Financial Accounting Report: AGL Energy Expense Analysis

VerifiedAdded on 2020/05/16

|11

|1809

|191

Report

AI Summary

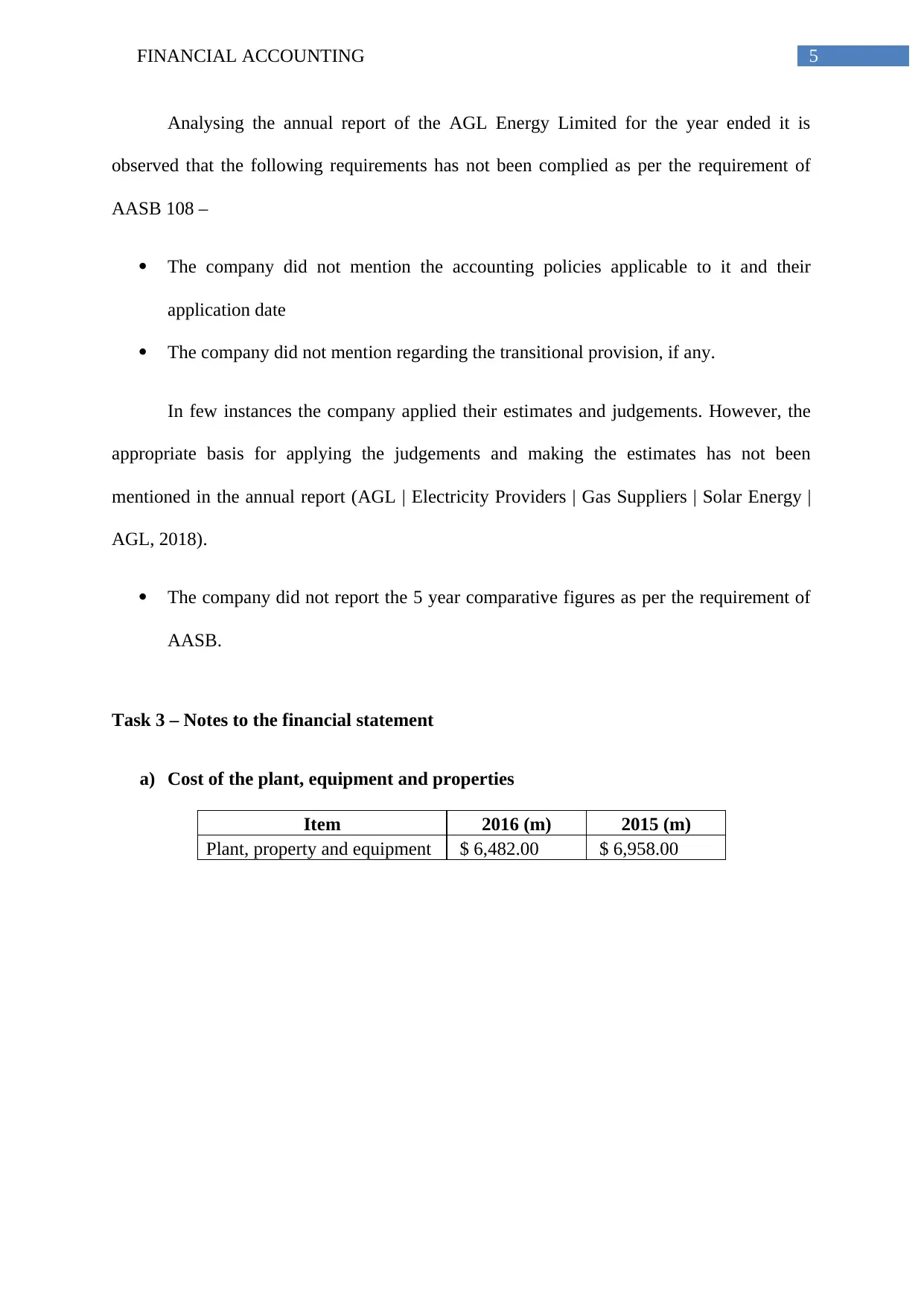

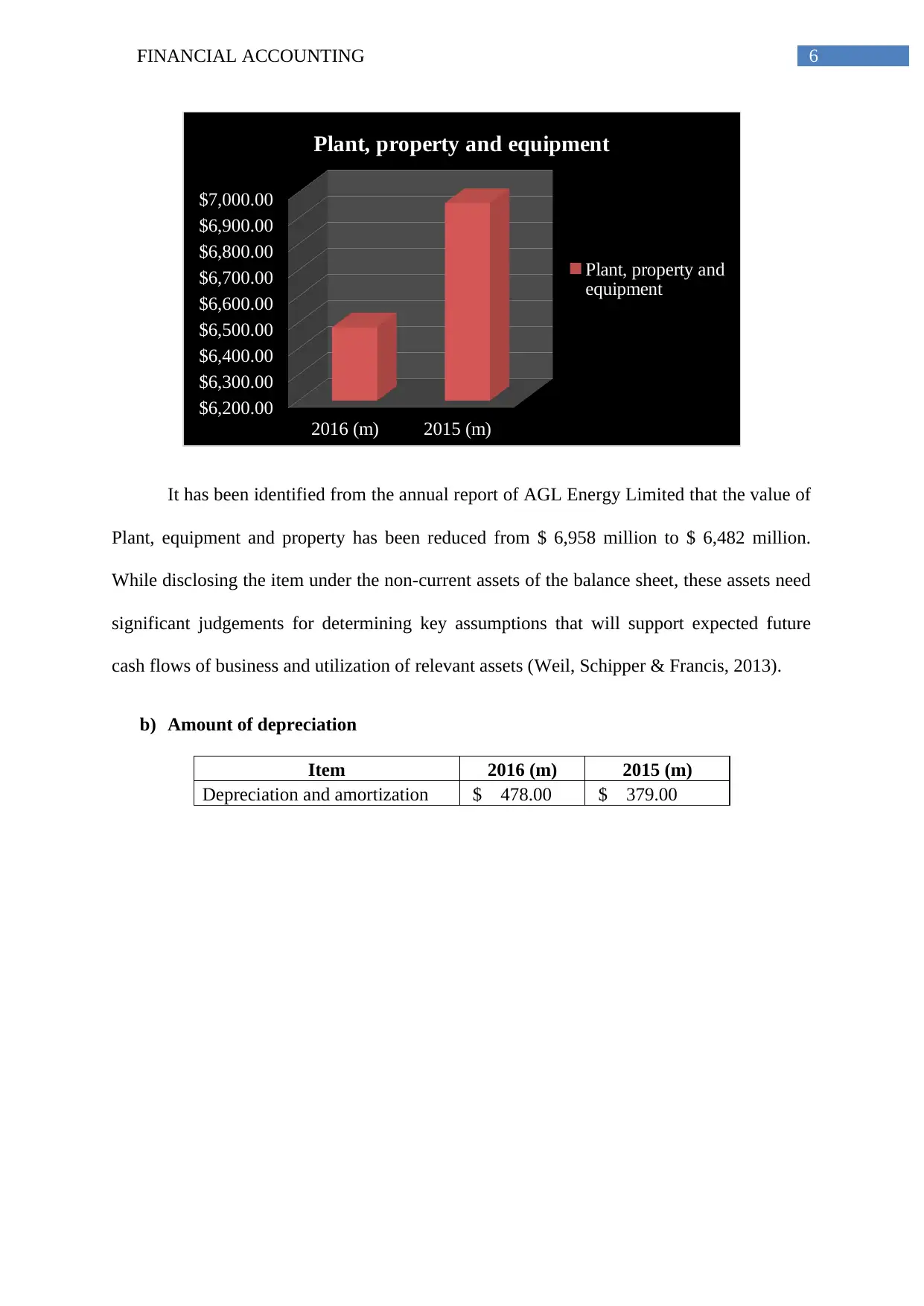

This report presents a financial accounting analysis, examining expense classification methods, accounting policies, and specific items from AGL Energy's financial statements. Task 1 delves into the classification of expenses by nature, comparing it to classification by function, and identifies the method used by AGL Energy. Task 2 focuses on accounting policies, particularly AASB 108, and highlights areas where AGL Energy's annual report might not fully comply. Task 3 examines the notes to the financial statements, including the cost of plant, equipment, and property, depreciation amounts and methods, depreciation periods, and impairment considerations. The report references relevant accounting standards and academic sources to support its analysis and findings, offering a detailed overview of AGL Energy's financial reporting practices. The report showcases the application of accounting principles to real-world financial data.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.