Financial Accounting & Reporting: Report on Brambles & CIMIC

VerifiedAdded on 2020/05/16

|14

|2710

|149

Report

AI Summary

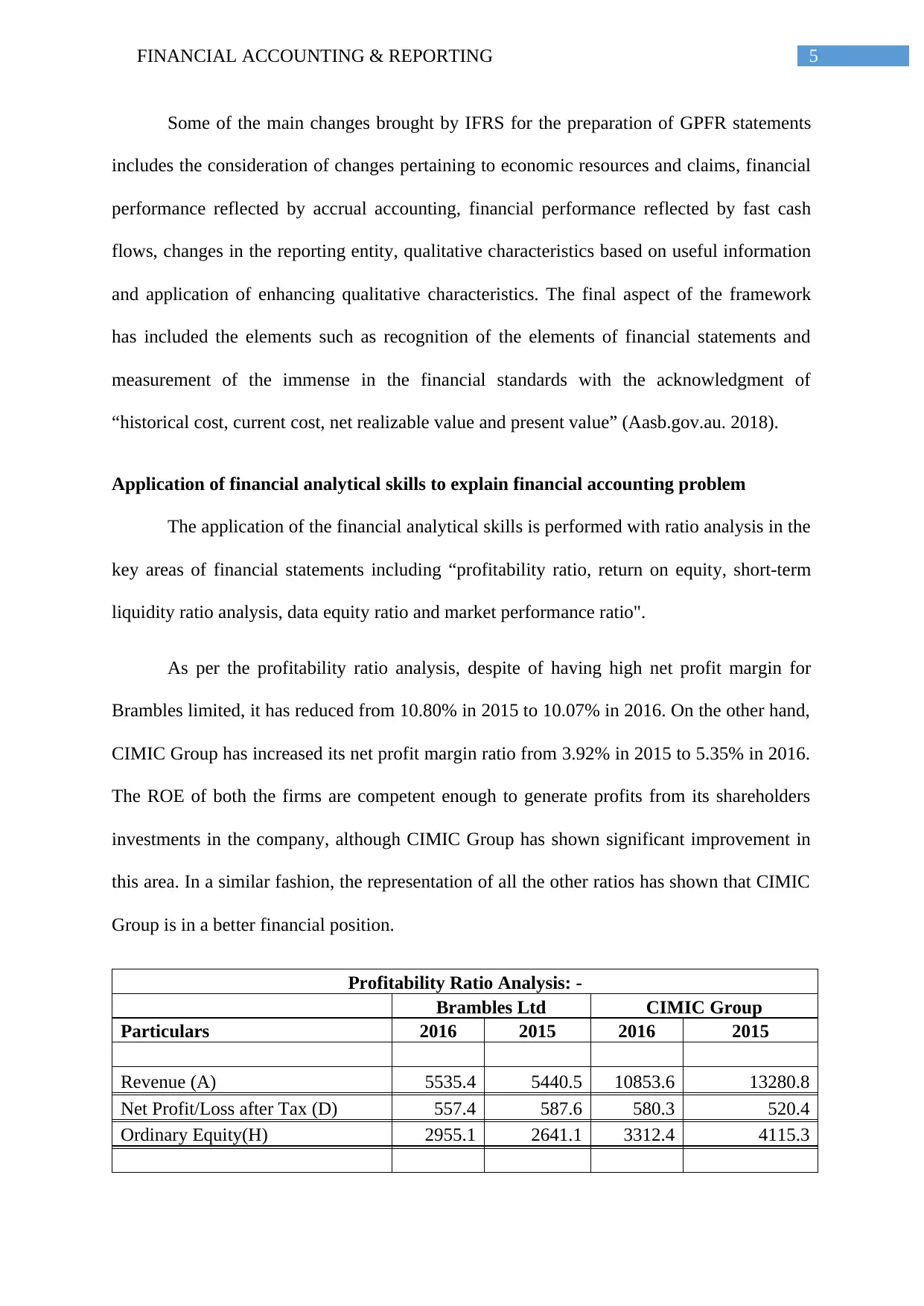

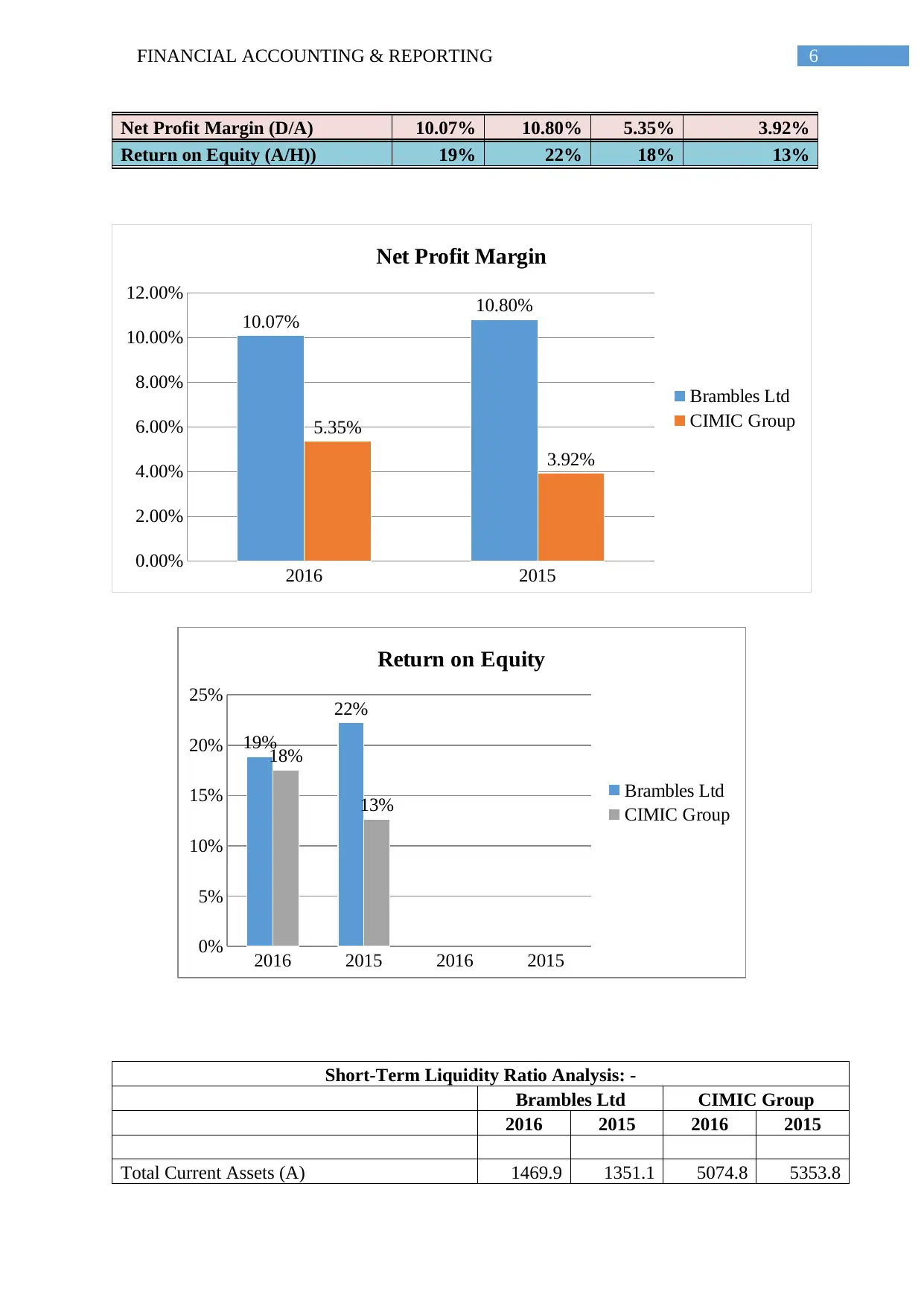

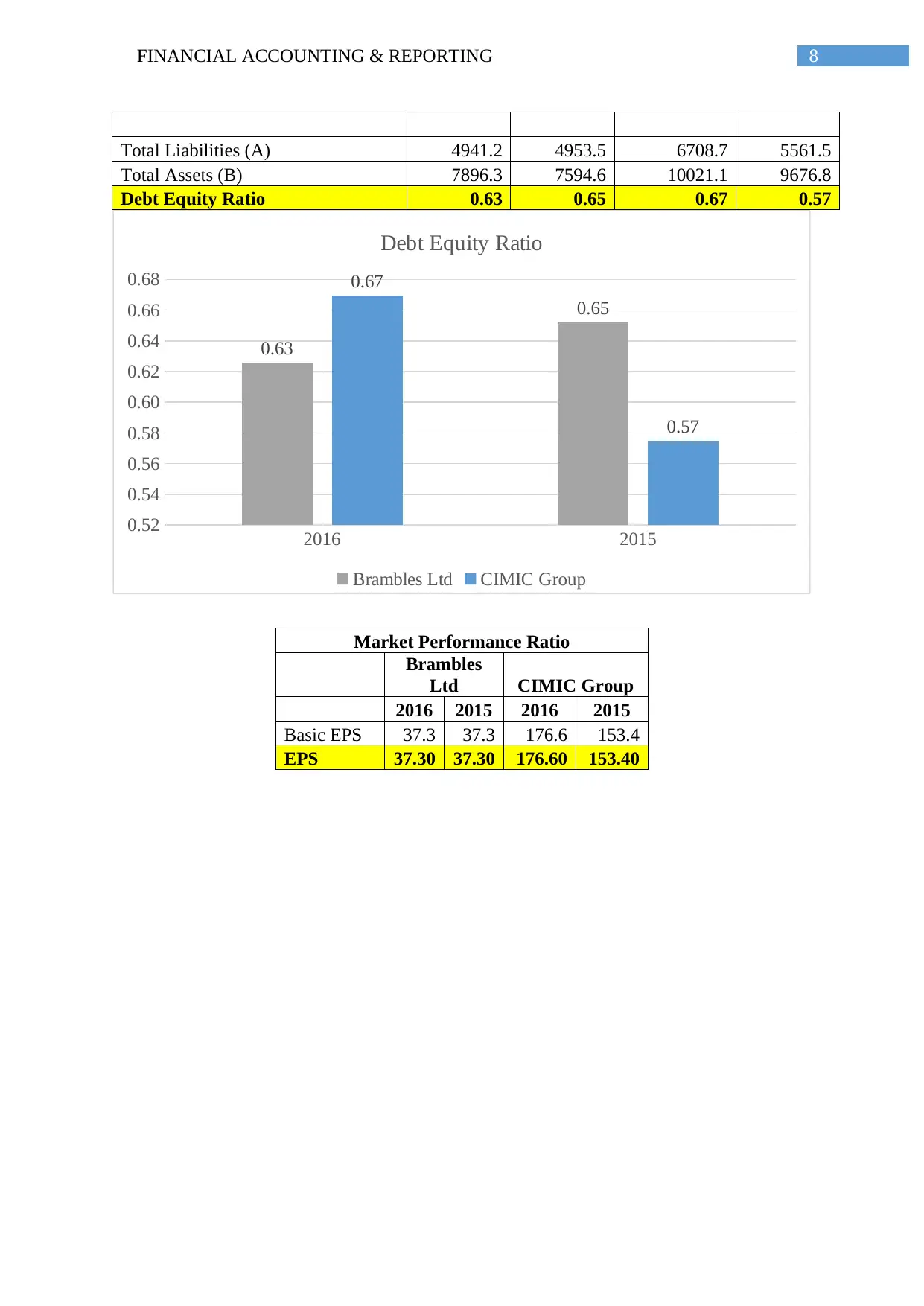

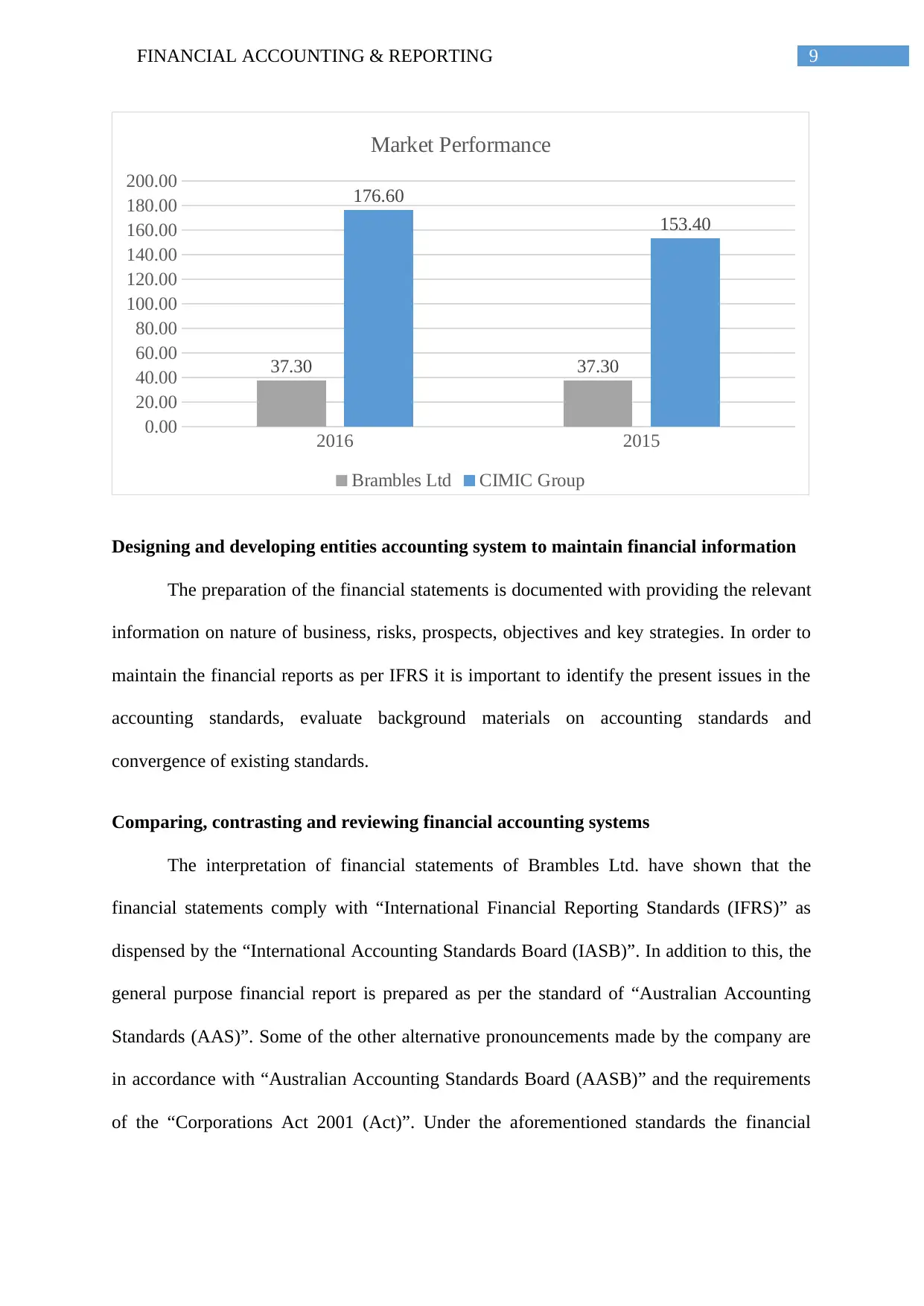

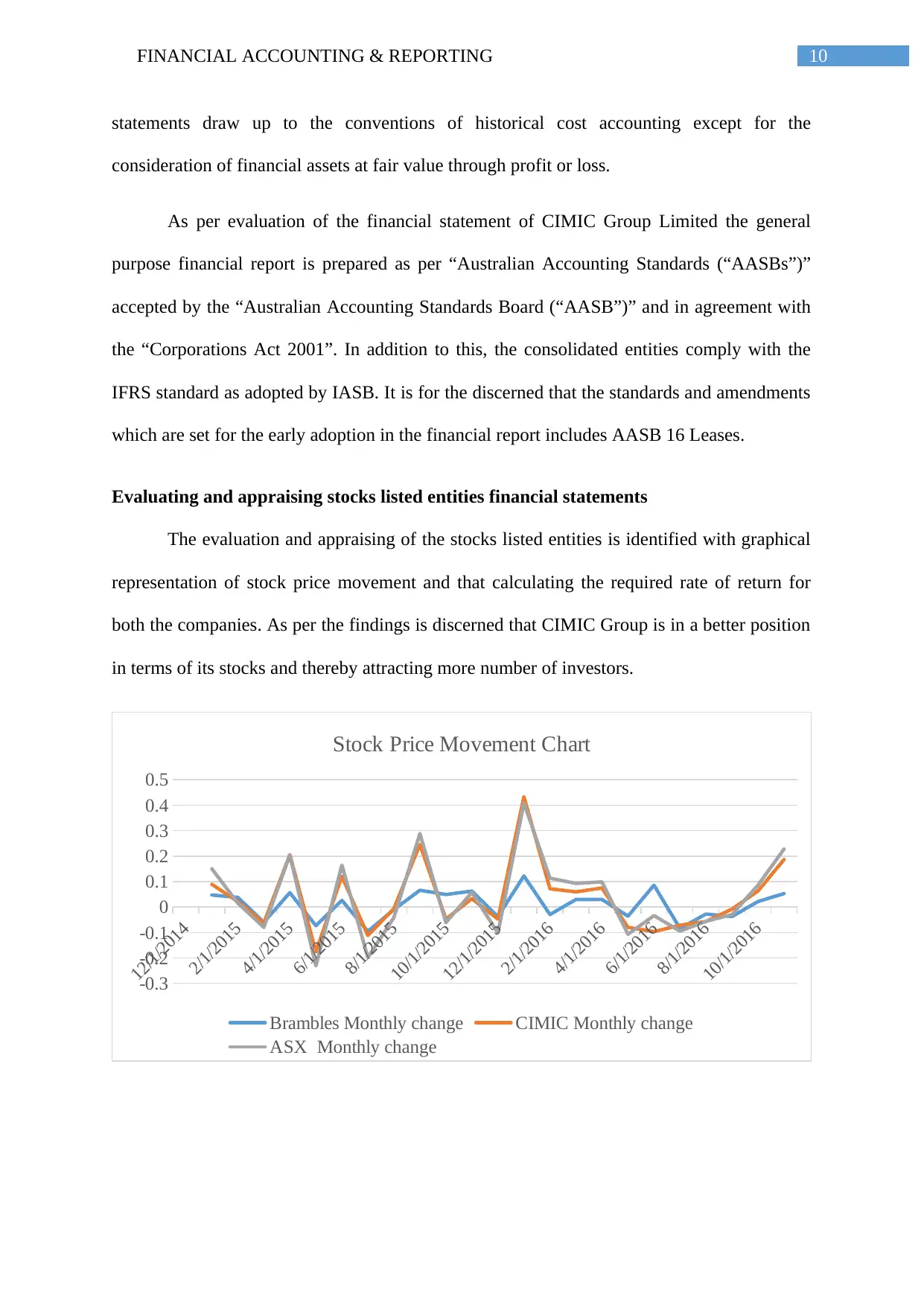

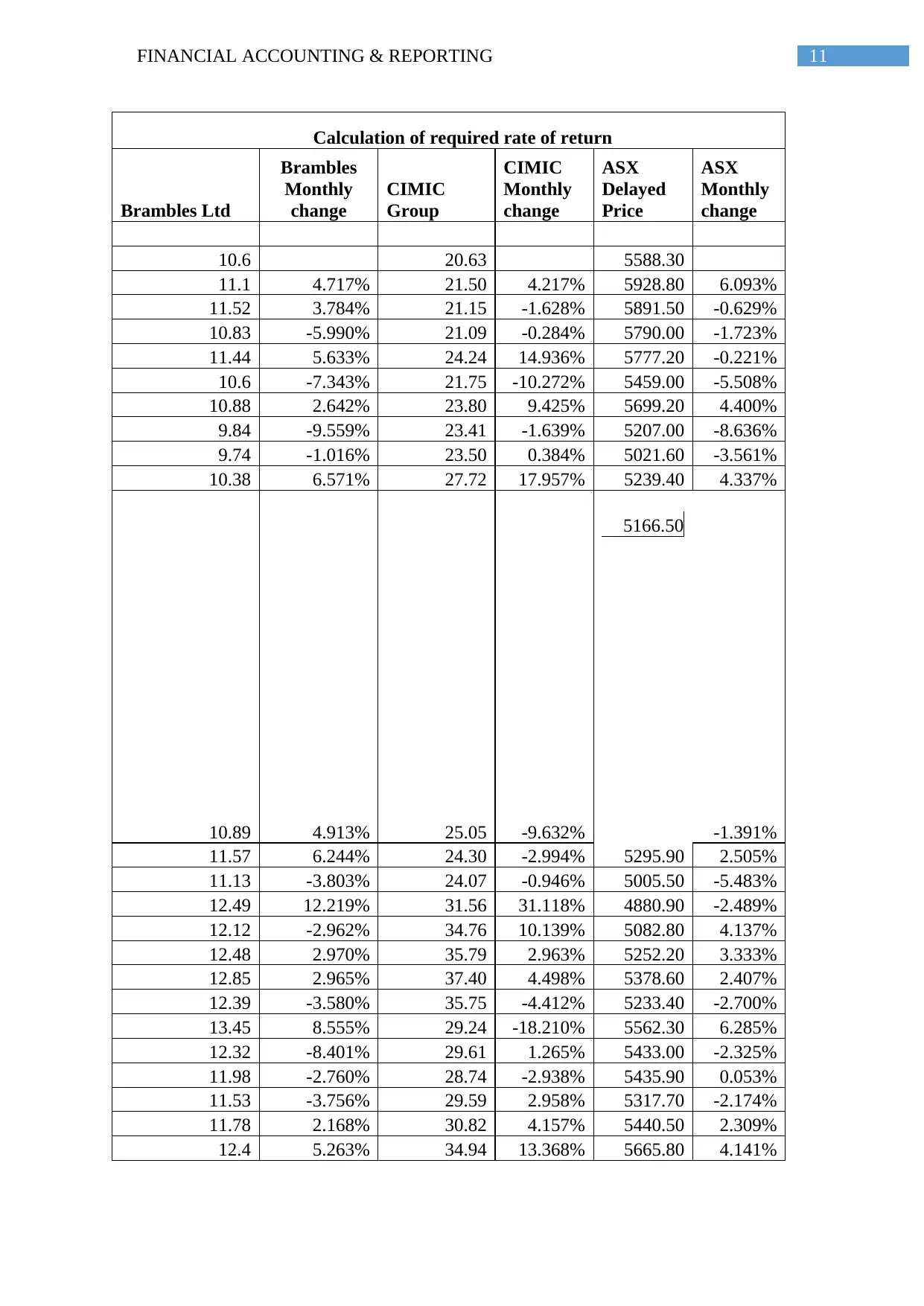

This report provides a comprehensive analysis of financial accounting and reporting, focusing on the application of International Financial Reporting Standards (IFRS) within the context of two companies: Brambles Limited and CIMIC Group Limited. The report discusses the function and role of high-quality financial accounting in the contemporary business environment, emphasizing its importance for accurate financial information, benchmarking, and securing financing. It delves into the application of IFRSs, including the framework for preparing General Purpose Financial Statements (GPFR), and applies financial analytical skills, particularly ratio analysis, to evaluate the financial performance of the two companies. The report also covers designing and developing accounting systems, comparing and contrasting financial accounting systems, evaluating stock-listed entities' financial statements, and developing solutions to ethical issues, all within the framework of IFRS and the Australian Accounting Standards (AAS). The analysis includes profitability, liquidity, debt-equity, and market performance ratios, as well as a calculation of the required rate of return and graphical representations of stock price movements for both companies. The report concludes by addressing ethical considerations in financial reporting, referencing stockholder and stakeholder theories.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.