Financial Accounting Report: Principles, Conventions, and Statements

VerifiedAdded on 2021/01/02

|31

|4337

|373

Report

AI Summary

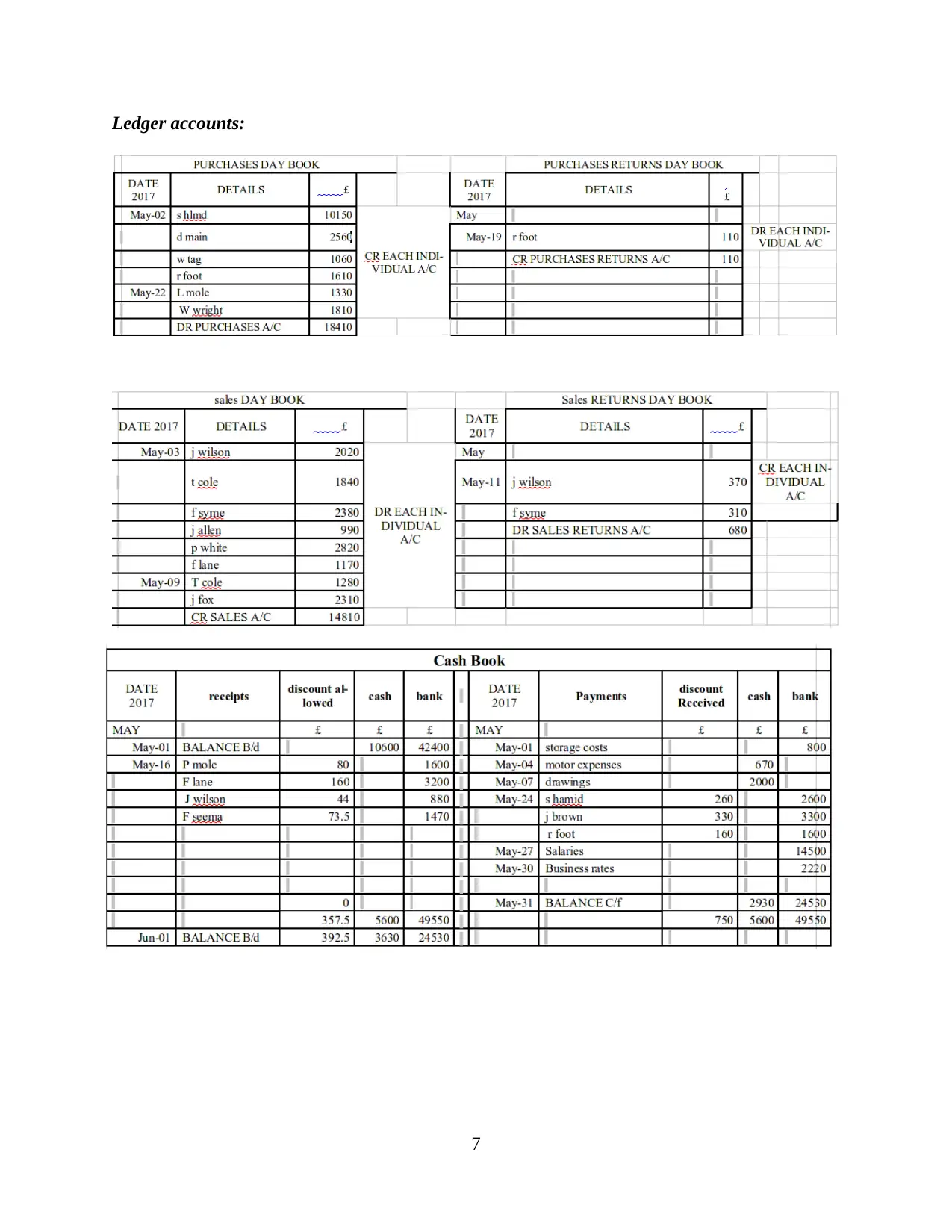

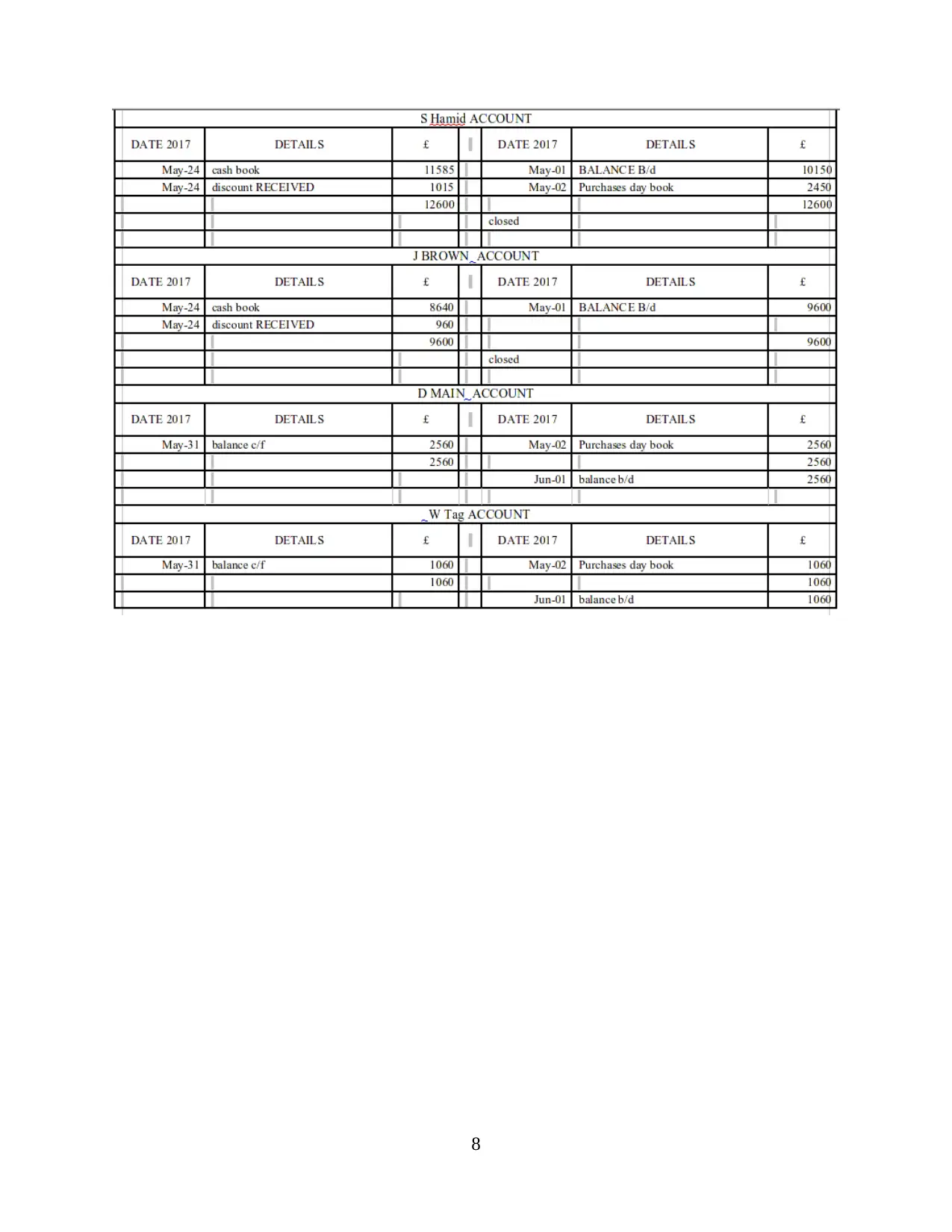

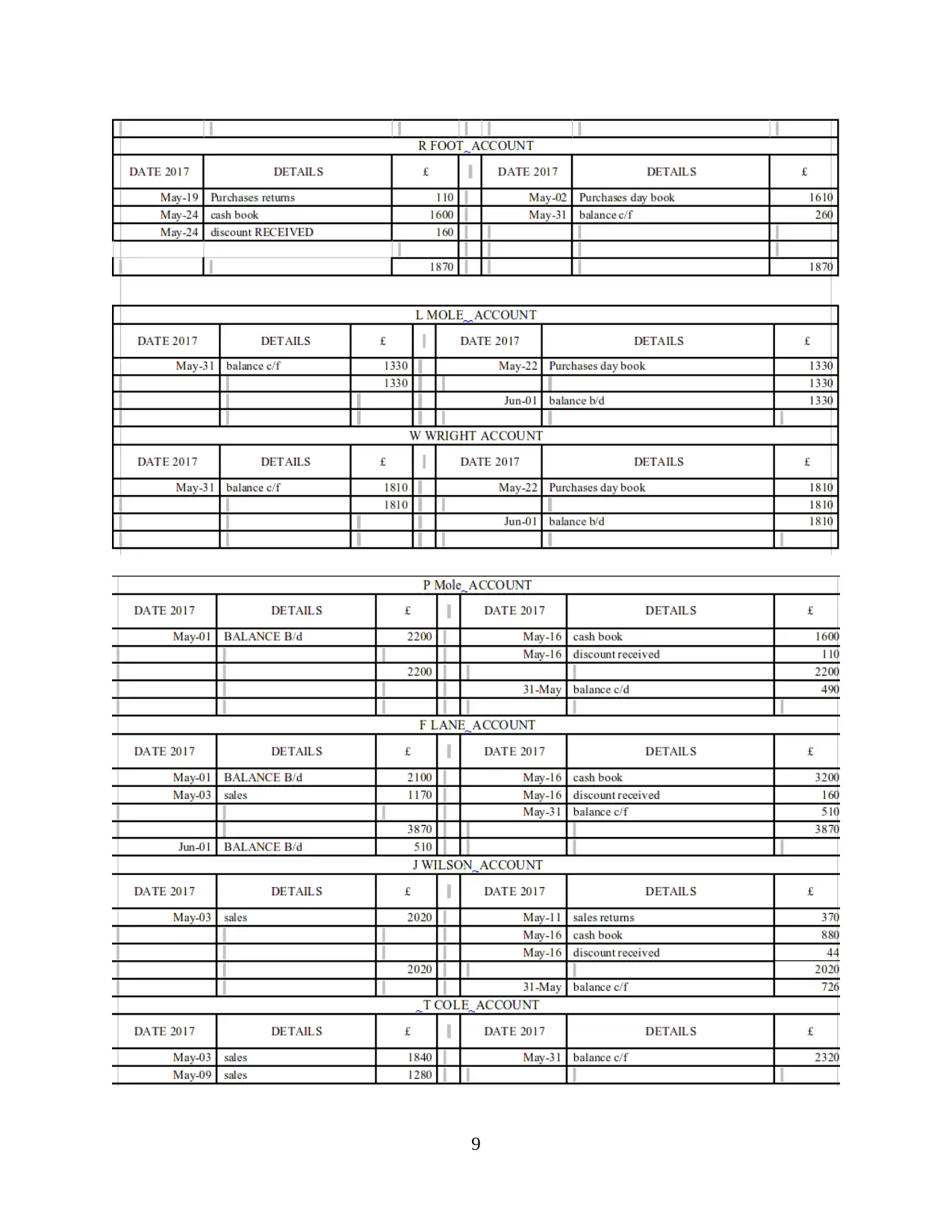

This financial accounting report, prepared for L.V. Audit Kft., provides a comprehensive overview of the subject. It begins by defining financial accounting and its purpose, followed by an examination of relevant regulations, including IASB, IFRS, and GAAP. The report then delves into accounting rules and principles, such as the economic entity assumption, monetary unit assumption, and cost principle. It further explains the concepts of consistency and material disclosure, emphasizing their importance in financial reporting. The report includes practical applications with financial statement analysis for different clients. The report also explains the purpose of preparing bank reconciliation statements, areas which cause records vary with bank records, preparation of accounts through cash flow statements, preparation of sales ledge and purchase ledger accounts and explanation of need for preparing control account. Finally, it concludes with a discussion of the consistency and prudency concepts in accounting.

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.