ACCT6003 Financial Accounting Processes Assignment Solution - Part 2

VerifiedAdded on 2023/06/10

|14

|1440

|148

Homework Assignment

AI Summary

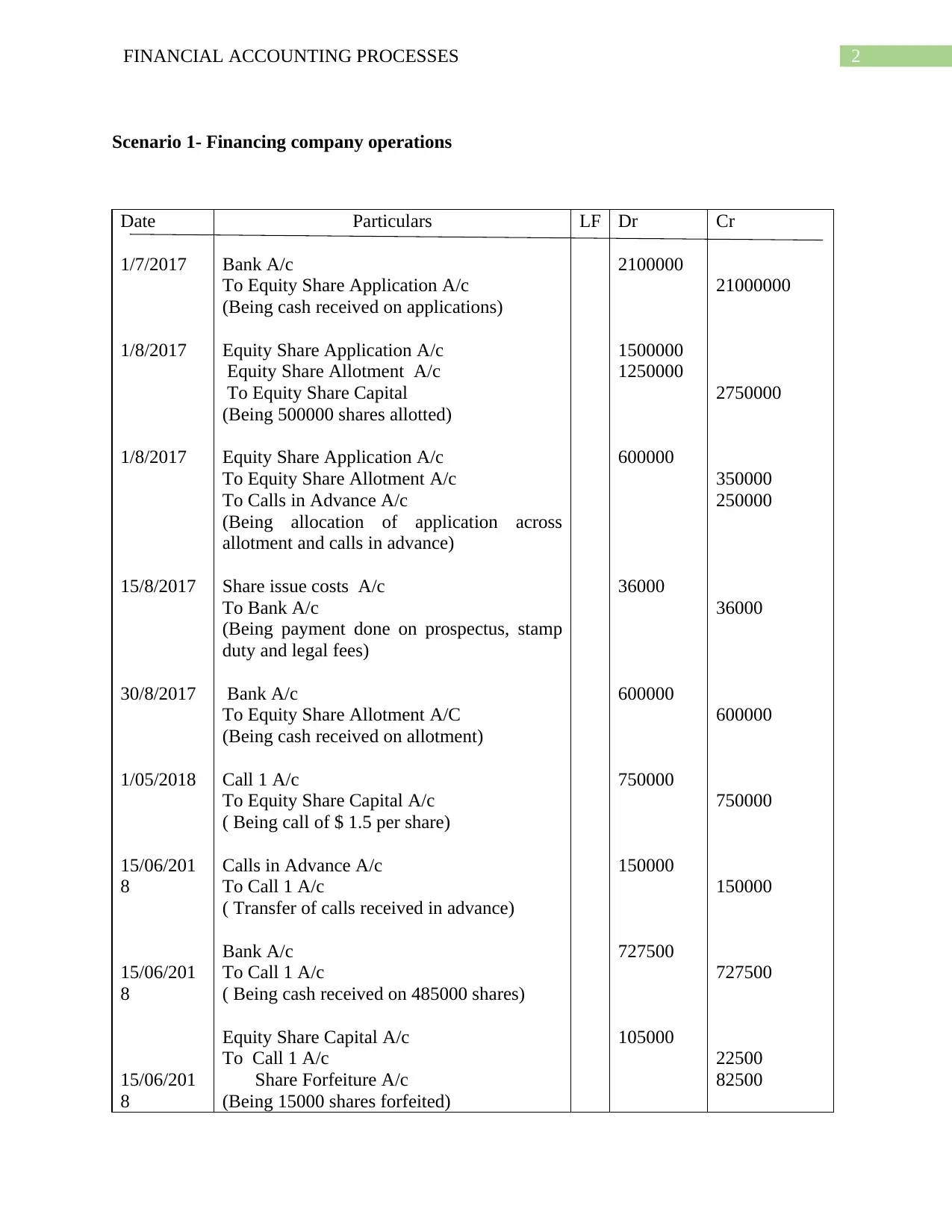

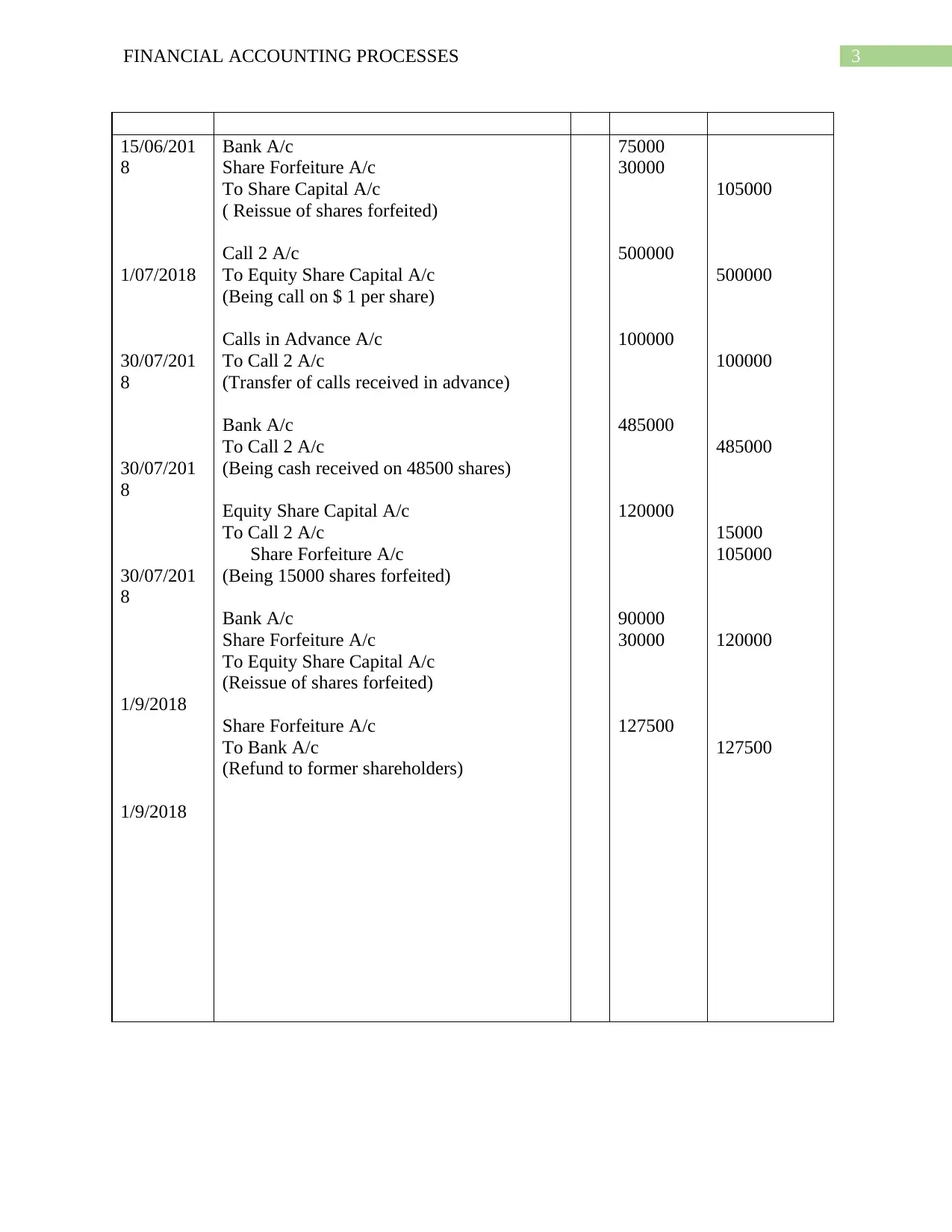

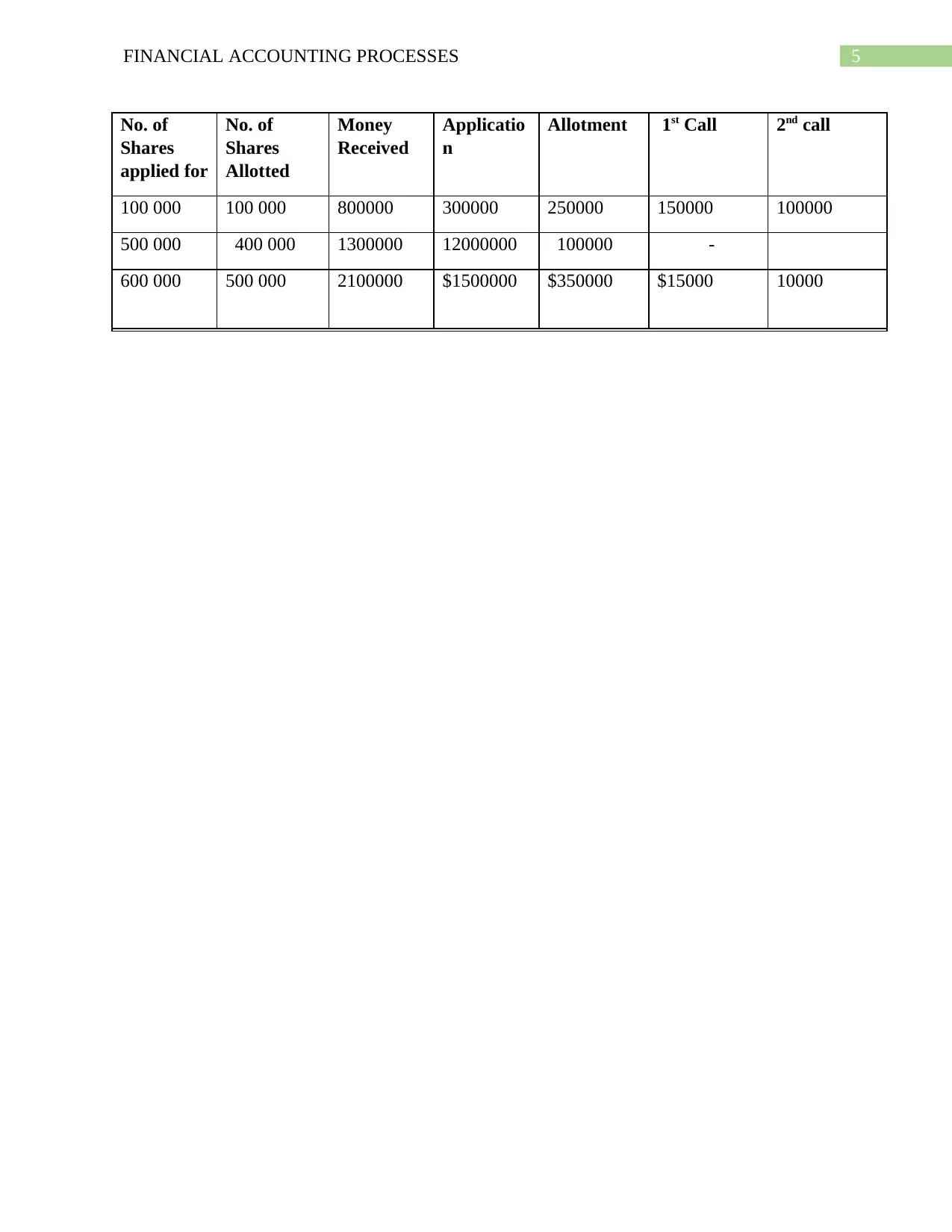

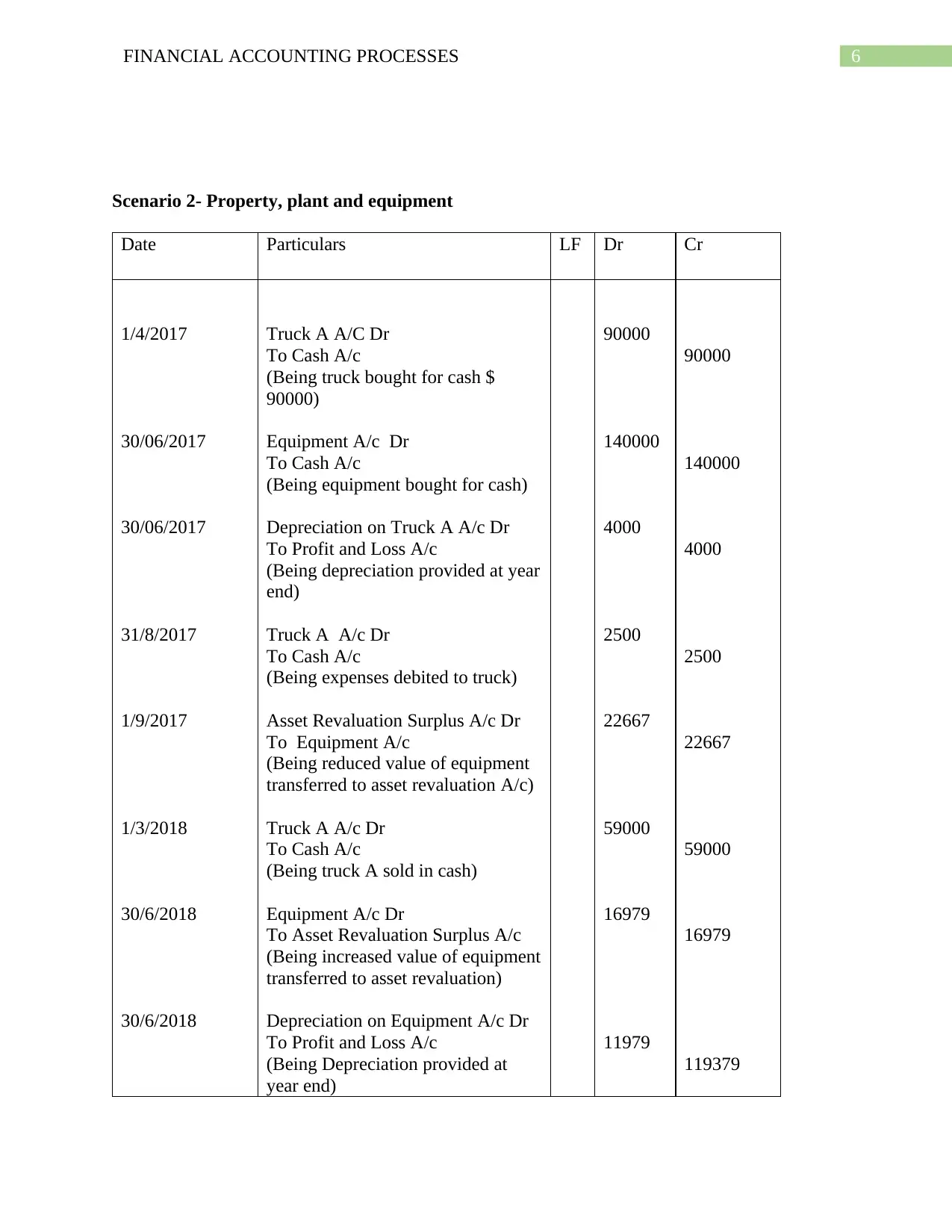

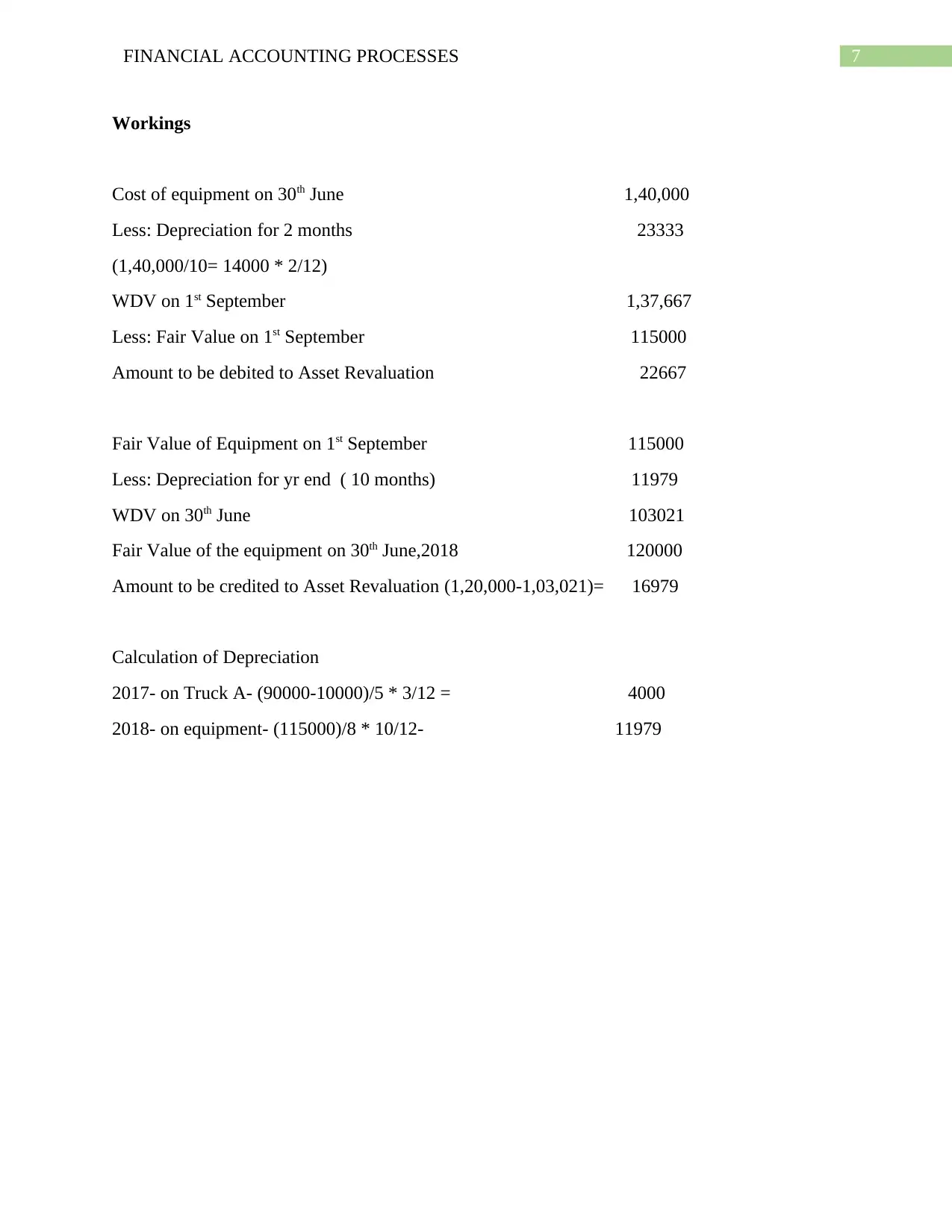

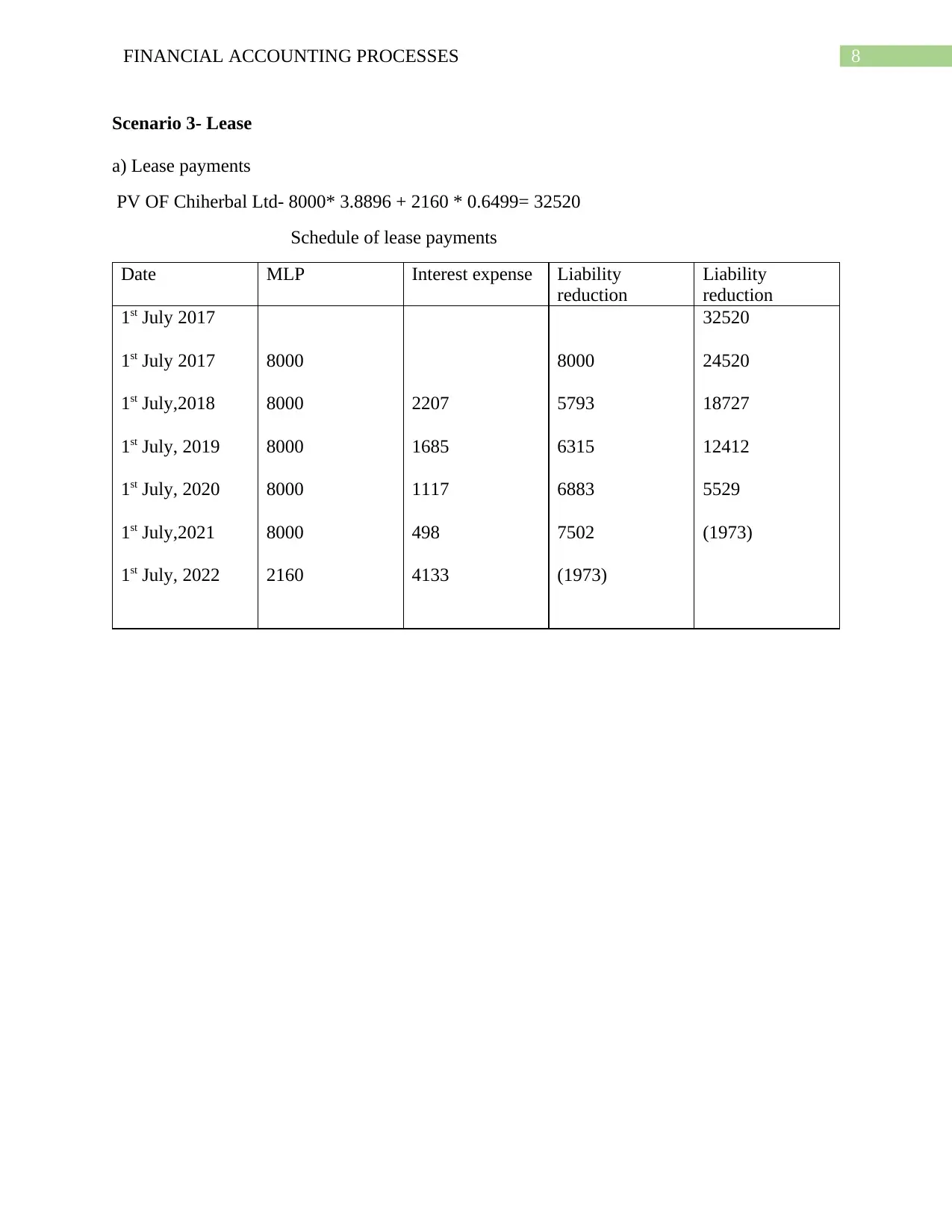

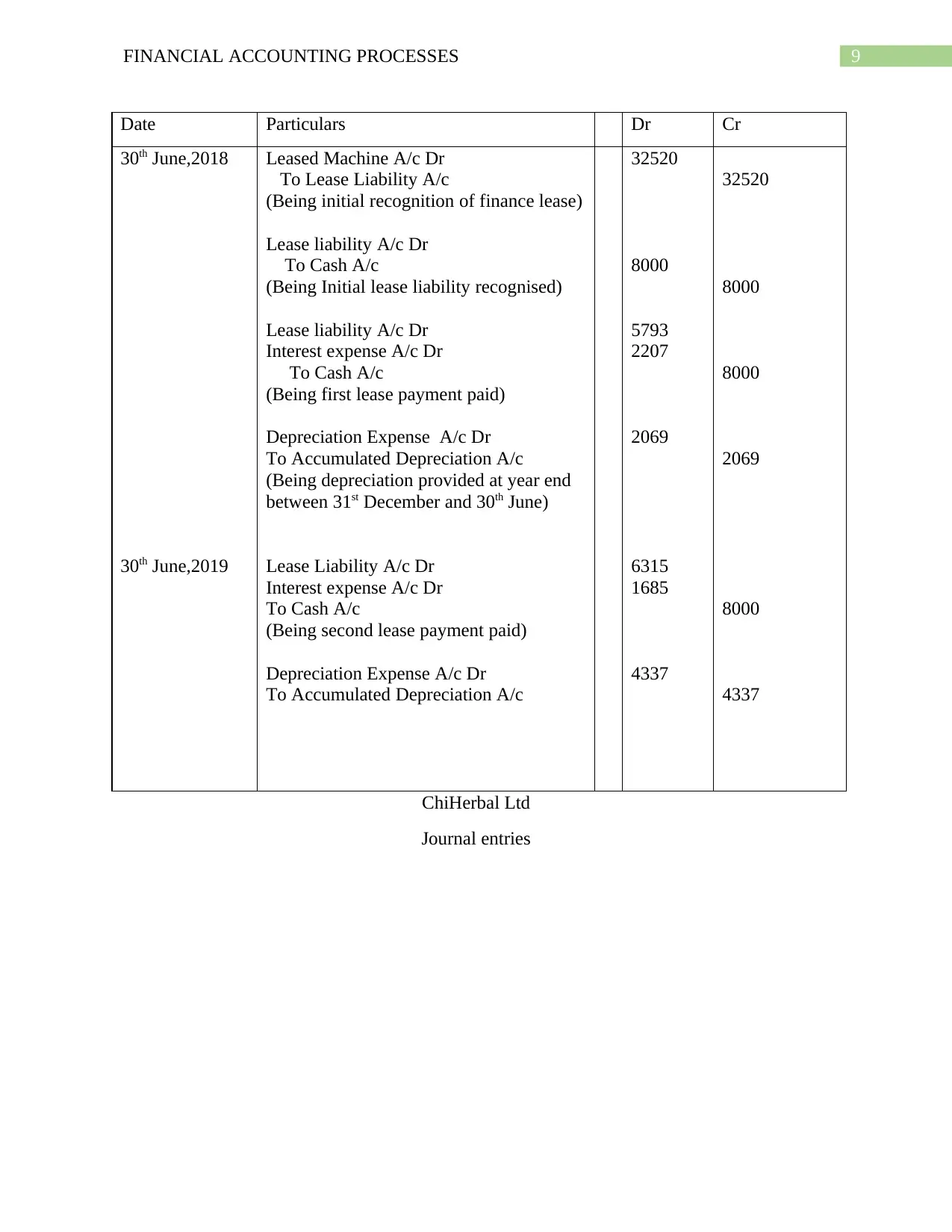

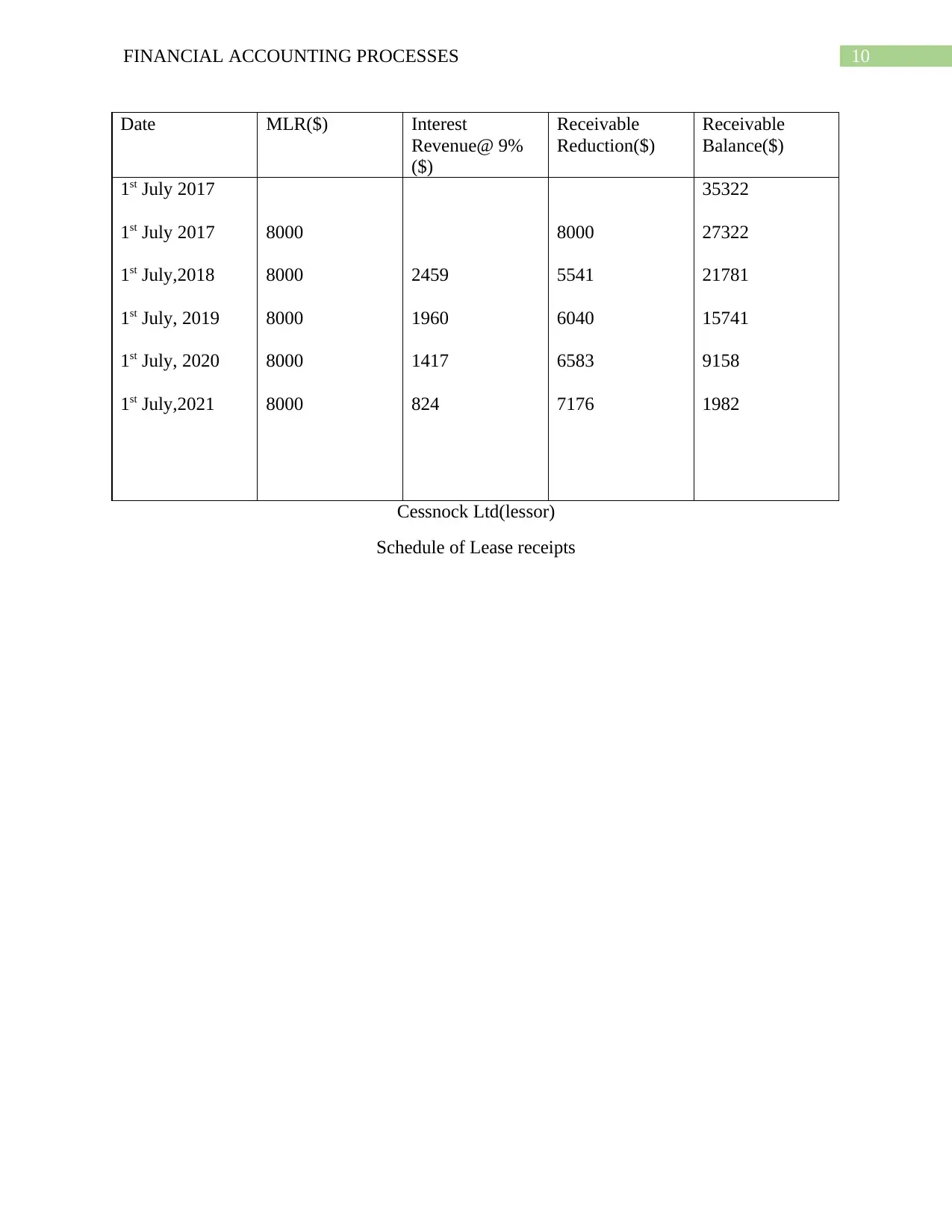

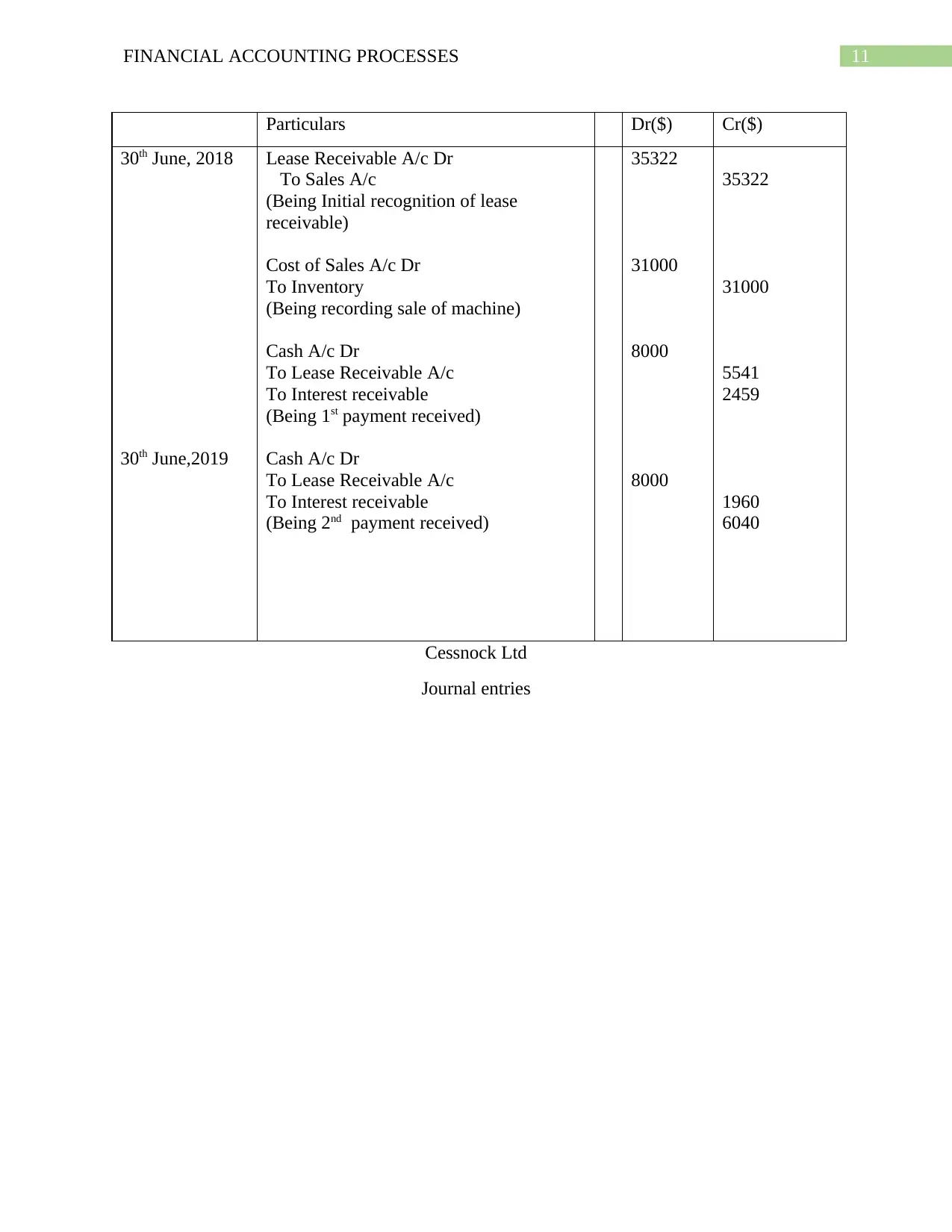

This assignment solution addresses various financial accounting processes for ChiHerbal Ltd. It begins with scenario-based journal entries for financing company operations, including share issuance, allotment, and calls, complete with working notes. The second scenario focuses on property, plant, and equipment, detailing transactions such as asset purchases, depreciation, and revaluation, with corresponding calculations. The third scenario explores lease accounting, outlining lease payments, journal entries for both the lessee (ChiHerbal Ltd) and the lessor (Cessnock Ltd), and schedule of lease receipts and payments. Finally, the solution discusses intangible assets, specifically addressing the accounting treatment for development costs and internally generated software, referencing IAS 38. The solution provides detailed calculations, journal entries, and explanations to comprehensively cover the accounting principles and standards applied in each scenario.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.