Financial Accounting: Regulations, Principles, and Analysis

VerifiedAdded on 2020/11/12

|19

|4006

|394

Report

AI Summary

This report provides a comprehensive overview of financial accounting, starting with its definition, purpose, and the regulations governing it, including the role of the International Accounting Standards Board (IASB) and International Financial Reporting Standards (IFRS). It details accounting rules, principles like conservatism and cost principles, and conventions such as consistency and material disclosure. The report includes a practical evaluation of bookkeeping and accounting systems, the preparation of financial statements, the purpose of bank reconciliation, ledger control accounts, and suspense accounts, illustrated through client examples and financial statements like profit and loss statements and balance sheets.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT .....................................................................................................................1

1. Financial accounting and its purpose......................................................................................1

2. Regulations relating to financial accounting...........................................................................2

3. Accounting rules and principles governs the presentations....................................................4

4. Conventions and concepts relating consistency and material disclosure................................5

CLIENT 1........................................................................................................................................6

CLIENT 2........................................................................................................................................9

CLIENT 3......................................................................................................................................10

CLIENT 4......................................................................................................................................14

CLIENT 5......................................................................................................................................15

CLIENT 6......................................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT .....................................................................................................................1

1. Financial accounting and its purpose......................................................................................1

2. Regulations relating to financial accounting...........................................................................2

3. Accounting rules and principles governs the presentations....................................................4

4. Conventions and concepts relating consistency and material disclosure................................5

CLIENT 1........................................................................................................................................6

CLIENT 2........................................................................................................................................9

CLIENT 3......................................................................................................................................10

CLIENT 4......................................................................................................................................14

CLIENT 5......................................................................................................................................15

CLIENT 6......................................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Financial accounting is the key field of accounting which remain associated with

analysing, summarising and reposting the financial transaction. It furnishes management a path

to deal with financial challenges and problems (Bellanca and Vandernoot, 2014). By

implementing financial rules and principles, managers be able to gather, summarise, bifurcate

and consolidate the financial information in a single format. This report contains two sections,

first section consist of the meaning and purpose of financial accounting, accounting rules and

principles, conventions to accounting concepts. Second portion contains practical evaluation of

bookkeeping and accounting system, preparing the financial statements, purpose of bank

reconciliation, ledger control accounts and suspense accounts that are illustrated in the

assignment.

BUSINESS REPORT

1. Financial accounting and its purpose

Financial accounting is a branch of accounting along with management accounting which

helps managers and accountants to deal with transactions and events related to finance. All the

finance related and monetary nature transactions are systematically records and summarised in

financial accounting. Financial analysis, forecasting, planning and controlling are the main

objective of financial accounting. Main purpose of financial accounting is to collect, summarise,

bifurcate and produce financial reports. It is essential part of organisation to make the

organisational structure viable and effective from stakeholders, owners, clients and director's

perspective.

Purpose of financial accounting

Providing accurate and fair financial report is the main purpose of financial accounting.

There are type of financial statements that are prepared under financial accounting which

represents and define the entire position and control of organisation.

Cash flow statement: This statement is prepared to analyse the fluctuation of cash

within operation and management. This statement provide brief information of fluctuation of

cash for a specific time duration. Information mainly bifurcated in major three categories as cash

generated form operation activities and functions, cash flow generated from investing activity

and cash flow generated by financing activity.

1

Financial accounting is the key field of accounting which remain associated with

analysing, summarising and reposting the financial transaction. It furnishes management a path

to deal with financial challenges and problems (Bellanca and Vandernoot, 2014). By

implementing financial rules and principles, managers be able to gather, summarise, bifurcate

and consolidate the financial information in a single format. This report contains two sections,

first section consist of the meaning and purpose of financial accounting, accounting rules and

principles, conventions to accounting concepts. Second portion contains practical evaluation of

bookkeeping and accounting system, preparing the financial statements, purpose of bank

reconciliation, ledger control accounts and suspense accounts that are illustrated in the

assignment.

BUSINESS REPORT

1. Financial accounting and its purpose

Financial accounting is a branch of accounting along with management accounting which

helps managers and accountants to deal with transactions and events related to finance. All the

finance related and monetary nature transactions are systematically records and summarised in

financial accounting. Financial analysis, forecasting, planning and controlling are the main

objective of financial accounting. Main purpose of financial accounting is to collect, summarise,

bifurcate and produce financial reports. It is essential part of organisation to make the

organisational structure viable and effective from stakeholders, owners, clients and director's

perspective.

Purpose of financial accounting

Providing accurate and fair financial report is the main purpose of financial accounting.

There are type of financial statements that are prepared under financial accounting which

represents and define the entire position and control of organisation.

Cash flow statement: This statement is prepared to analyse the fluctuation of cash

within operation and management. This statement provide brief information of fluctuation of

cash for a specific time duration. Information mainly bifurcated in major three categories as cash

generated form operation activities and functions, cash flow generated from investing activity

and cash flow generated by financing activity.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial position statement: For investors and stakeholders's point of view, it is very

important to analyse the financial position of organisation. Financial position statement is

prepared to analyse the financial position of organisation. This statement is made on the basis of

common accounting assumption that is considered as the assets remain equal to total liabilities

and capital.

Assets = capital + liabilities.

Income and expenditure statement: To analyse the profitability and control of

organisation, it is important to define the profit and loss of business. All the incomes are

compensated with expenditures and profit and loss is find out.

Change in equity statement: This statement is mainly prepared to analyse the change in

the capital structure and retain earnings. Profit, reserves, share capital are considered in this

statement (Saleh, Jaffar and Yatim, 2013). It helps to analyse the level of fluctuation of capital

and reserve in business.

2. Regulations relating to financial accounting

Ethics, rules and regulations assist the organisation to operate and execute the operations

in ethical and prominent way. Any unethical use and fluctuation is prohibited in the financial

accounting due to protecting customer interest and faith. Multinational organisation are bound to

adhere financial rules and regulation to validate the financial information form stakeholder and

owner's perspective (Palepu, Healy and Peek, 2013). Financial rules and regulations provides a

format to record financial information and details in proper manner so that stakeholders and

owners of organisation could understand the values of organisation. Financial rules and

regulations mainly helps in managing and operating the business operations with more

significant and specific manner. Accounting rules and financial representations helps in

providing effective structure to maintain and record the financial information and details in

accurate manner.

International Accounting Standard Board (IASB)

International Accounting Standard Board This is one of the essential aspect in terms of

managing the operations and functions at next level. This is one of the authoritative body which

is mainly associated with implementing the financial plans, rules and policies in subject to make

new plans and infrastructure of business. Board mainly associated with framing the framework

of completing the process of effective management and control.

2

important to analyse the financial position of organisation. Financial position statement is

prepared to analyse the financial position of organisation. This statement is made on the basis of

common accounting assumption that is considered as the assets remain equal to total liabilities

and capital.

Assets = capital + liabilities.

Income and expenditure statement: To analyse the profitability and control of

organisation, it is important to define the profit and loss of business. All the incomes are

compensated with expenditures and profit and loss is find out.

Change in equity statement: This statement is mainly prepared to analyse the change in

the capital structure and retain earnings. Profit, reserves, share capital are considered in this

statement (Saleh, Jaffar and Yatim, 2013). It helps to analyse the level of fluctuation of capital

and reserve in business.

2. Regulations relating to financial accounting

Ethics, rules and regulations assist the organisation to operate and execute the operations

in ethical and prominent way. Any unethical use and fluctuation is prohibited in the financial

accounting due to protecting customer interest and faith. Multinational organisation are bound to

adhere financial rules and regulation to validate the financial information form stakeholder and

owner's perspective (Palepu, Healy and Peek, 2013). Financial rules and regulations provides a

format to record financial information and details in proper manner so that stakeholders and

owners of organisation could understand the values of organisation. Financial rules and

regulations mainly helps in managing and operating the business operations with more

significant and specific manner. Accounting rules and financial representations helps in

providing effective structure to maintain and record the financial information and details in

accurate manner.

International Accounting Standard Board (IASB)

International Accounting Standard Board This is one of the essential aspect in terms of

managing the operations and functions at next level. This is one of the authoritative body which

is mainly associated with implementing the financial plans, rules and policies in subject to make

new plans and infrastructure of business. Board mainly associated with framing the framework

of completing the process of effective management and control.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International Financial reporting Standards (IFRS)

This is one of the major authority which helps in managing and controlling the practical

practice of accounting procedure and managing the standards in more effective manner.

Accounting standards board IASB retains the roles and liabilities to assist the technical matters

of the IFRS foundations. As the board mainly provides accounting formants and treatment for

different type of financial transactions, here are discussed some of the basic standards of IFRS

mentioned as below:

IFRS 1 (First-time approval of the standards of international financial reporting):

This rule provides a structure of presenting the financial reports for international organisations.

This rule mainly focus upon clear and complete presentation of financial records and

information.

IFRS 2 (Shared Based Payment): This rule provides a guilds and procedures regarding

treatment of losses and profit for a specific matter. IFRS 2 is formed to measure and prescribe

the revenue recognition for shared based payments. It is applied to those transactions which

remain unsettled in terms of cash and other assets.

IFRS 3 (Business Combination): This rule provides information and its details remain

associated with producing rules and articles for treatment of losses and profits. This rule help in

managing the transactions and evenest related to business combinations. It build up principles

and requirements that is how acquisition process take place in a business.

Evaluation and recognition of assets and liabilities acquired from existing business and

value of other assets acquired by acquiree form other parties.

Goodwill evaluation after acquisition or merger of existing business.

Evaluation of information to disclose and enable the financial statements to evaluate the

nature and financial effects of the business effect from the combination of business.

IFRS 9 (Financial Instruments): This rule contains the rules and procedures in terms of

identifying instruments used under financial accounting. Rule is made to classify and measure

financial assets, financial liabilities and contracts to buy or sell non-financial items and

instruments. It requires to recognise a financial assets or a financial liability in statements of

financial position when it become more viable to instruments. Financial assets and financial

liabilities are considered in this context to determine the profit and loss.

3

This is one of the major authority which helps in managing and controlling the practical

practice of accounting procedure and managing the standards in more effective manner.

Accounting standards board IASB retains the roles and liabilities to assist the technical matters

of the IFRS foundations. As the board mainly provides accounting formants and treatment for

different type of financial transactions, here are discussed some of the basic standards of IFRS

mentioned as below:

IFRS 1 (First-time approval of the standards of international financial reporting):

This rule provides a structure of presenting the financial reports for international organisations.

This rule mainly focus upon clear and complete presentation of financial records and

information.

IFRS 2 (Shared Based Payment): This rule provides a guilds and procedures regarding

treatment of losses and profit for a specific matter. IFRS 2 is formed to measure and prescribe

the revenue recognition for shared based payments. It is applied to those transactions which

remain unsettled in terms of cash and other assets.

IFRS 3 (Business Combination): This rule provides information and its details remain

associated with producing rules and articles for treatment of losses and profits. This rule help in

managing the transactions and evenest related to business combinations. It build up principles

and requirements that is how acquisition process take place in a business.

Evaluation and recognition of assets and liabilities acquired from existing business and

value of other assets acquired by acquiree form other parties.

Goodwill evaluation after acquisition or merger of existing business.

Evaluation of information to disclose and enable the financial statements to evaluate the

nature and financial effects of the business effect from the combination of business.

IFRS 9 (Financial Instruments): This rule contains the rules and procedures in terms of

identifying instruments used under financial accounting. Rule is made to classify and measure

financial assets, financial liabilities and contracts to buy or sell non-financial items and

instruments. It requires to recognise a financial assets or a financial liability in statements of

financial position when it become more viable to instruments. Financial assets and financial

liabilities are considered in this context to determine the profit and loss.

3

IFRS 10 (Consolidated statement of Finance): This is one of the essential aspect in

terms of determining and presenting the information subject to total control and management

(Păşcan, 2015). This is also one of the essential element in terms of deriving the skills and

management to next level for developing plans and diverting the skills for specific manner.

3. Accounting rules and principles governs the presentations

Accounting rules

There are three major accounting rules are found in accounting around which accounting

procedures flows or not. This is one of the essential process which helps in creating rules and

standards to make accurate financial statements and retaining the books (Louwers and et. al.,

2015). These rules are as follows:

Debit what comes in, credit what goes out: This management is utilized as a part of the

instance of genuine records. Genuine record covers every one of the records which are connected

with the advantages of the association, for example, building account, generosity account,

hardware account and so on. These benefits has a default charge adjust. As per this manage,

when an adjustment of the advantages is expanded or gotten then they are known as charge

exchanges. Apart form it, when adjust of these benefits diminish then these exchange are known

as credit exchanges.

Debit all the expenditures, losses and credit all the incomes and receivables: This

lead is connected on counterfeit records. Imitative record are the invented accounts which are

related with different costs, misfortunes, incomes and so on. As per this control, every one of the

costs are considered and recorded as charge exchanges and all incomes and salaries are executed

as credit.

Debit the receiver and credit all the giver: This manage is regularly followed on

account of individual records. Individual record manages an individual or legal person. As per

this lead, when a gathering gives their assets to the person that gathering is known as bank and

the collector organization is borrower and the other way around.

Accounting Principles

Principles of conservatism: This principle mainly help in adapting changes in cash

flows. Lowest possible inflows are considered with possible cash out flows.

Cost principles: This principle mainly says that all of the assets must be recorded at cost

rather than estimated cost and selling price.

4

terms of determining and presenting the information subject to total control and management

(Păşcan, 2015). This is also one of the essential element in terms of deriving the skills and

management to next level for developing plans and diverting the skills for specific manner.

3. Accounting rules and principles governs the presentations

Accounting rules

There are three major accounting rules are found in accounting around which accounting

procedures flows or not. This is one of the essential process which helps in creating rules and

standards to make accurate financial statements and retaining the books (Louwers and et. al.,

2015). These rules are as follows:

Debit what comes in, credit what goes out: This management is utilized as a part of the

instance of genuine records. Genuine record covers every one of the records which are connected

with the advantages of the association, for example, building account, generosity account,

hardware account and so on. These benefits has a default charge adjust. As per this manage,

when an adjustment of the advantages is expanded or gotten then they are known as charge

exchanges. Apart form it, when adjust of these benefits diminish then these exchange are known

as credit exchanges.

Debit all the expenditures, losses and credit all the incomes and receivables: This

lead is connected on counterfeit records. Imitative record are the invented accounts which are

related with different costs, misfortunes, incomes and so on. As per this control, every one of the

costs are considered and recorded as charge exchanges and all incomes and salaries are executed

as credit.

Debit the receiver and credit all the giver: This manage is regularly followed on

account of individual records. Individual record manages an individual or legal person. As per

this lead, when a gathering gives their assets to the person that gathering is known as bank and

the collector organization is borrower and the other way around.

Accounting Principles

Principles of conservatism: This principle mainly help in adapting changes in cash

flows. Lowest possible inflows are considered with possible cash out flows.

Cost principles: This principle mainly says that all of the assets must be recorded at cost

rather than estimated cost and selling price.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Going concern: As per this principle, an organisation is formed to operate the business

and operations for longer run. Rules and regulations are adapted to continuing the business for

longer run (Liubing and Feng, 2013).

Monetary unit: These transactions mainly helps in managing the inventories and

operations for longer run.

Full disclosure: This mainly helps in presenting the information regarding policies, rules

and standards which are used from long period.

Matching principles: This principle mainly centralised around one point that all the

expenditures must be compensated and equal to income.

Revenue recognition: This principle provides a time duration subject considering the

revenue within income and expenditure account.

Materiality: According to this rule, an accounting can overlook whatever other standard

which is considered as non appropriate in their mentality. Every single irrelevant rule can be

overlooked.

Time assumption: Under this rule, all the money related books and records are set up as

indicated by the time distributed. This announcements are set up in a money related year.

Economic substance presumption: According to this rule, it ought to be accepted that

the association has an unexpected element in comparison to its proprietor. This rule is considered

as reasonable for the organizations since they have various of proprietors which are known as

investors.

4. Conventions and concepts relating consistency and material disclosure

Consistency concepts

Consistency concepts and conventions defines that accounting principle that is once

adopted must be applied consistently in future accounting period and same principles or methods

are used for similar situations. If an organisation is changing its accounting principles or methods

on reasonable grounds in same accounting period then they must disclose the nature of change

and its impact on the financial statement (May, 2013).

For example if a company is using straight line depreciation method on its equipments

and alter, they wants to change it to declining balance depreciation method, then the company

must disclosed it in the financial reports.

Material disclosure

5

and operations for longer run. Rules and regulations are adapted to continuing the business for

longer run (Liubing and Feng, 2013).

Monetary unit: These transactions mainly helps in managing the inventories and

operations for longer run.

Full disclosure: This mainly helps in presenting the information regarding policies, rules

and standards which are used from long period.

Matching principles: This principle mainly centralised around one point that all the

expenditures must be compensated and equal to income.

Revenue recognition: This principle provides a time duration subject considering the

revenue within income and expenditure account.

Materiality: According to this rule, an accounting can overlook whatever other standard

which is considered as non appropriate in their mentality. Every single irrelevant rule can be

overlooked.

Time assumption: Under this rule, all the money related books and records are set up as

indicated by the time distributed. This announcements are set up in a money related year.

Economic substance presumption: According to this rule, it ought to be accepted that

the association has an unexpected element in comparison to its proprietor. This rule is considered

as reasonable for the organizations since they have various of proprietors which are known as

investors.

4. Conventions and concepts relating consistency and material disclosure

Consistency concepts

Consistency concepts and conventions defines that accounting principle that is once

adopted must be applied consistently in future accounting period and same principles or methods

are used for similar situations. If an organisation is changing its accounting principles or methods

on reasonable grounds in same accounting period then they must disclose the nature of change

and its impact on the financial statement (May, 2013).

For example if a company is using straight line depreciation method on its equipments

and alter, they wants to change it to declining balance depreciation method, then the company

must disclosed it in the financial reports.

Material disclosure

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

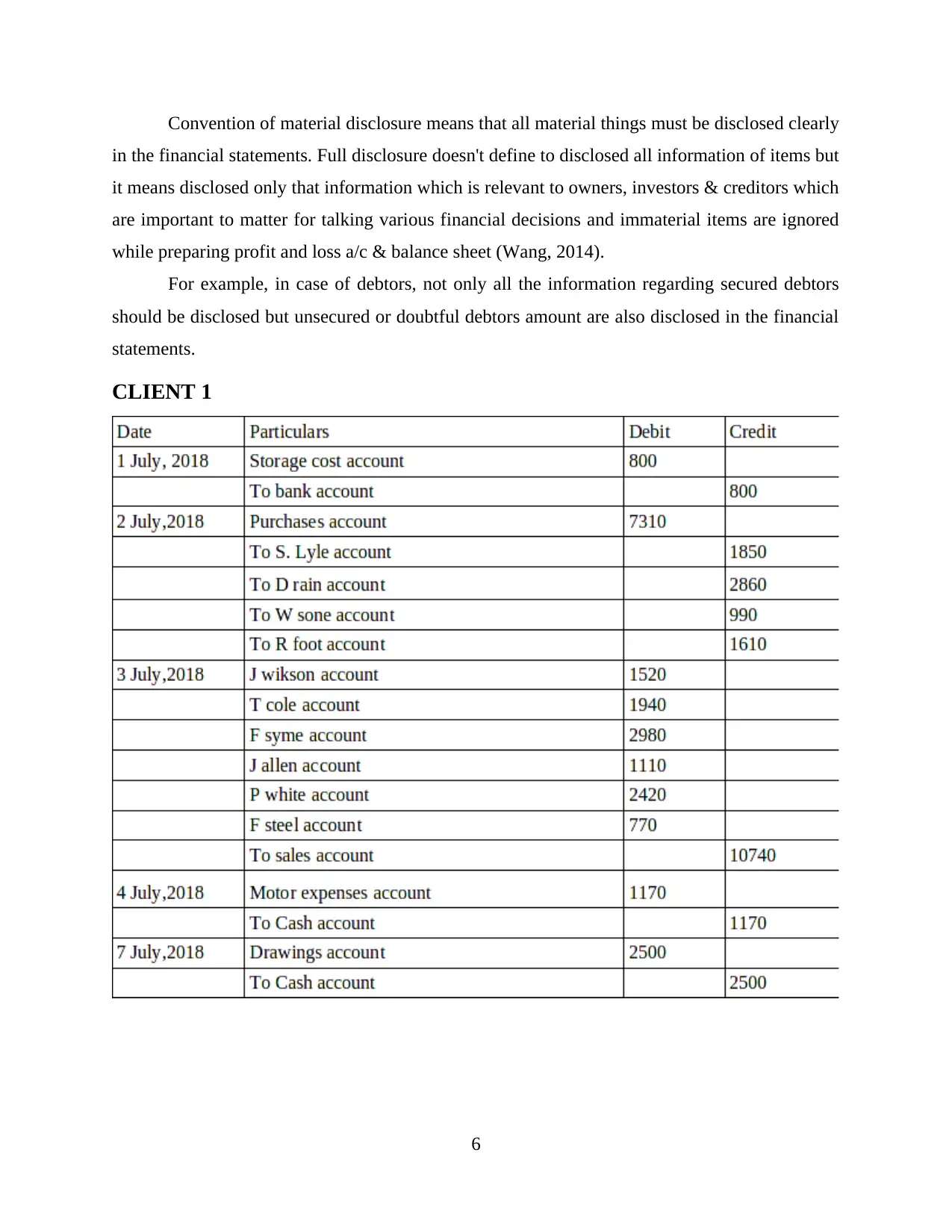

Convention of material disclosure means that all material things must be disclosed clearly

in the financial statements. Full disclosure doesn't define to disclosed all information of items but

it means disclosed only that information which is relevant to owners, investors & creditors which

are important to matter for talking various financial decisions and immaterial items are ignored

while preparing profit and loss a/c & balance sheet (Wang, 2014).

For example, in case of debtors, not only all the information regarding secured debtors

should be disclosed but unsecured or doubtful debtors amount are also disclosed in the financial

statements.

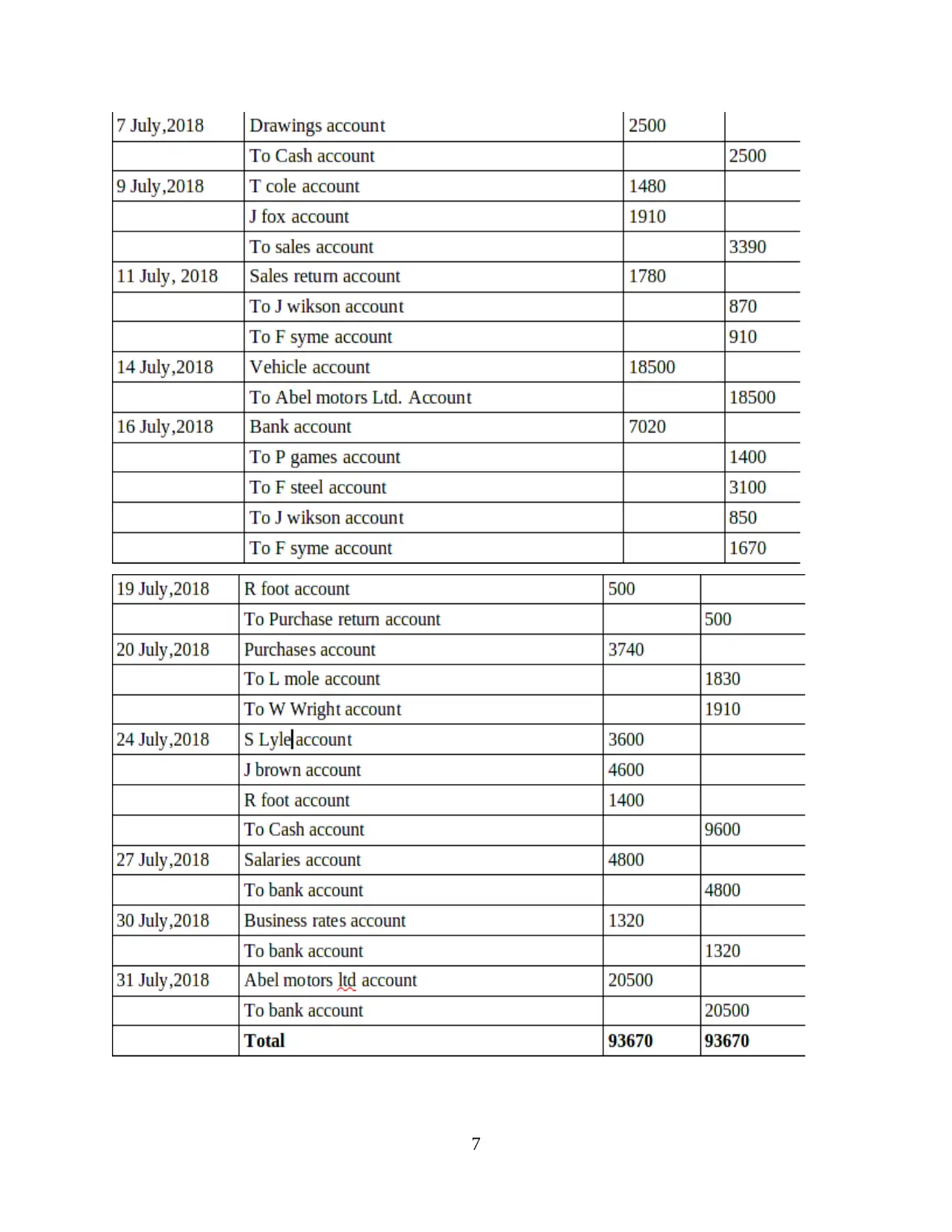

CLIENT 1

6

in the financial statements. Full disclosure doesn't define to disclosed all information of items but

it means disclosed only that information which is relevant to owners, investors & creditors which

are important to matter for talking various financial decisions and immaterial items are ignored

while preparing profit and loss a/c & balance sheet (Wang, 2014).

For example, in case of debtors, not only all the information regarding secured debtors

should be disclosed but unsecured or doubtful debtors amount are also disclosed in the financial

statements.

CLIENT 1

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

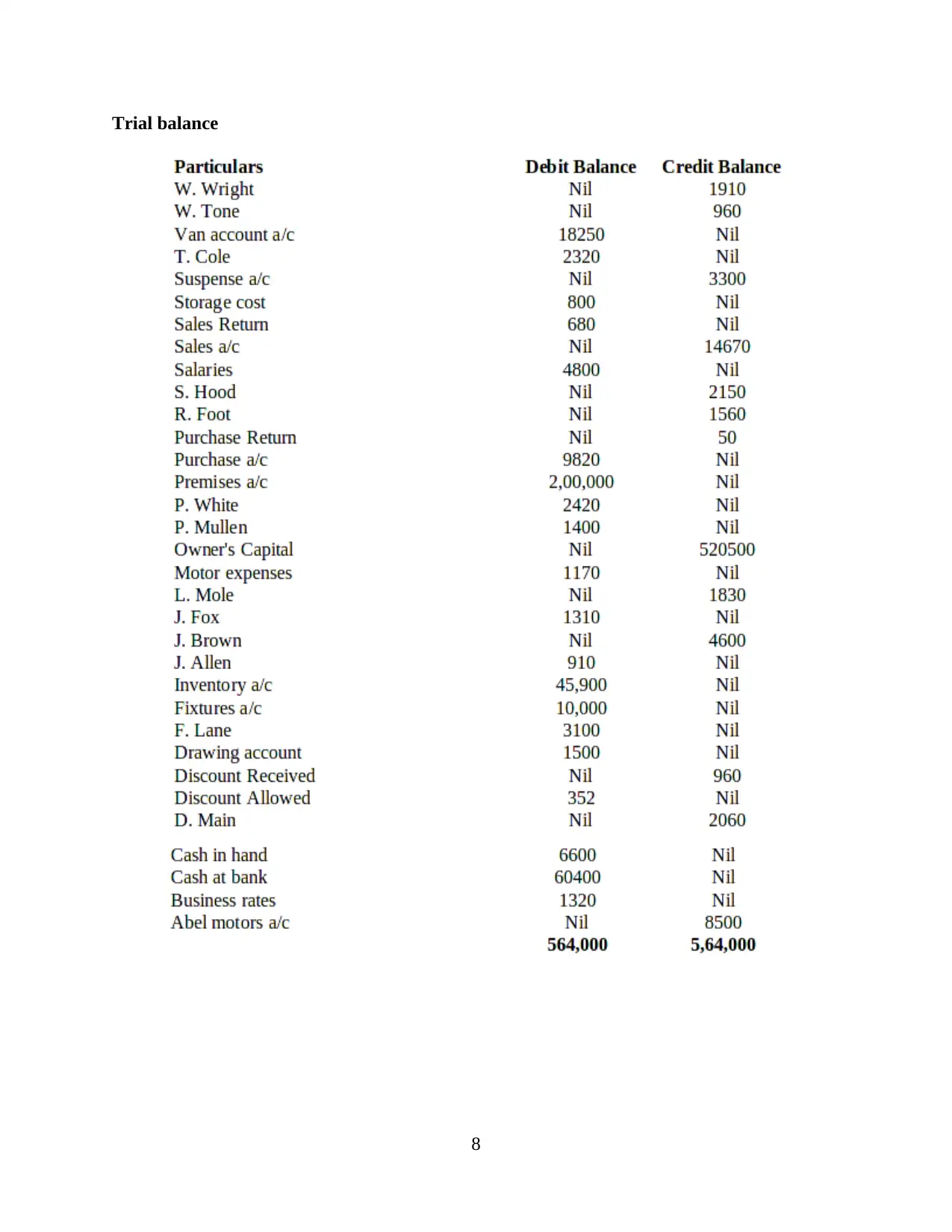

Trial balance

8

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

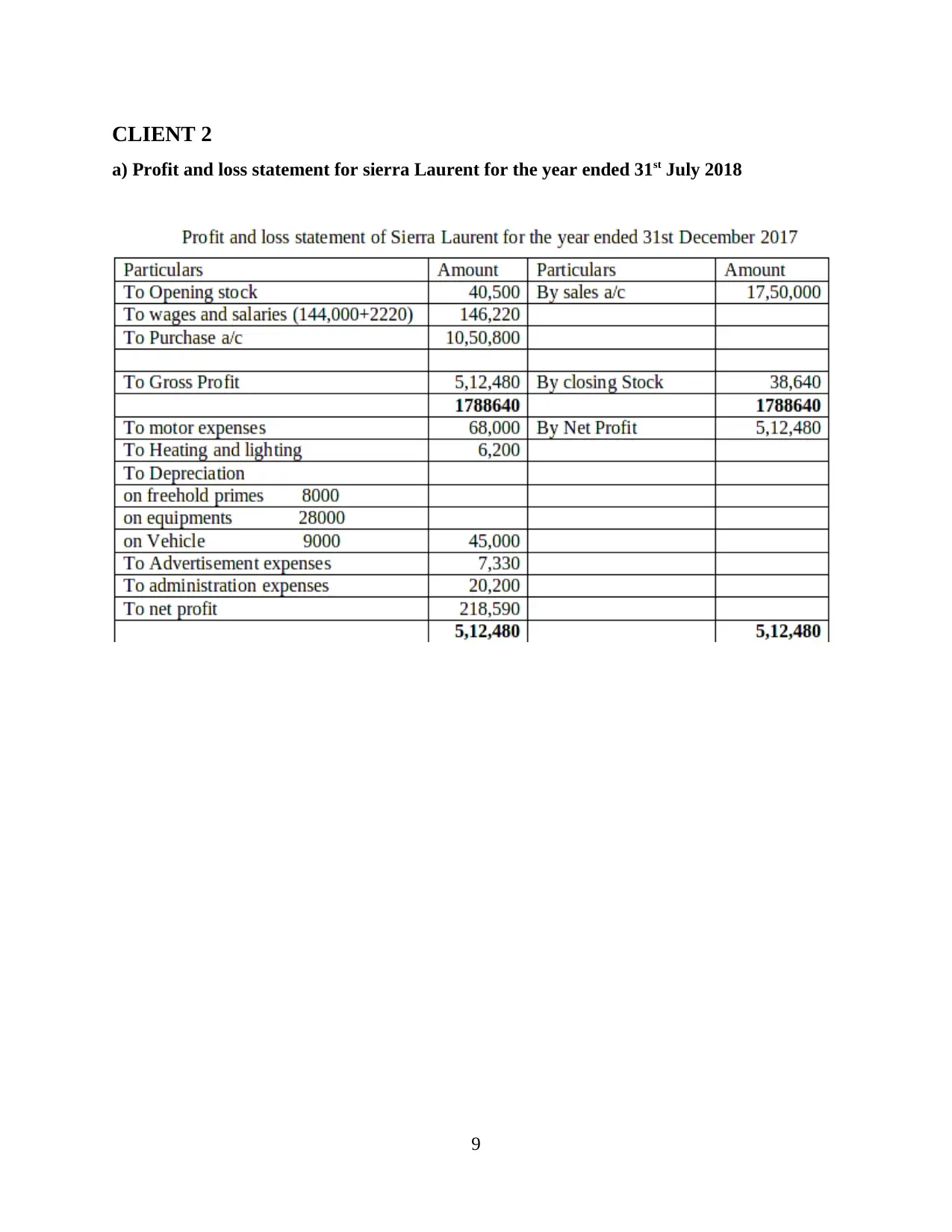

CLIENT 2

a) Profit and loss statement for sierra Laurent for the year ended 31st July 2018

9

a) Profit and loss statement for sierra Laurent for the year ended 31st July 2018

9

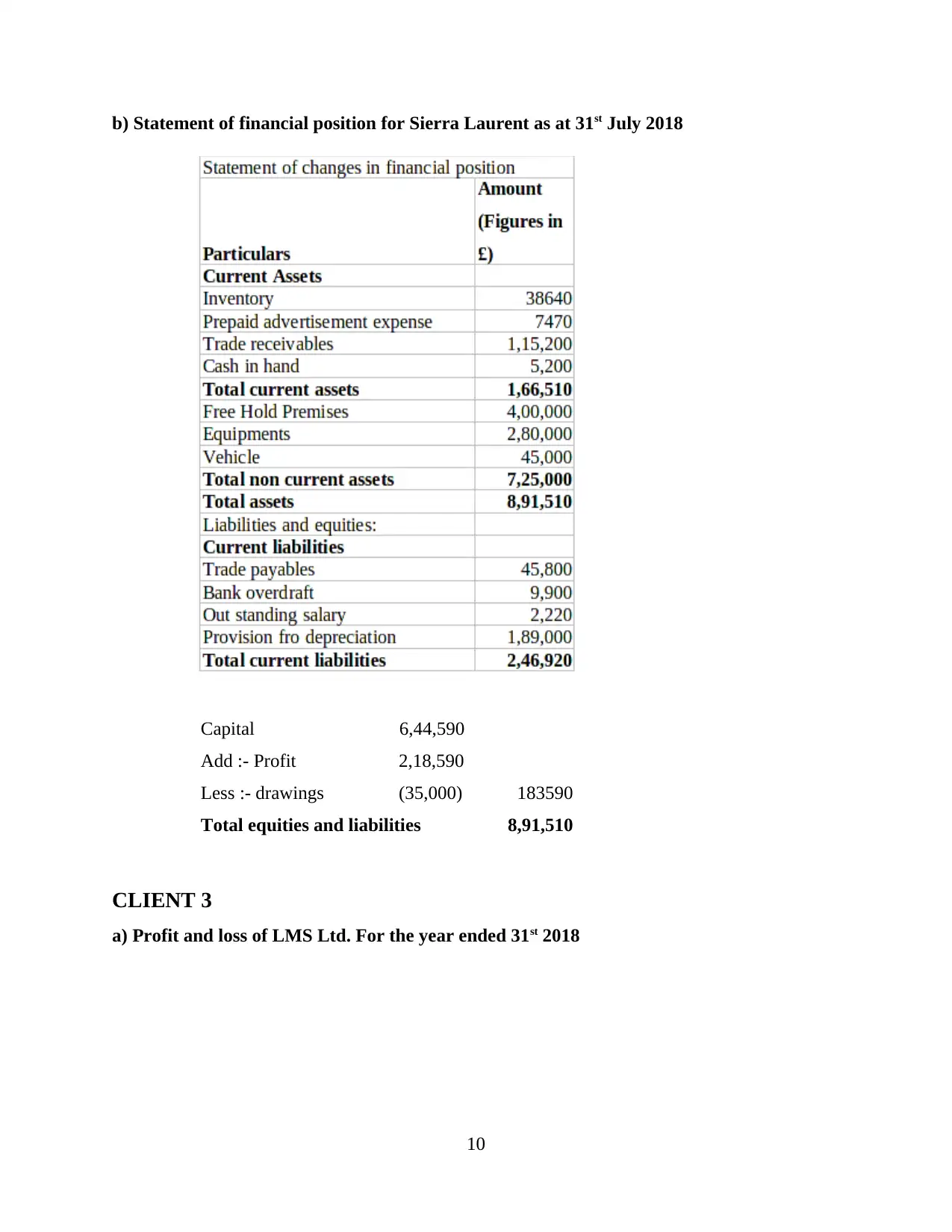

b) Statement of financial position for Sierra Laurent as at 31st July 2018

Capital 6,44,590

Add :- Profit 2,18,590

Less :- drawings (35,000) 183590

Total equities and liabilities 8,91,510

CLIENT 3

a) Profit and loss of LMS Ltd. For the year ended 31st 2018

10

Capital 6,44,590

Add :- Profit 2,18,590

Less :- drawings (35,000) 183590

Total equities and liabilities 8,91,510

CLIENT 3

a) Profit and loss of LMS Ltd. For the year ended 31st 2018

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.