Financial Accounting Report: Munteanu Ltd. and Bank Reconciliation

VerifiedAdded on 2021/02/22

|15

|3862

|115

Report

AI Summary

This report delves into the core principles of financial accounting, exploring the preparation of final accounts, bank reconciliation processes, and the application of accounting concepts. It begins with an introduction to financial accounting, emphasizing its role in decision-making and financial governance. The report then covers the preparation of financial statements (income statement and balance sheet) for Munteanu Ltd., along with the importance of accounting concepts such as consistency and prudence. It details the meaning and purpose of depreciation, including various methods like straight-line and diminishing balance. Furthermore, the report addresses the differences in financial statement preparation between sole traders and limited companies. The report also explains the bank reconciliation process and its importance for identifying and correcting errors in financial records. Finally, the report covers reconciliation of control accounts and clearing suspense accounts using provided examples.

Financial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

P3 Prepare final accounts with the help of given trial balance....................................................1

P4 Production of final accounts for range of examples...............................................................4

TASK 3............................................................................................................................................6

P5 Apply the bank reconciliation process to prepare a number of bank reconciliation..............6

TASK 5............................................................................................................................................9

P6 Explain the process taken to reconcile control accounts and clear suspense accounts using

given account examples...............................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

P3 Prepare final accounts with the help of given trial balance....................................................1

P4 Production of final accounts for range of examples...............................................................4

TASK 3............................................................................................................................................6

P5 Apply the bank reconciliation process to prepare a number of bank reconciliation..............6

TASK 5............................................................................................................................................9

P6 Explain the process taken to reconcile control accounts and clear suspense accounts using

given account examples...............................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Collection, allocation, bifurcation and recording of financial transactions and information in

appropriate format is considered as a financial accounting. Financial reporting is essential for

organisations in order to track the financial operation and performance of entity. With the crucial

requirement of financial governance, the rules and principles of financial reporting also become

broad in nature (Barron, Chung and Yong, 2016). This report explains the scope and importance

of monetary accounting in the direction of effective decision making and structure planning. Key

financial areas as preparing of final accounts, bank reconciliation statement and control accounts

are covered in this report. Major criteria of this report is focused upon formation of financial

accounts for sole traders, partnership firms and limited companies. Relevant accounting concepts

and principles in order to maintain the ethics while preparing accounts also covered in this

report.

TASK 2

P3 Prepare final accounts with the help of given trial balance

Financial statement: It can be defined as the accounts which are generated by

accounting professionals of companies in order to facilitate the internal as well as external

stakeholders to determine actual position of the company. There are two main types of them

which are as follows:

Income statement: It can be defined as a statement which is used for the purpose of

recording all the incomes and expenses of a company that are faced by it in a specific

time period. With the help of it stakeholders such as share holders, customers employees

and managers can assess that organisation is facing losses or generating profits. It is

beneficial for investors because it guides them to analyse ability of the enterprise to

provide them good returns on the money which will be invested by them in the business

(Chan, 2015).

Balance sheet: It is also known as statement of financial position which helps

stakeholders to monitor that the organisations is financially strong or weak. All the assets

and liabilities are recorded in it by the accounting professionals which are hired by

company to formulate financial statements. Shareholders and investors analyse it to

1

Collection, allocation, bifurcation and recording of financial transactions and information in

appropriate format is considered as a financial accounting. Financial reporting is essential for

organisations in order to track the financial operation and performance of entity. With the crucial

requirement of financial governance, the rules and principles of financial reporting also become

broad in nature (Barron, Chung and Yong, 2016). This report explains the scope and importance

of monetary accounting in the direction of effective decision making and structure planning. Key

financial areas as preparing of final accounts, bank reconciliation statement and control accounts

are covered in this report. Major criteria of this report is focused upon formation of financial

accounts for sole traders, partnership firms and limited companies. Relevant accounting concepts

and principles in order to maintain the ethics while preparing accounts also covered in this

report.

TASK 2

P3 Prepare final accounts with the help of given trial balance

Financial statement: It can be defined as the accounts which are generated by

accounting professionals of companies in order to facilitate the internal as well as external

stakeholders to determine actual position of the company. There are two main types of them

which are as follows:

Income statement: It can be defined as a statement which is used for the purpose of

recording all the incomes and expenses of a company that are faced by it in a specific

time period. With the help of it stakeholders such as share holders, customers employees

and managers can assess that organisation is facing losses or generating profits. It is

beneficial for investors because it guides them to analyse ability of the enterprise to

provide them good returns on the money which will be invested by them in the business

(Chan, 2015).

Balance sheet: It is also known as statement of financial position which helps

stakeholders to monitor that the organisations is financially strong or weak. All the assets

and liabilities are recorded in it by the accounting professionals which are hired by

company to formulate financial statements. Shareholders and investors analyse it to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determine that the enterprise in which funds are invested by them is using them

appropriately or not.

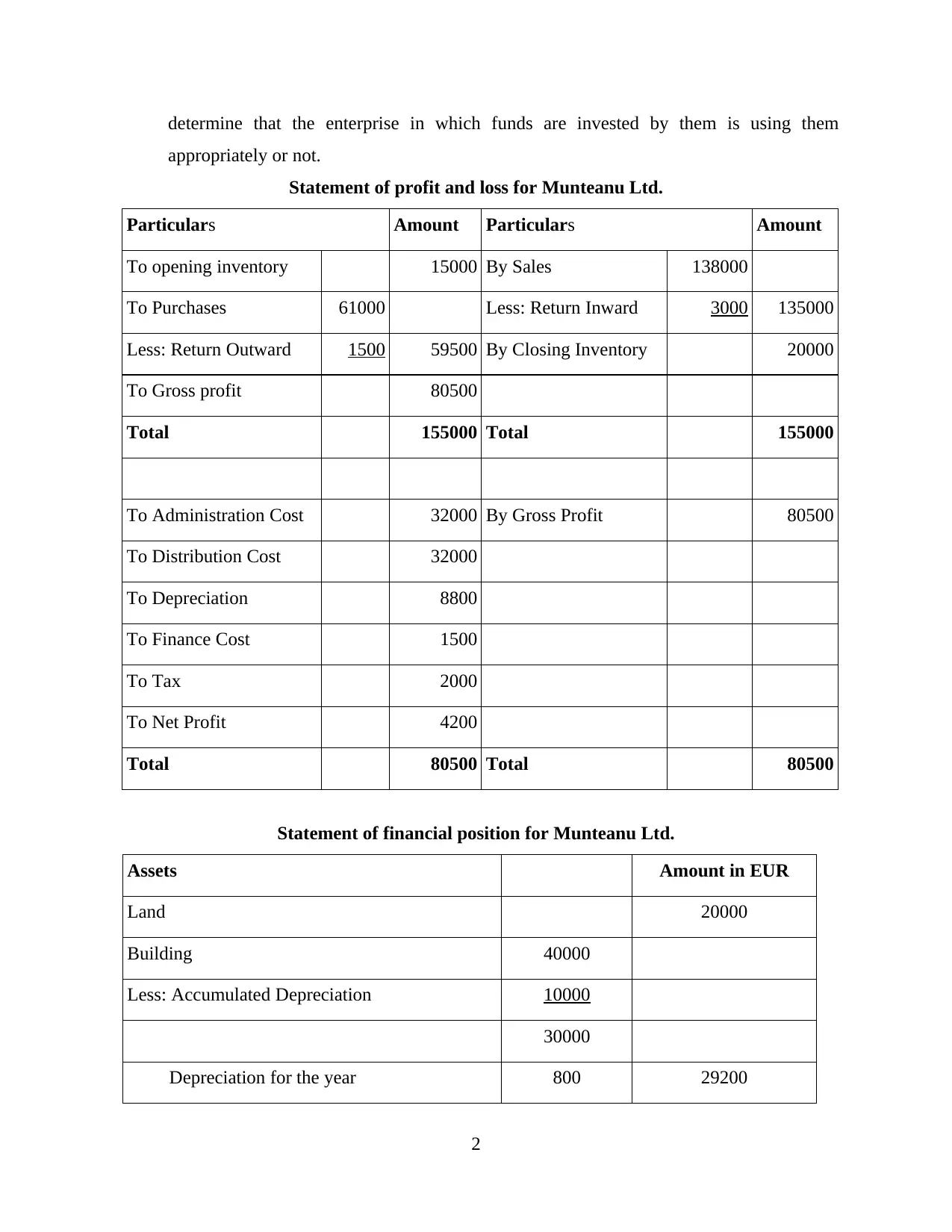

Statement of profit and loss for Munteanu Ltd.

Particulars Amount Particulars Amount

To opening inventory 15000 By Sales 138000

To Purchases 61000 Less: Return Inward 3000 135000

Less: Return Outward 1500 59500 By Closing Inventory 20000

To Gross profit 80500

Total 155000 Total 155000

To Administration Cost 32000 By Gross Profit 80500

To Distribution Cost 32000

To Depreciation 8800

To Finance Cost 1500

To Tax 2000

To Net Profit 4200

Total 80500 Total 80500

Statement of financial position for Munteanu Ltd.

Assets Amount in EUR

Land 20000

Building 40000

Less: Accumulated Depreciation 10000

30000

Depreciation for the year 800 29200

2

appropriately or not.

Statement of profit and loss for Munteanu Ltd.

Particulars Amount Particulars Amount

To opening inventory 15000 By Sales 138000

To Purchases 61000 Less: Return Inward 3000 135000

Less: Return Outward 1500 59500 By Closing Inventory 20000

To Gross profit 80500

Total 155000 Total 155000

To Administration Cost 32000 By Gross Profit 80500

To Distribution Cost 32000

To Depreciation 8800

To Finance Cost 1500

To Tax 2000

To Net Profit 4200

Total 80500 Total 80500

Statement of financial position for Munteanu Ltd.

Assets Amount in EUR

Land 20000

Building 40000

Less: Accumulated Depreciation 10000

30000

Depreciation for the year 800 29200

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

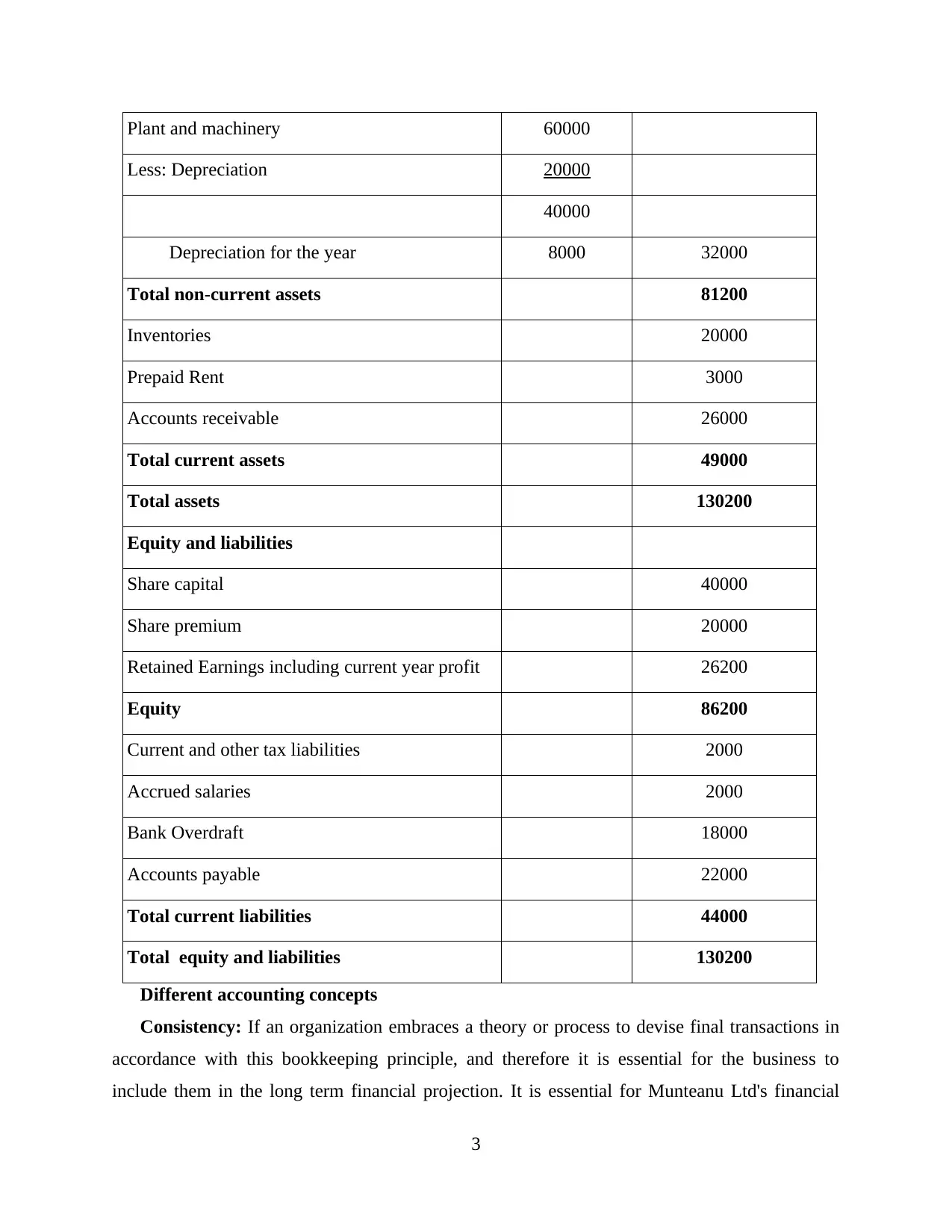

Plant and machinery 60000

Less: Depreciation 20000

40000

Depreciation for the year 8000 32000

Total non-current assets 81200

Inventories 20000

Prepaid Rent 3000

Accounts receivable 26000

Total current assets 49000

Total assets 130200

Equity and liabilities

Share capital 40000

Share premium 20000

Retained Earnings including current year profit 26200

Equity 86200

Current and other tax liabilities 2000

Accrued salaries 2000

Bank Overdraft 18000

Accounts payable 22000

Total current liabilities 44000

Total equity and liabilities 130200

Different accounting concepts

Consistency: If an organization embraces a theory or process to devise final transactions in

accordance with this bookkeeping principle, and therefore it is essential for the business to

include them in the long term financial projection. It is essential for Munteanu Ltd's financial

3

Less: Depreciation 20000

40000

Depreciation for the year 8000 32000

Total non-current assets 81200

Inventories 20000

Prepaid Rent 3000

Accounts receivable 26000

Total current assets 49000

Total assets 130200

Equity and liabilities

Share capital 40000

Share premium 20000

Retained Earnings including current year profit 26200

Equity 86200

Current and other tax liabilities 2000

Accrued salaries 2000

Bank Overdraft 18000

Accounts payable 22000

Total current liabilities 44000

Total equity and liabilities 130200

Different accounting concepts

Consistency: If an organization embraces a theory or process to devise final transactions in

accordance with this bookkeeping principle, and therefore it is essential for the business to

include them in the long term financial projection. It is essential for Munteanu Ltd's financial

3

experts to pursue these accounting concepts in order to form coherent financials to enable

shareholders to increase the rate of yield that they will be able to obtain throughout the future.

Reporting techniques may be changed unless the current model could enhance the accounts in

the very same manner (Drexler, Fischer and Schoar, 2014).

Prudency: It directs corporate businesses to disregard investment and profits overriding and

make clauses for potential expenditures and expenses to preserve the business's excellent

deliverables. This is also regarded as either the concept of progressivism, that is deemed one of

several major management notions. By utilising this concept managers of Munteanu Ltd. Be able

to elude over estimation of revenues and under estimation of expenses subject to effective

formulation of financial statements of organisation. However, auditors historically do not expect

earnings, providing for all liabilities. Until they can be received, revenues are not compensated

for. But, when there is a sensible chance that these playouts as well as expenditures will happen

in the long term, bookkeepers pursue for all probable revenues and expenditures (Edwards,

Schwab and Shevlin, 2015).

Meaning and purpose of depreciation: Depreciation is recognised as an impairment or

deficiency occurs due to regular use or devaluing of lifecycle of assets. For taxation planning as

well as reporting procedures, most of them are devalued by businesses. When determining

depreciation, distinct components that also include resale value, asset life and price are assessed

in accounting. One of the important fact is also required to consider while evaluating the amount

of depreciation that is capitalisation concept. Matching principle of accounting states that amount

of assets are required to capitalised while purchasing by debiting the account of fixed assets and

crediting the amount of accounts payables or cash (Jiang, Wang and Xie, 2015).

Methods of depreciation: Methods are also classified in major four categories as straight

line, double declining or diminishing balance, unit of production and sum of years digit method.

Straight line and diminishing balance method is one of the popular methods used by

organisations in general terms.

Diminishing balancing method: If businesses were prepared to raise product efficiency,

this technique is used and its business acquires various advantages. Throughout this technique,

amortization during the first year is added to both the book value of an asset and is measured on

WDV in the remainder of this year. the value of assets does not become zero in this method.

4

shareholders to increase the rate of yield that they will be able to obtain throughout the future.

Reporting techniques may be changed unless the current model could enhance the accounts in

the very same manner (Drexler, Fischer and Schoar, 2014).

Prudency: It directs corporate businesses to disregard investment and profits overriding and

make clauses for potential expenditures and expenses to preserve the business's excellent

deliverables. This is also regarded as either the concept of progressivism, that is deemed one of

several major management notions. By utilising this concept managers of Munteanu Ltd. Be able

to elude over estimation of revenues and under estimation of expenses subject to effective

formulation of financial statements of organisation. However, auditors historically do not expect

earnings, providing for all liabilities. Until they can be received, revenues are not compensated

for. But, when there is a sensible chance that these playouts as well as expenditures will happen

in the long term, bookkeepers pursue for all probable revenues and expenditures (Edwards,

Schwab and Shevlin, 2015).

Meaning and purpose of depreciation: Depreciation is recognised as an impairment or

deficiency occurs due to regular use or devaluing of lifecycle of assets. For taxation planning as

well as reporting procedures, most of them are devalued by businesses. When determining

depreciation, distinct components that also include resale value, asset life and price are assessed

in accounting. One of the important fact is also required to consider while evaluating the amount

of depreciation that is capitalisation concept. Matching principle of accounting states that amount

of assets are required to capitalised while purchasing by debiting the account of fixed assets and

crediting the amount of accounts payables or cash (Jiang, Wang and Xie, 2015).

Methods of depreciation: Methods are also classified in major four categories as straight

line, double declining or diminishing balance, unit of production and sum of years digit method.

Straight line and diminishing balance method is one of the popular methods used by

organisations in general terms.

Diminishing balancing method: If businesses were prepared to raise product efficiency,

this technique is used and its business acquires various advantages. Throughout this technique,

amortization during the first year is added to both the book value of an asset and is measured on

WDV in the remainder of this year. the value of assets does not become zero in this method.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Straight line method: It is utilized in this condition if there's no specific sequence on

how the assets will be operated over a period of time. It is regarded to be the simplest way to

apply dep on various company assets and its ease outcomes in low likelihood of mistakes in

accounting books. This method is beneficial for those organisations that operates a fixed

production line or manufacturing process. There is a fixed rate of depreciation is used in this

method that helps in write off the value of assets in systematic format (Kaplan and Atkinson,

2015).

P4 Production of final accounts for range of examples

Sole trading company: A business which is executed by a single person is known as

sole trading company and the individual who is owner of it is known as sole trader. All the

decisions regarding business execution are taken by the proprietor of business. If the decision

maker is willing to hire people to run the business then they could be hired by owner.

Limited company: An organisation which is limited by shares or guarantee is known as

this type of business. In such types of enterprises shareholders take dividend from the profits

which are generated by the organisation in a specific time period.

Difference between financial statements prepared by sole trader and limited

companies:

Sole trader Limited company

There is only one entry in the owner's equity of

sole trader in balance sheet of the company.

This amount is the money which is invested by

owner in the business while establishing it.

There are ample number of figures in the

owner's equity in limited company's balance

sheet. These are equity share capital,

preference share capital, net profits and

retained earnings (Difference between financial

statements of sole trader and limited company,

2019).

As there is no requirement of auditing of

financial statements of sole trader so there is

no set format for creating income statement.

All the limited companies are required to

formulate income statements according to legal

implications which are set by government of

the country.

The tax which is applied by the sole trader will In limited companies tax is implemented on the

5

how the assets will be operated over a period of time. It is regarded to be the simplest way to

apply dep on various company assets and its ease outcomes in low likelihood of mistakes in

accounting books. This method is beneficial for those organisations that operates a fixed

production line or manufacturing process. There is a fixed rate of depreciation is used in this

method that helps in write off the value of assets in systematic format (Kaplan and Atkinson,

2015).

P4 Production of final accounts for range of examples

Sole trading company: A business which is executed by a single person is known as

sole trading company and the individual who is owner of it is known as sole trader. All the

decisions regarding business execution are taken by the proprietor of business. If the decision

maker is willing to hire people to run the business then they could be hired by owner.

Limited company: An organisation which is limited by shares or guarantee is known as

this type of business. In such types of enterprises shareholders take dividend from the profits

which are generated by the organisation in a specific time period.

Difference between financial statements prepared by sole trader and limited

companies:

Sole trader Limited company

There is only one entry in the owner's equity of

sole trader in balance sheet of the company.

This amount is the money which is invested by

owner in the business while establishing it.

There are ample number of figures in the

owner's equity in limited company's balance

sheet. These are equity share capital,

preference share capital, net profits and

retained earnings (Difference between financial

statements of sole trader and limited company,

2019).

As there is no requirement of auditing of

financial statements of sole trader so there is

no set format for creating income statement.

All the limited companies are required to

formulate income statements according to legal

implications which are set by government of

the country.

The tax which is applied by the sole trader will In limited companies tax is implemented on the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be paid on the income which is generated by

owner.

profits which are generated by the company in

a specific time period.

The debts which are related to business

becomes the owner's debt because all the

profits and losses are faced by single person.

Limited liability company's final accounts are

generated by following separate entity concept

in which all the debts of business are paid from

the profits generated by the organisation.

Sole traders are not legally required to

formulate financial statements because it is

willingness of the owner to apply for a tax

return or not.

For all the limited companies it is very

important to create financial statements

because they are required to file for a income

tax return every year.

The value of assets is very low as compare to

the limited companies.

In Limited companies value of assets is very

high as compare to the business which is

executed by a single person.

All the records which are generated in sole

trader business are created by the owner.

The limited companies are required to hire

accounting professionals and establish a

accounting department in order to form final

accounts.

The owner is the employer of the company and

the only person who is responsible to take

decisions for business.

There are end number of employees are hired

by limited companies in order to execute all the

operations successfully (Kim and Zhang,

2016).

Losses and profits could be added to the

personal account of owner.

Incomes and losses are not reflected in owner's

account because the organisation and business

man both are considered separate.

TASK 3

P5 Apply the bank reconciliation process to prepare a number of bank reconciliation

Bank Reconciliation – A bank Reconciliation statement is a document that similar the

cash balance on a company's balance sheet. Through reconciliation find out any problem exist in

the two accounts after that made changes as per the requirement. It is completely at regular

6

owner.

profits which are generated by the company in

a specific time period.

The debts which are related to business

becomes the owner's debt because all the

profits and losses are faced by single person.

Limited liability company's final accounts are

generated by following separate entity concept

in which all the debts of business are paid from

the profits generated by the organisation.

Sole traders are not legally required to

formulate financial statements because it is

willingness of the owner to apply for a tax

return or not.

For all the limited companies it is very

important to create financial statements

because they are required to file for a income

tax return every year.

The value of assets is very low as compare to

the limited companies.

In Limited companies value of assets is very

high as compare to the business which is

executed by a single person.

All the records which are generated in sole

trader business are created by the owner.

The limited companies are required to hire

accounting professionals and establish a

accounting department in order to form final

accounts.

The owner is the employer of the company and

the only person who is responsible to take

decisions for business.

There are end number of employees are hired

by limited companies in order to execute all the

operations successfully (Kim and Zhang,

2016).

Losses and profits could be added to the

personal account of owner.

Incomes and losses are not reflected in owner's

account because the organisation and business

man both are considered separate.

TASK 3

P5 Apply the bank reconciliation process to prepare a number of bank reconciliation

Bank Reconciliation – A bank Reconciliation statement is a document that similar the

cash balance on a company's balance sheet. Through reconciliation find out any problem exist in

the two accounts after that made changes as per the requirement. It is completely at regular

6

intervals to assure that company records are corrected. It also help to aware from the fraud and

any cash manipulations (Lara, Osma and Penalva, 2016).

Purpose – Herein, below some purpose of preparing the bank reconciliation accounts are as

follows:

To check the errors – The main purpose of the bank reconciliation to find out the errors

that are become reason of inequality into both accounts. It means both accounts are not

matched.

Detecting the frauds – Another purpose of bank reconciliation statement tat easily

detecting frauds as well as errors that happened in the accounting books.

Provide clarity – Additionally, the bank reconciliation statement provide clarity and

helps to record amount at right place.

Match both accounts – Along with, the purpose of bank reconciliation that natch bank

statement with the cash balance it there is fining out any problem that find out in own

way.

Reason for differences between bank statement and company's accounting record -

If banks send bank statements to companies that time company include starting cash

balance as well as transaction during the financial accounting period of time and ending cash

balance. Most of the time it is identified that company's ending cash balance will never match

with the bank balance. There are defining some reasons of the differences such as - Deposit in transit – Cash and cheques has been received by the company but does not

recorded in the accounting books as well as bank statement. Outstanding checks – Many time cheques have been issued by the company but does not

depositor deposit into the bank so that time enter into the cash book but does not in the

bank statement. Bank service fees – Bank reduce charges of services that provide to clients but these

amounts are usually not detectable (Mussari, 2014). Interest income – Many times companies pay interest to bank regarding to loan and any

reason that was not recorded in the cash book.

Not sufficient funds (NSF) Checks – When a client deposit a cheque into an account but

the account of the issuer have not sufficient amount to pay regarding to cheque that time

7

any cash manipulations (Lara, Osma and Penalva, 2016).

Purpose – Herein, below some purpose of preparing the bank reconciliation accounts are as

follows:

To check the errors – The main purpose of the bank reconciliation to find out the errors

that are become reason of inequality into both accounts. It means both accounts are not

matched.

Detecting the frauds – Another purpose of bank reconciliation statement tat easily

detecting frauds as well as errors that happened in the accounting books.

Provide clarity – Additionally, the bank reconciliation statement provide clarity and

helps to record amount at right place.

Match both accounts – Along with, the purpose of bank reconciliation that natch bank

statement with the cash balance it there is fining out any problem that find out in own

way.

Reason for differences between bank statement and company's accounting record -

If banks send bank statements to companies that time company include starting cash

balance as well as transaction during the financial accounting period of time and ending cash

balance. Most of the time it is identified that company's ending cash balance will never match

with the bank balance. There are defining some reasons of the differences such as - Deposit in transit – Cash and cheques has been received by the company but does not

recorded in the accounting books as well as bank statement. Outstanding checks – Many time cheques have been issued by the company but does not

depositor deposit into the bank so that time enter into the cash book but does not in the

bank statement. Bank service fees – Bank reduce charges of services that provide to clients but these

amounts are usually not detectable (Mussari, 2014). Interest income – Many times companies pay interest to bank regarding to loan and any

reason that was not recorded in the cash book.

Not sufficient funds (NSF) Checks – When a client deposit a cheque into an account but

the account of the issuer have not sufficient amount to pay regarding to cheque that time

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

bank deduct from the client's account that was previously credited. The cheque is then

returned to the client as an NSF cheque.

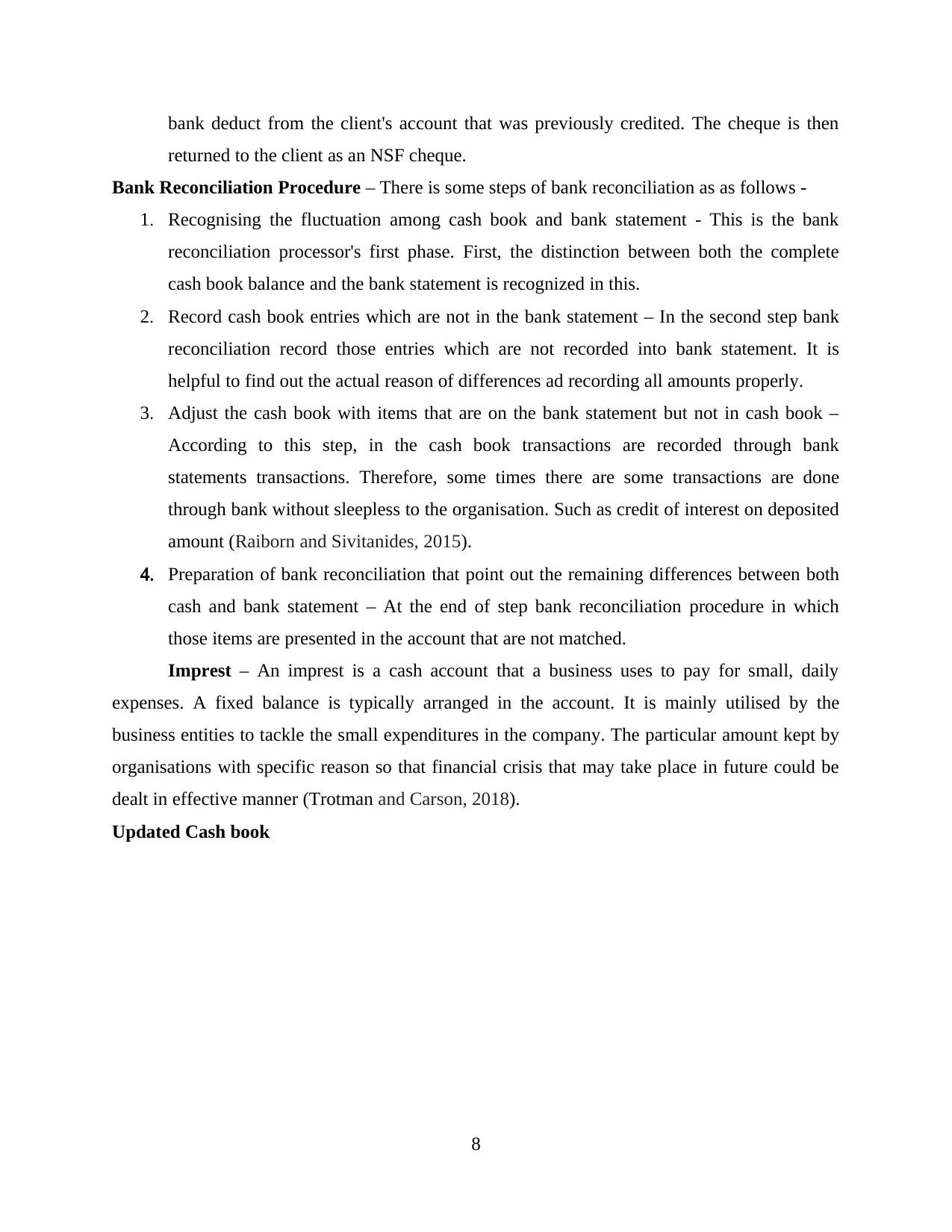

Bank Reconciliation Procedure – There is some steps of bank reconciliation as as follows -

1. Recognising the fluctuation among cash book and bank statement - This is the bank

reconciliation processor's first phase. First, the distinction between both the complete

cash book balance and the bank statement is recognized in this.

2. Record cash book entries which are not in the bank statement – In the second step bank

reconciliation record those entries which are not recorded into bank statement. It is

helpful to find out the actual reason of differences ad recording all amounts properly.

3. Adjust the cash book with items that are on the bank statement but not in cash book –

According to this step, in the cash book transactions are recorded through bank

statements transactions. Therefore, some times there are some transactions are done

through bank without sleepless to the organisation. Such as credit of interest on deposited

amount (Raiborn and Sivitanides, 2015).

4. Preparation of bank reconciliation that point out the remaining differences between both

cash and bank statement – At the end of step bank reconciliation procedure in which

those items are presented in the account that are not matched.

Imprest – An imprest is a cash account that a business uses to pay for small, daily

expenses. A fixed balance is typically arranged in the account. It is mainly utilised by the

business entities to tackle the small expenditures in the company. The particular amount kept by

organisations with specific reason so that financial crisis that may take place in future could be

dealt in effective manner (Trotman and Carson, 2018).

Updated Cash book

8

returned to the client as an NSF cheque.

Bank Reconciliation Procedure – There is some steps of bank reconciliation as as follows -

1. Recognising the fluctuation among cash book and bank statement - This is the bank

reconciliation processor's first phase. First, the distinction between both the complete

cash book balance and the bank statement is recognized in this.

2. Record cash book entries which are not in the bank statement – In the second step bank

reconciliation record those entries which are not recorded into bank statement. It is

helpful to find out the actual reason of differences ad recording all amounts properly.

3. Adjust the cash book with items that are on the bank statement but not in cash book –

According to this step, in the cash book transactions are recorded through bank

statements transactions. Therefore, some times there are some transactions are done

through bank without sleepless to the organisation. Such as credit of interest on deposited

amount (Raiborn and Sivitanides, 2015).

4. Preparation of bank reconciliation that point out the remaining differences between both

cash and bank statement – At the end of step bank reconciliation procedure in which

those items are presented in the account that are not matched.

Imprest – An imprest is a cash account that a business uses to pay for small, daily

expenses. A fixed balance is typically arranged in the account. It is mainly utilised by the

business entities to tackle the small expenditures in the company. The particular amount kept by

organisations with specific reason so that financial crisis that may take place in future could be

dealt in effective manner (Trotman and Carson, 2018).

Updated Cash book

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank Reconciliation statement

Particulars Amount

Bank Balance as per pass book 398

Add: Items having effects of higher balance in cash

book

Bank charges not recorded in cash book...... 36

Adjustment for direct debit rates.............. 105

Less: Items having effects of lower balance in cash

book

9

Particulars Amount

Bank Balance as per pass book 398

Add: Items having effects of higher balance in cash

book

Bank charges not recorded in cash book...... 36

Adjustment for direct debit rates.............. 105

Less: Items having effects of lower balance in cash

book

9

Payments to:

5. C David 122

S Leeming 116

C Lyons 87

Bank balance as per cash book 214

TASK 5

P6 Explain the process taken to reconcile control accounts and clear suspense accounts using

given account examples

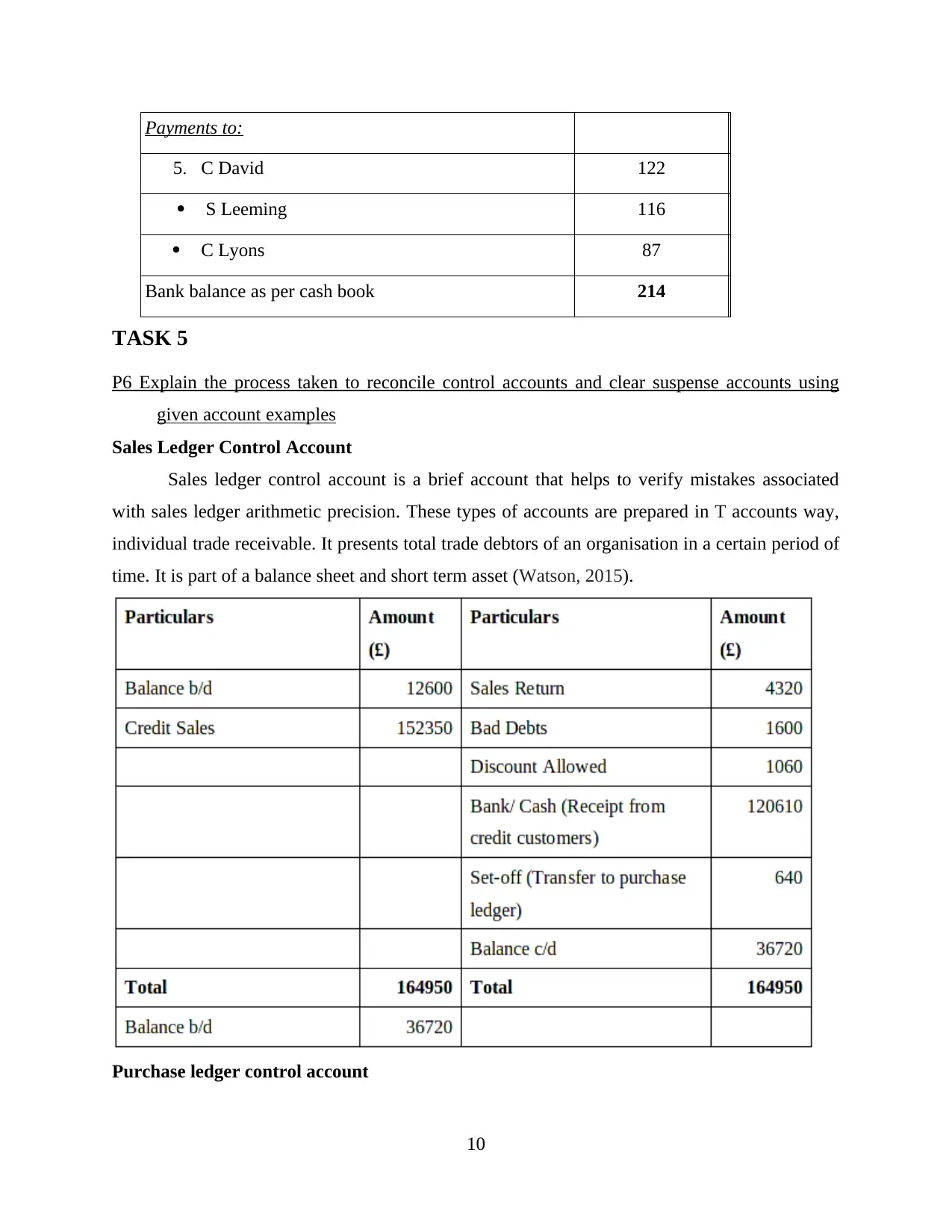

Sales Ledger Control Account

Sales ledger control account is a brief account that helps to verify mistakes associated

with sales ledger arithmetic precision. These types of accounts are prepared in T accounts way,

individual trade receivable. It presents total trade debtors of an organisation in a certain period of

time. It is part of a balance sheet and short term asset (Watson, 2015).

Purchase ledger control account

10

5. C David 122

S Leeming 116

C Lyons 87

Bank balance as per cash book 214

TASK 5

P6 Explain the process taken to reconcile control accounts and clear suspense accounts using

given account examples

Sales Ledger Control Account

Sales ledger control account is a brief account that helps to verify mistakes associated

with sales ledger arithmetic precision. These types of accounts are prepared in T accounts way,

individual trade receivable. It presents total trade debtors of an organisation in a certain period of

time. It is part of a balance sheet and short term asset (Watson, 2015).

Purchase ledger control account

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.