Financial Accounting Principles: CFS Case Study and Analysis Report

VerifiedAdded on 2020/10/22

|27

|6810

|416

Homework Assignment

AI Summary

This assignment provides a comprehensive overview of financial accounting principles, using Corporate Financial Solutions (CFS), London as a case study. It covers key concepts such as financial accounting's purpose, regulations (IFRS and IAS), and fundamental rules. The assignment delves into practical applications, including journal entries, ledger accounts, trial balances, and the preparation of profit and loss statements, balance sheets, and bank reconciliation statements for various clients. It also explores accounting concepts like business entity, dual aspect, money measurement, cost, going concern, and matching principles. Conventions such as consistency and material disclosure are explained, alongside depreciation methods. The report concludes with an analysis of suspense accounts and their role in drafting trial balances. This assignment demonstrates a strong understanding of financial accounting principles and their practical application in a business context.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1. Financial accounting and its purpose.......................................................................................1

2. Financial accounting regulations:-...........................................................................................2

3. Accounting rules and principles...............................................................................................2

4. Conventions and concepts related to consistency and material disclosure..............................4

CLIENT 1........................................................................................................................................4

1. Journal entry in books of David Study....................................................................................4

2. Ledger Account........................................................................................................................7

3. Trial Balance as on 31st January 2018..................................................................................13

CLIENT 2......................................................................................................................................14

A. Statement of profit and loss for Peter Hampau for year ended 31st July 2018.....................14

B. Statement of financial position for Peter Hampau for year ended on 31st July 2018...........15

CLIENT 3......................................................................................................................................16

A. Profit and loss account..........................................................................................................16

B. Balance Sheet........................................................................................................................17

C. Consistency and Prudence concepts......................................................................................18

D. Depreciation and its methods................................................................................................18

CLIENT 4......................................................................................................................................19

A. Purpose of BRS to CEO of Durrell.......................................................................................19

B. Prepare Durrell Ltd's updated cash book for December 2017..............................................19

C. Bank Reconciliation Statement.............................................................................................20

CLIENT 5......................................................................................................................................20

A. Ledger control accounts........................................................................................................20

B. Control account.....................................................................................................................21

CLIENT 6......................................................................................................................................21

A. Suspense Account.................................................................................................................21

B. Drafting of Trial Balance......................................................................................................22

C. Journal entry for suspense account........................................................................................22

D. Difference between suspense a/c and clearing a/c................................................................23

INTRODUCTION...........................................................................................................................1

1. Financial accounting and its purpose.......................................................................................1

2. Financial accounting regulations:-...........................................................................................2

3. Accounting rules and principles...............................................................................................2

4. Conventions and concepts related to consistency and material disclosure..............................4

CLIENT 1........................................................................................................................................4

1. Journal entry in books of David Study....................................................................................4

2. Ledger Account........................................................................................................................7

3. Trial Balance as on 31st January 2018..................................................................................13

CLIENT 2......................................................................................................................................14

A. Statement of profit and loss for Peter Hampau for year ended 31st July 2018.....................14

B. Statement of financial position for Peter Hampau for year ended on 31st July 2018...........15

CLIENT 3......................................................................................................................................16

A. Profit and loss account..........................................................................................................16

B. Balance Sheet........................................................................................................................17

C. Consistency and Prudence concepts......................................................................................18

D. Depreciation and its methods................................................................................................18

CLIENT 4......................................................................................................................................19

A. Purpose of BRS to CEO of Durrell.......................................................................................19

B. Prepare Durrell Ltd's updated cash book for December 2017..............................................19

C. Bank Reconciliation Statement.............................................................................................20

CLIENT 5......................................................................................................................................20

A. Ledger control accounts........................................................................................................20

B. Control account.....................................................................................................................21

CLIENT 6......................................................................................................................................21

A. Suspense Account.................................................................................................................21

B. Drafting of Trial Balance......................................................................................................22

C. Journal entry for suspense account........................................................................................22

D. Difference between suspense a/c and clearing a/c................................................................23

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

REFERENCES..............................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting principle assist an organisation to prepare their financial statements

in an adequate manner so that management can use these statements for making better decisions.

Financial accounting is the process of recording, summarizing and reporting the entries and

transactions in final accounts like Income statement and Balance sheet. These statements are

prepared on the basis of pre set standards which are followed by every organisation. With the

help of these statements of accounts one can come to know regarding the actual position and

performance of company in front of its stakeholders.

The main aim of this report is to ensure firm follows the rules and principles of

accountancy. To better understand this concept, Corporate Financial Solutions (CFS), London is

being selected for this present report. The financial accounting, its purposes, rules and principles

and regulations related to financial accounting is being discussed in this report. Apart from this,

there are various concepts such as conventions, consistency and material disclosure concept is

also explained in this project. Beside this, trial balance, sole trader, Bank Reconciliation

statements are prepared in this report.

1. Financial accounting and its purpose

Financial accounting: - It is a process of preparing financial statements that are helpful

in identifying financial performance and position of companies. These statements are useful for

internal as well as for external analysis. Outside parties such as investors, supplier, creditor or

customers. It is a specialized branch of accounting which continuously keep eyes on company’s

transactions and with the help of these transaction company tend to prepare financial report such

as income statement, balance sheet or cash flow statement.

Purpose of financial accounting: -

Main purpose of financial accounting is to provide accurate information that play a

major role in decision making.

Prepare financial report would show financial position of Corporate Financial

Solution that tend to provide information to external users such as creditors, potential

investors, suppliers and tax authorities.

1

Financial accounting principle assist an organisation to prepare their financial statements

in an adequate manner so that management can use these statements for making better decisions.

Financial accounting is the process of recording, summarizing and reporting the entries and

transactions in final accounts like Income statement and Balance sheet. These statements are

prepared on the basis of pre set standards which are followed by every organisation. With the

help of these statements of accounts one can come to know regarding the actual position and

performance of company in front of its stakeholders.

The main aim of this report is to ensure firm follows the rules and principles of

accountancy. To better understand this concept, Corporate Financial Solutions (CFS), London is

being selected for this present report. The financial accounting, its purposes, rules and principles

and regulations related to financial accounting is being discussed in this report. Apart from this,

there are various concepts such as conventions, consistency and material disclosure concept is

also explained in this project. Beside this, trial balance, sole trader, Bank Reconciliation

statements are prepared in this report.

1. Financial accounting and its purpose

Financial accounting: - It is a process of preparing financial statements that are helpful

in identifying financial performance and position of companies. These statements are useful for

internal as well as for external analysis. Outside parties such as investors, supplier, creditor or

customers. It is a specialized branch of accounting which continuously keep eyes on company’s

transactions and with the help of these transaction company tend to prepare financial report such

as income statement, balance sheet or cash flow statement.

Purpose of financial accounting: -

Main purpose of financial accounting is to provide accurate information that play a

major role in decision making.

Prepare financial report would show financial position of Corporate Financial

Solution that tend to provide information to external users such as creditors, potential

investors, suppliers and tax authorities.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Financial accounting regulations:-

International Financial Reporting Standard (IFRS):- IFRS contain some rules

and principles which is helpful in making financial reports like income statements,

balance sheet and cash flow statements. These reports follow the IFRS principle and

record transaction according to this. IFRS issued by IASB (International Accounting

Standard Board) it provide clear guidelines to accountant, how they maintain it's

accounts and prepare according to this regulation. If Corporate Financial Solution

follow IFRS principle, so company as well as investors get the benefits. Investors

invest in this company because of the transparency and the cost of investment is also

very low (Collins, Pasewark and Riley, 2012).

International Accounting Standers (IAS):- It is older accounting standard, which is

replaced by International Financial Reporting Standers (IFRS), and it is issued by

International Accounting Standard Board (IASB). It is globally comparable standard

and it promote accountability, efficiency and transparency in the world.

3. Accounting rules and principles

Accounting has different rules and principles which needs to be followed by the firms in

order to prepare the financial statements in adequate manner. These are discussed as below:

Debit The Receiver, Credit The Giver:

The rule is used for personal accounts like debtors, Banks, creditors and capital account

etc. As when company receives from organisation which becomes an inflow for the company

therefore the person needs to be credited in books of account.

Debit What Comes In, Credit What Goes Out

This rule is applied in the case of real accounts. The real account includes machineries,

land and buildings etc. These assets have their debit balance by default. Therefore, when debit

what comes in which means there is an addition to the existing balance. Similarly, is case with,

credit what goes out which means reducing the account balance when a tangible asset goes out of

the organisation (DRURY, 2013).

Debit All Expenses And Losses, Credit All Incomes And Gains

This rule is applied when there is something related with nominal account. As capital of

the company is considered as its liability. Thus it has a default credit balance. When all incomes

2

International Financial Reporting Standard (IFRS):- IFRS contain some rules

and principles which is helpful in making financial reports like income statements,

balance sheet and cash flow statements. These reports follow the IFRS principle and

record transaction according to this. IFRS issued by IASB (International Accounting

Standard Board) it provide clear guidelines to accountant, how they maintain it's

accounts and prepare according to this regulation. If Corporate Financial Solution

follow IFRS principle, so company as well as investors get the benefits. Investors

invest in this company because of the transparency and the cost of investment is also

very low (Collins, Pasewark and Riley, 2012).

International Accounting Standers (IAS):- It is older accounting standard, which is

replaced by International Financial Reporting Standers (IFRS), and it is issued by

International Accounting Standard Board (IASB). It is globally comparable standard

and it promote accountability, efficiency and transparency in the world.

3. Accounting rules and principles

Accounting has different rules and principles which needs to be followed by the firms in

order to prepare the financial statements in adequate manner. These are discussed as below:

Debit The Receiver, Credit The Giver:

The rule is used for personal accounts like debtors, Banks, creditors and capital account

etc. As when company receives from organisation which becomes an inflow for the company

therefore the person needs to be credited in books of account.

Debit What Comes In, Credit What Goes Out

This rule is applied in the case of real accounts. The real account includes machineries,

land and buildings etc. These assets have their debit balance by default. Therefore, when debit

what comes in which means there is an addition to the existing balance. Similarly, is case with,

credit what goes out which means reducing the account balance when a tangible asset goes out of

the organisation (DRURY, 2013).

Debit All Expenses And Losses, Credit All Incomes And Gains

This rule is applied when there is something related with nominal account. As capital of

the company is considered as its liability. Thus it has a default credit balance. When all incomes

2

and gains are credited than it increases the capital and by debiting expenses and losses it

decreases the capital. It helps organisation to stay in balance.

Corporate Financial Solution is following all the rules which are related to the accounting

and helps in preparing final accounts effectively and efficiently.

Principles:

Principles are the set of standards which defines the way of preparing financial

statements in appropriate manner. There are various principles which are as follows:

Business entity concept:

The business entity concept states that business and its owners are the separate from each

other. It means the Corporate Financial Solutions has different identification on the basis of the

transaction which are carried out in their own name. According to this concept Company can sue

or be sued and it can also open its bank account. (Edwards, 2013).

Dual aspect concept:

Dual aspect concept refers that companies are liable to record their transaction on both

debit and credit side of books. Single entry system records only one aspect of the transaction

which leads to recording of irrelevant information in books of accounts. Therefore, to avoid this

problem dual aspect principle assure that every transaction needs to be recorded on both debit

and credit side of accounts (Lobo and Zhao, 2013).

Money measurement concept:

The money measurement concept is based on the money value. This concept states that

only those transaction needs to be recorded in the books of accounts which are measured in terms

of money. Therefore, Corporate Financial Solution follows this concept and record only those

transaction which can be valued in monetary term.

Cost principle:

This principle states that amounts of assets should be recorded at their acquiring cost. It

can be said that businesses are obliged to record an asset on their balance sheet for the amount

paid for the assets.

Going concern concept:

In this principle, it is assumed that the business will continue for long time as an entity.

As this is also not concerned regarding member of business as due to separate entity concept.

Matching principle:

3

decreases the capital. It helps organisation to stay in balance.

Corporate Financial Solution is following all the rules which are related to the accounting

and helps in preparing final accounts effectively and efficiently.

Principles:

Principles are the set of standards which defines the way of preparing financial

statements in appropriate manner. There are various principles which are as follows:

Business entity concept:

The business entity concept states that business and its owners are the separate from each

other. It means the Corporate Financial Solutions has different identification on the basis of the

transaction which are carried out in their own name. According to this concept Company can sue

or be sued and it can also open its bank account. (Edwards, 2013).

Dual aspect concept:

Dual aspect concept refers that companies are liable to record their transaction on both

debit and credit side of books. Single entry system records only one aspect of the transaction

which leads to recording of irrelevant information in books of accounts. Therefore, to avoid this

problem dual aspect principle assure that every transaction needs to be recorded on both debit

and credit side of accounts (Lobo and Zhao, 2013).

Money measurement concept:

The money measurement concept is based on the money value. This concept states that

only those transaction needs to be recorded in the books of accounts which are measured in terms

of money. Therefore, Corporate Financial Solution follows this concept and record only those

transaction which can be valued in monetary term.

Cost principle:

This principle states that amounts of assets should be recorded at their acquiring cost. It

can be said that businesses are obliged to record an asset on their balance sheet for the amount

paid for the assets.

Going concern concept:

In this principle, it is assumed that the business will continue for long time as an entity.

As this is also not concerned regarding member of business as due to separate entity concept.

Matching principle:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to this principle, all expenses of business should be matched with the revenues

which are generated in same accounting period.

4. Conventions and concepts related to consistency and material disclosure

The conventions are guidelines which arises from the practical applications of principles

of accounting. These are following conventions of accounting which are described as below:

Consistency convention:

The consistency convention states that organisations should follow the same kind of

methods for the similar transactions which are done every year. For example, Corporate

Financial Solutions uses the market price method for stock valuation so according to this

convention organisation is obliged to use same method for over the years. Similarly, if it follows

the straight line depreciation method for depreciating its fixed assets than company needs to use

the same method for over the period of time (Maskell, Baggaley and Grasso, 2016).

Material disclosure convention:

This convention of material disclosure states that company should disclose each and

every information in the books of accounts. It is essential for business to give and disclose all the

financial information to the investors, creditors and owner for better decision making.

CLIENT 1

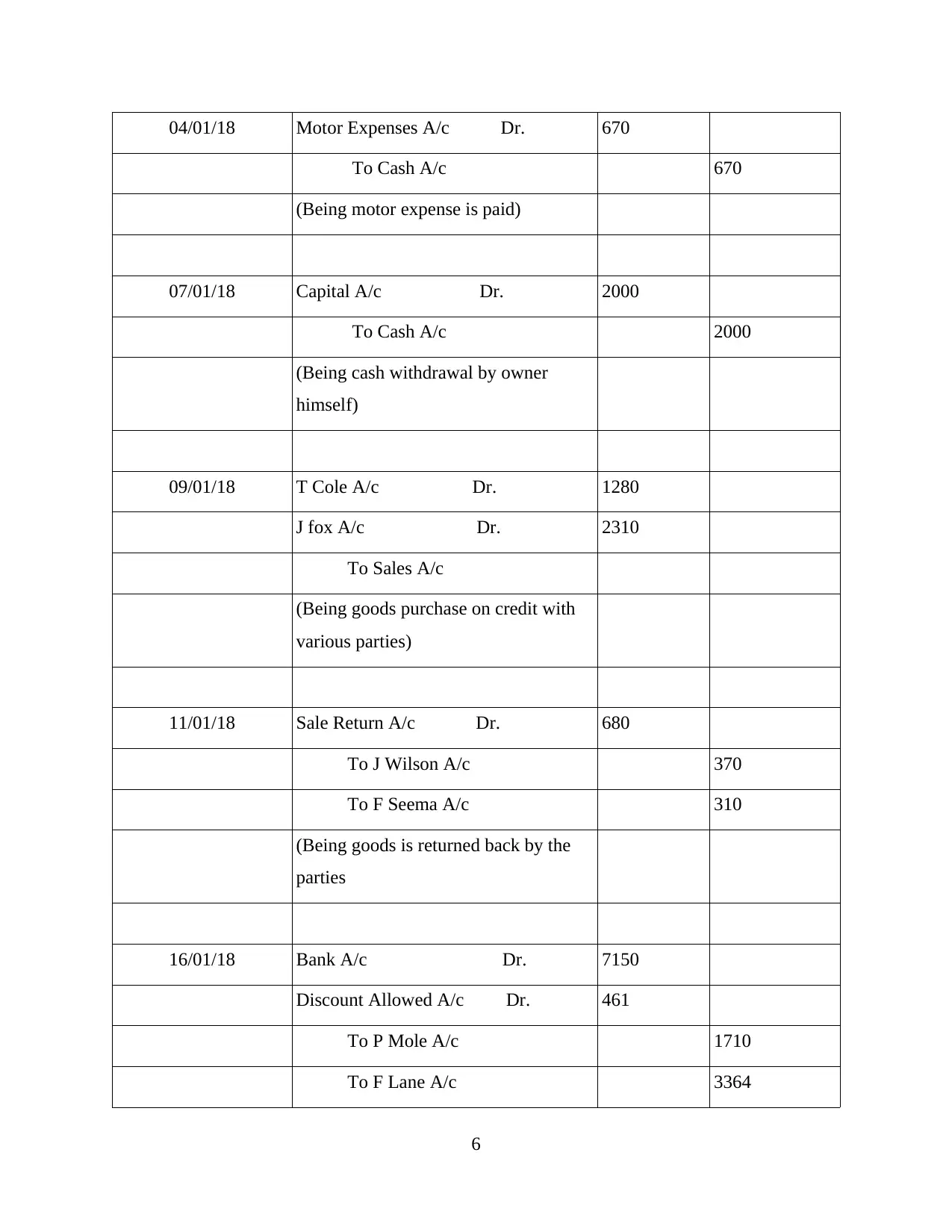

1. Journal entry in books of David Study

Date Particular Debit Credit

01/01/18 Premises A/C Dr. 440000

Motor Van A/C Dr. 45250

Fixtures A/C Dr. 10100

Inventory A/C Dr. 40900

P Mole A/C Dr. 2200

F Lane A/C Dr. 2100

Bank A/C Dr. 42400

Cash A/C Dr. 10600

4

which are generated in same accounting period.

4. Conventions and concepts related to consistency and material disclosure

The conventions are guidelines which arises from the practical applications of principles

of accounting. These are following conventions of accounting which are described as below:

Consistency convention:

The consistency convention states that organisations should follow the same kind of

methods for the similar transactions which are done every year. For example, Corporate

Financial Solutions uses the market price method for stock valuation so according to this

convention organisation is obliged to use same method for over the years. Similarly, if it follows

the straight line depreciation method for depreciating its fixed assets than company needs to use

the same method for over the period of time (Maskell, Baggaley and Grasso, 2016).

Material disclosure convention:

This convention of material disclosure states that company should disclose each and

every information in the books of accounts. It is essential for business to give and disclose all the

financial information to the investors, creditors and owner for better decision making.

CLIENT 1

1. Journal entry in books of David Study

Date Particular Debit Credit

01/01/18 Premises A/C Dr. 440000

Motor Van A/C Dr. 45250

Fixtures A/C Dr. 10100

Inventory A/C Dr. 40900

P Mole A/C Dr. 2200

F Lane A/C Dr. 2100

Bank A/C Dr. 42400

Cash A/C Dr. 10600

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To S Hamid A/c 10150

To J. Brown A/c 9600

To Capital A/c (Balancing Figure) 573800

(Being owner capital invested in

business)

01/01/01 Storage cost A/c Dr. 800

To bank a/c

(Being storage cost is paid)

800

02/01/18 Purchase A/c Dr. 7680

To S Hamid A/c 2450

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

(Being goods purchase on credit from

parties)

03/01/18 J Wilson A/c Dr. 2020

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

J Allen A/c Dr. 990

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c 11220

(Being goods sold on credit to various

parties)

5

To J. Brown A/c 9600

To Capital A/c (Balancing Figure) 573800

(Being owner capital invested in

business)

01/01/01 Storage cost A/c Dr. 800

To bank a/c

(Being storage cost is paid)

800

02/01/18 Purchase A/c Dr. 7680

To S Hamid A/c 2450

To D Main A/c 2560

To W Tag A/c 1060

To R Foot A/c 1610

(Being goods purchase on credit from

parties)

03/01/18 J Wilson A/c Dr. 2020

T Cole A/c Dr. 1840

F Seema A/c Dr. 2380

J Allen A/c Dr. 990

P White A/c Dr. 2820

F Lane A/c Dr. 1170

To Sales A/c 11220

(Being goods sold on credit to various

parties)

5

04/01/18 Motor Expenses A/c Dr. 670

To Cash A/c 670

(Being motor expense is paid)

07/01/18 Capital A/c Dr. 2000

To Cash A/c 2000

(Being cash withdrawal by owner

himself)

09/01/18 T Cole A/c Dr. 1280

J fox A/c Dr. 2310

To Sales A/c

(Being goods purchase on credit with

various parties)

11/01/18 Sale Return A/c Dr. 680

To J Wilson A/c 370

To F Seema A/c 310

(Being goods is returned back by the

parties

16/01/18 Bank A/c Dr. 7150

Discount Allowed A/c Dr. 461

To P Mole A/c 1710

To F Lane A/c 3364

6

To Cash A/c 670

(Being motor expense is paid)

07/01/18 Capital A/c Dr. 2000

To Cash A/c 2000

(Being cash withdrawal by owner

himself)

09/01/18 T Cole A/c Dr. 1280

J fox A/c Dr. 2310

To Sales A/c

(Being goods purchase on credit with

various parties)

11/01/18 Sale Return A/c Dr. 680

To J Wilson A/c 370

To F Seema A/c 310

(Being goods is returned back by the

parties

16/01/18 Bank A/c Dr. 7150

Discount Allowed A/c Dr. 461

To P Mole A/c 1710

To F Lane A/c 3364

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

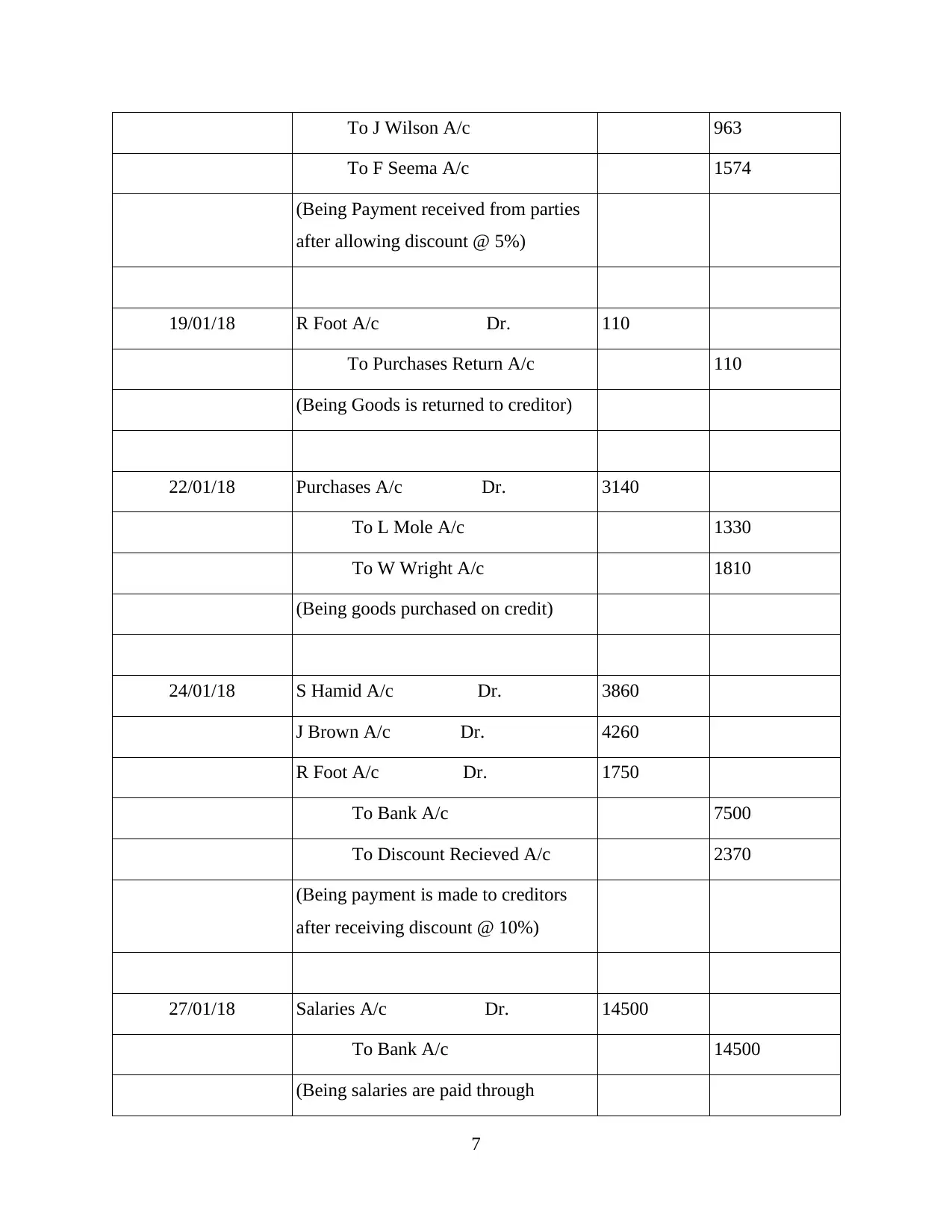

To J Wilson A/c 963

To F Seema A/c 1574

(Being Payment received from parties

after allowing discount @ 5%)

19/01/18 R Foot A/c Dr. 110

To Purchases Return A/c 110

(Being Goods is returned to creditor)

22/01/18 Purchases A/c Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/01/18 S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors

after receiving discount @ 10%)

27/01/18 Salaries A/c Dr. 14500

To Bank A/c 14500

(Being salaries are paid through

7

To F Seema A/c 1574

(Being Payment received from parties

after allowing discount @ 5%)

19/01/18 R Foot A/c Dr. 110

To Purchases Return A/c 110

(Being Goods is returned to creditor)

22/01/18 Purchases A/c Dr. 3140

To L Mole A/c 1330

To W Wright A/c 1810

(Being goods purchased on credit)

24/01/18 S Hamid A/c Dr. 3860

J Brown A/c Dr. 4260

R Foot A/c Dr. 1750

To Bank A/c 7500

To Discount Recieved A/c 2370

(Being payment is made to creditors

after receiving discount @ 10%)

27/01/18 Salaries A/c Dr. 14500

To Bank A/c 14500

(Being salaries are paid through

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

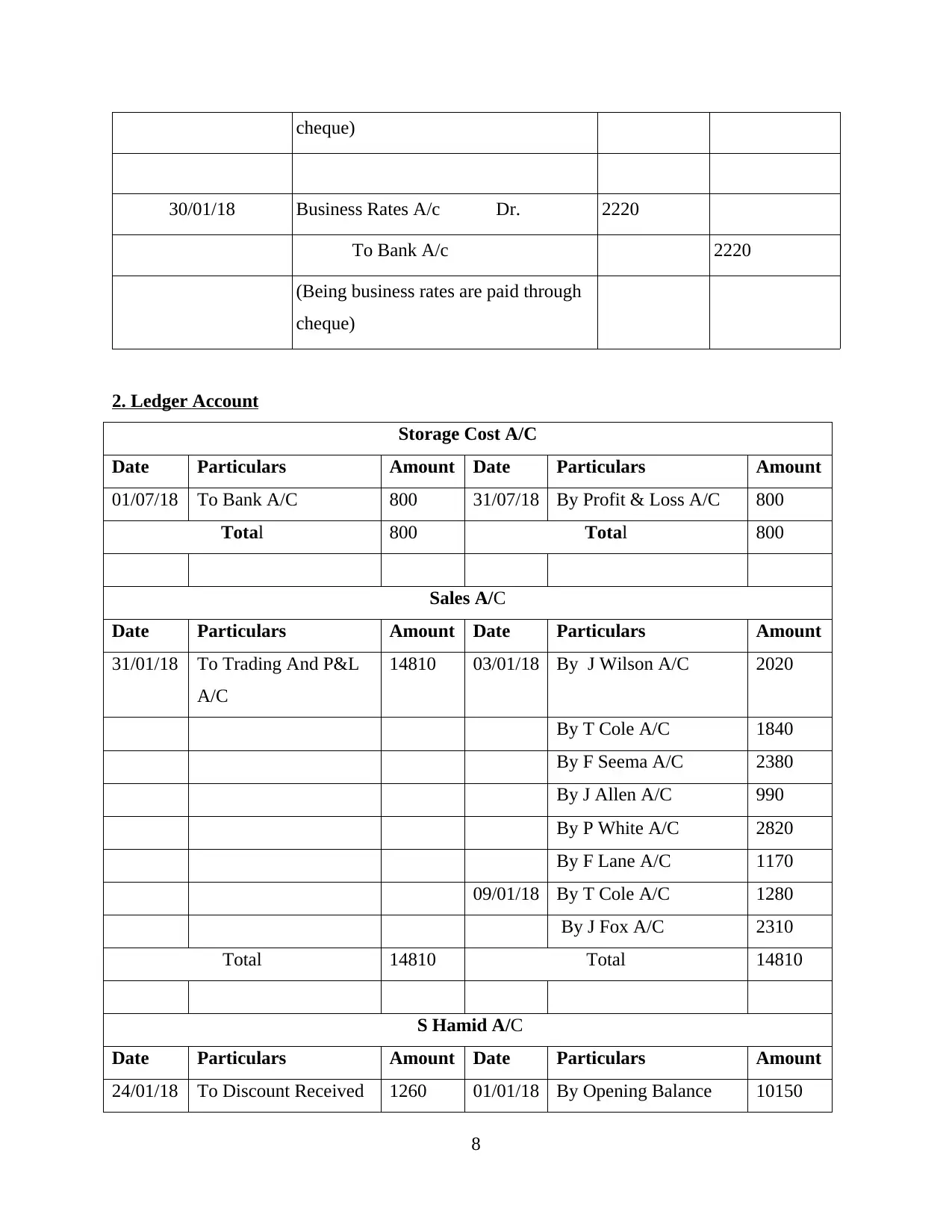

cheque)

30/01/18 Business Rates A/c Dr. 2220

To Bank A/c 2220

(Being business rates are paid through

cheque)

2. Ledger Account

Storage Cost A/C

Date Particulars Amount Date Particulars Amount

01/07/18 To Bank A/C 800 31/07/18 By Profit & Loss A/C 800

Total 800 Total 800

Sales A/C

Date Particulars Amount Date Particulars Amount

31/01/18 To Trading And P&L

A/C

14810 03/01/18 By J Wilson A/C 2020

By T Cole A/C 1840

By F Seema A/C 2380

By J Allen A/C 990

By P White A/C 2820

By F Lane A/C 1170

09/01/18 By T Cole A/C 1280

By J Fox A/C 2310

Total 14810 Total 14810

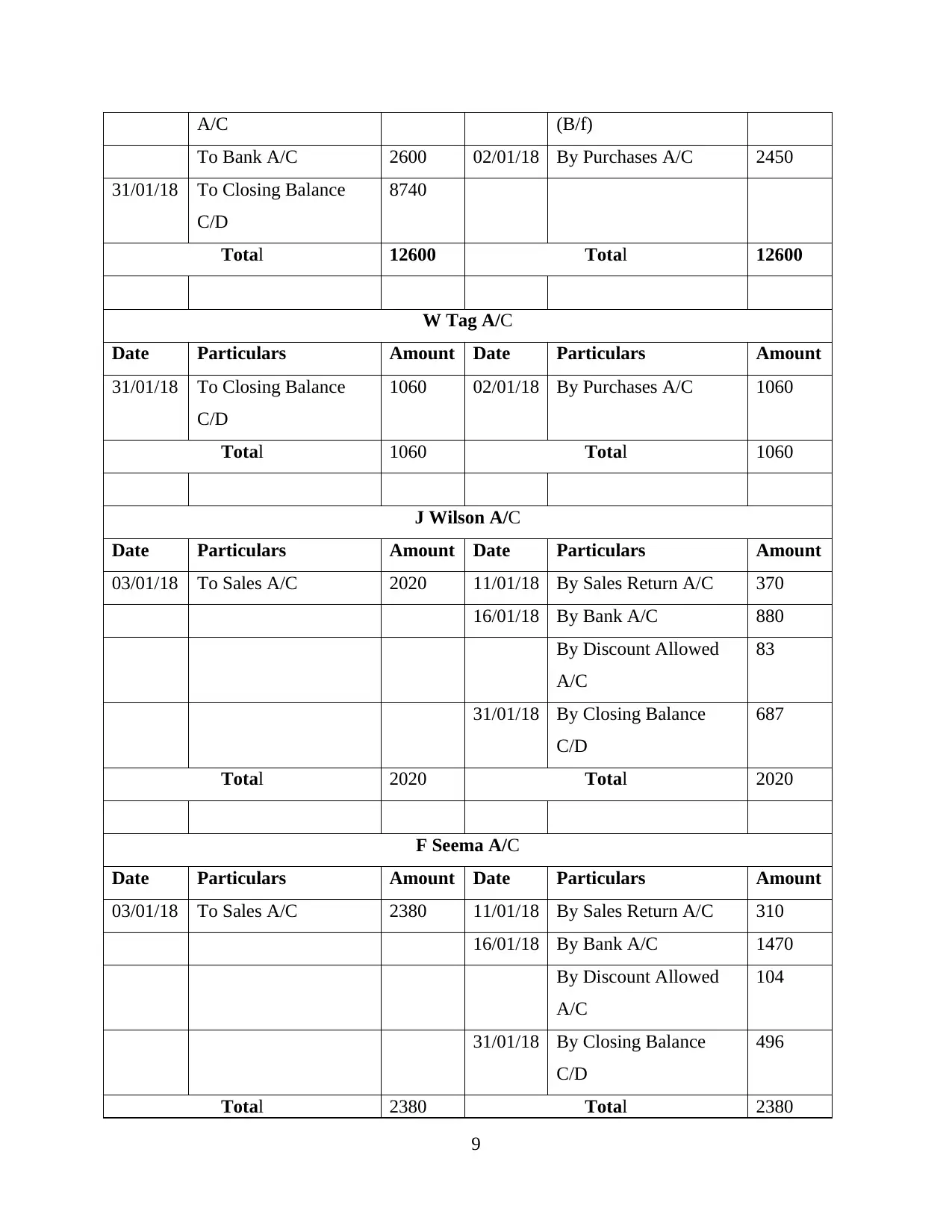

S Hamid A/C

Date Particulars Amount Date Particulars Amount

24/01/18 To Discount Received 1260 01/01/18 By Opening Balance 10150

8

30/01/18 Business Rates A/c Dr. 2220

To Bank A/c 2220

(Being business rates are paid through

cheque)

2. Ledger Account

Storage Cost A/C

Date Particulars Amount Date Particulars Amount

01/07/18 To Bank A/C 800 31/07/18 By Profit & Loss A/C 800

Total 800 Total 800

Sales A/C

Date Particulars Amount Date Particulars Amount

31/01/18 To Trading And P&L

A/C

14810 03/01/18 By J Wilson A/C 2020

By T Cole A/C 1840

By F Seema A/C 2380

By J Allen A/C 990

By P White A/C 2820

By F Lane A/C 1170

09/01/18 By T Cole A/C 1280

By J Fox A/C 2310

Total 14810 Total 14810

S Hamid A/C

Date Particulars Amount Date Particulars Amount

24/01/18 To Discount Received 1260 01/01/18 By Opening Balance 10150

8

A/C (B/f)

To Bank A/C 2600 02/01/18 By Purchases A/C 2450

31/01/18 To Closing Balance

C/D

8740

Total 12600 Total 12600

W Tag A/C

Date Particulars Amount Date Particulars Amount

31/01/18 To Closing Balance

C/D

1060 02/01/18 By Purchases A/C 1060

Total 1060 Total 1060

J Wilson A/C

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/C 2020 11/01/18 By Sales Return A/C 370

16/01/18 By Bank A/C 880

By Discount Allowed

A/C

83

31/01/18 By Closing Balance

C/D

687

Total 2020 Total 2020

F Seema A/C

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/C 2380 11/01/18 By Sales Return A/C 310

16/01/18 By Bank A/C 1470

By Discount Allowed

A/C

104

31/01/18 By Closing Balance

C/D

496

Total 2380 Total 2380

9

To Bank A/C 2600 02/01/18 By Purchases A/C 2450

31/01/18 To Closing Balance

C/D

8740

Total 12600 Total 12600

W Tag A/C

Date Particulars Amount Date Particulars Amount

31/01/18 To Closing Balance

C/D

1060 02/01/18 By Purchases A/C 1060

Total 1060 Total 1060

J Wilson A/C

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/C 2020 11/01/18 By Sales Return A/C 370

16/01/18 By Bank A/C 880

By Discount Allowed

A/C

83

31/01/18 By Closing Balance

C/D

687

Total 2020 Total 2020

F Seema A/C

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/C 2380 11/01/18 By Sales Return A/C 310

16/01/18 By Bank A/C 1470

By Discount Allowed

A/C

104

31/01/18 By Closing Balance

C/D

496

Total 2380 Total 2380

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.