Management Accounting Report: Financial Statement Analysis and Costing

VerifiedAdded on 2021/02/21

|16

|4722

|264

Report

AI Summary

This report delves into the core concepts of management accounting, focusing on its application within the context of Williams Performance Tenders, a UK-based SME manufacturing boats. It begins with an introduction to management accounting, outlining its principles, systems, and the distinction between management and financial accounting. The report then explores various management accounting systems, including inventory management, cost accounting, and price optimization. A significant portion is dedicated to costing techniques, such as cost-volume-profit analysis, flexible budgeting, and cost variances. The report also covers different costing methods, including absorption and marginal costing, along with cost allocation strategies. Furthermore, the report analyzes inventory costs and valuation methods (LIFO and FIFO). Finally, it examines the use of management accounting in addressing financial issues and concludes with a summary of the key findings.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

P1Explanation of management accounting and essential requirement of various accounting

systems.........................................................................................................................................3

P2. Explanation of various kind of methods of management accounting reporting....................5

TASK 2............................................................................................................................................6

P3 Costing Techniques for preparing the financial statements....................................................6

TASK 3..........................................................................................................................................10

P4 Benefits and drawbacks of different planning tools:............................................................10

TASK 4..........................................................................................................................................13

P5 Management accounting in response to overcome financial issues:....................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

P1Explanation of management accounting and essential requirement of various accounting

systems.........................................................................................................................................3

P2. Explanation of various kind of methods of management accounting reporting....................5

TASK 2............................................................................................................................................6

P3 Costing Techniques for preparing the financial statements....................................................6

TASK 3..........................................................................................................................................10

P4 Benefits and drawbacks of different planning tools:............................................................10

TASK 4..........................................................................................................................................13

P5 Management accounting in response to overcome financial issues:....................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

In trading and business context, management accounting concerned with presenting and

circulating, organisational and business information to different related or interested parties.

Managing key task of business to generate information is main motto of management

accounting. Decision-making task of managing officials is easily done by adoption of

management accounting's different systems (Ahrens and et.al., 2017). It provide a core

framework for strategic planning and effective actions plans while achieving pre-estimated goals.

It's planning tools are used by managers to recognise fiscal issues within entity. The study

contains a discussion on management accounting's definition and systems, its principles,

reporting and planning tools in context of Williams Performance Tenders. It is a SME, engaged

in manufacturing of boats in UK. Company aims to increase its revenue by expanding business

outside its current territories . Study also evaluates role of cost, analysis of different costs,

financial planning and use of tools or techniques to sort out such problems.

P1Explanation of management accounting and essential requirement of various

accounting systems.

Management Accounting: It is a classified and systematic branch of management, which also

combines accounting with aims to presenting the most relevant and considerable informations to

stakeholders. It can be defined as cognitive processes focused on presentation of information to

provide easiness in process of planning and actioning (Bromwich, 2012).

Management accounting system: In business entities management accounting is adopted as

different systems to cover different areas of operations. These systems facilitates procedures to

attain efficiencies in organisational processes. They are frameworks which defines purpose of

each organisational process. Every task in company is classified in these different systems to

implement them effectively.

Important to integrate these within an organisation:

Organisation's processes are implemented by different department and process heads to

conduct operations. To achieve effectiveness in trade and manufacturing processes, integration

of management accounting' systems is vital. As manufacturing heads manages inventory storage,

processing and handles different variety of stocks, which sometimes seems difficult for them. So

managers integrates inventory management's system in inventory processes by collecting basis

In trading and business context, management accounting concerned with presenting and

circulating, organisational and business information to different related or interested parties.

Managing key task of business to generate information is main motto of management

accounting. Decision-making task of managing officials is easily done by adoption of

management accounting's different systems (Ahrens and et.al., 2017). It provide a core

framework for strategic planning and effective actions plans while achieving pre-estimated goals.

It's planning tools are used by managers to recognise fiscal issues within entity. The study

contains a discussion on management accounting's definition and systems, its principles,

reporting and planning tools in context of Williams Performance Tenders. It is a SME, engaged

in manufacturing of boats in UK. Company aims to increase its revenue by expanding business

outside its current territories . Study also evaluates role of cost, analysis of different costs,

financial planning and use of tools or techniques to sort out such problems.

P1Explanation of management accounting and essential requirement of various

accounting systems.

Management Accounting: It is a classified and systematic branch of management, which also

combines accounting with aims to presenting the most relevant and considerable informations to

stakeholders. It can be defined as cognitive processes focused on presentation of information to

provide easiness in process of planning and actioning (Bromwich, 2012).

Management accounting system: In business entities management accounting is adopted as

different systems to cover different areas of operations. These systems facilitates procedures to

attain efficiencies in organisational processes. They are frameworks which defines purpose of

each organisational process. Every task in company is classified in these different systems to

implement them effectively.

Important to integrate these within an organisation:

Organisation's processes are implemented by different department and process heads to

conduct operations. To achieve effectiveness in trade and manufacturing processes, integration

of management accounting' systems is vital. As manufacturing heads manages inventory storage,

processing and handles different variety of stocks, which sometimes seems difficult for them. So

managers integrates inventory management's system in inventory processes by collecting basis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

stock information to effectively manage inventories. In Williams Performance Tenders, accounts

department operates accounting tasks and processes to provide accounting and fiscal related

informations for systems.

Origin, role and principles of management accounting:

The concept of management accounting was originated with the time of revolution of business

industries in England around 1960s. The term in initially regarded as cost accounting which is

further differentiated by different authors and committees (Origin of management accounting.

2019).

There are wide number of principles are proposed by different people but basically

principles are classified as:

Influence:

Information should be effective and must

contain power to influence organisational

processes.

Relevance:

Relevant information should be circulated in

management accounting's processes.

Values:

Results, informations and outcomes should

contain some values to business entity.

Trust:

processes must generate informations which

has creditworthiness and build trusts in entity.

Distinction between management and financial accounting:

Management Accounting Financial Accounting

It emphasises on presenting and directing the

flow of information for task of taking instant

decisions.

It emphasises on presentation of data for

different stake holder parties.

No legal formalities are required under

management accounting.

Here legals rules and procedures required to be

followed.

It focuses on qualitative and numerical or

quantitative elements.

It focuses on singly numerical terms and

elements.

Management Accounting Systems:

department operates accounting tasks and processes to provide accounting and fiscal related

informations for systems.

Origin, role and principles of management accounting:

The concept of management accounting was originated with the time of revolution of business

industries in England around 1960s. The term in initially regarded as cost accounting which is

further differentiated by different authors and committees (Origin of management accounting.

2019).

There are wide number of principles are proposed by different people but basically

principles are classified as:

Influence:

Information should be effective and must

contain power to influence organisational

processes.

Relevance:

Relevant information should be circulated in

management accounting's processes.

Values:

Results, informations and outcomes should

contain some values to business entity.

Trust:

processes must generate informations which

has creditworthiness and build trusts in entity.

Distinction between management and financial accounting:

Management Accounting Financial Accounting

It emphasises on presenting and directing the

flow of information for task of taking instant

decisions.

It emphasises on presentation of data for

different stake holder parties.

No legal formalities are required under

management accounting.

Here legals rules and procedures required to be

followed.

It focuses on qualitative and numerical or

quantitative elements.

It focuses on singly numerical terms and

elements.

Management Accounting Systems:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory Management System: It supports the whole process of inventory holding or

storage of stocks. In Williams Performance Tenders, inventory's of boat manufacturing process

is managed applying this system (Chapman and et.al., 2016). Company can assess the actual cost

of inventory at any time using this systems and can determine the effect of excessive inventory

on its profitability. It find out the root cause of increase in inventory cost and reason for

excessive holding period of inventories.

Cost accounting system: Different costs or expenditures are considerable variables in

profit evaluation. Particularly in manufacturing companies like Williams Performance Tenders

are always trying to decrease their price per product unit in order to attain targeted profitability

level. Cost accounting systems are used primarily by organizations to perform a thorough cost

analysis to guarantee profitability by effectively projecting costs linked to various operations.

Price-optimization system: It develops and creates a basis for keeping the price of

products or services at specific point where consumer demand is considerably highest (Chenhall

and et.al., 2018). In Williams Performance Tenders, it determine the price of boat manufactured

with aim to increase level of profitability and demand.

Job Costing Systems: Accounting and handling products that are completely distinct in

nature and in other variables is a challenging task, but adopting a job costing scheme can ensure

smooth recording and organizing of tasks associated with these products. This system effective

for manufacturing businesses such as Williams Performance Tenders with a variety and

differentiated products.

P2. Explanation of various kind of methods of management accounting reporting.

Presentation of financial information:

All the reports of management accounting are needed to provide different customers with

facts and figures within the business entity. Information must hold consistency, relevance and

reliability as it used by people who are not belongs to financial and accounting sectors. Below

presented are required financial information's characteristic:

Information require to provide creditworthiness in presented reports.

Information must be compatible with different users and departments in business entity.

Presented information should be up-to date and relevant for managerial and stakeholders'

use (Corbett, 2018).

Manner of presentation of information:

storage of stocks. In Williams Performance Tenders, inventory's of boat manufacturing process

is managed applying this system (Chapman and et.al., 2016). Company can assess the actual cost

of inventory at any time using this systems and can determine the effect of excessive inventory

on its profitability. It find out the root cause of increase in inventory cost and reason for

excessive holding period of inventories.

Cost accounting system: Different costs or expenditures are considerable variables in

profit evaluation. Particularly in manufacturing companies like Williams Performance Tenders

are always trying to decrease their price per product unit in order to attain targeted profitability

level. Cost accounting systems are used primarily by organizations to perform a thorough cost

analysis to guarantee profitability by effectively projecting costs linked to various operations.

Price-optimization system: It develops and creates a basis for keeping the price of

products or services at specific point where consumer demand is considerably highest (Chenhall

and et.al., 2018). In Williams Performance Tenders, it determine the price of boat manufactured

with aim to increase level of profitability and demand.

Job Costing Systems: Accounting and handling products that are completely distinct in

nature and in other variables is a challenging task, but adopting a job costing scheme can ensure

smooth recording and organizing of tasks associated with these products. This system effective

for manufacturing businesses such as Williams Performance Tenders with a variety and

differentiated products.

P2. Explanation of various kind of methods of management accounting reporting.

Presentation of financial information:

All the reports of management accounting are needed to provide different customers with

facts and figures within the business entity. Information must hold consistency, relevance and

reliability as it used by people who are not belongs to financial and accounting sectors. Below

presented are required financial information's characteristic:

Information require to provide creditworthiness in presented reports.

Information must be compatible with different users and departments in business entity.

Presented information should be up-to date and relevant for managerial and stakeholders'

use (Corbett, 2018).

Manner of presentation of information:

Presentation of information using report must be in a manner which is favourable for

users and easily understandable to all users. Some users are not comfortable with technical or

fiscal terms so reports is required to be presented in compatible manner. Such informations and

relevant facts should provide comparable figures for momentous and quick decision process.

Management Accounting Reports:

Report preparation and presentation is vital elements of management accounting. Reports

are major way of communicating informations within and outside the business organisation. At

the end of managerial processes reports are prepared and circulated to ensure effectiveness in

process of making decisions (Hansen and et.al., 2017). Preparation of reports and making

representation of these formulated reports called as reporting process. Here is a discussion on

various reports prepared under management accounting systems, as follows:

Inventories Report: This report is formulated to trace the occurrence and procurement

of inventories, ultimate usage and movement of inventories. In Williams Performance Tenders,

inventory heads prepare inventory reports which includes inventories like raw items required in

manufacturing of boats, any processes inventories, finished goods etc. This report help to

evaluate costs of inventories with to maximise unit profit.

Performance Report: The performance of an organization is directly depends and

related to the performance of staff, employees and workers, so it is important to evaluate and

asses employee's performance to obtain targeted performance (Hopwood and et.al., 2014). This

report supports treatment of employees as per their skills, qualities and performance. In Williams

Performance Tenders, employee reward and policy system is formulated by using performance

report of all its employees and workers.

Cost report: It consists of all analysis and essential details of costs incurred during a

specific period. As Williams Performance Tenders is manufacturer of boats and other related

equipment, so company apply this report to determine the cost of selling items and minimise

expenses to reach at targeted profit level. This report is being also used to manage the unwanted

expenses due to which company is not able to focus on other important activities such as

incentive policy.

users and easily understandable to all users. Some users are not comfortable with technical or

fiscal terms so reports is required to be presented in compatible manner. Such informations and

relevant facts should provide comparable figures for momentous and quick decision process.

Management Accounting Reports:

Report preparation and presentation is vital elements of management accounting. Reports

are major way of communicating informations within and outside the business organisation. At

the end of managerial processes reports are prepared and circulated to ensure effectiveness in

process of making decisions (Hansen and et.al., 2017). Preparation of reports and making

representation of these formulated reports called as reporting process. Here is a discussion on

various reports prepared under management accounting systems, as follows:

Inventories Report: This report is formulated to trace the occurrence and procurement

of inventories, ultimate usage and movement of inventories. In Williams Performance Tenders,

inventory heads prepare inventory reports which includes inventories like raw items required in

manufacturing of boats, any processes inventories, finished goods etc. This report help to

evaluate costs of inventories with to maximise unit profit.

Performance Report: The performance of an organization is directly depends and

related to the performance of staff, employees and workers, so it is important to evaluate and

asses employee's performance to obtain targeted performance (Hopwood and et.al., 2014). This

report supports treatment of employees as per their skills, qualities and performance. In Williams

Performance Tenders, employee reward and policy system is formulated by using performance

report of all its employees and workers.

Cost report: It consists of all analysis and essential details of costs incurred during a

specific period. As Williams Performance Tenders is manufacturer of boats and other related

equipment, so company apply this report to determine the cost of selling items and minimise

expenses to reach at targeted profit level. This report is being also used to manage the unwanted

expenses due to which company is not able to focus on other important activities such as

incentive policy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

P3 Costing Techniques for preparing the financial statements.

Cost, its types and cost analysis: It means money or consideration that business entities

pay for acquiring something, producing something, or operating company operations and

functions. Costs are crucial element in determining the profitability of trade enterprise.

Analysing costs assist in determining the factors causing increment in expenditures.

Particularly companies engaged in manufacturing of products, analysing costs is

important to enhance graph of profits by reducing expenses. Williams Performance

Tenders analyse its boat manufacturing and other costs to prepare budgets and achieve set

tagetes. Costs are summarised by company as variable, semi variable and fixed.

Cost-volume profit: This assessment is implemented by executives in Williams Performance

Tenders products, which involves analysis and assessment of the connection between the

quantity of manufacturing and expenses to determine the impact on the net gain of the

organization.

Flexible budgeting: It known as variable budget, it used in business of Williams Performance

Tenders as it offers flexibility in evaluating efficiency and net income at various levels and

manufacturing units. At varying production level, it sees differences in net revenue.

Cost Variances: By assessing the impact of variations and variance in distinct operating fields,

this technique or is used by Williams Performance Tenders to recognize the weak and dull

operating regions within the business.

Absorption and marginal costing:

Management uses marginal costs to asses contribution amount related to each unit and

net income under marginal costing. Marginal costs is simply a sum of all direct and variable

costs such as direct expenses, direct material, overhead variable, etc. In this approach, only fixed

costs are shown individually, whether or not they are linked to manufacturing, in revenue

statements as period expense (Horngren and et.al., 2012).

All manufacturing costs (including both variable & fixed costs) are absorption costs in

absorption costing technique. It does not divides cost as fixed and variables to compute the net

profit's amount.

P3 Costing Techniques for preparing the financial statements.

Cost, its types and cost analysis: It means money or consideration that business entities

pay for acquiring something, producing something, or operating company operations and

functions. Costs are crucial element in determining the profitability of trade enterprise.

Analysing costs assist in determining the factors causing increment in expenditures.

Particularly companies engaged in manufacturing of products, analysing costs is

important to enhance graph of profits by reducing expenses. Williams Performance

Tenders analyse its boat manufacturing and other costs to prepare budgets and achieve set

tagetes. Costs are summarised by company as variable, semi variable and fixed.

Cost-volume profit: This assessment is implemented by executives in Williams Performance

Tenders products, which involves analysis and assessment of the connection between the

quantity of manufacturing and expenses to determine the impact on the net gain of the

organization.

Flexible budgeting: It known as variable budget, it used in business of Williams Performance

Tenders as it offers flexibility in evaluating efficiency and net income at various levels and

manufacturing units. At varying production level, it sees differences in net revenue.

Cost Variances: By assessing the impact of variations and variance in distinct operating fields,

this technique or is used by Williams Performance Tenders to recognize the weak and dull

operating regions within the business.

Absorption and marginal costing:

Management uses marginal costs to asses contribution amount related to each unit and

net income under marginal costing. Marginal costs is simply a sum of all direct and variable

costs such as direct expenses, direct material, overhead variable, etc. In this approach, only fixed

costs are shown individually, whether or not they are linked to manufacturing, in revenue

statements as period expense (Horngren and et.al., 2012).

All manufacturing costs (including both variable & fixed costs) are absorption costs in

absorption costing technique. It does not divides cost as fixed and variables to compute the net

profit's amount.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost allocation: This is simple task of costing process which summarises the cost as per their

nature and element quality and includes assigning of costs to particular product. In this regard

different costs are discussed below:

Fixed Costs: These are regarded as period costs that stay the same as changes made in

units of manufacturing or ultimate outputs.

Variable Costs: These are expenses and factors which are extremely affected by changes

in units of manufacturing or ultimate outputs.

Normal Costing: It is traditional and easy costing method that is used by Williams

Performance Tenders to calculate manufacturing cost of each equipment and in price

determining. Simply consider real material, labor and other expense or overhead costs when

setting price and each product's cost are regarded in this technique.

Standard Costing: In this technique, Williams Performance Tenders incomes are computed

by formulating comparative analysis of standard and actual result.

Activity-based costing: This method summarises costs based on different activities and tasks.

Costs are specifically assigned to different tasks for better accountability in calculation of cost

and income.

Inventory Costs: Inventory and stock costs in income statement are determining element

as it affects organisation's amount of net profits. In trading account change in inventories is

specifically recorded to asses gross or operating income. Williams Performance Tenders

records inventory costs like logistic expenses, managing costs, storing costs, warehouse

costs etc. It is advantageous for company to control these costs to increase amount of

profit (Types of inventory cost. 2019).

Inventory valuation methods:

LIFO Method: This method focus on recording of different items of inventories as last

purchased item would be issued at first.

FIFO Method: Whereas this method records different items of inventories as first

purchased items are issued first.

Cost variances: It is tool which is adopted by cost accountants to assess any variation in

budgeted, standard and actual figures of costs to address the any problems in cost process.

nature and element quality and includes assigning of costs to particular product. In this regard

different costs are discussed below:

Fixed Costs: These are regarded as period costs that stay the same as changes made in

units of manufacturing or ultimate outputs.

Variable Costs: These are expenses and factors which are extremely affected by changes

in units of manufacturing or ultimate outputs.

Normal Costing: It is traditional and easy costing method that is used by Williams

Performance Tenders to calculate manufacturing cost of each equipment and in price

determining. Simply consider real material, labor and other expense or overhead costs when

setting price and each product's cost are regarded in this technique.

Standard Costing: In this technique, Williams Performance Tenders incomes are computed

by formulating comparative analysis of standard and actual result.

Activity-based costing: This method summarises costs based on different activities and tasks.

Costs are specifically assigned to different tasks for better accountability in calculation of cost

and income.

Inventory Costs: Inventory and stock costs in income statement are determining element

as it affects organisation's amount of net profits. In trading account change in inventories is

specifically recorded to asses gross or operating income. Williams Performance Tenders

records inventory costs like logistic expenses, managing costs, storing costs, warehouse

costs etc. It is advantageous for company to control these costs to increase amount of

profit (Types of inventory cost. 2019).

Inventory valuation methods:

LIFO Method: This method focus on recording of different items of inventories as last

purchased item would be issued at first.

FIFO Method: Whereas this method records different items of inventories as first

purchased items are issued first.

Cost variances: It is tool which is adopted by cost accountants to assess any variation in

budgeted, standard and actual figures of costs to address the any problems in cost process.

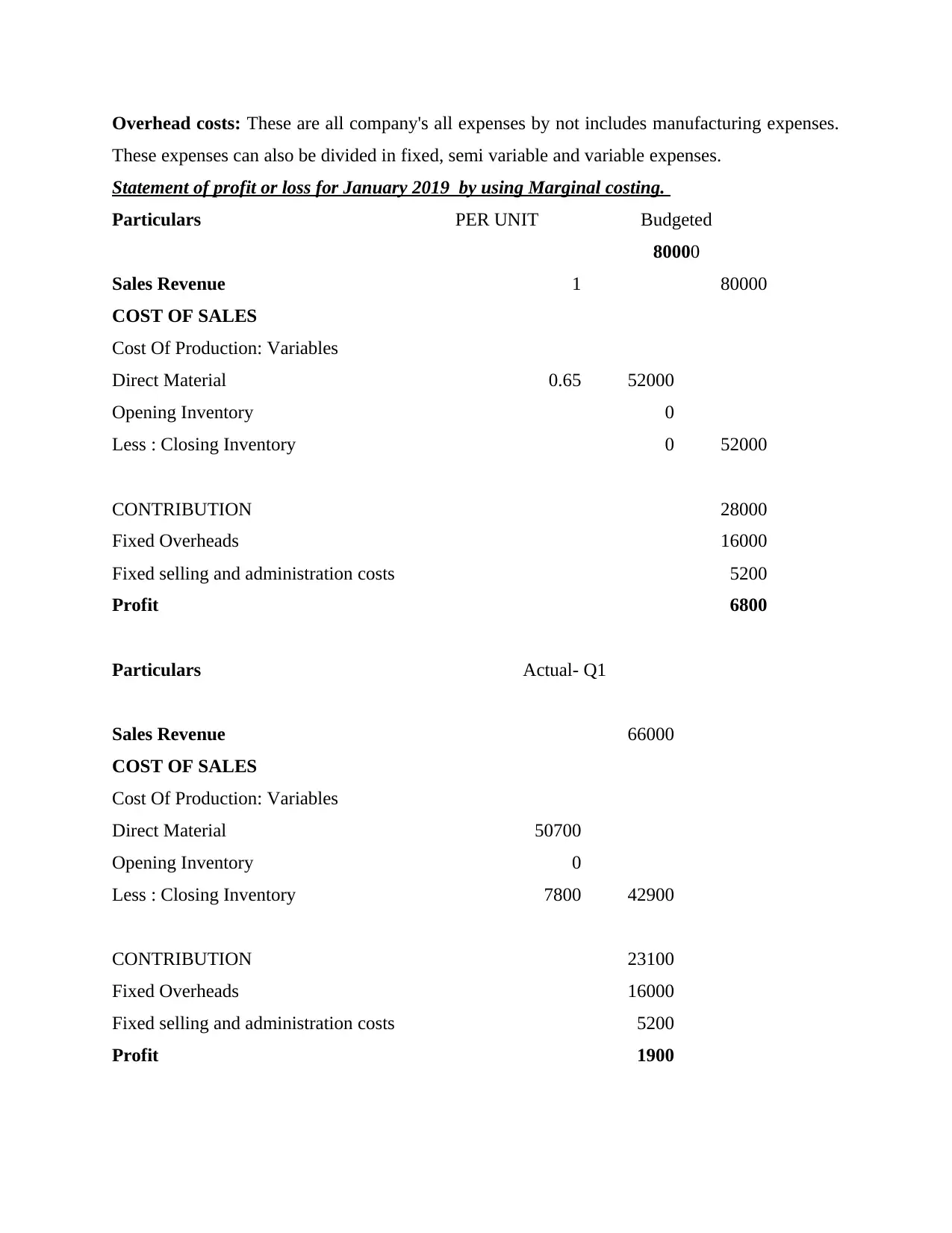

Overhead costs: These are all company's all expenses by not includes manufacturing expenses.

These expenses can also be divided in fixed, semi variable and variable expenses.

Statement of profit or loss for January 2019 by using Marginal costing.

Particulars PER UNIT Budgeted

80000

Sales Revenue 1 80000

COST OF SALES

Cost Of Production: Variables

Direct Material 0.65 52000

Opening Inventory 0

Less : Closing Inventory 0 52000

CONTRIBUTION 28000

Fixed Overheads 16000

Fixed selling and administration costs 5200

Profit 6800

Particulars Actual- Q1

Sales Revenue 66000

COST OF SALES

Cost Of Production: Variables

Direct Material 50700

Opening Inventory 0

Less : Closing Inventory 7800 42900

CONTRIBUTION 23100

Fixed Overheads 16000

Fixed selling and administration costs 5200

Profit 1900

These expenses can also be divided in fixed, semi variable and variable expenses.

Statement of profit or loss for January 2019 by using Marginal costing.

Particulars PER UNIT Budgeted

80000

Sales Revenue 1 80000

COST OF SALES

Cost Of Production: Variables

Direct Material 0.65 52000

Opening Inventory 0

Less : Closing Inventory 0 52000

CONTRIBUTION 28000

Fixed Overheads 16000

Fixed selling and administration costs 5200

Profit 6800

Particulars Actual- Q1

Sales Revenue 66000

COST OF SALES

Cost Of Production: Variables

Direct Material 50700

Opening Inventory 0

Less : Closing Inventory 7800 42900

CONTRIBUTION 23100

Fixed Overheads 16000

Fixed selling and administration costs 5200

Profit 1900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

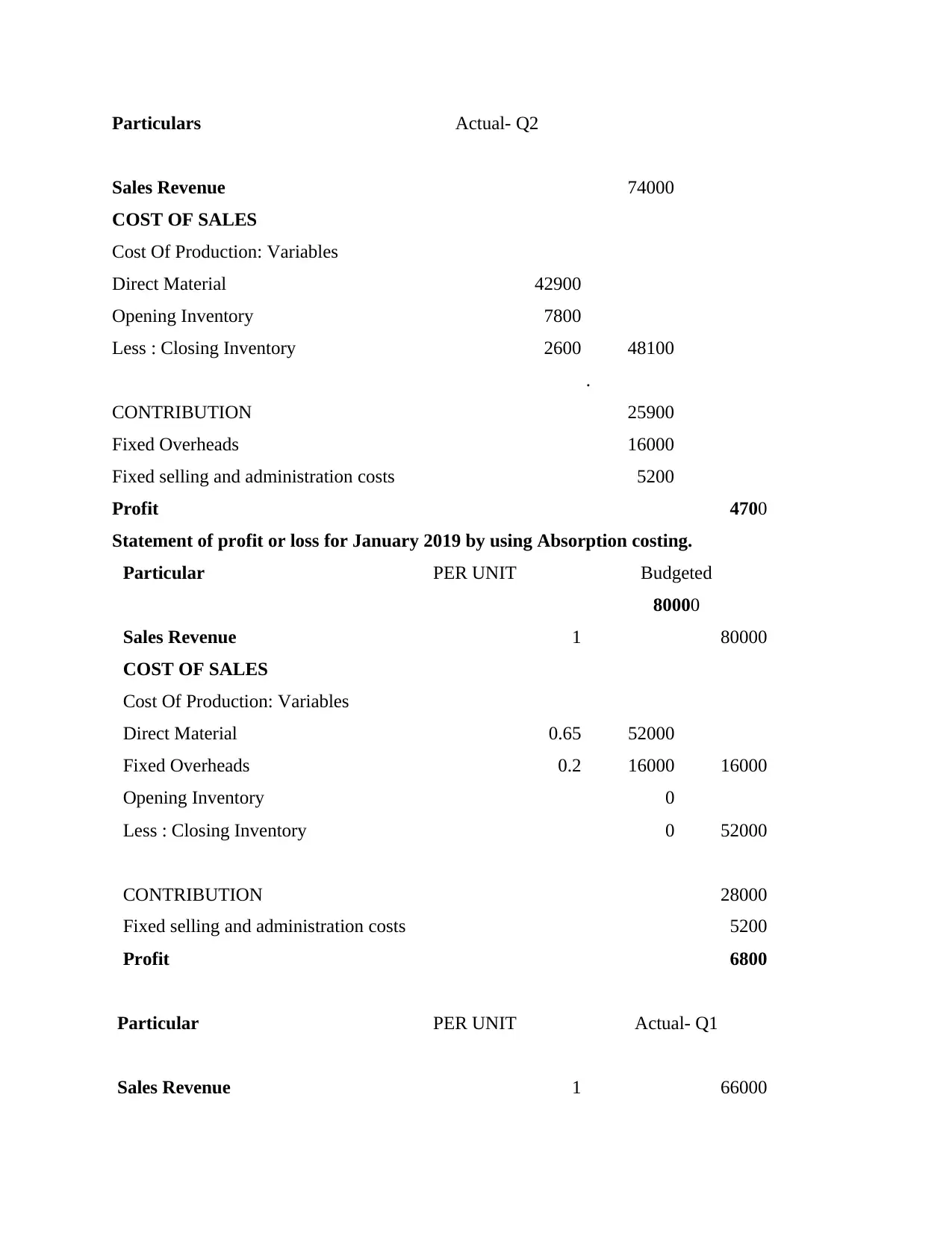

Particulars Actual- Q2

Sales Revenue 74000

COST OF SALES

Cost Of Production: Variables

Direct Material 42900

Opening Inventory 7800

Less : Closing Inventory 2600 48100

.

CONTRIBUTION 25900

Fixed Overheads 16000

Fixed selling and administration costs 5200

Profit 4700

Statement of profit or loss for January 2019 by using Absorption costing.

Particular PER UNIT Budgeted

80000

Sales Revenue 1 80000

COST OF SALES

Cost Of Production: Variables

Direct Material 0.65 52000

Fixed Overheads 0.2 16000 16000

Opening Inventory 0

Less : Closing Inventory 0 52000

CONTRIBUTION 28000

Fixed selling and administration costs 5200

Profit 6800

Particular PER UNIT Actual- Q1

Sales Revenue 1 66000

Sales Revenue 74000

COST OF SALES

Cost Of Production: Variables

Direct Material 42900

Opening Inventory 7800

Less : Closing Inventory 2600 48100

.

CONTRIBUTION 25900

Fixed Overheads 16000

Fixed selling and administration costs 5200

Profit 4700

Statement of profit or loss for January 2019 by using Absorption costing.

Particular PER UNIT Budgeted

80000

Sales Revenue 1 80000

COST OF SALES

Cost Of Production: Variables

Direct Material 0.65 52000

Fixed Overheads 0.2 16000 16000

Opening Inventory 0

Less : Closing Inventory 0 52000

CONTRIBUTION 28000

Fixed selling and administration costs 5200

Profit 6800

Particular PER UNIT Actual- Q1

Sales Revenue 1 66000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

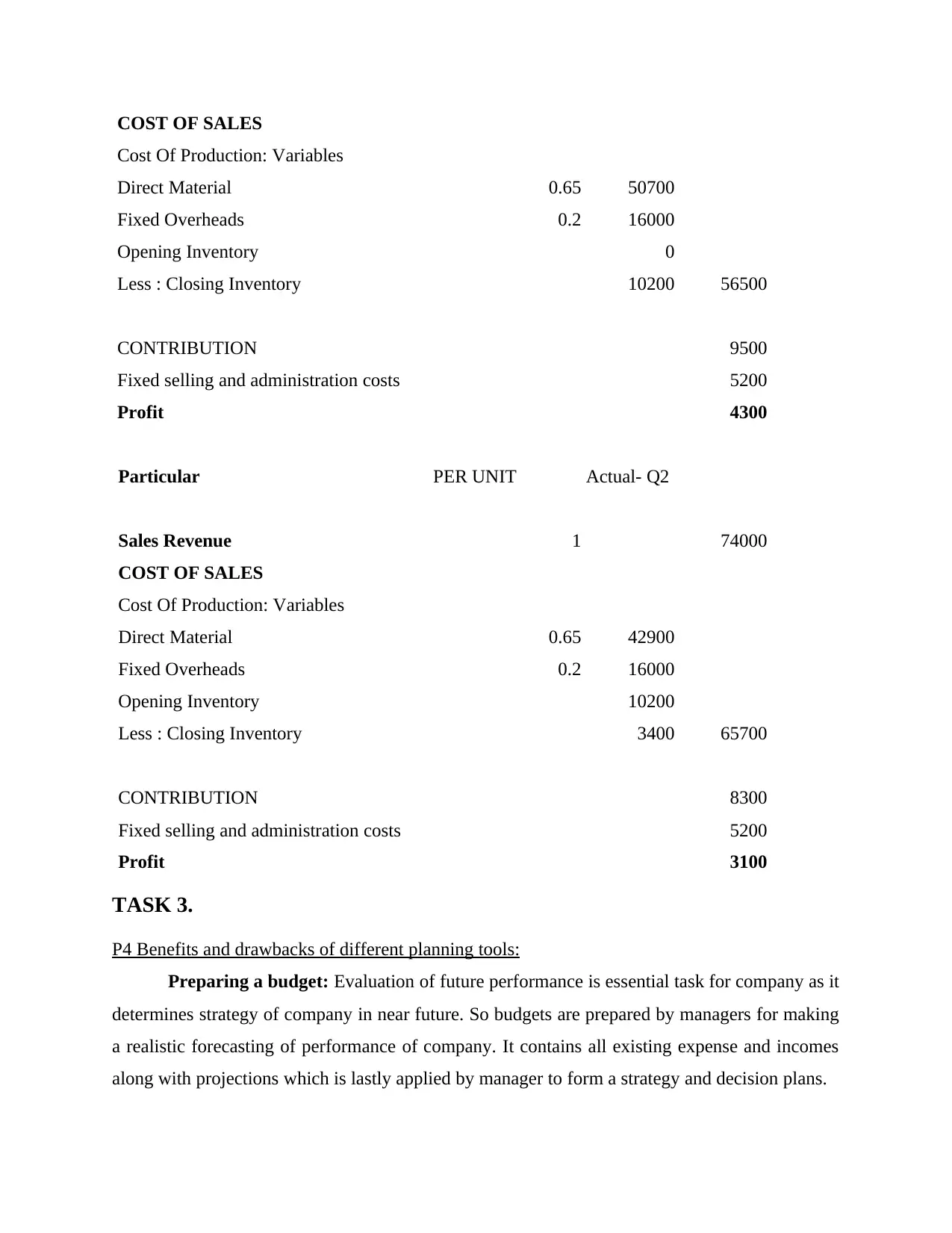

COST OF SALES

Cost Of Production: Variables

Direct Material 0.65 50700

Fixed Overheads 0.2 16000

Opening Inventory 0

Less : Closing Inventory 10200 56500

CONTRIBUTION 9500

Fixed selling and administration costs 5200

Profit 4300

Particular PER UNIT Actual- Q2

Sales Revenue 1 74000

COST OF SALES

Cost Of Production: Variables

Direct Material 0.65 42900

Fixed Overheads 0.2 16000

Opening Inventory 10200

Less : Closing Inventory 3400 65700

CONTRIBUTION 8300

Fixed selling and administration costs 5200

Profit 3100

TASK 3.

P4 Benefits and drawbacks of different planning tools:

Preparing a budget: Evaluation of future performance is essential task for company as it

determines strategy of company in near future. So budgets are prepared by managers for making

a realistic forecasting of performance of company. It contains all existing expense and incomes

along with projections which is lastly applied by manager to form a strategy and decision plans.

Cost Of Production: Variables

Direct Material 0.65 50700

Fixed Overheads 0.2 16000

Opening Inventory 0

Less : Closing Inventory 10200 56500

CONTRIBUTION 9500

Fixed selling and administration costs 5200

Profit 4300

Particular PER UNIT Actual- Q2

Sales Revenue 1 74000

COST OF SALES

Cost Of Production: Variables

Direct Material 0.65 42900

Fixed Overheads 0.2 16000

Opening Inventory 10200

Less : Closing Inventory 3400 65700

CONTRIBUTION 8300

Fixed selling and administration costs 5200

Profit 3100

TASK 3.

P4 Benefits and drawbacks of different planning tools:

Preparing a budget: Evaluation of future performance is essential task for company as it

determines strategy of company in near future. So budgets are prepared by managers for making

a realistic forecasting of performance of company. It contains all existing expense and incomes

along with projections which is lastly applied by manager to form a strategy and decision plans.

Different types of budgets: Following are some key considerable budgets prepared by

Williams Performance Tenders, as follows:

Capital Budget: It is a kind of run term budget which defines company's long

term decisions. It is an extended version of change in equity statement as it also shows

any fluctuation in capital employed. It also contains figures which help to determine the

practicality and viability of projects and investments. In Williams Performance Tenders,

this budget is proposed to know the viability of tenders of boats and other investments.

Advantage: It is beneficial for company to evaluate any long-term capital

investments.

Disadvantage: A wrong assumption in capital budget can affect performance and

growth of company in long run.

Operating Budget: It emphasises on managing the small operative and routine

expenses to asses company's future operating efficiencies (Kaplan, 2014). In Williams

Performance Tenders it is prepared by accountants to assess the future operating

effectiveness. It considers all current operating expenses and incomes to make

forecasting.

Advantage: This budget helps from the primary streamline to avoid unproductive

and other inefficient operations and expenses.

Disadvantage: As it is formulated generally on daily basis so in SME firms like

Williams Performance Tenders it does not have so much usefulness or relevance.

Alternative methods of budgeting:

Cash Budget: It is similar to cash flow analysis as it contains all cash incomes

and expenses along with projections of such cash expenses. This budget alters about

possible negative flow in organisation and manage cash flow. It determines company's

liquidity position in near future that assist in decision making.

Behavioural implications of budgets:

Williams Performance Tenders asses its entire performance by preparation of

different budgets, following discussed are merits of preparation of budgets:

Williams Performance Tenders, as follows:

Capital Budget: It is a kind of run term budget which defines company's long

term decisions. It is an extended version of change in equity statement as it also shows

any fluctuation in capital employed. It also contains figures which help to determine the

practicality and viability of projects and investments. In Williams Performance Tenders,

this budget is proposed to know the viability of tenders of boats and other investments.

Advantage: It is beneficial for company to evaluate any long-term capital

investments.

Disadvantage: A wrong assumption in capital budget can affect performance and

growth of company in long run.

Operating Budget: It emphasises on managing the small operative and routine

expenses to asses company's future operating efficiencies (Kaplan, 2014). In Williams

Performance Tenders it is prepared by accountants to assess the future operating

effectiveness. It considers all current operating expenses and incomes to make

forecasting.

Advantage: This budget helps from the primary streamline to avoid unproductive

and other inefficient operations and expenses.

Disadvantage: As it is formulated generally on daily basis so in SME firms like

Williams Performance Tenders it does not have so much usefulness or relevance.

Alternative methods of budgeting:

Cash Budget: It is similar to cash flow analysis as it contains all cash incomes

and expenses along with projections of such cash expenses. This budget alters about

possible negative flow in organisation and manage cash flow. It determines company's

liquidity position in near future that assist in decision making.

Behavioural implications of budgets:

Williams Performance Tenders asses its entire performance by preparation of

different budgets, following discussed are merits of preparation of budgets:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.