Financial Accounting Report: Income Statement and Balance Sheet

VerifiedAdded on 2021/02/20

|16

|3926

|79

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles and practices. It begins with an introduction to financial accounting, defining its role in recording, summarizing, and reporting business transactions. The report then delves into the specifics of financial statements, including the income statement, balance sheet, and statement of cash flows, illustrating their components and purposes with examples. It explores the differences between the income statement and balance sheet, highlighting key items like revenue, assets, liabilities, and equity. The report also covers the statement of profit and loss, and analyzes financial statements to assess a company's financial health, ability to repay debts, and overall performance. The report includes worked examples and working notes to demonstrate how to prepare and interpret these financial statements. Finally, the report discusses the uses of financial statements for various stakeholders, such as investors and creditors, and emphasizes the importance of accurate and reliable financial reporting.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Question 2........................................................................................................................................2

Question 3........................................................................................................................................4

Question 4........................................................................................................................................7

Question 5......................................................................................................................................10

CONCLUSION .............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Question 2........................................................................................................................................2

Question 3........................................................................................................................................4

Question 4........................................................................................................................................7

Question 5......................................................................................................................................10

CONCLUSION .............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION

Financial accounting is really the method by which the countless transactions arising

from company activities are recorded, summarized and reported throughout a number of years

(Financial reporting, 2019). These operations are described in the preparing of annual reports

which document the working efficiency of the corporation over a defined period, such as the

statement of financial position, income statement and cash flow statement. The choice of

accounting standards used during financial reporting relies on the legislative and reporting

demands faced by the company. It is essential to note that the aim of economic accounting is not

just to disclose a company value. Financial accounting norms in particular, rigorous guidelines

should be applied to ensure that financial disclosures are helpful and of excellent quality. The

aim of report is to provide information to managers to assess the actual financial condition.

Under report, compare between balance sheet and income statement is mentioned. As

well as multiple components of the remark of bank reconciliation and how to reconcile check

and suspense records.

Question 1

Income statement: This statement's shows the financial outcomes of a business during a

particular time frame. It discloses the amount of income generated and expenses incurred by a

company to run operation in effective manner and maintain a proper net profit throughout the

year (Dayanandan and et.al., 2016). There are number of item that are part of income statement's

such as:

Revenue

Tax expenditure

Post profit before deducting tax for discounted operations

Profit or loss at the end of year.

Other comprehensive income which are divided intro different component.

Total comprehensive revenue.

Financial statements of Sole Trader

Particulars Amount Particulars Amount

To Opening 160000 By Sales 1400000

1

Financial accounting is really the method by which the countless transactions arising

from company activities are recorded, summarized and reported throughout a number of years

(Financial reporting, 2019). These operations are described in the preparing of annual reports

which document the working efficiency of the corporation over a defined period, such as the

statement of financial position, income statement and cash flow statement. The choice of

accounting standards used during financial reporting relies on the legislative and reporting

demands faced by the company. It is essential to note that the aim of economic accounting is not

just to disclose a company value. Financial accounting norms in particular, rigorous guidelines

should be applied to ensure that financial disclosures are helpful and of excellent quality. The

aim of report is to provide information to managers to assess the actual financial condition.

Under report, compare between balance sheet and income statement is mentioned. As

well as multiple components of the remark of bank reconciliation and how to reconcile check

and suspense records.

Question 1

Income statement: This statement's shows the financial outcomes of a business during a

particular time frame. It discloses the amount of income generated and expenses incurred by a

company to run operation in effective manner and maintain a proper net profit throughout the

year (Dayanandan and et.al., 2016). There are number of item that are part of income statement's

such as:

Revenue

Tax expenditure

Post profit before deducting tax for discounted operations

Profit or loss at the end of year.

Other comprehensive income which are divided intro different component.

Total comprehensive revenue.

Financial statements of Sole Trader

Particulars Amount Particulars Amount

To Opening 160000 By Sales 1400000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

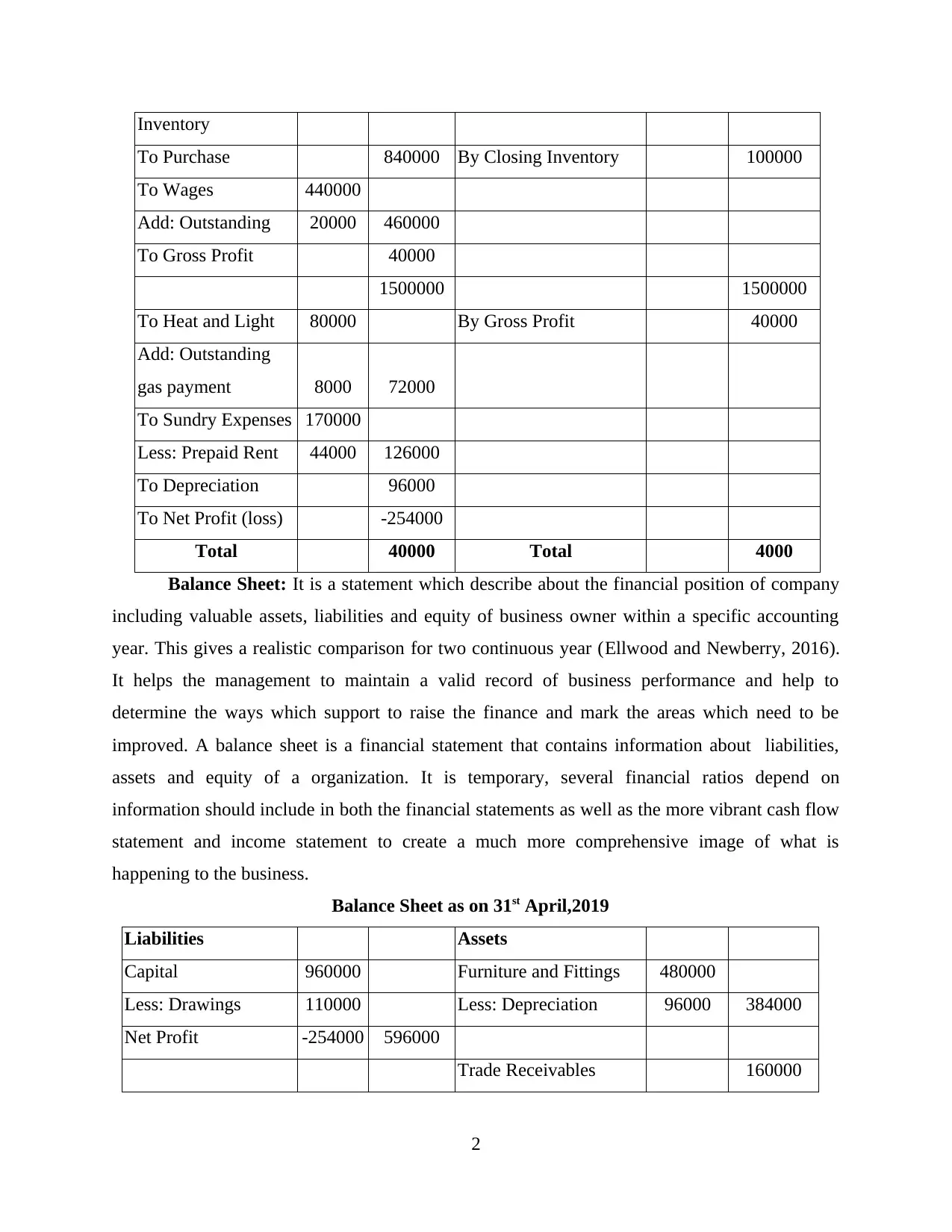

Inventory

To Purchase 840000 By Closing Inventory 100000

To Wages 440000

Add: Outstanding 20000 460000

To Gross Profit 40000

1500000 1500000

To Heat and Light 80000 By Gross Profit 40000

Add: Outstanding

gas payment 8000 72000

To Sundry Expenses 170000

Less: Prepaid Rent 44000 126000

To Depreciation 96000

To Net Profit (loss) -254000

Total 40000 Total 4000

Balance Sheet: It is a statement which describe about the financial position of company

including valuable assets, liabilities and equity of business owner within a specific accounting

year. This gives a realistic comparison for two continuous year (Ellwood and Newberry, 2016).

It helps the management to maintain a valid record of business performance and help to

determine the ways which support to raise the finance and mark the areas which need to be

improved. A balance sheet is a financial statement that contains information about liabilities,

assets and equity of a organization. It is temporary, several financial ratios depend on

information should include in both the financial statements as well as the more vibrant cash flow

statement and income statement to create a much more comprehensive image of what is

happening to the business.

Balance Sheet as on 31st April,2019

Liabilities Assets

Capital 960000 Furniture and Fittings 480000

Less: Drawings 110000 Less: Depreciation 96000 384000

Net Profit -254000 596000

Trade Receivables 160000

2

To Purchase 840000 By Closing Inventory 100000

To Wages 440000

Add: Outstanding 20000 460000

To Gross Profit 40000

1500000 1500000

To Heat and Light 80000 By Gross Profit 40000

Add: Outstanding

gas payment 8000 72000

To Sundry Expenses 170000

Less: Prepaid Rent 44000 126000

To Depreciation 96000

To Net Profit (loss) -254000

Total 40000 Total 4000

Balance Sheet: It is a statement which describe about the financial position of company

including valuable assets, liabilities and equity of business owner within a specific accounting

year. This gives a realistic comparison for two continuous year (Ellwood and Newberry, 2016).

It helps the management to maintain a valid record of business performance and help to

determine the ways which support to raise the finance and mark the areas which need to be

improved. A balance sheet is a financial statement that contains information about liabilities,

assets and equity of a organization. It is temporary, several financial ratios depend on

information should include in both the financial statements as well as the more vibrant cash flow

statement and income statement to create a much more comprehensive image of what is

happening to the business.

Balance Sheet as on 31st April,2019

Liabilities Assets

Capital 960000 Furniture and Fittings 480000

Less: Drawings 110000 Less: Depreciation 96000 384000

Net Profit -254000 596000

Trade Receivables 160000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

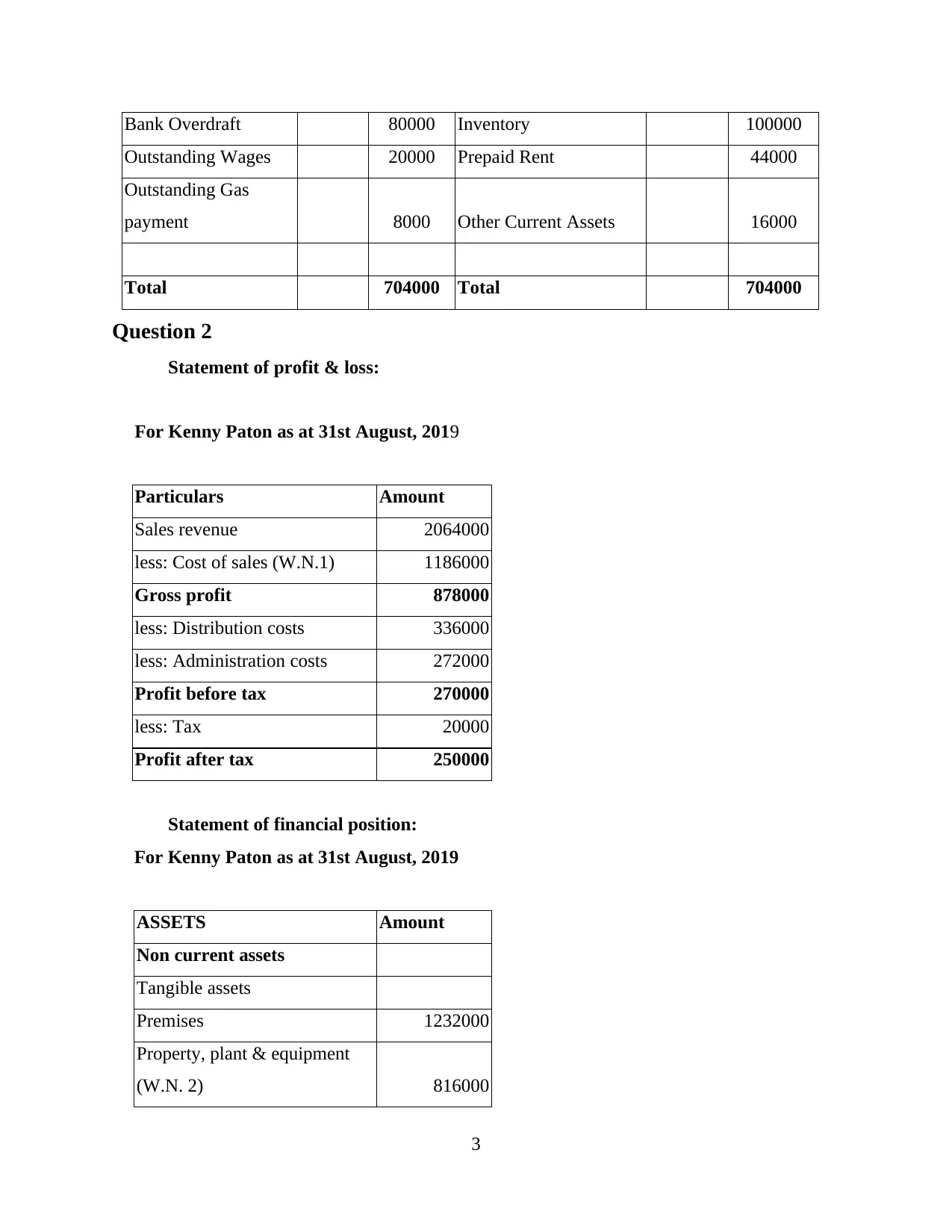

Bank Overdraft 80000 Inventory 100000

Outstanding Wages 20000 Prepaid Rent 44000

Outstanding Gas

payment 8000 Other Current Assets 16000

Total 704000 Total 704000

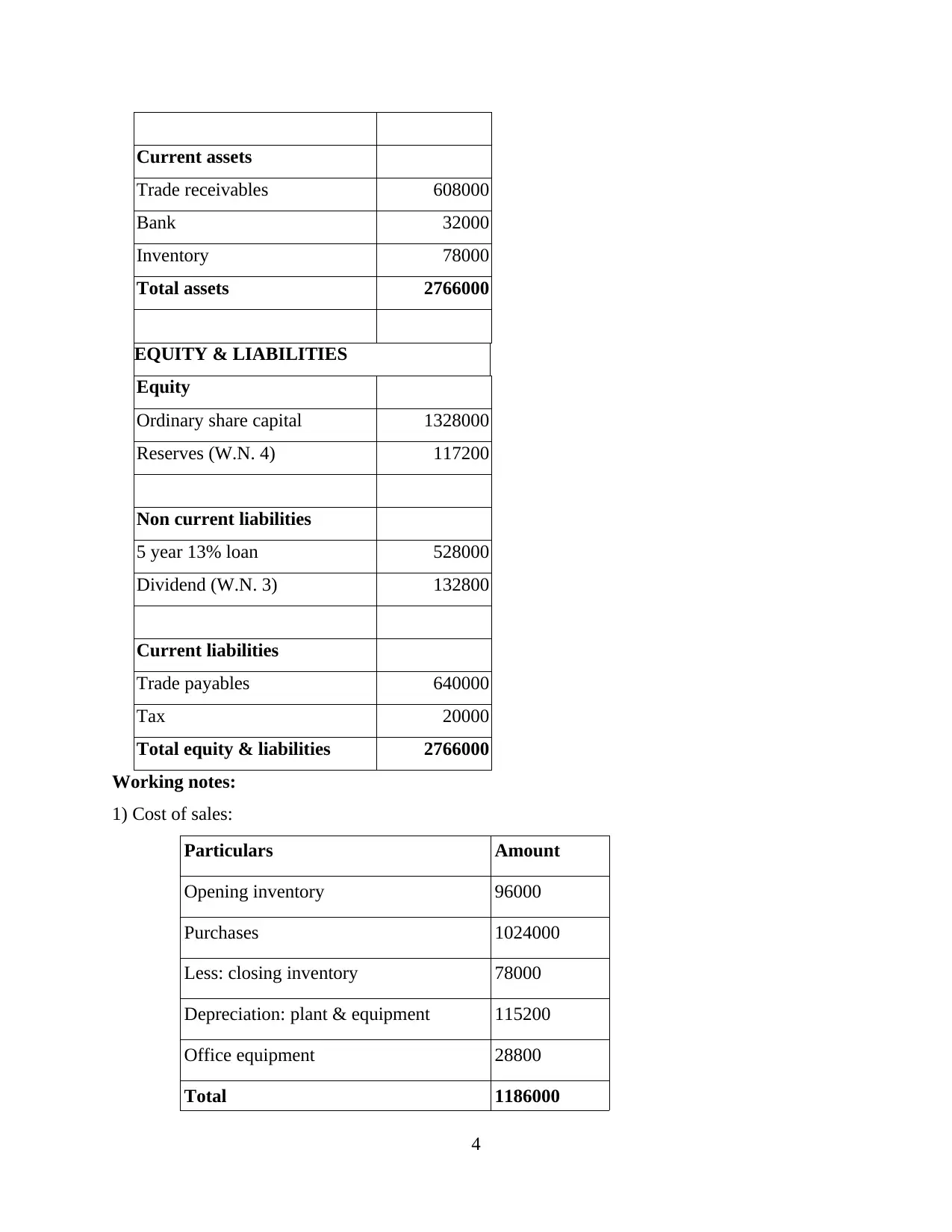

Question 2

Statement of profit & loss:

For Kenny Paton as at 31st August, 2019

Particulars Amount

Sales revenue 2064000

less: Cost of sales (W.N.1) 1186000

Gross profit 878000

less: Distribution costs 336000

less: Administration costs 272000

Profit before tax 270000

less: Tax 20000

Profit after tax 250000

Statement of financial position:

For Kenny Paton as at 31st August, 2019

ASSETS Amount

Non current assets

Tangible assets

Premises 1232000

Property, plant & equipment

(W.N. 2) 816000

3

Outstanding Wages 20000 Prepaid Rent 44000

Outstanding Gas

payment 8000 Other Current Assets 16000

Total 704000 Total 704000

Question 2

Statement of profit & loss:

For Kenny Paton as at 31st August, 2019

Particulars Amount

Sales revenue 2064000

less: Cost of sales (W.N.1) 1186000

Gross profit 878000

less: Distribution costs 336000

less: Administration costs 272000

Profit before tax 270000

less: Tax 20000

Profit after tax 250000

Statement of financial position:

For Kenny Paton as at 31st August, 2019

ASSETS Amount

Non current assets

Tangible assets

Premises 1232000

Property, plant & equipment

(W.N. 2) 816000

3

Current assets

Trade receivables 608000

Bank 32000

Inventory 78000

Total assets 2766000

EQUITY & LIABILITIES

Equity

Ordinary share capital 1328000

Reserves (W.N. 4) 117200

Non current liabilities

5 year 13% loan 528000

Dividend (W.N. 3) 132800

Current liabilities

Trade payables 640000

Tax 20000

Total equity & liabilities 2766000

Working notes:

1) Cost of sales:

Particulars Amount

Opening inventory 96000

Purchases 1024000

Less: closing inventory 78000

Depreciation: plant & equipment 115200

Office equipment 28800

Total 1186000

4

Trade receivables 608000

Bank 32000

Inventory 78000

Total assets 2766000

EQUITY & LIABILITIES

Equity

Ordinary share capital 1328000

Reserves (W.N. 4) 117200

Non current liabilities

5 year 13% loan 528000

Dividend (W.N. 3) 132800

Current liabilities

Trade payables 640000

Tax 20000

Total equity & liabilities 2766000

Working notes:

1) Cost of sales:

Particulars Amount

Opening inventory 96000

Purchases 1024000

Less: closing inventory 78000

Depreciation: plant & equipment 115200

Office equipment 28800

Total 1186000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

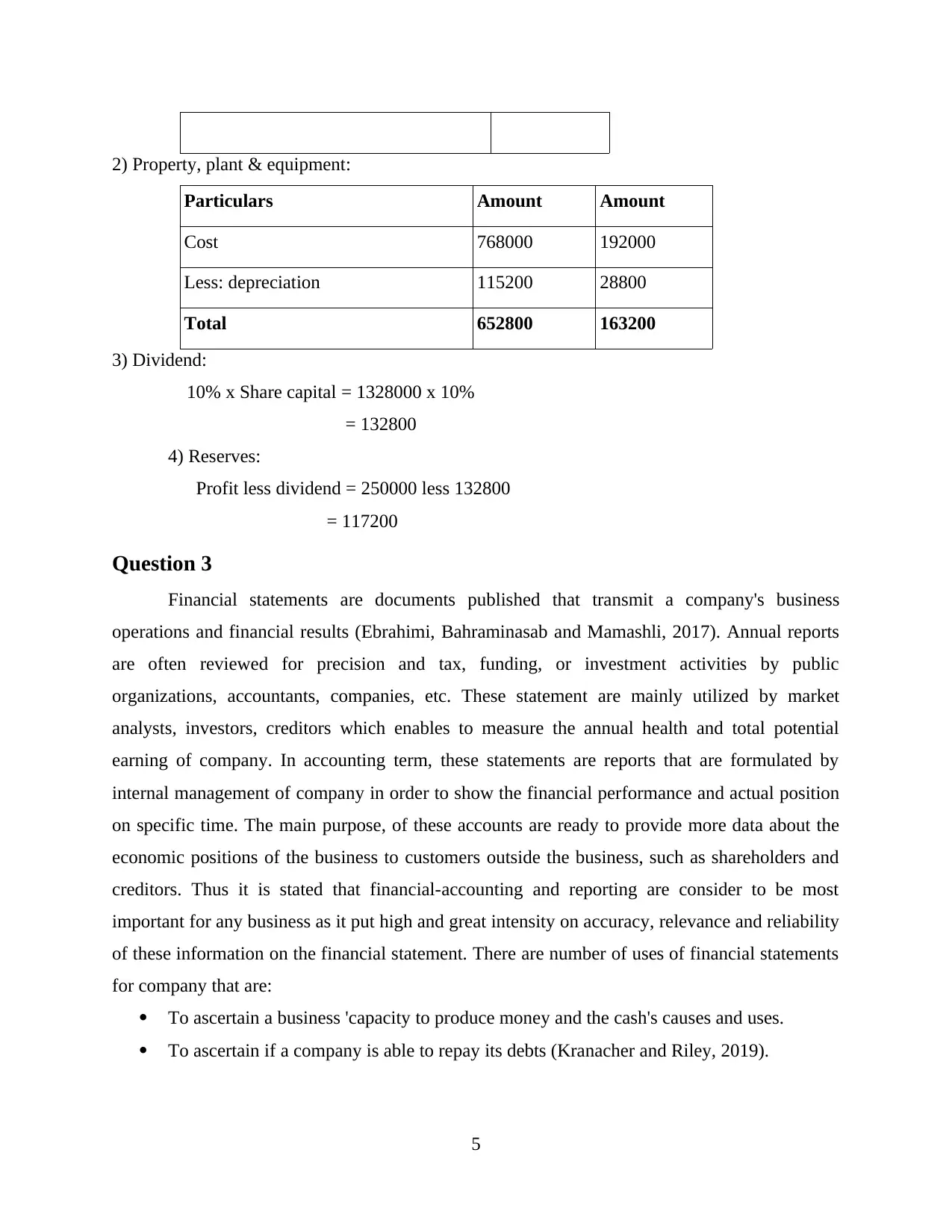

2) Property, plant & equipment:

Particulars Amount Amount

Cost 768000 192000

Less: depreciation 115200 28800

Total 652800 163200

3) Dividend:

10% x Share capital = 1328000 x 10%

= 132800

4) Reserves:

Profit less dividend = 250000 less 132800

= 117200

Question 3

Financial statements are documents published that transmit a company's business

operations and financial results (Ebrahimi, Bahraminasab and Mamashli, 2017). Annual reports

are often reviewed for precision and tax, funding, or investment activities by public

organizations, accountants, companies, etc. These statement are mainly utilized by market

analysts, investors, creditors which enables to measure the annual health and total potential

earning of company. In accounting term, these statements are reports that are formulated by

internal management of company in order to show the financial performance and actual position

on specific time. The main purpose, of these accounts are ready to provide more data about the

economic positions of the business to customers outside the business, such as shareholders and

creditors. Thus it is stated that financial-accounting and reporting are consider to be most

important for any business as it put high and great intensity on accuracy, relevance and reliability

of these information on the financial statement. There are number of uses of financial statements

for company that are:

To ascertain a business 'capacity to produce money and the cash's causes and uses.

To ascertain if a company is able to repay its debts (Kranacher and Riley, 2019).

5

Particulars Amount Amount

Cost 768000 192000

Less: depreciation 115200 28800

Total 652800 163200

3) Dividend:

10% x Share capital = 1328000 x 10%

= 132800

4) Reserves:

Profit less dividend = 250000 less 132800

= 117200

Question 3

Financial statements are documents published that transmit a company's business

operations and financial results (Ebrahimi, Bahraminasab and Mamashli, 2017). Annual reports

are often reviewed for precision and tax, funding, or investment activities by public

organizations, accountants, companies, etc. These statement are mainly utilized by market

analysts, investors, creditors which enables to measure the annual health and total potential

earning of company. In accounting term, these statements are reports that are formulated by

internal management of company in order to show the financial performance and actual position

on specific time. The main purpose, of these accounts are ready to provide more data about the

economic positions of the business to customers outside the business, such as shareholders and

creditors. Thus it is stated that financial-accounting and reporting are consider to be most

important for any business as it put high and great intensity on accuracy, relevance and reliability

of these information on the financial statement. There are number of uses of financial statements

for company that are:

To ascertain a business 'capacity to produce money and the cash's causes and uses.

To ascertain if a company is able to repay its debts (Kranacher and Riley, 2019).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To monitor economic outcomes on a long term trend to identify any future problems with

revenue growth.

To obtain financial proportions from assessments that may show the business's situation.

To Examine the information of certain company operations as described in the statements

accompanying disclosures.

There are different type of financial statement' that are basically prepared by management

of company such as:

Balance sheet: This use to show the company assets, liabilities and shareholder equity on

the certain specific date. The main importance of balance sheet is that it does not display

the information which covers a period of moment.

Income statement: It demonstrates the outcomes for both the current period of the

individual's personal procedures and economic activities. It involves income,

expenditures, profits, and losses.

Statement of cash flows: It display the alteration in the business firm cash flows during

the reporting period of time. It is a financial statement that offers historical data across all

cash flows received by a corporation from its continuing operations and alternative

sources of expenditure. It also involves all money outflows during a specified time pay

for business operations and securities. There are three section of this statements that are

discussed below:

1. Operating Activities: These activities are related to those activities which is basically

related with cash flow from current assets and liabilities during an accounting year

(Kwok, 2017).

2. Investing Activities: It is related with any cash flow that have been generated from

acquisition and disposal of investment which are not consider as the part of cash

equivalent and long term assets.

3. Financing Activities: It is related to the capacity and composition of equity amount or

certain borrowing of respective firm that are bonds, dividend and stock.

Supplementary notes: Includes descriptions of different operations, extra details on some

records and other things as prescribed by the relevant accounting structure, such as

GAAP or IFRS.

6

revenue growth.

To obtain financial proportions from assessments that may show the business's situation.

To Examine the information of certain company operations as described in the statements

accompanying disclosures.

There are different type of financial statement' that are basically prepared by management

of company such as:

Balance sheet: This use to show the company assets, liabilities and shareholder equity on

the certain specific date. The main importance of balance sheet is that it does not display

the information which covers a period of moment.

Income statement: It demonstrates the outcomes for both the current period of the

individual's personal procedures and economic activities. It involves income,

expenditures, profits, and losses.

Statement of cash flows: It display the alteration in the business firm cash flows during

the reporting period of time. It is a financial statement that offers historical data across all

cash flows received by a corporation from its continuing operations and alternative

sources of expenditure. It also involves all money outflows during a specified time pay

for business operations and securities. There are three section of this statements that are

discussed below:

1. Operating Activities: These activities are related to those activities which is basically

related with cash flow from current assets and liabilities during an accounting year

(Kwok, 2017).

2. Investing Activities: It is related with any cash flow that have been generated from

acquisition and disposal of investment which are not consider as the part of cash

equivalent and long term assets.

3. Financing Activities: It is related to the capacity and composition of equity amount or

certain borrowing of respective firm that are bonds, dividend and stock.

Supplementary notes: Includes descriptions of different operations, extra details on some

records and other things as prescribed by the relevant accounting structure, such as

GAAP or IFRS.

6

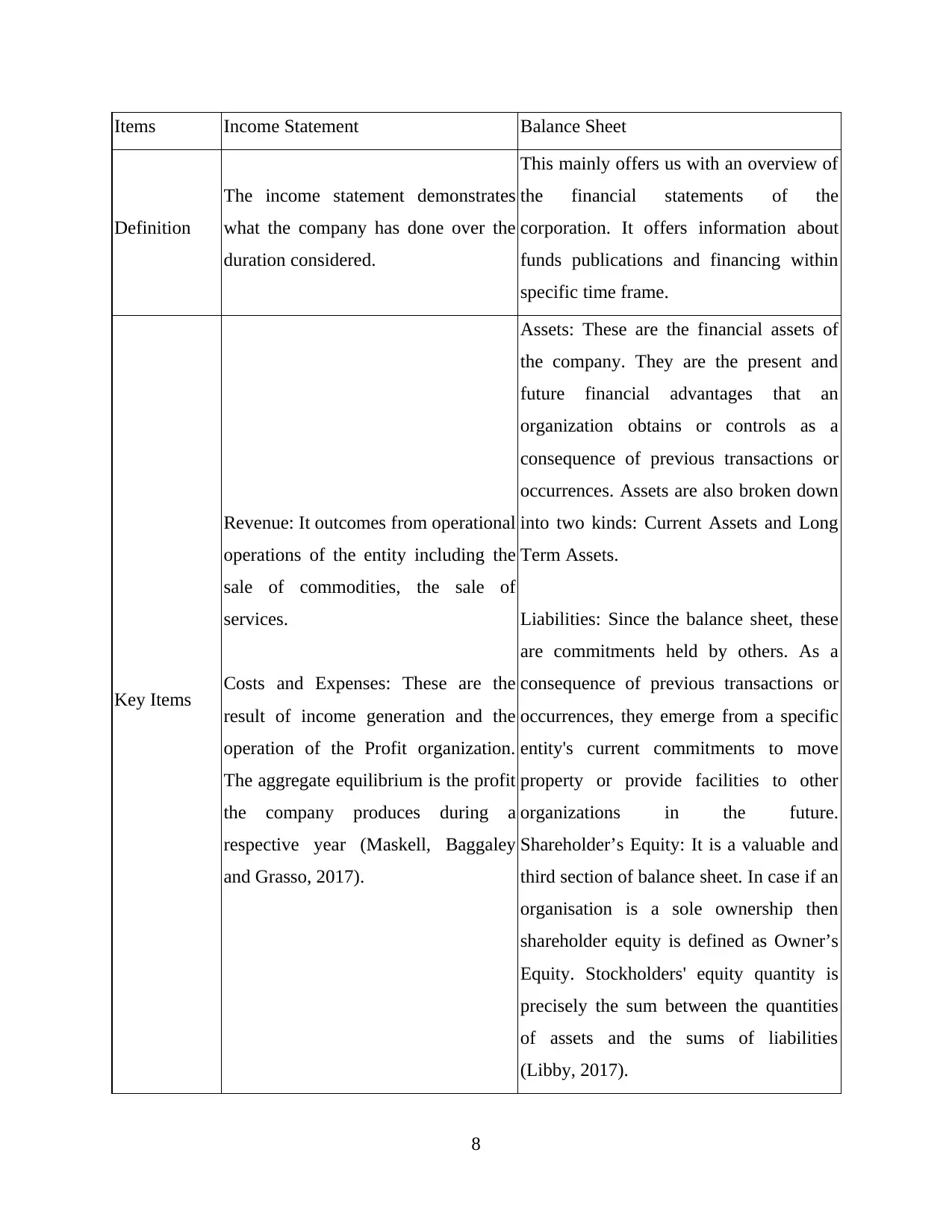

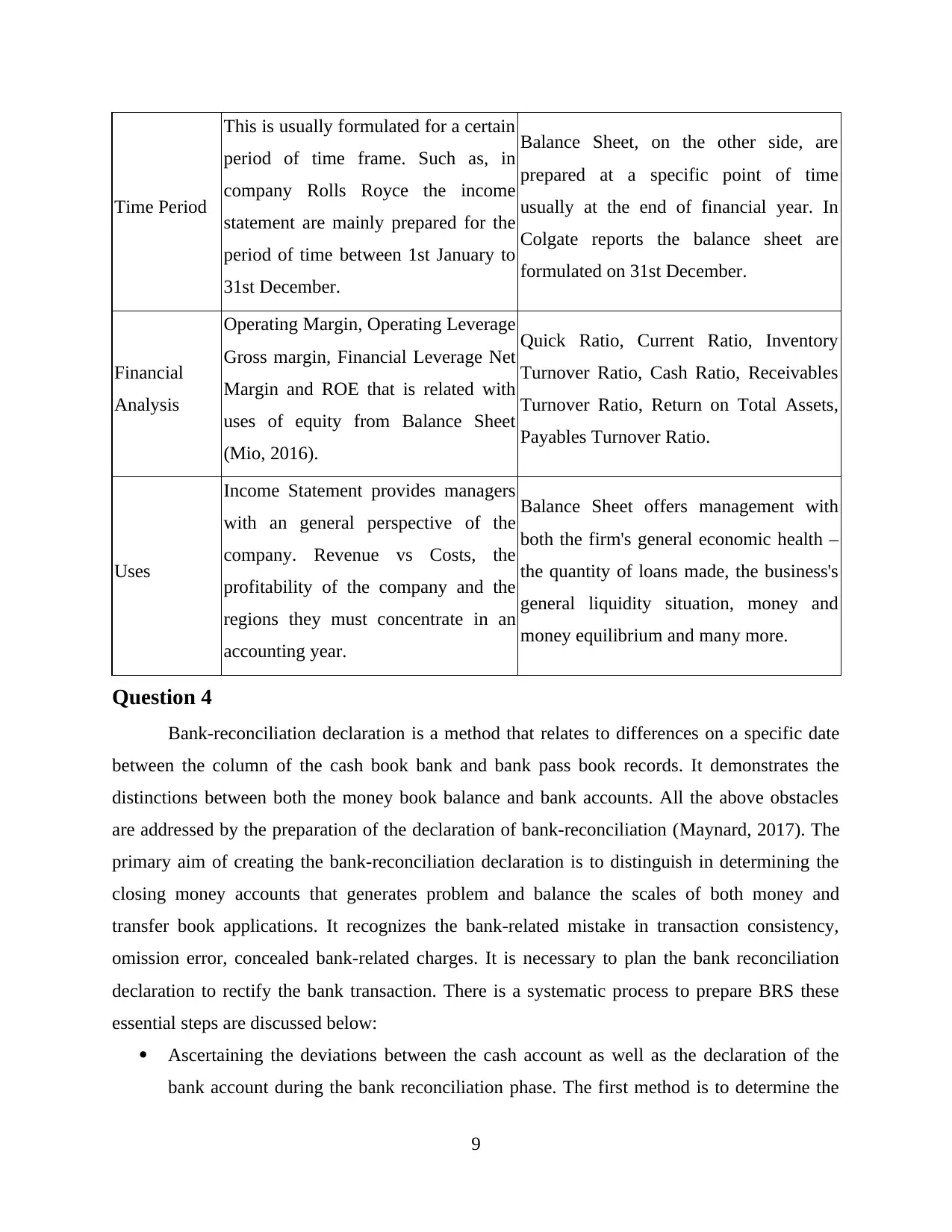

Difference between income statement and balance sheet:

7

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Items Income Statement Balance Sheet

Definition

The income statement demonstrates

what the company has done over the

duration considered.

This mainly offers us with an overview of

the financial statements of the

corporation. It offers information about

funds publications and financing within

specific time frame.

Key Items

Revenue: It outcomes from operational

operations of the entity including the

sale of commodities, the sale of

services.

Costs and Expenses: These are the

result of income generation and the

operation of the Profit organization.

The aggregate equilibrium is the profit

the company produces during a

respective year (Maskell, Baggaley

and Grasso, 2017).

Assets: These are the financial assets of

the company. They are the present and

future financial advantages that an

organization obtains or controls as a

consequence of previous transactions or

occurrences. Assets are also broken down

into two kinds: Current Assets and Long

Term Assets.

Liabilities: Since the balance sheet, these

are commitments held by others. As a

consequence of previous transactions or

occurrences, they emerge from a specific

entity's current commitments to move

property or provide facilities to other

organizations in the future.

Shareholder’s Equity: It is a valuable and

third section of balance sheet. In case if an

organisation is a sole ownership then

shareholder equity is defined as Owner’s

Equity. Stockholders' equity quantity is

precisely the sum between the quantities

of assets and the sums of liabilities

(Libby, 2017).

8

Definition

The income statement demonstrates

what the company has done over the

duration considered.

This mainly offers us with an overview of

the financial statements of the

corporation. It offers information about

funds publications and financing within

specific time frame.

Key Items

Revenue: It outcomes from operational

operations of the entity including the

sale of commodities, the sale of

services.

Costs and Expenses: These are the

result of income generation and the

operation of the Profit organization.

The aggregate equilibrium is the profit

the company produces during a

respective year (Maskell, Baggaley

and Grasso, 2017).

Assets: These are the financial assets of

the company. They are the present and

future financial advantages that an

organization obtains or controls as a

consequence of previous transactions or

occurrences. Assets are also broken down

into two kinds: Current Assets and Long

Term Assets.

Liabilities: Since the balance sheet, these

are commitments held by others. As a

consequence of previous transactions or

occurrences, they emerge from a specific

entity's current commitments to move

property or provide facilities to other

organizations in the future.

Shareholder’s Equity: It is a valuable and

third section of balance sheet. In case if an

organisation is a sole ownership then

shareholder equity is defined as Owner’s

Equity. Stockholders' equity quantity is

precisely the sum between the quantities

of assets and the sums of liabilities

(Libby, 2017).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Time Period

This is usually formulated for a certain

period of time frame. Such as, in

company Rolls Royce the income

statement are mainly prepared for the

period of time between 1st January to

31st December.

Balance Sheet, on the other side, are

prepared at a specific point of time

usually at the end of financial year. In

Colgate reports the balance sheet are

formulated on 31st December.

Financial

Analysis

Operating Margin, Operating Leverage

Gross margin, Financial Leverage Net

Margin and ROE that is related with

uses of equity from Balance Sheet

(Mio, 2016).

Quick Ratio, Current Ratio, Inventory

Turnover Ratio, Cash Ratio, Receivables

Turnover Ratio, Return on Total Assets,

Payables Turnover Ratio.

Uses

Income Statement provides managers

with an general perspective of the

company. Revenue vs Costs, the

profitability of the company and the

regions they must concentrate in an

accounting year.

Balance Sheet offers management with

both the firm's general economic health –

the quantity of loans made, the business's

general liquidity situation, money and

money equilibrium and many more.

Question 4

Bank-reconciliation declaration is a method that relates to differences on a specific date

between the column of the cash book bank and bank pass book records. It demonstrates the

distinctions between both the money book balance and bank accounts. All the above obstacles

are addressed by the preparation of the declaration of bank-reconciliation (Maynard, 2017). The

primary aim of creating the bank-reconciliation declaration is to distinguish in determining the

closing money accounts that generates problem and balance the scales of both money and

transfer book applications. It recognizes the bank-related mistake in transaction consistency,

omission error, concealed bank-related charges. It is necessary to plan the bank reconciliation

declaration to rectify the bank transaction. There is a systematic process to prepare BRS these

essential steps are discussed below:

Ascertaining the deviations between the cash account as well as the declaration of the

bank account during the bank reconciliation phase. The first method is to determine the

9

This is usually formulated for a certain

period of time frame. Such as, in

company Rolls Royce the income

statement are mainly prepared for the

period of time between 1st January to

31st December.

Balance Sheet, on the other side, are

prepared at a specific point of time

usually at the end of financial year. In

Colgate reports the balance sheet are

formulated on 31st December.

Financial

Analysis

Operating Margin, Operating Leverage

Gross margin, Financial Leverage Net

Margin and ROE that is related with

uses of equity from Balance Sheet

(Mio, 2016).

Quick Ratio, Current Ratio, Inventory

Turnover Ratio, Cash Ratio, Receivables

Turnover Ratio, Return on Total Assets,

Payables Turnover Ratio.

Uses

Income Statement provides managers

with an general perspective of the

company. Revenue vs Costs, the

profitability of the company and the

regions they must concentrate in an

accounting year.

Balance Sheet offers management with

both the firm's general economic health –

the quantity of loans made, the business's

general liquidity situation, money and

money equilibrium and many more.

Question 4

Bank-reconciliation declaration is a method that relates to differences on a specific date

between the column of the cash book bank and bank pass book records. It demonstrates the

distinctions between both the money book balance and bank accounts. All the above obstacles

are addressed by the preparation of the declaration of bank-reconciliation (Maynard, 2017). The

primary aim of creating the bank-reconciliation declaration is to distinguish in determining the

closing money accounts that generates problem and balance the scales of both money and

transfer book applications. It recognizes the bank-related mistake in transaction consistency,

omission error, concealed bank-related charges. It is necessary to plan the bank reconciliation

declaration to rectify the bank transaction. There is a systematic process to prepare BRS these

essential steps are discussed below:

Ascertaining the deviations between the cash account as well as the declaration of the

bank account during the bank reconciliation phase. The first method is to determine the

9

gaps between both the money transfer with the information of the bank as well as the

variations in the quantity to be entered in this declaration.

It help to observe the cash book submissions that are not on the banking account

declaration. Even more this method is use to discover out which money transaction is not

on the bank statement. These transactions are also very useful in creating the declaration

about the Bank's reconciliation (Renz and Herman, 2016).

Making the change with some of those transactions which are not available throughout

the cash ledger by using account books to make the bank payment. The products are like

bank charges, collected cash interest, overhead interest.

Forming a bank-reconciliation declaration by changing those transactions that understand

the relationship that is done by reviewing all of the above mentioned points, the bank

transfer should be included in the money book submitted in the bank records when

preparing the bank reconciliation declaration. In order to produce the listings which are

not shown in the cash books or even that make the disparities between the cash and bank

transfer book, it really is necessary to make adjustments by the number of variations.

The main tag-line of BRS anticipation is to evaluate and identify the main reason for the

distinction in these scales. It also acknowledges any mistakes in transactions and

equilibrium, miss characterizations, hidden defects and inaccuracies (Rikhardsson, 2017).

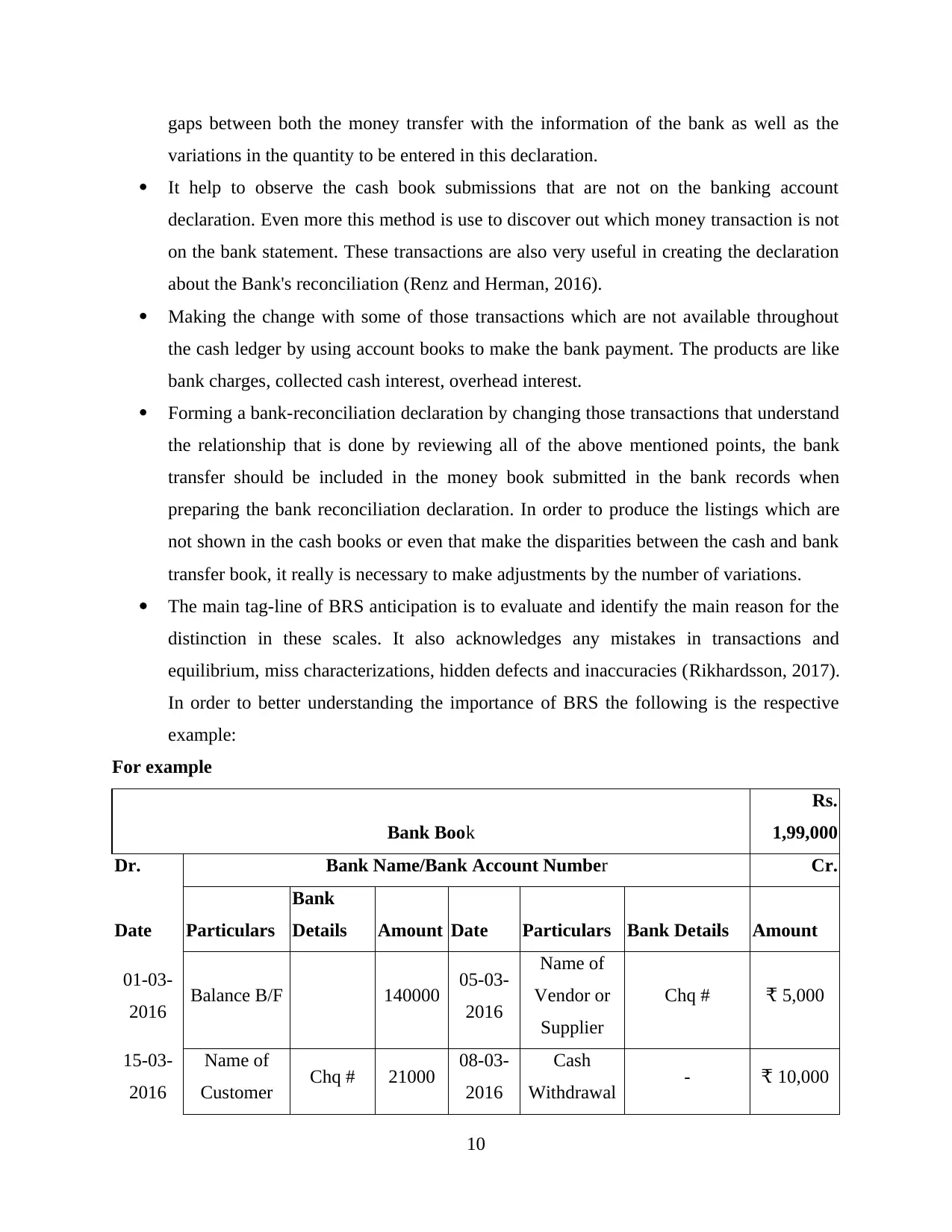

In order to better understanding the importance of BRS the following is the respective

example:

For example

Bank Book

Rs.

1,99,000

Dr. Bank Name/Bank Account Number Cr.

Date Particulars

Bank

Details Amount Date Particulars Bank Details Amount

01-03-

2016 Balance B/F 140000 05-03-

2016

Name of

Vendor or

Supplier

Chq # ₹ 5,000

15-03-

2016

Name of

Customer Chq # 21000 08-03-

2016

Cash

Withdrawal - ₹ 10,000

10

variations in the quantity to be entered in this declaration.

It help to observe the cash book submissions that are not on the banking account

declaration. Even more this method is use to discover out which money transaction is not

on the bank statement. These transactions are also very useful in creating the declaration

about the Bank's reconciliation (Renz and Herman, 2016).

Making the change with some of those transactions which are not available throughout

the cash ledger by using account books to make the bank payment. The products are like

bank charges, collected cash interest, overhead interest.

Forming a bank-reconciliation declaration by changing those transactions that understand

the relationship that is done by reviewing all of the above mentioned points, the bank

transfer should be included in the money book submitted in the bank records when

preparing the bank reconciliation declaration. In order to produce the listings which are

not shown in the cash books or even that make the disparities between the cash and bank

transfer book, it really is necessary to make adjustments by the number of variations.

The main tag-line of BRS anticipation is to evaluate and identify the main reason for the

distinction in these scales. It also acknowledges any mistakes in transactions and

equilibrium, miss characterizations, hidden defects and inaccuracies (Rikhardsson, 2017).

In order to better understanding the importance of BRS the following is the respective

example:

For example

Bank Book

Rs.

1,99,000

Dr. Bank Name/Bank Account Number Cr.

Date Particulars

Bank

Details Amount Date Particulars Bank Details Amount

01-03-

2016 Balance B/F 140000 05-03-

2016

Name of

Vendor or

Supplier

Chq # ₹ 5,000

15-03-

2016

Name of

Customer Chq # 21000 08-03-

2016

Cash

Withdrawal - ₹ 10,000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.