Financial Accounting Report: Principles, Regulations, and Concepts

VerifiedAdded on 2020/11/12

|27

|6999

|247

Report

AI Summary

This report provides a comprehensive overview of financial accounting, encompassing its purposes, regulations, and fundamental principles. It details the role of financial accounting in recording transactions, classifying data, and generating financial statements such as profit and loss accounts, balance sheets, and cash flow statements. The report examines key accounting rules, including those for personal, real, and nominal accounts, and highlights important accounting principles like the economic entity, monetary measurement, historical cost, full disclosure, and going concern. Furthermore, it explores the concepts of consistency and materiality disclosure, illustrating their significance in financial reporting. The report also includes practical examples, such as bank reconciliation statements and the use of suspense accounts, and provides financial statements for various clients, demonstrating the application of these principles. The appendix provides journal entries and ledger accounts to further illustrate the concepts discussed.

Finance Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

1.Financial Accounting and its purposes................................................................................1

2:Regulation related to finance...............................................................................................2

3: Accounting rules and principles.........................................................................................3

4 Convection and concept related to consistency and material disclosure.............................4

CLIENT 1........................................................................................................................................4

CLIENT 2........................................................................................................................................4

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 ..........4

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ................6

CLIENT 3........................................................................................................................................6

(a) Profit and loss account of Bowling Limited:....................................................................6

(b) Balance Sheet of Bowling Limited...................................................................................7

(c) Accounts concepts : Consistency and Prudence:..............................................................8

(d) Purpose of depreciation in formulating accounting statements and methods of

Depreciation:..........................................................................................................................8

CLIENT 4........................................................................................................................................9

(i) Bank reconciliation statement at 1st December 2017:......................................................9

(ii) Durrell Ltd's updated cash book for December 2017 :.....................................................9

(iii) Bank Reconciliation Statement as at 31"t December 2017:..........................................10

CLIENT 5......................................................................................................................................10

(a) Sales Ledger Control and Purchase Ledger Control Account:.......................................10

(b) Control Account:.............................................................................................................11

CLIENT 6......................................................................................................................................11

(a) Suspense Account:..........................................................................................................11

(b) Preparation of Trail Balance:..........................................................................................11

(c) Journal entries in order to show necessary corrections for eliminating suspense account

balance:.................................................................................................................................12

(d) Difference between a Suspense A/c and Clearing A/c:..................................................12

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

1.Financial Accounting and its purposes................................................................................1

2:Regulation related to finance...............................................................................................2

3: Accounting rules and principles.........................................................................................3

4 Convection and concept related to consistency and material disclosure.............................4

CLIENT 1........................................................................................................................................4

CLIENT 2........................................................................................................................................4

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018 ..........4

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018 ................6

CLIENT 3........................................................................................................................................6

(a) Profit and loss account of Bowling Limited:....................................................................6

(b) Balance Sheet of Bowling Limited...................................................................................7

(c) Accounts concepts : Consistency and Prudence:..............................................................8

(d) Purpose of depreciation in formulating accounting statements and methods of

Depreciation:..........................................................................................................................8

CLIENT 4........................................................................................................................................9

(i) Bank reconciliation statement at 1st December 2017:......................................................9

(ii) Durrell Ltd's updated cash book for December 2017 :.....................................................9

(iii) Bank Reconciliation Statement as at 31"t December 2017:..........................................10

CLIENT 5......................................................................................................................................10

(a) Sales Ledger Control and Purchase Ledger Control Account:.......................................10

(b) Control Account:.............................................................................................................11

CLIENT 6......................................................................................................................................11

(a) Suspense Account:..........................................................................................................11

(b) Preparation of Trail Balance:..........................................................................................11

(c) Journal entries in order to show necessary corrections for eliminating suspense account

balance:.................................................................................................................................12

(d) Difference between a Suspense A/c and Clearing A/c:..................................................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

APPENDIX....................................................................................................................................15

(a) Journal Entry in the books of David Study....................................................................15

(b) LEDGER ACCOUNTS..................................................................................................17

REFERENCES .............................................................................................................................14

APPENDIX....................................................................................................................................15

(a) Journal Entry in the books of David Study....................................................................15

(b) LEDGER ACCOUNTS..................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is field of accounting mainly concerned with recording of financial

transaction, classification of different transactions, reporting and analysis in order to know

performance and profitability of business organisation. Furthermore, it include financial

statement, profit and loss account, cash flow statements and other significant statements to know

true position of business organisation (Edwards, J. R., 2013). Main duty of accountant in a

business organisation is to record all financial transaction in journals, post them in ledger,

prepare trial balance and finally reporting through financial statements to present true and fair

view of financial statement. This report exhibits various aspects of financial accounting like

purpose of financial accounting, regulations relating to financial accounting, accounting rules

and principles and explanation about convections and concepts relating to consistency and

material disclosure. This report also covers bank reconciliation statement, process of preparing

bank reconciliation statement and, suspense account and its importance.

BUSINESS REPORT

1.Financial Accounting and its purposes

Financial accounting refers to set of activities related to preparation of final accounts of

a business organisation in order to access and provide information about actual performance and

financial position to internal and external users of financial accounting such as employees,

investors, lenders and creditors, suppliers, government, customers and other regulatory bodies.

Such final accounts are prepared by business organisations while considering various accounting

policies, guidelines, rules and regulations (Hale, 2012). A Business organisation prepare

financial accounting which mainly includes statement of financial position, profit and loss

account or income statement, statement for change in equity and cash flow statement.

Purpose of Financial statement

Financial statement shows financial details of company like profit earned, assets, retained

earnings for both internal and external user who so ever are interested in financial

statements of company.

Financial accounting is field of accounting mainly concerned with recording of financial

transaction, classification of different transactions, reporting and analysis in order to know

performance and profitability of business organisation. Furthermore, it include financial

statement, profit and loss account, cash flow statements and other significant statements to know

true position of business organisation (Edwards, J. R., 2013). Main duty of accountant in a

business organisation is to record all financial transaction in journals, post them in ledger,

prepare trial balance and finally reporting through financial statements to present true and fair

view of financial statement. This report exhibits various aspects of financial accounting like

purpose of financial accounting, regulations relating to financial accounting, accounting rules

and principles and explanation about convections and concepts relating to consistency and

material disclosure. This report also covers bank reconciliation statement, process of preparing

bank reconciliation statement and, suspense account and its importance.

BUSINESS REPORT

1.Financial Accounting and its purposes

Financial accounting refers to set of activities related to preparation of final accounts of

a business organisation in order to access and provide information about actual performance and

financial position to internal and external users of financial accounting such as employees,

investors, lenders and creditors, suppliers, government, customers and other regulatory bodies.

Such final accounts are prepared by business organisations while considering various accounting

policies, guidelines, rules and regulations (Hale, 2012). A Business organisation prepare

financial accounting which mainly includes statement of financial position, profit and loss

account or income statement, statement for change in equity and cash flow statement.

Purpose of Financial statement

Financial statement shows financial details of company like profit earned, assets, retained

earnings for both internal and external user who so ever are interested in financial

statements of company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Investor invest in company after analysing the financial statement of the company. Firm

with more assets and profits will attract more investor. Therefore, this is win win

situation for both investor as well as for firm.

Lenders/Creditor prior of extending loan thoroughly checks financial statement of

respective company and then make decision related to extending or restricting their credit

requirement.

Taxation are imposed by government on basis of revenue and assets of company. Hence,

real position is displayed by financial statement thus charged tax accordingly.

Financial statements help in making external comparison (between different firm) as well

as internal comparison (within the firm).

2:Regulation related to finance

Stakeholder of company are the users of financial statement. They access financial

statement for their personal interest like investment/purchase share of particular company,

provide credit to company, purchase product etc. Moreover, the main concern of user is that they

get useful, reliable and relevant data as a base for future actions. Taking into consideration the

requirement of user, government has developed a regulatory framework known as GAAP

(General Accepted Accounting Principle). It is a standard method that involve concept, rules or

principle, which ensure financial statement of company is transparent, reliable as well as

consistent (Fourie, 2015).

There are three regulatory/financial standard in UK

Financial policy committee: It check financial statement as a whole. It's work is to manage risk

associated with the stability of firm. Hence, they are responsible for macroeconomic regulation.

Prudential regulatory authority: These authority are responsible for microeconomic regulation.

Their objective is to safeguard the interest, safety and financial strength of firm by reducing

external factor that have negative effect on firm.

Financial conduct authority: Financial conduct authority's responsibility is to conduct business

regulation, safeguard interest of investors and promote competition for customers. They have

additional power like withdraw existing product, or imitated product as well as they can stop the

functioning of any firm, which provide misleading data to outside party.

2

with more assets and profits will attract more investor. Therefore, this is win win

situation for both investor as well as for firm.

Lenders/Creditor prior of extending loan thoroughly checks financial statement of

respective company and then make decision related to extending or restricting their credit

requirement.

Taxation are imposed by government on basis of revenue and assets of company. Hence,

real position is displayed by financial statement thus charged tax accordingly.

Financial statements help in making external comparison (between different firm) as well

as internal comparison (within the firm).

2:Regulation related to finance

Stakeholder of company are the users of financial statement. They access financial

statement for their personal interest like investment/purchase share of particular company,

provide credit to company, purchase product etc. Moreover, the main concern of user is that they

get useful, reliable and relevant data as a base for future actions. Taking into consideration the

requirement of user, government has developed a regulatory framework known as GAAP

(General Accepted Accounting Principle). It is a standard method that involve concept, rules or

principle, which ensure financial statement of company is transparent, reliable as well as

consistent (Fourie, 2015).

There are three regulatory/financial standard in UK

Financial policy committee: It check financial statement as a whole. It's work is to manage risk

associated with the stability of firm. Hence, they are responsible for macroeconomic regulation.

Prudential regulatory authority: These authority are responsible for microeconomic regulation.

Their objective is to safeguard the interest, safety and financial strength of firm by reducing

external factor that have negative effect on firm.

Financial conduct authority: Financial conduct authority's responsibility is to conduct business

regulation, safeguard interest of investors and promote competition for customers. They have

additional power like withdraw existing product, or imitated product as well as they can stop the

functioning of any firm, which provide misleading data to outside party.

2

3: Accounting rules and principles

Accounting rules: Accounting is a dual entry system, which affect two account one is debit

account, and other one is credit account. There are three rules of accounting for personal account,

real account and nominal account (Hall, J. A., 2012).

Personal account:It includes account of human being (sole proprietor, debtor) and artificial

independent body (company, bank). As well as account of group person like drawing account,

prepaid salary account etc. Hence, the golden rule for personal account is “debit the receiver and

credit the giver”.

Real account: Real account is a part of impersonal account that include firm's tangible asset

(machinery account, cash account) and intangible assets (patent account, goodwill account). The

golden rule for real account is “Debit what comes in, credit what goes out”

Nominal account: Nominal is again a part of impersonal account that include all fictitious

account like expense, revenue, gain and loss of firm. Such as travelling expenses account,

advertisement expense, commission paid and rent received account. The golden rule for nominal

account is “debit all expenses and losses, credit all income and gain” .

Accounting principles

Economic Entity: As business and businessmen are two separate legal entities. So it is duty of

accountant to separate the account of business owner from its business. Like drawings are

liability of business owner.

Monetary measurement: Accountant of firm record only those transaction which can be

displayed in term of money. There can be non monetary transaction which are important for

business but can't become part of financial transaction.

Historical cost principle: The value of assets keeps on changing with time. Moreover, it is the

duty of accountant to update only that price on which assets were taken or brought into the firm.

Firm don't have to do anything with current value of asset. Their further valuation takes place on

basis of historical prices.

Full disclosure of account: Any relevant information to stakeholder must be displayed in the

books of firm. This principle make sure that stakeholders don't get manipulative or misleading

data as well as it ensure firm don't hide any relevant entry.

3

Accounting rules: Accounting is a dual entry system, which affect two account one is debit

account, and other one is credit account. There are three rules of accounting for personal account,

real account and nominal account (Hall, J. A., 2012).

Personal account:It includes account of human being (sole proprietor, debtor) and artificial

independent body (company, bank). As well as account of group person like drawing account,

prepaid salary account etc. Hence, the golden rule for personal account is “debit the receiver and

credit the giver”.

Real account: Real account is a part of impersonal account that include firm's tangible asset

(machinery account, cash account) and intangible assets (patent account, goodwill account). The

golden rule for real account is “Debit what comes in, credit what goes out”

Nominal account: Nominal is again a part of impersonal account that include all fictitious

account like expense, revenue, gain and loss of firm. Such as travelling expenses account,

advertisement expense, commission paid and rent received account. The golden rule for nominal

account is “debit all expenses and losses, credit all income and gain” .

Accounting principles

Economic Entity: As business and businessmen are two separate legal entities. So it is duty of

accountant to separate the account of business owner from its business. Like drawings are

liability of business owner.

Monetary measurement: Accountant of firm record only those transaction which can be

displayed in term of money. There can be non monetary transaction which are important for

business but can't become part of financial transaction.

Historical cost principle: The value of assets keeps on changing with time. Moreover, it is the

duty of accountant to update only that price on which assets were taken or brought into the firm.

Firm don't have to do anything with current value of asset. Their further valuation takes place on

basis of historical prices.

Full disclosure of account: Any relevant information to stakeholder must be displayed in the

books of firm. This principle make sure that stakeholders don't get manipulative or misleading

data as well as it ensure firm don't hide any relevant entry.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Going concern principles: This principle says whenever a firm operate, it operate with life long

running prospective. In case accountant comes to know that company can't continue any more

then this information must also be disclosed in their statements.

4 Convection and concept related to consistency and material disclosure

Consistency: This method states that the policy formed by company should be followed for years

and years they cannot change them repeatedly. Adopting same policy helps company to make

better comparison within the industry. For instance, if a firm is following straight line method of

depreciation they should try to continue with that only (Jönsson, 2013).

Materiality disclosure: All transaction should be recorded or disclosed properly. This brings

transparency to firm and attract stakeholders. Like if the company’s liabilities are more than

asset they should disclose it in their financial statements. All petty information should not be

hide from outside party for the self-motives of firm.

CLIENT 1

See appendix

CLIENT 2

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018

Peter Hampau

Statement of Profit or Loss for the year

ended 31 July 2018

£ £ £

Revenue 1,20,000

Less cost of sales

Opening inventory 4,500

Add purchases 70,000

74,500

Less closing inventory Note 1 -42,640 -31,860

4

running prospective. In case accountant comes to know that company can't continue any more

then this information must also be disclosed in their statements.

4 Convection and concept related to consistency and material disclosure

Consistency: This method states that the policy formed by company should be followed for years

and years they cannot change them repeatedly. Adopting same policy helps company to make

better comparison within the industry. For instance, if a firm is following straight line method of

depreciation they should try to continue with that only (Jönsson, 2013).

Materiality disclosure: All transaction should be recorded or disclosed properly. This brings

transparency to firm and attract stakeholders. Like if the company’s liabilities are more than

asset they should disclose it in their financial statements. All petty information should not be

hide from outside party for the self-motives of firm.

CLIENT 1

See appendix

CLIENT 2

(a) Statement of profit and loss for Peter Hampau for the year ended 31st July 2018

Peter Hampau

Statement of Profit or Loss for the year

ended 31 July 2018

£ £ £

Revenue 1,20,000

Less cost of sales

Opening inventory 4,500

Add purchases 70,000

74,500

Less closing inventory Note 1 -42,640 -31,860

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross profit 88,140

less expenses

Wages and salaries 16,500

Add wages and salaries accrued 1,520 18,020

Motor expenses 4580

Admin expenses 1,650

Heating and lighting 550

Advertising expenses 1,030

Less advertising expenses

prepaid -447 583

Depreciation on premises 560

Depreciatiomn on equipment 1,900

Deprecition on motor vehicles 360 2,820

28,203

Net profit 59,937

5

less expenses

Wages and salaries 16,500

Add wages and salaries accrued 1,520 18,020

Motor expenses 4580

Admin expenses 1,650

Heating and lighting 550

Advertising expenses 1,030

Less advertising expenses

prepaid -447 583

Depreciation on premises 560

Depreciatiomn on equipment 1,900

Deprecition on motor vehicles 360 2,820

28,203

Net profit 59,937

5

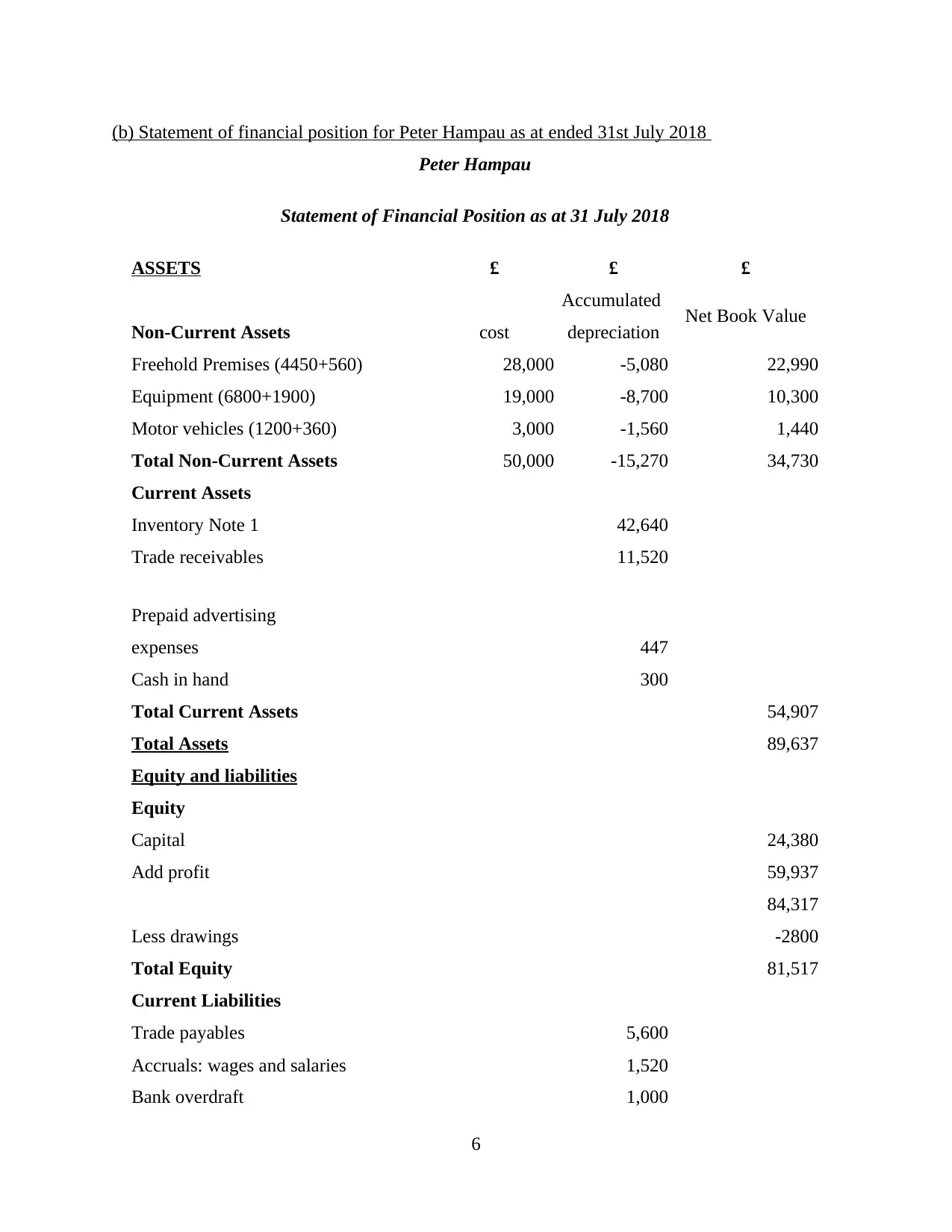

(b) Statement of financial position for Peter Hampau as at ended 31st July 2018

Peter Hampau

Statement of Financial Position as at 31 July 2018

ASSETS £ £ £

Non-Current Assets cost

Accumulated

depreciation Net Book Value

Freehold Premises (4450+560) 28,000 -5,080 22,990

Equipment (6800+1900) 19,000 -8,700 10,300

Motor vehicles (1200+360) 3,000 -1,560 1,440

Total Non-Current Assets 50,000 -15,270 34,730

Current Assets

Inventory Note 1 42,640

Trade receivables 11,520

Prepaid advertising

expenses 447

Cash in hand 300

Total Current Assets 54,907

Total Assets 89,637

Equity and liabilities

Equity

Capital 24,380

Add profit 59,937

84,317

Less drawings -2800

Total Equity 81,517

Current Liabilities

Trade payables 5,600

Accruals: wages and salaries 1,520

Bank overdraft 1,000

6

Peter Hampau

Statement of Financial Position as at 31 July 2018

ASSETS £ £ £

Non-Current Assets cost

Accumulated

depreciation Net Book Value

Freehold Premises (4450+560) 28,000 -5,080 22,990

Equipment (6800+1900) 19,000 -8,700 10,300

Motor vehicles (1200+360) 3,000 -1,560 1,440

Total Non-Current Assets 50,000 -15,270 34,730

Current Assets

Inventory Note 1 42,640

Trade receivables 11,520

Prepaid advertising

expenses 447

Cash in hand 300

Total Current Assets 54,907

Total Assets 89,637

Equity and liabilities

Equity

Capital 24,380

Add profit 59,937

84,317

Less drawings -2800

Total Equity 81,517

Current Liabilities

Trade payables 5,600

Accruals: wages and salaries 1,520

Bank overdraft 1,000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Current Liabilities 8,120

Total Equity and Liabilities 89,637

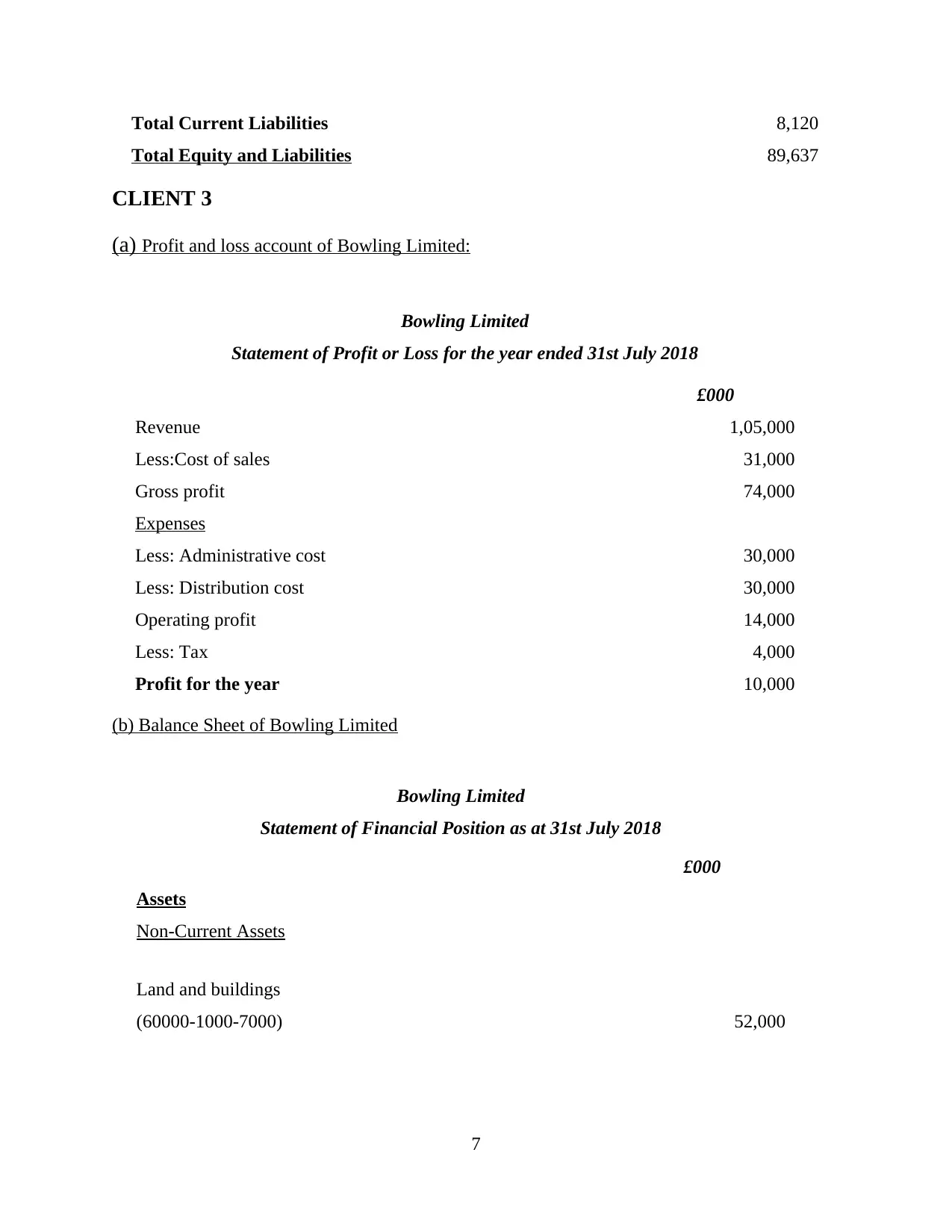

CLIENT 3

(a) Profit and loss account of Bowling Limited:

Bowling Limited

Statement of Profit or Loss for the year ended 31st July 2018

£000

Revenue 1,05,000

Less:Cost of sales 31,000

Gross profit 74,000

Expenses

Less: Administrative cost 30,000

Less: Distribution cost 30,000

Operating profit 14,000

Less: Tax 4,000

Profit for the year 10,000

(b) Balance Sheet of Bowling Limited

Bowling Limited

Statement of Financial Position as at 31st July 2018

£000

Assets

Non-Current Assets

Land and buildings

(60000-1000-7000) 52,000

7

Total Equity and Liabilities 89,637

CLIENT 3

(a) Profit and loss account of Bowling Limited:

Bowling Limited

Statement of Profit or Loss for the year ended 31st July 2018

£000

Revenue 1,05,000

Less:Cost of sales 31,000

Gross profit 74,000

Expenses

Less: Administrative cost 30,000

Less: Distribution cost 30,000

Operating profit 14,000

Less: Tax 4,000

Profit for the year 10,000

(b) Balance Sheet of Bowling Limited

Bowling Limited

Statement of Financial Position as at 31st July 2018

£000

Assets

Non-Current Assets

Land and buildings

(60000-1000-7000) 52,000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

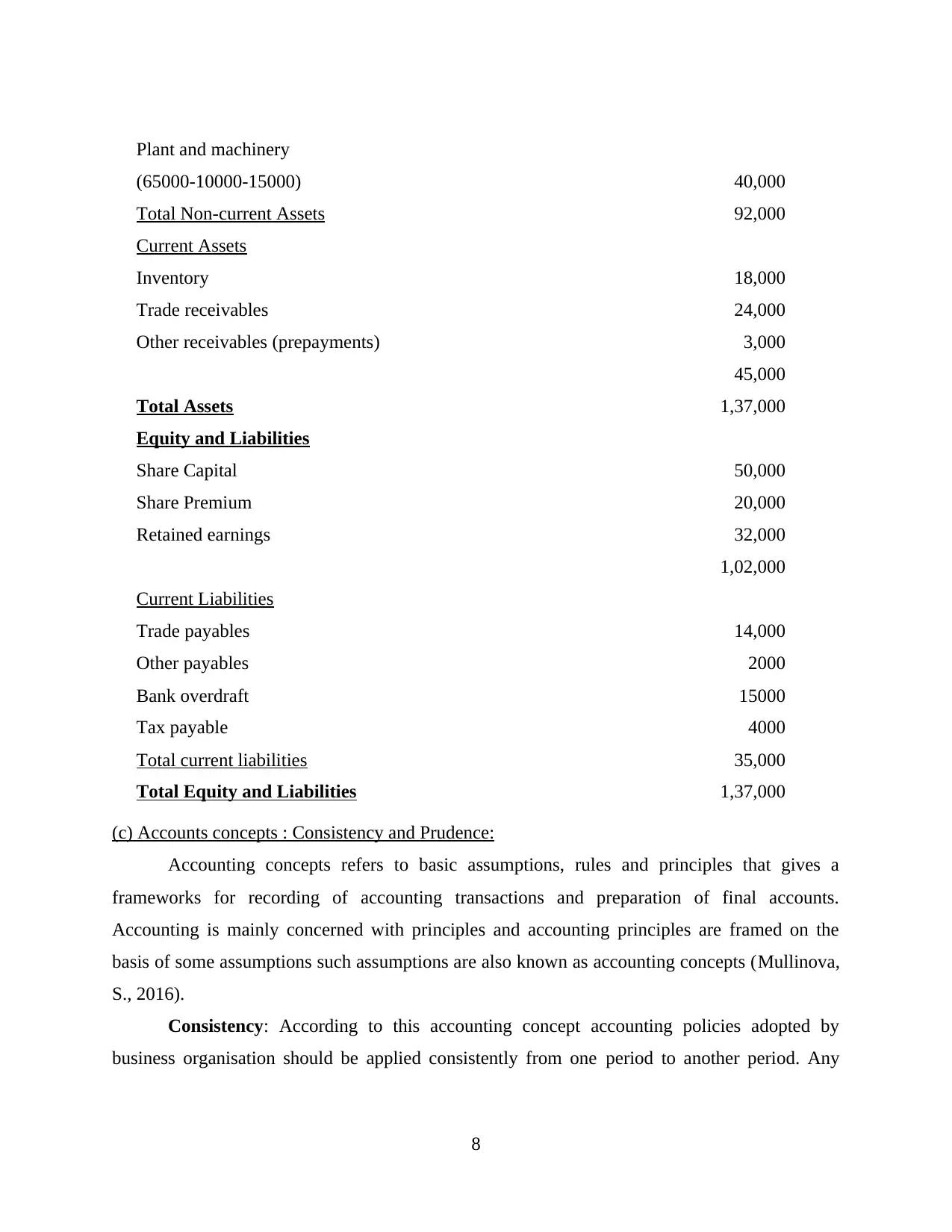

Plant and machinery

(65000-10000-15000) 40,000

Total Non-current Assets 92,000

Current Assets

Inventory 18,000

Trade receivables 24,000

Other receivables (prepayments) 3,000

45,000

Total Assets 1,37,000

Equity and Liabilities

Share Capital 50,000

Share Premium 20,000

Retained earnings 32,000

1,02,000

Current Liabilities

Trade payables 14,000

Other payables 2000

Bank overdraft 15000

Tax payable 4000

Total current liabilities 35,000

Total Equity and Liabilities 1,37,000

(c) Accounts concepts : Consistency and Prudence:

Accounting concepts refers to basic assumptions, rules and principles that gives a

frameworks for recording of accounting transactions and preparation of final accounts.

Accounting is mainly concerned with principles and accounting principles are framed on the

basis of some assumptions such assumptions are also known as accounting concepts (Mullinova,

S., 2016).

Consistency: According to this accounting concept accounting policies adopted by

business organisation should be applied consistently from one period to another period. Any

8

(65000-10000-15000) 40,000

Total Non-current Assets 92,000

Current Assets

Inventory 18,000

Trade receivables 24,000

Other receivables (prepayments) 3,000

45,000

Total Assets 1,37,000

Equity and Liabilities

Share Capital 50,000

Share Premium 20,000

Retained earnings 32,000

1,02,000

Current Liabilities

Trade payables 14,000

Other payables 2000

Bank overdraft 15000

Tax payable 4000

Total current liabilities 35,000

Total Equity and Liabilities 1,37,000

(c) Accounts concepts : Consistency and Prudence:

Accounting concepts refers to basic assumptions, rules and principles that gives a

frameworks for recording of accounting transactions and preparation of final accounts.

Accounting is mainly concerned with principles and accounting principles are framed on the

basis of some assumptions such assumptions are also known as accounting concepts (Mullinova,

S., 2016).

Consistency: According to this accounting concept accounting policies adopted by

business organisation should be applied consistently from one period to another period. Any

8

change in already adopted accounting policies and assumption can be made only if it is as per

relevant statue or any change would results in better presentation of accounts.

Prudence: According to this accounting concept business organisation can record

expenses, liabilities and obligation as soon as they occur whereas any revenues and incomes

should be recorded as they realized.

(d) Purpose of depreciation in formulating accounting statements and methods of Depreciation:

Depreciation used by business organisation to exhibit decrease in assets arises due to

obsolescence or physical wear and tear of assets during a particular period (Bushman and Smith,

2001). Depreciation is simply shows actual consumption of particular asset. Following are major

methods to calculate depreciation:

Straight line method: In straight line method an equal amount of depreciation is

provided by business organisation during the whole useful life of asset. This is an simple and

most widely used method of depreciation. Formula of depreciation under this method is:

Cost of assets less Residual value

Total Useful life of asset

Written down value method: In this method a certain formula is used to calculate fix

percentage of depreciation and such percentage is applied to book value of asset to get amount of

depreciation for the year. This method is used for assets that have more efficiency in the

beginning and thereafter decreases year after year (Holthausen and Watts, 2001). This method is

usually adopted for plant and machinery, fixtures and fittings, motor vehicles, etc..

CLIENT 4

Purpose of bank reconciliation: Bank-reconciliation statement is prepared by organisation to

reconcile the amount of bank account prepared by organisation with amount shown in bank

statement or pass book of bank (Libby, Bloomfield and Nelson, 2002).

Reason for variation in cash book and bank statement: Due to deposit of any amount by

customers directly into bank account, bank charges charged by bank and organisation in unaware

the fact, cheque issued but not presented etc. are major reason for difference in balance of cash

book and bank statement as on a particular date (Bank reconciliation statement. 2017).

(i) Bank reconciliation statement at 1st December 2017:

9

relevant statue or any change would results in better presentation of accounts.

Prudence: According to this accounting concept business organisation can record

expenses, liabilities and obligation as soon as they occur whereas any revenues and incomes

should be recorded as they realized.

(d) Purpose of depreciation in formulating accounting statements and methods of Depreciation:

Depreciation used by business organisation to exhibit decrease in assets arises due to

obsolescence or physical wear and tear of assets during a particular period (Bushman and Smith,

2001). Depreciation is simply shows actual consumption of particular asset. Following are major

methods to calculate depreciation:

Straight line method: In straight line method an equal amount of depreciation is

provided by business organisation during the whole useful life of asset. This is an simple and

most widely used method of depreciation. Formula of depreciation under this method is:

Cost of assets less Residual value

Total Useful life of asset

Written down value method: In this method a certain formula is used to calculate fix

percentage of depreciation and such percentage is applied to book value of asset to get amount of

depreciation for the year. This method is used for assets that have more efficiency in the

beginning and thereafter decreases year after year (Holthausen and Watts, 2001). This method is

usually adopted for plant and machinery, fixtures and fittings, motor vehicles, etc..

CLIENT 4

Purpose of bank reconciliation: Bank-reconciliation statement is prepared by organisation to

reconcile the amount of bank account prepared by organisation with amount shown in bank

statement or pass book of bank (Libby, Bloomfield and Nelson, 2002).

Reason for variation in cash book and bank statement: Due to deposit of any amount by

customers directly into bank account, bank charges charged by bank and organisation in unaware

the fact, cheque issued but not presented etc. are major reason for difference in balance of cash

book and bank statement as on a particular date (Bank reconciliation statement. 2017).

(i) Bank reconciliation statement at 1st December 2017:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.