Financial Accounting: Final Accounts and Bank Reconciliation

VerifiedAdded on 2023/01/18

|16

|2919

|79

Report

AI Summary

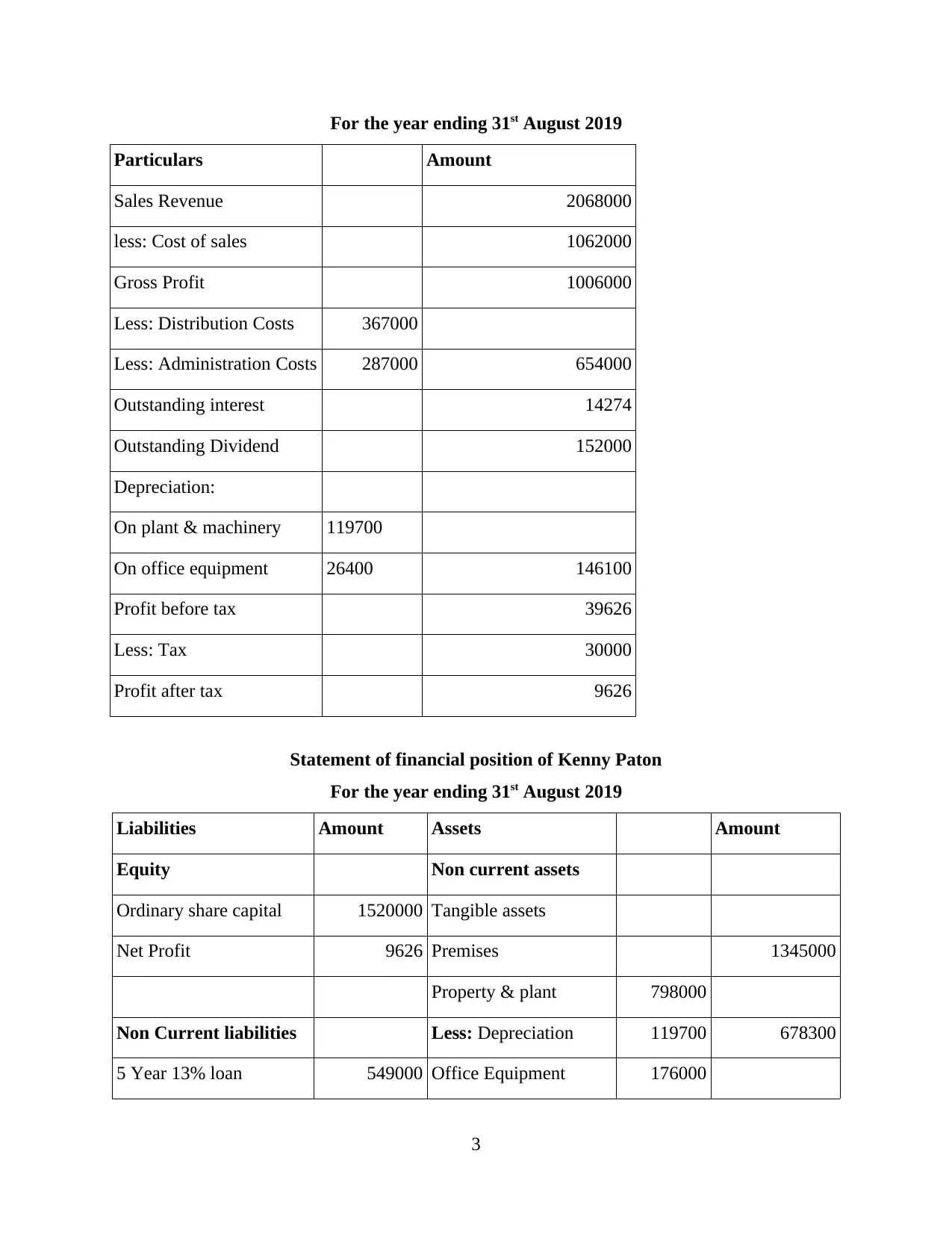

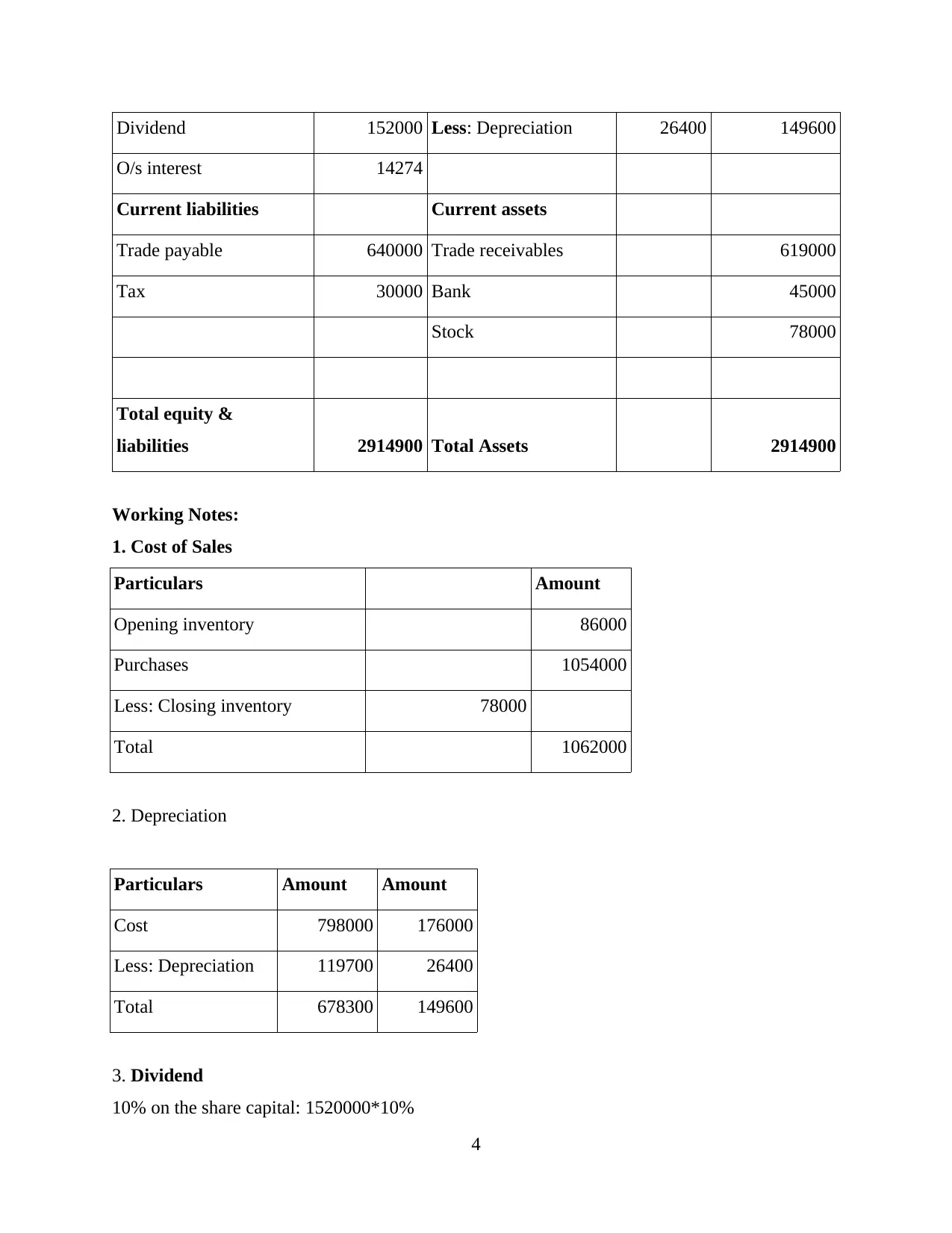

This report delves into the core principles of financial accounting, exploring the processes of recording, summarizing, and reporting business transactions to generate financial statements. It details the preparation of final accounts, including income statements, balance sheets, and cash flow statements, and their significance for external stakeholders such as investors and creditors. The report includes examples of profit and loss accounts, statements of financial position, and bank reconciliation statements, explaining their components and purposes. It also highlights the differences between income statements and statements of financial position in terms of timing, items reported, and their use for management and lenders. Furthermore, the report discusses the importance of control accounts and suspense accounts, including their reconciliation procedures, providing a comprehensive overview of financial accounting practices and their role in presenting an accurate view of an organization's financial performance.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.