HNBS 310 Financial Accounting Report: Scenario Analysis

VerifiedAdded on 2023/01/09

|24

|4442

|69

Report

AI Summary

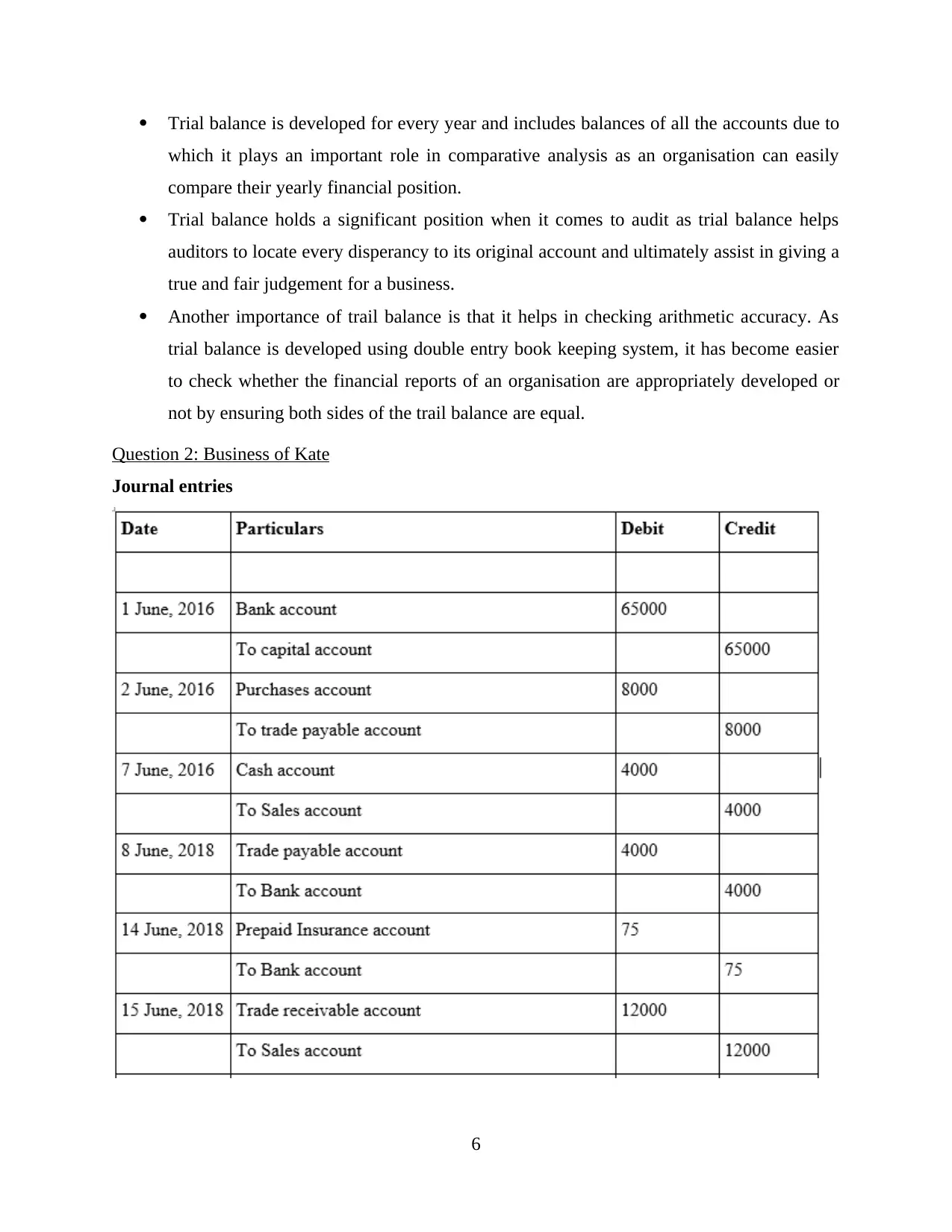

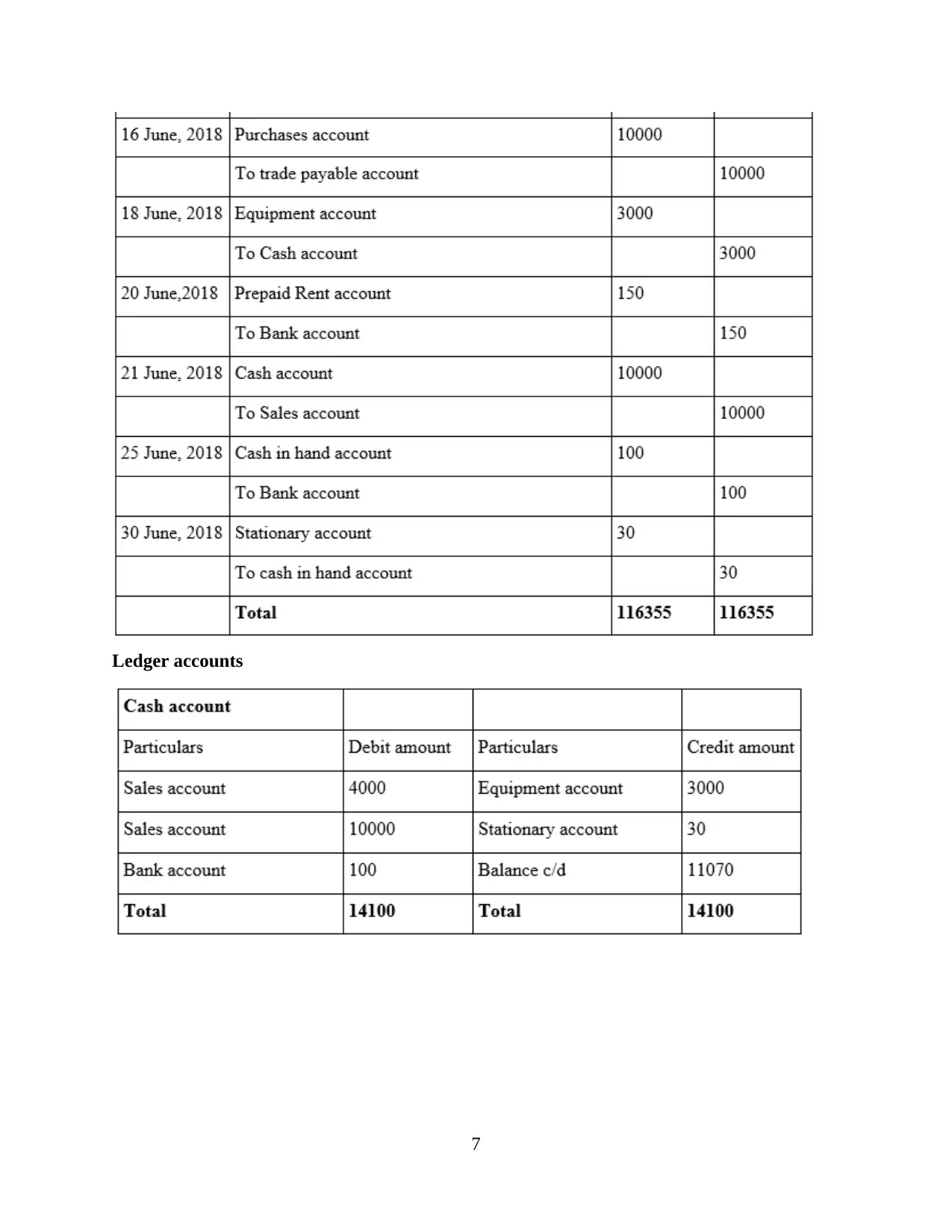

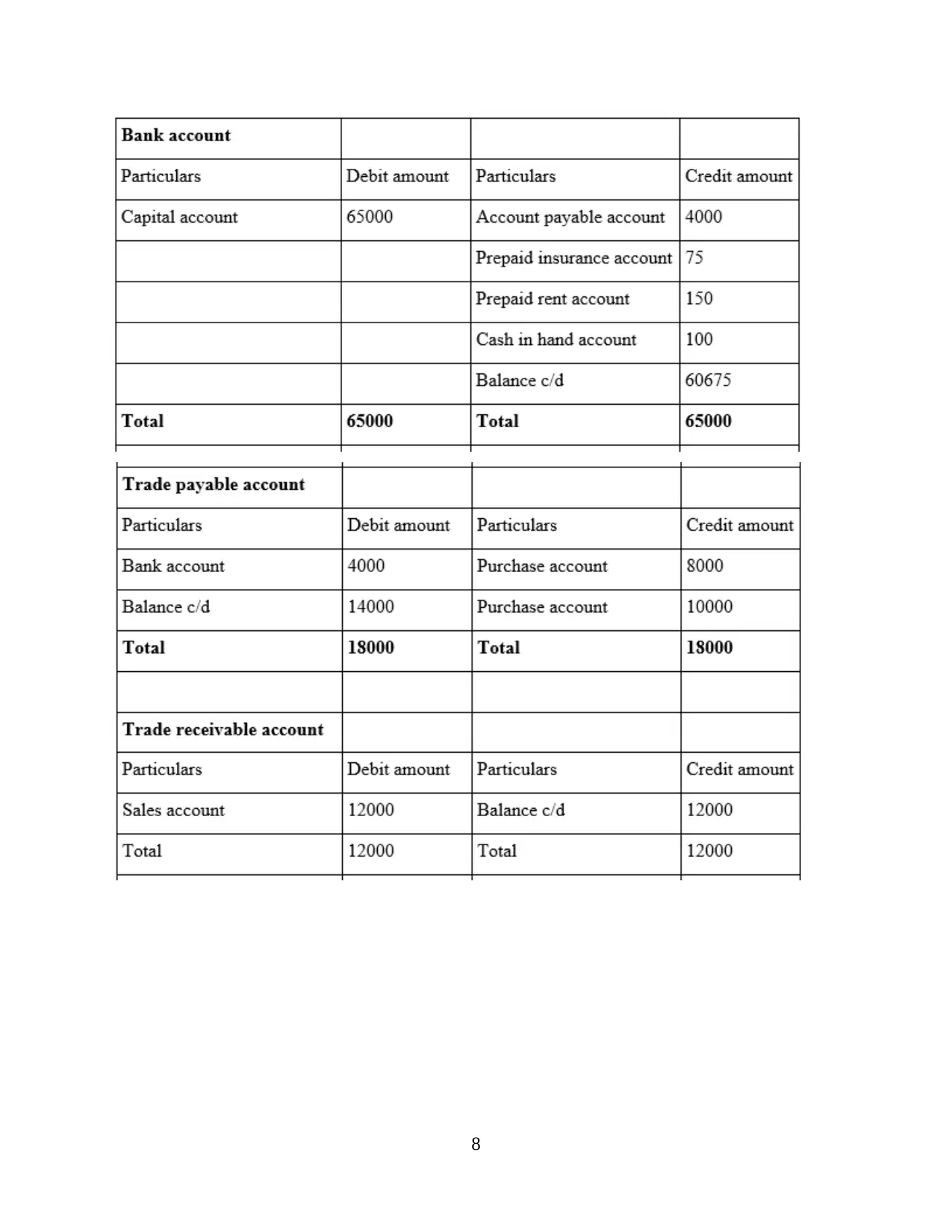

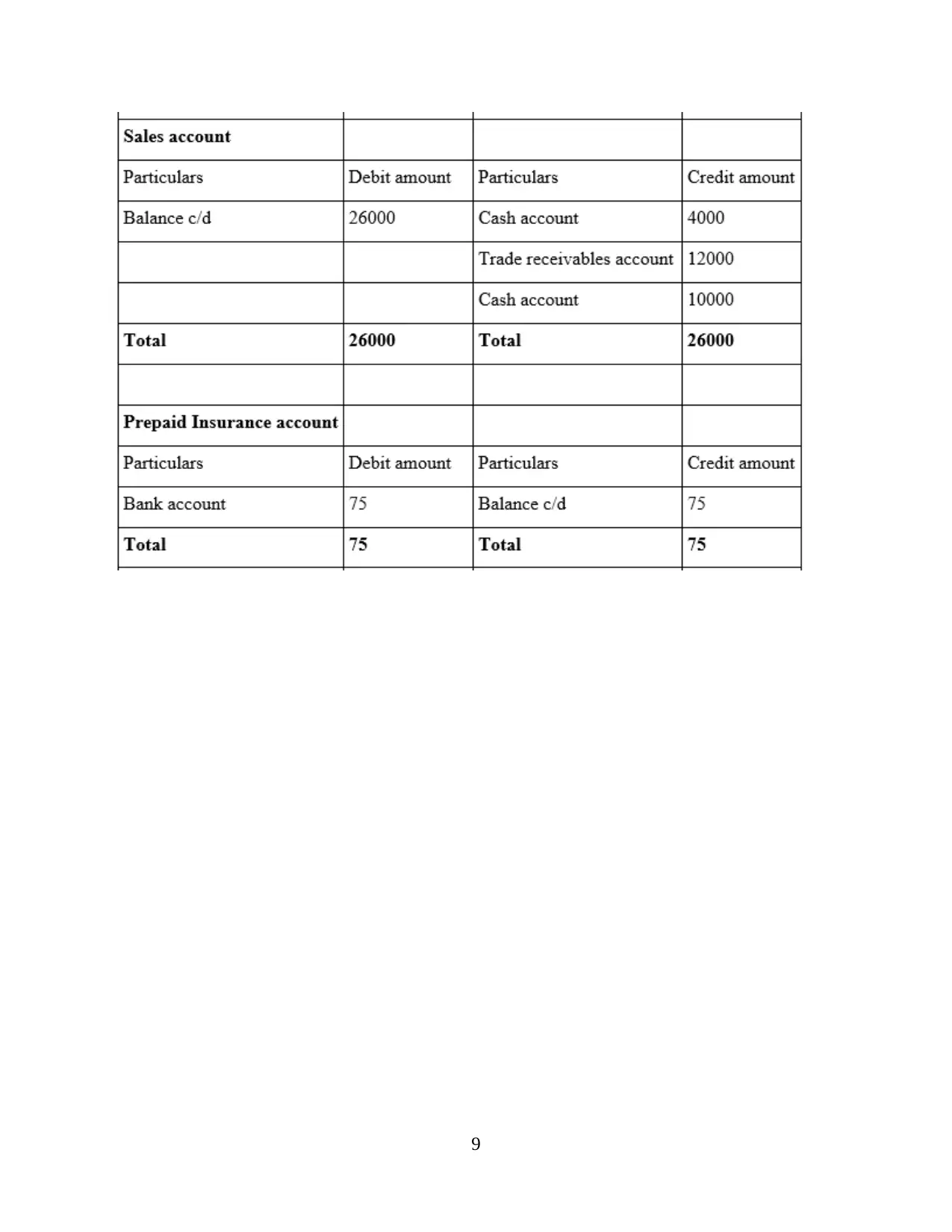

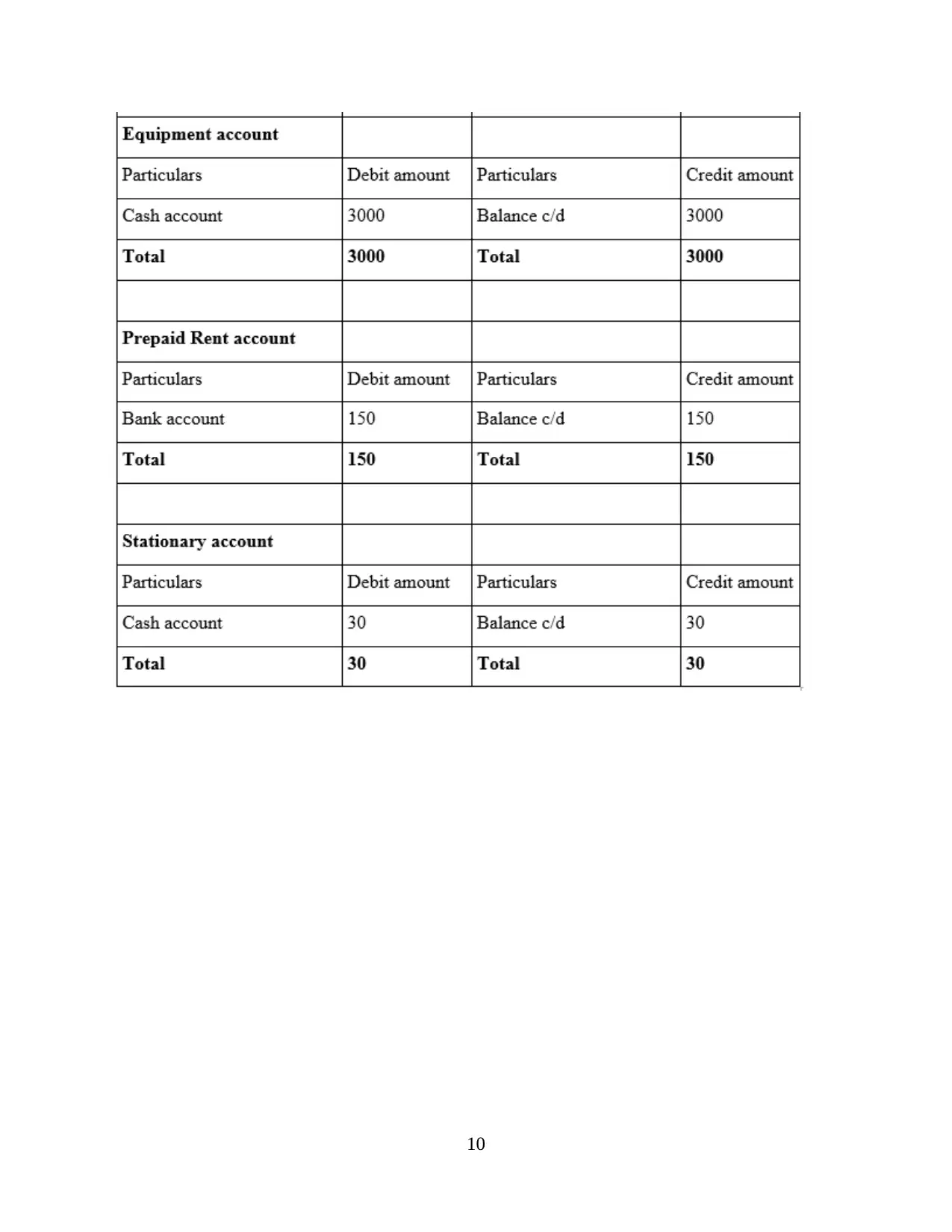

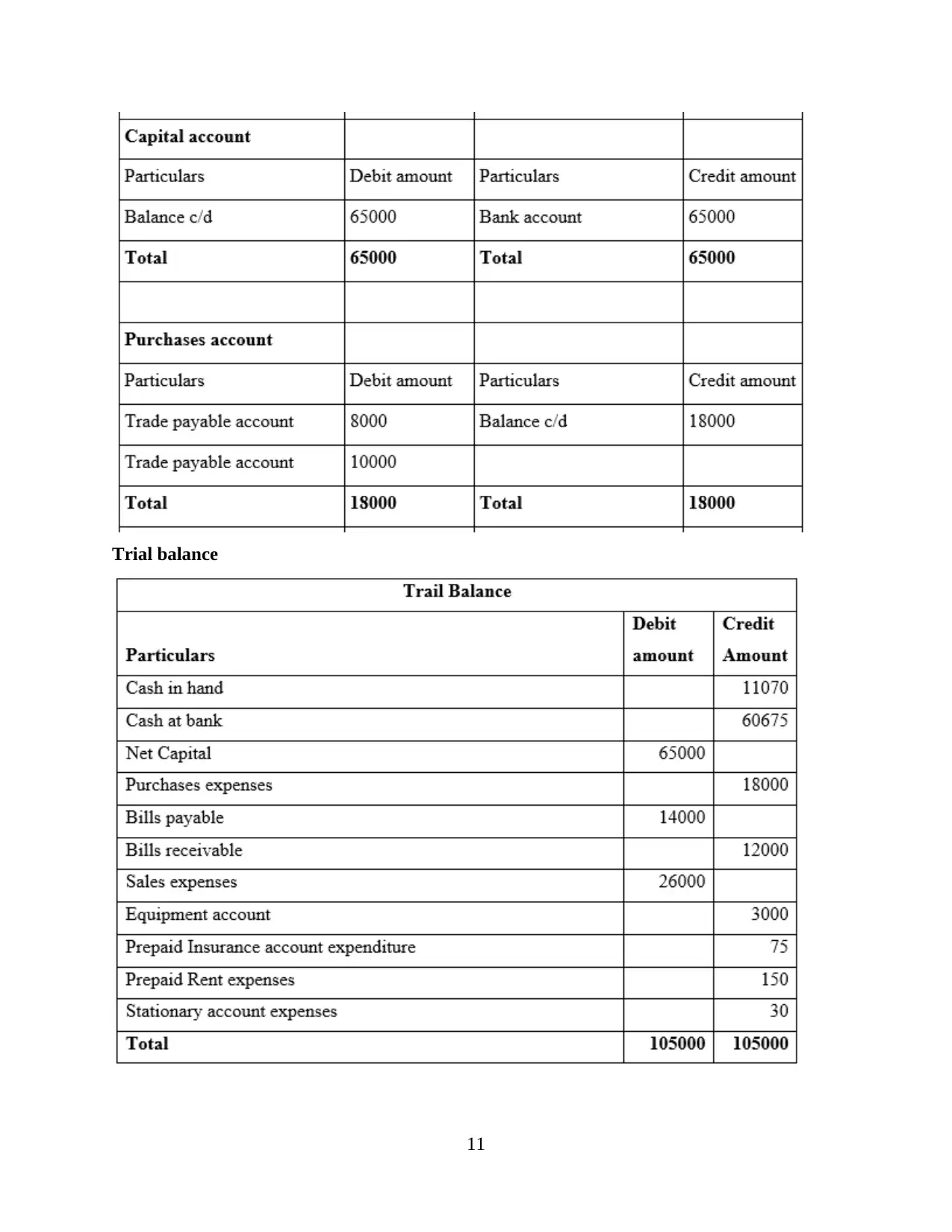

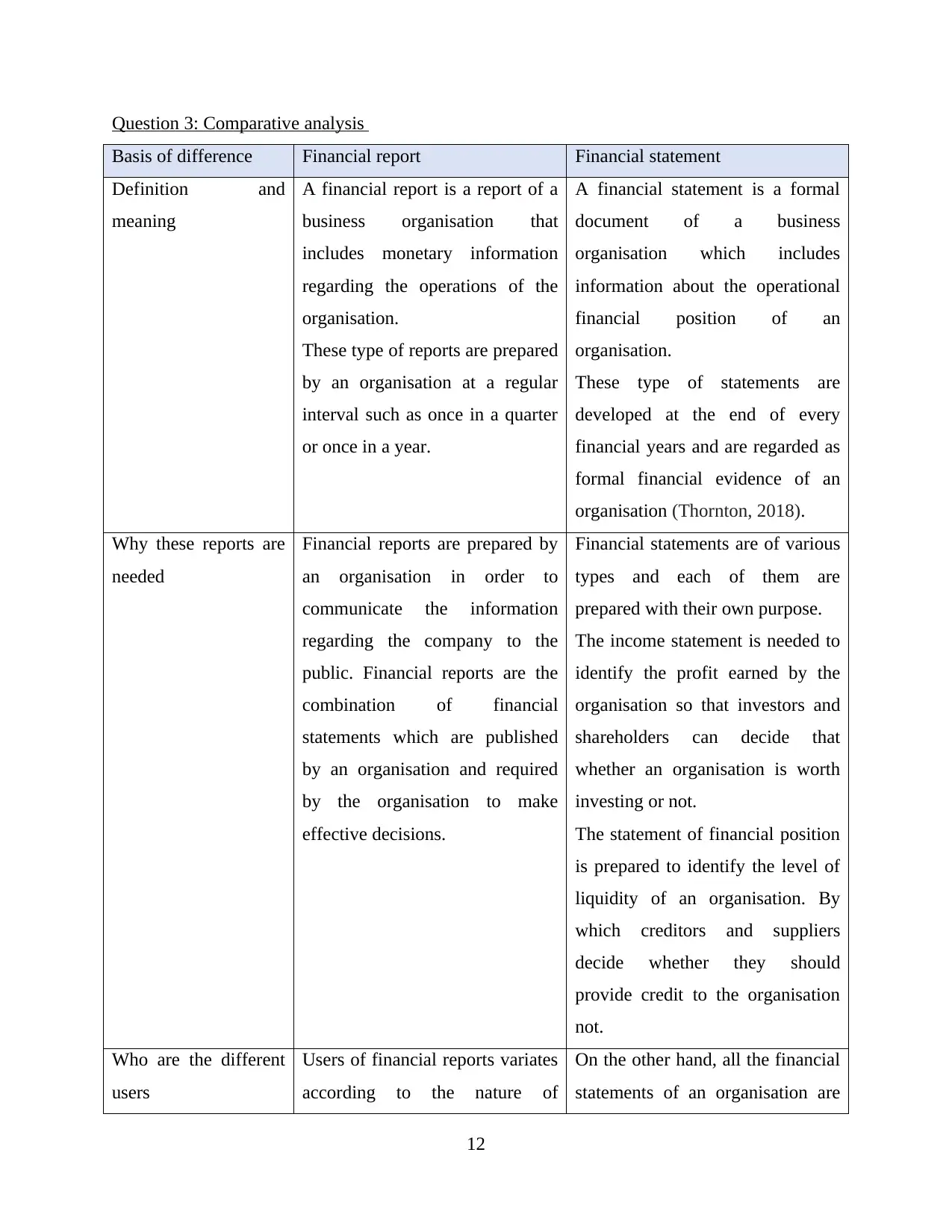

This comprehensive financial accounting report, created for the HNBS 310 course, delves into various aspects of financial accounting through two distinct scenarios. The first scenario explores the analysis of business transactions, encompassing internal and external transactions, single and double-entry bookkeeping systems, and the importance of the trial balance. It includes practical applications such as journal entries, ledger accounts, trial balance, and the preparation of financial statements for a hypothetical business. Additionally, the report provides a comparative analysis of financial reports and financial statements, along with an examination of fundamental accounting principles like the cost principle, going concern principle, full disclosure principle, revenue recognition principle, and matching principle. The second scenario focuses on the bank reconciliation process, the use of control accounts, and suspense accounts. The report concludes with a practical application of these concepts through the analysis of business scenarios, providing a well-rounded understanding of financial accounting principles and practices.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.