Advanced Financial Accounting Report: AASB Updates and Analysis

VerifiedAdded on 2020/02/24

|6

|871

|49

Report

AI Summary

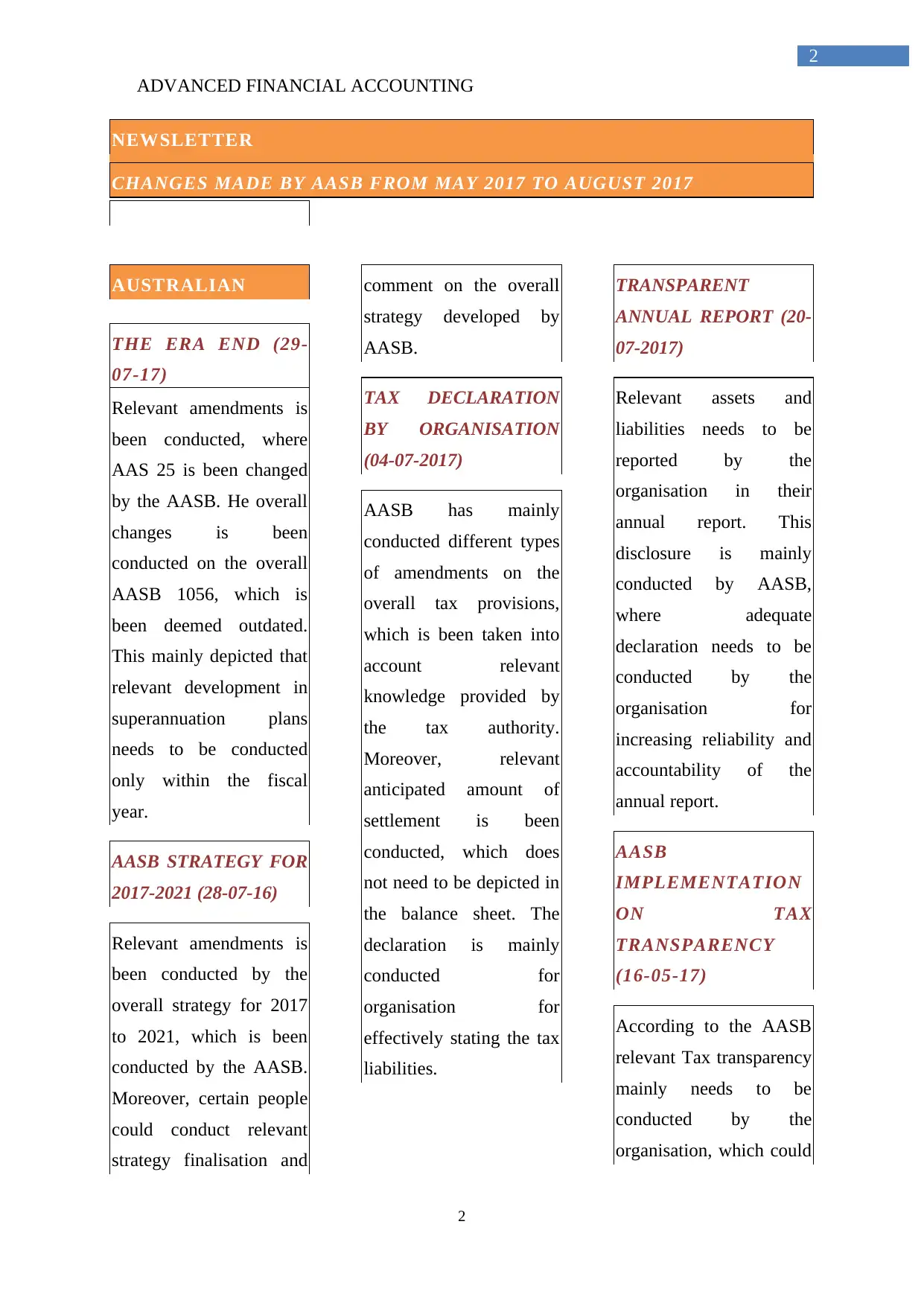

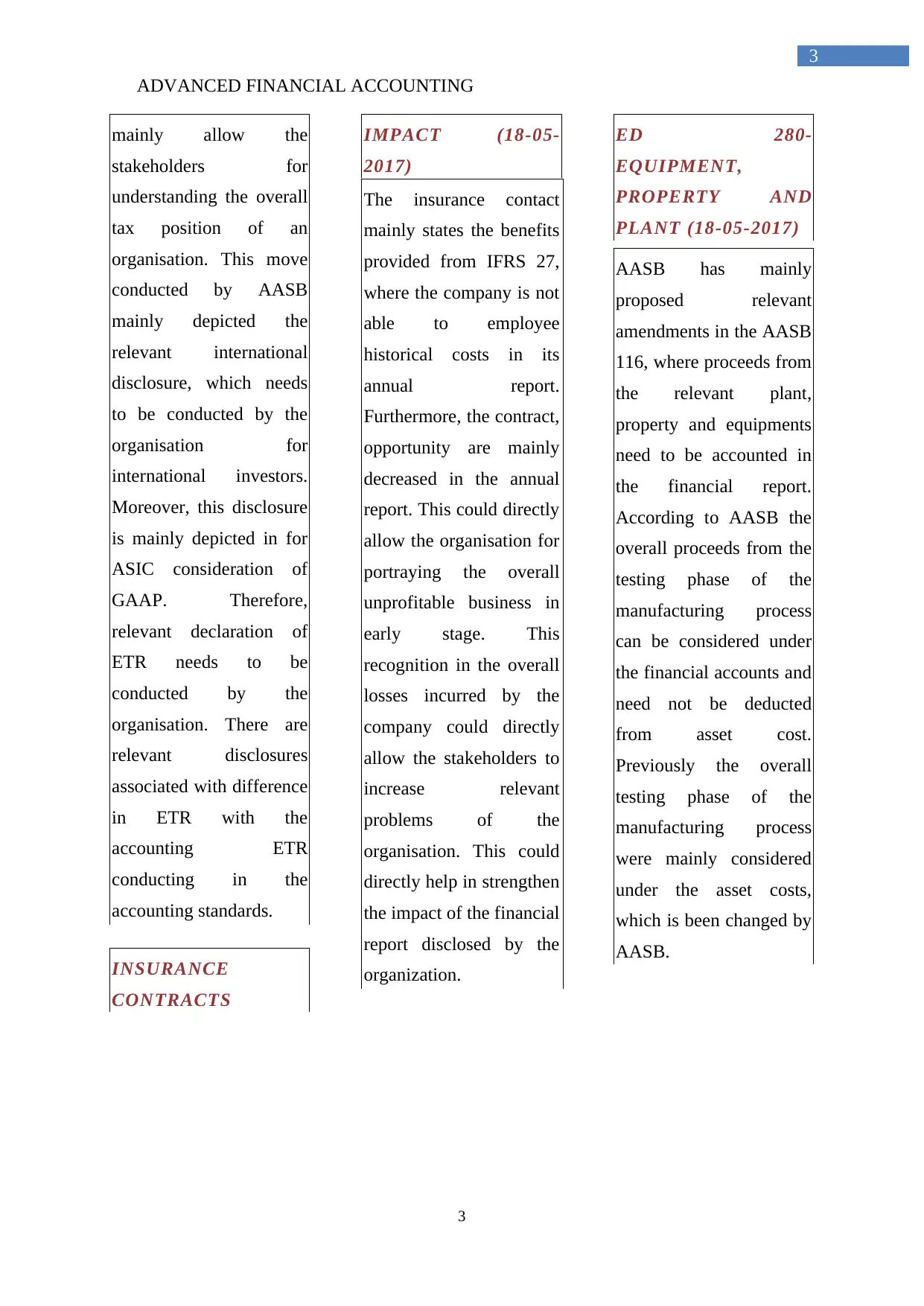

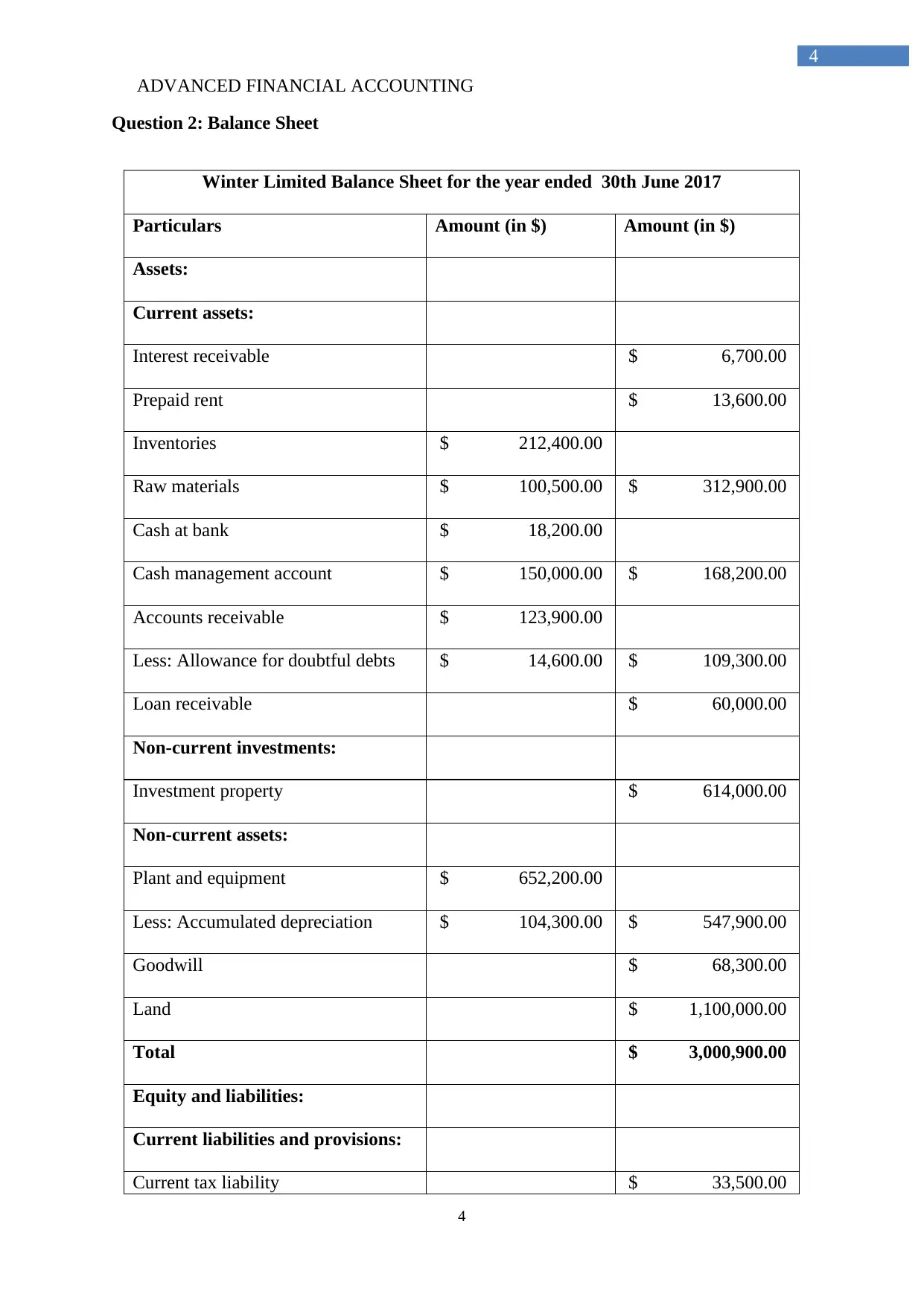

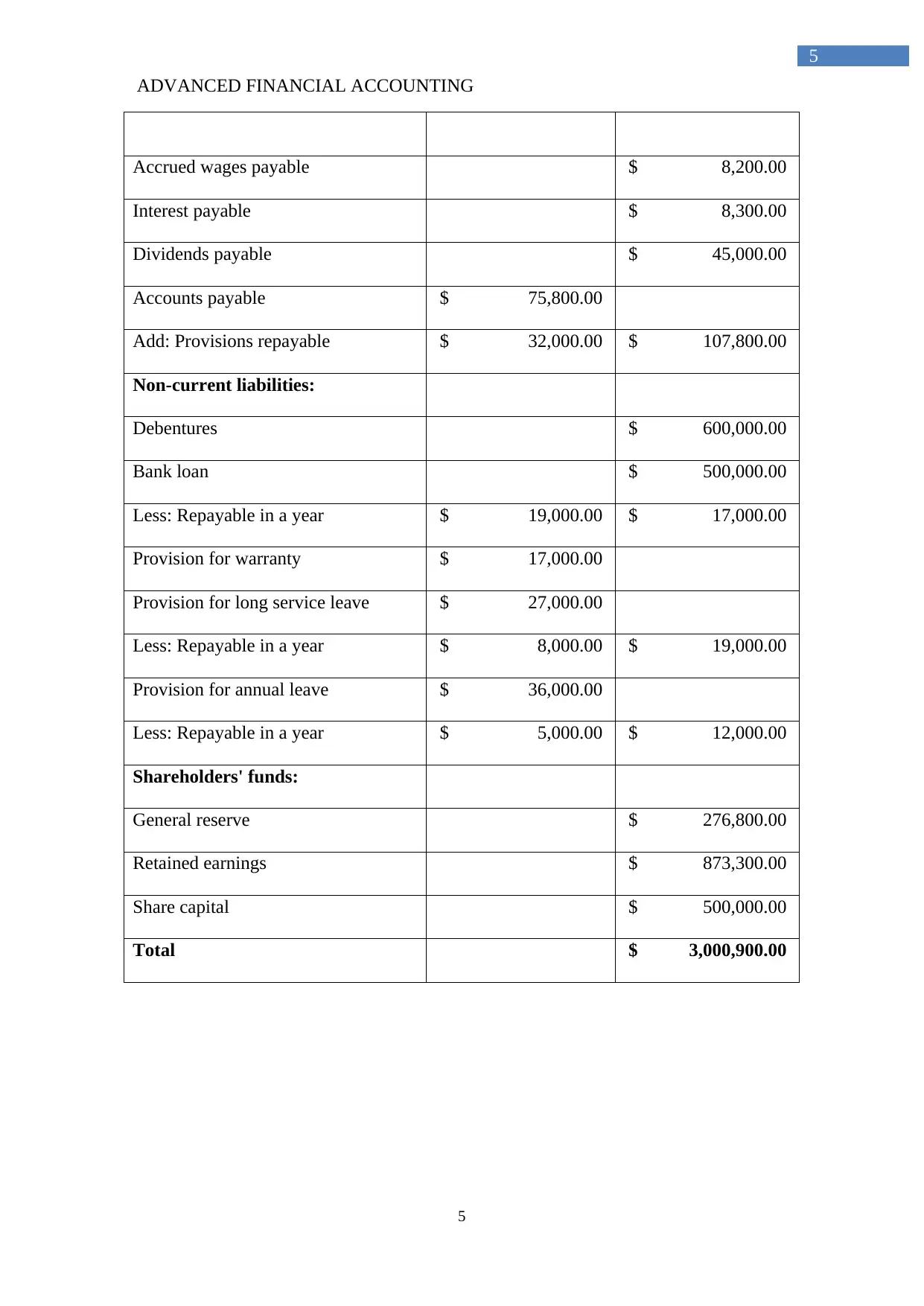

This report, created for an Advanced Financial Accounting course, examines amendments made by the Australian Accounting Standards Board (AASB) between May and August 2017. It details changes to standards like AAS 25 and AASB 1056, as well as the AASB's strategy for 2017-2021. The report also explores updates related to tax declarations, transparent annual reports, and the implementation of tax transparency. Furthermore, it analyzes the impact of insurance contracts and ED 280 on property, plant, and equipment. The second part of the report presents a detailed balance sheet for Winter Limited as of June 30, 2017, including assets, liabilities, and shareholders' equity. Finally, the report includes a bibliography of the sources used. This assignment provides a comprehensive overview of accounting standards and financial statement analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.