Financial Accounting Assignment Report BAO2202 Semester 2 2017

VerifiedAdded on 2020/03/01

|17

|4922

|183

Report

AI Summary

This report, prepared for a Financial Accounting course (BAO2202), delves into key aspects of financial reporting. Part I focuses on the qualitative characteristics of financial information as defined by the AASB Framework, emphasizing relevance, faithful representation, comparability, and consistency. The report highlights how these characteristics enhance the decision-usefulness of financial statements for stakeholders. Part II examines AASB 13, which addresses fair value measurement, and discusses its limitations, such as limited reliability, misleading information, and volatility. The report emphasizes the importance of viable disclosure and accounting judgments when applying this standard. The report uses various research articles and journals to support its findings, providing a comprehensive overview of these critical accounting concepts.

BAO2202

Financial Accounting

Assignment Semester 2 2017

Financial Accounting

Assignment Semester 2 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Part I...........................................................................................................................................3

Abstract..................................................................................................................................3

Introduction............................................................................................................................3

Part I.......................................................................................................................................3

Conclusion..............................................................................................................................3

Bibliography...........................................................................................................................3

Part II..........................................................................................................................................4

Abstract..................................................................................................................................4

Introduction............................................................................................................................4

Part II......................................................................................................................................4

Conclusion..............................................................................................................................4

Bibliography...........................................................................................................................4

Part III........................................................................................................................................5

Abstract..................................................................................................................................5

Introduction............................................................................................................................5

Part III....................................................................................................................................5

Conclusion..............................................................................................................................5

Bibliography...........................................................................................................................5

Part I...........................................................................................................................................3

Abstract..................................................................................................................................3

Introduction............................................................................................................................3

Part I.......................................................................................................................................3

Conclusion..............................................................................................................................3

Bibliography...........................................................................................................................3

Part II..........................................................................................................................................4

Abstract..................................................................................................................................4

Introduction............................................................................................................................4

Part II......................................................................................................................................4

Conclusion..............................................................................................................................4

Bibliography...........................................................................................................................4

Part III........................................................................................................................................5

Abstract..................................................................................................................................5

Introduction............................................................................................................................5

Part III....................................................................................................................................5

Conclusion..............................................................................................................................5

Bibliography...........................................................................................................................5

PART I

Abstract

This part of the study is focused on the description of qualitative characteristics of

financial information by considering AASB Framework. Qualitative characteristics enhance

relevancy of financial information to assist stakeholders in making decisions concerned with

the business entity. Due to this factor, managerial authorities are required to consider this

framework in preparation of financial statements to ensure its viability for stakeholders.

Introduction

AASB framework is highly concerned for viability for accounting information as it is

used by stakeholders for assisting them in decision-making procedures. This part of the study

is based on examination of qualitative characteristics of accounting information by

considering appropriate research articles and journals.

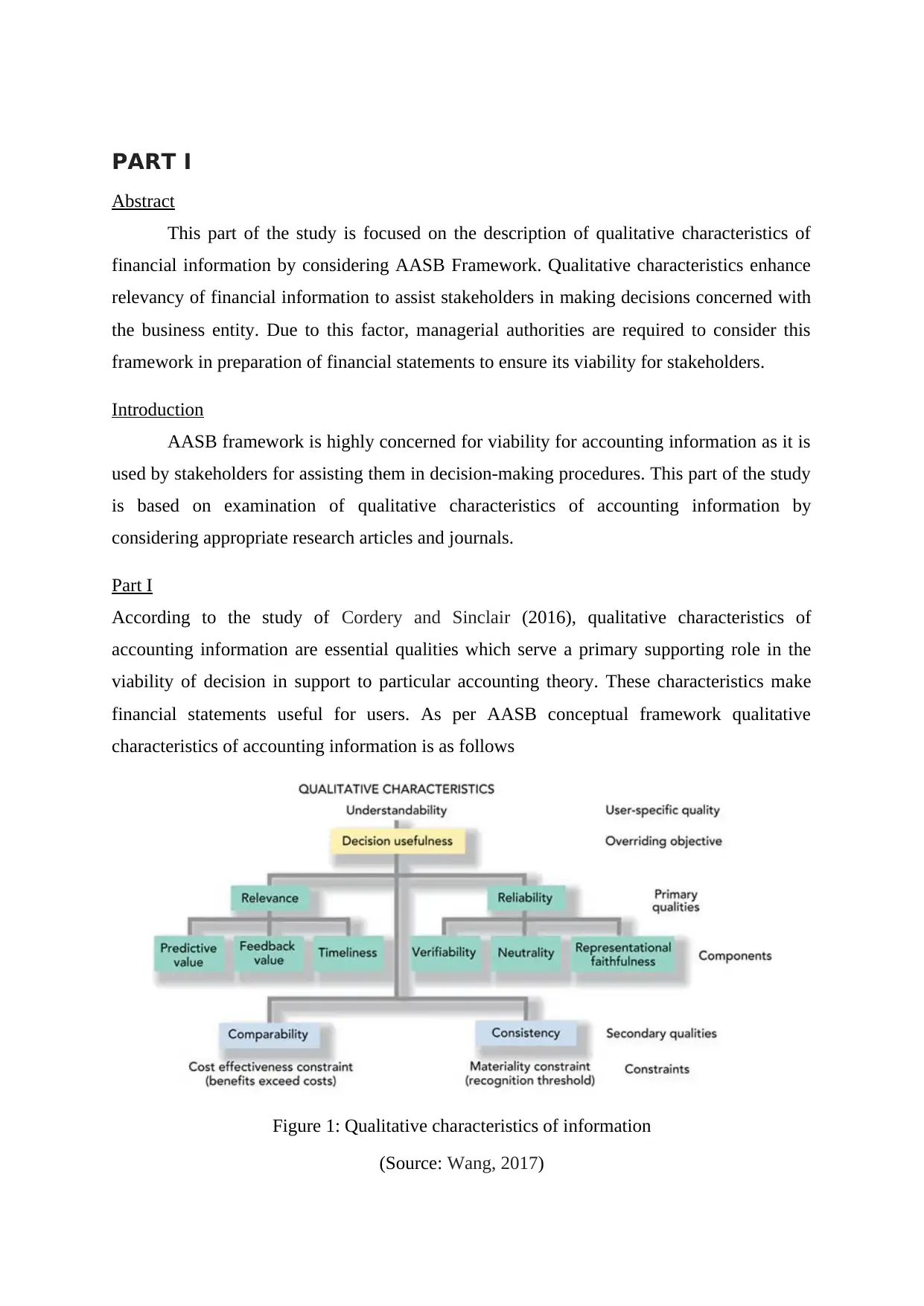

Part I

According to the study of Cordery and Sinclair (2016), qualitative characteristics of

accounting information are essential qualities which serve a primary supporting role in the

viability of decision in support to particular accounting theory. These characteristics make

financial statements useful for users. As per AASB conceptual framework qualitative

characteristics of accounting information is as follows

Figure 1: Qualitative characteristics of information

(Source: Wang, 2017)

Abstract

This part of the study is focused on the description of qualitative characteristics of

financial information by considering AASB Framework. Qualitative characteristics enhance

relevancy of financial information to assist stakeholders in making decisions concerned with

the business entity. Due to this factor, managerial authorities are required to consider this

framework in preparation of financial statements to ensure its viability for stakeholders.

Introduction

AASB framework is highly concerned for viability for accounting information as it is

used by stakeholders for assisting them in decision-making procedures. This part of the study

is based on examination of qualitative characteristics of accounting information by

considering appropriate research articles and journals.

Part I

According to the study of Cordery and Sinclair (2016), qualitative characteristics of

accounting information are essential qualities which serve a primary supporting role in the

viability of decision in support to particular accounting theory. These characteristics make

financial statements useful for users. As per AASB conceptual framework qualitative

characteristics of accounting information is as follows

Figure 1: Qualitative characteristics of information

(Source: Wang, 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The fundamental qualitative characteristic of accounting information is relevance and

faithful representation. Both of these qualities are important, if the information is 100%

reliable but not relevant, then it will be of no use. On the other hand, accurate information

consists less or no value if the same is not reliable (Amendments to the Australian

Conceptual Framework, 2013). These qualities are enumerated as below and are inclusive of

the elements which will make these qualities more desirable. In addition to two secondary

qualities are considers which are comparability and consistency. These characteristics must

be steady to each other.

The information must be relevant as it helps users to determine the past, current and

future capacity of generating income of the business. Relevant information can make

significant in the opinion of the user as decision requires either predictive or confirmatory

value or both. Relevance also consists a significant element which is timeliness. Information

must be provided at the right time to the user to enable its use in the process of decision

making (Barker and Penman, 2016). Further, reliability is an amount on which the

information is verifiable as it assists in assuring the users that the information shows exactly

the economic phenomenon that seeks to represent them. The word objectivity refers to

verifiability. Verifiability of accounting information ensures faithful representation of

economic phenomena. Accounting information provided statements must be verifiable

whether it is by the direct or indirect method. It means information must be supported by

reliable evidence and individuals are in a position to cross check that cited information is

represented in a faithful manner. This quality takes place when both measure and

phenomenon makes an agreement; it claims to be represented.

In accordance with the viewpoint of Collier (2015), faithful representation does not

refer to complete accuracy of financial aspects but refers that provide information is free from

errors and omissions. For example, estimation in disclosure or computation cannot be

perfectly accurate, but representation can be faithful if complete information is provided

along with the limitation of the estimation process and providing assurance that process is

free from error and biases. Although, faithful representation does not necessarily imply useful

information. For a better understanding of this aspect, following example can be considered;

in the case where estimation is to be made regarding the amount by which carrying amount of

assets is required to be adjusted to provide effective on impairment on the value of the asset

(Amendments to the Australian Conceptual Framework, 2013). In this case is disclosure of

impairment is faithful representation only if the entity has applied an appropriate process in a

faithful representation. Both of these qualities are important, if the information is 100%

reliable but not relevant, then it will be of no use. On the other hand, accurate information

consists less or no value if the same is not reliable (Amendments to the Australian

Conceptual Framework, 2013). These qualities are enumerated as below and are inclusive of

the elements which will make these qualities more desirable. In addition to two secondary

qualities are considers which are comparability and consistency. These characteristics must

be steady to each other.

The information must be relevant as it helps users to determine the past, current and

future capacity of generating income of the business. Relevant information can make

significant in the opinion of the user as decision requires either predictive or confirmatory

value or both. Relevance also consists a significant element which is timeliness. Information

must be provided at the right time to the user to enable its use in the process of decision

making (Barker and Penman, 2016). Further, reliability is an amount on which the

information is verifiable as it assists in assuring the users that the information shows exactly

the economic phenomenon that seeks to represent them. The word objectivity refers to

verifiability. Verifiability of accounting information ensures faithful representation of

economic phenomena. Accounting information provided statements must be verifiable

whether it is by the direct or indirect method. It means information must be supported by

reliable evidence and individuals are in a position to cross check that cited information is

represented in a faithful manner. This quality takes place when both measure and

phenomenon makes an agreement; it claims to be represented.

In accordance with the viewpoint of Collier (2015), faithful representation does not

refer to complete accuracy of financial aspects but refers that provide information is free from

errors and omissions. For example, estimation in disclosure or computation cannot be

perfectly accurate, but representation can be faithful if complete information is provided

along with the limitation of the estimation process and providing assurance that process is

free from error and biases. Although, faithful representation does not necessarily imply useful

information. For a better understanding of this aspect, following example can be considered;

in the case where estimation is to be made regarding the amount by which carrying amount of

assets is required to be adjusted to provide effective on impairment on the value of the asset

(Amendments to the Australian Conceptual Framework, 2013). In this case is disclosure of

impairment is faithful representation only if the entity has applied an appropriate process in a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

proper manner by describing the estimates along with the uncertainties associated with it.

However, in the presume case if the level of cited uncertainty regarding estimate is

satisfactorily large then it will not be particularly useful. It simple words, the relevancy of the

asset regarding faithful representation will be questionable. In such situation, if there is no

scope of other better alternative representation then cited estimate may work as the

superlative available information.

Accounting information provided to users must be material to them on the basis of its

magnitude or nature. In accordance with the study of, information is considered to be material

if its misstatement or omitting can influence the decision of user (Cordery and Sinclair,

2016). Due to this factor, the board cannot determine the quantitative threshold for

materiality which is uniform or predetermined as the materiality of information vary to

business to business. Along with this, it must be represented faithful, and same can be

attained by ensuring that fact is complete, free from error and unbiased.

Secondary characteristics of accounting information that is significant for making

decisions are comparability, consistency, verifiability, timeliness and understandability.

Relating to comparability, it is the concept of applying consistency in practices of accounting

among different time periods. Both the predictive and feedback values can be improved if

users make a comparison of the company’s performance over time. This characteristic makes

user capable of determining and understanding similarity and dissimilarity among accounting

items. In accordance with the study of Wang (2014), characteristic of comparability is

connected with the characteristic of consistency. In this aspect, AASB states that

comparability is the goal which is achieved through consistency. Change in any of the policy

needs disclosure in the notes to accounts of financial statements to re-establish the

comparability in the accounting periods. However, comparability does not refer to

uniformity, but it means the development of standard norms to enhance understanding of user

regarding the interpretation of financial statements (Amendments to the Australian

Conceptual Framework, 2013).

Accounting information is measured to be understandable if it is classified,

characterised and presented in an appropriate manner. However, some of the accounting

phenomena are inherently complex which is not easy to understand, and exclusion of such

facts make interpretation easy (Barker and Penman, 2016). Although exclusion of such facts

can mislead users and same is considered to be unethical accounting practice thus it is

However, in the presume case if the level of cited uncertainty regarding estimate is

satisfactorily large then it will not be particularly useful. It simple words, the relevancy of the

asset regarding faithful representation will be questionable. In such situation, if there is no

scope of other better alternative representation then cited estimate may work as the

superlative available information.

Accounting information provided to users must be material to them on the basis of its

magnitude or nature. In accordance with the study of, information is considered to be material

if its misstatement or omitting can influence the decision of user (Cordery and Sinclair,

2016). Due to this factor, the board cannot determine the quantitative threshold for

materiality which is uniform or predetermined as the materiality of information vary to

business to business. Along with this, it must be represented faithful, and same can be

attained by ensuring that fact is complete, free from error and unbiased.

Secondary characteristics of accounting information that is significant for making

decisions are comparability, consistency, verifiability, timeliness and understandability.

Relating to comparability, it is the concept of applying consistency in practices of accounting

among different time periods. Both the predictive and feedback values can be improved if

users make a comparison of the company’s performance over time. This characteristic makes

user capable of determining and understanding similarity and dissimilarity among accounting

items. In accordance with the study of Wang (2014), characteristic of comparability is

connected with the characteristic of consistency. In this aspect, AASB states that

comparability is the goal which is achieved through consistency. Change in any of the policy

needs disclosure in the notes to accounts of financial statements to re-establish the

comparability in the accounting periods. However, comparability does not refer to

uniformity, but it means the development of standard norms to enhance understanding of user

regarding the interpretation of financial statements (Amendments to the Australian

Conceptual Framework, 2013).

Accounting information is measured to be understandable if it is classified,

characterised and presented in an appropriate manner. However, some of the accounting

phenomena are inherently complex which is not easy to understand, and exclusion of such

facts make interpretation easy (Barker and Penman, 2016). Although exclusion of such facts

can mislead users and same is considered to be unethical accounting practice thus it is

expected that users must have reasonable knowledge regarding business and economic

activities so they can make a viable interpretation. This characteristic also states that

information must not be restricted to the interest of average investor or generation users as it

must serve the purpose of a broad range of users.

For making accounting information more useful, it must include assured qualities and

meet the standards. FASB (Financial Accounting Standards Advisory Board) initiates and

manages GAAP (generally accepted accounting principles) that set the standards and

qualities of the accounting information (irt, Muthusamy and Bir, 2017). Business entities

should focus on enhancing qualitative characteristics to the maximum possible extent.

Application of these qualitative characteristics is an iterative process which does not comply

with the specific procedure as it needs subjective qualification supported by the appropriate

disclosure of material facts (Wang, 2014).

Conclusion

In accordance with this part of the study, it can be concluded that corporate entities

are required to prepare financial statements by considering all the qualitative characteristics

of accounting information cited by AASB framework to provide assurance that they are free

from all material misstatements.

activities so they can make a viable interpretation. This characteristic also states that

information must not be restricted to the interest of average investor or generation users as it

must serve the purpose of a broad range of users.

For making accounting information more useful, it must include assured qualities and

meet the standards. FASB (Financial Accounting Standards Advisory Board) initiates and

manages GAAP (generally accepted accounting principles) that set the standards and

qualities of the accounting information (irt, Muthusamy and Bir, 2017). Business entities

should focus on enhancing qualitative characteristics to the maximum possible extent.

Application of these qualitative characteristics is an iterative process which does not comply

with the specific procedure as it needs subjective qualification supported by the appropriate

disclosure of material facts (Wang, 2014).

Conclusion

In accordance with this part of the study, it can be concluded that corporate entities

are required to prepare financial statements by considering all the qualitative characteristics

of accounting information cited by AASB framework to provide assurance that they are free

from all material misstatements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bibliography

Amendments to the Australian Conceptual Framework. 2013. [Online]. Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB_CF_2013-1_12-13.pdf>. [Accessed

on 31st August 2017].

Barker, R. and Penman, S., 2016. Moving the conceptual framework forward: Accounting for

uncertainty. Unpublished paper, Oxford University and Columbia University.

Birt, J.L., Muthusamy, K. and Bir, P., 2017. XBRL and the Qualitative Characteristics of

Useful Financial Information. Accounting Research Journal, 30(1).

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Cordery, C.J. and Sinclair, R., 2016. Decision-Usefulness and Stewardship As Conceptual

Framework Objectives: Continuing Challenges.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Amendments to the Australian Conceptual Framework. 2013. [Online]. Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB_CF_2013-1_12-13.pdf>. [Accessed

on 31st August 2017].

Barker, R. and Penman, S., 2016. Moving the conceptual framework forward: Accounting for

uncertainty. Unpublished paper, Oxford University and Columbia University.

Birt, J.L., Muthusamy, K. and Bir, P., 2017. XBRL and the Qualitative Characteristics of

Useful Financial Information. Accounting Research Journal, 30(1).

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Cordery, C.J. and Sinclair, R., 2016. Decision-Usefulness and Stewardship As Conceptual

Framework Objectives: Continuing Challenges.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Wang, C., 2014. Accounting standards harmonization and financial statement comparability:

Evidence from transnational information transfer. Journal of Accounting Research, 52(4),

pp.955-992.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART II

Abstract

AASB 13 provides a description of measuring the fair value of assets and liabilities,

but same is associated with various limitation such as Limited reliability, Misleading

Information and Volatility. Due to this factor, this standard is applied by considering viable

disclosure and other relevant accounting judgements.

Introduction

AASB 13 deals with fair value measurement with the objective to develop a uniform

procedure for measurement and disclosure of fair values to ensure consistency and

comparability. However, this standard comprises various uncertainties and this part of study

deals with the description of limitations of the fair value of accounting in terms of providing

decision-useful information for the users of financial statements by considering the viewpoint

of various research scholars.

Part II

In accordance with AASB 13, the definition of fair value is an existing exit price, not

an entrance price. However, this exit price of a particular asset or liability theoretically varies

from its transactional price. Despite from the fact that entry and exit price can be similar in

certain circumstances, the transactional price cannot be accepted to present the asset or

liability fair value on its primary acknowledgement as stated under AASB 13 (AASB

Standard, 2015). The objective of exit price of fair value extent applies apart from the

reporting company’s value or ability to transfer liability or sell the asset at the date of

measurement.

Fair value is considered to be the exit price in principle market (or lack of principle

market and the transaction could be made by the reporting business entity in the most

benefitted market). However, the exit market’s price must not be used to adjust the

transactional costs. Also, the fair value is measured on markets, and same is identified on the

basis of assumptions of the participants of the market that would be used in pricing liability

and assets. The fair value measurement goal does not alter on the basis of activities level

existing in the exit market or the techniques of valuation been used (Majercakova and Skoda,

2015). Fair value holds up to be a based on market exit price that assesses the current

conditions of the market on the date of measurement, even when it has been a considerable

Abstract

AASB 13 provides a description of measuring the fair value of assets and liabilities,

but same is associated with various limitation such as Limited reliability, Misleading

Information and Volatility. Due to this factor, this standard is applied by considering viable

disclosure and other relevant accounting judgements.

Introduction

AASB 13 deals with fair value measurement with the objective to develop a uniform

procedure for measurement and disclosure of fair values to ensure consistency and

comparability. However, this standard comprises various uncertainties and this part of study

deals with the description of limitations of the fair value of accounting in terms of providing

decision-useful information for the users of financial statements by considering the viewpoint

of various research scholars.

Part II

In accordance with AASB 13, the definition of fair value is an existing exit price, not

an entrance price. However, this exit price of a particular asset or liability theoretically varies

from its transactional price. Despite from the fact that entry and exit price can be similar in

certain circumstances, the transactional price cannot be accepted to present the asset or

liability fair value on its primary acknowledgement as stated under AASB 13 (AASB

Standard, 2015). The objective of exit price of fair value extent applies apart from the

reporting company’s value or ability to transfer liability or sell the asset at the date of

measurement.

Fair value is considered to be the exit price in principle market (or lack of principle

market and the transaction could be made by the reporting business entity in the most

benefitted market). However, the exit market’s price must not be used to adjust the

transactional costs. Also, the fair value is measured on markets, and same is identified on the

basis of assumptions of the participants of the market that would be used in pricing liability

and assets. The fair value measurement goal does not alter on the basis of activities level

existing in the exit market or the techniques of valuation been used (Majercakova and Skoda,

2015). Fair value holds up to be a based on market exit price that assesses the current

conditions of the market on the date of measurement, even when it has been a considerable

reduction in the level of activities for the liability and assets. AASB 13 standard states fair

value as the price been received in order to sell the asset or to pay off a liability in a timely

and systematic transaction among participant of the market at the date of measurement.

AASB 13 is the Standard which defines fair value and sets out a particular framework to

measure fair value and needs company’s disclosures regarding the measurement of fair value.

Fair value is based on market measurement, not a company’s particular measurement.

Information cannot be provided for certain assets and liabilities on the basis of noticeable

transactions or information of market (Hu, Percy and Yao, 2015). However, fair value

measurement aim in both the cases is similar, that is to consider the value at which an orderly

transaction is to be done for the sale of asset or liability will occur between the participants of

the market at the date of measurement under the existing market conditions. That is at the

date of, measurement the exit price from the view of market participant which is holding the

asset or outstanding liability

The standard is applied if another standard need or enables the disclosures or fair

value regarding the measurements such as fair value deduced by costs to make it in sellable

conditions, based on fair value or disclosures about those measurements), except which are

specifies in the following paragraphs such as Transactions of share based payments within

the extent of AASB 2 (Freeman, Wells and Wyatt, 2017). Transactions of leasing within the

extent of AASB 117. Measurements which consists same fair value, however, but aren’t fair

value. For example, under AASB 102 Inventories of net realisable value or value in use in

AASB 136 Impairment of Assets. The standard requires disclosure but not required for these

specific transactions, which are covered under AASB 119 Employee Benefits) plan assets

measured at fair value and AASB 136 assets for which recoverable amount is a fair value

fewer costs of disposal.

By considering above described literature primary limitations associated with this standard is

enumerated as below:

Limited reliability

It is negotiated that the method of fair value accounting which provides the

information is reliable and relevant for a certain period of time. As the financial statement

information is time-particular for the specified market condition. From the point of an

inexperienced expert in accounting, they will suffer from confusion by seeing changes in the

value as the price been received in order to sell the asset or to pay off a liability in a timely

and systematic transaction among participant of the market at the date of measurement.

AASB 13 is the Standard which defines fair value and sets out a particular framework to

measure fair value and needs company’s disclosures regarding the measurement of fair value.

Fair value is based on market measurement, not a company’s particular measurement.

Information cannot be provided for certain assets and liabilities on the basis of noticeable

transactions or information of market (Hu, Percy and Yao, 2015). However, fair value

measurement aim in both the cases is similar, that is to consider the value at which an orderly

transaction is to be done for the sale of asset or liability will occur between the participants of

the market at the date of measurement under the existing market conditions. That is at the

date of, measurement the exit price from the view of market participant which is holding the

asset or outstanding liability

The standard is applied if another standard need or enables the disclosures or fair

value regarding the measurements such as fair value deduced by costs to make it in sellable

conditions, based on fair value or disclosures about those measurements), except which are

specifies in the following paragraphs such as Transactions of share based payments within

the extent of AASB 2 (Freeman, Wells and Wyatt, 2017). Transactions of leasing within the

extent of AASB 117. Measurements which consists same fair value, however, but aren’t fair

value. For example, under AASB 102 Inventories of net realisable value or value in use in

AASB 136 Impairment of Assets. The standard requires disclosure but not required for these

specific transactions, which are covered under AASB 119 Employee Benefits) plan assets

measured at fair value and AASB 136 assets for which recoverable amount is a fair value

fewer costs of disposal.

By considering above described literature primary limitations associated with this standard is

enumerated as below:

Limited reliability

It is negotiated that the method of fair value accounting which provides the

information is reliable and relevant for a certain period of time. As the financial statement

information is time-particular for the specified market condition. From the point of an

inexperienced expert in accounting, they will suffer from confusion by seeing changes in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

market situation to determine the trend of profitability of the firm (Yao, Percy and Hu, 2015).

To obtain reliable information the expert must request for a new financial statement.

Conversely, it would result expensive for the company if this request is frequently made. It is

potential that an experienced expertise is capable of considering the changing conditions of

the business; as in that case the individual will solve and understand the process in using the

fair value, without requesting for a new financial statement.

Misleading Information

It is likely that often the asset’s noticeable value is not pinpointing the asset’s real

value. The market may be ineffective and does not show in its approximate all openly

provided information. Some factors could impact the market estimate to get diverge, such as

behavioural bias or investor absurdity (Barth, 2013). In addition to, standard states that the

liquidity of market is significant matter; it is because reach can be as large as it can cause

considerable uncertainty regarding fair value and thus set up large total value deviation in the

financial statements.

Volatility

The major issue of volatility is concerned with the prior problem of limited and

minimum reliability. In a situation where the asset’s fair value chases the market environment

improvement, then the asset’s value also changes with the change in the market. A market’s

volatility is an existing risk as well as opportunity, thus generates a surplus risk and might

adversely influence firm’s investment ability (Malone, Tarca and Wee, 2016). In accordance

with the research carried out by experts of European Central Bank’s for the assets and

liabilities found to maturity, in the financial statements the volatility observed is fake and can

result deceptive, so any of the deviation occurred from the cost would be compensated for a

lifetime of the financial mechanism.

While considering the fair value information’s quality, the primary thing to consider

is either the information will result useful to investors or not. The main purpose of financial

reporting is to available useful information to creditors, investors and the ones who make

investments, credit and alike resource allotment decisions. Further, the users contain a wide

range of subjects, the FASB and IASB aims at the requirements of capital market

participants.

To obtain reliable information the expert must request for a new financial statement.

Conversely, it would result expensive for the company if this request is frequently made. It is

potential that an experienced expertise is capable of considering the changing conditions of

the business; as in that case the individual will solve and understand the process in using the

fair value, without requesting for a new financial statement.

Misleading Information

It is likely that often the asset’s noticeable value is not pinpointing the asset’s real

value. The market may be ineffective and does not show in its approximate all openly

provided information. Some factors could impact the market estimate to get diverge, such as

behavioural bias or investor absurdity (Barth, 2013). In addition to, standard states that the

liquidity of market is significant matter; it is because reach can be as large as it can cause

considerable uncertainty regarding fair value and thus set up large total value deviation in the

financial statements.

Volatility

The major issue of volatility is concerned with the prior problem of limited and

minimum reliability. In a situation where the asset’s fair value chases the market environment

improvement, then the asset’s value also changes with the change in the market. A market’s

volatility is an existing risk as well as opportunity, thus generates a surplus risk and might

adversely influence firm’s investment ability (Malone, Tarca and Wee, 2016). In accordance

with the research carried out by experts of European Central Bank’s for the assets and

liabilities found to maturity, in the financial statements the volatility observed is fake and can

result deceptive, so any of the deviation occurred from the cost would be compensated for a

lifetime of the financial mechanism.

While considering the fair value information’s quality, the primary thing to consider

is either the information will result useful to investors or not. The main purpose of financial

reporting is to available useful information to creditors, investors and the ones who make

investments, credit and alike resource allotment decisions. Further, the users contain a wide

range of subjects, the FASB and IASB aims at the requirements of capital market

participants.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

This part of the study shows that despite complete standard there are significant

limitations associated with the measurement and disclosure of fair values such as Limited

reliability, Misleading Information and Volatility. To cope up with these limitations,

reporting entities are required to apply this standard by considering viable disclosure and

other relevant accounting judgements.

This part of the study shows that despite complete standard there are significant

limitations associated with the measurement and disclosure of fair values such as Limited

reliability, Misleading Information and Volatility. To cope up with these limitations,

reporting entities are required to apply this standard by considering viable disclosure and

other relevant accounting judgements.

Bibliography

AASB Standard. 2015. Fair value measurement. [PDF]. Available through

<http://www.aasb.gov.au/admin/file/content105/c9/AASB13_08-15.pdf>. [Accessed on 31st

August 2017].

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Freeman, W., Wells, P. and Wyatt, A., 2017. Measurement Model or Asset Type: Evidence

from an Evaluation of the Relevance of Financial Assets. Abacus, 53(2), pp.180-210.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Majercakova, D. and Skoda, M., 2015. Fair value in financial statements after financial

crisis. Journal of Applied Accounting Research, 16(3), pp.312-332.

Malone, L., Tarca, A. and Wee, M., 2016. IFRS non‐GAAP earnings disclosures and fair

value measurement. Accounting & Finance, 56(1), pp.59-97.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

AASB Standard. 2015. Fair value measurement. [PDF]. Available through

<http://www.aasb.gov.au/admin/file/content105/c9/AASB13_08-15.pdf>. [Accessed on 31st

August 2017].

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Freeman, W., Wells, P. and Wyatt, A., 2017. Measurement Model or Asset Type: Evidence

from an Evaluation of the Relevance of Financial Assets. Abacus, 53(2), pp.180-210.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Majercakova, D. and Skoda, M., 2015. Fair value in financial statements after financial

crisis. Journal of Applied Accounting Research, 16(3), pp.312-332.

Malone, L., Tarca, A. and Wee, M., 2016. IFRS non‐GAAP earnings disclosures and fair

value measurement. Accounting & Finance, 56(1), pp.59-97.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.