Management Accounting Report: Systems, Methods and Financial Issues

VerifiedAdded on 2020/10/05

|13

|3355

|216

Report

AI Summary

This report delves into the core principles of management accounting, providing a detailed analysis of various accounting systems and their applications within an organization. It explores different types of cost accounting systems, job costing systems, price optimization systems, inventory management systems, and management information systems, highlighting their significance in decision-making, cost control, and performance evaluation. The report also examines different reporting methods, including cost reports, budget reports, performance reports, and receivable reports, emphasizing their role in providing crucial financial information for internal and external stakeholders. Furthermore, it discusses various costing methods such as marginal costing, absorption costing, standard costing, historical costing, and activity-based costing, illustrating their application in determining production costs and enhancing profitability. The report also includes financial analysis and measure to resolve it

MANAGEMENT

ACOUNTING

1

ACOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

P1: Following various types of accounting system and their essential applications...................3

P2: Different types of accounting system use in reporting.........................................................4

P3: Different costing methods.....................................................................................................5

SECTION 2......................................................................................................................................9

Part 1...........................................................................................................................................9

P4: Merits and demerits of using planning tools in budgetary control.......................................9

Part 2.........................................................................................................................................11

P5: Various financial issues and measure to resolve it.............................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

P1: Following various types of accounting system and their essential applications...................3

P2: Different types of accounting system use in reporting.........................................................4

P3: Different costing methods.....................................................................................................5

SECTION 2......................................................................................................................................9

Part 1...........................................................................................................................................9

P4: Merits and demerits of using planning tools in budgetary control.......................................9

Part 2.........................................................................................................................................11

P5: Various financial issues and measure to resolve it.............................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

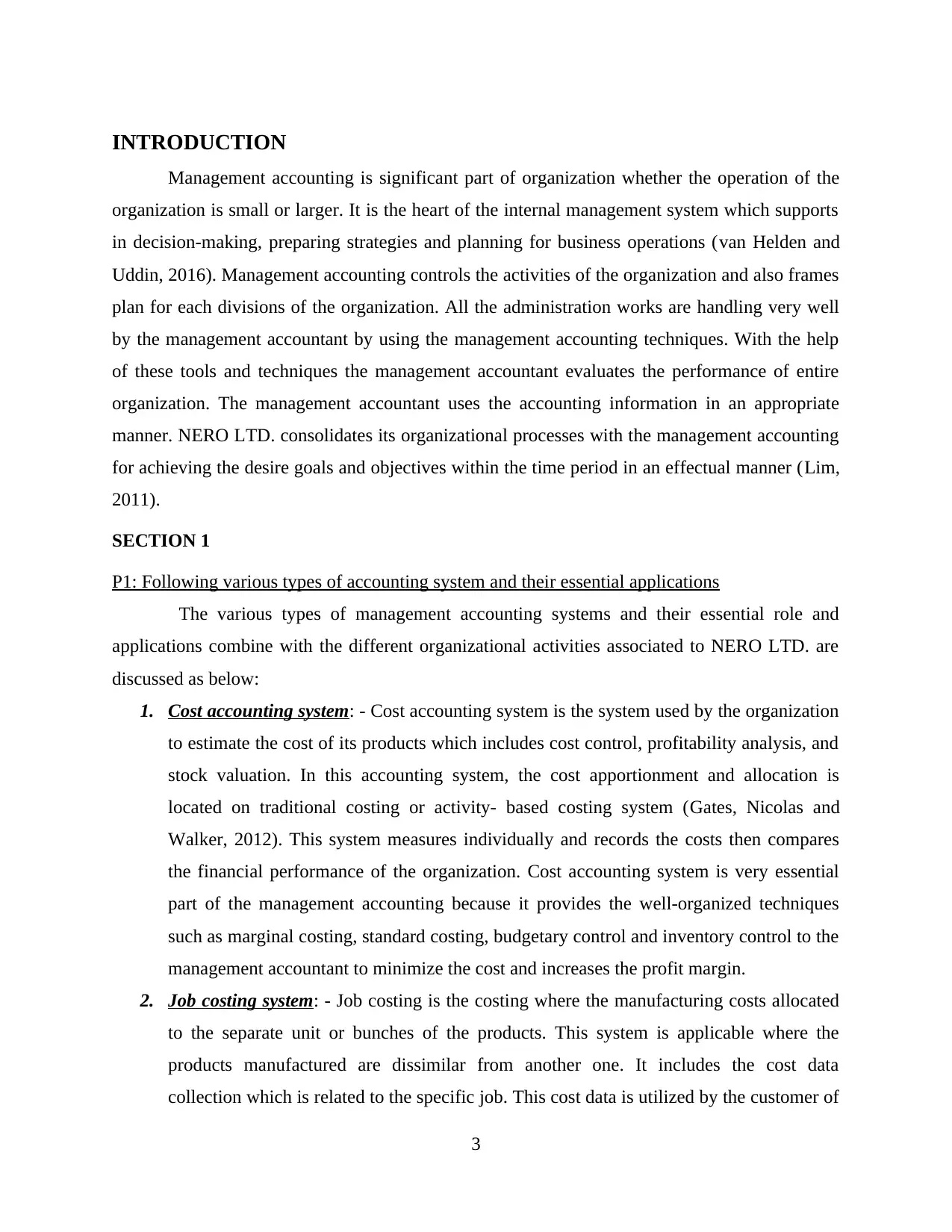

INTRODUCTION

Management accounting is significant part of organization whether the operation of the

organization is small or larger. It is the heart of the internal management system which supports

in decision-making, preparing strategies and planning for business operations (van Helden and

Uddin, 2016). Management accounting controls the activities of the organization and also frames

plan for each divisions of the organization. All the administration works are handling very well

by the management accountant by using the management accounting techniques. With the help

of these tools and techniques the management accountant evaluates the performance of entire

organization. The management accountant uses the accounting information in an appropriate

manner. NERO LTD. consolidates its organizational processes with the management accounting

for achieving the desire goals and objectives within the time period in an effectual manner (Lim,

2011).

SECTION 1

P1: Following various types of accounting system and their essential applications

The various types of management accounting systems and their essential role and

applications combine with the different organizational activities associated to NERO LTD. are

discussed as below:

1. Cost accounting system: - Cost accounting system is the system used by the organization

to estimate the cost of its products which includes cost control, profitability analysis, and

stock valuation. In this accounting system, the cost apportionment and allocation is

located on traditional costing or activity- based costing system (Gates, Nicolas and

Walker, 2012). This system measures individually and records the costs then compares

the financial performance of the organization. Cost accounting system is very essential

part of the management accounting because it provides the well-organized techniques

such as marginal costing, standard costing, budgetary control and inventory control to the

management accountant to minimize the cost and increases the profit margin.

2. Job costing system: - Job costing is the costing where the manufacturing costs allocated

to the separate unit or bunches of the products. This system is applicable where the

products manufactured are dissimilar from another one. It includes the cost data

collection which is related to the specific job. This cost data is utilized by the customer of

3

Management accounting is significant part of organization whether the operation of the

organization is small or larger. It is the heart of the internal management system which supports

in decision-making, preparing strategies and planning for business operations (van Helden and

Uddin, 2016). Management accounting controls the activities of the organization and also frames

plan for each divisions of the organization. All the administration works are handling very well

by the management accountant by using the management accounting techniques. With the help

of these tools and techniques the management accountant evaluates the performance of entire

organization. The management accountant uses the accounting information in an appropriate

manner. NERO LTD. consolidates its organizational processes with the management accounting

for achieving the desire goals and objectives within the time period in an effectual manner (Lim,

2011).

SECTION 1

P1: Following various types of accounting system and their essential applications

The various types of management accounting systems and their essential role and

applications combine with the different organizational activities associated to NERO LTD. are

discussed as below:

1. Cost accounting system: - Cost accounting system is the system used by the organization

to estimate the cost of its products which includes cost control, profitability analysis, and

stock valuation. In this accounting system, the cost apportionment and allocation is

located on traditional costing or activity- based costing system (Gates, Nicolas and

Walker, 2012). This system measures individually and records the costs then compares

the financial performance of the organization. Cost accounting system is very essential

part of the management accounting because it provides the well-organized techniques

such as marginal costing, standard costing, budgetary control and inventory control to the

management accountant to minimize the cost and increases the profit margin.

2. Job costing system: - Job costing is the costing where the manufacturing costs allocated

to the separate unit or bunches of the products. This system is applicable where the

products manufactured are dissimilar from another one. It includes the cost data

collection which is related to the specific job. This cost data is utilized by the customer of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

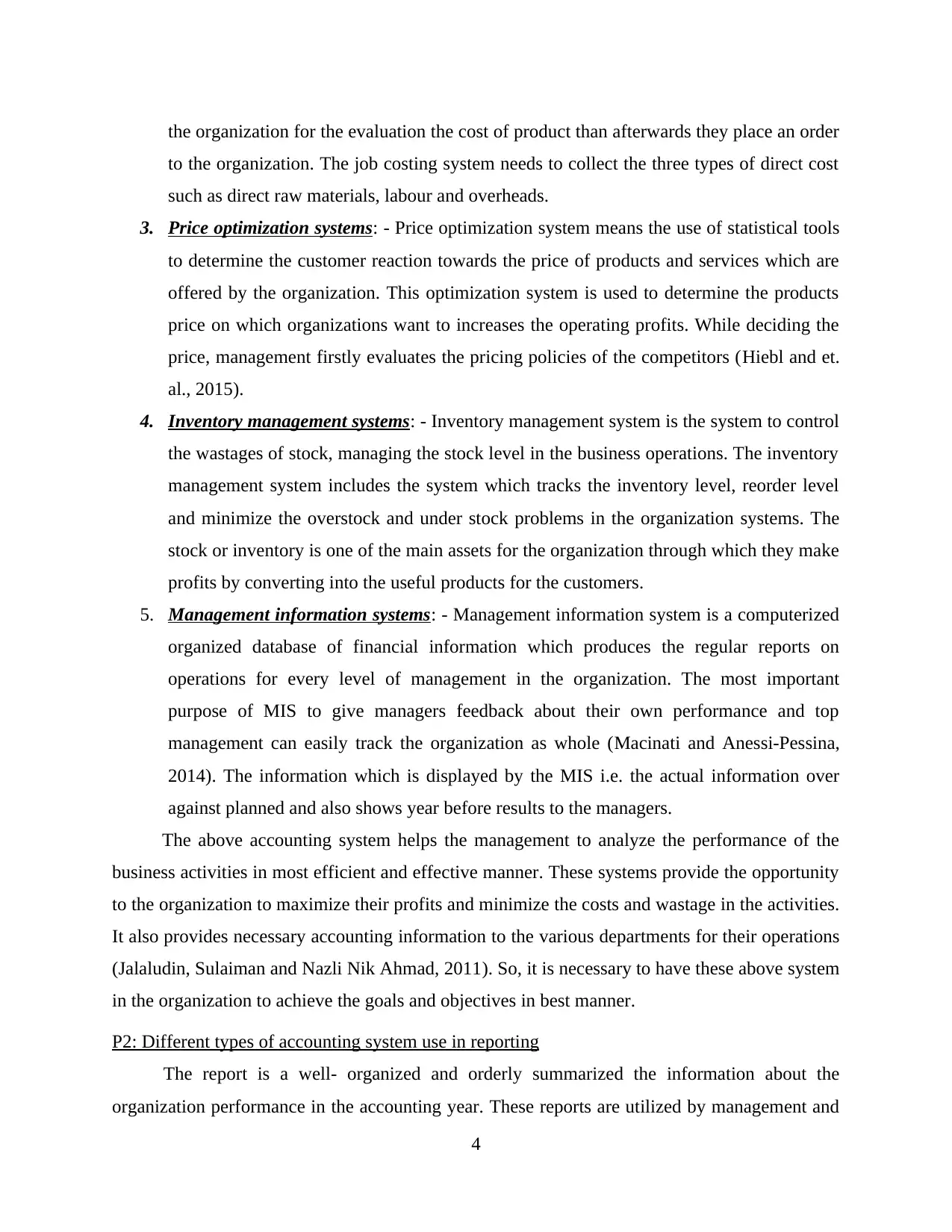

the organization for the evaluation the cost of product than afterwards they place an order

to the organization. The job costing system needs to collect the three types of direct cost

such as direct raw materials, labour and overheads.

3. Price optimization systems: - Price optimization system means the use of statistical tools

to determine the customer reaction towards the price of products and services which are

offered by the organization. This optimization system is used to determine the products

price on which organizations want to increases the operating profits. While deciding the

price, management firstly evaluates the pricing policies of the competitors (Hiebl and et.

al., 2015).

4. Inventory management systems: - Inventory management system is the system to control

the wastages of stock, managing the stock level in the business operations. The inventory

management system includes the system which tracks the inventory level, reorder level

and minimize the overstock and under stock problems in the organization systems. The

stock or inventory is one of the main assets for the organization through which they make

profits by converting into the useful products for the customers.

5. Management information systems: - Management information system is a computerized

organized database of financial information which produces the regular reports on

operations for every level of management in the organization. The most important

purpose of MIS to give managers feedback about their own performance and top

management can easily track the organization as whole (Macinati and Anessi-Pessina,

2014). The information which is displayed by the MIS i.e. the actual information over

against planned and also shows year before results to the managers.

The above accounting system helps the management to analyze the performance of the

business activities in most efficient and effective manner. These systems provide the opportunity

to the organization to maximize their profits and minimize the costs and wastage in the activities.

It also provides necessary accounting information to the various departments for their operations

(Jalaludin, Sulaiman and Nazli Nik Ahmad, 2011). So, it is necessary to have these above system

in the organization to achieve the goals and objectives in best manner.

P2: Different types of accounting system use in reporting

The report is a well- organized and orderly summarized the information about the

organization performance in the accounting year. These reports are utilized by management and

4

to the organization. The job costing system needs to collect the three types of direct cost

such as direct raw materials, labour and overheads.

3. Price optimization systems: - Price optimization system means the use of statistical tools

to determine the customer reaction towards the price of products and services which are

offered by the organization. This optimization system is used to determine the products

price on which organizations want to increases the operating profits. While deciding the

price, management firstly evaluates the pricing policies of the competitors (Hiebl and et.

al., 2015).

4. Inventory management systems: - Inventory management system is the system to control

the wastages of stock, managing the stock level in the business operations. The inventory

management system includes the system which tracks the inventory level, reorder level

and minimize the overstock and under stock problems in the organization systems. The

stock or inventory is one of the main assets for the organization through which they make

profits by converting into the useful products for the customers.

5. Management information systems: - Management information system is a computerized

organized database of financial information which produces the regular reports on

operations for every level of management in the organization. The most important

purpose of MIS to give managers feedback about their own performance and top

management can easily track the organization as whole (Macinati and Anessi-Pessina,

2014). The information which is displayed by the MIS i.e. the actual information over

against planned and also shows year before results to the managers.

The above accounting system helps the management to analyze the performance of the

business activities in most efficient and effective manner. These systems provide the opportunity

to the organization to maximize their profits and minimize the costs and wastage in the activities.

It also provides necessary accounting information to the various departments for their operations

(Jalaludin, Sulaiman and Nazli Nik Ahmad, 2011). So, it is necessary to have these above system

in the organization to achieve the goals and objectives in best manner.

P2: Different types of accounting system use in reporting

The report is a well- organized and orderly summarized the information about the

organization performance in the accounting year. These reports are utilized by management and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

externals for their own decisions in regards to the company. NERO LTD. uses this reporting

system to record all the important events related to the company’s performance. These reports

are prepared by the management at the end of the year and evaluate the entire performance of the

organization.

The various different types of reports prepared by the management and their advantages

are discussed below:

1. Costs reports: - The report allows to the management accountant to view the cost value

of products vs. selling price. It helps the management accountant to control the costs and

plans for profitability of the products. Cost reports include the raw materials, overhead,

labour costs of the manufactured product. These reports are shown to the top

management for the further decisions related to the business activities.

2. Budget reports: - The budgets are most important components of the management

accounting because it assists the management in future forecasting. The budgets are

prepared with the help of past data and estimate the future requirements (Zang, 2011).

Each budget is assigned to each department of the organization through which they

achieve their targets on the time.

3. Performance reports: - Performance reports assists the manager to apply the budgets to

measures the actual income and expenses to the budgeted figures. The difference in

between both is measured by the manager when they are preparing for the new budgets.

All the positive and negative aspects are recorded in this report for the further use. These

reports are prepared by the managers on yearly basis.

4. Receivable reports: - Receivable reports show all the receivables to the organization. It

includes all credit sales, debtors, and bill receivables. This report shows that how much

amount is due and paid by the customers of the organization. Receivable reports also

states that how much debtors are become bad- debts for the organization (Amoako,

2013 ). These reports also help the management to maintain the liquidity for the business

activities.

P3: Different costing methods

Cost accounting is an accounting method that main focus to capture a business cost of

production by evaluating the input costs of each step of production (Vakalfotis, Ballantine and

Wall, 2013). While cost accounting is usually used in the organization in various decisions-

5

system to record all the important events related to the company’s performance. These reports

are prepared by the management at the end of the year and evaluate the entire performance of the

organization.

The various different types of reports prepared by the management and their advantages

are discussed below:

1. Costs reports: - The report allows to the management accountant to view the cost value

of products vs. selling price. It helps the management accountant to control the costs and

plans for profitability of the products. Cost reports include the raw materials, overhead,

labour costs of the manufactured product. These reports are shown to the top

management for the further decisions related to the business activities.

2. Budget reports: - The budgets are most important components of the management

accounting because it assists the management in future forecasting. The budgets are

prepared with the help of past data and estimate the future requirements (Zang, 2011).

Each budget is assigned to each department of the organization through which they

achieve their targets on the time.

3. Performance reports: - Performance reports assists the manager to apply the budgets to

measures the actual income and expenses to the budgeted figures. The difference in

between both is measured by the manager when they are preparing for the new budgets.

All the positive and negative aspects are recorded in this report for the further use. These

reports are prepared by the managers on yearly basis.

4. Receivable reports: - Receivable reports show all the receivables to the organization. It

includes all credit sales, debtors, and bill receivables. This report shows that how much

amount is due and paid by the customers of the organization. Receivable reports also

states that how much debtors are become bad- debts for the organization (Amoako,

2013 ). These reports also help the management to maintain the liquidity for the business

activities.

P3: Different costing methods

Cost accounting is an accounting method that main focus to capture a business cost of

production by evaluating the input costs of each step of production (Vakalfotis, Ballantine and

Wall, 2013). While cost accounting is usually used in the organization in various decisions-

5

making processes. Cost accounting is the most important tool for management in budgeting, and

also in preparing the cost control plans which enhances the net operating profits for the

organization.

Following there are different types of costing: Marginal costing: In this costing, only the variable costs are allocated or assigned i.e.

direct materials, labor, expenses and variable overheads to the production. It does not

include the fixed cost of production. Absorption costing: In this costing, the fixed and variable costs are absorbed to

production. The cost includes here are direct materials, labor, expenses, and fixed and

variable overheads. In the absorption costing, a portion of the fixed overhead cost is

assigned to each unit of production. Standard costing: In this costing, the costs are predetermined in advance for the product.

When the standard cost is used to control the cost it is known as standard costing

(McGraw-Hill.Soin and Collier, 2013). Standard cost is the estimated cost for the raw

materials, labor, and overhead for a particular time period. In standard costing, the

variances are incurred in between the actual and standard cost and accordingly the

manager takes the corrective action to maximize the production. Historical costing: In this costing, the costs are determined in terms of actual costs and

not the estimated standard costs. In this method costs are determined only after it is

incurred. Mostly the organizations follow this costing method because it is easy to

evaluate the cost and take on the spot measurement.

Activity- based costing: The ABC system firstly collects the overhead cost for each

business activity and then assigns the costs of the activities to the products i.e. cost

objects of that activity (Bodie, 2013). In other words, activity- based costing allocates the

all direct and indirect costs to the cost objects. ABC is a crucial tool for making strategic

decisions, as it allows the manager to prepare the picture of exact profitability of product

lines, distribution channels, customer segments, etc.

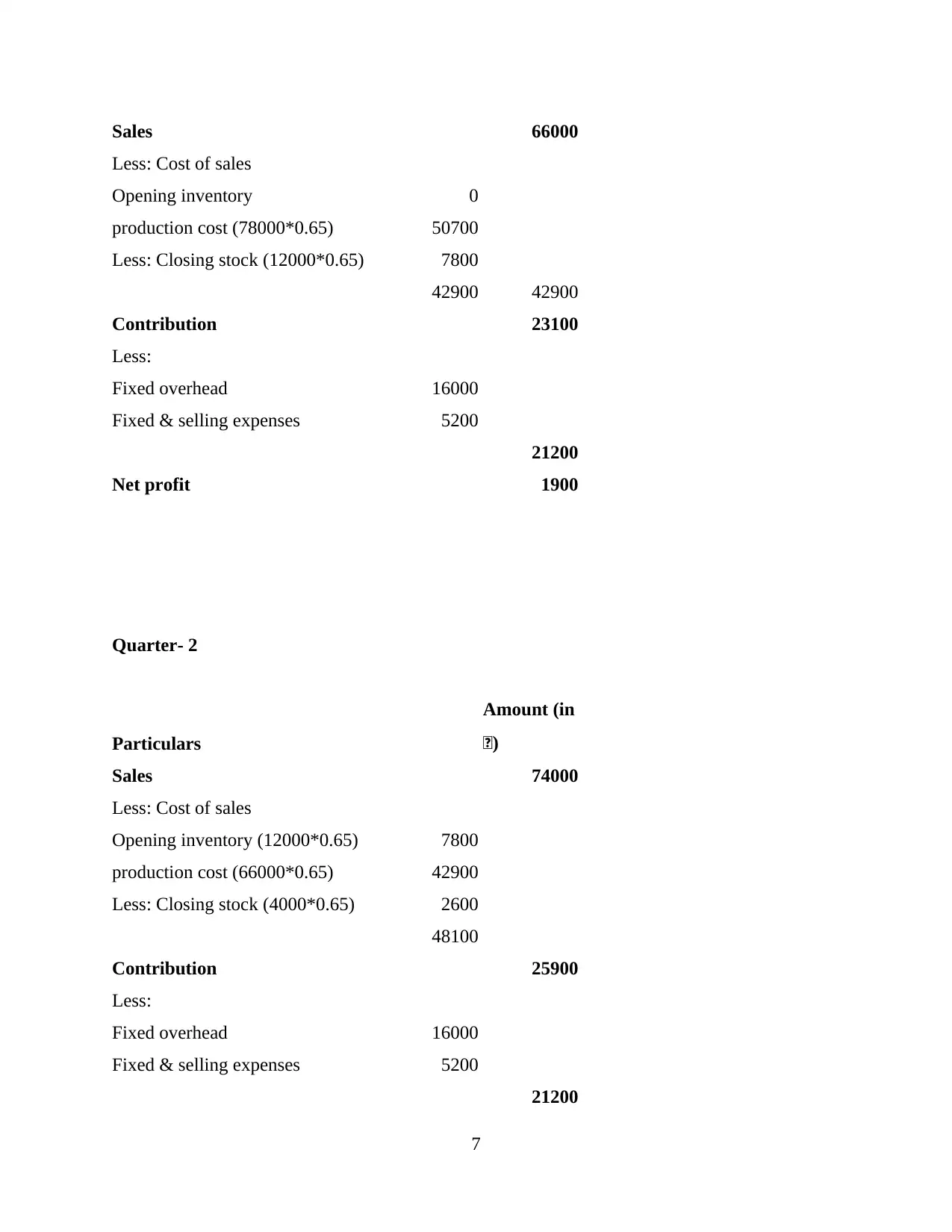

Quarter 1

Particulars

Amount (in

£)

6

also in preparing the cost control plans which enhances the net operating profits for the

organization.

Following there are different types of costing: Marginal costing: In this costing, only the variable costs are allocated or assigned i.e.

direct materials, labor, expenses and variable overheads to the production. It does not

include the fixed cost of production. Absorption costing: In this costing, the fixed and variable costs are absorbed to

production. The cost includes here are direct materials, labor, expenses, and fixed and

variable overheads. In the absorption costing, a portion of the fixed overhead cost is

assigned to each unit of production. Standard costing: In this costing, the costs are predetermined in advance for the product.

When the standard cost is used to control the cost it is known as standard costing

(McGraw-Hill.Soin and Collier, 2013). Standard cost is the estimated cost for the raw

materials, labor, and overhead for a particular time period. In standard costing, the

variances are incurred in between the actual and standard cost and accordingly the

manager takes the corrective action to maximize the production. Historical costing: In this costing, the costs are determined in terms of actual costs and

not the estimated standard costs. In this method costs are determined only after it is

incurred. Mostly the organizations follow this costing method because it is easy to

evaluate the cost and take on the spot measurement.

Activity- based costing: The ABC system firstly collects the overhead cost for each

business activity and then assigns the costs of the activities to the products i.e. cost

objects of that activity (Bodie, 2013). In other words, activity- based costing allocates the

all direct and indirect costs to the cost objects. ABC is a crucial tool for making strategic

decisions, as it allows the manager to prepare the picture of exact profitability of product

lines, distribution channels, customer segments, etc.

Quarter 1

Particulars

Amount (in

£)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

Quarter- 2

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

7

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

Quarter- 2

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

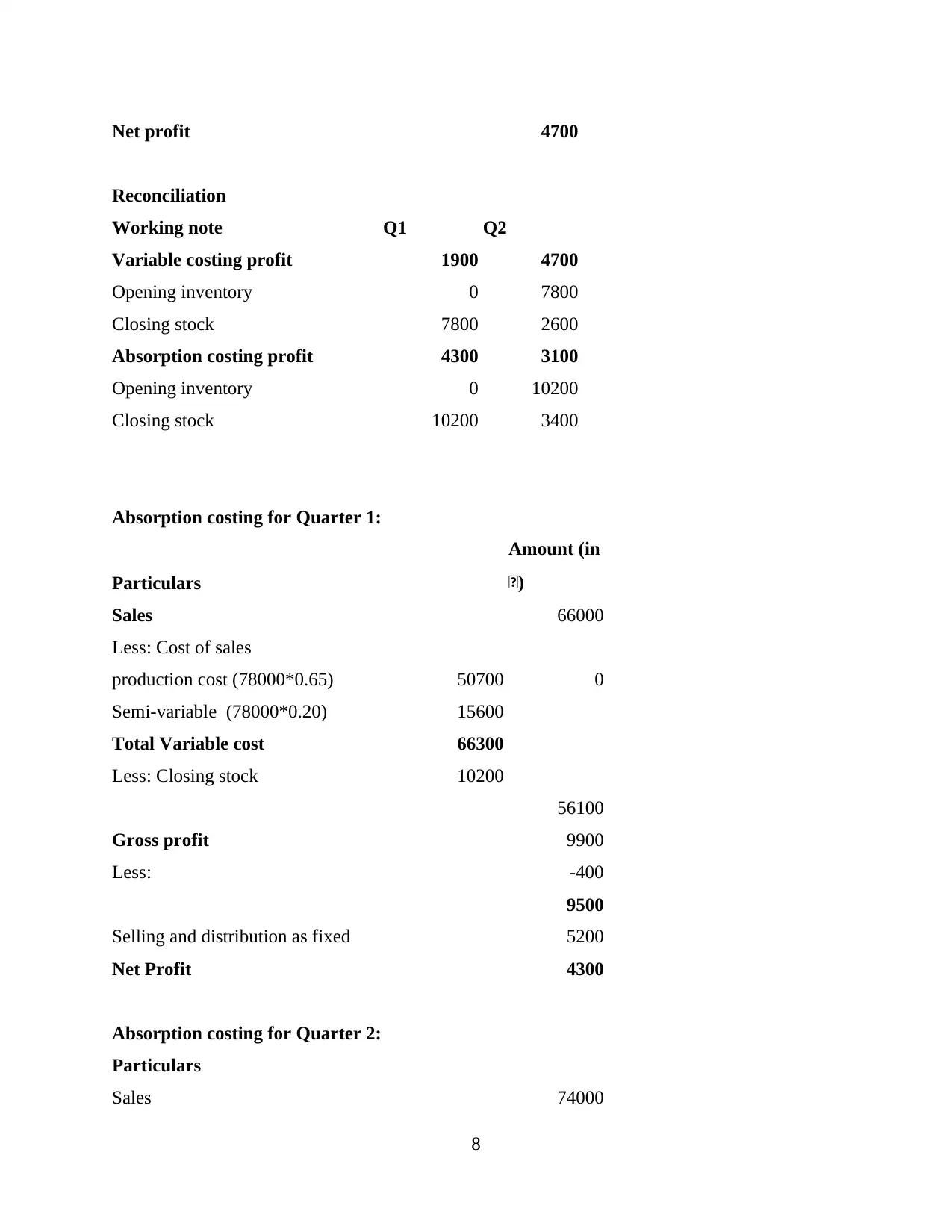

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

8

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

8

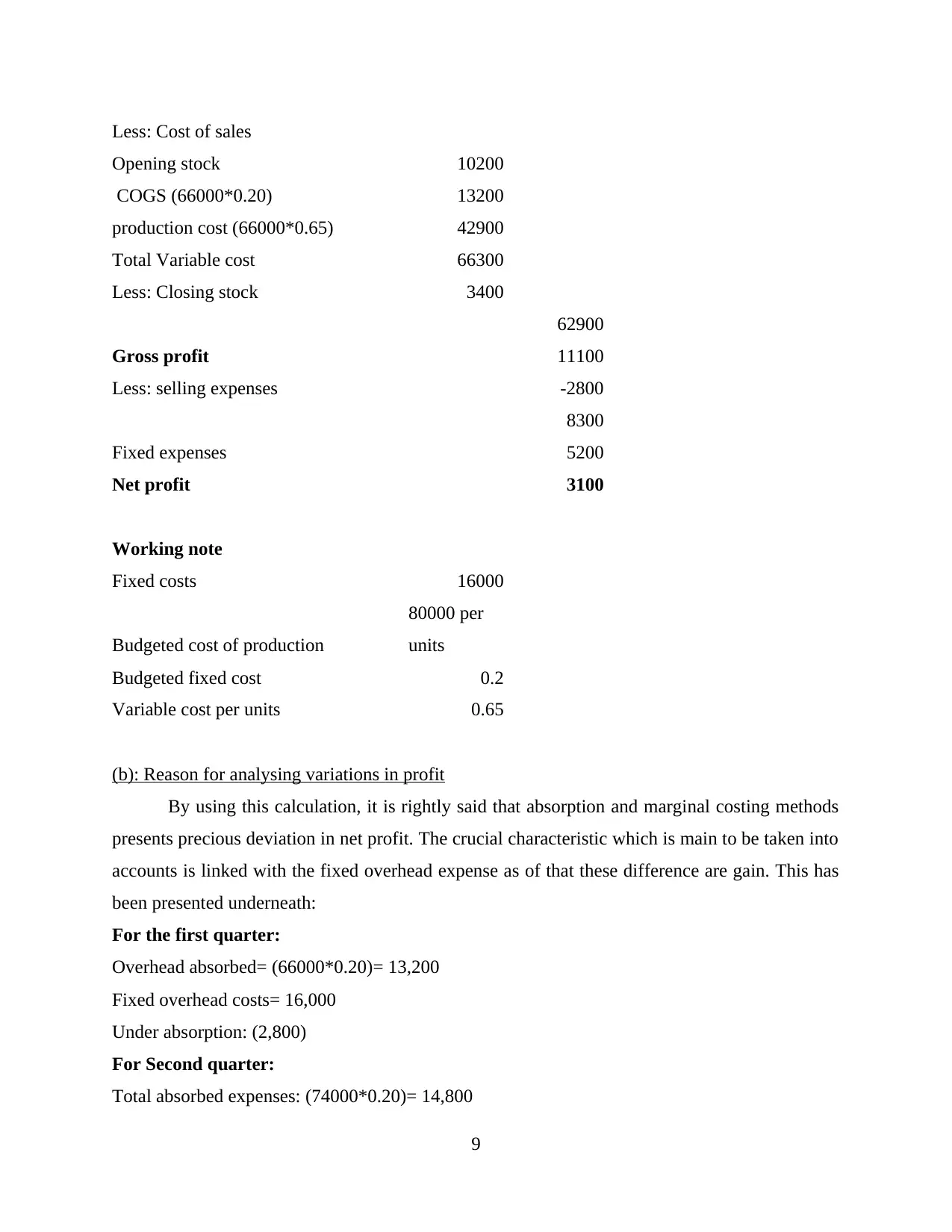

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

(b): Reason for analysing variations in profit

By using this calculation, it is rightly said that absorption and marginal costing methods

presents precious deviation in net profit. The crucial characteristic which is main to be taken into

accounts is linked with the fixed overhead expense as of that these difference are gain. This has

been presented underneath:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

9

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

(b): Reason for analysing variations in profit

By using this calculation, it is rightly said that absorption and marginal costing methods

presents precious deviation in net profit. The crucial characteristic which is main to be taken into

accounts is linked with the fixed overhead expense as of that these difference are gain. This has

been presented underneath:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

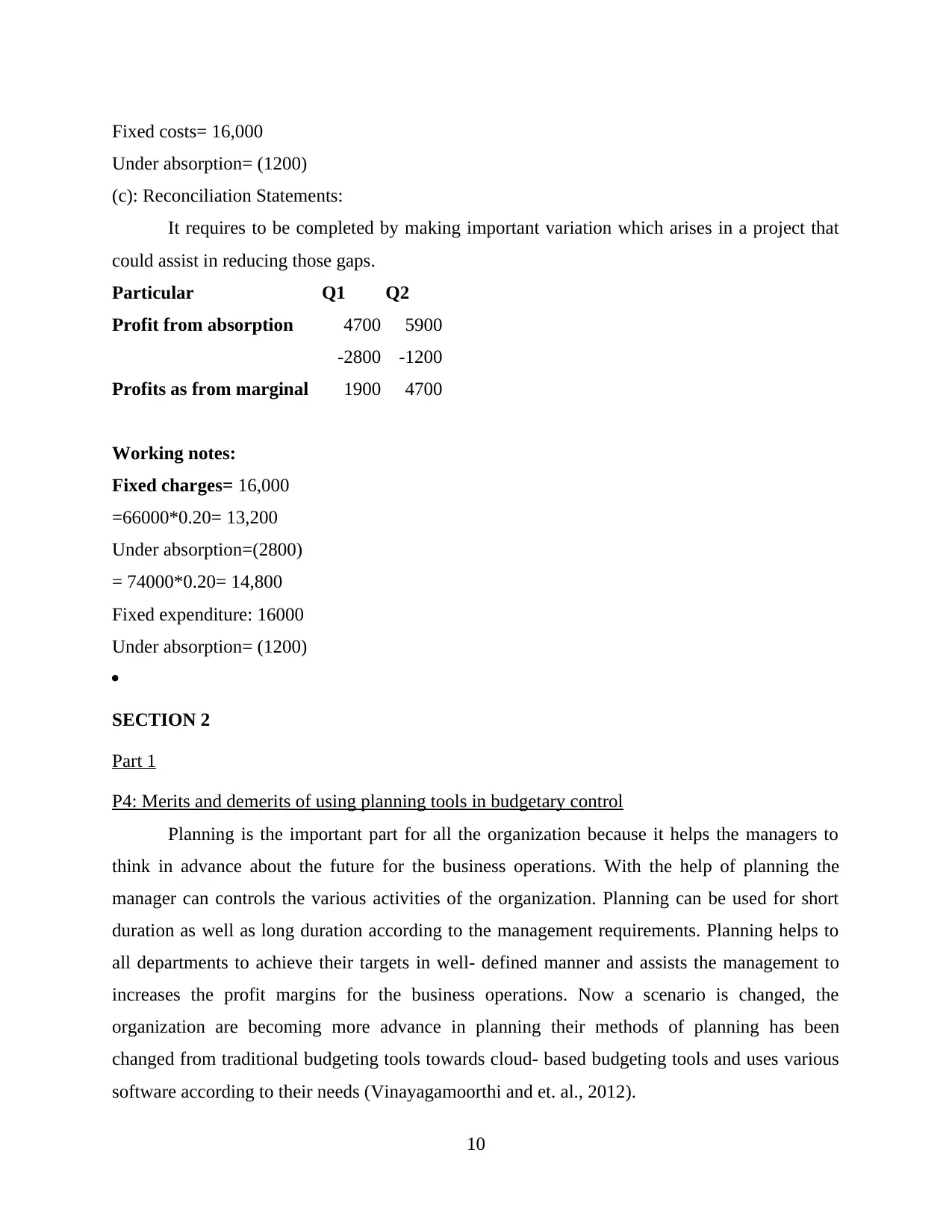

Fixed costs= 16,000

Under absorption= (1200)

(c): Reconciliation Statements:

It requires to be completed by making important variation which arises in a project that

could assist in reducing those gaps.

Particular Q1 Q2

Profit from absorption 4700 5900

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

SECTION 2

Part 1

P4: Merits and demerits of using planning tools in budgetary control

Planning is the important part for all the organization because it helps the managers to

think in advance about the future for the business operations. With the help of planning the

manager can controls the various activities of the organization. Planning can be used for short

duration as well as long duration according to the management requirements. Planning helps to

all departments to achieve their targets in well- defined manner and assists the management to

increases the profit margins for the business operations. Now a scenario is changed, the

organization are becoming more advance in planning their methods of planning has been

changed from traditional budgeting tools towards cloud- based budgeting tools and uses various

software according to their needs (Vinayagamoorthi and et. al., 2012).

10

Under absorption= (1200)

(c): Reconciliation Statements:

It requires to be completed by making important variation which arises in a project that

could assist in reducing those gaps.

Particular Q1 Q2

Profit from absorption 4700 5900

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

SECTION 2

Part 1

P4: Merits and demerits of using planning tools in budgetary control

Planning is the important part for all the organization because it helps the managers to

think in advance about the future for the business operations. With the help of planning the

manager can controls the various activities of the organization. Planning can be used for short

duration as well as long duration according to the management requirements. Planning helps to

all departments to achieve their targets in well- defined manner and assists the management to

increases the profit margins for the business operations. Now a scenario is changed, the

organization are becoming more advance in planning their methods of planning has been

changed from traditional budgeting tools towards cloud- based budgeting tools and uses various

software according to their needs (Vinayagamoorthi and et. al., 2012).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different planning tools and their application which is used in preparation of projected

future budgets are explained below:

Prediction or forecasting tools: This tool is very effective tool for the management in

which future projections are made with the help of past data (Lukka and Vinnari, 2014). While

preparing the budgets the past and current trends are analysed by the manager in deeply manner

so that their in mistake incur in the future.

Merits

It helps the management to prepare the future forecast budget in very well- manner.

This tool helps in preparing the all types of budget.

Demerits

It creates very difficult to predict for future because future prediction is not very easy and

change rapidly. It incurred cost for the organization.

Contingency tools: Another important aspect in preparation of the budgets is contingency

or future event which affects the budgets. While preparing the budgets the manager evaluates the

total uncertainty which affects the organizational profitability index. To fix this problem, the

manager prepares the strategies for the contingencies and enormously estimates and evaluates the

risk creating factors which affects the future budgets.

Merits

It helps the manager to eliminate the risk factors for the future budgets.

It also assists the manager to take the important decisions for the organization.

Demerits

It is a time consuming process because it requires deeply study of risk creating factors. It is also takes time to prepare it.

Systematic planning: It is also known as scenario planning which is the technique of the

planning. This planning is makes the assumptions about the future and how the business

environment will change in the future which affects the business operations of the organization

(Wickramasinghe and Alawattage, 2012). In other words, the systematic or scenario planning

helps to the manager to identify a particular set of uncertainties and different realities which

might happen in the future of the organization business activities.

Merits

11

future budgets are explained below:

Prediction or forecasting tools: This tool is very effective tool for the management in

which future projections are made with the help of past data (Lukka and Vinnari, 2014). While

preparing the budgets the past and current trends are analysed by the manager in deeply manner

so that their in mistake incur in the future.

Merits

It helps the management to prepare the future forecast budget in very well- manner.

This tool helps in preparing the all types of budget.

Demerits

It creates very difficult to predict for future because future prediction is not very easy and

change rapidly. It incurred cost for the organization.

Contingency tools: Another important aspect in preparation of the budgets is contingency

or future event which affects the budgets. While preparing the budgets the manager evaluates the

total uncertainty which affects the organizational profitability index. To fix this problem, the

manager prepares the strategies for the contingencies and enormously estimates and evaluates the

risk creating factors which affects the future budgets.

Merits

It helps the manager to eliminate the risk factors for the future budgets.

It also assists the manager to take the important decisions for the organization.

Demerits

It is a time consuming process because it requires deeply study of risk creating factors. It is also takes time to prepare it.

Systematic planning: It is also known as scenario planning which is the technique of the

planning. This planning is makes the assumptions about the future and how the business

environment will change in the future which affects the business operations of the organization

(Wickramasinghe and Alawattage, 2012). In other words, the systematic or scenario planning

helps to the manager to identify a particular set of uncertainties and different realities which

might happen in the future of the organization business activities.

Merits

11

It assists the manager to plan for future uncertainty and accordingly they take decision for

it.

It is the most important method for evaluating the future uncertainty.

Demerits

Correct future prediction is very difficult for the manager of the organization because it

changes every minute of time.

It creates so many issues when the manager estimates for the future.

Part 2

P5: Various financial issues and measure to resolve it

It is very important for all the organization to prepare the plan and policies for the

business activities according to their requirements. It increases the productivity of the business

when it creates plans according to it. Financial issues come when the plans are not matched with

the business activities and it incurred further cost for the organization (Hilton and Platt, 2013).

The issues may be come from the external environment like change in the government policies,

tax rates, inflation rates, etc. which affects the business activities of the organization.

The management can use the following management accounting ways to react quickly to

financial issues of the organization:

Firstly, identify the financial issues by applying various management accounting techniques

and address them without any delays.

Secondly, the organization should interpret the financial governance and understand it and

analyze it. The financial governance monitors the financial issues and prevents it in most

effectual manner.

Thirdly and lastly, apply the management accounting techniques and tools set to prevent these

financial issues in the organization by applying these methods, the management of the company

can faces these problems in most appropriate manner.

CONCLUSION

From the above mentioned report, it is rightly said that by evaluating the management

accounting methods, it has been concluded that it is very effective and necessary technique for

the organization business processes. NERO LTD. earns lot of benefits while applying the

management accounting tools and techniques. By applying the various management accounting

12

it.

It is the most important method for evaluating the future uncertainty.

Demerits

Correct future prediction is very difficult for the manager of the organization because it

changes every minute of time.

It creates so many issues when the manager estimates for the future.

Part 2

P5: Various financial issues and measure to resolve it

It is very important for all the organization to prepare the plan and policies for the

business activities according to their requirements. It increases the productivity of the business

when it creates plans according to it. Financial issues come when the plans are not matched with

the business activities and it incurred further cost for the organization (Hilton and Platt, 2013).

The issues may be come from the external environment like change in the government policies,

tax rates, inflation rates, etc. which affects the business activities of the organization.

The management can use the following management accounting ways to react quickly to

financial issues of the organization:

Firstly, identify the financial issues by applying various management accounting techniques

and address them without any delays.

Secondly, the organization should interpret the financial governance and understand it and

analyze it. The financial governance monitors the financial issues and prevents it in most

effectual manner.

Thirdly and lastly, apply the management accounting techniques and tools set to prevent these

financial issues in the organization by applying these methods, the management of the company

can faces these problems in most appropriate manner.

CONCLUSION

From the above mentioned report, it is rightly said that by evaluating the management

accounting methods, it has been concluded that it is very effective and necessary technique for

the organization business processes. NERO LTD. earns lot of benefits while applying the

management accounting tools and techniques. By applying the various management accounting

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.