Finance for Managers Report: Financial Records and Project Appraisal

VerifiedAdded on 2020/12/09

|16

|3912

|361

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles and their application in a managerial context. It begins by examining the purpose and requirements of financial records, including techniques for recording financial information and the relevant legal and organizational requirements. The report then explores the importance and usefulness of financial statements to stakeholders, highlighting the differences between management and financial accounting. Budgetary control processes and various costing methods used for pricing policies are also discussed. The second part of the report delves into determining variances on cost and revenue, followed by an analysis of project appraisal methods, including payback period, net present value, internal rate of return, and average rate of return. Finally, the report covers different sources of funding and the components of working capital management. The report utilizes examples from Malta Ltd. to illustrate key concepts, providing a practical guide to financial analysis and management.

FINANCE FOR

MANAGER

MANAGER

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 The purpose and requirement of financial records................................................................1

1.2 Techniques for recording financial information....................................................................2

1.3 The legal and organisational requirements of financial records............................................3

1.4 The importance and usefulness of financial statements to stakeholders................................3

3.3 Differences in management and financial accounting...........................................................4

3.2. The process of budgetary control. ........................................................................................5

3.4 Different costing methods used for pricing policies.............................................................6

TASK 2............................................................................................................................................7

3.3 Determining the variances on cost and revenue....................................................................7

4.1 Demonstrate the main methods of project appraisal..............................................................8

4.2 Calculation of the projects.....................................................................................................9

4.3 Different sources of funding................................................................................................12

2.1 The components of working capital and how it is useful in working capital management.13

2.2 The components of working capital management...............................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 The purpose and requirement of financial records................................................................1

1.2 Techniques for recording financial information....................................................................2

1.3 The legal and organisational requirements of financial records............................................3

1.4 The importance and usefulness of financial statements to stakeholders................................3

3.3 Differences in management and financial accounting...........................................................4

3.2. The process of budgetary control. ........................................................................................5

3.4 Different costing methods used for pricing policies.............................................................6

TASK 2............................................................................................................................................7

3.3 Determining the variances on cost and revenue....................................................................7

4.1 Demonstrate the main methods of project appraisal..............................................................8

4.2 Calculation of the projects.....................................................................................................9

4.3 Different sources of funding................................................................................................12

2.1 The components of working capital and how it is useful in working capital management.13

2.2 The components of working capital management...............................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Financial accounting is a key element for financial management of any organization.

Financial control is very important to for all the financial activities in an organization. The

present report focuses on various aspects in Malta Ltd company which is important for a

financial manager. The report depicts purpose of keeping financial records and why it is

important. Different techniques of financial reporting are mentioned in report. The rules and

regulations required for financial recording is presented. Different costing methods of pricing is

described in the report. Calculation on variance is present in report which shows actual and

budgeted profit figures. The report presents the calculation on different techniques of project

appraisal for Board of Director to choose a suitable project for investment., by describing

methods of project appraisal.

TASK 1

1.1 The purpose and requirement of financial records

It is a document which records all financial transactions of an organization, individual or

business entity (Yin, Arbaiy and Din. 2017). Books of account records all the necessary

transactions which helps in financial statements such as balance sheet, trail balance, general

ledger etc.

The purpose of financial records is:

Maintaining proper records of expenses, income would help in filing the taxes, and will

avoid any problem regarding financial accounting.

It helps in establishing accurate and complete accounting and recording system. For preparing accurate financial statements which helps in ascertaining financial

performance at end of year.

The importance of keeping financial records are:

Financial records help in monitoring the performance of a business. It improves in

decision-making for business,

1

Financial accounting is a key element for financial management of any organization.

Financial control is very important to for all the financial activities in an organization. The

present report focuses on various aspects in Malta Ltd company which is important for a

financial manager. The report depicts purpose of keeping financial records and why it is

important. Different techniques of financial reporting are mentioned in report. The rules and

regulations required for financial recording is presented. Different costing methods of pricing is

described in the report. Calculation on variance is present in report which shows actual and

budgeted profit figures. The report presents the calculation on different techniques of project

appraisal for Board of Director to choose a suitable project for investment., by describing

methods of project appraisal.

TASK 1

1.1 The purpose and requirement of financial records

It is a document which records all financial transactions of an organization, individual or

business entity (Yin, Arbaiy and Din. 2017). Books of account records all the necessary

transactions which helps in financial statements such as balance sheet, trail balance, general

ledger etc.

The purpose of financial records is:

Maintaining proper records of expenses, income would help in filing the taxes, and will

avoid any problem regarding financial accounting.

It helps in establishing accurate and complete accounting and recording system. For preparing accurate financial statements which helps in ascertaining financial

performance at end of year.

The importance of keeping financial records are:

Financial records help in monitoring the performance of a business. It improves in

decision-making for business,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Keeping good financial records are the key element in preparing financial statements for

company, like income statements, balance sheet of company (WHAT IS FINANCIAL

RECORD, 2018).

Financial records assist in identifying the sources of different transactions. It is important

to keep different accounts for sources like income and expenditure.

Recording of financial transactions will help to prepare the tax return files.

1.2 Techniques for recording financial information

Data of all financial activities in business are called financial information. It would help

in financial records and preparing financial statements of company.

Techniques for recording financial information are:

Reconciliation: It is a process of comparing financial information that is being recorded

in two systems or accounts (Schinckus ,2018). It is important to analyse and compare both the

entries of transactions and make correction if required to make information accurate to use.

Verification: It is a process of examining information contained in report or system to

ensure that the information is accurate and complete. Every information should be verified

before recording in financial books.

Journals: It refers to record the accounting transaction of the organization with the

particular date. It helps the company to record all the transaction systematically and with

accuracy for the further use by Ledger.

Ledger: It helps to record the economic transaction in term of money with debit and credit

side. It is used to record the book keeping entries for the further calculation of balance sheet and

profit and loss account.

Double entry system: It refers that for every transaction amount will be recorded in two

accounts to maintain the accuracy of the data. It helps to match the debit side of the transactions

to its credit side. Companies normally use the double entry system to minimize the errors and

fraudulent activities.

2

company, like income statements, balance sheet of company (WHAT IS FINANCIAL

RECORD, 2018).

Financial records assist in identifying the sources of different transactions. It is important

to keep different accounts for sources like income and expenditure.

Recording of financial transactions will help to prepare the tax return files.

1.2 Techniques for recording financial information

Data of all financial activities in business are called financial information. It would help

in financial records and preparing financial statements of company.

Techniques for recording financial information are:

Reconciliation: It is a process of comparing financial information that is being recorded

in two systems or accounts (Schinckus ,2018). It is important to analyse and compare both the

entries of transactions and make correction if required to make information accurate to use.

Verification: It is a process of examining information contained in report or system to

ensure that the information is accurate and complete. Every information should be verified

before recording in financial books.

Journals: It refers to record the accounting transaction of the organization with the

particular date. It helps the company to record all the transaction systematically and with

accuracy for the further use by Ledger.

Ledger: It helps to record the economic transaction in term of money with debit and credit

side. It is used to record the book keeping entries for the further calculation of balance sheet and

profit and loss account.

Double entry system: It refers that for every transaction amount will be recorded in two

accounts to maintain the accuracy of the data. It helps to match the debit side of the transactions

to its credit side. Companies normally use the double entry system to minimize the errors and

fraudulent activities.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 The legal and organisational requirements of financial records

The laws and regulations are very important for recording of financial information.

They are the basic requirements for recording financial information, as every external or internal

user of financial statements wants it to be accurate, relevant and fairly presented (Collier, 2015).

The major authorities involved in formatting regulations are:

IASB: International Accounting Standard Board is the conceptual framework for

recording of financial reporting. The general purpose of financial recording is to help in making

financial statements. Laws are required so that financial statements would be accurate and can be

useful to the external users of financial statements.

FRS: Financial Reporting Council is regulation board which frameworks guidelines for

monitoring and execution of different financial disclosures associated with financial recording

system. It is issued by IFRS to provide a common global language for business affairs so that the

financial statements of company can be used by different companies across the world.

GAAP: General Accepted Accounting Principles established the laws and regulations

about how company should manage its books of accounting. Company should make accounting

records according to applicable company law (Page., 2014). New UK GAAP aim to make the

preparation of financial statement to be easier and cheaper.

1.4 The importance and usefulness of financial statements to stakeholders

Financial statements are prepared for the external users so that they can understand and

compare financial position of a company, which will help them to make decisions about their

investment (Flower,2016). The usefulness of financial statements to different users are as

follows:

Owners and investors: The stakeholders of company need to know financial information

of with in a specific time period. This information will help them to make decisions regarding

whether to invest in company or not. Owners of small business will access financial statements

to know success and profitability of business.

Management: Financial information is useful to management of the organization for

accessing planning, controlling and decision-making process (Chen and et.al., 2018). The

3

The laws and regulations are very important for recording of financial information.

They are the basic requirements for recording financial information, as every external or internal

user of financial statements wants it to be accurate, relevant and fairly presented (Collier, 2015).

The major authorities involved in formatting regulations are:

IASB: International Accounting Standard Board is the conceptual framework for

recording of financial reporting. The general purpose of financial recording is to help in making

financial statements. Laws are required so that financial statements would be accurate and can be

useful to the external users of financial statements.

FRS: Financial Reporting Council is regulation board which frameworks guidelines for

monitoring and execution of different financial disclosures associated with financial recording

system. It is issued by IFRS to provide a common global language for business affairs so that the

financial statements of company can be used by different companies across the world.

GAAP: General Accepted Accounting Principles established the laws and regulations

about how company should manage its books of accounting. Company should make accounting

records according to applicable company law (Page., 2014). New UK GAAP aim to make the

preparation of financial statement to be easier and cheaper.

1.4 The importance and usefulness of financial statements to stakeholders

Financial statements are prepared for the external users so that they can understand and

compare financial position of a company, which will help them to make decisions about their

investment (Flower,2016). The usefulness of financial statements to different users are as

follows:

Owners and investors: The stakeholders of company need to know financial information

of with in a specific time period. This information will help them to make decisions regarding

whether to invest in company or not. Owners of small business will access financial statements

to know success and profitability of business.

Management: Financial information is useful to management of the organization for

accessing planning, controlling and decision-making process (Chen and et.al., 2018). The

3

necessary steps can be taken to improve financial performance of the company by evaluating the

information within a specific time period.

Lenders: Banks and other financial institutions will need these statements to ascertain

repayment capability of company.

Government: The government bodies and tax authorities will use company financial

statements for taxation and regulatory purpose.

Customer: The company's ability to continue its existence can be found from its

financial position in management and financial accounting. The statements will help the

customers to evaluate the solvency position of the company.

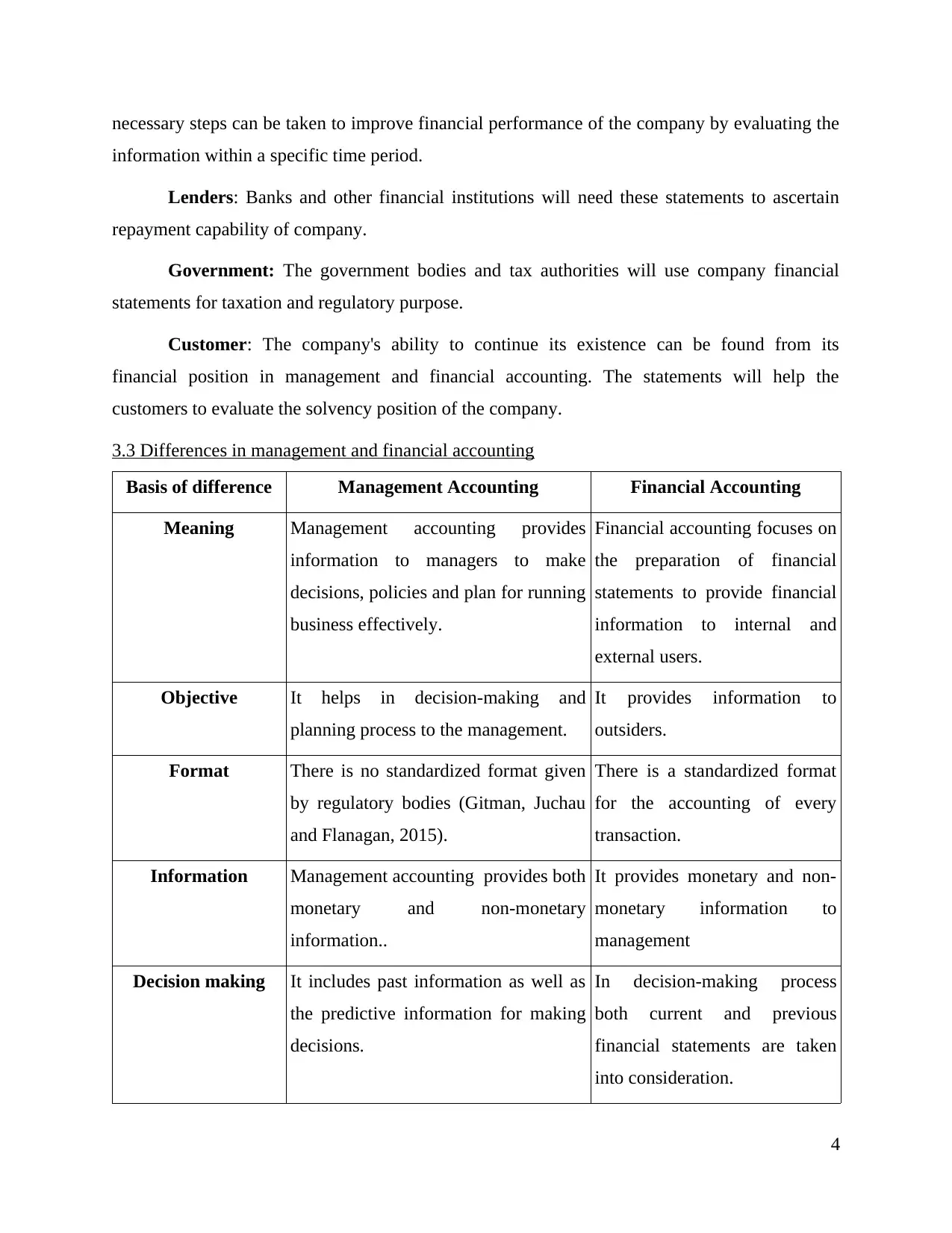

3.3 Differences in management and financial accounting

Basis of difference Management Accounting Financial Accounting

Meaning Management accounting provides

information to managers to make

decisions, policies and plan for running

business effectively.

Financial accounting focuses on

the preparation of financial

statements to provide financial

information to internal and

external users.

Objective It helps in decision-making and

planning process to the management.

It provides information to

outsiders.

Format There is no standardized format given

by regulatory bodies (Gitman, Juchau

and Flanagan, 2015).

There is a standardized format

for the accounting of every

transaction.

Information Management accounting provides both

monetary and non-monetary

information..

It provides monetary and non-

monetary information to

management

Decision making It includes past information as well as

the predictive information for making

decisions.

In decision-making process

both current and previous

financial statements are taken

into consideration.

4

information within a specific time period.

Lenders: Banks and other financial institutions will need these statements to ascertain

repayment capability of company.

Government: The government bodies and tax authorities will use company financial

statements for taxation and regulatory purpose.

Customer: The company's ability to continue its existence can be found from its

financial position in management and financial accounting. The statements will help the

customers to evaluate the solvency position of the company.

3.3 Differences in management and financial accounting

Basis of difference Management Accounting Financial Accounting

Meaning Management accounting provides

information to managers to make

decisions, policies and plan for running

business effectively.

Financial accounting focuses on

the preparation of financial

statements to provide financial

information to internal and

external users.

Objective It helps in decision-making and

planning process to the management.

It provides information to

outsiders.

Format There is no standardized format given

by regulatory bodies (Gitman, Juchau

and Flanagan, 2015).

There is a standardized format

for the accounting of every

transaction.

Information Management accounting provides both

monetary and non-monetary

information..

It provides monetary and non-

monetary information to

management

Decision making It includes past information as well as

the predictive information for making

decisions.

In decision-making process

both current and previous

financial statements are taken

into consideration.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

User It is used by internal management only It is used by both management

and external users like

stakeholders, investors etc.

3.2. The process of budgetary control.

The process of controlling and monitoring budget in given accounting period is

Budgetary-control (Schaltegger and Burritt, 2017). it controls the actual and budgeted income

and expenditure; it monitors whether a company is operating according to planned budget or

there is a need for any changes is required.

The budgetary-control process includes the following steps:

Establish a plan: At first the budget will be created which will coordinate with all

business activities. The planning for income and spending on department will be done. A set of

goals should be prepared that management wants to achieve.

Record the actual performance and comparison: After budget is created, next step is to

monitoring and analysing and interpreting actual performance of a company with budgeted goals

(Maelah and Yadzid, 2018). The management will use budget report for comparison.

Standard report: After knowing comparing value, next step is to set a standard report for

budgetary control process. This report will allow the managers to focus on favourable and

unfavourable variance (What is Budgetary Control, 2018).

Taking actions: These steps occurs at the end of accounting year; management takes

steps against the actual performance of year and budgeted goals. A proper action will be planned

by management, and it will execute in the next accounting year.

3.4 Different costing methods used for pricing policies

Cost method which are used in pricing policies are as follows:

Absorption costing: It refers to the cost associated with the production of particular

product and services. It helps the organization in inventory valuation to present accurate

amount in balance sheet. It includes all the fixed and variable cost while calculating the

actual cost of the product.

5

and external users like

stakeholders, investors etc.

3.2. The process of budgetary control.

The process of controlling and monitoring budget in given accounting period is

Budgetary-control (Schaltegger and Burritt, 2017). it controls the actual and budgeted income

and expenditure; it monitors whether a company is operating according to planned budget or

there is a need for any changes is required.

The budgetary-control process includes the following steps:

Establish a plan: At first the budget will be created which will coordinate with all

business activities. The planning for income and spending on department will be done. A set of

goals should be prepared that management wants to achieve.

Record the actual performance and comparison: After budget is created, next step is to

monitoring and analysing and interpreting actual performance of a company with budgeted goals

(Maelah and Yadzid, 2018). The management will use budget report for comparison.

Standard report: After knowing comparing value, next step is to set a standard report for

budgetary control process. This report will allow the managers to focus on favourable and

unfavourable variance (What is Budgetary Control, 2018).

Taking actions: These steps occurs at the end of accounting year; management takes

steps against the actual performance of year and budgeted goals. A proper action will be planned

by management, and it will execute in the next accounting year.

3.4 Different costing methods used for pricing policies

Cost method which are used in pricing policies are as follows:

Absorption costing: It refers to the cost associated with the production of particular

product and services. It helps the organization in inventory valuation to present accurate

amount in balance sheet. It includes all the fixed and variable cost while calculating the

actual cost of the product.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal cost : It refers to the cost related to one additional unit of production. In this

fixed cost of the production is considered as cost of period while variable cost considered

as product cost.

Cost based pricing: In this method a certain percentage of desired profit margin which

will be added to final price of a product. The profit margin will be decided according to

cost of production.

Demand based pricing: In this method price of the product is determined on demand of

the product (Hanna and Dodge, 2017). If a demand of product is more, organization will

set the high price to gain profit and vice versa.

TASK 2

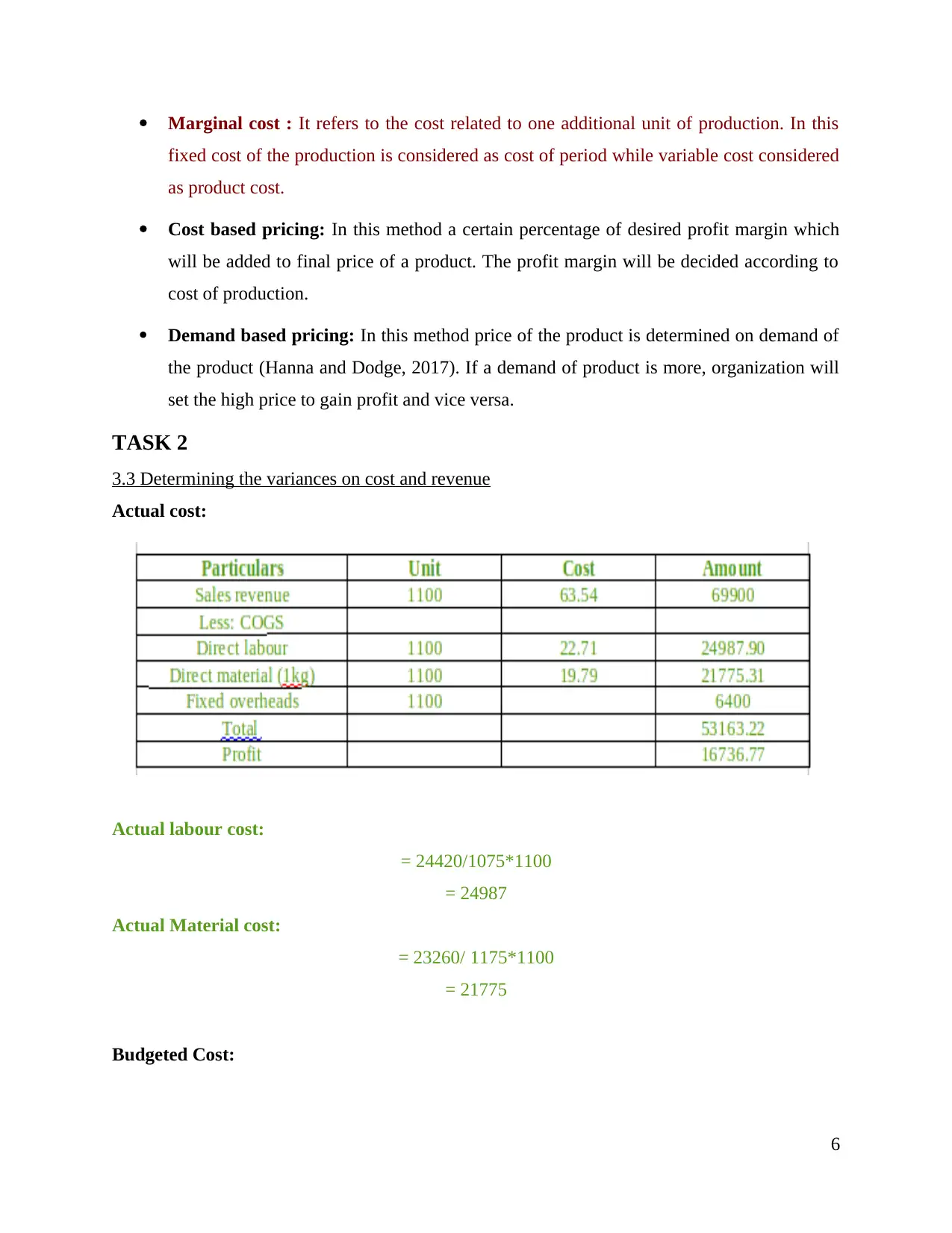

3.3 Determining the variances on cost and revenue

Actual cost:

Actual labour cost:

= 24420/1075*1100

= 24987

Actual Material cost:

= 23260/ 1175*1100

= 21775

Budgeted Cost:

6

fixed cost of the production is considered as cost of period while variable cost considered

as product cost.

Cost based pricing: In this method a certain percentage of desired profit margin which

will be added to final price of a product. The profit margin will be decided according to

cost of production.

Demand based pricing: In this method price of the product is determined on demand of

the product (Hanna and Dodge, 2017). If a demand of product is more, organization will

set the high price to gain profit and vice versa.

TASK 2

3.3 Determining the variances on cost and revenue

Actual cost:

Actual labour cost:

= 24420/1075*1100

= 24987

Actual Material cost:

= 23260/ 1175*1100

= 21775

Budgeted Cost:

6

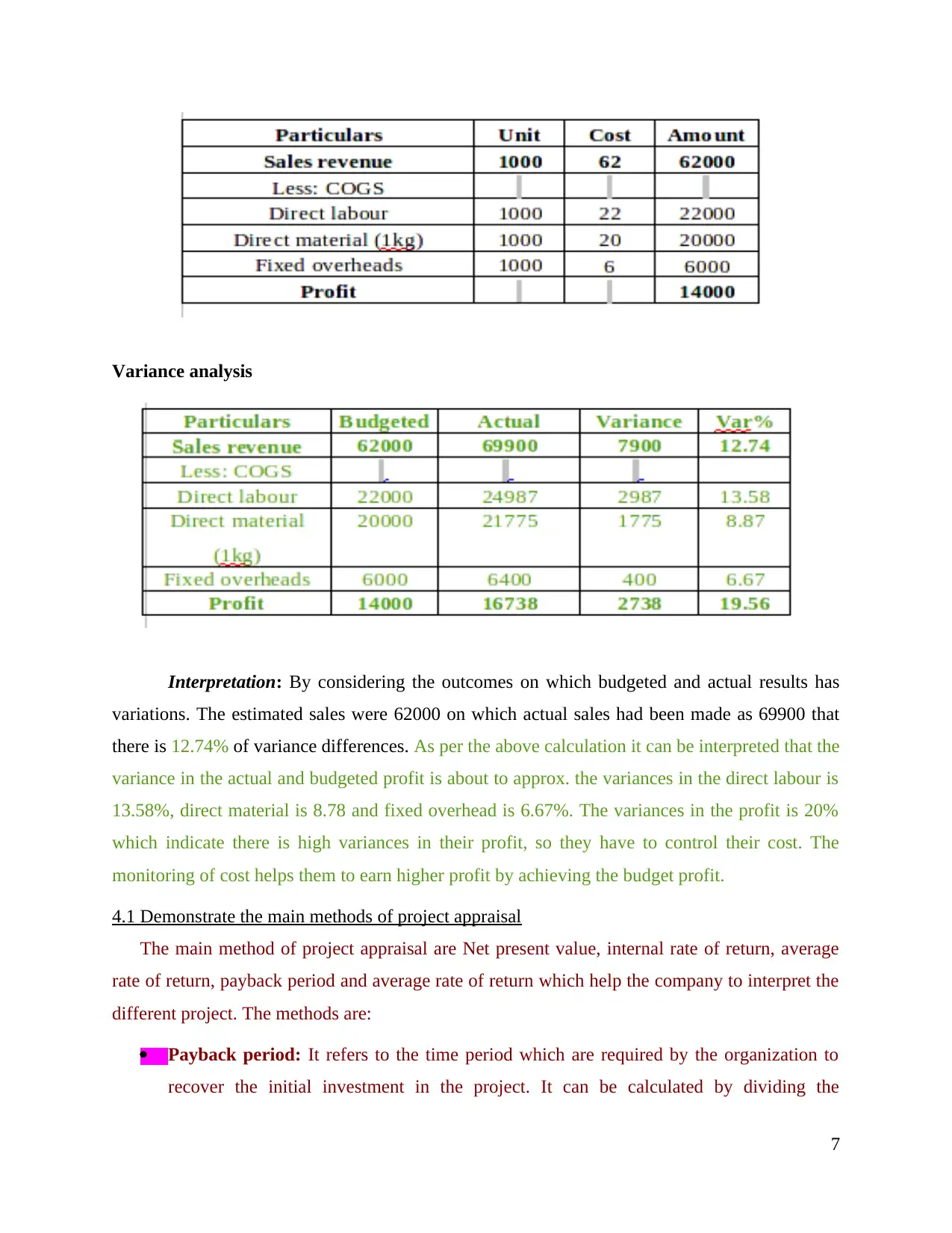

Variance analysis

Interpretation: By considering the outcomes on which budgeted and actual results has

variations. The estimated sales were 62000 on which actual sales had been made as 69900 that

there is 12.74% of variance differences. As per the above calculation it can be interpreted that the

variance in the actual and budgeted profit is about to approx. the variances in the direct labour is

13.58%, direct material is 8.78 and fixed overhead is 6.67%. The variances in the profit is 20%

which indicate there is high variances in their profit, so they have to control their cost. The

monitoring of cost helps them to earn higher profit by achieving the budget profit.

4.1 Demonstrate the main methods of project appraisal

The main method of project appraisal are Net present value, internal rate of return, average

rate of return, payback period and average rate of return which help the company to interpret the

different project. The methods are:

Payback period: It refers to the time period which are required by the organization to

recover the initial investment in the project. It can be calculated by dividing the

7

Interpretation: By considering the outcomes on which budgeted and actual results has

variations. The estimated sales were 62000 on which actual sales had been made as 69900 that

there is 12.74% of variance differences. As per the above calculation it can be interpreted that the

variance in the actual and budgeted profit is about to approx. the variances in the direct labour is

13.58%, direct material is 8.78 and fixed overhead is 6.67%. The variances in the profit is 20%

which indicate there is high variances in their profit, so they have to control their cost. The

monitoring of cost helps them to earn higher profit by achieving the budget profit.

4.1 Demonstrate the main methods of project appraisal

The main method of project appraisal are Net present value, internal rate of return, average

rate of return, payback period and average rate of return which help the company to interpret the

different project. The methods are:

Payback period: It refers to the time period which are required by the organization to

recover the initial investment in the project. It can be calculated by dividing the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

investment cost with the annual cash flow. It is simple to calculate and interpret the data

but the drawback is it does not include the present value and life of the project or assets.

Net present value: It is used in capital budgeting and investment planning to evaluate the

profitability of the project. Positive NPV indicate that project is beneficial for the

organization. It helps the organization to compare the profitability of two project. But it is

based on certain assumptions i.e. firm's cost of capital.

Internal rate of return: It is used by company to evaluate the profitability and

attractiveness of the project. The advantage of IRR is that it consider the timed value of

money and easy to understand and interpret the data. But it also has some disadvantages

that it ignore the future cost and size of the project.

Average rate of return: It is used to calculate the profitability of the firm by comparing

two and more investment opportunities. The percentage of ARR indicates the earning of

the project. It is easy to understand and calculate but it ignores the time value of money

which does not provide accurate data and information.

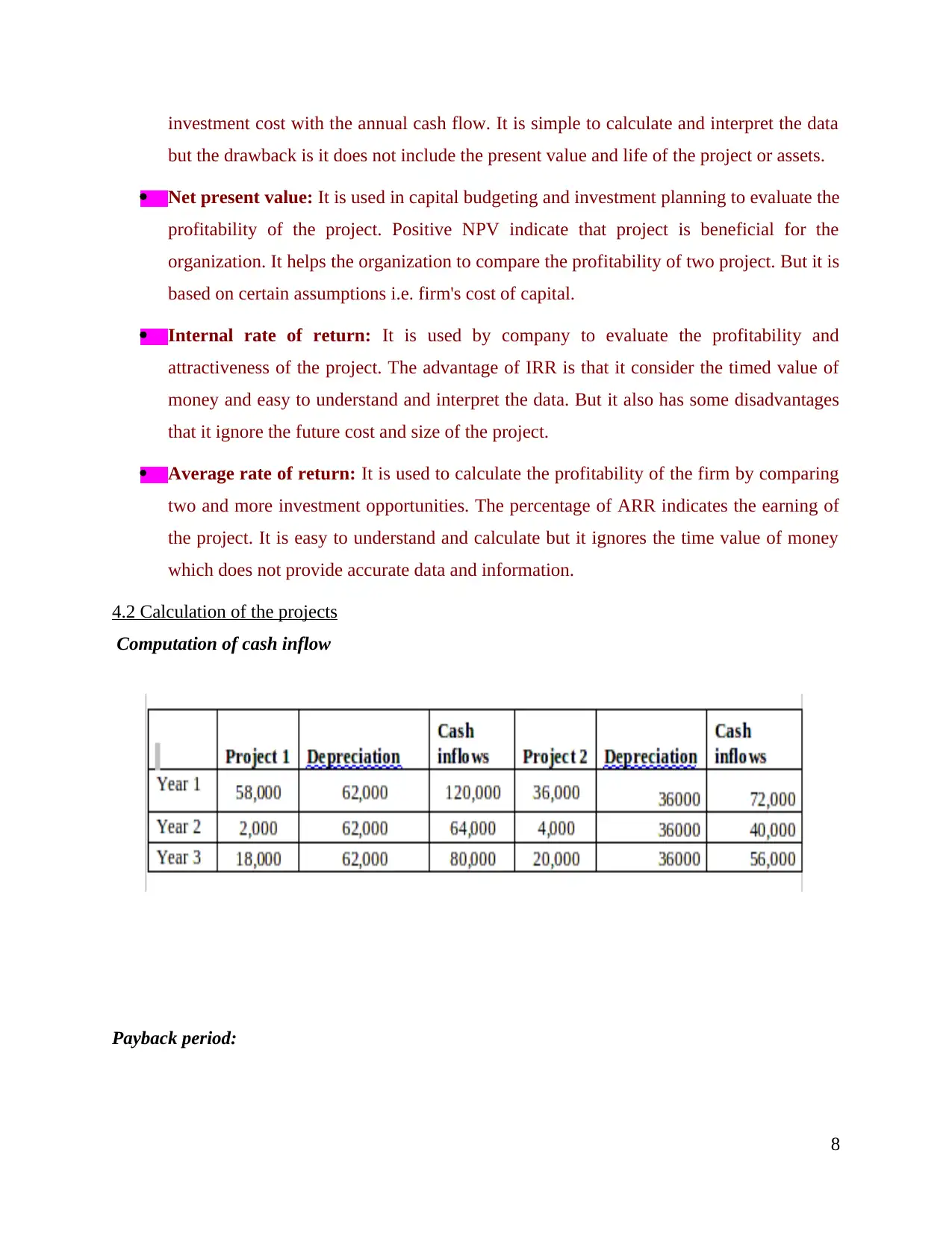

4.2 Calculation of the projects

Computation of cash inflow

Payback period:

8

but the drawback is it does not include the present value and life of the project or assets.

Net present value: It is used in capital budgeting and investment planning to evaluate the

profitability of the project. Positive NPV indicate that project is beneficial for the

organization. It helps the organization to compare the profitability of two project. But it is

based on certain assumptions i.e. firm's cost of capital.

Internal rate of return: It is used by company to evaluate the profitability and

attractiveness of the project. The advantage of IRR is that it consider the timed value of

money and easy to understand and interpret the data. But it also has some disadvantages

that it ignore the future cost and size of the project.

Average rate of return: It is used to calculate the profitability of the firm by comparing

two and more investment opportunities. The percentage of ARR indicates the earning of

the project. It is easy to understand and calculate but it ignores the time value of money

which does not provide accurate data and information.

4.2 Calculation of the projects

Computation of cash inflow

Payback period:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

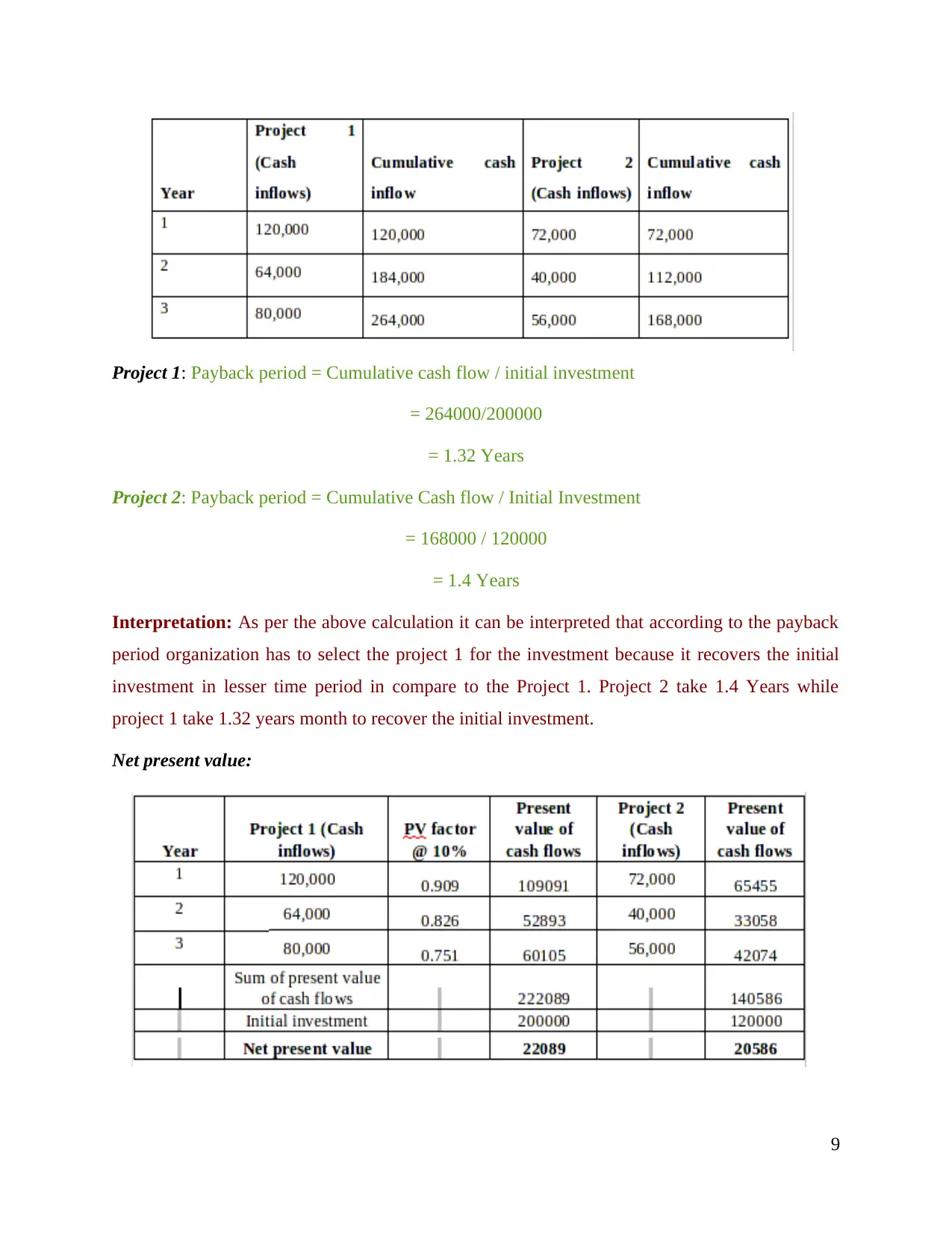

Project 1: Payback period = Cumulative cash flow / initial investment

= 264000/200000

= 1.32 Years

Project 2: Payback period = Cumulative Cash flow / Initial Investment

= 168000 / 120000

= 1.4 Years

Interpretation: As per the above calculation it can be interpreted that according to the payback

period organization has to select the project 1 for the investment because it recovers the initial

investment in lesser time period in compare to the Project 1. Project 2 take 1.4 Years while

project 1 take 1.32 years month to recover the initial investment.

Net present value:

9

= 264000/200000

= 1.32 Years

Project 2: Payback period = Cumulative Cash flow / Initial Investment

= 168000 / 120000

= 1.4 Years

Interpretation: As per the above calculation it can be interpreted that according to the payback

period organization has to select the project 1 for the investment because it recovers the initial

investment in lesser time period in compare to the Project 1. Project 2 take 1.4 Years while

project 1 take 1.32 years month to recover the initial investment.

Net present value:

9

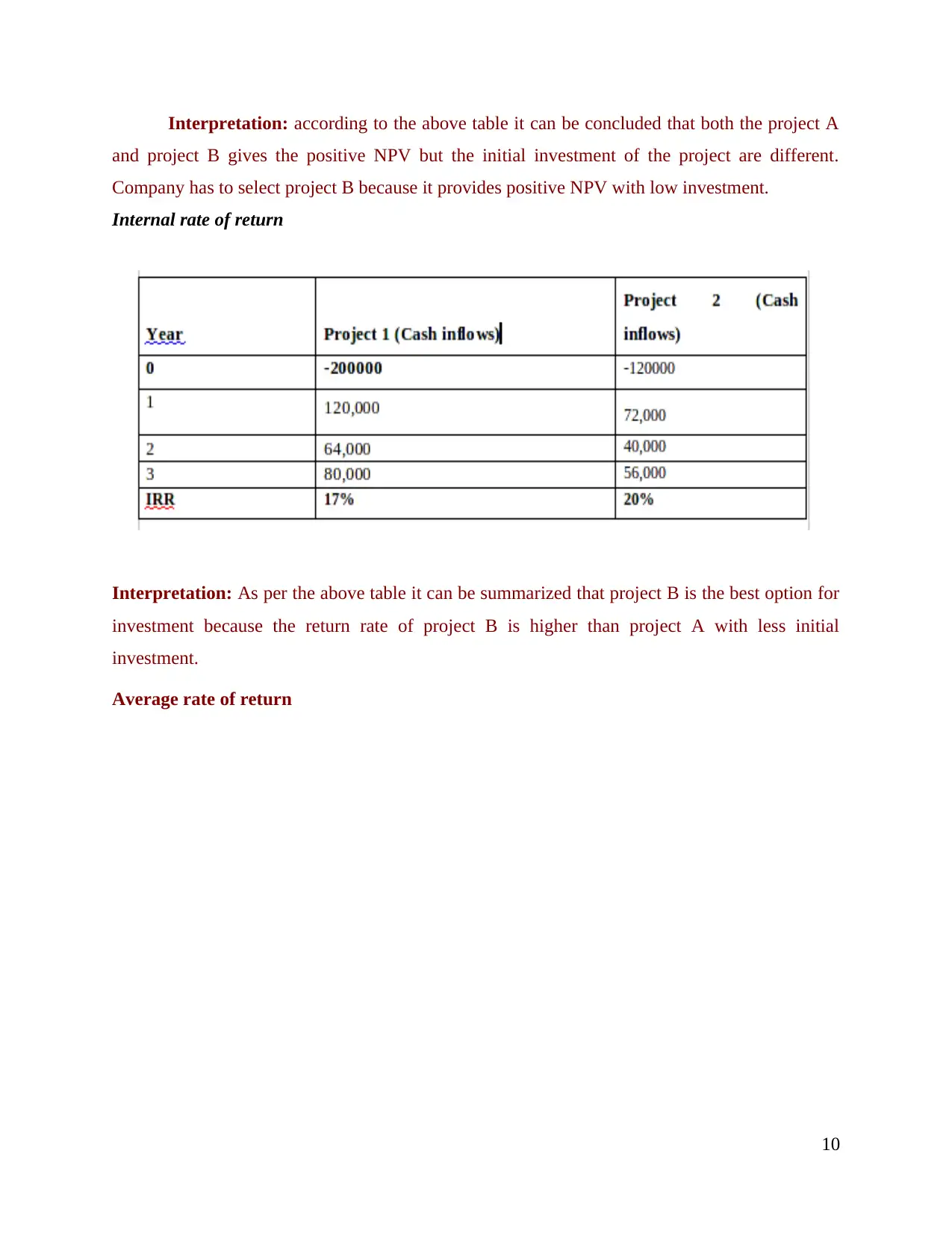

Interpretation: according to the above table it can be concluded that both the project A

and project B gives the positive NPV but the initial investment of the project are different.

Company has to select project B because it provides positive NPV with low investment.

Internal rate of return

Interpretation: As per the above table it can be summarized that project B is the best option for

investment because the return rate of project B is higher than project A with less initial

investment.

Average rate of return

10

and project B gives the positive NPV but the initial investment of the project are different.

Company has to select project B because it provides positive NPV with low investment.

Internal rate of return

Interpretation: As per the above table it can be summarized that project B is the best option for

investment because the return rate of project B is higher than project A with less initial

investment.

Average rate of return

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.