Advanced Financial Accounting: CBU, Qantas, and Cash Flow Analysis

VerifiedAdded on 2021/06/15

|14

|1469

|342

Report

AI Summary

This comprehensive financial accounting report delves into several key areas of business finance. It begins by defining Cash Generating Units (CBU) as per AASB 136, discussing their significance in asset impairment, and analyzing Wentnor Dairy Ltd. The report then examines Qantas Ltd, calculating and interpreting significant financial ratios for 2017 to assess the company's performance in areas such as profitability, solvency, and efficiency. The analysis includes an examination of foreign currency transactions and their accounting treatment. Finally, the report demonstrates the preparation of a cash flow statement using both the direct and indirect methods, providing a complete overview of financial statement analysis and accounting principles. The report also includes appendices with ratio calculations and figures illustrating the cash flow statements.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student:

Name of the University:

Author’s Note

Advanced Financial Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED FINANCIAL ACCOUNTING

Executive Summary

The assignment consists of four parts which are related to different areas of different business.

The first question, Cash Generating Units (CBU) is to defined as per AASB 136 which is on

impairment of assets and discuss why a business recognizes CBU for the purpose of

impairments. The first part will be based on analysis of company Wentnor Dairy ltd for which

discussions are to be made. The second question requires calculations of significant ratios of

Qantas ltd for the year 2017 and analyzing the same to determine performance of the business.

The third question also relates to Qantas ltd where facts and treatments of foreign transaction

will be discussed. The last question will be showing a cash flow statement prepared on the basis

of both indirect and direct method.

ADVANCED FINANCIAL ACCOUNTING

Executive Summary

The assignment consists of four parts which are related to different areas of different business.

The first question, Cash Generating Units (CBU) is to defined as per AASB 136 which is on

impairment of assets and discuss why a business recognizes CBU for the purpose of

impairments. The first part will be based on analysis of company Wentnor Dairy ltd for which

discussions are to be made. The second question requires calculations of significant ratios of

Qantas ltd for the year 2017 and analyzing the same to determine performance of the business.

The third question also relates to Qantas ltd where facts and treatments of foreign transaction

will be discussed. The last question will be showing a cash flow statement prepared on the basis

of both indirect and direct method.

2

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Answer to Question 1......................................................................................................................3

Requirement A.............................................................................................................................3

Requirement B.............................................................................................................................3

Requirement C.............................................................................................................................4

Answer to Question 2......................................................................................................................4

Requirement A.............................................................................................................................4

Requirement B.............................................................................................................................4

Requirement C.............................................................................................................................5

Answer to Question 3......................................................................................................................6

Answer to Question 4......................................................................................................................7

Reference.......................................................................................................................................11

Appendix........................................................................................................................................12

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Answer to Question 1......................................................................................................................3

Requirement A.............................................................................................................................3

Requirement B.............................................................................................................................3

Requirement C.............................................................................................................................4

Answer to Question 2......................................................................................................................4

Requirement A.............................................................................................................................4

Requirement B.............................................................................................................................4

Requirement C.............................................................................................................................5

Answer to Question 3......................................................................................................................6

Answer to Question 4......................................................................................................................7

Reference.......................................................................................................................................11

Appendix........................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED FINANCIAL ACCOUNTING

Answer to Question 1

Requirement A

As per the provisions which is set out in para 6 of AASB 136 “Impairment of Assets”

states that a cash generating unit is the smallest group of assets which can be identified which are

capable of generating cash inflows and are independent from the assets which belongs to other

groups. For the purpose of charging impairment, assets are identified in CBUs (Bond, Govendir

and Wells 2016).

Requirement B

As per the provision which is stated in AASB 136, the test of impairment on the assets of

the company requires appropriate comparison of recoverable amount which is to be higher of the

asset value or fair value of the asset less cost of disposal of the asset. As per the standard, value

in use measurement requires the estimate of the future cash flows that the business estimates that

they will be receiving from the use of the asset (Guthrie and Pang 2013). The expectation about

the timing of the cash flow of the business. The price for bearing the uncertainty of the assets.

There are certain assets needs to be taken in group to effectively calculate the cash which

is generated from the use of the asset. The machines which are used by Wentnor Dairy ltd does

not generate cash flow on their own but are to be taken as a group to identify the cash which is

generated from such an asset. The main source of cash inflow for the business is through

producing milk and milk related products. The machine such as purifying machines and

extracting machine are taken togethers as a group of assets when impairment is charged as per

respective provisions.

ADVANCED FINANCIAL ACCOUNTING

Answer to Question 1

Requirement A

As per the provisions which is set out in para 6 of AASB 136 “Impairment of Assets”

states that a cash generating unit is the smallest group of assets which can be identified which are

capable of generating cash inflows and are independent from the assets which belongs to other

groups. For the purpose of charging impairment, assets are identified in CBUs (Bond, Govendir

and Wells 2016).

Requirement B

As per the provision which is stated in AASB 136, the test of impairment on the assets of

the company requires appropriate comparison of recoverable amount which is to be higher of the

asset value or fair value of the asset less cost of disposal of the asset. As per the standard, value

in use measurement requires the estimate of the future cash flows that the business estimates that

they will be receiving from the use of the asset (Guthrie and Pang 2013). The expectation about

the timing of the cash flow of the business. The price for bearing the uncertainty of the assets.

There are certain assets needs to be taken in group to effectively calculate the cash which

is generated from the use of the asset. The machines which are used by Wentnor Dairy ltd does

not generate cash flow on their own but are to be taken as a group to identify the cash which is

generated from such an asset. The main source of cash inflow for the business is through

producing milk and milk related products. The machine such as purifying machines and

extracting machine are taken togethers as a group of assets when impairment is charged as per

respective provisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED FINANCIAL ACCOUNTING

Requirement C

There are various factors which are used for identifying the cash generating units of a

business which involves identifying the lowest value of assets which can be which can act

independently for generating cash flow for the business. The chief financial officer needs to

identify the cash generating units of the business which will as per the requirement of AASB

136.

The CFO of the business needs to identify cash generating units of the business from year

to year basis consistently unless there are some changes has occurred to the asset of the

company. The recognition of cash generating units requires accurate judgements on the part of

the management and also following the AASB 136 which is on Impairment of assets of the

business.

Answer to Question 2

Requirement A

As per this question, significant ratios which deals with different areas of business such

as profitability, solvency, efficiency and other areas of business. The computation of significant

ratios is shown in the Appendix.

Requirement B

The current ratio and the acid test ratio as shown in the appendix shows that the business

is having unfavorable estimates when it comes to liquidity ratio. The current ratio and quick ratio

is shown as 0.793 and 0.330 respectively for the year 2017. The ratio reveals that the business is

facing liquidity problems. The gross profit ratio of the business shows that the same has

ADVANCED FINANCIAL ACCOUNTING

Requirement C

There are various factors which are used for identifying the cash generating units of a

business which involves identifying the lowest value of assets which can be which can act

independently for generating cash flow for the business. The chief financial officer needs to

identify the cash generating units of the business which will as per the requirement of AASB

136.

The CFO of the business needs to identify cash generating units of the business from year

to year basis consistently unless there are some changes has occurred to the asset of the

company. The recognition of cash generating units requires accurate judgements on the part of

the management and also following the AASB 136 which is on Impairment of assets of the

business.

Answer to Question 2

Requirement A

As per this question, significant ratios which deals with different areas of business such

as profitability, solvency, efficiency and other areas of business. The computation of significant

ratios is shown in the Appendix.

Requirement B

The current ratio and the acid test ratio as shown in the appendix shows that the business

is having unfavorable estimates when it comes to liquidity ratio. The current ratio and quick ratio

is shown as 0.793 and 0.330 respectively for the year 2017. The ratio reveals that the business is

facing liquidity problems. The gross profit ratio of the business shows that the same has

5

ADVANCED FINANCIAL ACCOUNTING

improved from the previous year which is shown to be 28.71% as per calculation which is shown

for 2017. The receivable turnover ratio of the company has also improved from the previous year

and the same is shown as 74.49 for the year 2017 and the same is shown to be 70.00 for the year

2016. The receivable turnover ratio signifies that the receivable period is strong. The return on

assets and return on equity have significantly improved from the previous year (Moghimi and

Anvari 2014). The return on equity of the business shows that the same has tremendously

improved from previous year’s estimate which suggest that the business is growing and meeting

the expectation of the shareholders of the company. The dividend payout ratio for 2017 is shown

as 70.35% which has tremendously improved from the previous year’s analysis. It can be

effectively concluded that the potential investors should invest in the shares of the company as

the company has a favorable gross margin and has appropriate return on equity which suggests

that the company is meeting the expectations of the shareholders effectively. However, the

company needs to improve the liquidity of the business which can pose a concern in the long run

operations of the business.

Requirement C

The current ratio and quick ratio of the business shows that the ratio for the year 2017 is

0.793 and 0.330 respectively. The ratio which is computed does not matches with the ideal ratio

for current ratio and quick ratio which is 2:1 and 1.5:1. The ratio which is computed for

Woolsworth ltd shows that the business is facing liquidity problems which the business needs to

solve as quickly as possible. The ideal standard for current and quick ratio are given above which

every company needs to consider and try to maintain when measuring the financial performance

of the business. The current ratio and quick ratio represent liquidity situation in the business and

therefore the company needs to improve the same.

ADVANCED FINANCIAL ACCOUNTING

improved from the previous year which is shown to be 28.71% as per calculation which is shown

for 2017. The receivable turnover ratio of the company has also improved from the previous year

and the same is shown as 74.49 for the year 2017 and the same is shown to be 70.00 for the year

2016. The receivable turnover ratio signifies that the receivable period is strong. The return on

assets and return on equity have significantly improved from the previous year (Moghimi and

Anvari 2014). The return on equity of the business shows that the same has tremendously

improved from previous year’s estimate which suggest that the business is growing and meeting

the expectation of the shareholders of the company. The dividend payout ratio for 2017 is shown

as 70.35% which has tremendously improved from the previous year’s analysis. It can be

effectively concluded that the potential investors should invest in the shares of the company as

the company has a favorable gross margin and has appropriate return on equity which suggests

that the company is meeting the expectations of the shareholders effectively. However, the

company needs to improve the liquidity of the business which can pose a concern in the long run

operations of the business.

Requirement C

The current ratio and quick ratio of the business shows that the ratio for the year 2017 is

0.793 and 0.330 respectively. The ratio which is computed does not matches with the ideal ratio

for current ratio and quick ratio which is 2:1 and 1.5:1. The ratio which is computed for

Woolsworth ltd shows that the business is facing liquidity problems which the business needs to

solve as quickly as possible. The ideal standard for current and quick ratio are given above which

every company needs to consider and try to maintain when measuring the financial performance

of the business. The current ratio and quick ratio represent liquidity situation in the business and

therefore the company needs to improve the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCED FINANCIAL ACCOUNTING

Answer to Question 3

As per the paragraph which is given deals with the transactions which are related to

foreign trade and involves translation of foreign currency into domestic currency. The technique

which is used mostly for translation of currency is current rate method. The paragraph which

forms a part of the notes to accounts section suggest that the company has engaged in foreign

transaction during the year (Boesch et al. 2013).

The basic reasons due to which the foreign exchange translation difference arises due to

fluctuation in the rate of foreign currency. The difference in foreign currency is recognized in the

comprehensive income statement and any gains is transferred to the Foreign currency translation

reserve account.

ADVANCED FINANCIAL ACCOUNTING

Answer to Question 3

As per the paragraph which is given deals with the transactions which are related to

foreign trade and involves translation of foreign currency into domestic currency. The technique

which is used mostly for translation of currency is current rate method. The paragraph which

forms a part of the notes to accounts section suggest that the company has engaged in foreign

transaction during the year (Boesch et al. 2013).

The basic reasons due to which the foreign exchange translation difference arises due to

fluctuation in the rate of foreign currency. The difference in foreign currency is recognized in the

comprehensive income statement and any gains is transferred to the Foreign currency translation

reserve account.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

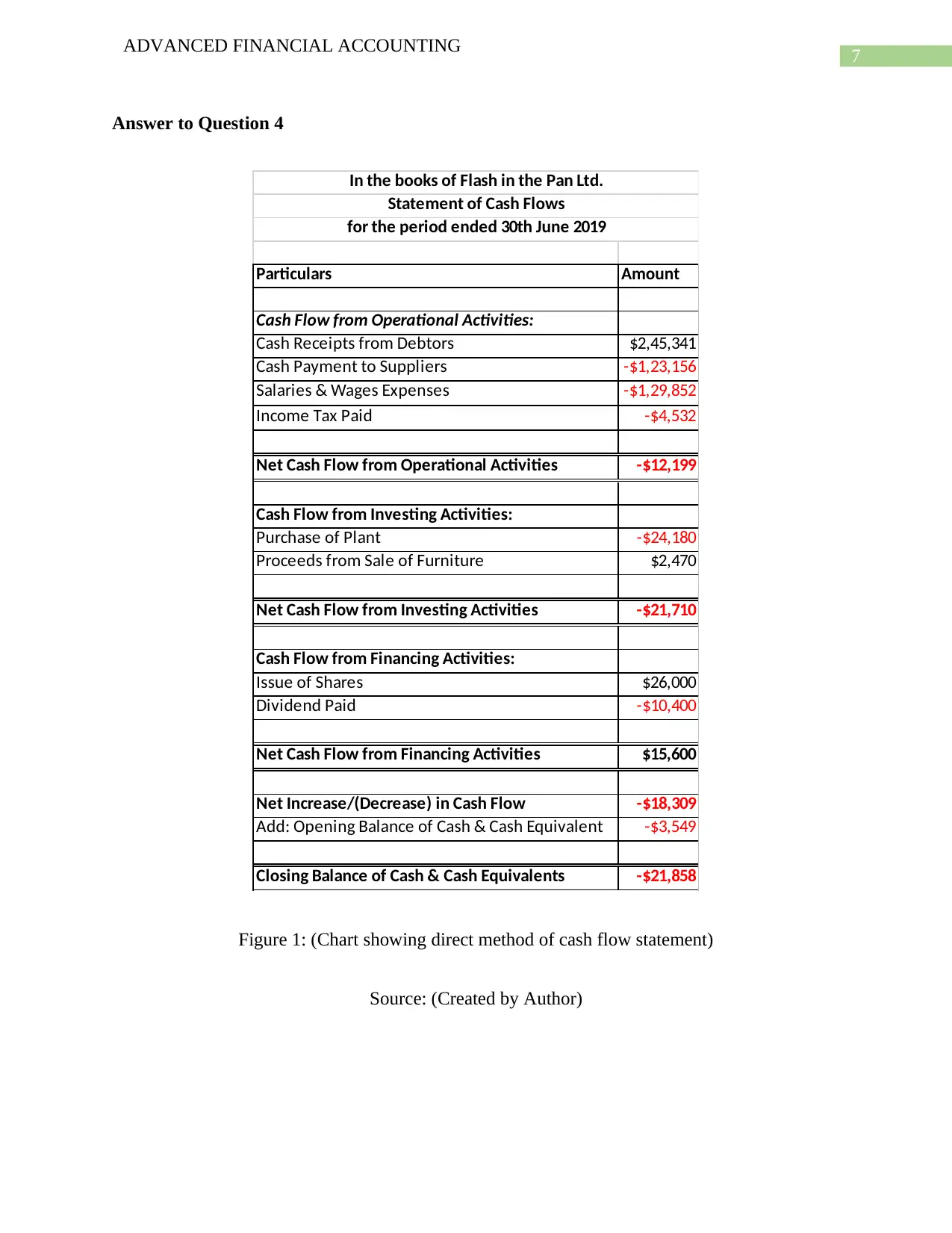

Answer to Question 4

Particulars Amount

Cash Flow from Operational Activities:

Cash Receipts from Debtors $2,45,341

Cash Payment to Suppliers -$1,23,156

Salaries & Wages Expenses -$1,29,852

Income Tax Paid -$4,532

Net Cash Flow from Operational Activities -$12,199

Cash Flow from Investing Activities:

Purchase of Plant -$24,180

Proceeds from Sale of Furniture $2,470

Net Cash Flow from Investing Activities -$21,710

Cash Flow from Financing Activities:

Issue of Shares $26,000

Dividend Paid -$10,400

Net Cash Flow from Financing Activities $15,600

Net Increase/(Decrease) in Cash Flow -$18,309

Add: Opening Balance of Cash & Cash Equivalent -$3,549

Closing Balance of Cash & Cash Equivalents -$21,858

In the books of Flash in the Pan Ltd.

Statement of Cash Flows

for the period ended 30th June 2019

Figure 1: (Chart showing direct method of cash flow statement)

Source: (Created by Author)

ADVANCED FINANCIAL ACCOUNTING

Answer to Question 4

Particulars Amount

Cash Flow from Operational Activities:

Cash Receipts from Debtors $2,45,341

Cash Payment to Suppliers -$1,23,156

Salaries & Wages Expenses -$1,29,852

Income Tax Paid -$4,532

Net Cash Flow from Operational Activities -$12,199

Cash Flow from Investing Activities:

Purchase of Plant -$24,180

Proceeds from Sale of Furniture $2,470

Net Cash Flow from Investing Activities -$21,710

Cash Flow from Financing Activities:

Issue of Shares $26,000

Dividend Paid -$10,400

Net Cash Flow from Financing Activities $15,600

Net Increase/(Decrease) in Cash Flow -$18,309

Add: Opening Balance of Cash & Cash Equivalent -$3,549

Closing Balance of Cash & Cash Equivalents -$21,858

In the books of Flash in the Pan Ltd.

Statement of Cash Flows

for the period ended 30th June 2019

Figure 1: (Chart showing direct method of cash flow statement)

Source: (Created by Author)

8

ADVANCED FINANCIAL ACCOUNTING

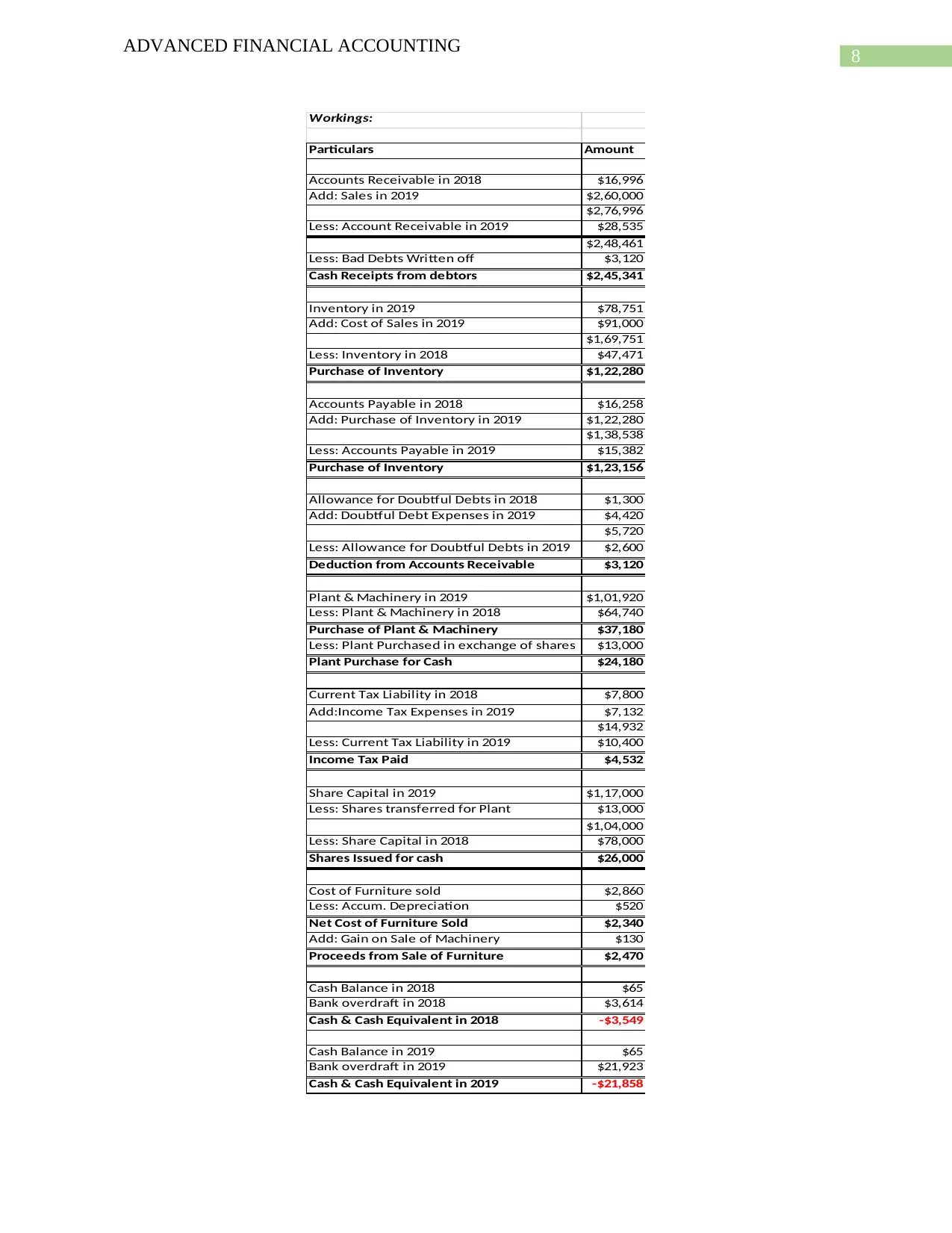

Workings:

Particulars Amount

Accounts Receivable in 2018 $16,996

Add: Sales in 2019 $2,60,000

$2,76,996

Less: Account Receivable in 2019 $28,535

$2,48,461

Less: Bad Debts Written off $3,120

Cash Receipts from debtors $2,45,341

Inventory in 2019 $78,751

Add: Cost of Sales in 2019 $91,000

$1,69,751

Less: Inventory in 2018 $47,471

Purchase of Inventory $1,22,280

Accounts Payable in 2018 $16,258

Add: Purchase of Inventory in 2019 $1,22,280

$1,38,538

Less: Accounts Payable in 2019 $15,382

Purchase of Inventory $1,23,156

Allowance for Doubtful Debts in 2018 $1,300

Add: Doubtful Debt Expenses in 2019 $4,420

$5,720

Less: Allowance for Doubtful Debts in 2019 $2,600

Deduction from Accounts Receivable $3,120

Plant & Machinery in 2019 $1,01,920

Less: Plant & Machinery in 2018 $64,740

Purchase of Plant & Machinery $37,180

Less: Plant Purchased in exchange of shares $13,000

Plant Purchase for Cash $24,180

Current Tax Liability in 2018 $7,800

Add:Income Tax Expenses in 2019 $7,132

$14,932

Less: Current Tax Liability in 2019 $10,400

Income Tax Paid $4,532

Share Capital in 2019 $1,17,000

Less: Shares transferred for Plant $13,000

$1,04,000

Less: Share Capital in 2018 $78,000

Shares Issued for cash $26,000

Cost of Furniture sold $2,860

Less: Accum. Depreciation $520

Net Cost of Furniture Sold $2,340

Add: Gain on Sale of Machinery $130

Proceeds from Sale of Furniture $2,470

Cash Balance in 2018 $65

Bank overdraft in 2018 $3,614

Cash & Cash Equivalent in 2018 -$3,549

Cash Balance in 2019 $65

Bank overdraft in 2019 $21,923

Cash & Cash Equivalent in 2019 -$21,858

ADVANCED FINANCIAL ACCOUNTING

Workings:

Particulars Amount

Accounts Receivable in 2018 $16,996

Add: Sales in 2019 $2,60,000

$2,76,996

Less: Account Receivable in 2019 $28,535

$2,48,461

Less: Bad Debts Written off $3,120

Cash Receipts from debtors $2,45,341

Inventory in 2019 $78,751

Add: Cost of Sales in 2019 $91,000

$1,69,751

Less: Inventory in 2018 $47,471

Purchase of Inventory $1,22,280

Accounts Payable in 2018 $16,258

Add: Purchase of Inventory in 2019 $1,22,280

$1,38,538

Less: Accounts Payable in 2019 $15,382

Purchase of Inventory $1,23,156

Allowance for Doubtful Debts in 2018 $1,300

Add: Doubtful Debt Expenses in 2019 $4,420

$5,720

Less: Allowance for Doubtful Debts in 2019 $2,600

Deduction from Accounts Receivable $3,120

Plant & Machinery in 2019 $1,01,920

Less: Plant & Machinery in 2018 $64,740

Purchase of Plant & Machinery $37,180

Less: Plant Purchased in exchange of shares $13,000

Plant Purchase for Cash $24,180

Current Tax Liability in 2018 $7,800

Add:Income Tax Expenses in 2019 $7,132

$14,932

Less: Current Tax Liability in 2019 $10,400

Income Tax Paid $4,532

Share Capital in 2019 $1,17,000

Less: Shares transferred for Plant $13,000

$1,04,000

Less: Share Capital in 2018 $78,000

Shares Issued for cash $26,000

Cost of Furniture sold $2,860

Less: Accum. Depreciation $520

Net Cost of Furniture Sold $2,340

Add: Gain on Sale of Machinery $130

Proceeds from Sale of Furniture $2,470

Cash Balance in 2018 $65

Bank overdraft in 2018 $3,614

Cash & Cash Equivalent in 2018 -$3,549

Cash Balance in 2019 $65

Bank overdraft in 2019 $21,923

Cash & Cash Equivalent in 2019 -$21,858

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED FINANCIAL ACCOUNTING

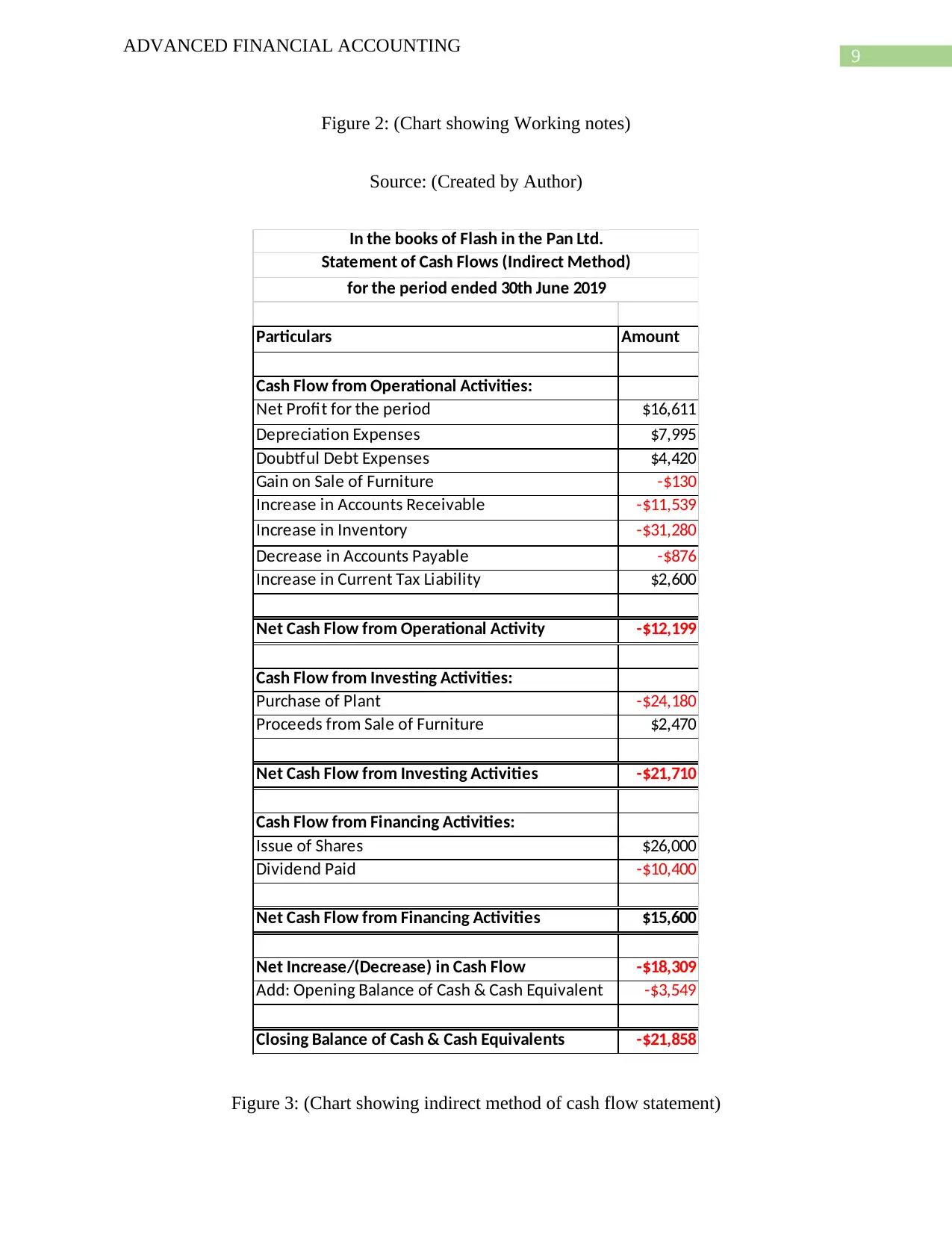

Figure 2: (Chart showing Working notes)

Source: (Created by Author)

Particulars Amount

Cash Flow from Operational Activities:

Net Profit for the period $16,611

Depreciation Expenses $7,995

Doubtful Debt Expenses $4,420

Gain on Sale of Furniture -$130

Increase in Accounts Receivable -$11,539

Increase in Inventory -$31,280

Decrease in Accounts Payable -$876

Increase in Current Tax Liability $2,600

Net Cash Flow from Operational Activity -$12,199

Cash Flow from Investing Activities:

Purchase of Plant -$24,180

Proceeds from Sale of Furniture $2,470

Net Cash Flow from Investing Activities -$21,710

Cash Flow from Financing Activities:

Issue of Shares $26,000

Dividend Paid -$10,400

Net Cash Flow from Financing Activities $15,600

Net Increase/(Decrease) in Cash Flow -$18,309

Add: Opening Balance of Cash & Cash Equivalent -$3,549

Closing Balance of Cash & Cash Equivalents -$21,858

In the books of Flash in the Pan Ltd.

Statement of Cash Flows (Indirect Method)

for the period ended 30th June 2019

Figure 3: (Chart showing indirect method of cash flow statement)

ADVANCED FINANCIAL ACCOUNTING

Figure 2: (Chart showing Working notes)

Source: (Created by Author)

Particulars Amount

Cash Flow from Operational Activities:

Net Profit for the period $16,611

Depreciation Expenses $7,995

Doubtful Debt Expenses $4,420

Gain on Sale of Furniture -$130

Increase in Accounts Receivable -$11,539

Increase in Inventory -$31,280

Decrease in Accounts Payable -$876

Increase in Current Tax Liability $2,600

Net Cash Flow from Operational Activity -$12,199

Cash Flow from Investing Activities:

Purchase of Plant -$24,180

Proceeds from Sale of Furniture $2,470

Net Cash Flow from Investing Activities -$21,710

Cash Flow from Financing Activities:

Issue of Shares $26,000

Dividend Paid -$10,400

Net Cash Flow from Financing Activities $15,600

Net Increase/(Decrease) in Cash Flow -$18,309

Add: Opening Balance of Cash & Cash Equivalent -$3,549

Closing Balance of Cash & Cash Equivalents -$21,858

In the books of Flash in the Pan Ltd.

Statement of Cash Flows (Indirect Method)

for the period ended 30th June 2019

Figure 3: (Chart showing indirect method of cash flow statement)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED FINANCIAL ACCOUNTING

Source: (Created by Author)

ADVANCED FINANCIAL ACCOUNTING

Source: (Created by Author)

11

ADVANCED FINANCIAL ACCOUNTING

Reference

Boesch, B.P., Crocker, S.D., Eastlake III, D.E., Hart Jr, A.S., Jackson, A., Lindenberg, R.A. and

Paredes, D.M., PayPal International Ltd and PayPal Inc, 2013. System and method for multi-

currency transactions. U.S. Patent Application 12/855,603.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Guthrie, J. and Pang, T.T., 2013. Disclosure of Goodwill Impairment under AASB 136 from

2005–2010. Australian Accounting Review, 23(3), pp.216-231.

Moghimi, R. and Anvari, A., 2014. An integrated fuzzy MCDM approach and analysis to

evaluate the financial performance of Iranian cement companies. The International Journal of

Advanced Manufacturing Technology, 71(1-4), pp.685-698.

ADVANCED FINANCIAL ACCOUNTING

Reference

Boesch, B.P., Crocker, S.D., Eastlake III, D.E., Hart Jr, A.S., Jackson, A., Lindenberg, R.A. and

Paredes, D.M., PayPal International Ltd and PayPal Inc, 2013. System and method for multi-

currency transactions. U.S. Patent Application 12/855,603.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Guthrie, J. and Pang, T.T., 2013. Disclosure of Goodwill Impairment under AASB 136 from

2005–2010. Australian Accounting Review, 23(3), pp.216-231.

Moghimi, R. and Anvari, A., 2014. An integrated fuzzy MCDM approach and analysis to

evaluate the financial performance of Iranian cement companies. The International Journal of

Advanced Manufacturing Technology, 71(1-4), pp.685-698.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.