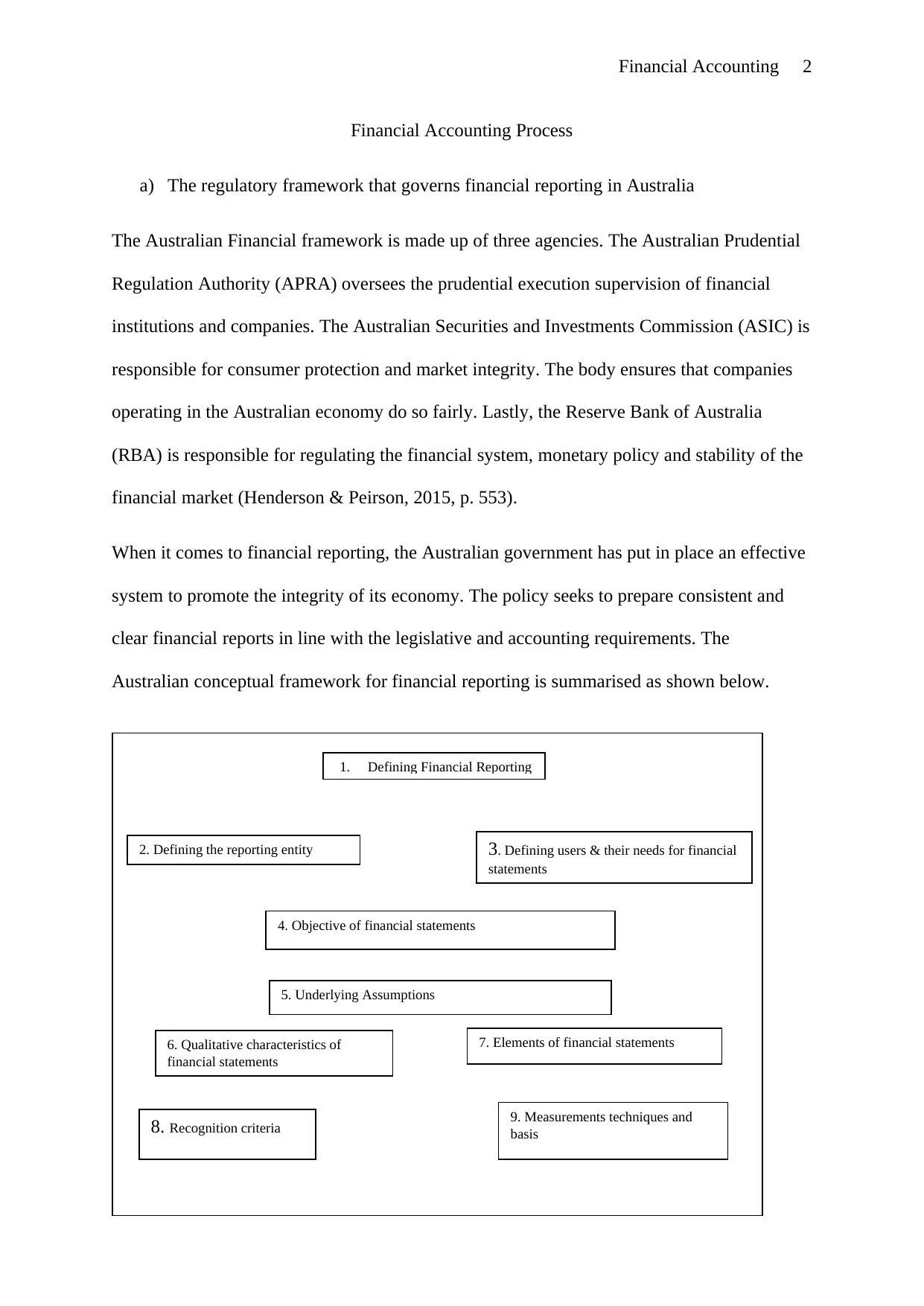

This report provides a detailed analysis of the financial accounting process within the Australian context. It begins by outlining the regulatory framework that governs financial reporting in Australia, including the roles of APRA, ASIC, and the Reserve Bank of Australia, and the Australian Accounting Standard Board (AASB). The report then examines the process of accounting for non-current assets, revenue recognition under AASB 15, and liabilities. It differentiates between shares and debentures, highlighting their key differences in terms of ownership, return, convertibility, and control. The report references various sources including AASB standards and provides a comprehensive overview of financial accounting principles and practices.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.