Financial Accounting Principles Report: Case Studies and Analysis

VerifiedAdded on 2020/10/22

|21

|5839

|347

Report

AI Summary

This report provides a comprehensive overview of financial accounting principles, including their purpose and application. It begins with an introduction to financial accounting, defining its role in recording, classifying, and reporting financial transactions for internal and external stakeholders. The report then explores the purpose of financial accounting, emphasizing its significance in providing information for decision-making, assessing business performance, and ensuring compliance with regulations. It distinguishes between internal and external stakeholders, detailing their respective interests in financial information. The report further delves into practical aspects, such as journal entries, ledgers, trial balances, statements of profit and loss, and statements of financial position. It covers accounting concepts like consistency and prudence, the role of depreciation, and the differences between financial statements of sole traders and limited companies. Additionally, it explains bank reconciliation statements, control accounts, and suspense accounts, providing examples and practical applications. The report concludes with a summary of key findings and a list of references.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

BUSINESS REPORT......................................................................................................................4

1.Financial Accounting and its purpose:................................................................................4

2. Internal and external stakeholder:......................................................................................5

CLIENT 1........................................................................................................................................6

1. Journal Entries and Ledgers in the book of Alexandra Study:...........................................6

2. Trial Balance as at 31st January 2019 in the books of Alexandra Study:........................13

CLIENT 2......................................................................................................................................14

1. Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018:14

2. Statement of financial position of Munteanu Ltd. As at 31st December 2018:...............15

3. Accounting Concepts: Consistency and Prudency:..........................................................16

4. Purpose of depreciation in formulating accounting statement:........................................16

5. Evaluation of difference between financial statements prepared by the sole trader & the

limited companies ................................................................................................................16

CLIENT 3 .....................................................................................................................................17

1. Purpose of preparation of Bank-reconciliation Statement:..............................................17

2. Reasons for difference between balance of bank column of cash book and bank statements:

..............................................................................................................................................17

3. Imprest:.............................................................................................................................17

4. Bank-reconciliation Statement as at 30 September 2018:................................................17

CLIENT 4......................................................................................................................................18

1. Sales Ledger Control Account in the books of January 2018:.........................................18

2. Purchase Ledger Control Account in the books of January 2018:...................................18

3. Control Account:..............................................................................................................19

CLIENT 5......................................................................................................................................19

1. Suspense account and its main features:..........................................................................19

2. Trial Balance using a control account as balancing figure:..............................................19

3. Journal Entries for corrections:........................................................................................20

CONCLUSION..............................................................................................................................20

INTRODUCTION...........................................................................................................................4

BUSINESS REPORT......................................................................................................................4

1.Financial Accounting and its purpose:................................................................................4

2. Internal and external stakeholder:......................................................................................5

CLIENT 1........................................................................................................................................6

1. Journal Entries and Ledgers in the book of Alexandra Study:...........................................6

2. Trial Balance as at 31st January 2019 in the books of Alexandra Study:........................13

CLIENT 2......................................................................................................................................14

1. Statement of Profit and Loss of Munteanu Ltd. For the year ended 31st December 2018:14

2. Statement of financial position of Munteanu Ltd. As at 31st December 2018:...............15

3. Accounting Concepts: Consistency and Prudency:..........................................................16

4. Purpose of depreciation in formulating accounting statement:........................................16

5. Evaluation of difference between financial statements prepared by the sole trader & the

limited companies ................................................................................................................16

CLIENT 3 .....................................................................................................................................17

1. Purpose of preparation of Bank-reconciliation Statement:..............................................17

2. Reasons for difference between balance of bank column of cash book and bank statements:

..............................................................................................................................................17

3. Imprest:.............................................................................................................................17

4. Bank-reconciliation Statement as at 30 September 2018:................................................17

CLIENT 4......................................................................................................................................18

1. Sales Ledger Control Account in the books of January 2018:.........................................18

2. Purchase Ledger Control Account in the books of January 2018:...................................18

3. Control Account:..............................................................................................................19

CLIENT 5......................................................................................................................................19

1. Suspense account and its main features:..........................................................................19

2. Trial Balance using a control account as balancing figure:..............................................19

3. Journal Entries for corrections:........................................................................................20

CONCLUSION..............................................................................................................................20

REFERENCES .............................................................................................................................22

INTRODUCTION

Financial accounting is an organised course of action including activities such as

recording of accounting transaction, classification, verification, interpreting, summarizing and

communicating or reporting of financial information. Financial accounting provides details and

information regarding availability of existing or potential resources, way of financing and output

through their utilisation. Financial accounting also provides groundwork for Internal and external

stakeholders in order to take significant decisions (Agasisti and Catalano, 2013). In order to

analyse the performance of PURCO company has been taken into account. All activities and

functions of financial accounting are governed or administrated by some rules and guidelines

called as financial accounting principles such as UK GAAP (Generally Accepted Accounting

Principles). This report provides an explanation about definition of financial accounting, purpose

of financial accounting, internal and external stakeholders and brief knowledge about accounting

concepts, purpose of providing depreciation and major methods of depreciation, control accounts

and purpose of bank reconciliation statements.

BUSINESS REPORT

1. Financial Accounting and its purpose:

Financial accounting refers to a systematic process classification of financial and non-

financial transactions, recording of transaction, summarizing them for a better interpretation and

reporting under a formal format to internal and external stakeholders. Financial accounting

processes are structure in a systematic way and ensures compliances of various accounting

principles, policies, rules and regulations (Alver, Alver and Talpas, 2013). Financial accounting

gives a structure for quick assessment of any problems and for taking vital decisions. Following

are the most considerable purpose of financial accounting, as follows:

Financial reporting helps to record all financial transactions as per double entry

system in an organised manner.

It helps to assess the actual position and performance of business organisation.

It assists in projecting anticipated earnings and performance of business organisation.

INTRODUCTION

Financial accounting is an organised course of action including activities such as

recording of accounting transaction, classification, verification, interpreting, summarizing and

communicating or reporting of financial information. Financial accounting provides details and

information regarding availability of existing or potential resources, way of financing and output

through their utilisation. Financial accounting also provides groundwork for Internal and external

stakeholders in order to take significant decisions (Agasisti and Catalano, 2013). In order to

analyse the performance of PURCO company has been taken into account. All activities and

functions of financial accounting are governed or administrated by some rules and guidelines

called as financial accounting principles such as UK GAAP (Generally Accepted Accounting

Principles). This report provides an explanation about definition of financial accounting, purpose

of financial accounting, internal and external stakeholders and brief knowledge about accounting

concepts, purpose of providing depreciation and major methods of depreciation, control accounts

and purpose of bank reconciliation statements.

BUSINESS REPORT

1. Financial Accounting and its purpose:

Financial accounting refers to a systematic process classification of financial and non-

financial transactions, recording of transaction, summarizing them for a better interpretation and

reporting under a formal format to internal and external stakeholders. Financial accounting

processes are structure in a systematic way and ensures compliances of various accounting

principles, policies, rules and regulations (Alver, Alver and Talpas, 2013). Financial accounting

gives a structure for quick assessment of any problems and for taking vital decisions. Following

are the most considerable purpose of financial accounting, as follows:

Financial reporting helps to record all financial transactions as per double entry

system in an organised manner.

It helps to assess the actual position and performance of business organisation.

It assists in projecting anticipated earnings and performance of business organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial reporting provides a basis for better decision making to investors and other

stakeholders actual profitability and liquidity situation of business organisation as on

a particular date.

It ensures compliance of statutory requirements, policies, framework, rules and

regulations.

It provides a comparative data and records along with previous years’ data and

competitor’s data and record to evaluate the performance effectively.

It serves as a formal report of financial health of business organisation to top

management and external users of financial information (Barth, 2015).

It helps to classify organisation's various assets and liabilities in order to manage

them efficiently.

2. Internal and external stakeholder:

Stakeholders are person, individual, group, body of individuals or organisation having

direct or indirect interest in organisation's position, performance, objectives or goals and results.

Stakeholder are classified as internal stakeholders and external stakeholders. Internal

stakeholders are person, group or individuals within the business organisation having substantial

interest. Whereas external stakeholders are individuals, persons, group or organisation outside

the business organisation associated with organisation and having direct or indirect interest

(Edwards, 2013).

Internal Stakeholder: In a large business organisation, internal stakeholders are shareholders,

owners, management and employees (Stice and Stice, 2013). Following is a brief discussion

about major internal stakeholders and, possible way through which they are interested in

financial information of organisation, as follows:

Owners and shareholders: They are real stakeholders of entity. Owner and shareholders

are holding major shares of a large business organisation and gain profits in case of

increase in share price. They are highly affected by the performance and financial

position of company.

Employees: Employees are most considerable resources of a business organisation and

always wants to achieve growth within the organisation. Employees are having

sustainable stake in business organisation because their salary and career are dependent

on performance and growth of organisation.

stakeholders actual profitability and liquidity situation of business organisation as on

a particular date.

It ensures compliance of statutory requirements, policies, framework, rules and

regulations.

It provides a comparative data and records along with previous years’ data and

competitor’s data and record to evaluate the performance effectively.

It serves as a formal report of financial health of business organisation to top

management and external users of financial information (Barth, 2015).

It helps to classify organisation's various assets and liabilities in order to manage

them efficiently.

2. Internal and external stakeholder:

Stakeholders are person, individual, group, body of individuals or organisation having

direct or indirect interest in organisation's position, performance, objectives or goals and results.

Stakeholder are classified as internal stakeholders and external stakeholders. Internal

stakeholders are person, group or individuals within the business organisation having substantial

interest. Whereas external stakeholders are individuals, persons, group or organisation outside

the business organisation associated with organisation and having direct or indirect interest

(Edwards, 2013).

Internal Stakeholder: In a large business organisation, internal stakeholders are shareholders,

owners, management and employees (Stice and Stice, 2013). Following is a brief discussion

about major internal stakeholders and, possible way through which they are interested in

financial information of organisation, as follows:

Owners and shareholders: They are real stakeholders of entity. Owner and shareholders

are holding major shares of a large business organisation and gain profits in case of

increase in share price. They are highly affected by the performance and financial

position of company.

Employees: Employees are most considerable resources of a business organisation and

always wants to achieve growth within the organisation. Employees are having

sustainable stake in business organisation because their salary and career are dependent

on performance and growth of organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

External Stakeholder: External stakeholders in case of a large business organisation are its

customers. Suppliers, government, creditors etc. Following is a short explanation about key

external stakeholders and, manner through which they are interested in financial information of

organisation, as follows:

Government: Government collect various taxes on income of business organisation so

government hold stake in profits of entities in form of taxes. Government along with collection

of taxes insures proper compliance of rules and regulation in business organisation.

Suppliers: Suppliers of goods and raw material receives payments from business

organisation and full-fills the demands. They always try to receive payment in scheduled times

and provides credit based on liquidity position of company so suppliers having stake in business

organisation in form of their payments and sales (DRURY, 2013).

Customers: Customers decides an organisation's growth and revenue. They contribute in

business by purchasing and by recommending product of company to others. Customers buy

product or services of organisation by analysing their popularity, quality, performance, growth

and beliefs therefore they are holding stake in form of performance and sustainability of business

organisation.

Investors: Investors are most significant for business organisation because they

contribute in expansion and growth of company by investing their money or other financial

assets in company. They are highly affected by performance and growth of business

organisation. Investors are actual stakeholder of company because they always try to get

maximum return from investment made by in business organisation.

CLIENT 1

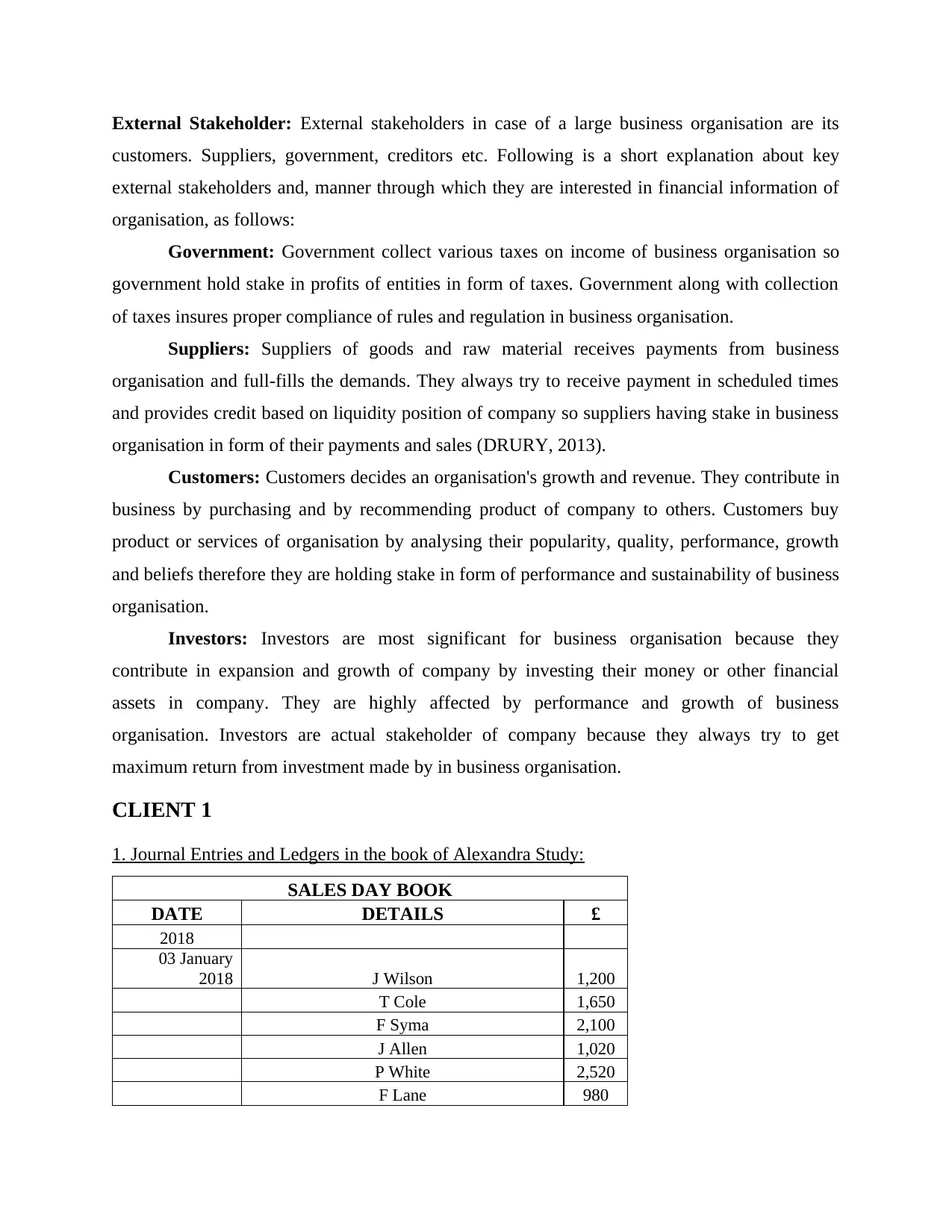

1. Journal Entries and Ledgers in the book of Alexandra Study:

SALES DAY BOOK

DATE DETAILS £

2018

03 January

2018 J Wilson 1,200

T Cole 1,650

F Syma 2,100

J Allen 1,020

P White 2,520

F Lane 980

customers. Suppliers, government, creditors etc. Following is a short explanation about key

external stakeholders and, manner through which they are interested in financial information of

organisation, as follows:

Government: Government collect various taxes on income of business organisation so

government hold stake in profits of entities in form of taxes. Government along with collection

of taxes insures proper compliance of rules and regulation in business organisation.

Suppliers: Suppliers of goods and raw material receives payments from business

organisation and full-fills the demands. They always try to receive payment in scheduled times

and provides credit based on liquidity position of company so suppliers having stake in business

organisation in form of their payments and sales (DRURY, 2013).

Customers: Customers decides an organisation's growth and revenue. They contribute in

business by purchasing and by recommending product of company to others. Customers buy

product or services of organisation by analysing their popularity, quality, performance, growth

and beliefs therefore they are holding stake in form of performance and sustainability of business

organisation.

Investors: Investors are most significant for business organisation because they

contribute in expansion and growth of company by investing their money or other financial

assets in company. They are highly affected by performance and growth of business

organisation. Investors are actual stakeholder of company because they always try to get

maximum return from investment made by in business organisation.

CLIENT 1

1. Journal Entries and Ledgers in the book of Alexandra Study:

SALES DAY BOOK

DATE DETAILS £

2018

03 January

2018 J Wilson 1,200

T Cole 1,650

F Syma 2,100

J Allen 1,020

P White 2,520

F Lane 980

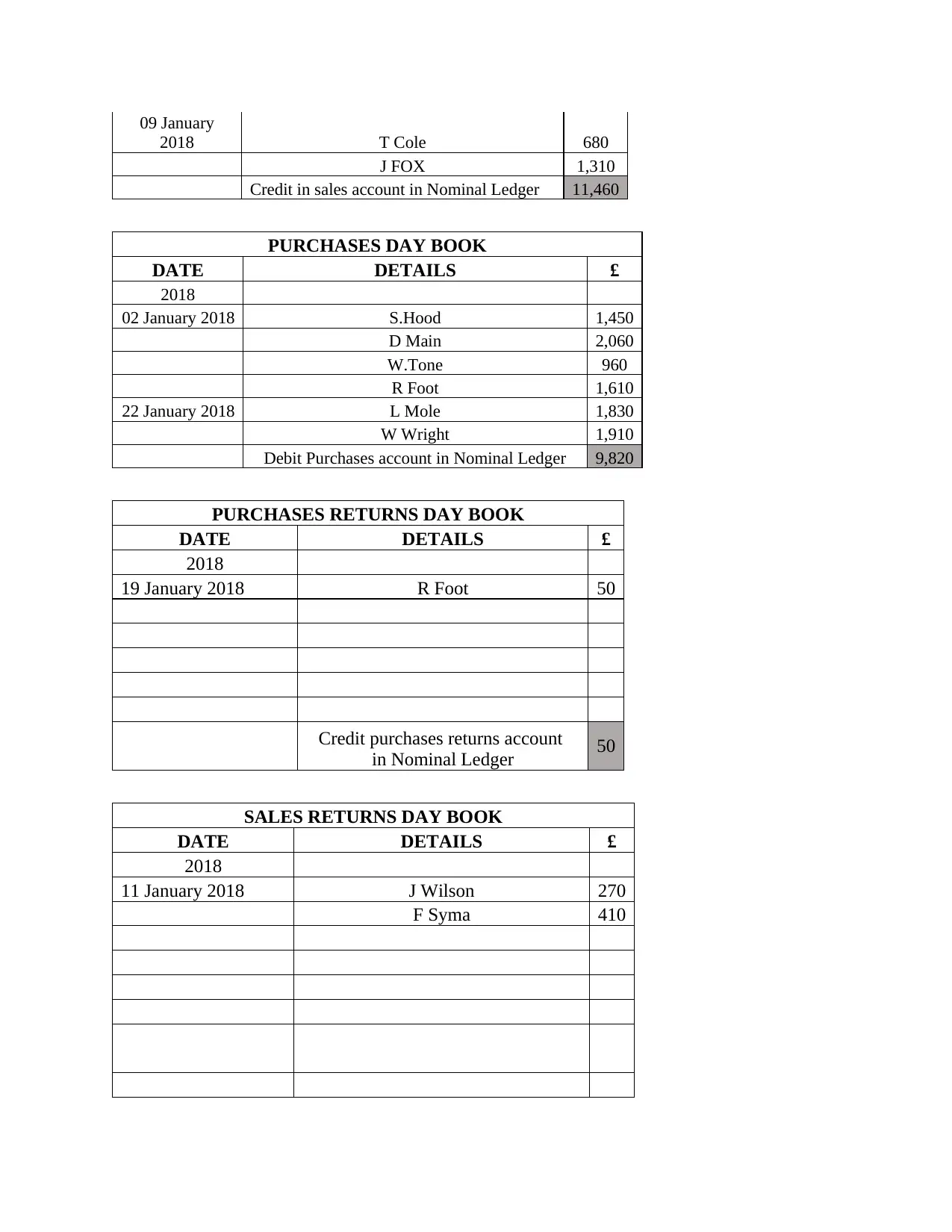

09 January

2018 T Cole 680

J FOX 1,310

Credit in sales account in Nominal Ledger 11,460

PURCHASES DAY BOOK

DATE DETAILS £

2018

02 January 2018 S.Hood 1,450

D Main 2,060

W.Tone 960

R Foot 1,610

22 January 2018 L Mole 1,830

W Wright 1,910

Debit Purchases account in Nominal Ledger 9,820

PURCHASES RETURNS DAY BOOK

DATE DETAILS £

2018

19 January 2018 R Foot 50

Credit purchases returns account

in Nominal Ledger 50

SALES RETURNS DAY BOOK

DATE DETAILS £

2018

11 January 2018 J Wilson 270

F Syma 410

2018 T Cole 680

J FOX 1,310

Credit in sales account in Nominal Ledger 11,460

PURCHASES DAY BOOK

DATE DETAILS £

2018

02 January 2018 S.Hood 1,450

D Main 2,060

W.Tone 960

R Foot 1,610

22 January 2018 L Mole 1,830

W Wright 1,910

Debit Purchases account in Nominal Ledger 9,820

PURCHASES RETURNS DAY BOOK

DATE DETAILS £

2018

19 January 2018 R Foot 50

Credit purchases returns account

in Nominal Ledger 50

SALES RETURNS DAY BOOK

DATE DETAILS £

2018

11 January 2018 J Wilson 270

F Syma 410

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debit sales returns account

in Nominal Ledger 680

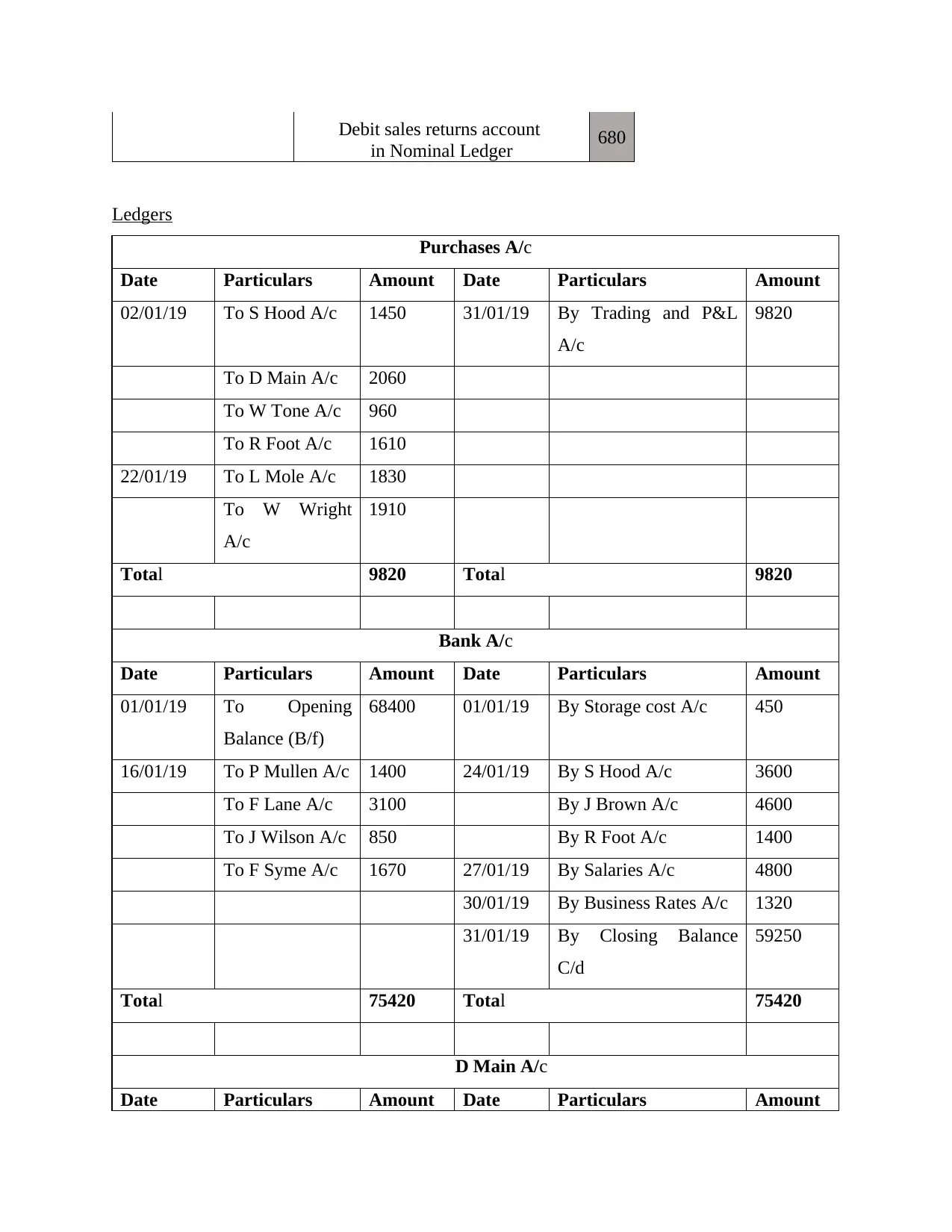

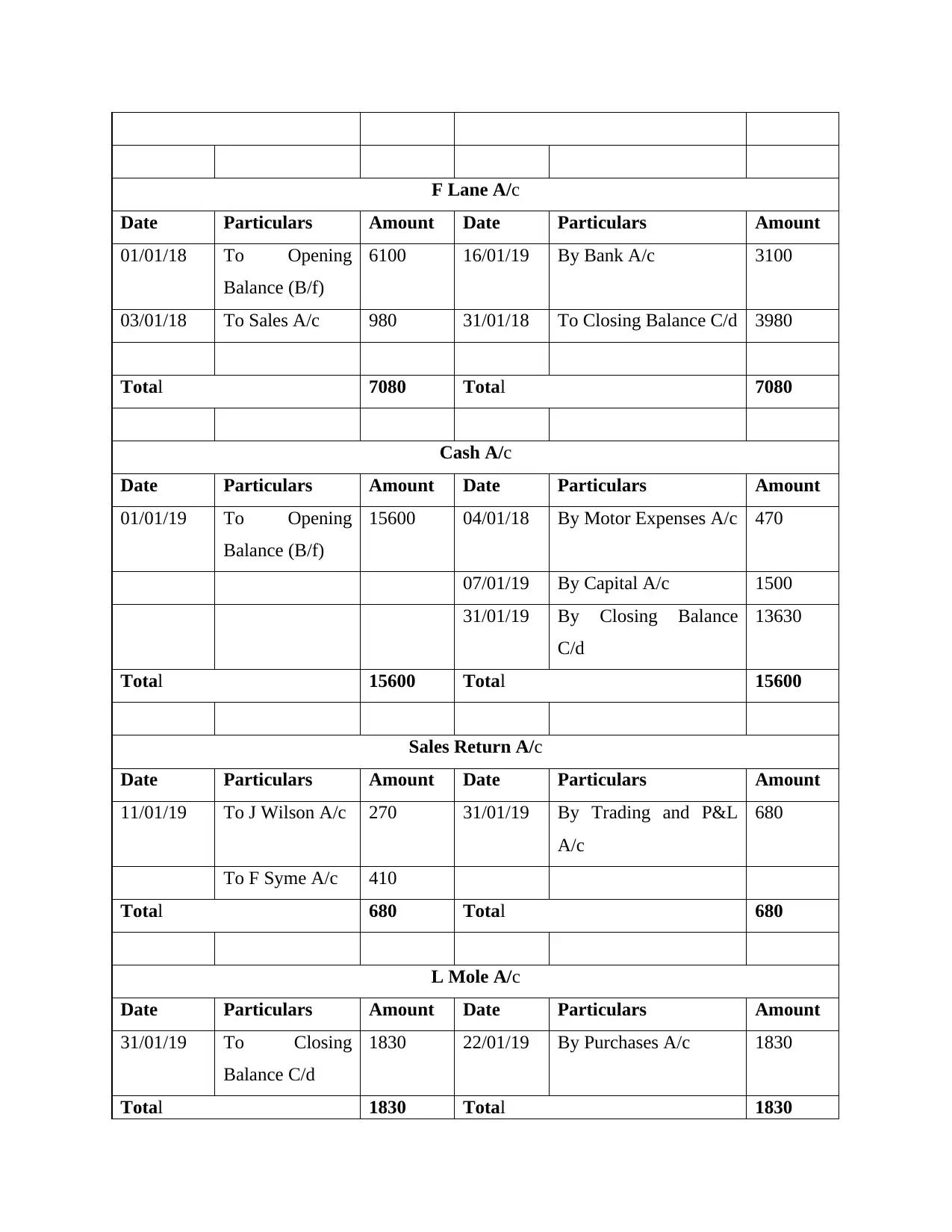

Ledgers

Purchases A/c

Date Particulars Amount Date Particulars Amount

02/01/19 To S Hood A/c 1450 31/01/19 By Trading and P&L

A/c

9820

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

22/01/19 To L Mole A/c 1830

To W Wright

A/c

1910

Total 9820 Total 9820

Bank A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

68400 01/01/19 By Storage cost A/c 450

16/01/19 To P Mullen A/c 1400 24/01/19 By S Hood A/c 3600

To F Lane A/c 3100 By J Brown A/c 4600

To J Wilson A/c 850 By R Foot A/c 1400

To F Syme A/c 1670 27/01/19 By Salaries A/c 4800

30/01/19 By Business Rates A/c 1320

31/01/19 By Closing Balance

C/d

59250

Total 75420 Total 75420

D Main A/c

Date Particulars Amount Date Particulars Amount

in Nominal Ledger 680

Ledgers

Purchases A/c

Date Particulars Amount Date Particulars Amount

02/01/19 To S Hood A/c 1450 31/01/19 By Trading and P&L

A/c

9820

To D Main A/c 2060

To W Tone A/c 960

To R Foot A/c 1610

22/01/19 To L Mole A/c 1830

To W Wright

A/c

1910

Total 9820 Total 9820

Bank A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

68400 01/01/19 By Storage cost A/c 450

16/01/19 To P Mullen A/c 1400 24/01/19 By S Hood A/c 3600

To F Lane A/c 3100 By J Brown A/c 4600

To J Wilson A/c 850 By R Foot A/c 1400

To F Syme A/c 1670 27/01/19 By Salaries A/c 4800

30/01/19 By Business Rates A/c 1320

31/01/19 By Closing Balance

C/d

59250

Total 75420 Total 75420

D Main A/c

Date Particulars Amount Date Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31/01/19 To Closing

Balance A/c

2060 02/01/19 By purchases A/c 2060

Total 2060 Total 2060

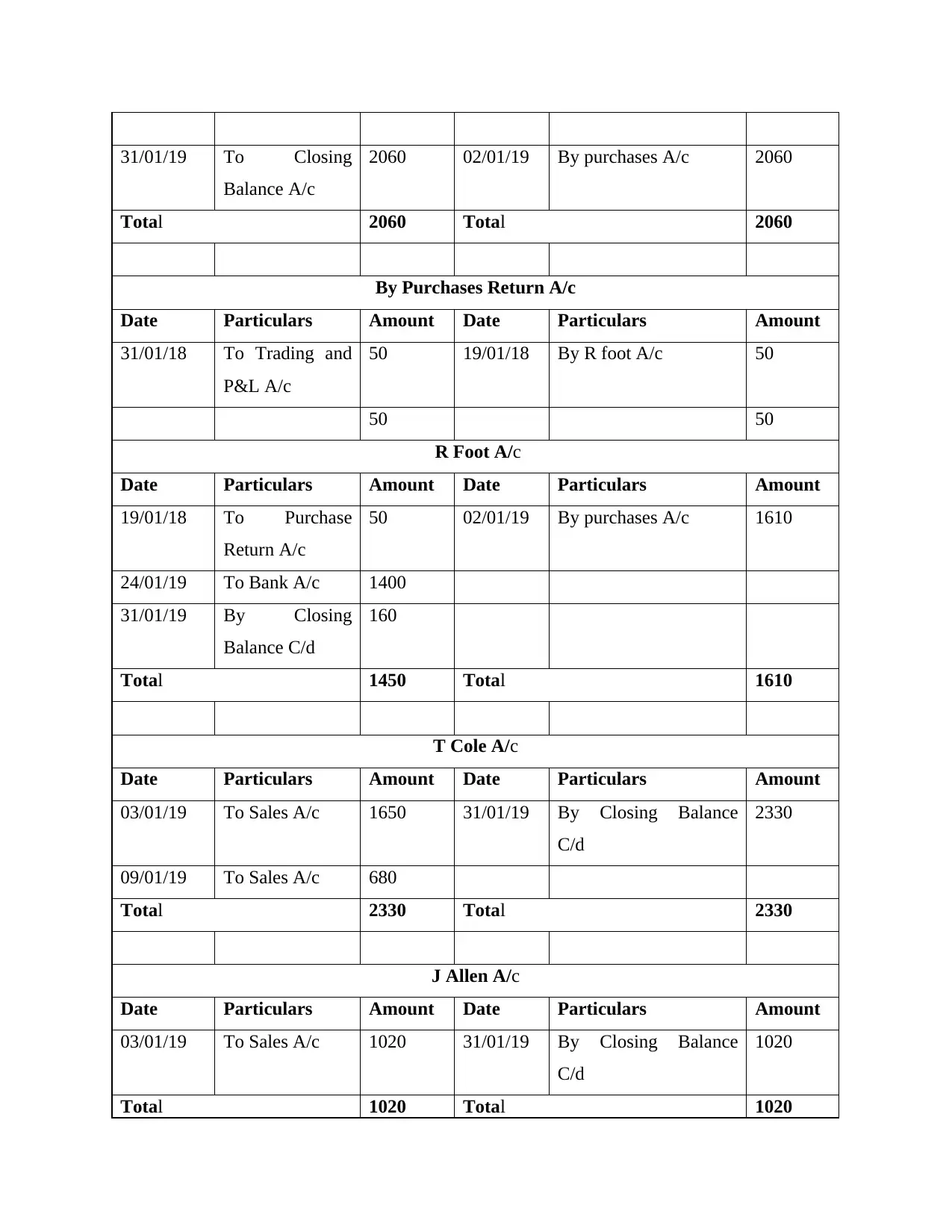

By Purchases Return A/c

Date Particulars Amount Date Particulars Amount

31/01/18 To Trading and

P&L A/c

50 19/01/18 By R foot A/c 50

50 50

R Foot A/c

Date Particulars Amount Date Particulars Amount

19/01/18 To Purchase

Return A/c

50 02/01/19 By purchases A/c 1610

24/01/19 To Bank A/c 1400

31/01/19 By Closing

Balance C/d

160

Total 1450 Total 1610

T Cole A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1650 31/01/19 By Closing Balance

C/d

2330

09/01/19 To Sales A/c 680

Total 2330 Total 2330

J Allen A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1020 31/01/19 By Closing Balance

C/d

1020

Total 1020 Total 1020

Balance A/c

2060 02/01/19 By purchases A/c 2060

Total 2060 Total 2060

By Purchases Return A/c

Date Particulars Amount Date Particulars Amount

31/01/18 To Trading and

P&L A/c

50 19/01/18 By R foot A/c 50

50 50

R Foot A/c

Date Particulars Amount Date Particulars Amount

19/01/18 To Purchase

Return A/c

50 02/01/19 By purchases A/c 1610

24/01/19 To Bank A/c 1400

31/01/19 By Closing

Balance C/d

160

Total 1450 Total 1610

T Cole A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1650 31/01/19 By Closing Balance

C/d

2330

09/01/19 To Sales A/c 680

Total 2330 Total 2330

J Allen A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1020 31/01/19 By Closing Balance

C/d

1020

Total 1020 Total 1020

F Lane A/c

Date Particulars Amount Date Particulars Amount

01/01/18 To Opening

Balance (B/f)

6100 16/01/19 By Bank A/c 3100

03/01/18 To Sales A/c 980 31/01/18 To Closing Balance C/d 3980

Total 7080 Total 7080

Cash A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

15600 04/01/18 By Motor Expenses A/c 470

07/01/19 By Capital A/c 1500

31/01/19 By Closing Balance

C/d

13630

Total 15600 Total 15600

Sales Return A/c

Date Particulars Amount Date Particulars Amount

11/01/19 To J Wilson A/c 270 31/01/19 By Trading and P&L

A/c

680

To F Syme A/c 410

Total 680 Total 680

L Mole A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1830 22/01/19 By Purchases A/c 1830

Total 1830 Total 1830

Date Particulars Amount Date Particulars Amount

01/01/18 To Opening

Balance (B/f)

6100 16/01/19 By Bank A/c 3100

03/01/18 To Sales A/c 980 31/01/18 To Closing Balance C/d 3980

Total 7080 Total 7080

Cash A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

15600 04/01/18 By Motor Expenses A/c 470

07/01/19 By Capital A/c 1500

31/01/19 By Closing Balance

C/d

13630

Total 15600 Total 15600

Sales Return A/c

Date Particulars Amount Date Particulars Amount

11/01/19 To J Wilson A/c 270 31/01/19 By Trading and P&L

A/c

680

To F Syme A/c 410

Total 680 Total 680

L Mole A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1830 22/01/19 By Purchases A/c 1830

Total 1830 Total 1830

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

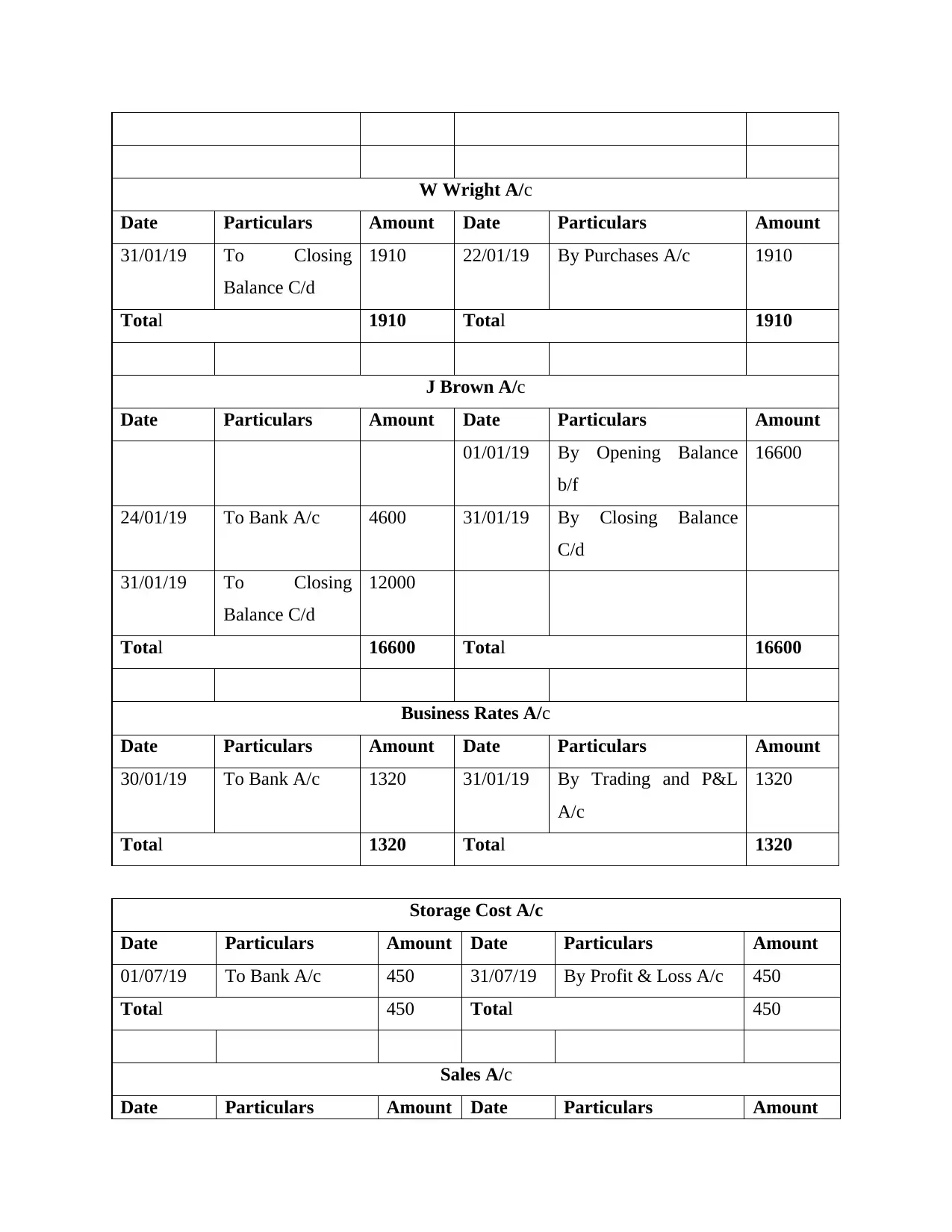

W Wright A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1910 22/01/19 By Purchases A/c 1910

Total 1910 Total 1910

J Brown A/c

Date Particulars Amount Date Particulars Amount

01/01/19 By Opening Balance

b/f

16600

24/01/19 To Bank A/c 4600 31/01/19 By Closing Balance

C/d

31/01/19 To Closing

Balance C/d

12000

Total 16600 Total 16600

Business Rates A/c

Date Particulars Amount Date Particulars Amount

30/01/19 To Bank A/c 1320 31/01/19 By Trading and P&L

A/c

1320

Total 1320 Total 1320

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/19 To Bank A/c 450 31/07/19 By Profit & Loss A/c 450

Total 450 Total 450

Sales A/c

Date Particulars Amount Date Particulars Amount

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

1910 22/01/19 By Purchases A/c 1910

Total 1910 Total 1910

J Brown A/c

Date Particulars Amount Date Particulars Amount

01/01/19 By Opening Balance

b/f

16600

24/01/19 To Bank A/c 4600 31/01/19 By Closing Balance

C/d

31/01/19 To Closing

Balance C/d

12000

Total 16600 Total 16600

Business Rates A/c

Date Particulars Amount Date Particulars Amount

30/01/19 To Bank A/c 1320 31/01/19 By Trading and P&L

A/c

1320

Total 1320 Total 1320

Storage Cost A/c

Date Particulars Amount Date Particulars Amount

01/07/19 To Bank A/c 450 31/07/19 By Profit & Loss A/c 450

Total 450 Total 450

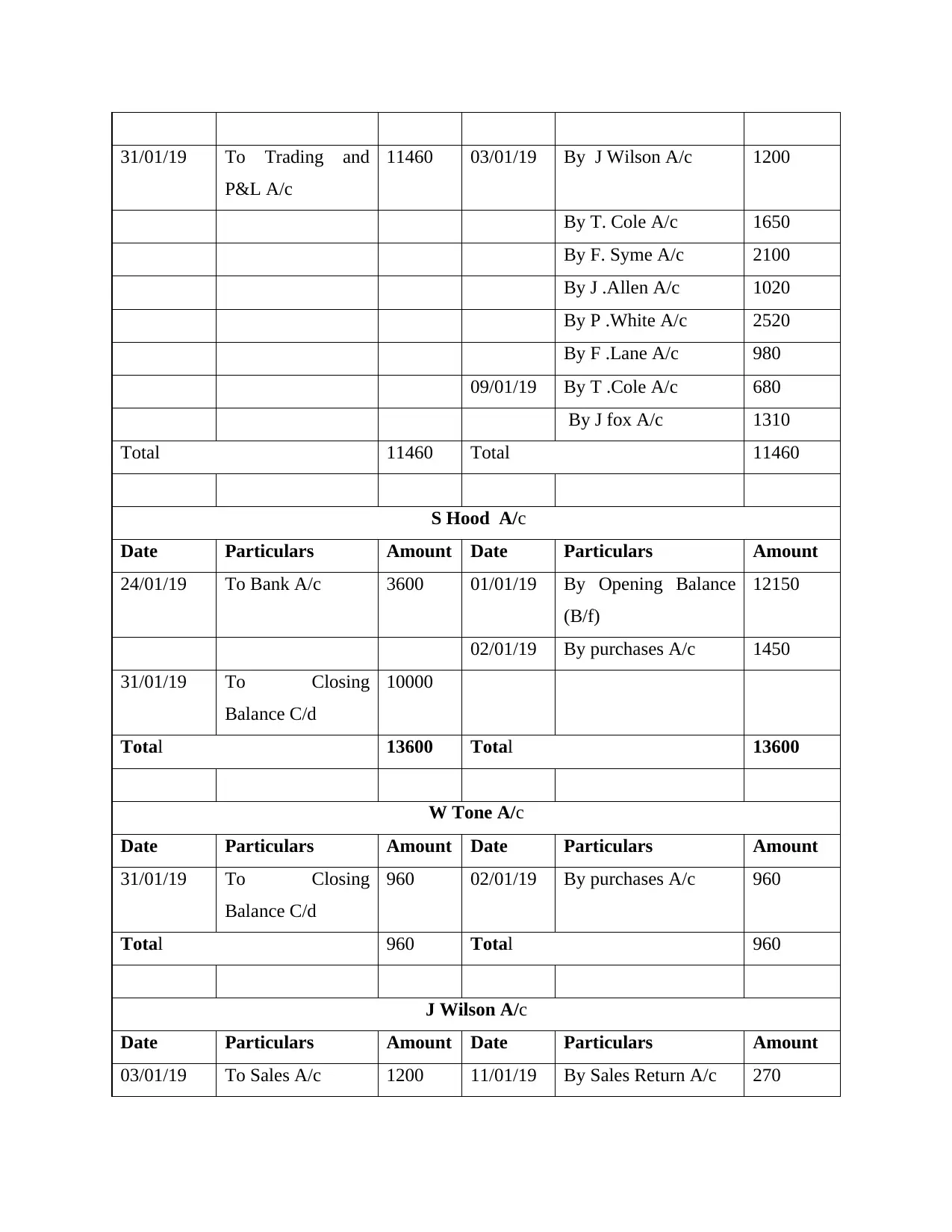

Sales A/c

Date Particulars Amount Date Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31/01/19 To Trading and

P&L A/c

11460 03/01/19 By J Wilson A/c 1200

By T. Cole A/c 1650

By F. Syme A/c 2100

By J .Allen A/c 1020

By P .White A/c 2520

By F .Lane A/c 980

09/01/19 By T .Cole A/c 680

By J fox A/c 1310

Total 11460 Total 11460

S Hood A/c

Date Particulars Amount Date Particulars Amount

24/01/19 To Bank A/c 3600 01/01/19 By Opening Balance

(B/f)

12150

02/01/19 By purchases A/c 1450

31/01/19 To Closing

Balance C/d

10000

Total 13600 Total 13600

W Tone A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

960 02/01/19 By purchases A/c 960

Total 960 Total 960

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1200 11/01/19 By Sales Return A/c 270

P&L A/c

11460 03/01/19 By J Wilson A/c 1200

By T. Cole A/c 1650

By F. Syme A/c 2100

By J .Allen A/c 1020

By P .White A/c 2520

By F .Lane A/c 980

09/01/19 By T .Cole A/c 680

By J fox A/c 1310

Total 11460 Total 11460

S Hood A/c

Date Particulars Amount Date Particulars Amount

24/01/19 To Bank A/c 3600 01/01/19 By Opening Balance

(B/f)

12150

02/01/19 By purchases A/c 1450

31/01/19 To Closing

Balance C/d

10000

Total 13600 Total 13600

W Tone A/c

Date Particulars Amount Date Particulars Amount

31/01/19 To Closing

Balance C/d

960 02/01/19 By purchases A/c 960

Total 960 Total 960

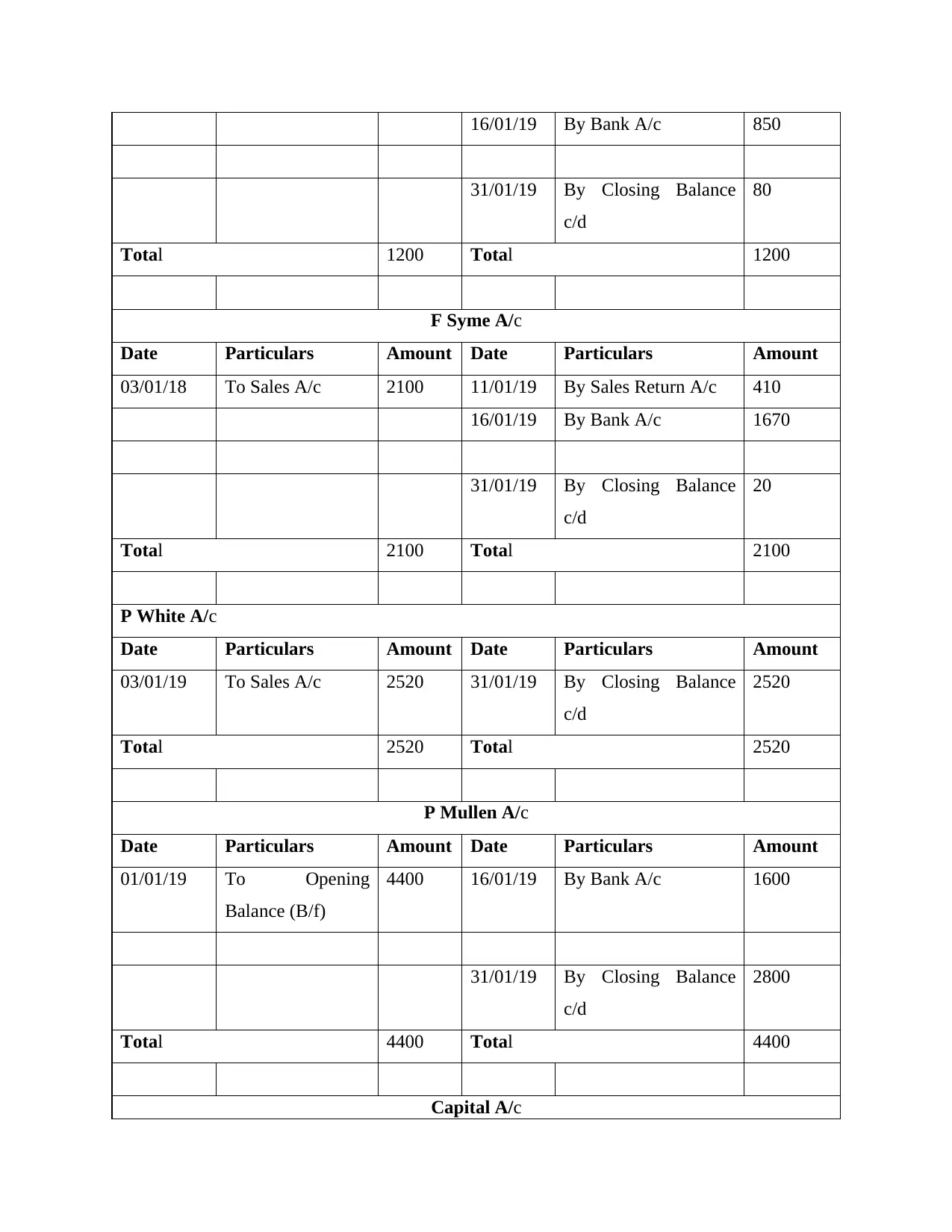

J Wilson A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 1200 11/01/19 By Sales Return A/c 270

16/01/19 By Bank A/c 850

31/01/19 By Closing Balance

c/d

80

Total 1200 Total 1200

F Syme A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2100 11/01/19 By Sales Return A/c 410

16/01/19 By Bank A/c 1670

31/01/19 By Closing Balance

c/d

20

Total 2100 Total 2100

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 2520 31/01/19 By Closing Balance

c/d

2520

Total 2520 Total 2520

P Mullen A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

4400 16/01/19 By Bank A/c 1600

31/01/19 By Closing Balance

c/d

2800

Total 4400 Total 4400

Capital A/c

31/01/19 By Closing Balance

c/d

80

Total 1200 Total 1200

F Syme A/c

Date Particulars Amount Date Particulars Amount

03/01/18 To Sales A/c 2100 11/01/19 By Sales Return A/c 410

16/01/19 By Bank A/c 1670

31/01/19 By Closing Balance

c/d

20

Total 2100 Total 2100

P White A/c

Date Particulars Amount Date Particulars Amount

03/01/19 To Sales A/c 2520 31/01/19 By Closing Balance

c/d

2520

Total 2520 Total 2520

P Mullen A/c

Date Particulars Amount Date Particulars Amount

01/01/19 To Opening

Balance (B/f)

4400 16/01/19 By Bank A/c 1600

31/01/19 By Closing Balance

c/d

2800

Total 4400 Total 4400

Capital A/c

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.