Financial Accounting Report on Accounting Principles and Practices

VerifiedAdded on 2020/10/05

|20

|5015

|146

Report

AI Summary

This report provides a comprehensive overview of financial accounting, encompassing its definition, regulations, and core principles. It delves into the significance of financial accounting in organizational contexts, emphasizing its role in financial planning, strategy, and decision-making by stakeholders. The report explores accounting rules, including debit and credit principles, and conventions like consistency and material disclosure. It further includes detailed client examples, such as journal entries, ledger postings, and the preparation of financial statements like profit and loss statements and bank reconciliation statements. The report references key accounting standards and boards, such as FASB, IASB, and ASB, and also offers an understanding of financial statements such as income statement, balance sheet, cash flow statement, and statement of changes in equity. Overall, this report provides a valuable resource for understanding financial accounting principles and their application in real-world scenarios.

FINANCIAL ACCOUNTING

PRINCIPLE

PRINCIPLE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

BUSINESS REPORT......................................................................................................................1

Define financial accounting........................................................................................................1

Regulations related to financial accounting................................................................................3

Describe accounting rules and principles....................................................................................4

Conventions and concepts relating to consistency and material disclosure................................5

PART B............................................................................................................................................6

CLIENT 1........................................................................................................................................6

Journal entries.............................................................................................................................6

Ledger posting.............................................................................................................................8

CLIENT 2......................................................................................................................................10

Profit and loss statement...........................................................................................................10

Financial position statement......................................................................................................11

CLIENT 3......................................................................................................................................11

Statement of profit and loss statement of Raintree Ltd ...........................................................11

CLIENT 4......................................................................................................................................14

Bank reconciliation statement...................................................................................................14

Cash book..................................................................................................................................16

CLIENT 5......................................................................................................................................17

Ledger control accounts............................................................................................................17

CLIENT 6......................................................................................................................................17

Suspense account and reconcile................................................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

BUSINESS REPORT......................................................................................................................1

Define financial accounting........................................................................................................1

Regulations related to financial accounting................................................................................3

Describe accounting rules and principles....................................................................................4

Conventions and concepts relating to consistency and material disclosure................................5

PART B............................................................................................................................................6

CLIENT 1........................................................................................................................................6

Journal entries.............................................................................................................................6

Ledger posting.............................................................................................................................8

CLIENT 2......................................................................................................................................10

Profit and loss statement...........................................................................................................10

Financial position statement......................................................................................................11

CLIENT 3......................................................................................................................................11

Statement of profit and loss statement of Raintree Ltd ...........................................................11

CLIENT 4......................................................................................................................................14

Bank reconciliation statement...................................................................................................14

Cash book..................................................................................................................................16

CLIENT 5......................................................................................................................................17

Ledger control accounts............................................................................................................17

CLIENT 6......................................................................................................................................17

Suspense account and reconcile................................................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

Financial accounting is a part of managerial accounting. It not only depends upon

managing the financial accounts and operating the financial activities but also align the

functional department of organisation. There are some financial data and information are defined

in respect of making the financial plans and strategies. with the applicable data in regards to the

monetary position and soundness of the organization by abridging and deciphering the

informations in the money related explanations of the organization, for example, articulation of

benefit and misfortune, asset report, income proclamations and far reaching wage articulation.

This data is then utilized by different partners that are associated with the organization in taking

choices in regards to whether to put resources into the future undertakings of the organization or

not (Wang, 2014). These budgetary explanations likewise helps the providers in choosing

whether or not to give the crude material to the organization by decisions subject to financial

position of organisation.

This report is bifurcated in separate two parts. First part cover the meaning of financial

accounting, accounting principles and rules are defined in this context. Accounting rules and

principles which are used in organisational context are defined in this context. Accounting

conventions and concepts are related to consistency and material disclosure are also defined in

this context.

PART A

BUSINESS REPORT

Define financial accounting

Financial accounting is considered as a format of keeping the financial records and

information in effective manner so that the desired aim and objectives can be achieved in well

organised manner. There are type of rules and principles are made in terms of making the

accounting rules and principles are also defined in this context. It is required to analyse the

essential aspects in terms of measure the financial stability and build up capital base. Financial

accounting is mandatory for organisations in order to manage the functions and the departments

of association on regular basis and daily expenses are utilised as per the availability of financial

sources and management (Vyas, 2011).

There are some responsibility remain associated with finance managers and accountants

for data used in financial accounting and principle. Finance related bookkeeping procedure

1

Financial accounting is a part of managerial accounting. It not only depends upon

managing the financial accounts and operating the financial activities but also align the

functional department of organisation. There are some financial data and information are defined

in respect of making the financial plans and strategies. with the applicable data in regards to the

monetary position and soundness of the organization by abridging and deciphering the

informations in the money related explanations of the organization, for example, articulation of

benefit and misfortune, asset report, income proclamations and far reaching wage articulation.

This data is then utilized by different partners that are associated with the organization in taking

choices in regards to whether to put resources into the future undertakings of the organization or

not (Wang, 2014). These budgetary explanations likewise helps the providers in choosing

whether or not to give the crude material to the organization by decisions subject to financial

position of organisation.

This report is bifurcated in separate two parts. First part cover the meaning of financial

accounting, accounting principles and rules are defined in this context. Accounting rules and

principles which are used in organisational context are defined in this context. Accounting

conventions and concepts are related to consistency and material disclosure are also defined in

this context.

PART A

BUSINESS REPORT

Define financial accounting

Financial accounting is considered as a format of keeping the financial records and

information in effective manner so that the desired aim and objectives can be achieved in well

organised manner. There are type of rules and principles are made in terms of making the

accounting rules and principles are also defined in this context. It is required to analyse the

essential aspects in terms of measure the financial stability and build up capital base. Financial

accounting is mandatory for organisations in order to manage the functions and the departments

of association on regular basis and daily expenses are utilised as per the availability of financial

sources and management (Vyas, 2011).

There are some responsibility remain associated with finance managers and accountants

for data used in financial accounting and principle. Finance related bookkeeping procedure

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

examines about the how budgetary exchanges are overseen and posted in the announcements so

they wind up viable in taking choices. It is introduced in the budgetary proclamations of the

organization speaks to genuine and reasonable perspective of the organization and it is

dependable for the financial specialists of the organization to take choices with respect to

whether to put resources into the organization or not. The different procedure of compromise are

talked about in this reports, for example, accounting framework, record posting framework,

planning of trial adjust and so forth. The standards of bookkeeping , significance of money

related records are additionally talked about in this undertaking report (Objectives of Financial

Accounting. 2017).

Financial accounting also considered as a process of making the financial accounts and

managing the operations and functions of business in well planned structure. The financial

accounting process is finished with utilization of certain pre decided rules which are issued by

the standard setting bodies, for example, FASB, IASB and so forth. The distinctive organizations

picks diverse bookkeeping frameworks that are set up by these standard setting bodies, for

example, US-GAAP, IFRS and so forth (Skogstad and et. al., 2011). Money related bookkeeping

is finished by keeping in see these gauges and it is the obligation of budgetary supervisors to

give the monetary proclamations moral benchmarks with the end goal that they speaks to

organizations genuine financial transactions and events. There are three main statements are

prepared by the organisation which are as follows;

Income statement: Balance sheet is the another name through which organisations are

defined in this context. this is the statement which is considered essential in terms of making the

financial accounts and variability of organisation in effective manner. All the expenses and

income which are revenue nature are considered in this statement. Sales, dividend received,

interest received are the examples of income. Depreciation, administration expenses, selling and

distribution expenses are the examples of income statement.

Financial Position statement: There are type of information remain divided in multiple

parts such as

Assets: these are considered as owners property such as inventory, plant and machinery,

cash are the main elements considered in financial statements. Liabilities: these are considered as debts which are required to paid by organisation.

There are two type of debts are found in organisational context such as short term debt

2

they wind up viable in taking choices. It is introduced in the budgetary proclamations of the

organization speaks to genuine and reasonable perspective of the organization and it is

dependable for the financial specialists of the organization to take choices with respect to

whether to put resources into the organization or not. The different procedure of compromise are

talked about in this reports, for example, accounting framework, record posting framework,

planning of trial adjust and so forth. The standards of bookkeeping , significance of money

related records are additionally talked about in this undertaking report (Objectives of Financial

Accounting. 2017).

Financial accounting also considered as a process of making the financial accounts and

managing the operations and functions of business in well planned structure. The financial

accounting process is finished with utilization of certain pre decided rules which are issued by

the standard setting bodies, for example, FASB, IASB and so forth. The distinctive organizations

picks diverse bookkeeping frameworks that are set up by these standard setting bodies, for

example, US-GAAP, IFRS and so forth (Skogstad and et. al., 2011). Money related bookkeeping

is finished by keeping in see these gauges and it is the obligation of budgetary supervisors to

give the monetary proclamations moral benchmarks with the end goal that they speaks to

organizations genuine financial transactions and events. There are three main statements are

prepared by the organisation which are as follows;

Income statement: Balance sheet is the another name through which organisations are

defined in this context. this is the statement which is considered essential in terms of making the

financial accounts and variability of organisation in effective manner. All the expenses and

income which are revenue nature are considered in this statement. Sales, dividend received,

interest received are the examples of income. Depreciation, administration expenses, selling and

distribution expenses are the examples of income statement.

Financial Position statement: There are type of information remain divided in multiple

parts such as

Assets: these are considered as owners property such as inventory, plant and machinery,

cash are the main elements considered in financial statements. Liabilities: these are considered as debts which are required to paid by organisation.

There are two type of debts are found in organisational context such as short term debt

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and long term debt. Creditors, bank overdraft, loans and debentures are the examples of

liabilities.

Cash flow statement: with the help of cash flow statements managers and accountants be

able to understand the flow of cash with in the operations and functions effectively. Cash flow is

evaluated in majorly three forms such as cash flow from operating activity, cash flow from

investing activity and cash flow form financing activity.

Change in Equity position Statement: there are changes seen in respect of analysing the

financial position of organisation and helps to determine the financial aspect. Change in equity

statement contains net profit and loss during the year from income statement, share capital issued

or repaid during the year and the dividend payments, gain or losses are also considered in terms

of equity (Scott, 2015).

Regulations related to financial accounting

There are a few standard of measurement and controls are made the degree that dealing

with the money related activities and transactions for better execution of budgetary actions.

Financial Reporting Council (FRC) are made in regard of showing budgetary data particularly

affiliation. Bookkeeping benchmarks and checks which are given by Sound accounting measures

(GAAP). This is on an extremely fundamental level remain related with caused noteworthy harm

standards, going concern, arranging rule, money related segment, importance, insurance and

immovability of money related introduction. ASB (Accounting Standard Board) in like way

gives foundations and benchmarks identified with monetary illuminations are in addition

portrayed in this uncommon condition (P Simnett and et. al., 2011.). It in like manner issues the

group decrees which gives quick bearing on the endorsed treatment of a particular trade where

unanticipated comprehension of a recommended accounting standard and treatment is required

(Biondi, and Zambon, 2013).

These standards overall urges manager and accountants to demonstrate the budgetary

information and accounting revelation of accounting systems. Models which are prepared under

ASB stay related with taking a gander at treatment of utilization and pay structure of coalition.

The main game-plan of standards was enlisted as Uniform Game arrangement of Records

(USOA) and Irish and UK GAAP issues essentials and approvals to the degree making measures

and establishments for keeping up and structure budgetary illuminations (Skogstad and et. al.,

2011). Enormous degree of bookkeeping course a significant part of the time issued to make and

3

liabilities.

Cash flow statement: with the help of cash flow statements managers and accountants be

able to understand the flow of cash with in the operations and functions effectively. Cash flow is

evaluated in majorly three forms such as cash flow from operating activity, cash flow from

investing activity and cash flow form financing activity.

Change in Equity position Statement: there are changes seen in respect of analysing the

financial position of organisation and helps to determine the financial aspect. Change in equity

statement contains net profit and loss during the year from income statement, share capital issued

or repaid during the year and the dividend payments, gain or losses are also considered in terms

of equity (Scott, 2015).

Regulations related to financial accounting

There are a few standard of measurement and controls are made the degree that dealing

with the money related activities and transactions for better execution of budgetary actions.

Financial Reporting Council (FRC) are made in regard of showing budgetary data particularly

affiliation. Bookkeeping benchmarks and checks which are given by Sound accounting measures

(GAAP). This is on an extremely fundamental level remain related with caused noteworthy harm

standards, going concern, arranging rule, money related segment, importance, insurance and

immovability of money related introduction. ASB (Accounting Standard Board) in like way

gives foundations and benchmarks identified with monetary illuminations are in addition

portrayed in this uncommon condition (P Simnett and et. al., 2011.). It in like manner issues the

group decrees which gives quick bearing on the endorsed treatment of a particular trade where

unanticipated comprehension of a recommended accounting standard and treatment is required

(Biondi, and Zambon, 2013).

These standards overall urges manager and accountants to demonstrate the budgetary

information and accounting revelation of accounting systems. Models which are prepared under

ASB stay related with taking a gander at treatment of utilization and pay structure of coalition.

The main game-plan of standards was enlisted as Uniform Game arrangement of Records

(USOA) and Irish and UK GAAP issues essentials and approvals to the degree making measures

and establishments for keeping up and structure budgetary illuminations (Skogstad and et. al.,

2011). Enormous degree of bookkeeping course a significant part of the time issued to make and

3

enlighten bookkeeping traditions by specific endeavor. Specific undertakings, as monetary guide,

annuity, keeping money and affirmation. Elucidations which are set up according to these

controls and principles are called as Statement of Recommended Practice (SORPs).

There are two or three statutes and heading moreover gave by the International

Accounting Standard board of trustees (IASC) as for organizing in 1973 (Scott, 2015). the IASC

produces bookkeeping models which are called as comprehensive bookkeeping measures (IAS).

There is a particular board is made subject to screen the exercises and the endeavor to make new

benchmarks and approvals. It is fundamental for relationship to the degree making the money

related structure in different structures. Chief focal point of legitimate experts and the

administrative bodies is to push the purposeful straightforwardness and consistency with the

money related declarations planned by relationship around the world. There is no any vitality of

law made comparatively as following the across the board cash related and bookkeeping rules for

affiliations working at authoritative level (Openshaw, 2013).

IASB is of the legitimate which issues standards, strategies and benchmarks subject to

cash related bookkeeping and bookkeeping presentation. The structure of IASB of various

sections, for example, Checking board (open capital market pros), IFRS establishment trustees,

by and large bookkeeping rules sheets, IFRS alerted chamber, IFRS understanding board. IFRS

which is known as General Budgetary Showing Models are the measures issues by IASB. GAAP

(Legitimate accounting standard) are taken after at careful level. General connection which

works business sharpens in different nations comprehend the benchmarks and proportions of ISA

and GAAP. There are techniques working party was framed in 1997 and reprimanded for

auditing with terms of structure and process.

Describe accounting rules and principles

There are three major rules are given in respect of accounting rules which are also

considered as golden rules of accounting;

1. Debit the receiver and credit the giver: The person that is suggested in this thought can

be a trademark individual and legal person. This control of accounting is material on all

the individual records with whom the associations deal on ordinary commence. In

addition, if that individual offers anything to the business then the persom is called

provider and his record is credited in the association's records. If such individual gets

4

annuity, keeping money and affirmation. Elucidations which are set up according to these

controls and principles are called as Statement of Recommended Practice (SORPs).

There are two or three statutes and heading moreover gave by the International

Accounting Standard board of trustees (IASC) as for organizing in 1973 (Scott, 2015). the IASC

produces bookkeeping models which are called as comprehensive bookkeeping measures (IAS).

There is a particular board is made subject to screen the exercises and the endeavor to make new

benchmarks and approvals. It is fundamental for relationship to the degree making the money

related structure in different structures. Chief focal point of legitimate experts and the

administrative bodies is to push the purposeful straightforwardness and consistency with the

money related declarations planned by relationship around the world. There is no any vitality of

law made comparatively as following the across the board cash related and bookkeeping rules for

affiliations working at authoritative level (Openshaw, 2013).

IASB is of the legitimate which issues standards, strategies and benchmarks subject to

cash related bookkeeping and bookkeeping presentation. The structure of IASB of various

sections, for example, Checking board (open capital market pros), IFRS establishment trustees,

by and large bookkeeping rules sheets, IFRS alerted chamber, IFRS understanding board. IFRS

which is known as General Budgetary Showing Models are the measures issues by IASB. GAAP

(Legitimate accounting standard) are taken after at careful level. General connection which

works business sharpens in different nations comprehend the benchmarks and proportions of ISA

and GAAP. There are techniques working party was framed in 1997 and reprimanded for

auditing with terms of structure and process.

Describe accounting rules and principles

There are three major rules are given in respect of accounting rules which are also

considered as golden rules of accounting;

1. Debit the receiver and credit the giver: The person that is suggested in this thought can

be a trademark individual and legal person. This control of accounting is material on all

the individual records with whom the associations deal on ordinary commence. In

addition, if that individual offers anything to the business then the persom is called

provider and his record is credited in the association's records. If such individual gets

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

anything in light of a legitimate concern for the association then he charged in the records

of the association (Bhattacharyya, 2012).

2. Debit what comes in, credit what goes out: The veritable records are related to the

advantages of the association which can either come in or go out from the business. This

accounting guideline thinks about all the certifiable records of the association. If any of

the favourable position, for instance, device and stock come into the association then this

record is charged by the lead charge what comes in (Narayanaswamy, 2017). In addition,

if the association discards or offers any advantage then the record of that particular asset

is ascribed by the association as demonstrated by the accounting block credit what goes.

3. Debit all the expenses and losses and credit all income and gains: The apparent

records are those which considers the expenses and jobs of the association. This

accounting standard ponders all the apparent records. The utilizations and adversities are

charged by the administer and the wage and grabs are credited in the association account.

Conventions and concepts relating to consistency and material disclosure

Accounting conventions are considered as uniformity subject to maintenance of accounts

and records in terms of making the plans and structure of organisation in effective manner.

Conventions indicates towards the dimensions of customs or traditions usage which are followed

from long duration.

Material disclosure: This accounting convention communicates that the budgetary

explanations of the association and the accounting trade and balances are having botches in them

(Mulford and Comiskey, 2011). Cash related clarifications are orchestrated so the customers of

them can settle on correlated decisions by using them. Thusly it is basic that the information that

is contained in the financials of the association should be done in all the material edges with the

objective that they can address the certified and sensible point of view of the budgetary

soundness of the association. In any case, is the information communicated in those declarations

are avoided or misquoted then it could affect the decisions of the customers. Materiality is

related to the size and particular conditions of the affiliations.

Consistency convention: This accounting convention communicates that the measures

and plans that are gotten by the affiliation should be unfaltering for a more drawn out period and

traverse. For example if the association is unsurprising with its gauges, and it uses FIFO stock

organization system then it will end up being straightforward for the association in

5

of the association (Bhattacharyya, 2012).

2. Debit what comes in, credit what goes out: The veritable records are related to the

advantages of the association which can either come in or go out from the business. This

accounting guideline thinks about all the certifiable records of the association. If any of

the favourable position, for instance, device and stock come into the association then this

record is charged by the lead charge what comes in (Narayanaswamy, 2017). In addition,

if the association discards or offers any advantage then the record of that particular asset

is ascribed by the association as demonstrated by the accounting block credit what goes.

3. Debit all the expenses and losses and credit all income and gains: The apparent

records are those which considers the expenses and jobs of the association. This

accounting standard ponders all the apparent records. The utilizations and adversities are

charged by the administer and the wage and grabs are credited in the association account.

Conventions and concepts relating to consistency and material disclosure

Accounting conventions are considered as uniformity subject to maintenance of accounts

and records in terms of making the plans and structure of organisation in effective manner.

Conventions indicates towards the dimensions of customs or traditions usage which are followed

from long duration.

Material disclosure: This accounting convention communicates that the budgetary

explanations of the association and the accounting trade and balances are having botches in them

(Mulford and Comiskey, 2011). Cash related clarifications are orchestrated so the customers of

them can settle on correlated decisions by using them. Thusly it is basic that the information that

is contained in the financials of the association should be done in all the material edges with the

objective that they can address the certified and sensible point of view of the budgetary

soundness of the association. In any case, is the information communicated in those declarations

are avoided or misquoted then it could affect the decisions of the customers. Materiality is

related to the size and particular conditions of the affiliations.

Consistency convention: This accounting convention communicates that the measures

and plans that are gotten by the affiliation should be unfaltering for a more drawn out period and

traverse. For example if the association is unsurprising with its gauges, and it uses FIFO stock

organization system then it will end up being straightforward for the association in

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

differentiating the inventories of prior years and the present year rather by then if the association

was clashing with its guidelines (Beatty and Liao, 2014). This must be reviewed that the whether

the connection is staying obvious with the benchmarks and models later on. Right when the

relentless accounting procedures are used by the associations in its fiscal announcements then it

winds up less requesting for the examiners and managers in differentiating it and another

associations and besides the associations financials clarifications with the prior years (Kirsch,

2012).

PART B

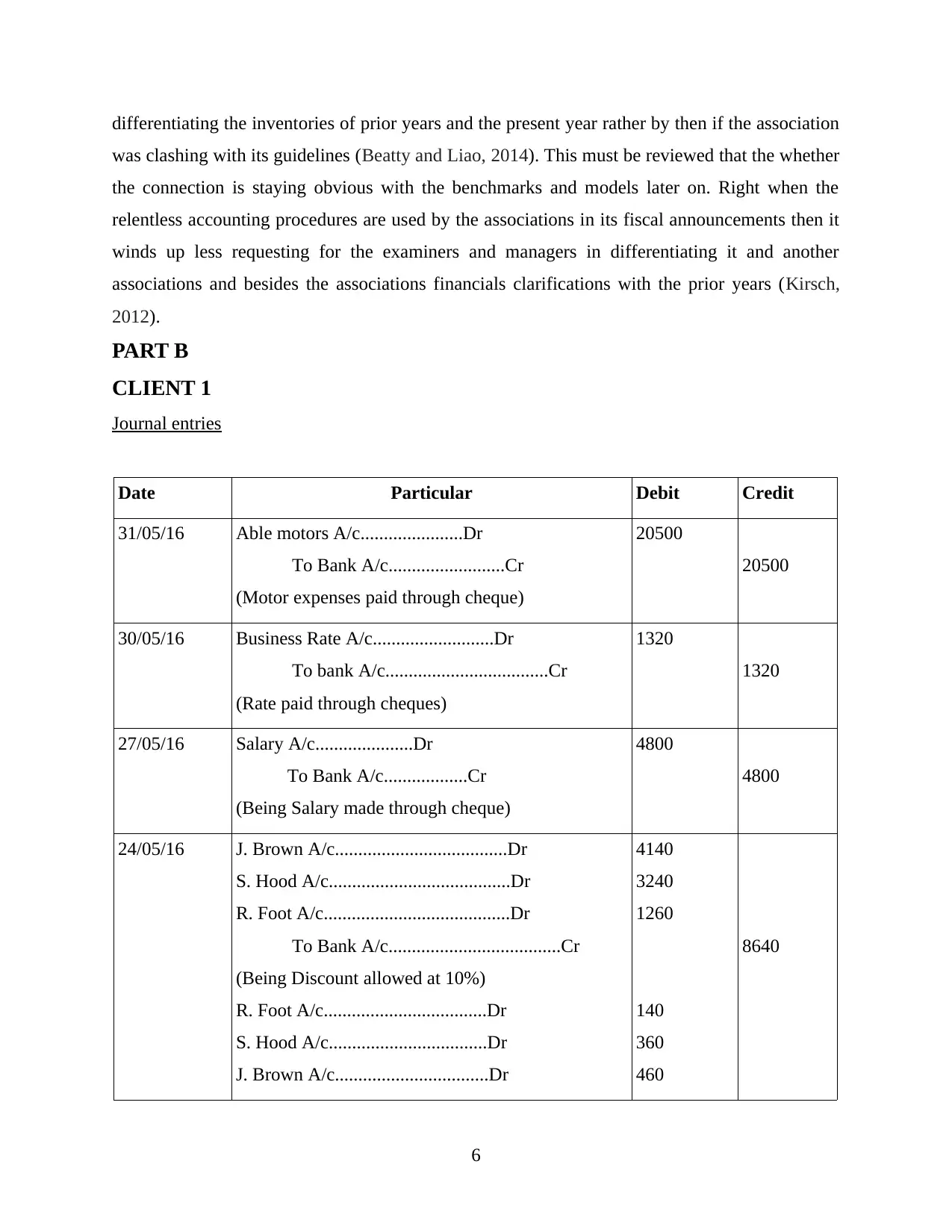

CLIENT 1

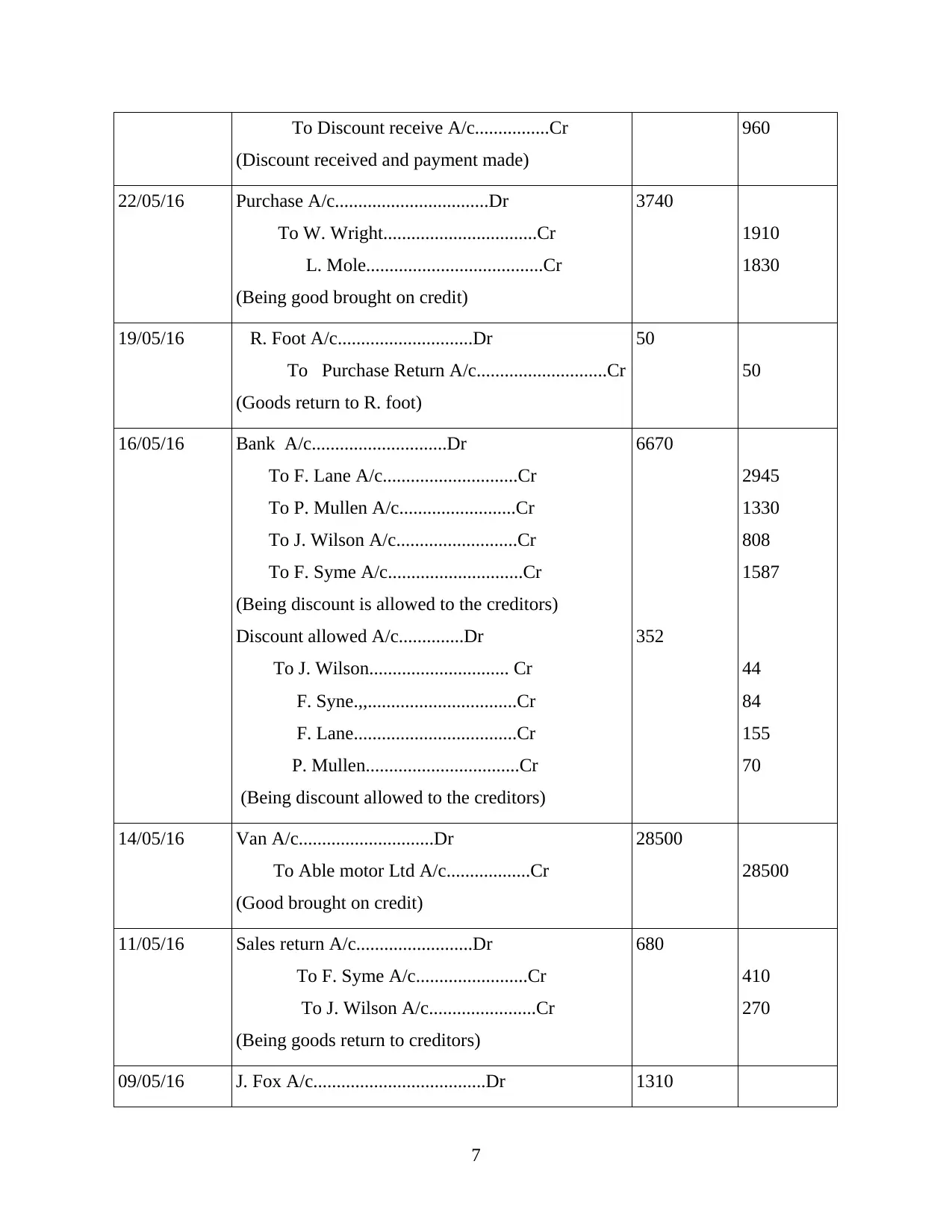

Journal entries

Date Particular Debit Credit

31/05/16 Able motors A/c......................Dr

To Bank A/c.........................Cr

(Motor expenses paid through cheque)

20500

20500

30/05/16 Business Rate A/c..........................Dr

To bank A/c...................................Cr

(Rate paid through cheques)

1320

1320

27/05/16 Salary A/c.....................Dr

To Bank A/c..................Cr

(Being Salary made through cheque)

4800

4800

24/05/16 J. Brown A/c.....................................Dr

S. Hood A/c.......................................Dr

R. Foot A/c........................................Dr

To Bank A/c.....................................Cr

(Being Discount allowed at 10%)

R. Foot A/c...................................Dr

S. Hood A/c..................................Dr

J. Brown A/c.................................Dr

4140

3240

1260

140

360

460

8640

6

was clashing with its guidelines (Beatty and Liao, 2014). This must be reviewed that the whether

the connection is staying obvious with the benchmarks and models later on. Right when the

relentless accounting procedures are used by the associations in its fiscal announcements then it

winds up less requesting for the examiners and managers in differentiating it and another

associations and besides the associations financials clarifications with the prior years (Kirsch,

2012).

PART B

CLIENT 1

Journal entries

Date Particular Debit Credit

31/05/16 Able motors A/c......................Dr

To Bank A/c.........................Cr

(Motor expenses paid through cheque)

20500

20500

30/05/16 Business Rate A/c..........................Dr

To bank A/c...................................Cr

(Rate paid through cheques)

1320

1320

27/05/16 Salary A/c.....................Dr

To Bank A/c..................Cr

(Being Salary made through cheque)

4800

4800

24/05/16 J. Brown A/c.....................................Dr

S. Hood A/c.......................................Dr

R. Foot A/c........................................Dr

To Bank A/c.....................................Cr

(Being Discount allowed at 10%)

R. Foot A/c...................................Dr

S. Hood A/c..................................Dr

J. Brown A/c.................................Dr

4140

3240

1260

140

360

460

8640

6

To Discount receive A/c................Cr

(Discount received and payment made)

960

22/05/16 Purchase A/c.................................Dr

To W. Wright.................................Cr

L. Mole......................................Cr

(Being good brought on credit)

3740

1910

1830

19/05/16 R. Foot A/c.............................Dr

To Purchase Return A/c............................Cr

(Goods return to R. foot)

50

50

16/05/16 Bank A/c.............................Dr

To F. Lane A/c.............................Cr

To P. Mullen A/c.........................Cr

To J. Wilson A/c..........................Cr

To F. Syme A/c.............................Cr

(Being discount is allowed to the creditors)

Discount allowed A/c..............Dr

To J. Wilson.............................. Cr

F. Syne.,,................................Cr

F. Lane...................................Cr

P. Mullen.................................Cr

(Being discount allowed to the creditors)

6670

352

2945

1330

808

1587

44

84

155

70

14/05/16 Van A/c.............................Dr

To Able motor Ltd A/c..................Cr

(Good brought on credit)

28500

28500

11/05/16 Sales return A/c.........................Dr

To F. Syme A/c........................Cr

To J. Wilson A/c.......................Cr

(Being goods return to creditors)

680

410

270

09/05/16 J. Fox A/c.....................................Dr 1310

7

(Discount received and payment made)

960

22/05/16 Purchase A/c.................................Dr

To W. Wright.................................Cr

L. Mole......................................Cr

(Being good brought on credit)

3740

1910

1830

19/05/16 R. Foot A/c.............................Dr

To Purchase Return A/c............................Cr

(Goods return to R. foot)

50

50

16/05/16 Bank A/c.............................Dr

To F. Lane A/c.............................Cr

To P. Mullen A/c.........................Cr

To J. Wilson A/c..........................Cr

To F. Syme A/c.............................Cr

(Being discount is allowed to the creditors)

Discount allowed A/c..............Dr

To J. Wilson.............................. Cr

F. Syne.,,................................Cr

F. Lane...................................Cr

P. Mullen.................................Cr

(Being discount allowed to the creditors)

6670

352

2945

1330

808

1587

44

84

155

70

14/05/16 Van A/c.............................Dr

To Able motor Ltd A/c..................Cr

(Good brought on credit)

28500

28500

11/05/16 Sales return A/c.........................Dr

To F. Syme A/c........................Cr

To J. Wilson A/c.......................Cr

(Being goods return to creditors)

680

410

270

09/05/16 J. Fox A/c.....................................Dr 1310

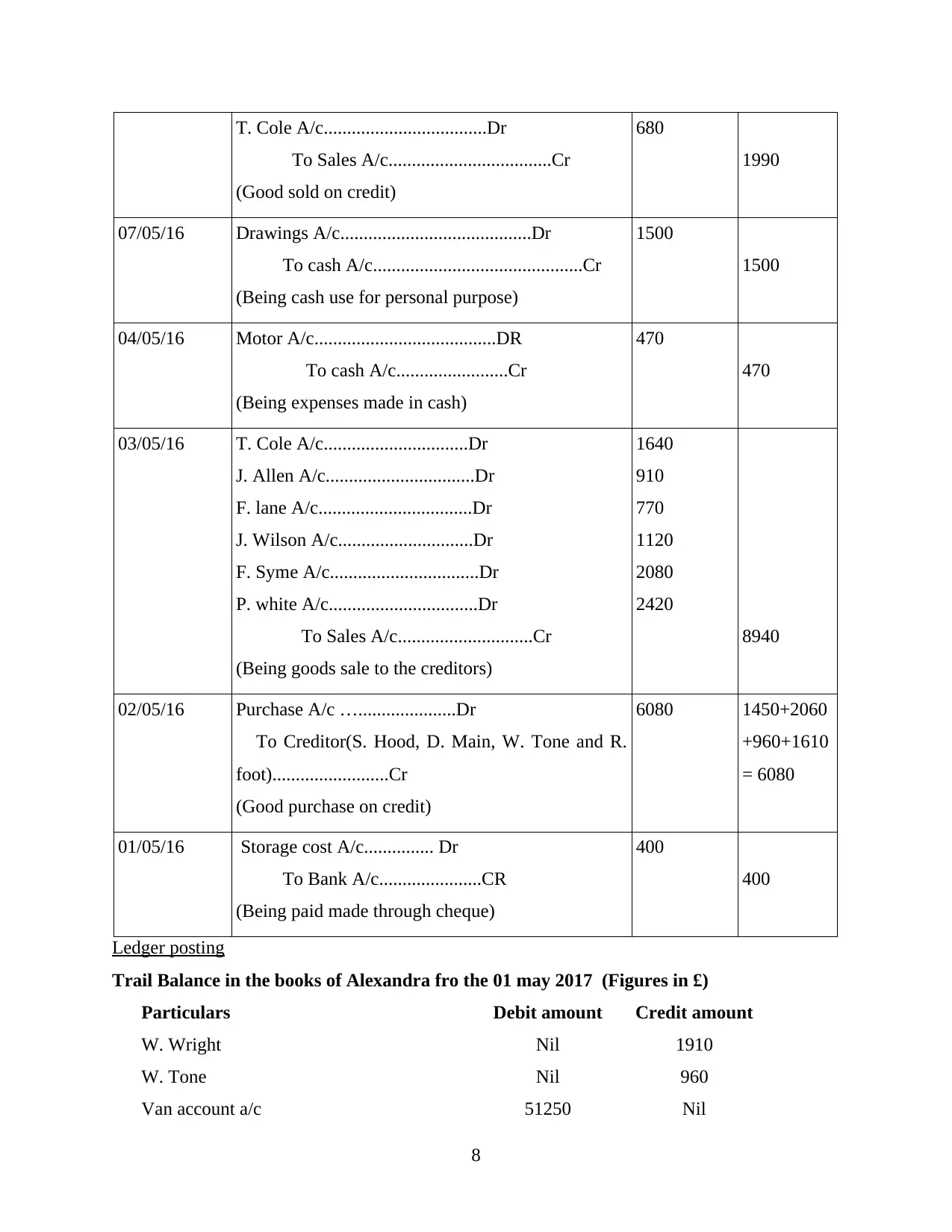

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T. Cole A/c...................................Dr

To Sales A/c...................................Cr

(Good sold on credit)

680

1990

07/05/16 Drawings A/c.........................................Dr

To cash A/c.............................................Cr

(Being cash use for personal purpose)

1500

1500

04/05/16 Motor A/c.......................................DR

To cash A/c........................Cr

(Being expenses made in cash)

470

470

03/05/16 T. Cole A/c...............................Dr

J. Allen A/c................................Dr

F. lane A/c.................................Dr

J. Wilson A/c.............................Dr

F. Syme A/c................................Dr

P. white A/c................................Dr

To Sales A/c.............................Cr

(Being goods sale to the creditors)

1640

910

770

1120

2080

2420

8940

02/05/16 Purchase A/c ….....................Dr

To Creditor(S. Hood, D. Main, W. Tone and R.

foot).........................Cr

(Good purchase on credit)

6080 1450+2060

+960+1610

= 6080

01/05/16 Storage cost A/c............... Dr

To Bank A/c......................CR

(Being paid made through cheque)

400

400

Ledger posting

Trail Balance in the books of Alexandra fro the 01 may 2017 (Figures in £)

Particulars Debit amount Credit amount

W. Wright Nil 1910

W. Tone Nil 960

Van account a/c 51250 Nil

8

To Sales A/c...................................Cr

(Good sold on credit)

680

1990

07/05/16 Drawings A/c.........................................Dr

To cash A/c.............................................Cr

(Being cash use for personal purpose)

1500

1500

04/05/16 Motor A/c.......................................DR

To cash A/c........................Cr

(Being expenses made in cash)

470

470

03/05/16 T. Cole A/c...............................Dr

J. Allen A/c................................Dr

F. lane A/c.................................Dr

J. Wilson A/c.............................Dr

F. Syme A/c................................Dr

P. white A/c................................Dr

To Sales A/c.............................Cr

(Being goods sale to the creditors)

1640

910

770

1120

2080

2420

8940

02/05/16 Purchase A/c ….....................Dr

To Creditor(S. Hood, D. Main, W. Tone and R.

foot).........................Cr

(Good purchase on credit)

6080 1450+2060

+960+1610

= 6080

01/05/16 Storage cost A/c............... Dr

To Bank A/c......................CR

(Being paid made through cheque)

400

400

Ledger posting

Trail Balance in the books of Alexandra fro the 01 may 2017 (Figures in £)

Particulars Debit amount Credit amount

W. Wright Nil 1910

W. Tone Nil 960

Van account a/c 51250 Nil

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

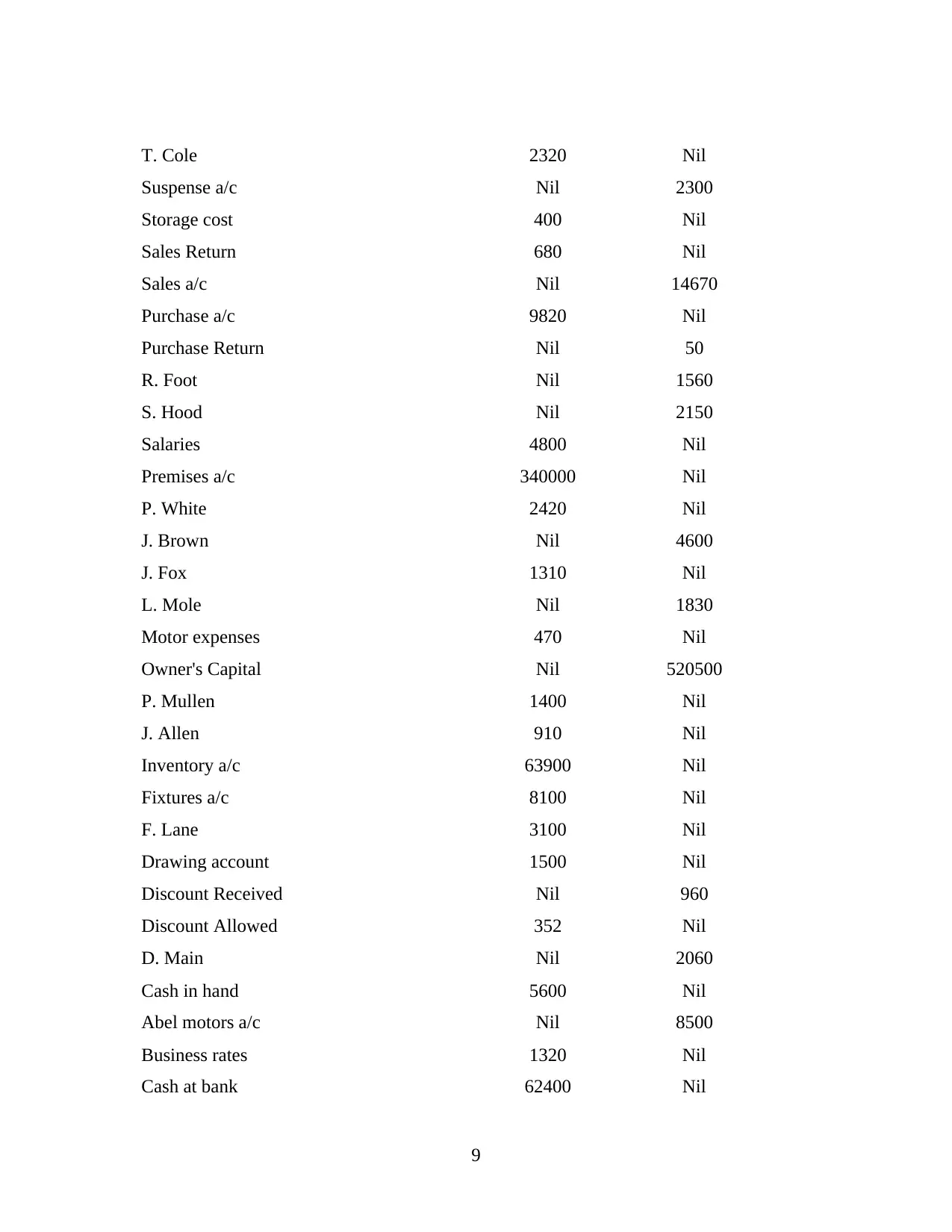

T. Cole 2320 Nil

Suspense a/c Nil 2300

Storage cost 400 Nil

Sales Return 680 Nil

Sales a/c Nil 14670

Purchase a/c 9820 Nil

Purchase Return Nil 50

R. Foot Nil 1560

S. Hood Nil 2150

Salaries 4800 Nil

Premises a/c 340000 Nil

P. White 2420 Nil

J. Brown Nil 4600

J. Fox 1310 Nil

L. Mole Nil 1830

Motor expenses 470 Nil

Owner's Capital Nil 520500

P. Mullen 1400 Nil

J. Allen 910 Nil

Inventory a/c 63900 Nil

Fixtures a/c 8100 Nil

F. Lane 3100 Nil

Drawing account 1500 Nil

Discount Received Nil 960

Discount Allowed 352 Nil

D. Main Nil 2060

Cash in hand 5600 Nil

Abel motors a/c Nil 8500

Business rates 1320 Nil

Cash at bank 62400 Nil

9

Suspense a/c Nil 2300

Storage cost 400 Nil

Sales Return 680 Nil

Sales a/c Nil 14670

Purchase a/c 9820 Nil

Purchase Return Nil 50

R. Foot Nil 1560

S. Hood Nil 2150

Salaries 4800 Nil

Premises a/c 340000 Nil

P. White 2420 Nil

J. Brown Nil 4600

J. Fox 1310 Nil

L. Mole Nil 1830

Motor expenses 470 Nil

Owner's Capital Nil 520500

P. Mullen 1400 Nil

J. Allen 910 Nil

Inventory a/c 63900 Nil

Fixtures a/c 8100 Nil

F. Lane 3100 Nil

Drawing account 1500 Nil

Discount Received Nil 960

Discount Allowed 352 Nil

D. Main Nil 2060

Cash in hand 5600 Nil

Abel motors a/c Nil 8500

Business rates 1320 Nil

Cash at bank 62400 Nil

9

562052 562052

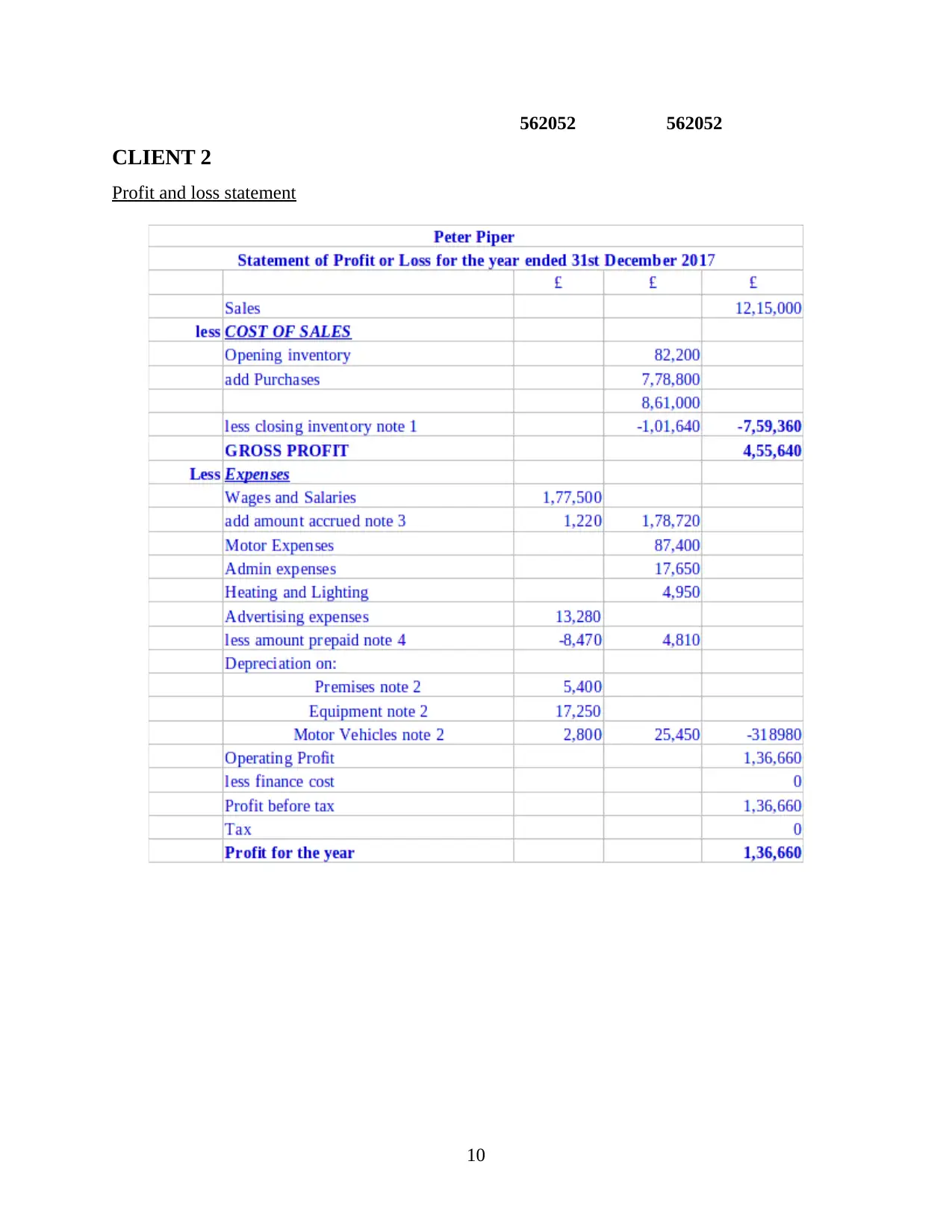

CLIENT 2

Profit and loss statement

10

CLIENT 2

Profit and loss statement

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.