Financial Accounting Report: Regulations, Conventions, and Statements

VerifiedAdded on 2019/12/28

|41

|5576

|222

Report

AI Summary

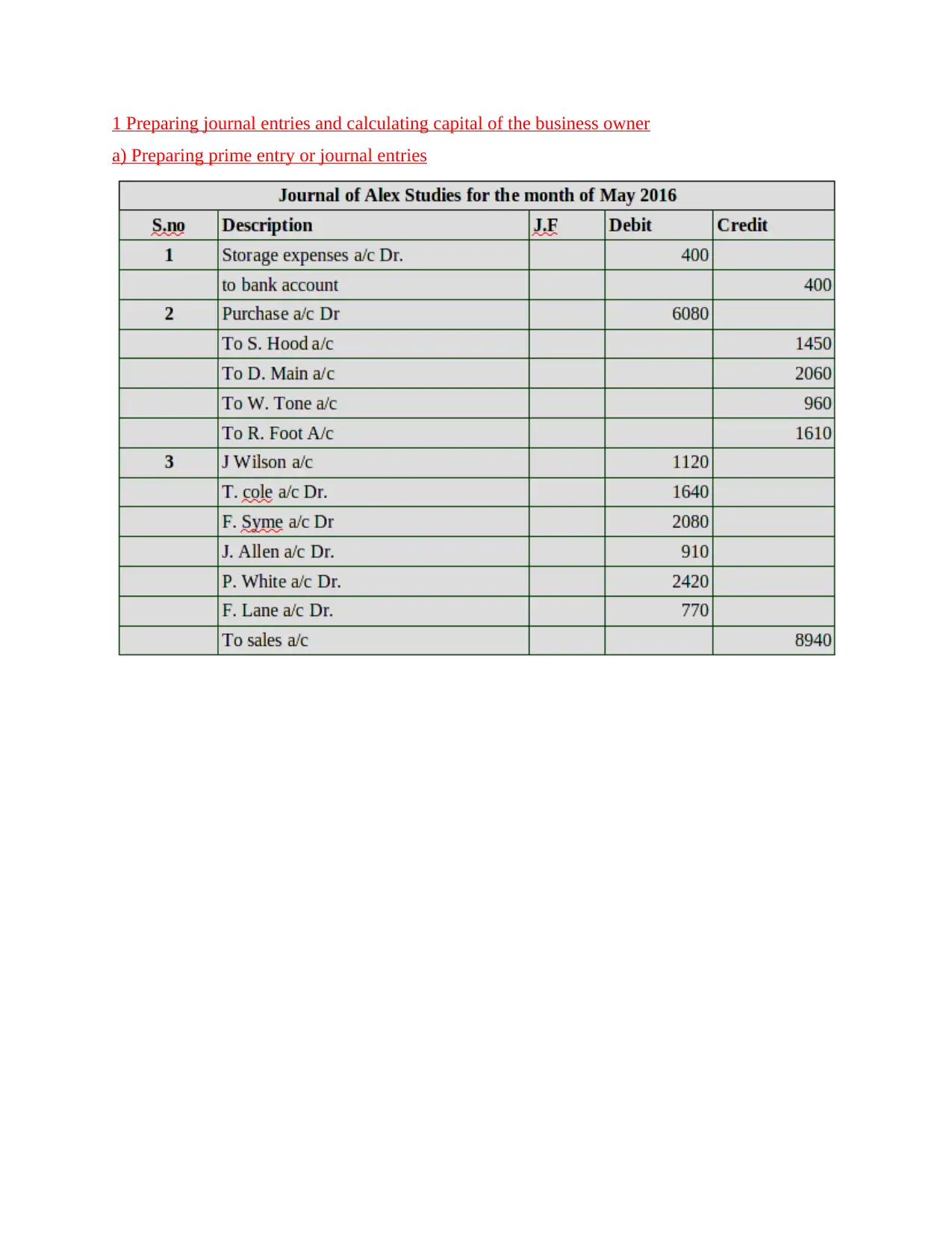

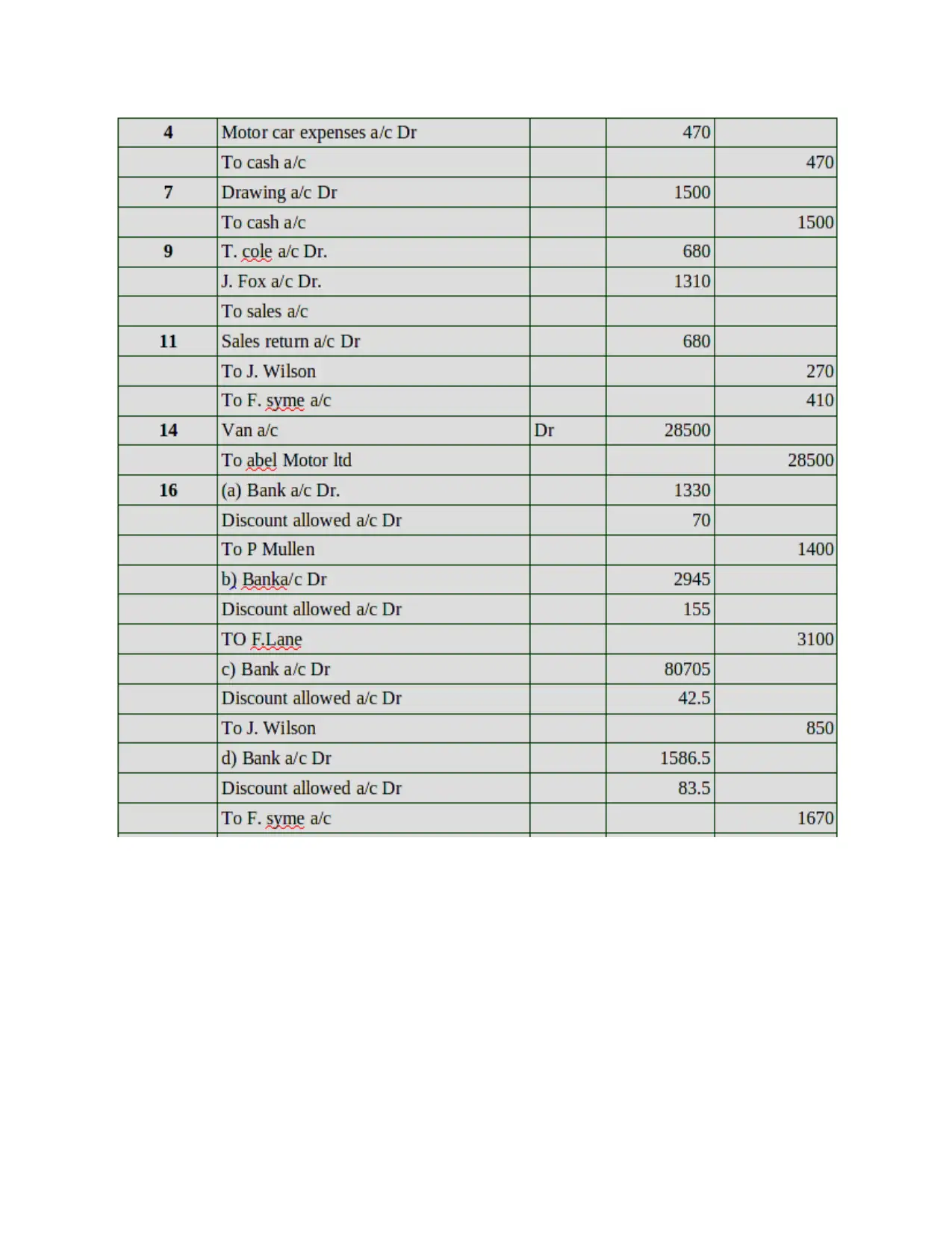

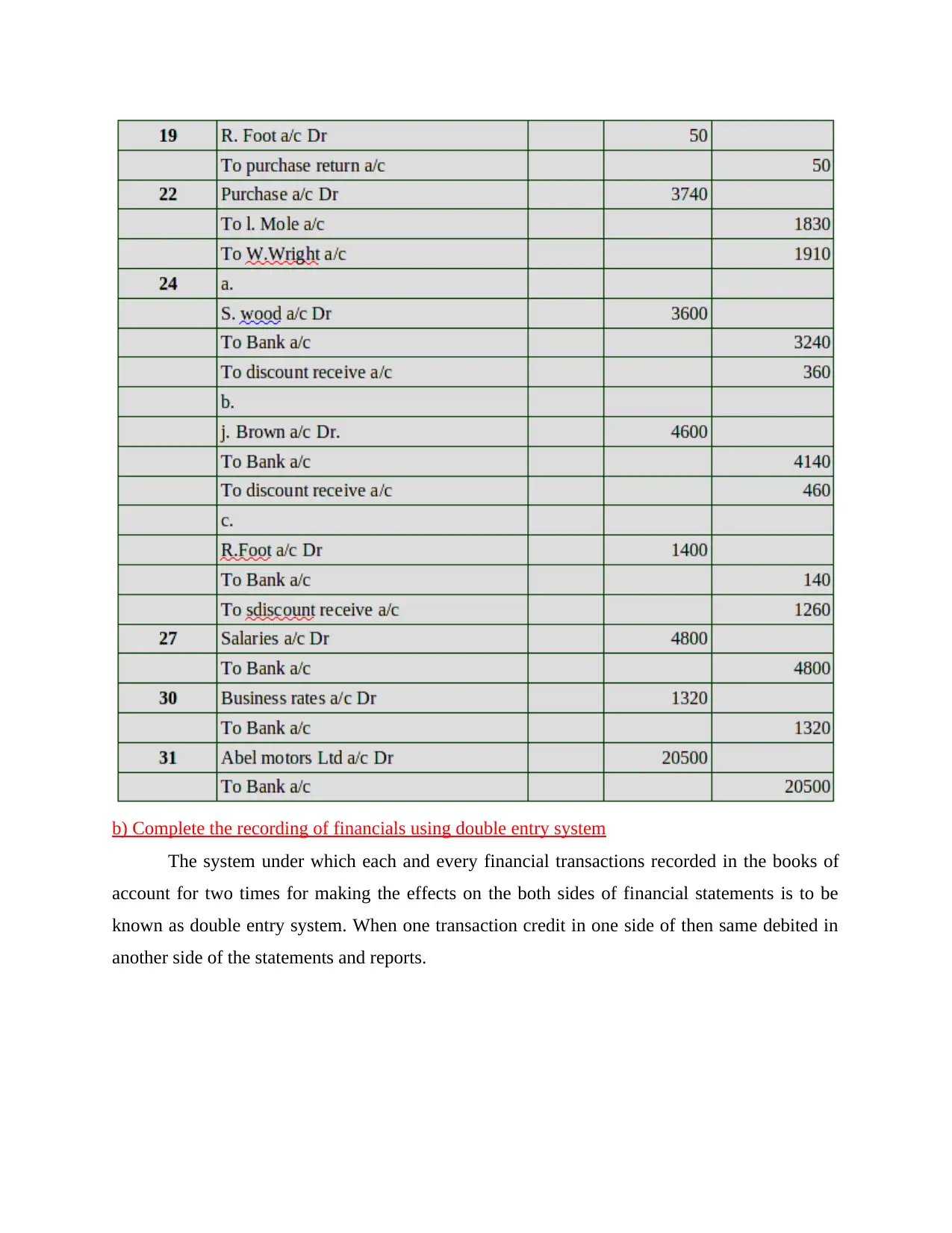

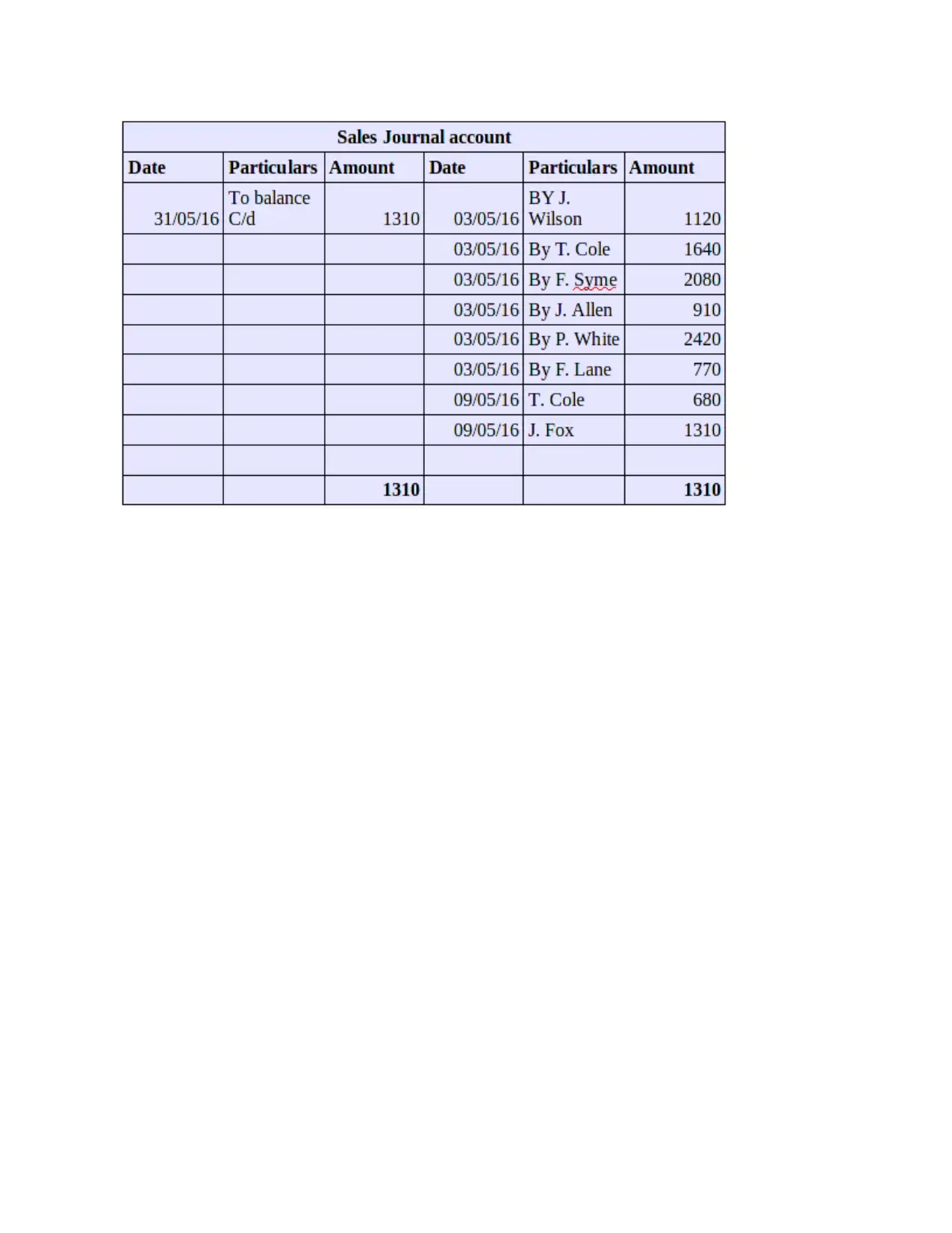

This report provides a comprehensive overview of financial accounting, covering fundamental concepts, regulations, and practical applications. It begins with a definition of financial accounting, emphasizing its role in recording, reporting, and presenting financial performance, and highlights the importance of tools like balance sheets, income statements, and journal entries. The report then delves into the regulations governing financial accounting, including International Financial Reporting Standards (IFRS) and the Accounting Standards Board (ASB), outlining their impact on financial reporting and decision-making. It also explores key accounting principles such as the economic entity assumption, monetary unit assumption, full disclosure principles, going concern principle, and revenue recognition principle. The report further examines conventions related to consistency and material disclosure, providing guidelines for accountants. The report includes examples from client cases, demonstrating the preparation of journal entries, trial balances, profit and loss statements, and balance sheets. The report also analyzes the P&L statement of Rain Tree Ltd, demonstrating how to assess the company's profitability and financial health. This report provides a detailed understanding of financial accounting practices and their implications for business operations and decision-making.

1 out of 41

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.