Financial Accounting Principles: Stakeholders, Clients, and Analysis

VerifiedAdded on 2020/10/23

|26

|5321

|460

Report

AI Summary

This report delves into the core principles of financial accounting, encompassing the recording, summarization, and reporting of financial transactions. It explores the purpose of financial accounting and its importance in providing a framework for decision-making. The report identifies and analyzes both internal and external stakeholders, highlighting their interests in an organization's financial information. It presents journal entries, trial balances, profit and loss statements, and balance sheets for various clients. Furthermore, it explains crucial accounting concepts such as depreciation, bank reconciliation, and the imprest system in petty cash. The report also compares financial statements of sole traders and limited companies, and discusses the use of control and suspense accounts. The report also includes example journal entries. Overall, the report offers a detailed analysis of financial accounting practices, providing valuable insights for students.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

1. Defining financial accounting and its purpose...................................................................4

2. Internal and External stakeholders of an organization and why they are interested in

organization's financial information.......................................................................................6

CLIENT 1........................................................................................................................................8

Journal entry in the books of Alexandra study.......................................................................8

Trial balance:........................................................................................................................18

CLIENT 2......................................................................................................................................18

A.) Preparation of profit and loss statement of Munteanu Ltd. For the year ended 31st

december 2018......................................................................................................................18

B.) Statement of financial position of Munteanu Ltd as on 31st December 2018................18

C.) Explanation on following concepts................................................................................19

D.) Describing purpose of depreciation with its two methods.............................................20

E.) Critically evaluating the difference between the financial statements prepared by sole

trader and the limited companies..........................................................................................20

CLIENT 3......................................................................................................................................21

A.) Explaining the purpose of preparing the bank reconciliation statement and reason of this

preparation on monthly basis................................................................................................21

B.) Explaining areas which may cause record vary from the bank records.........................22

C.) Explaining the term imprest which is used in petty cash system...................................22

D.) Cash book and bank reconciliation statements..............................................................22

CLIENT 4......................................................................................................................................24

A.) preparation of balances...................................................................................................24

B.) Explaining the term Control account..............................................................................25

CLIENT 5......................................................................................................................................25

a.) Explaining the term suspense account with its main features.........................................25

b) Trial balance.....................................................................................................................26

c.) Journal entries and correction..........................................................................................26

CONCLUSION..............................................................................................................................27

INTRODUCTION...........................................................................................................................4

1. Defining financial accounting and its purpose...................................................................4

2. Internal and External stakeholders of an organization and why they are interested in

organization's financial information.......................................................................................6

CLIENT 1........................................................................................................................................8

Journal entry in the books of Alexandra study.......................................................................8

Trial balance:........................................................................................................................18

CLIENT 2......................................................................................................................................18

A.) Preparation of profit and loss statement of Munteanu Ltd. For the year ended 31st

december 2018......................................................................................................................18

B.) Statement of financial position of Munteanu Ltd as on 31st December 2018................18

C.) Explanation on following concepts................................................................................19

D.) Describing purpose of depreciation with its two methods.............................................20

E.) Critically evaluating the difference between the financial statements prepared by sole

trader and the limited companies..........................................................................................20

CLIENT 3......................................................................................................................................21

A.) Explaining the purpose of preparing the bank reconciliation statement and reason of this

preparation on monthly basis................................................................................................21

B.) Explaining areas which may cause record vary from the bank records.........................22

C.) Explaining the term imprest which is used in petty cash system...................................22

D.) Cash book and bank reconciliation statements..............................................................22

CLIENT 4......................................................................................................................................24

A.) preparation of balances...................................................................................................24

B.) Explaining the term Control account..............................................................................25

CLIENT 5......................................................................................................................................25

a.) Explaining the term suspense account with its main features.........................................25

b) Trial balance.....................................................................................................................26

c.) Journal entries and correction..........................................................................................26

CONCLUSION..............................................................................................................................27

REFERENCE...................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is the process of recording, summarizing and reporting the financial

transactions of a company. Field of financial accounting is highly significant which in turn

provides stakeholders with suitable framework for decision making. Thus, the assessment will

create for developing better understanding of financial accounting and its purpose. Further, in

this report two internal stakeholders and four external stakeholders for large businesses will

evaluate in order to identify their interest in financial information of the organization. Small

accountancy firm which is selected in this report is Berley Chartered accountant which deals in

giving financial services to clients. Moreover, in this report calculation related to clients will also

be provided.

1. Defining financial accounting and its purpose

Financial accounting:

The financial accounting can be described as that branch of accounting that deals with

tracking the financial transaction of the company. The transactions are recorded in the books of

account as per the guidelines, standards to summaries the same and present the information in

financial reports or statement which includes profits and loss account, balance sheet, cash flow

statement etc. This is a process of recording, summarizing and reporting the myriad of

transaction which are a result from the operations and activities of a business over a period of

time (Financial accounting, 2018). The presentation of financing information of business

activities as per the standardized guidelines in various forms of statements record the operating

performance of company for a specific period. This utilize pre determined accounting principles

to decide the treatments of a particulate transaction as per the established principles.

The financial accounting may be performed using either of two methods accuracy and

cash method or a both. In general practice accrual method is followed as this record the dual

effect of a transaction giving the exact accounting treatments of each financial transaction of the

organization. The transactions are recorded in accordance with Generally accepted Accounting

principles (GAAP).

Purpose served by financial accounting:

The purpose of financial accounting is to make sure that all the certified accounting

standards are aided with in summarizing and recording of the financial transaction of the firm.

The purpose served by the financial accounting are not limited but its main aims is to assists in

Financial accounting is the process of recording, summarizing and reporting the financial

transactions of a company. Field of financial accounting is highly significant which in turn

provides stakeholders with suitable framework for decision making. Thus, the assessment will

create for developing better understanding of financial accounting and its purpose. Further, in

this report two internal stakeholders and four external stakeholders for large businesses will

evaluate in order to identify their interest in financial information of the organization. Small

accountancy firm which is selected in this report is Berley Chartered accountant which deals in

giving financial services to clients. Moreover, in this report calculation related to clients will also

be provided.

1. Defining financial accounting and its purpose

Financial accounting:

The financial accounting can be described as that branch of accounting that deals with

tracking the financial transaction of the company. The transactions are recorded in the books of

account as per the guidelines, standards to summaries the same and present the information in

financial reports or statement which includes profits and loss account, balance sheet, cash flow

statement etc. This is a process of recording, summarizing and reporting the myriad of

transaction which are a result from the operations and activities of a business over a period of

time (Financial accounting, 2018). The presentation of financing information of business

activities as per the standardized guidelines in various forms of statements record the operating

performance of company for a specific period. This utilize pre determined accounting principles

to decide the treatments of a particulate transaction as per the established principles.

The financial accounting may be performed using either of two methods accuracy and

cash method or a both. In general practice accrual method is followed as this record the dual

effect of a transaction giving the exact accounting treatments of each financial transaction of the

organization. The transactions are recorded in accordance with Generally accepted Accounting

principles (GAAP).

Purpose served by financial accounting:

The purpose of financial accounting is to make sure that all the certified accounting

standards are aided with in summarizing and recording of the financial transaction of the firm.

The purpose served by the financial accounting are not limited but its main aims is to assists in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

harmonized recording, decision making etc. Some of the main purpose served by it are recouped

below:

Recording of the financial transaction:

The most important aspect of financial accounting is to record the financial and monetary

data and information of a business. To be carried out in such a manner that gives the final

extract about the performance of company as well as assist in decision making process.

Harmonized way record the transaction:

The main purpose served by financial accounting is summarizing and recording of the

monetary transaction related to a business pertaining to a particular period. This allow the

business to follow a uniform method in recording of the transaction with uniformity giving a

scope of comparison regarding own financial performance & position and competitors as well.

Assist in decision making process:

The main purpose served by financial accounting is to accumulate reports on the financial

information regarding the performance, financial position and cash flow of the business (The

importance of financial accounting, 2018). The information is used by the management in

decision making process on how to manage the business, invests and lend money etc.

Adherence with prescribed standard and guidelines:

This accounting emphasizes on abiding with regulatory guidelines and standards for

recording financial transaction associated with business. The transaction must be recorded as per

guidelines of GAAP, FASB, IFRS etc. which fulfills the legal obligation of the business

organization.

Relevance:

Purpose of financial accounting is to help its reader in making decision by analyzing

financial capability of company. Thus, financial accounting has the purpose to for providing

useful information which must be relevant. For satisfying these objective, entity report result on

quarterly and annual basis (Freedman, 2019).

Reliability-

It is the purpose financial accounting to provide information which must be reliable. It

reliable financial statements are not produce by company then investors are not able to gain the

information by which they will able to develop economic decision.

Comparability-

below:

Recording of the financial transaction:

The most important aspect of financial accounting is to record the financial and monetary

data and information of a business. To be carried out in such a manner that gives the final

extract about the performance of company as well as assist in decision making process.

Harmonized way record the transaction:

The main purpose served by financial accounting is summarizing and recording of the

monetary transaction related to a business pertaining to a particular period. This allow the

business to follow a uniform method in recording of the transaction with uniformity giving a

scope of comparison regarding own financial performance & position and competitors as well.

Assist in decision making process:

The main purpose served by financial accounting is to accumulate reports on the financial

information regarding the performance, financial position and cash flow of the business (The

importance of financial accounting, 2018). The information is used by the management in

decision making process on how to manage the business, invests and lend money etc.

Adherence with prescribed standard and guidelines:

This accounting emphasizes on abiding with regulatory guidelines and standards for

recording financial transaction associated with business. The transaction must be recorded as per

guidelines of GAAP, FASB, IFRS etc. which fulfills the legal obligation of the business

organization.

Relevance:

Purpose of financial accounting is to help its reader in making decision by analyzing

financial capability of company. Thus, financial accounting has the purpose to for providing

useful information which must be relevant. For satisfying these objective, entity report result on

quarterly and annual basis (Freedman, 2019).

Reliability-

It is the purpose financial accounting to provide information which must be reliable. It

reliable financial statements are not produce by company then investors are not able to gain the

information by which they will able to develop economic decision.

Comparability-

Another purpose of financial accounting is to provide information which is comparable.

System of recording and reporting accounting information is developed in order to provide

information which is more comparable.

Consistency-

It is the secondary quality of information which must be comparable where users will

able to relay and develop their decision regarding investment in company.

2. Internal and External stakeholders of an organization and why they are interested in

organization's financial information

Stakeholders can be defined as an independent body or institutions such as organizations,

individuals, groups that are concerned with the operations of a company and are interested in the

financial results of a business concern. Such stakeholders can be internal and external that are

briefly discussed below:

Internal stakeholders:

Internal stakeholders can be referred as those groups or individual that are present within

in the business organisation. Examples of such internal stakeholders are:

Employees- these are the group of stakeholders which have direct interest for business

operations of the entity. Reason which states their interest is that they are one which plays

main role in developing effective business functions. They analyse their involvement by

analysing the nature of business in which they will earn of themselves. For example:

transportation, mining, construction are the business where employees develop interest by

analysing health and safety policies. Management- these are also a group of internal stakeholder which has the direct interest

in business operations of the entity. They generally want to earn high wages and also

wants to retain their jobs for long term perspective. Thus, they have huge interest in

financial capability and growth of business.

External stakeholders

External stakeholders are such individuals and groups that are not within the business

organisation but are affected by the operations of the company (Bredmar, 2016). Examples of

such groups or individuals are :

Customers- These are the main group of stakeholder for every organisation because it is

said that the business only exists to serve their customers. That is why it is been said that

System of recording and reporting accounting information is developed in order to provide

information which is more comparable.

Consistency-

It is the secondary quality of information which must be comparable where users will

able to relay and develop their decision regarding investment in company.

2. Internal and External stakeholders of an organization and why they are interested in

organization's financial information

Stakeholders can be defined as an independent body or institutions such as organizations,

individuals, groups that are concerned with the operations of a company and are interested in the

financial results of a business concern. Such stakeholders can be internal and external that are

briefly discussed below:

Internal stakeholders:

Internal stakeholders can be referred as those groups or individual that are present within

in the business organisation. Examples of such internal stakeholders are:

Employees- these are the group of stakeholders which have direct interest for business

operations of the entity. Reason which states their interest is that they are one which plays

main role in developing effective business functions. They analyse their involvement by

analysing the nature of business in which they will earn of themselves. For example:

transportation, mining, construction are the business where employees develop interest by

analysing health and safety policies. Management- these are also a group of internal stakeholder which has the direct interest

in business operations of the entity. They generally want to earn high wages and also

wants to retain their jobs for long term perspective. Thus, they have huge interest in

financial capability and growth of business.

External stakeholders

External stakeholders are such individuals and groups that are not within the business

organisation but are affected by the operations of the company (Bredmar, 2016). Examples of

such groups or individuals are :

Customers- These are the main group of stakeholder for every organisation because it is

said that the business only exists to serve their customers. That is why it is been said that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the consumers are the actual stakeholder of the business which mainly impacted by value

and quality of service which entity provides.

Investors- these are the form of stakeholders which include both shareholders and debt

holders. They generally invest capital in business with the expectation of getting of

earning a certain rate of return. They are mainly concerned with concept of shareholder

value.

Government Authorities- these are also a major stakeholder group in business because

they collect taxes from the entity as well as from people which are employed in the

company. They get benefited from the overall gross domestic product which is also

contributed by companies. Suppliers/Creditors- these are the group of stakeholders which sells goods and services

to the business and will only relay upon the revenue generation with the business

operations conduct on daily basis. It is also true that these are the group which directly

involved in the functions which operated by company because of which their interest

generated with health and safety too.

The different stakeholders are interested in company's financial reasons because of the

various reasons that are briefly discussed below:

Employees: The employees of a company are concerned with the profitability and

stability. This is because of profitability of the company helps employees to assess the ability of

firm to pay their salaries on time. Profits are the basis on which employees' benefits are decided.

Through company's stability, employees are assured of their jobs in the future. This satisfies their

need of job security. Further, personnel evaluate organisation's financial performance with the

motive to assess or identify probabilities of organisation in relation to expansion of operations in

different markets (Osadchy and et.al., 2018). Moreover, such expansion possibilities provides a

gateway for the career development and growth opportunities to the existing workforce of the

company.

Management: In big and large organisations, management are the professionals

appointed by the Board of Directors, who are also elected by the shareholders of company to run

the business in the most effective manner. This group of the entity is given with the

responsibility of conducting day to day activities of business on the behalf of owners. The

financial performance of the company helps the managers in assessing the level of effectiveness

and quality of service which entity provides.

Investors- these are the form of stakeholders which include both shareholders and debt

holders. They generally invest capital in business with the expectation of getting of

earning a certain rate of return. They are mainly concerned with concept of shareholder

value.

Government Authorities- these are also a major stakeholder group in business because

they collect taxes from the entity as well as from people which are employed in the

company. They get benefited from the overall gross domestic product which is also

contributed by companies. Suppliers/Creditors- these are the group of stakeholders which sells goods and services

to the business and will only relay upon the revenue generation with the business

operations conduct on daily basis. It is also true that these are the group which directly

involved in the functions which operated by company because of which their interest

generated with health and safety too.

The different stakeholders are interested in company's financial reasons because of the

various reasons that are briefly discussed below:

Employees: The employees of a company are concerned with the profitability and

stability. This is because of profitability of the company helps employees to assess the ability of

firm to pay their salaries on time. Profits are the basis on which employees' benefits are decided.

Through company's stability, employees are assured of their jobs in the future. This satisfies their

need of job security. Further, personnel evaluate organisation's financial performance with the

motive to assess or identify probabilities of organisation in relation to expansion of operations in

different markets (Osadchy and et.al., 2018). Moreover, such expansion possibilities provides a

gateway for the career development and growth opportunities to the existing workforce of the

company.

Management: In big and large organisations, management are the professionals

appointed by the Board of Directors, who are also elected by the shareholders of company to run

the business in the most effective manner. This group of the entity is given with the

responsibility of conducting day to day activities of business on the behalf of owners. The

financial performance of the company helps the managers in assessing the level of effectiveness

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of firm's policies and strategies regarding every aspect of enterprise. The current financial

position of the company helps the management in deciding the future plans in terms of expansion

of operations. For example, finance manager is concerned with profits made by the company

during a particular period. This in turn helps management team in assessing the funds available

within company. Meanwhile, financial statement analysis helps management in identifying

opportunities in relation to taking new projects (Harrison and van der Laan Smith, 2015).

The management analyses the financial position of the organisation for determining the

long term and short term solvency, profitability, liquidity and return from the investments made

by the business. In other words, by evaluating financial statement management team can assess

whether goals pertaining to sales and profit are met or not. Hence, by undertaking such

information management team of business unit can develop strategic framework for upcoming

time period.

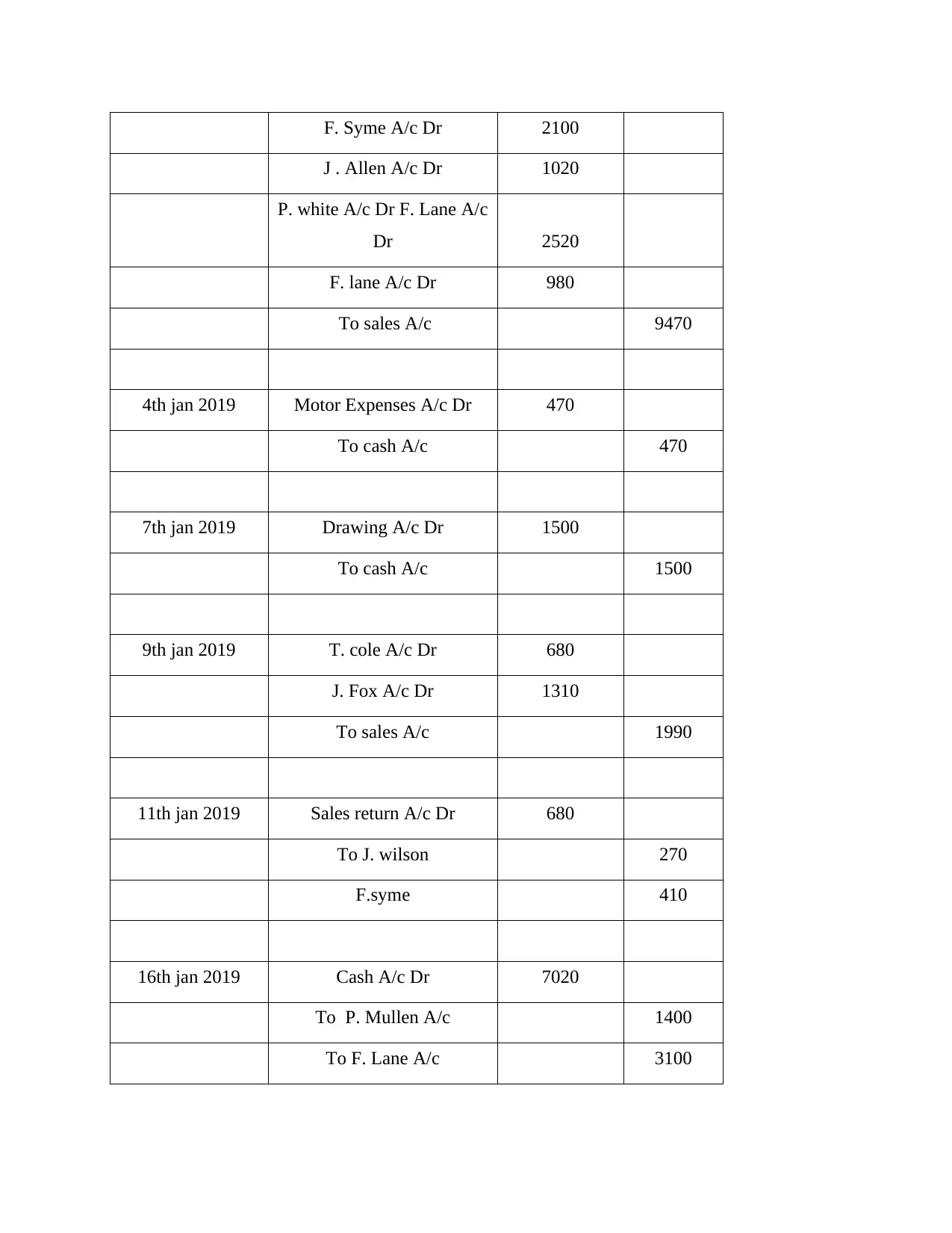

CLIENT 1

Journal entry in the books of Alexandra study

Journal entries in the books of Alexandra for January are as follows

Date particulars Debit Credit

1st jan 2019 Storage expense A/c Dr 450

To bank A/c

2nd jan 2019 Purchase A/c Dr 6080

To S. hood A/c 1450

To D main A/c 2060

To W Tone A/c 960

To R foot A/c 1610

3rd jan 2019 J Wilson A/c Dr 1200

T . Cole A/c dr 1650

position of the company helps the management in deciding the future plans in terms of expansion

of operations. For example, finance manager is concerned with profits made by the company

during a particular period. This in turn helps management team in assessing the funds available

within company. Meanwhile, financial statement analysis helps management in identifying

opportunities in relation to taking new projects (Harrison and van der Laan Smith, 2015).

The management analyses the financial position of the organisation for determining the

long term and short term solvency, profitability, liquidity and return from the investments made

by the business. In other words, by evaluating financial statement management team can assess

whether goals pertaining to sales and profit are met or not. Hence, by undertaking such

information management team of business unit can develop strategic framework for upcoming

time period.

CLIENT 1

Journal entry in the books of Alexandra study

Journal entries in the books of Alexandra for January are as follows

Date particulars Debit Credit

1st jan 2019 Storage expense A/c Dr 450

To bank A/c

2nd jan 2019 Purchase A/c Dr 6080

To S. hood A/c 1450

To D main A/c 2060

To W Tone A/c 960

To R foot A/c 1610

3rd jan 2019 J Wilson A/c Dr 1200

T . Cole A/c dr 1650

F. Syme A/c Dr 2100

J . Allen A/c Dr 1020

P. white A/c Dr F. Lane A/c

Dr 2520

F. lane A/c Dr 980

To sales A/c 9470

4th jan 2019 Motor Expenses A/c Dr 470

To cash A/c 470

7th jan 2019 Drawing A/c Dr 1500

To cash A/c 1500

9th jan 2019 T. cole A/c Dr 680

J. Fox A/c Dr 1310

To sales A/c 1990

11th jan 2019 Sales return A/c Dr 680

To J. wilson 270

F.syme 410

16th jan 2019 Cash A/c Dr 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

J . Allen A/c Dr 1020

P. white A/c Dr F. Lane A/c

Dr 2520

F. lane A/c Dr 980

To sales A/c 9470

4th jan 2019 Motor Expenses A/c Dr 470

To cash A/c 470

7th jan 2019 Drawing A/c Dr 1500

To cash A/c 1500

9th jan 2019 T. cole A/c Dr 680

J. Fox A/c Dr 1310

To sales A/c 1990

11th jan 2019 Sales return A/c Dr 680

To J. wilson 270

F.syme 410

16th jan 2019 Cash A/c Dr 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

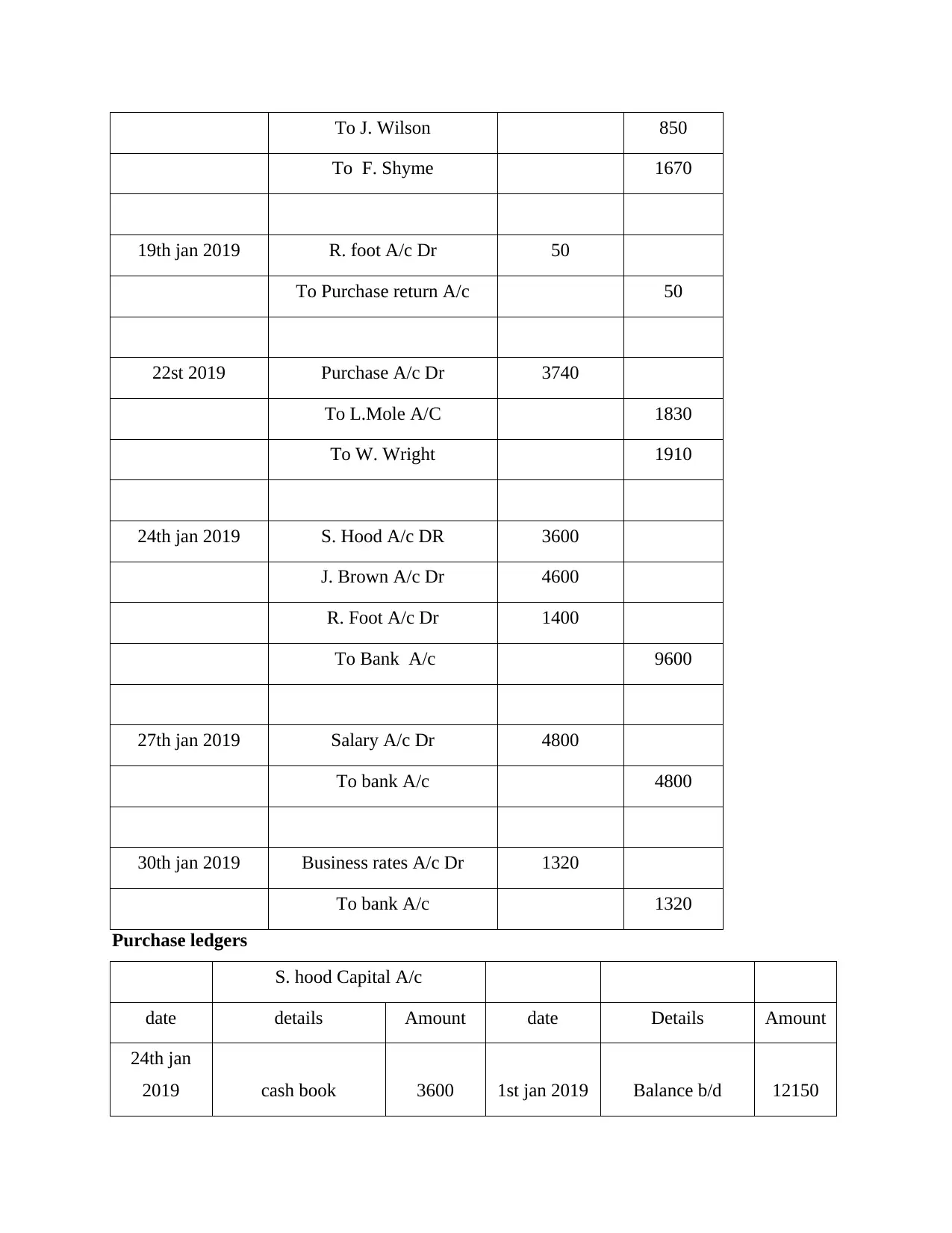

To J. Wilson 850

To F. Shyme 1670

19th jan 2019 R. foot A/c Dr 50

To Purchase return A/c 50

22st 2019 Purchase A/c Dr 3740

To L.Mole A/C 1830

To W. Wright 1910

24th jan 2019 S. Hood A/c DR 3600

J. Brown A/c Dr 4600

R. Foot A/c Dr 1400

To Bank A/c 9600

27th jan 2019 Salary A/c Dr 4800

To bank A/c 4800

30th jan 2019 Business rates A/c Dr 1320

To bank A/c 1320

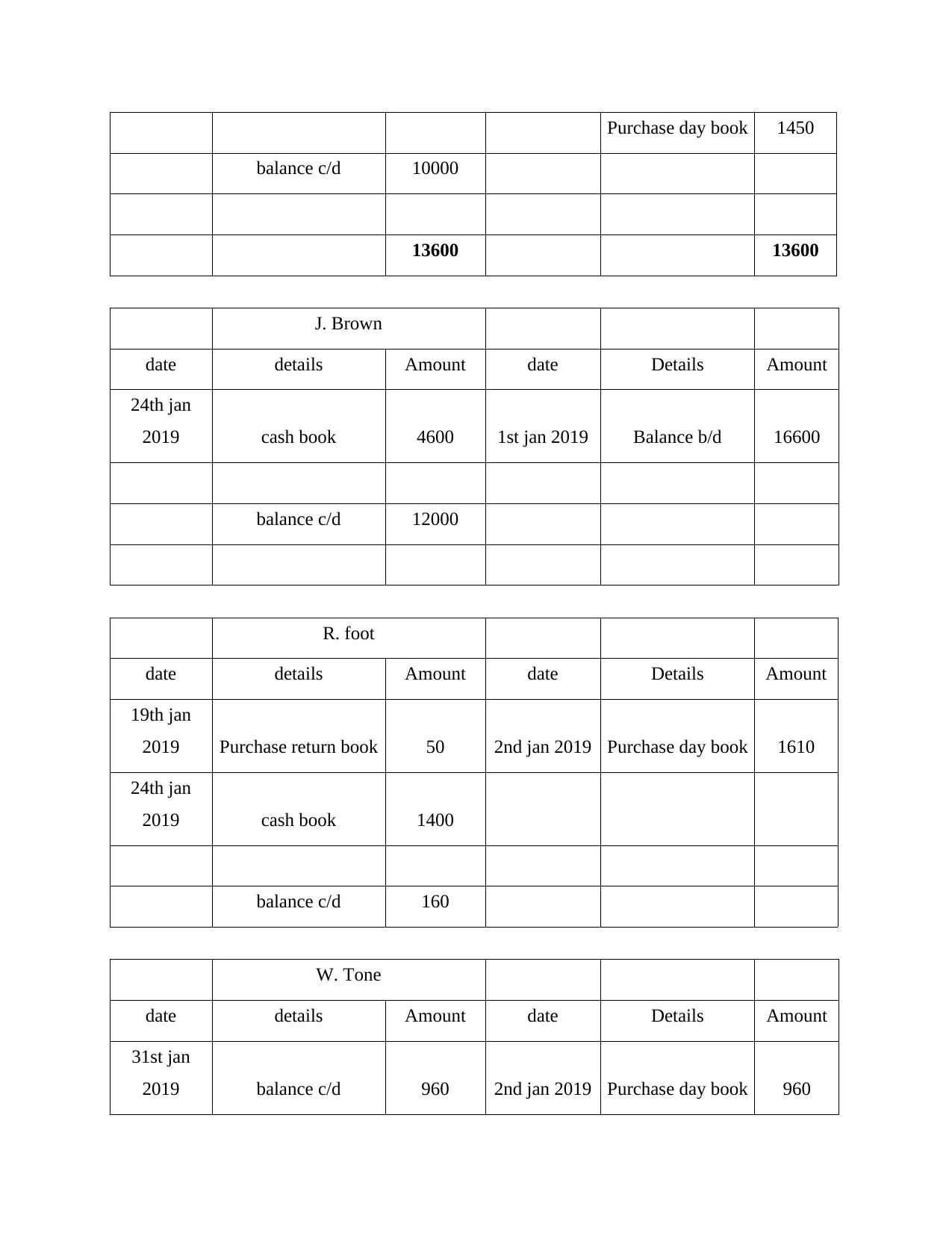

Purchase ledgers

S. hood Capital A/c

date details Amount date Details Amount

24th jan

2019 cash book 3600 1st jan 2019 Balance b/d 12150

To F. Shyme 1670

19th jan 2019 R. foot A/c Dr 50

To Purchase return A/c 50

22st 2019 Purchase A/c Dr 3740

To L.Mole A/C 1830

To W. Wright 1910

24th jan 2019 S. Hood A/c DR 3600

J. Brown A/c Dr 4600

R. Foot A/c Dr 1400

To Bank A/c 9600

27th jan 2019 Salary A/c Dr 4800

To bank A/c 4800

30th jan 2019 Business rates A/c Dr 1320

To bank A/c 1320

Purchase ledgers

S. hood Capital A/c

date details Amount date Details Amount

24th jan

2019 cash book 3600 1st jan 2019 Balance b/d 12150

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Purchase day book 1450

balance c/d 10000

13600 13600

J. Brown

date details Amount date Details Amount

24th jan

2019 cash book 4600 1st jan 2019 Balance b/d 16600

balance c/d 12000

R. foot

date details Amount date Details Amount

19th jan

2019 Purchase return book 50 2nd jan 2019 Purchase day book 1610

24th jan

2019 cash book 1400

balance c/d 160

W. Tone

date details Amount date Details Amount

31st jan

2019 balance c/d 960 2nd jan 2019 Purchase day book 960

balance c/d 10000

13600 13600

J. Brown

date details Amount date Details Amount

24th jan

2019 cash book 4600 1st jan 2019 Balance b/d 16600

balance c/d 12000

R. foot

date details Amount date Details Amount

19th jan

2019 Purchase return book 50 2nd jan 2019 Purchase day book 1610

24th jan

2019 cash book 1400

balance c/d 160

W. Tone

date details Amount date Details Amount

31st jan

2019 balance c/d 960 2nd jan 2019 Purchase day book 960

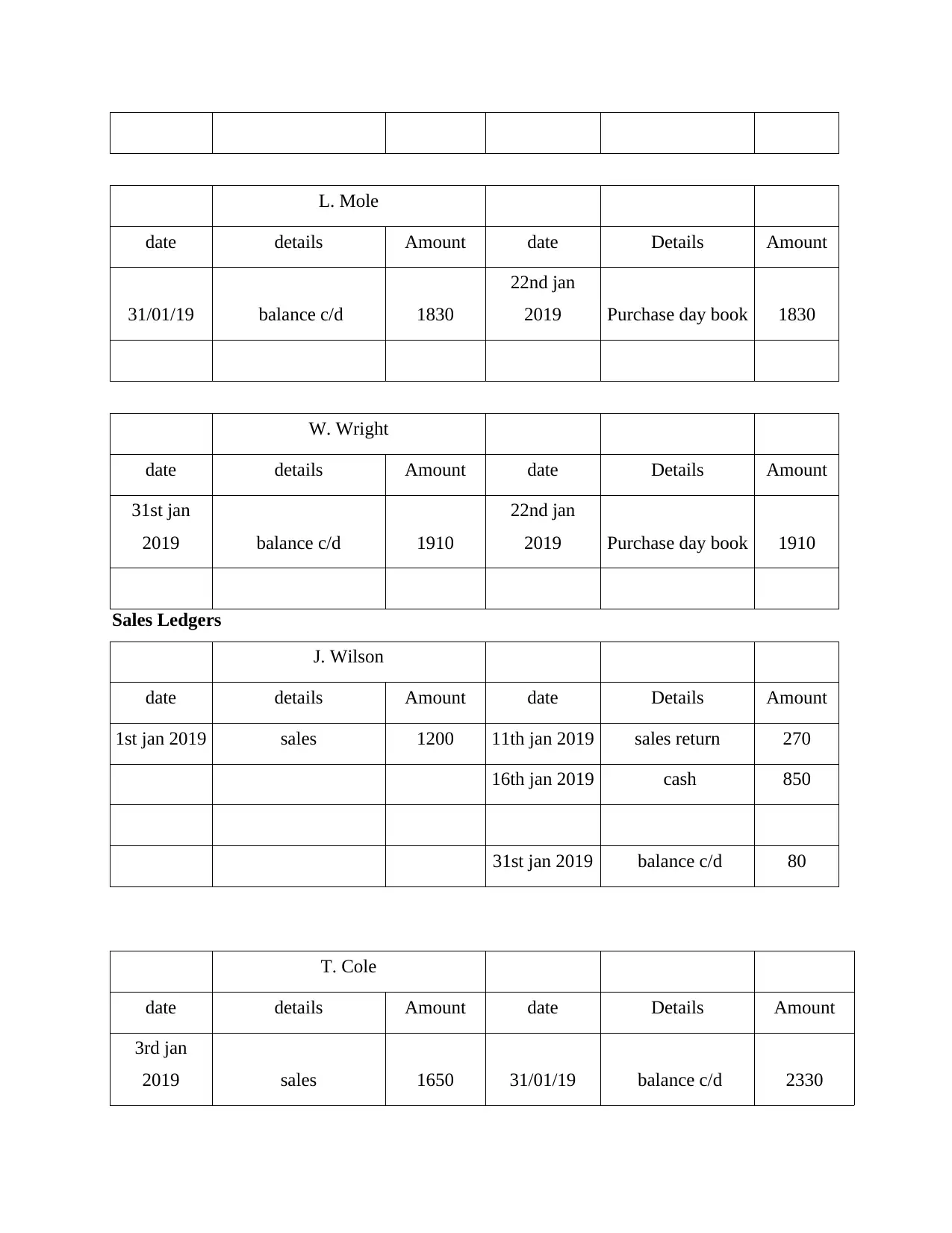

L. Mole

date details Amount date Details Amount

31/01/19 balance c/d 1830

22nd jan

2019 Purchase day book 1830

W. Wright

date details Amount date Details Amount

31st jan

2019 balance c/d 1910

22nd jan

2019 Purchase day book 1910

Sales Ledgers

J. Wilson

date details Amount date Details Amount

1st jan 2019 sales 1200 11th jan 2019 sales return 270

16th jan 2019 cash 850

31st jan 2019 balance c/d 80

T. Cole

date details Amount date Details Amount

3rd jan

2019 sales 1650 31/01/19 balance c/d 2330

date details Amount date Details Amount

31/01/19 balance c/d 1830

22nd jan

2019 Purchase day book 1830

W. Wright

date details Amount date Details Amount

31st jan

2019 balance c/d 1910

22nd jan

2019 Purchase day book 1910

Sales Ledgers

J. Wilson

date details Amount date Details Amount

1st jan 2019 sales 1200 11th jan 2019 sales return 270

16th jan 2019 cash 850

31st jan 2019 balance c/d 80

T. Cole

date details Amount date Details Amount

3rd jan

2019 sales 1650 31/01/19 balance c/d 2330

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.