Analysis of Financial Accounting Concepts: Accounting 1 Report

VerifiedAdded on 2023/01/10

|21

|4292

|44

Report

AI Summary

This report provides a comprehensive analysis of financial accounting principles and practices, divided into two scenarios. Scenario 1 explores various business transactions, including internal and external transactions, and contrasts single and double-entry bookkeeping systems. It delves into journal entries, ledger accounts, trial balances, and the preparation of profit and loss accounts and balance sheets. The report also differentiates between financial statements and financial reports and examines fundamental accounting principles. Scenario 2 focuses on practical applications, specifically bank reconciliation, control accounts, and suspense accounts, demonstrating the practical implications of these concepts through rectification accounts and updated cash books. The report concludes with a thorough understanding of financial accounting concepts.

Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

SCENARIO 1..................................................................................................................................3

Question 1:...................................................................................................................................3

Question 2....................................................................................................................................5

Question 3: Difference between financial statement and financial report.................................10

Question 4: Fundamental principles of accounting...................................................................12

Question 5..................................................................................................................................13

SCENARIO 2................................................................................................................................14

Question 1: Bank reconciliation................................................................................................14

Question 2: Control accounts.....................................................................................................15

Question 3: Suspense account...................................................................................................16

Question 4..................................................................................................................................17

Question 5..................................................................................................................................18

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

2

SCENARIO 1..................................................................................................................................3

Question 1:...................................................................................................................................3

Question 2....................................................................................................................................5

Question 3: Difference between financial statement and financial report.................................10

Question 4: Fundamental principles of accounting...................................................................12

Question 5..................................................................................................................................13

SCENARIO 2................................................................................................................................14

Question 1: Bank reconciliation................................................................................................14

Question 2: Control accounts.....................................................................................................15

Question 3: Suspense account...................................................................................................16

Question 4..................................................................................................................................17

Question 5..................................................................................................................................18

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

2

INTRODUCTION

Financial accounting is a concept of recording, classifying, analysing and evaluating the

financial transactions of an organisation. This process requires special skills of knowledge of

financial theories and concepts (Berry, 2018). The main aim of this report is to build an

understanding regarding the double entry system and the process of recording a business

transaction. For this purpose, this report is classified into two sections.

The first section of this report will address five questions related to different types of

business transactions. In these section journal entries, ledger accounts, trial balance, P&L

account and balance sheet will be developed along with analysing the difference between

financial statement and financial report. In the second section of this report, the concepts of

suspense account and control account are analysed along with bank reconciliation. This section

will represent the practical implication of such concepts by the use of rectification account and

updated cash book.

SCENARIO 1

Question 1:

Types of business transaction

Business transaction is an event which has occurred in an economic organisation which

can be measured in terms of money. Such events have a financial impact on the organisation.

There are different types of business transactions and in this case, all these business transactions

are classified as external and internal transactions.

Internal transactions are those events in which no external parties such as investors,

supplier or debtors are involved. These transactions are does not include any exchange of money

with external parties but its occurrence highly impacts financial position of the organisation.

These transactions include depreciation, accumulated depreciation, realising of losses and many

more (Cascino and et.al, 2019).

On the other hand external business transactions are opposite of above transactions as it

includes involvement of external parties as well. Business entity exchanges money from external

parties for such transactions and the scope of such transactions are much higher than the internal.

These transactions include purchase of raw material from suppliers, sales of finished goods to

customers, purchase of current and non-current assets, purchasing services from external service

3

Financial accounting is a concept of recording, classifying, analysing and evaluating the

financial transactions of an organisation. This process requires special skills of knowledge of

financial theories and concepts (Berry, 2018). The main aim of this report is to build an

understanding regarding the double entry system and the process of recording a business

transaction. For this purpose, this report is classified into two sections.

The first section of this report will address five questions related to different types of

business transactions. In these section journal entries, ledger accounts, trial balance, P&L

account and balance sheet will be developed along with analysing the difference between

financial statement and financial report. In the second section of this report, the concepts of

suspense account and control account are analysed along with bank reconciliation. This section

will represent the practical implication of such concepts by the use of rectification account and

updated cash book.

SCENARIO 1

Question 1:

Types of business transaction

Business transaction is an event which has occurred in an economic organisation which

can be measured in terms of money. Such events have a financial impact on the organisation.

There are different types of business transactions and in this case, all these business transactions

are classified as external and internal transactions.

Internal transactions are those events in which no external parties such as investors,

supplier or debtors are involved. These transactions are does not include any exchange of money

with external parties but its occurrence highly impacts financial position of the organisation.

These transactions include depreciation, accumulated depreciation, realising of losses and many

more (Cascino and et.al, 2019).

On the other hand external business transactions are opposite of above transactions as it

includes involvement of external parties as well. Business entity exchanges money from external

parties for such transactions and the scope of such transactions are much higher than the internal.

These transactions include purchase of raw material from suppliers, sales of finished goods to

customers, purchase of current and non-current assets, purchasing services from external service

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

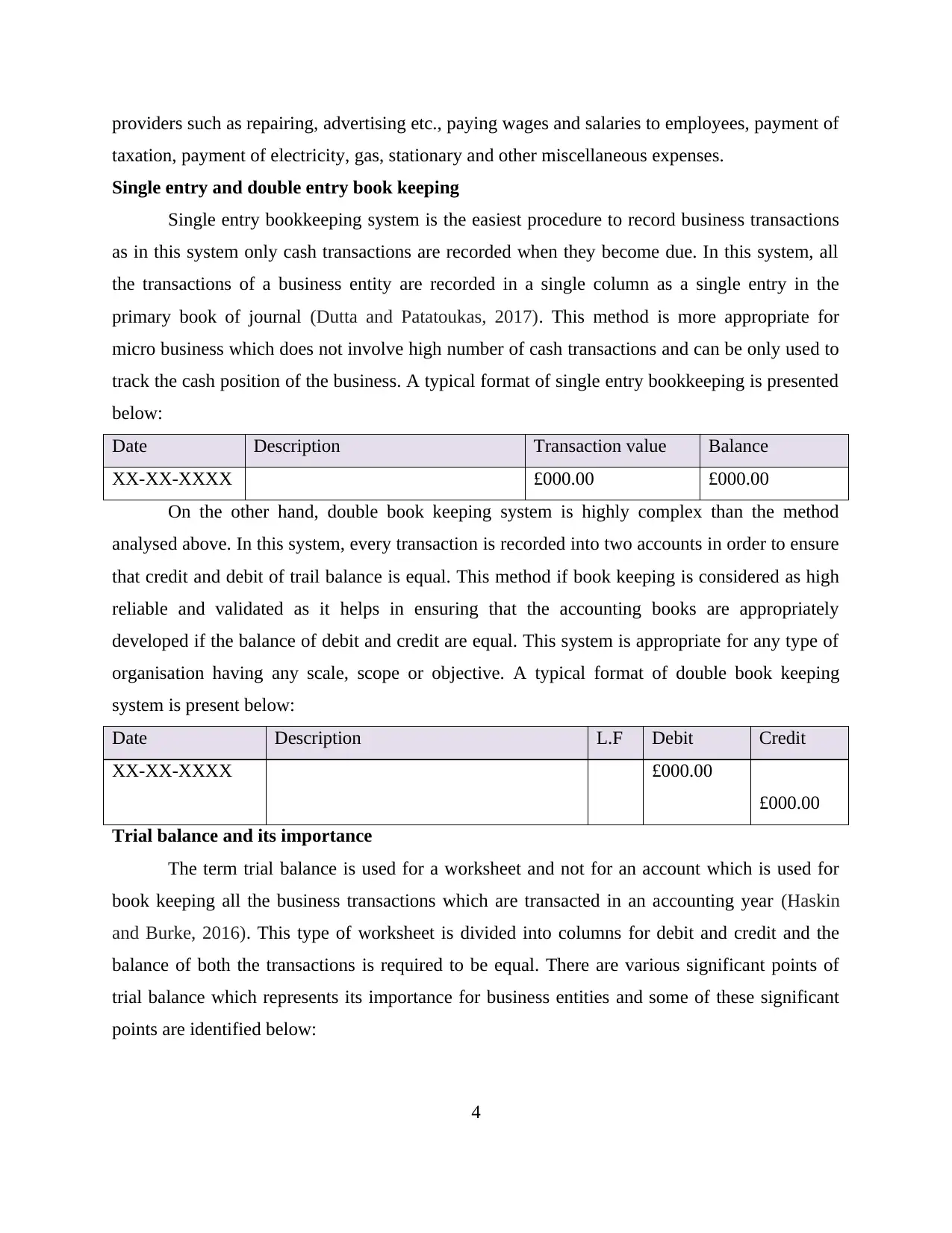

providers such as repairing, advertising etc., paying wages and salaries to employees, payment of

taxation, payment of electricity, gas, stationary and other miscellaneous expenses.

Single entry and double entry book keeping

Single entry bookkeeping system is the easiest procedure to record business transactions

as in this system only cash transactions are recorded when they become due. In this system, all

the transactions of a business entity are recorded in a single column as a single entry in the

primary book of journal (Dutta and Patatoukas, 2017). This method is more appropriate for

micro business which does not involve high number of cash transactions and can be only used to

track the cash position of the business. A typical format of single entry bookkeeping is presented

below:

Date Description Transaction value Balance

XX-XX-XXXX £000.00 £000.00

On the other hand, double book keeping system is highly complex than the method

analysed above. In this system, every transaction is recorded into two accounts in order to ensure

that credit and debit of trail balance is equal. This method if book keeping is considered as high

reliable and validated as it helps in ensuring that the accounting books are appropriately

developed if the balance of debit and credit are equal. This system is appropriate for any type of

organisation having any scale, scope or objective. A typical format of double book keeping

system is present below:

Date Description L.F Debit Credit

XX-XX-XXXX £000.00

£000.00

Trial balance and its importance

The term trial balance is used for a worksheet and not for an account which is used for

book keeping all the business transactions which are transacted in an accounting year (Haskin

and Burke, 2016). This type of worksheet is divided into columns for debit and credit and the

balance of both the transactions is required to be equal. There are various significant points of

trial balance which represents its importance for business entities and some of these significant

points are identified below:

4

taxation, payment of electricity, gas, stationary and other miscellaneous expenses.

Single entry and double entry book keeping

Single entry bookkeeping system is the easiest procedure to record business transactions

as in this system only cash transactions are recorded when they become due. In this system, all

the transactions of a business entity are recorded in a single column as a single entry in the

primary book of journal (Dutta and Patatoukas, 2017). This method is more appropriate for

micro business which does not involve high number of cash transactions and can be only used to

track the cash position of the business. A typical format of single entry bookkeeping is presented

below:

Date Description Transaction value Balance

XX-XX-XXXX £000.00 £000.00

On the other hand, double book keeping system is highly complex than the method

analysed above. In this system, every transaction is recorded into two accounts in order to ensure

that credit and debit of trail balance is equal. This method if book keeping is considered as high

reliable and validated as it helps in ensuring that the accounting books are appropriately

developed if the balance of debit and credit are equal. This system is appropriate for any type of

organisation having any scale, scope or objective. A typical format of double book keeping

system is present below:

Date Description L.F Debit Credit

XX-XX-XXXX £000.00

£000.00

Trial balance and its importance

The term trial balance is used for a worksheet and not for an account which is used for

book keeping all the business transactions which are transacted in an accounting year (Haskin

and Burke, 2016). This type of worksheet is divided into columns for debit and credit and the

balance of both the transactions is required to be equal. There are various significant points of

trial balance which represents its importance for business entities and some of these significant

points are identified below:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

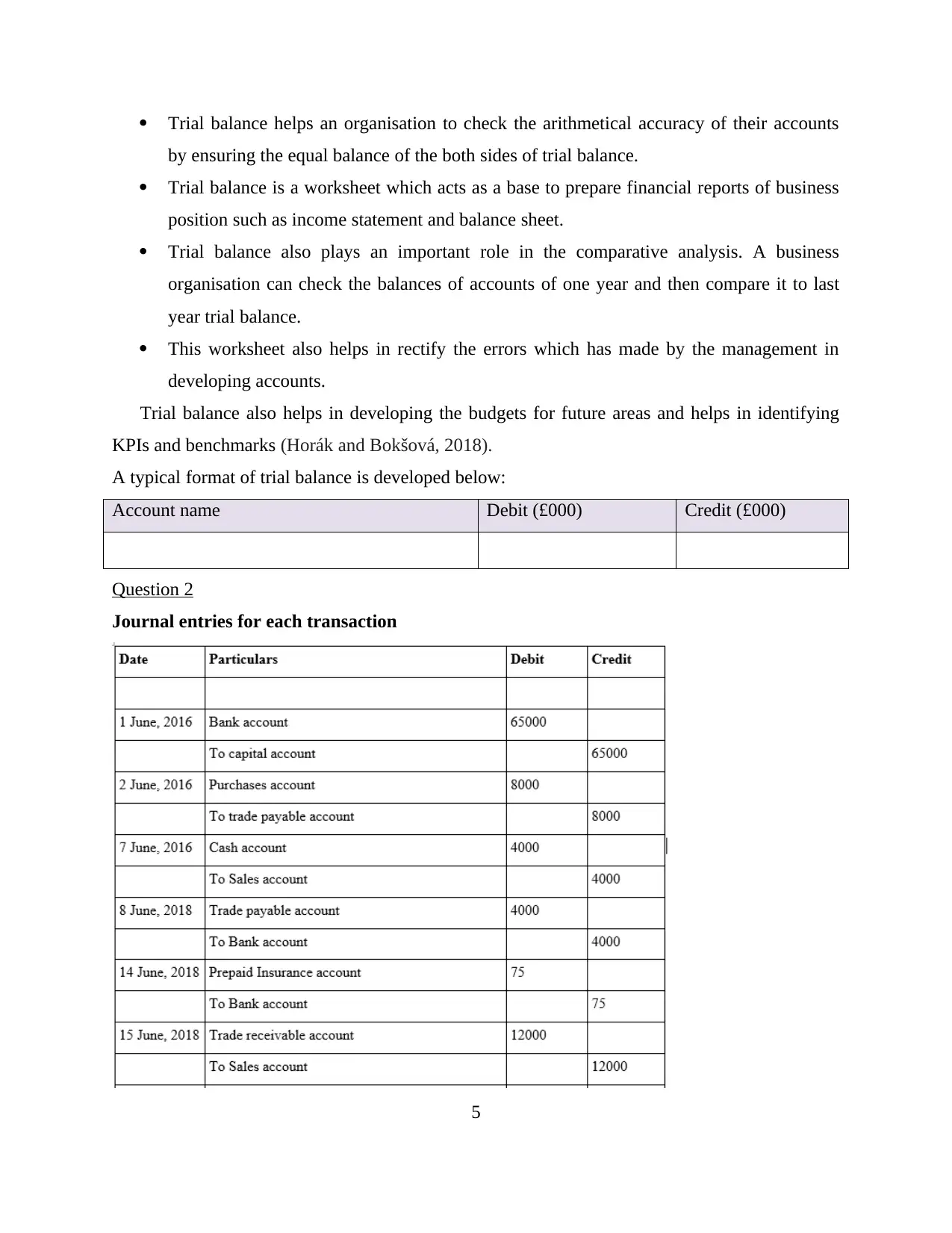

Trial balance helps an organisation to check the arithmetical accuracy of their accounts

by ensuring the equal balance of the both sides of trial balance.

Trial balance is a worksheet which acts as a base to prepare financial reports of business

position such as income statement and balance sheet.

Trial balance also plays an important role in the comparative analysis. A business

organisation can check the balances of accounts of one year and then compare it to last

year trial balance.

This worksheet also helps in rectify the errors which has made by the management in

developing accounts.

Trial balance also helps in developing the budgets for future areas and helps in identifying

KPIs and benchmarks (Horák and Bokšová, 2018).

A typical format of trial balance is developed below:

Account name Debit (£000) Credit (£000)

Question 2

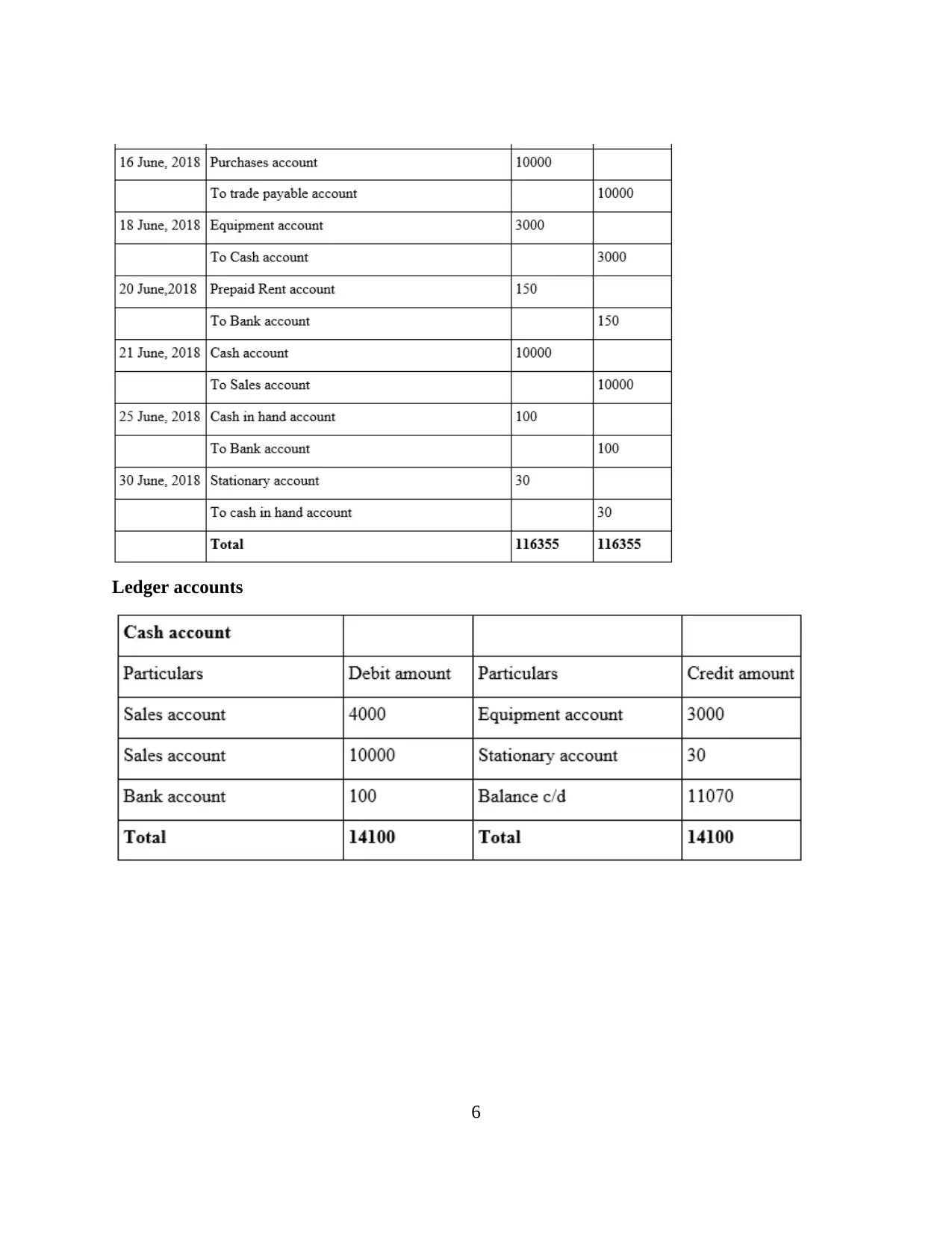

Journal entries for each transaction

5

by ensuring the equal balance of the both sides of trial balance.

Trial balance is a worksheet which acts as a base to prepare financial reports of business

position such as income statement and balance sheet.

Trial balance also plays an important role in the comparative analysis. A business

organisation can check the balances of accounts of one year and then compare it to last

year trial balance.

This worksheet also helps in rectify the errors which has made by the management in

developing accounts.

Trial balance also helps in developing the budgets for future areas and helps in identifying

KPIs and benchmarks (Horák and Bokšová, 2018).

A typical format of trial balance is developed below:

Account name Debit (£000) Credit (£000)

Question 2

Journal entries for each transaction

5

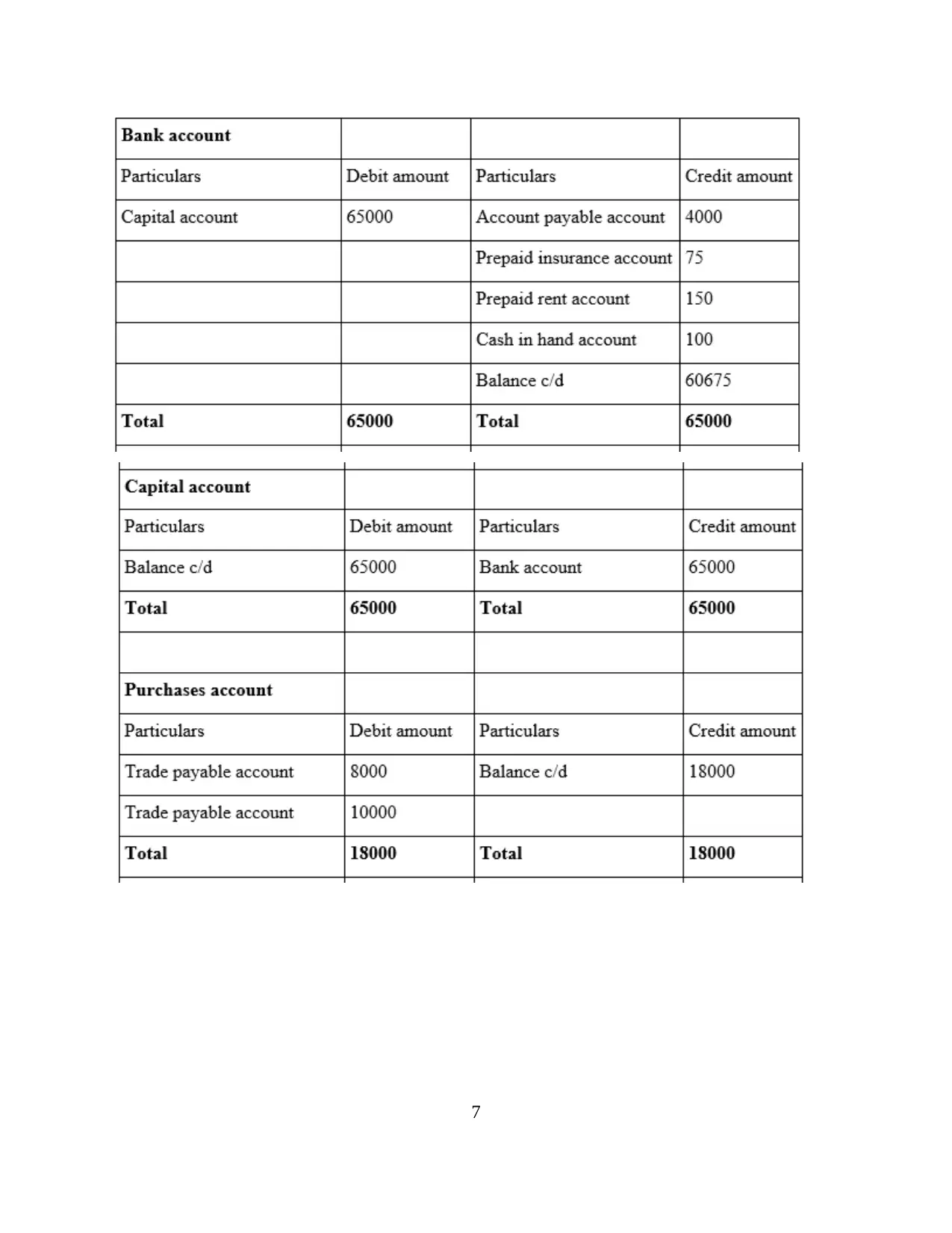

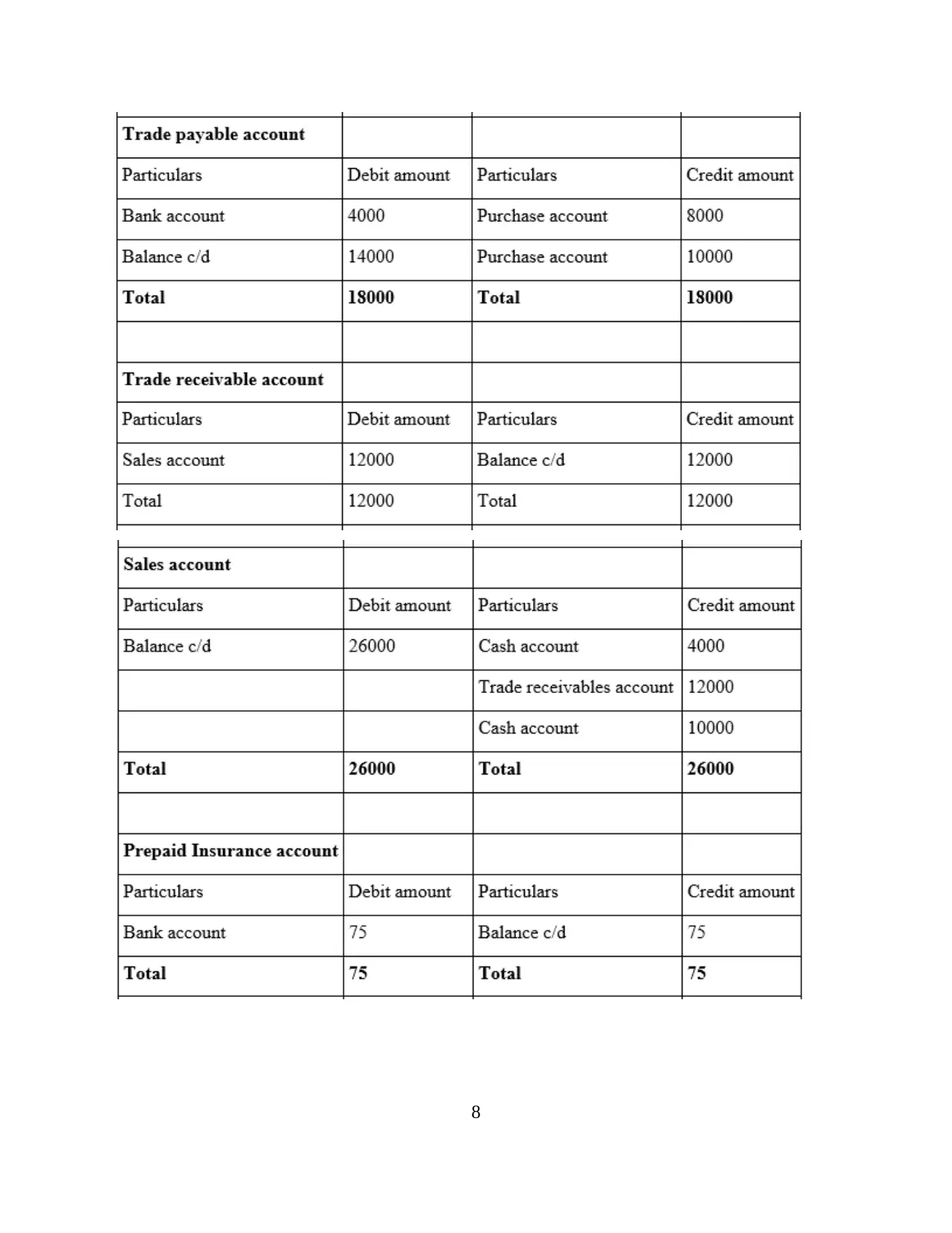

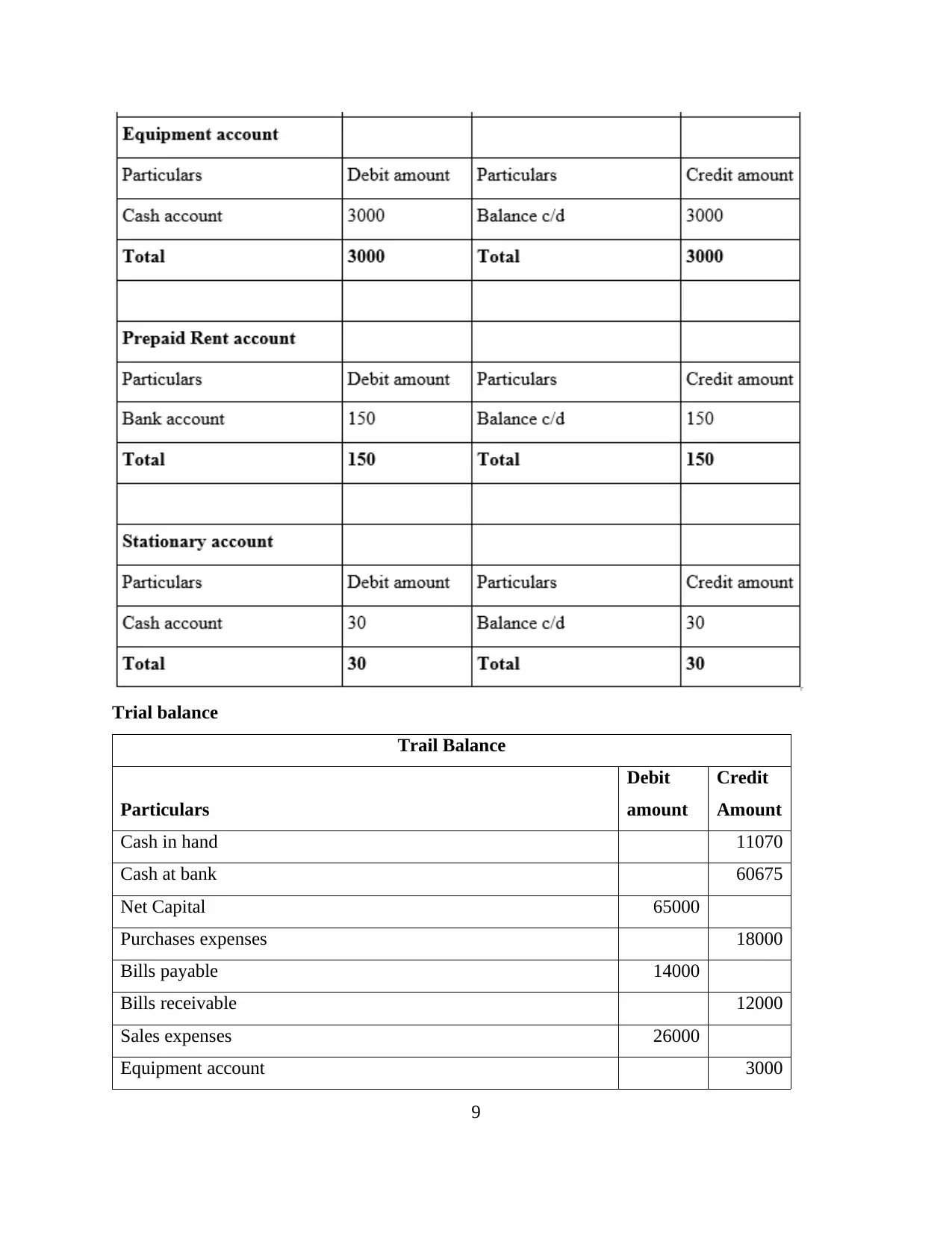

Ledger accounts

6

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Trial balance

Trail Balance

Particulars

Debit

amount

Credit

Amount

Cash in hand 11070

Cash at bank 60675

Net Capital 65000

Purchases expenses 18000

Bills payable 14000

Bills receivable 12000

Sales expenses 26000

Equipment account 3000

9

Trail Balance

Particulars

Debit

amount

Credit

Amount

Cash in hand 11070

Cash at bank 60675

Net Capital 65000

Purchases expenses 18000

Bills payable 14000

Bills receivable 12000

Sales expenses 26000

Equipment account 3000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

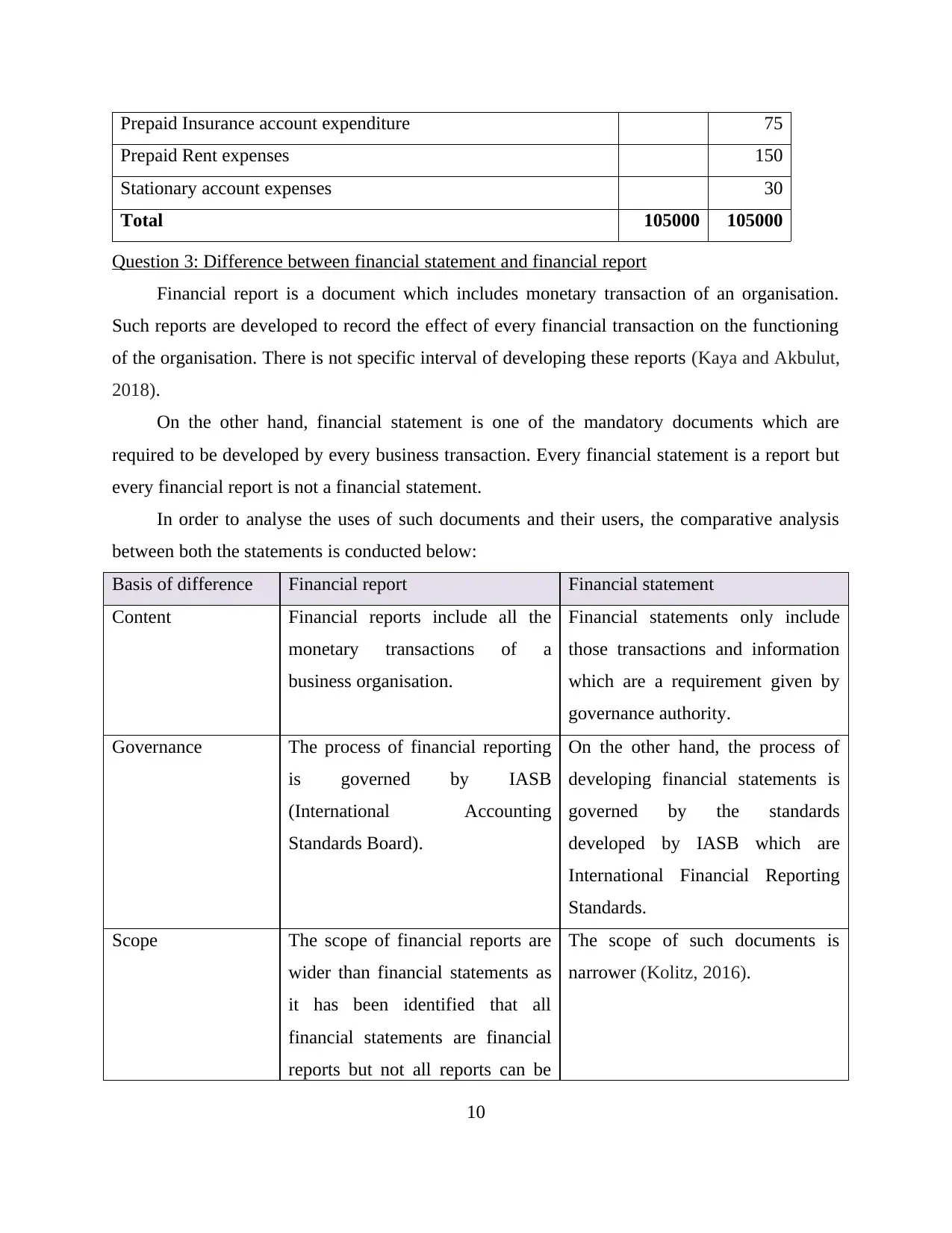

Prepaid Insurance account expenditure 75

Prepaid Rent expenses 150

Stationary account expenses 30

Total 105000 105000

Question 3: Difference between financial statement and financial report

Financial report is a document which includes monetary transaction of an organisation.

Such reports are developed to record the effect of every financial transaction on the functioning

of the organisation. There is not specific interval of developing these reports (Kaya and Akbulut,

2018).

On the other hand, financial statement is one of the mandatory documents which are

required to be developed by every business transaction. Every financial statement is a report but

every financial report is not a financial statement.

In order to analyse the uses of such documents and their users, the comparative analysis

between both the statements is conducted below:

Basis of difference Financial report Financial statement

Content Financial reports include all the

monetary transactions of a

business organisation.

Financial statements only include

those transactions and information

which are a requirement given by

governance authority.

Governance The process of financial reporting

is governed by IASB

(International Accounting

Standards Board).

On the other hand, the process of

developing financial statements is

governed by the standards

developed by IASB which are

International Financial Reporting

Standards.

Scope The scope of financial reports are

wider than financial statements as

it has been identified that all

financial statements are financial

reports but not all reports can be

The scope of such documents is

narrower (Kolitz, 2016).

10

Prepaid Rent expenses 150

Stationary account expenses 30

Total 105000 105000

Question 3: Difference between financial statement and financial report

Financial report is a document which includes monetary transaction of an organisation.

Such reports are developed to record the effect of every financial transaction on the functioning

of the organisation. There is not specific interval of developing these reports (Kaya and Akbulut,

2018).

On the other hand, financial statement is one of the mandatory documents which are

required to be developed by every business transaction. Every financial statement is a report but

every financial report is not a financial statement.

In order to analyse the uses of such documents and their users, the comparative analysis

between both the statements is conducted below:

Basis of difference Financial report Financial statement

Content Financial reports include all the

monetary transactions of a

business organisation.

Financial statements only include

those transactions and information

which are a requirement given by

governance authority.

Governance The process of financial reporting

is governed by IASB

(International Accounting

Standards Board).

On the other hand, the process of

developing financial statements is

governed by the standards

developed by IASB which are

International Financial Reporting

Standards.

Scope The scope of financial reports are

wider than financial statements as

it has been identified that all

financial statements are financial

reports but not all reports can be

The scope of such documents is

narrower (Kolitz, 2016).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial statements.

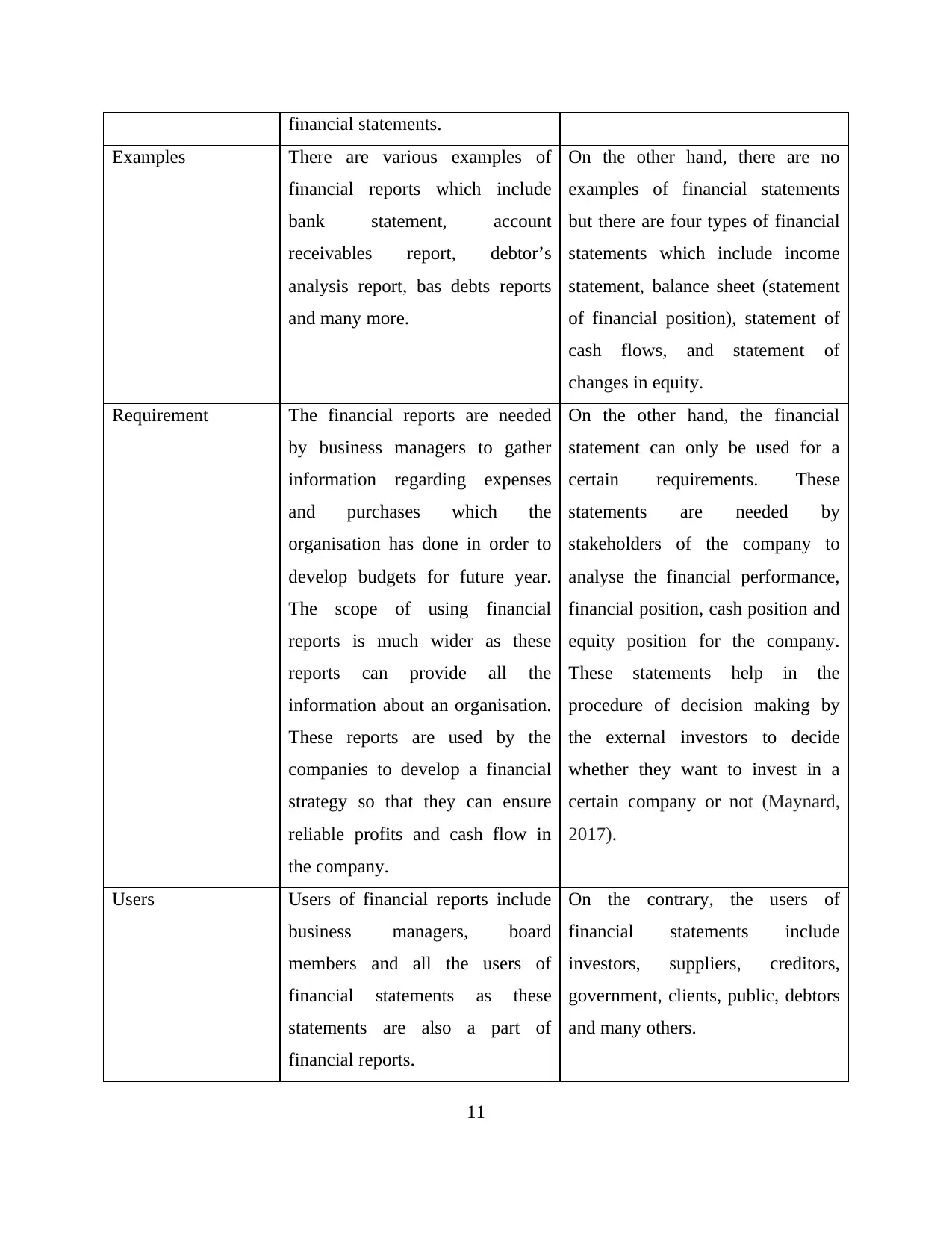

Examples There are various examples of

financial reports which include

bank statement, account

receivables report, debtor’s

analysis report, bas debts reports

and many more.

On the other hand, there are no

examples of financial statements

but there are four types of financial

statements which include income

statement, balance sheet (statement

of financial position), statement of

cash flows, and statement of

changes in equity.

Requirement The financial reports are needed

by business managers to gather

information regarding expenses

and purchases which the

organisation has done in order to

develop budgets for future year.

The scope of using financial

reports is much wider as these

reports can provide all the

information about an organisation.

These reports are used by the

companies to develop a financial

strategy so that they can ensure

reliable profits and cash flow in

the company.

On the other hand, the financial

statement can only be used for a

certain requirements. These

statements are needed by

stakeholders of the company to

analyse the financial performance,

financial position, cash position and

equity position for the company.

These statements help in the

procedure of decision making by

the external investors to decide

whether they want to invest in a

certain company or not (Maynard,

2017).

Users Users of financial reports include

business managers, board

members and all the users of

financial statements as these

statements are also a part of

financial reports.

On the contrary, the users of

financial statements include

investors, suppliers, creditors,

government, clients, public, debtors

and many others.

11

Examples There are various examples of

financial reports which include

bank statement, account

receivables report, debtor’s

analysis report, bas debts reports

and many more.

On the other hand, there are no

examples of financial statements

but there are four types of financial

statements which include income

statement, balance sheet (statement

of financial position), statement of

cash flows, and statement of

changes in equity.

Requirement The financial reports are needed

by business managers to gather

information regarding expenses

and purchases which the

organisation has done in order to

develop budgets for future year.

The scope of using financial

reports is much wider as these

reports can provide all the

information about an organisation.

These reports are used by the

companies to develop a financial

strategy so that they can ensure

reliable profits and cash flow in

the company.

On the other hand, the financial

statement can only be used for a

certain requirements. These

statements are needed by

stakeholders of the company to

analyse the financial performance,

financial position, cash position and

equity position for the company.

These statements help in the

procedure of decision making by

the external investors to decide

whether they want to invest in a

certain company or not (Maynard,

2017).

Users Users of financial reports include

business managers, board

members and all the users of

financial statements as these

statements are also a part of

financial reports.

On the contrary, the users of

financial statements include

investors, suppliers, creditors,

government, clients, public, debtors

and many others.

11

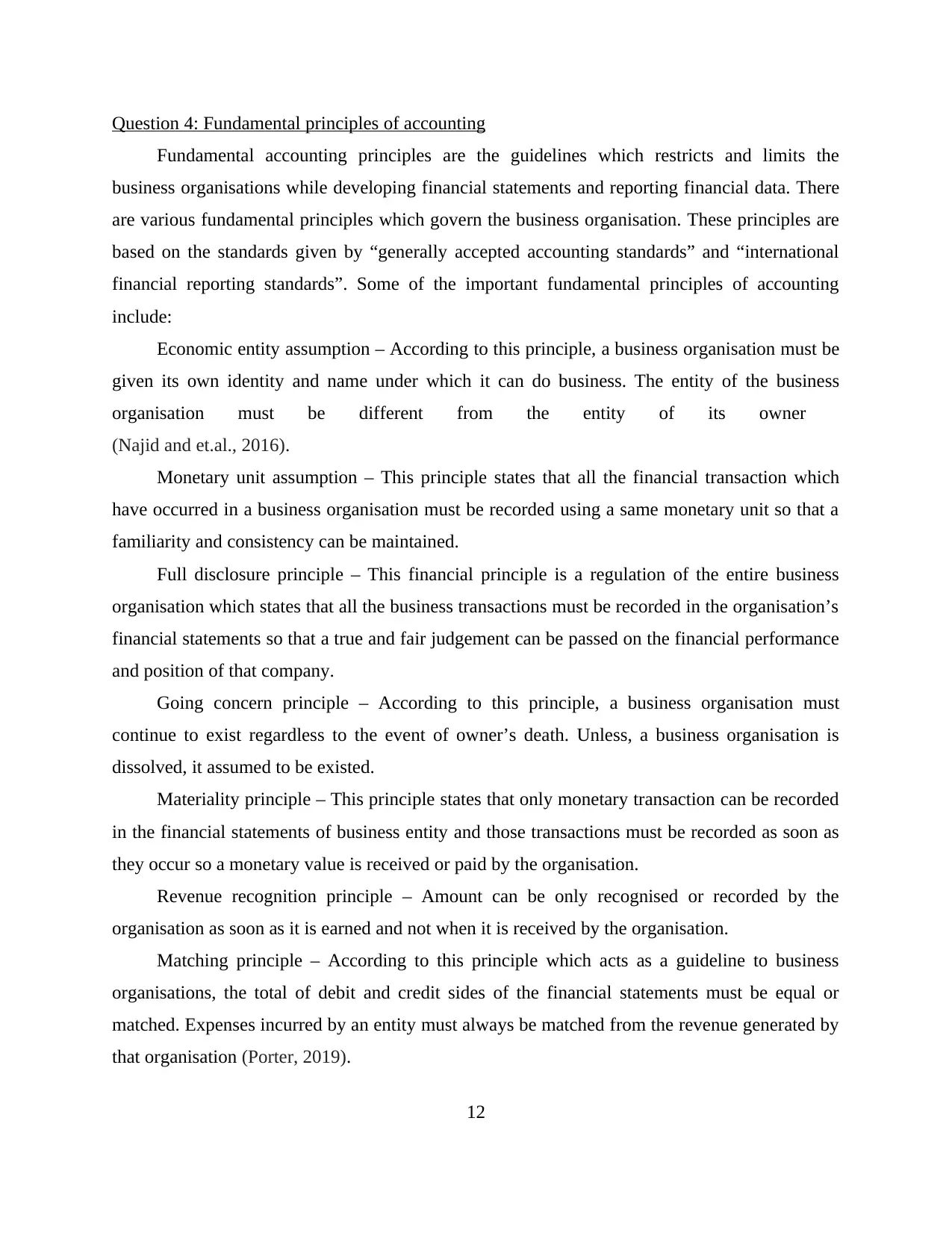

Question 4: Fundamental principles of accounting

Fundamental accounting principles are the guidelines which restricts and limits the

business organisations while developing financial statements and reporting financial data. There

are various fundamental principles which govern the business organisation. These principles are

based on the standards given by “generally accepted accounting standards” and “international

financial reporting standards”. Some of the important fundamental principles of accounting

include:

Economic entity assumption – According to this principle, a business organisation must be

given its own identity and name under which it can do business. The entity of the business

organisation must be different from the entity of its owner

(Najid and et.al., 2016).

Monetary unit assumption – This principle states that all the financial transaction which

have occurred in a business organisation must be recorded using a same monetary unit so that a

familiarity and consistency can be maintained.

Full disclosure principle – This financial principle is a regulation of the entire business

organisation which states that all the business transactions must be recorded in the organisation’s

financial statements so that a true and fair judgement can be passed on the financial performance

and position of that company.

Going concern principle – According to this principle, a business organisation must

continue to exist regardless to the event of owner’s death. Unless, a business organisation is

dissolved, it assumed to be existed.

Materiality principle – This principle states that only monetary transaction can be recorded

in the financial statements of business entity and those transactions must be recorded as soon as

they occur so a monetary value is received or paid by the organisation.

Revenue recognition principle – Amount can be only recognised or recorded by the

organisation as soon as it is earned and not when it is received by the organisation.

Matching principle – According to this principle which acts as a guideline to business

organisations, the total of debit and credit sides of the financial statements must be equal or

matched. Expenses incurred by an entity must always be matched from the revenue generated by

that organisation (Porter, 2019).

12

Fundamental accounting principles are the guidelines which restricts and limits the

business organisations while developing financial statements and reporting financial data. There

are various fundamental principles which govern the business organisation. These principles are

based on the standards given by “generally accepted accounting standards” and “international

financial reporting standards”. Some of the important fundamental principles of accounting

include:

Economic entity assumption – According to this principle, a business organisation must be

given its own identity and name under which it can do business. The entity of the business

organisation must be different from the entity of its owner

(Najid and et.al., 2016).

Monetary unit assumption – This principle states that all the financial transaction which

have occurred in a business organisation must be recorded using a same monetary unit so that a

familiarity and consistency can be maintained.

Full disclosure principle – This financial principle is a regulation of the entire business

organisation which states that all the business transactions must be recorded in the organisation’s

financial statements so that a true and fair judgement can be passed on the financial performance

and position of that company.

Going concern principle – According to this principle, a business organisation must

continue to exist regardless to the event of owner’s death. Unless, a business organisation is

dissolved, it assumed to be existed.

Materiality principle – This principle states that only monetary transaction can be recorded

in the financial statements of business entity and those transactions must be recorded as soon as

they occur so a monetary value is received or paid by the organisation.

Revenue recognition principle – Amount can be only recognised or recorded by the

organisation as soon as it is earned and not when it is received by the organisation.

Matching principle – According to this principle which acts as a guideline to business

organisations, the total of debit and credit sides of the financial statements must be equal or

matched. Expenses incurred by an entity must always be matched from the revenue generated by

that organisation (Porter, 2019).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.