Financial Accounting Report: Investment Appraisal and Analysis

VerifiedAdded on 2023/01/05

|16

|3721

|79

Report

AI Summary

This report is a comprehensive financial accounting analysis, divided into three parts. Part A focuses on the income statement and financial position, including calculations of depreciation and income tax. It presents the income statement for the year ending December 31, 2019, and the balance sheet as of the same date. Part B delves into break-even analysis, calculating the break-even point and margin of safety, along with an analysis of a proposed business strategy. It includes calculations of contribution margin and profit under different scenarios. Part C discusses capital investment appraisal methods, exploring their merits and demerits, and also examines the limitations and benefits of using budgets for strategic planning. The report aims to provide a thorough understanding of financial accounting principles and their application.

UGB 163

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Part A...............................................................................................................................................4

Part B...............................................................................................................................................9

PART 3..........................................................................................................................................11

a. Calculation for different investment appraisal techniques such as payback period, net

present value and accounting rate of return...............................................................................11

b. Explanation of all the limitations and merits of different techniques of investment appraisal

...................................................................................................................................................13

c. All the limitations and benefits of using budgets as the tool for strategic planning..............14

Conclusion.....................................................................................................................................15

REFERENCES..............................................................................................................................16

Introduction......................................................................................................................................3

Part A...............................................................................................................................................4

Part B...............................................................................................................................................9

PART 3..........................................................................................................................................11

a. Calculation for different investment appraisal techniques such as payback period, net

present value and accounting rate of return...............................................................................11

b. Explanation of all the limitations and merits of different techniques of investment appraisal

...................................................................................................................................................13

c. All the limitations and benefits of using budgets as the tool for strategic planning..............14

Conclusion.....................................................................................................................................15

REFERENCES..............................................................................................................................16

Introduction

Financial accounting is a specific branch of accounting involving a process of recording,

summarizing, and reporting the myriad of transactions resulting from business operations over a

period of time. These exchanges are provided in the design of the balance sheet summaries,

including the accounting report, the pay explanation, and the revenue claim, which records the

presentation of the organization's work in the pre-defined time.

Financial accounting uses incremental accounting rates. The choice of accounting

standards to be applied in accounting depends on the administrative and detailed requirements

that the sector faces. For US government agencies, organizations are required to save in

accordance with rigorous accounting standards (GAAP). The basis of these accounting standards

is to provide stable data to speculators, lenders, regulators and cost experts.

The financial statements used in cash accounting reflect the five main orders of cash

information: income, expenses, resources, liabilities, and value. Income and expenses are

represented and written on the payment definition. They can take everything from research and

development to finance.

Financial accounting determines total profitability at the lower end of the payment

definition. Resources, liabilities and accounts of value are accounted for in the cash register. The

cash register uses the cash reserves to account for liability for the organization's future financial

benefits.

The main objective of this report is to understand fundamental models, concepts and

techniques used in financial accounting and understanding the role of finance at local and

international level. The project report is divided into three parts; Part A, B and C. Where, Part A

discusses about income statement and financial position of the company. Part B is based on

analyses of break-even point and margin of safety. The final Part C is based on discussion of

capital investment appraisal methods. This part also discusses about merits and demerits of

investment appraisal techniques.

Financial accounting is a specific branch of accounting involving a process of recording,

summarizing, and reporting the myriad of transactions resulting from business operations over a

period of time. These exchanges are provided in the design of the balance sheet summaries,

including the accounting report, the pay explanation, and the revenue claim, which records the

presentation of the organization's work in the pre-defined time.

Financial accounting uses incremental accounting rates. The choice of accounting

standards to be applied in accounting depends on the administrative and detailed requirements

that the sector faces. For US government agencies, organizations are required to save in

accordance with rigorous accounting standards (GAAP). The basis of these accounting standards

is to provide stable data to speculators, lenders, regulators and cost experts.

The financial statements used in cash accounting reflect the five main orders of cash

information: income, expenses, resources, liabilities, and value. Income and expenses are

represented and written on the payment definition. They can take everything from research and

development to finance.

Financial accounting determines total profitability at the lower end of the payment

definition. Resources, liabilities and accounts of value are accounted for in the cash register. The

cash register uses the cash reserves to account for liability for the organization's future financial

benefits.

The main objective of this report is to understand fundamental models, concepts and

techniques used in financial accounting and understanding the role of finance at local and

international level. The project report is divided into three parts; Part A, B and C. Where, Part A

discusses about income statement and financial position of the company. Part B is based on

analyses of break-even point and margin of safety. The final Part C is based on discussion of

capital investment appraisal methods. This part also discusses about merits and demerits of

investment appraisal techniques.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part A

Income statement:

The income statement is one of three significant tax summaries used to denote the presentation

of an organization’s cash in a particular accounting period, with the other two key statements

being the accounting report and the income statement. Also known as a benefit and misfortune

claim or income and expense claim, the payment call focuses specifically on the organization’s

income and expenses at a particular point in time.

The income statement is an important part of a group's performance reporting reports that

must be submitted to the Securities and Exchange Commission (SEC). While cash flow provides

the representation of an organization’s financial data as a specific date, salary definition reports

pay over a specific period of time and its headline shows the range.

The income statement is based on four main elements: income, expenses, additions and

disadvantages. It does not distinguish between cash and non-cash receipts (real money versus

loan offers) or cash payments / payments versus non-cash payments (real money versus layaway

purchases). Start with the subtleties of the contracts and then work your way up to measuring net

earnings and, in the long run, earnings per share (EPS). In essence, it provides a table of how the

organization's recognized income has been converted to net income (profit or deficit).

Revenues and Gains

The next ones are folded into a salary structure, but its arrangement may vary depending on a

neighbor's administrative prerequisites, extension of scope of activity and associated years of

work:

Operating Revenue

Income recognized through essential exercises is often referred to as earned income. For an

organization that manufactures an item, or for a circulator, trader or retailer that is busy selling

that item, the income from essential businesses refers to the income- in from offering the thing.

Also, for an organization (or their friends) that is busy with an administrative offer, the income

from an essential business refers to the income or expenses received in exchange for trading

those administrations offered.

Non-Operating Revenue

Income statement:

The income statement is one of three significant tax summaries used to denote the presentation

of an organization’s cash in a particular accounting period, with the other two key statements

being the accounting report and the income statement. Also known as a benefit and misfortune

claim or income and expense claim, the payment call focuses specifically on the organization’s

income and expenses at a particular point in time.

The income statement is an important part of a group's performance reporting reports that

must be submitted to the Securities and Exchange Commission (SEC). While cash flow provides

the representation of an organization’s financial data as a specific date, salary definition reports

pay over a specific period of time and its headline shows the range.

The income statement is based on four main elements: income, expenses, additions and

disadvantages. It does not distinguish between cash and non-cash receipts (real money versus

loan offers) or cash payments / payments versus non-cash payments (real money versus layaway

purchases). Start with the subtleties of the contracts and then work your way up to measuring net

earnings and, in the long run, earnings per share (EPS). In essence, it provides a table of how the

organization's recognized income has been converted to net income (profit or deficit).

Revenues and Gains

The next ones are folded into a salary structure, but its arrangement may vary depending on a

neighbor's administrative prerequisites, extension of scope of activity and associated years of

work:

Operating Revenue

Income recognized through essential exercises is often referred to as earned income. For an

organization that manufactures an item, or for a circulator, trader or retailer that is busy selling

that item, the income from essential businesses refers to the income- in from offering the thing.

Also, for an organization (or their friends) that is busy with an administrative offer, the income

from an essential business refers to the income or expenses received in exchange for trading

those administrations offered.

Non-Operating Revenue

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue recognized through elective and non-selective industries is regularly referred to as non-

business income. This income is derived from profits outside the purchase and supply of goods

and enterprises and may include the earning of the income earned on the corporate capital

employed. in the bank, the rent from the business funds, the payment of principal associations

such as receipts for prestigious contributions or payment from an advertisement posted on a

company premises.

Gains

Also called other income, gains indicate the net money made from other activities, such as the

provision of long-range facilities. These include the net profit recognized by one-time non-

commercial businesses, such as an organization that sells its old transport van, unused land, or

support group.

Income should not be confused with income. Revenue is usually accounted for in the

period in which agreements are entered into or benefits are transferred. Receipts are the money

received and are represented when the money is received. For example, a customer can take

goods / administrations from an organization on September 28th, which requires the revenue

represented over the long term of September. Due to its high reputation, the customer may be

offered a 30-day lead time. It will take him until October 28 to make the allowance, which is

when the money will be represented.

Expenses and Losses

A company is called a cost to run the business and make money. Some of these costs may be

discounted on an expense form if they comply with IRS rules.

Primary Activity Expenses

All costs incurred in providing the normal operating income related to the essential activities of

the company Include product sales costs (COGS), sales, general and authoritative expenses

(SG&A) ), depreciation or impairment, and innovative labor costs (R&D). The common causes

of the downturn are representative salaries, business commissions, and costs for services such as

energy and transportation.

Secondary Activity Expenses

All costs associated with non-media commercial establishments, similar to the price paid in cash

on credit.

business income. This income is derived from profits outside the purchase and supply of goods

and enterprises and may include the earning of the income earned on the corporate capital

employed. in the bank, the rent from the business funds, the payment of principal associations

such as receipts for prestigious contributions or payment from an advertisement posted on a

company premises.

Gains

Also called other income, gains indicate the net money made from other activities, such as the

provision of long-range facilities. These include the net profit recognized by one-time non-

commercial businesses, such as an organization that sells its old transport van, unused land, or

support group.

Income should not be confused with income. Revenue is usually accounted for in the

period in which agreements are entered into or benefits are transferred. Receipts are the money

received and are represented when the money is received. For example, a customer can take

goods / administrations from an organization on September 28th, which requires the revenue

represented over the long term of September. Due to its high reputation, the customer may be

offered a 30-day lead time. It will take him until October 28 to make the allowance, which is

when the money will be represented.

Expenses and Losses

A company is called a cost to run the business and make money. Some of these costs may be

discounted on an expense form if they comply with IRS rules.

Primary Activity Expenses

All costs incurred in providing the normal operating income related to the essential activities of

the company Include product sales costs (COGS), sales, general and authoritative expenses

(SG&A) ), depreciation or impairment, and innovative labor costs (R&D). The common causes

of the downturn are representative salaries, business commissions, and costs for services such as

energy and transportation.

Secondary Activity Expenses

All costs associated with non-media commercial establishments, similar to the price paid in cash

on credit.

Losses as Expenses

All costs go to embarrassment offering long range facilities, one-off or other extraordinary

expenses, or costs for applications.

While essential income and expenses provide insights into the performance of the

organization's core business, support income and costs make a contribution the group and its

ability to cope with non-progressive and non-replacement exercises. Compared to paying from

an artifact offering, a very high cash payment at the bank indicates that the company may not be

using the accessible currency to its full potential 'Growth is the end of creation, or that it is

having difficulty expanding its part of the whole sector in the middle of the conflict.

Reimbursement of rent payments collected by the licensing boards at the organization's interstate

organized production line indicates that the administration is subscribing to the accessible

facilities and facilities for an additional benefit.

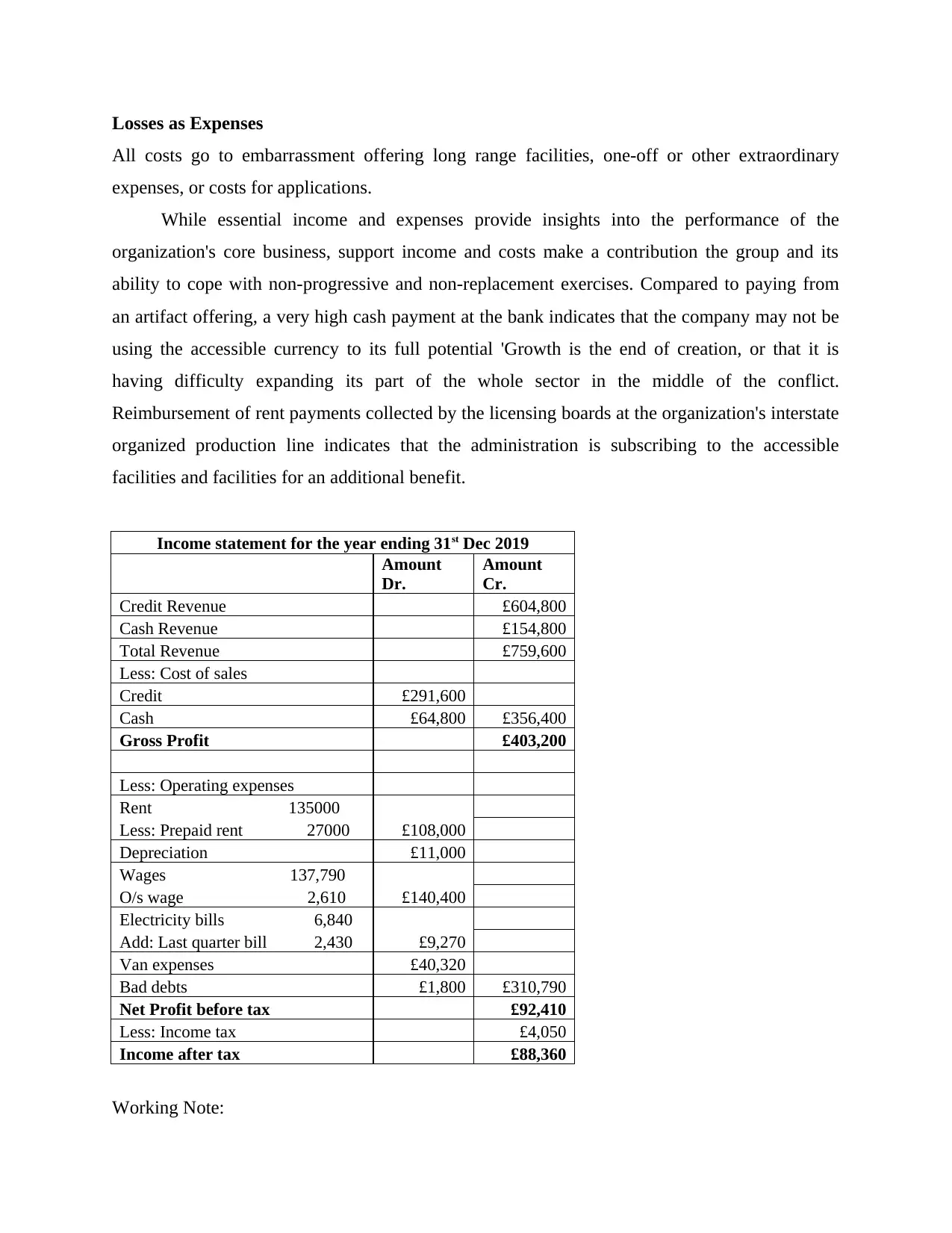

Income statement for the year ending 31st Dec 2019

Amount

Dr.

Amount

Cr.

Credit Revenue £604,800

Cash Revenue £154,800

Total Revenue £759,600

Less: Cost of sales

Credit £291,600

Cash £64,800 £356,400

Gross Profit £403,200

Less: Operating expenses

Rent 135000

Less: Prepaid rent 27000 £108,000

Depreciation £11,000

Wages 137,790

O/s wage 2,610 £140,400

Electricity bills 6,840

Add: Last quarter bill 2,430 £9,270

Van expenses £40,320

Bad debts £1,800 £310,790

Net Profit before tax £92,410

Less: Income tax £4,050

Income after tax £88,360

Working Note:

All costs go to embarrassment offering long range facilities, one-off or other extraordinary

expenses, or costs for applications.

While essential income and expenses provide insights into the performance of the

organization's core business, support income and costs make a contribution the group and its

ability to cope with non-progressive and non-replacement exercises. Compared to paying from

an artifact offering, a very high cash payment at the bank indicates that the company may not be

using the accessible currency to its full potential 'Growth is the end of creation, or that it is

having difficulty expanding its part of the whole sector in the middle of the conflict.

Reimbursement of rent payments collected by the licensing boards at the organization's interstate

organized production line indicates that the administration is subscribing to the accessible

facilities and facilities for an additional benefit.

Income statement for the year ending 31st Dec 2019

Amount

Dr.

Amount

Cr.

Credit Revenue £604,800

Cash Revenue £154,800

Total Revenue £759,600

Less: Cost of sales

Credit £291,600

Cash £64,800 £356,400

Gross Profit £403,200

Less: Operating expenses

Rent 135000

Less: Prepaid rent 27000 £108,000

Depreciation £11,000

Wages 137,790

O/s wage 2,610 £140,400

Electricity bills 6,840

Add: Last quarter bill 2,430 £9,270

Van expenses £40,320

Bad debts £1,800 £310,790

Net Profit before tax £92,410

Less: Income tax £4,050

Income after tax £88,360

Working Note:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

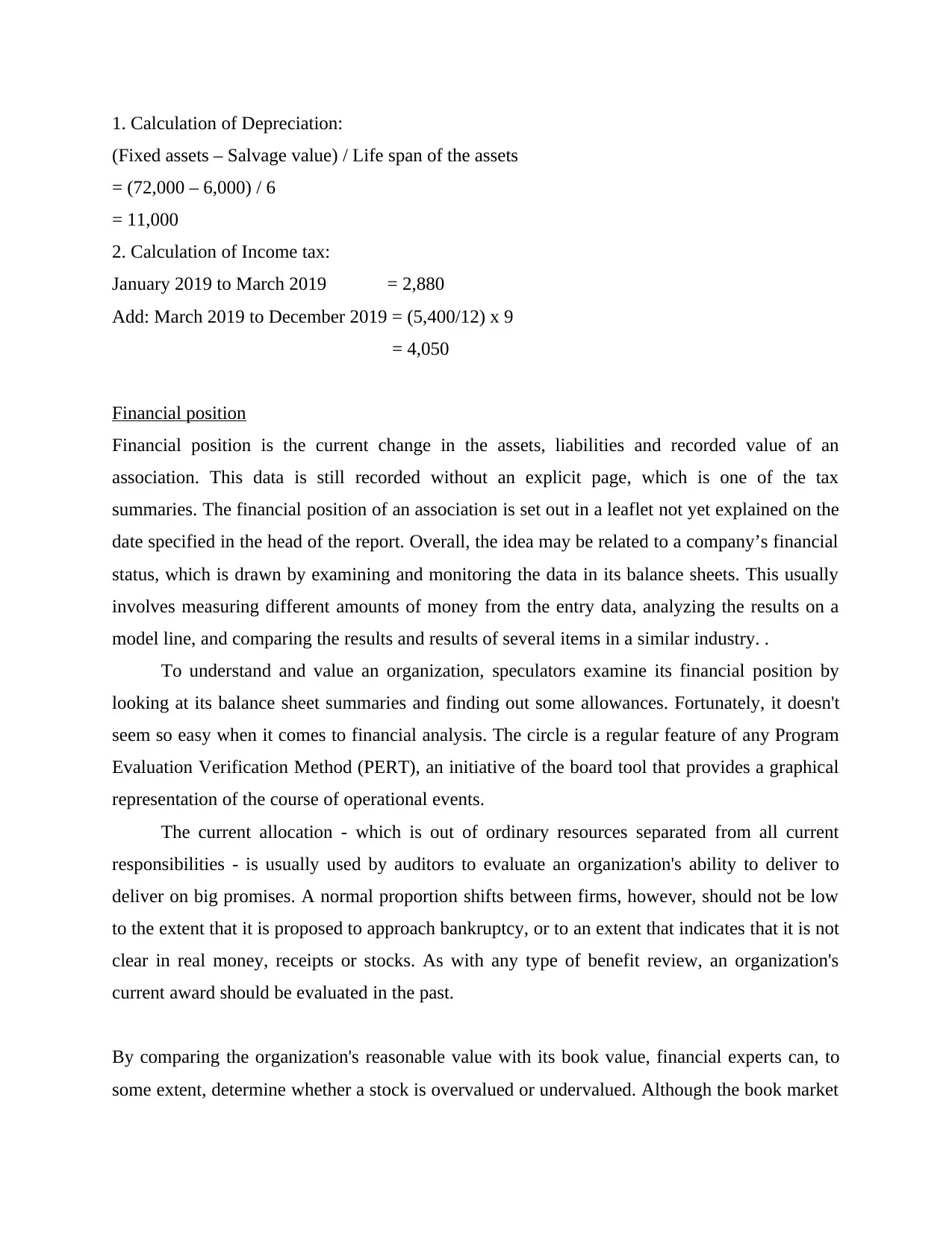

1. Calculation of Depreciation:

(Fixed assets – Salvage value) / Life span of the assets

= (72,000 – 6,000) / 6

= 11,000

2. Calculation of Income tax:

January 2019 to March 2019 = 2,880

Add: March 2019 to December 2019 = (5,400/12) x 9

= 4,050

Financial position

Financial position is the current change in the assets, liabilities and recorded value of an

association. This data is still recorded without an explicit page, which is one of the tax

summaries. The financial position of an association is set out in a leaflet not yet explained on the

date specified in the head of the report. Overall, the idea may be related to a company’s financial

status, which is drawn by examining and monitoring the data in its balance sheets. This usually

involves measuring different amounts of money from the entry data, analyzing the results on a

model line, and comparing the results and results of several items in a similar industry. .

To understand and value an organization, speculators examine its financial position by

looking at its balance sheet summaries and finding out some allowances. Fortunately, it doesn't

seem so easy when it comes to financial analysis. The circle is a regular feature of any Program

Evaluation Verification Method (PERT), an initiative of the board tool that provides a graphical

representation of the course of operational events.

The current allocation - which is out of ordinary resources separated from all current

responsibilities - is usually used by auditors to evaluate an organization's ability to deliver to

deliver on big promises. A normal proportion shifts between firms, however, should not be low

to the extent that it is proposed to approach bankruptcy, or to an extent that indicates that it is not

clear in real money, receipts or stocks. As with any type of benefit review, an organization's

current award should be evaluated in the past.

By comparing the organization's reasonable value with its book value, financial experts can, to

some extent, determine whether a stock is overvalued or undervalued. Although the book market

(Fixed assets – Salvage value) / Life span of the assets

= (72,000 – 6,000) / 6

= 11,000

2. Calculation of Income tax:

January 2019 to March 2019 = 2,880

Add: March 2019 to December 2019 = (5,400/12) x 9

= 4,050

Financial position

Financial position is the current change in the assets, liabilities and recorded value of an

association. This data is still recorded without an explicit page, which is one of the tax

summaries. The financial position of an association is set out in a leaflet not yet explained on the

date specified in the head of the report. Overall, the idea may be related to a company’s financial

status, which is drawn by examining and monitoring the data in its balance sheets. This usually

involves measuring different amounts of money from the entry data, analyzing the results on a

model line, and comparing the results and results of several items in a similar industry. .

To understand and value an organization, speculators examine its financial position by

looking at its balance sheet summaries and finding out some allowances. Fortunately, it doesn't

seem so easy when it comes to financial analysis. The circle is a regular feature of any Program

Evaluation Verification Method (PERT), an initiative of the board tool that provides a graphical

representation of the course of operational events.

The current allocation - which is out of ordinary resources separated from all current

responsibilities - is usually used by auditors to evaluate an organization's ability to deliver to

deliver on big promises. A normal proportion shifts between firms, however, should not be low

to the extent that it is proposed to approach bankruptcy, or to an extent that indicates that it is not

clear in real money, receipts or stocks. As with any type of benefit review, an organization's

current award should be evaluated in the past.

By comparing the organization's reasonable value with its book value, financial experts can, to

some extent, determine whether a stock is overvalued or undervalued. Although the book market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is in short supply, despite its lack, it is still an important tool for speculators to appreciate.

Numerous scientific evidence has shown that organizations with low book-to-book inventory

perform better than those with high returns. This is fine as a low market for a book shows that

the organization is in a difficult financial position relative to its sticker price.

Balance sheet as at 31 December 2019

Assets

Non Current Assets

Deliver van £72,000

Less: Accumulated dep. £11,000 £61,000

Current assets

Prepaid rent £27,000

Cash

£132,57

0

Inventories

£273,60

0

Bank

£216,00

0

£649,17

0

Total Assets

£710,17

0

Equities and Liabilities

Equity

Capital

£216,00

0

Add: Retained earnings £88,360

£304,36

0

Current Liabilities

O/s wages £2,610

Credit purchases

£583,20

0

Add: Cost of sales

£291,60

0

Less: Payments

£471,60

0

Trade payables

£403,20

0

£405,81

0

Total equities and liabilities

£710,17

0

Numerous scientific evidence has shown that organizations with low book-to-book inventory

perform better than those with high returns. This is fine as a low market for a book shows that

the organization is in a difficult financial position relative to its sticker price.

Balance sheet as at 31 December 2019

Assets

Non Current Assets

Deliver van £72,000

Less: Accumulated dep. £11,000 £61,000

Current assets

Prepaid rent £27,000

Cash

£132,57

0

Inventories

£273,60

0

Bank

£216,00

0

£649,17

0

Total Assets

£710,17

0

Equities and Liabilities

Equity

Capital

£216,00

0

Add: Retained earnings £88,360

£304,36

0

Current Liabilities

O/s wages £2,610

Credit purchases

£583,20

0

Add: Cost of sales

£291,60

0

Less: Payments

£471,60

0

Trade payables

£403,20

0

£405,81

0

Total equities and liabilities

£710,17

0

Working Note:

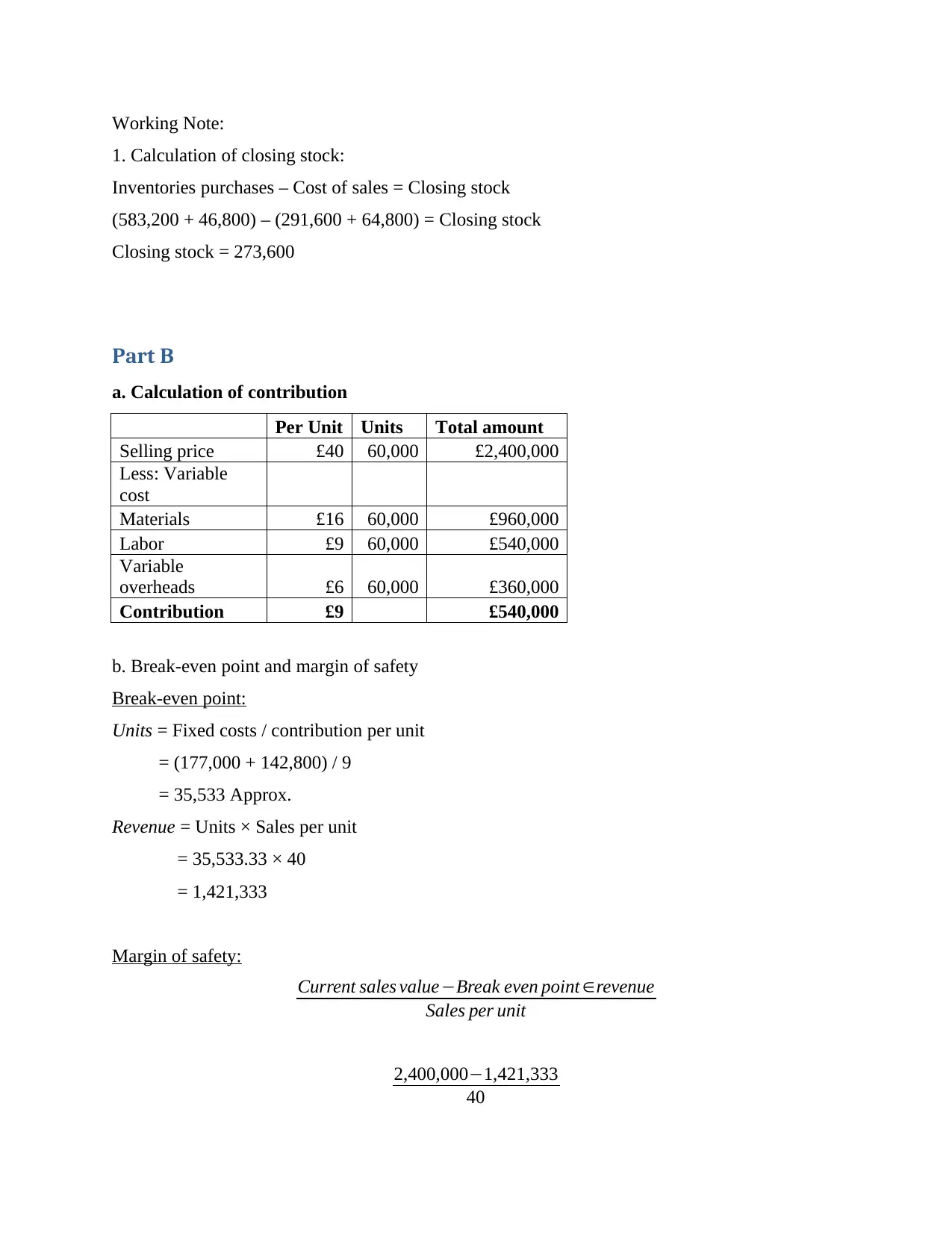

1. Calculation of closing stock:

Inventories purchases – Cost of sales = Closing stock

(583,200 + 46,800) – (291,600 + 64,800) = Closing stock

Closing stock = 273,600

Part B

a. Calculation of contribution

Per Unit Units Total amount

Selling price £40 60,000 £2,400,000

Less: Variable

cost

Materials £16 60,000 £960,000

Labor £9 60,000 £540,000

Variable

overheads £6 60,000 £360,000

Contribution £9 £540,000

b. Break-even point and margin of safety

Break-even point:

Units = Fixed costs / contribution per unit

= (177,000 + 142,800) / 9

= 35,533 Approx.

Revenue = Units × Sales per unit

= 35,533.33 × 40

= 1,421,333

Margin of safety:

Current sales value−Break even point ∈revenue

Sales per unit

2,400,000−1,421,333

40

1. Calculation of closing stock:

Inventories purchases – Cost of sales = Closing stock

(583,200 + 46,800) – (291,600 + 64,800) = Closing stock

Closing stock = 273,600

Part B

a. Calculation of contribution

Per Unit Units Total amount

Selling price £40 60,000 £2,400,000

Less: Variable

cost

Materials £16 60,000 £960,000

Labor £9 60,000 £540,000

Variable

overheads £6 60,000 £360,000

Contribution £9 £540,000

b. Break-even point and margin of safety

Break-even point:

Units = Fixed costs / contribution per unit

= (177,000 + 142,800) / 9

= 35,533 Approx.

Revenue = Units × Sales per unit

= 35,533.33 × 40

= 1,421,333

Margin of safety:

Current sales value−Break even point ∈revenue

Sales per unit

2,400,000−1,421,333

40

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

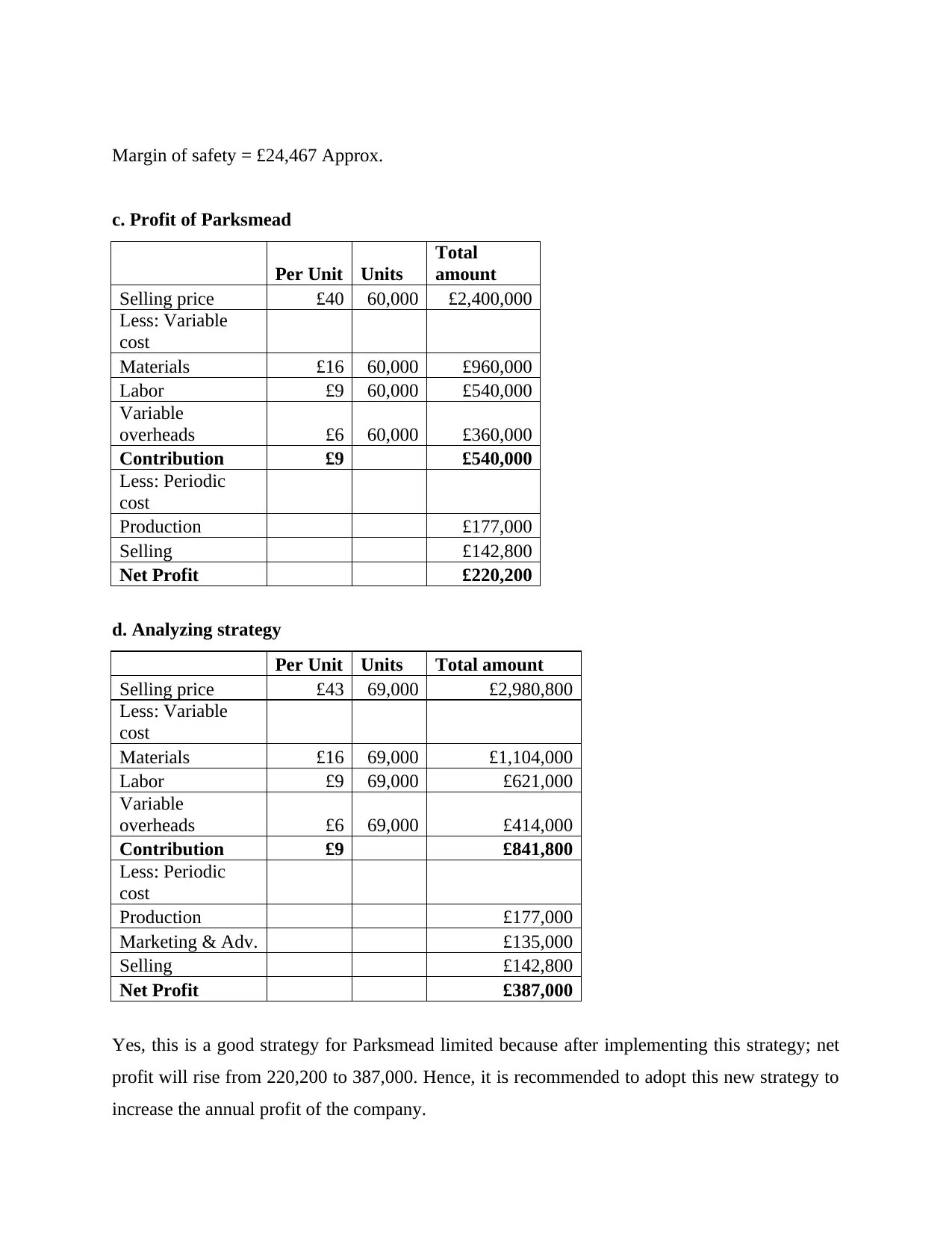

Margin of safety = £24,467 Approx.

c. Profit of Parksmead

Per Unit Units

Total

amount

Selling price £40 60,000 £2,400,000

Less: Variable

cost

Materials £16 60,000 £960,000

Labor £9 60,000 £540,000

Variable

overheads £6 60,000 £360,000

Contribution £9 £540,000

Less: Periodic

cost

Production £177,000

Selling £142,800

Net Profit £220,200

d. Analyzing strategy

Per Unit Units Total amount

Selling price £43 69,000 £2,980,800

Less: Variable

cost

Materials £16 69,000 £1,104,000

Labor £9 69,000 £621,000

Variable

overheads £6 69,000 £414,000

Contribution £9 £841,800

Less: Periodic

cost

Production £177,000

Marketing & Adv. £135,000

Selling £142,800

Net Profit £387,000

Yes, this is a good strategy for Parksmead limited because after implementing this strategy; net

profit will rise from 220,200 to 387,000. Hence, it is recommended to adopt this new strategy to

increase the annual profit of the company.

c. Profit of Parksmead

Per Unit Units

Total

amount

Selling price £40 60,000 £2,400,000

Less: Variable

cost

Materials £16 60,000 £960,000

Labor £9 60,000 £540,000

Variable

overheads £6 60,000 £360,000

Contribution £9 £540,000

Less: Periodic

cost

Production £177,000

Selling £142,800

Net Profit £220,200

d. Analyzing strategy

Per Unit Units Total amount

Selling price £43 69,000 £2,980,800

Less: Variable

cost

Materials £16 69,000 £1,104,000

Labor £9 69,000 £621,000

Variable

overheads £6 69,000 £414,000

Contribution £9 £841,800

Less: Periodic

cost

Production £177,000

Marketing & Adv. £135,000

Selling £142,800

Net Profit £387,000

Yes, this is a good strategy for Parksmead limited because after implementing this strategy; net

profit will rise from 220,200 to 387,000. Hence, it is recommended to adopt this new strategy to

increase the annual profit of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

e. Underpinning assumptions

For identification of break-even point; it is assumed that variable costs are fully variable and

fixed costs are pure fixed nature. There’s not costs which are mix of both variable and fixed

while calculating BEP analysis. No, model cannot be utilized by a range of differing businesses;

especially for service sectors. In this sector, there are no tangible products and most of the costs

are mixture of fixed and variable both. Hence, application of Break-even point in that situation is

not compatible.

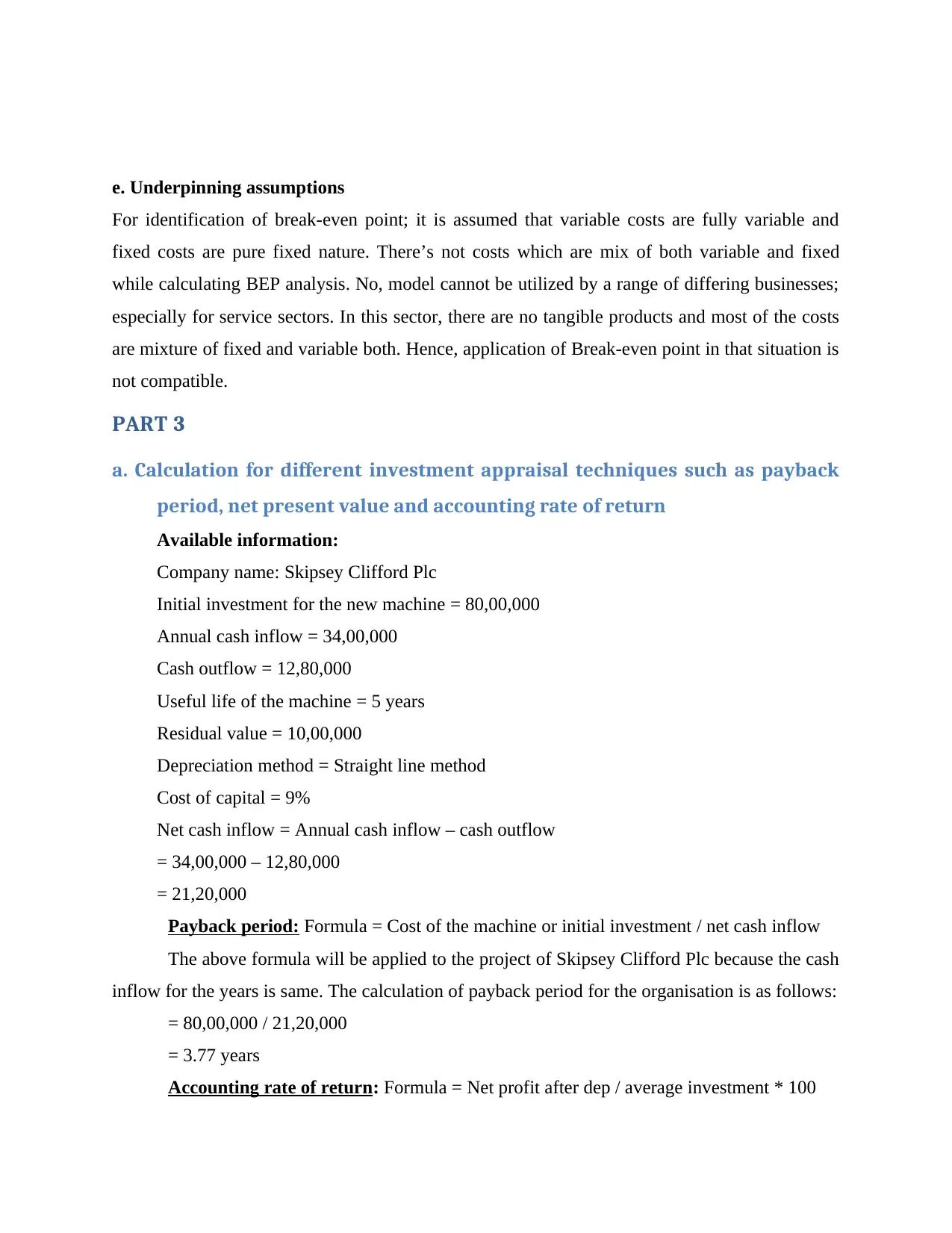

PART 3

a. Calculation for different investment appraisal techniques such as payback

period, net present value and accounting rate of return

Available information:

Company name: Skipsey Clifford Plc

Initial investment for the new machine = 80,00,000

Annual cash inflow = 34,00,000

Cash outflow = 12,80,000

Useful life of the machine = 5 years

Residual value = 10,00,000

Depreciation method = Straight line method

Cost of capital = 9%

Net cash inflow = Annual cash inflow – cash outflow

= 34,00,000 – 12,80,000

= 21,20,000

Payback period: Formula = Cost of the machine or initial investment / net cash inflow

The above formula will be applied to the project of Skipsey Clifford Plc because the cash

inflow for the years is same. The calculation of payback period for the organisation is as follows:

= 80,00,000 / 21,20,000

= 3.77 years

Accounting rate of return: Formula = Net profit after dep / average investment * 100

For identification of break-even point; it is assumed that variable costs are fully variable and

fixed costs are pure fixed nature. There’s not costs which are mix of both variable and fixed

while calculating BEP analysis. No, model cannot be utilized by a range of differing businesses;

especially for service sectors. In this sector, there are no tangible products and most of the costs

are mixture of fixed and variable both. Hence, application of Break-even point in that situation is

not compatible.

PART 3

a. Calculation for different investment appraisal techniques such as payback

period, net present value and accounting rate of return

Available information:

Company name: Skipsey Clifford Plc

Initial investment for the new machine = 80,00,000

Annual cash inflow = 34,00,000

Cash outflow = 12,80,000

Useful life of the machine = 5 years

Residual value = 10,00,000

Depreciation method = Straight line method

Cost of capital = 9%

Net cash inflow = Annual cash inflow – cash outflow

= 34,00,000 – 12,80,000

= 21,20,000

Payback period: Formula = Cost of the machine or initial investment / net cash inflow

The above formula will be applied to the project of Skipsey Clifford Plc because the cash

inflow for the years is same. The calculation of payback period for the organisation is as follows:

= 80,00,000 / 21,20,000

= 3.77 years

Accounting rate of return: Formula = Net profit after dep / average investment * 100

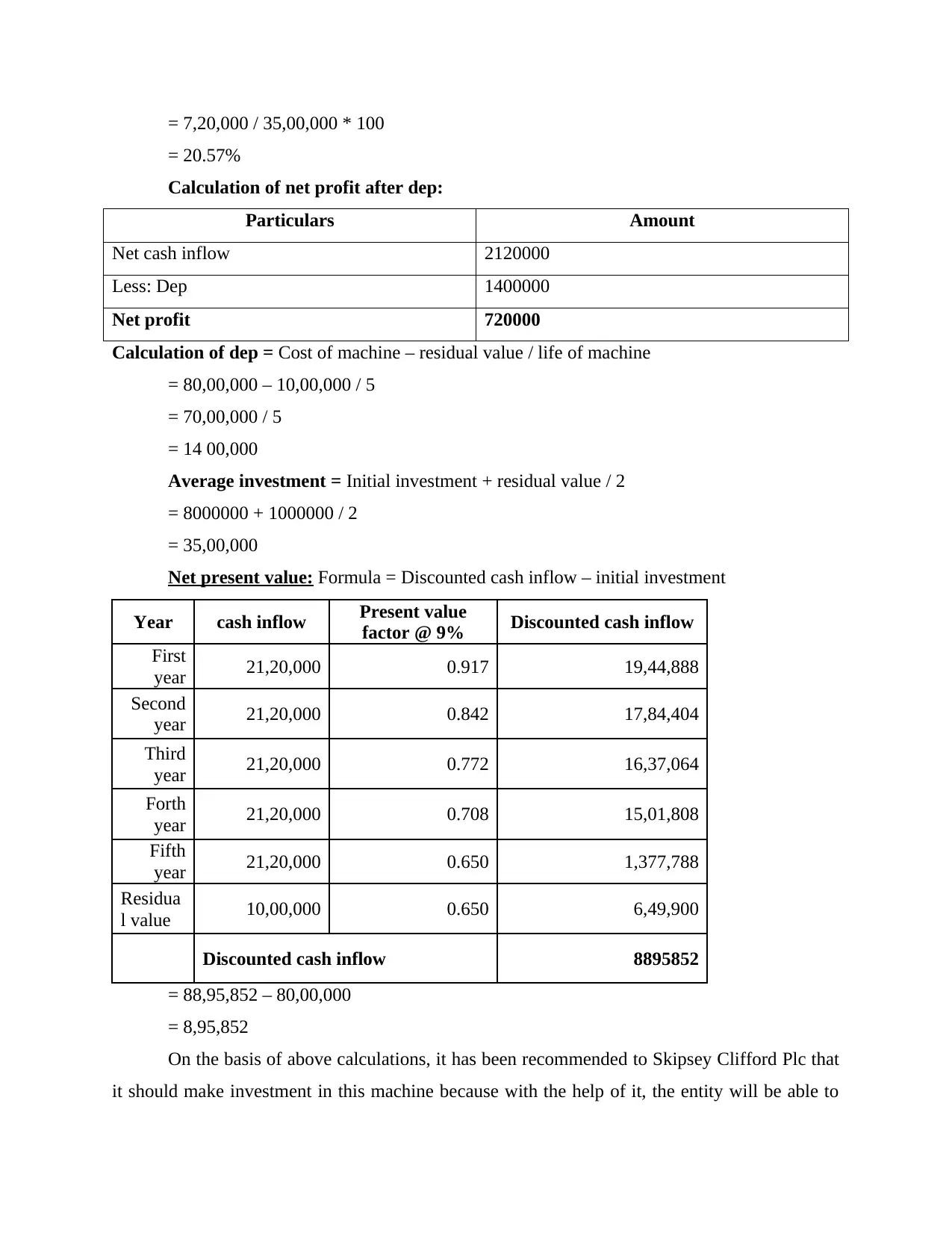

= 7,20,000 / 35,00,000 * 100

= 20.57%

Calculation of net profit after dep:

Particulars Amount

Net cash inflow 2120000

Less: Dep 1400000

Net profit 720000

Calculation of dep = Cost of machine – residual value / life of machine

= 80,00,000 – 10,00,000 / 5

= 70,00,000 / 5

= 14 00,000

Average investment = Initial investment + residual value / 2

= 8000000 + 1000000 / 2

= 35,00,000

Net present value: Formula = Discounted cash inflow – initial investment

Year cash inflow Present value

factor @ 9% Discounted cash inflow

First

year 21,20,000 0.917 19,44,888

Second

year 21,20,000 0.842 17,84,404

Third

year 21,20,000 0.772 16,37,064

Forth

year 21,20,000 0.708 15,01,808

Fifth

year 21,20,000 0.650 1,377,788

Residua

l value 10,00,000 0.650 6,49,900

Discounted cash inflow 8895852

= 88,95,852 – 80,00,000

= 8,95,852

On the basis of above calculations, it has been recommended to Skipsey Clifford Plc that

it should make investment in this machine because with the help of it, the entity will be able to

= 20.57%

Calculation of net profit after dep:

Particulars Amount

Net cash inflow 2120000

Less: Dep 1400000

Net profit 720000

Calculation of dep = Cost of machine – residual value / life of machine

= 80,00,000 – 10,00,000 / 5

= 70,00,000 / 5

= 14 00,000

Average investment = Initial investment + residual value / 2

= 8000000 + 1000000 / 2

= 35,00,000

Net present value: Formula = Discounted cash inflow – initial investment

Year cash inflow Present value

factor @ 9% Discounted cash inflow

First

year 21,20,000 0.917 19,44,888

Second

year 21,20,000 0.842 17,84,404

Third

year 21,20,000 0.772 16,37,064

Forth

year 21,20,000 0.708 15,01,808

Fifth

year 21,20,000 0.650 1,377,788

Residua

l value 10,00,000 0.650 6,49,900

Discounted cash inflow 8895852

= 88,95,852 – 80,00,000

= 8,95,852

On the basis of above calculations, it has been recommended to Skipsey Clifford Plc that

it should make investment in this machine because with the help of it, the entity will be able to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.