Financial Accounting Report: Valuation and Investment Analysis

VerifiedAdded on 2023/01/10

|19

|3907

|97

Report

AI Summary

This report provides an overview of financial accounting principles, focusing on valuation techniques and investment appraisal methods. It addresses two key issues: acquisition strategies through takeover and expense assessment. The report delves into the Price-Earnings (P/E) ratio, Dividend Discount Model (DVM), and Discounted Cash Flow (DCF) methods, analyzing their advantages and disadvantages. It recommends the P/E metric for valuing inventory. The report also examines investment appraisal processes, including payback period, Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR), providing calculations and interpretations for each. The analysis aims to assist companies in making informed financial decisions.

Assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial accounting involves the planning, administration, oversight and monitoring of

the Company's financial activities and the accumulation and use of the funds. Within this review,

we need to answer two concerns that are based on strategies for acquisition through takeover and

expense assessment (Yuniningsih, Pertiwi and Purwanto, 2019). Fund is the lifeline of one

company. However, finance is always limited, as are most other instruments. On the contrary, it

has yet to continue to stay infinite. Hence, it is important for an organization to control its assets

properly. As an introduction to finance management is covered in this report. This means

implementing the basic managerial ideas to the company's financial assets. There are several

functions that are used for various purposes such as estimates of capital spending, money

management, source of funds, redistribution of funds etc. Moreover, the second issue is linked to

the methods of investment evaluation.

MAIN BODY

Question 2

PE ratio: That is correlation between both the price of the shares and the profits from the EPS.

This is an increasing ratio giving a better picture of the company’s value. The P / E ratio

symbolizes the customer's requirements and is the cost payable per existing cash amount. Funds

usually like to know about the intrinsic value of an investment before having committed. They

look at risk, revenues, cash flow and different parts of financial statements. The P / E ratio and

other assessment tools are one of the most common approaches used to study the underlying

worth of a commodity (Davidova and Latruffe, 2020).

Financial accounting involves the planning, administration, oversight and monitoring of

the Company's financial activities and the accumulation and use of the funds. Within this review,

we need to answer two concerns that are based on strategies for acquisition through takeover and

expense assessment (Yuniningsih, Pertiwi and Purwanto, 2019). Fund is the lifeline of one

company. However, finance is always limited, as are most other instruments. On the contrary, it

has yet to continue to stay infinite. Hence, it is important for an organization to control its assets

properly. As an introduction to finance management is covered in this report. This means

implementing the basic managerial ideas to the company's financial assets. There are several

functions that are used for various purposes such as estimates of capital spending, money

management, source of funds, redistribution of funds etc. Moreover, the second issue is linked to

the methods of investment evaluation.

MAIN BODY

Question 2

PE ratio: That is correlation between both the price of the shares and the profits from the EPS.

This is an increasing ratio giving a better picture of the company’s value. The P / E ratio

symbolizes the customer's requirements and is the cost payable per existing cash amount. Funds

usually like to know about the intrinsic value of an investment before having committed. They

look at risk, revenues, cash flow and different parts of financial statements. The P / E ratio and

other assessment tools are one of the most common approaches used to study the underlying

worth of a commodity (Davidova and Latruffe, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

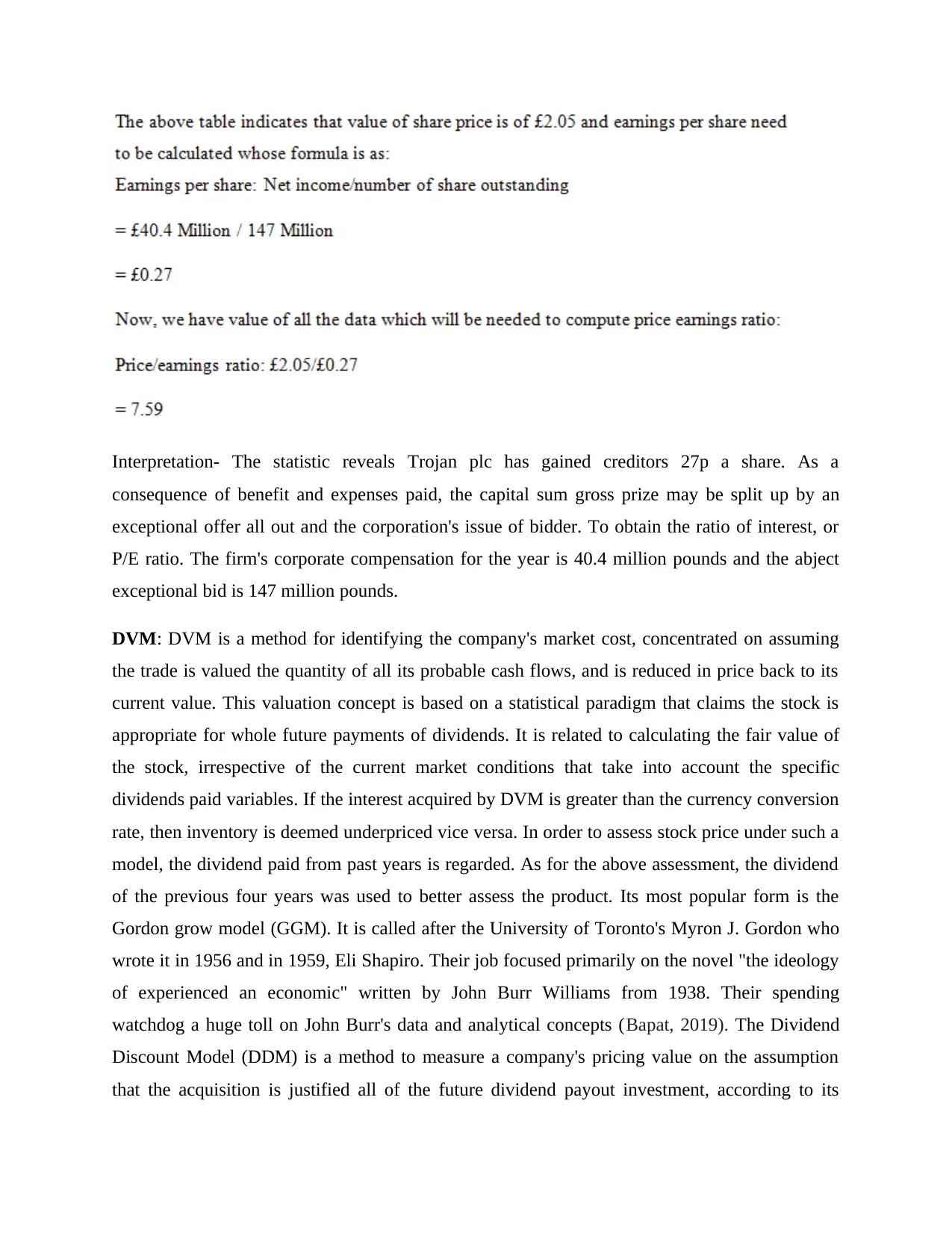

Interpretation- The statistic reveals Trojan plc has gained creditors 27p a share. As a

consequence of benefit and expenses paid, the capital sum gross prize may be split up by an

exceptional offer all out and the corporation's issue of bidder. To obtain the ratio of interest, or

P/E ratio. The firm's corporate compensation for the year is 40.4 million pounds and the abject

exceptional bid is 147 million pounds.

DVM: DVM is a method for identifying the company's market cost, concentrated on assuming

the trade is valued the quantity of all its probable cash flows, and is reduced in price back to its

current value. This valuation concept is based on a statistical paradigm that claims the stock is

appropriate for whole future payments of dividends. It is related to calculating the fair value of

the stock, irrespective of the current market conditions that take into account the specific

dividends paid variables. If the interest acquired by DVM is greater than the currency conversion

rate, then inventory is deemed underpriced vice versa. In order to assess stock price under such a

model, the dividend paid from past years is regarded. As for the above assessment, the dividend

of the previous four years was used to better assess the product. Its most popular form is the

Gordon grow model (GGM). It is called after the University of Toronto's Myron J. Gordon who

wrote it in 1956 and in 1959, Eli Shapiro. Their job focused primarily on the novel "the ideology

of experienced an economic" written by John Burr Williams from 1938. Their spending

watchdog a huge toll on John Burr's data and analytical concepts (Bapat, 2019). The Dividend

Discount Model (DDM) is a method to measure a company's pricing value on the assumption

that the acquisition is justified all of the future dividend payout investment, according to its

consequence of benefit and expenses paid, the capital sum gross prize may be split up by an

exceptional offer all out and the corporation's issue of bidder. To obtain the ratio of interest, or

P/E ratio. The firm's corporate compensation for the year is 40.4 million pounds and the abject

exceptional bid is 147 million pounds.

DVM: DVM is a method for identifying the company's market cost, concentrated on assuming

the trade is valued the quantity of all its probable cash flows, and is reduced in price back to its

current value. This valuation concept is based on a statistical paradigm that claims the stock is

appropriate for whole future payments of dividends. It is related to calculating the fair value of

the stock, irrespective of the current market conditions that take into account the specific

dividends paid variables. If the interest acquired by DVM is greater than the currency conversion

rate, then inventory is deemed underpriced vice versa. In order to assess stock price under such a

model, the dividend paid from past years is regarded. As for the above assessment, the dividend

of the previous four years was used to better assess the product. Its most popular form is the

Gordon grow model (GGM). It is called after the University of Toronto's Myron J. Gordon who

wrote it in 1956 and in 1959, Eli Shapiro. Their job focused primarily on the novel "the ideology

of experienced an economic" written by John Burr Williams from 1938. Their spending

watchdog a huge toll on John Burr's data and analytical concepts (Bapat, 2019). The Dividend

Discount Model (DDM) is a method to measure a company's pricing value on the assumption

that the acquisition is justified all of the future dividend payout investment, according to its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

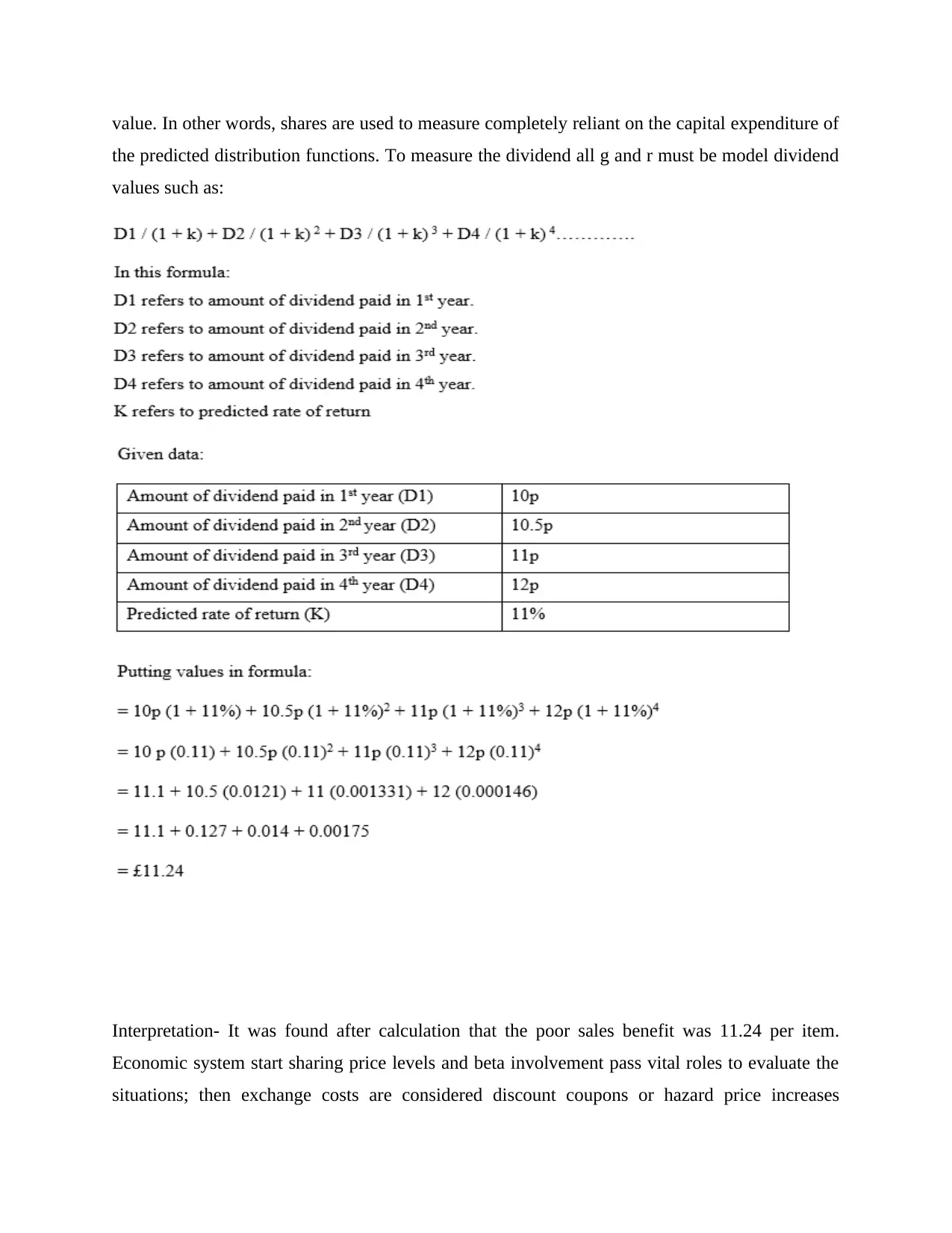

value. In other words, shares are used to measure completely reliant on the capital expenditure of

the predicted distribution functions. To measure the dividend all g and r must be model dividend

values such as:

Interpretation- It was found after calculation that the poor sales benefit was 11.24 per item.

Economic system start sharing price levels and beta involvement pass vital roles to evaluate the

situations; then exchange costs are considered discount coupons or hazard price increases

the predicted distribution functions. To measure the dividend all g and r must be model dividend

values such as:

Interpretation- It was found after calculation that the poor sales benefit was 11.24 per item.

Economic system start sharing price levels and beta involvement pass vital roles to evaluate the

situations; then exchange costs are considered discount coupons or hazard price increases

because rivalry threatens this additional motivation. Though free loading rates are likely to

hamper, owing to potential interest losses.

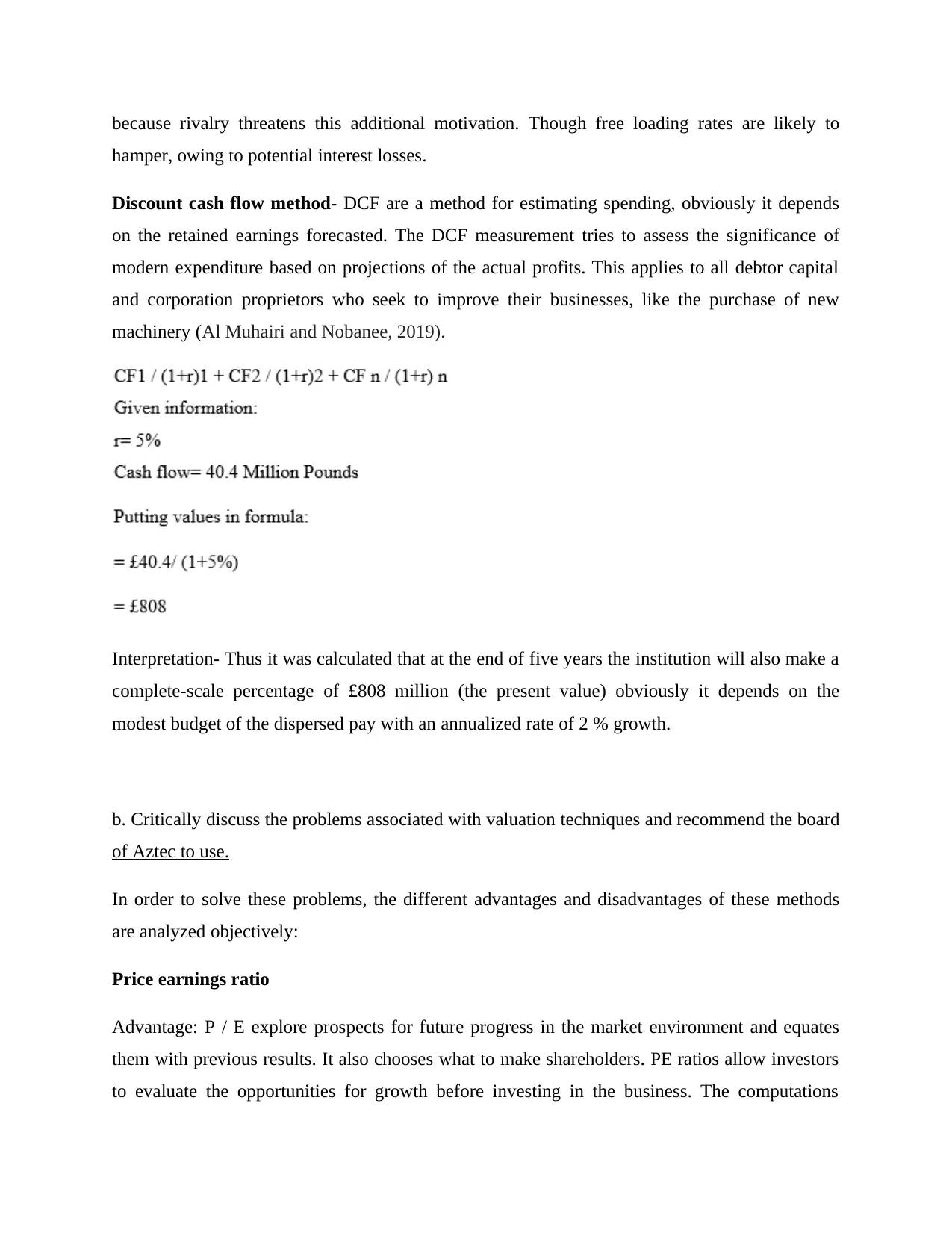

Discount cash flow method- DCF are a method for estimating spending, obviously it depends

on the retained earnings forecasted. The DCF measurement tries to assess the significance of

modern expenditure based on projections of the actual profits. This applies to all debtor capital

and corporation proprietors who seek to improve their businesses, like the purchase of new

machinery (Al Muhairi and Nobanee, 2019).

Interpretation- Thus it was calculated that at the end of five years the institution will also make a

complete-scale percentage of £808 million (the present value) obviously it depends on the

modest budget of the dispersed pay with an annualized rate of 2 % growth.

b. Critically discuss the problems associated with valuation techniques and recommend the board

of Aztec to use.

In order to solve these problems, the different advantages and disadvantages of these methods

are analyzed objectively:

Price earnings ratio

Advantage: P / E explore prospects for future progress in the market environment and equates

them with previous results. It also chooses what to make shareholders. PE ratios allow investors

to evaluate the opportunities for growth before investing in the business. The computations

hamper, owing to potential interest losses.

Discount cash flow method- DCF are a method for estimating spending, obviously it depends

on the retained earnings forecasted. The DCF measurement tries to assess the significance of

modern expenditure based on projections of the actual profits. This applies to all debtor capital

and corporation proprietors who seek to improve their businesses, like the purchase of new

machinery (Al Muhairi and Nobanee, 2019).

Interpretation- Thus it was calculated that at the end of five years the institution will also make a

complete-scale percentage of £808 million (the present value) obviously it depends on the

modest budget of the dispersed pay with an annualized rate of 2 % growth.

b. Critically discuss the problems associated with valuation techniques and recommend the board

of Aztec to use.

In order to solve these problems, the different advantages and disadvantages of these methods

are analyzed objectively:

Price earnings ratio

Advantage: P / E explore prospects for future progress in the market environment and equates

them with previous results. It also chooses what to make shareholders. PE ratios allow investors

to evaluate the opportunities for growth before investing in the business. The computations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

represent companies that can witness a spectacular cost increase. High PE tends to protect the

sector, while low PE is indicative of consistent country growth. Let the owners determine how

much they want to offer a share in exchange for every dollar. It can depend on this knowledge

for the identification of undervalued stocks (Alawattage and Azure, 2019).

Disadvantage: Value profits cannot take into consideration debt / financial arrangement when

calculating financial performance. Unique financial accounts prevent companies and separate

countries from having PE resemblances. Such actions include strategies to deplete, deplete and

tax. It's impossible to know what price earnings will produce to make P / E by sustainable

conduct logically subjective. Inventory growth or conservation may increase the company

income level, although it will result in higher costs for this. Companies that make losses are

unable to use the PE method as they cannot evaluate failures in the early stages of business

development.

DCF model

Advantage: DCF method has a significant benefit in that it restricts investment to a fixed

expense. If the present values gain is positive, the investment is called a source of earnings; it is a

failure if it is detrimental. This allows users to settle on investment accounts. Often, the approach

lets you pick between significantly different assets. Investments are the most exact and efficient

strategy. Presuming the metrics are perfectly appropriate, it's no other method to decide which

capital expenditure generates the highest benefit.

Disadvantage: DCF’s principal constraint is the need to generate a wide range of presumptions.

Cash flows may depend on multiple factors in the near future, such as economic trade, business

dynamics, unexpected issues and more. Calculating hypothetical potential cash flows can lead to

decisions requiring a spending that does not ruin income later on. Earning capital travels too low,

which may trigger a high-priced investment to lose out on chances? One should rely heavily on

the return date of the variant, so that the compensation for version may have to be estimated

correctly.

DVM:

sector, while low PE is indicative of consistent country growth. Let the owners determine how

much they want to offer a share in exchange for every dollar. It can depend on this knowledge

for the identification of undervalued stocks (Alawattage and Azure, 2019).

Disadvantage: Value profits cannot take into consideration debt / financial arrangement when

calculating financial performance. Unique financial accounts prevent companies and separate

countries from having PE resemblances. Such actions include strategies to deplete, deplete and

tax. It's impossible to know what price earnings will produce to make P / E by sustainable

conduct logically subjective. Inventory growth or conservation may increase the company

income level, although it will result in higher costs for this. Companies that make losses are

unable to use the PE method as they cannot evaluate failures in the early stages of business

development.

DCF model

Advantage: DCF method has a significant benefit in that it restricts investment to a fixed

expense. If the present values gain is positive, the investment is called a source of earnings; it is a

failure if it is detrimental. This allows users to settle on investment accounts. Often, the approach

lets you pick between significantly different assets. Investments are the most exact and efficient

strategy. Presuming the metrics are perfectly appropriate, it's no other method to decide which

capital expenditure generates the highest benefit.

Disadvantage: DCF’s principal constraint is the need to generate a wide range of presumptions.

Cash flows may depend on multiple factors in the near future, such as economic trade, business

dynamics, unexpected issues and more. Calculating hypothetical potential cash flows can lead to

decisions requiring a spending that does not ruin income later on. Earning capital travels too low,

which may trigger a high-priced investment to lose out on chances? One should rely heavily on

the return date of the variant, so that the compensation for version may have to be estimated

correctly.

DVM:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantage: This approach does not give model dividend assessment. The dividend yield must be

higher than the rate of return for the measured securities; else the measurement will not work.

This indicates that they use this method to approximate expected performance, predicated about

what looks like the exact payout. With this form of evaluation, it is easier to select a method of

investing because the investment will be sustained. At the very same time, it would be able to

earn money from distributions, enabling them to increase the asset’s total valuation, especially if

they have accumulated in a number of dividends shares (Al Ahbabi and Nobanee, 2019).

Disadvantage- DCF’s principal constraint is the need to generate a wide range of presumptions.

Cash flows may depend on multiple factors in the near future, such as economic trade, business

dynamics, unexpected issues and more. Calculating hypothetical potential cash flows can lead to

decisions requiring a spending that does not ruin income later on. Accruing capital travels too

low, which may trigger a high-priced investment to lose out on chances? One must rely heavily

on the date of return of the variant, so that the compensation for version may have to be

estimated correctly. Without a consistent and established dividend development, there's certain

non-dividend variables that affect cash flow. Thus the investment test does not reach the

intended effects even though use it.

Using the latter analysis, it is suggested that the business follow the P / E metric for valuing their

inventory. It allows manager to identify company choices to boost the enterprise 's efficiency or

competitive nature (Spuhlera and Dew, 2019).

Recommendation: The Board of Aztec plc should be urged to adapt the dividend valuation

formula for Trojan plc to the appraisal on the grounds of the three valuation techniques alluded

to above. The rationale behind this is that under DVM, a share appraisal is carried out that helps

company owners to revalue a particular company. While the remaining two methods, such as

price earnings ratio and discounted cash flow, have a variety of drawbacks, making the valuation

less effective. Although these two methods are primarily helpful, rather than share price analysis,

to assess earnings and stock price.

Question 3

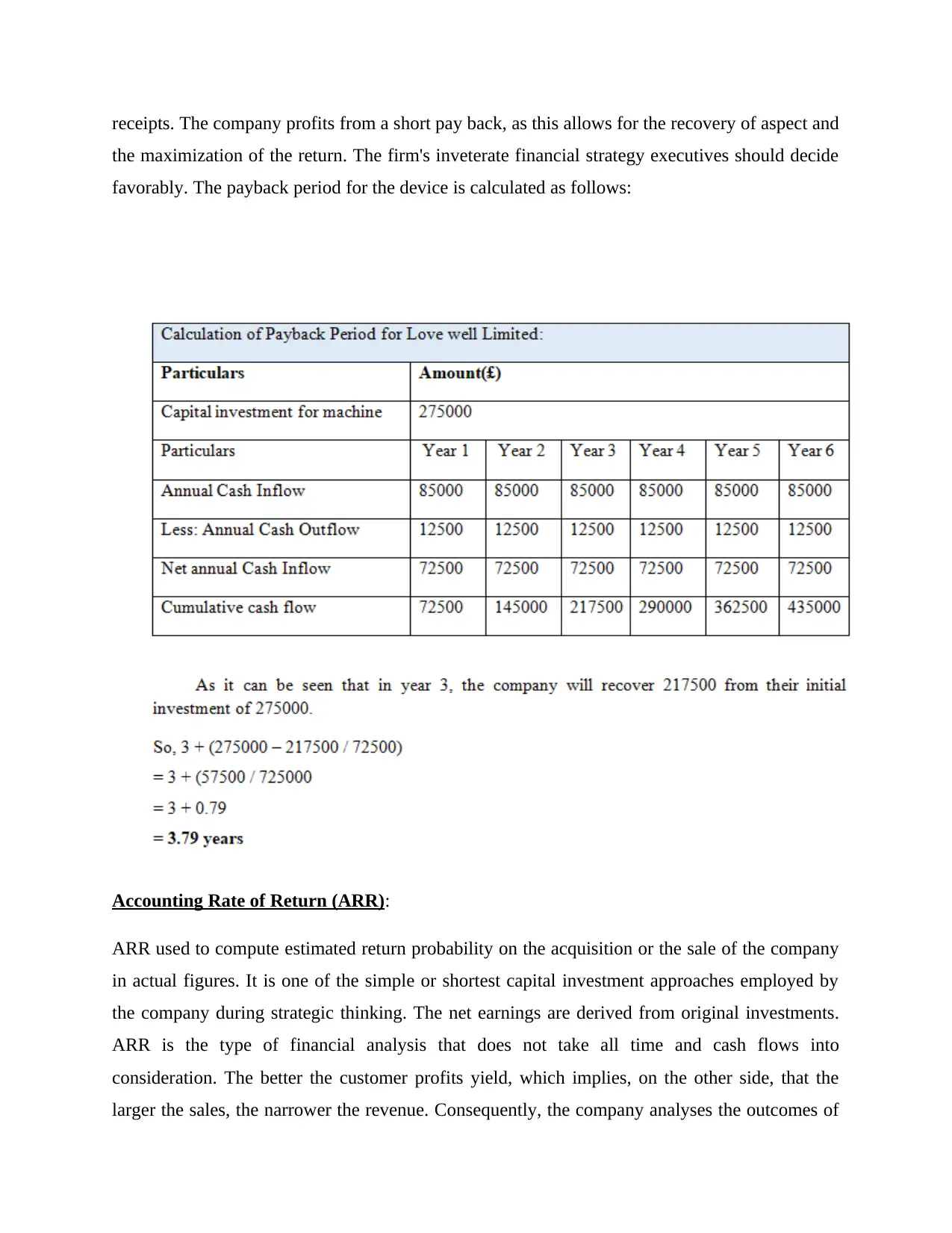

Payback period: It is the investment appraisal process, which determines extra costs and allows

the user to choose or select the correct solution. Payback time is the number of the customer's

higher than the rate of return for the measured securities; else the measurement will not work.

This indicates that they use this method to approximate expected performance, predicated about

what looks like the exact payout. With this form of evaluation, it is easier to select a method of

investing because the investment will be sustained. At the very same time, it would be able to

earn money from distributions, enabling them to increase the asset’s total valuation, especially if

they have accumulated in a number of dividends shares (Al Ahbabi and Nobanee, 2019).

Disadvantage- DCF’s principal constraint is the need to generate a wide range of presumptions.

Cash flows may depend on multiple factors in the near future, such as economic trade, business

dynamics, unexpected issues and more. Calculating hypothetical potential cash flows can lead to

decisions requiring a spending that does not ruin income later on. Accruing capital travels too

low, which may trigger a high-priced investment to lose out on chances? One must rely heavily

on the date of return of the variant, so that the compensation for version may have to be

estimated correctly. Without a consistent and established dividend development, there's certain

non-dividend variables that affect cash flow. Thus the investment test does not reach the

intended effects even though use it.

Using the latter analysis, it is suggested that the business follow the P / E metric for valuing their

inventory. It allows manager to identify company choices to boost the enterprise 's efficiency or

competitive nature (Spuhlera and Dew, 2019).

Recommendation: The Board of Aztec plc should be urged to adapt the dividend valuation

formula for Trojan plc to the appraisal on the grounds of the three valuation techniques alluded

to above. The rationale behind this is that under DVM, a share appraisal is carried out that helps

company owners to revalue a particular company. While the remaining two methods, such as

price earnings ratio and discounted cash flow, have a variety of drawbacks, making the valuation

less effective. Although these two methods are primarily helpful, rather than share price analysis,

to assess earnings and stock price.

Question 3

Payback period: It is the investment appraisal process, which determines extra costs and allows

the user to choose or select the correct solution. Payback time is the number of the customer's

receipts. The company profits from a short pay back, as this allows for the recovery of aspect and

the maximization of the return. The firm's inveterate financial strategy executives should decide

favorably. The payback period for the device is calculated as follows:

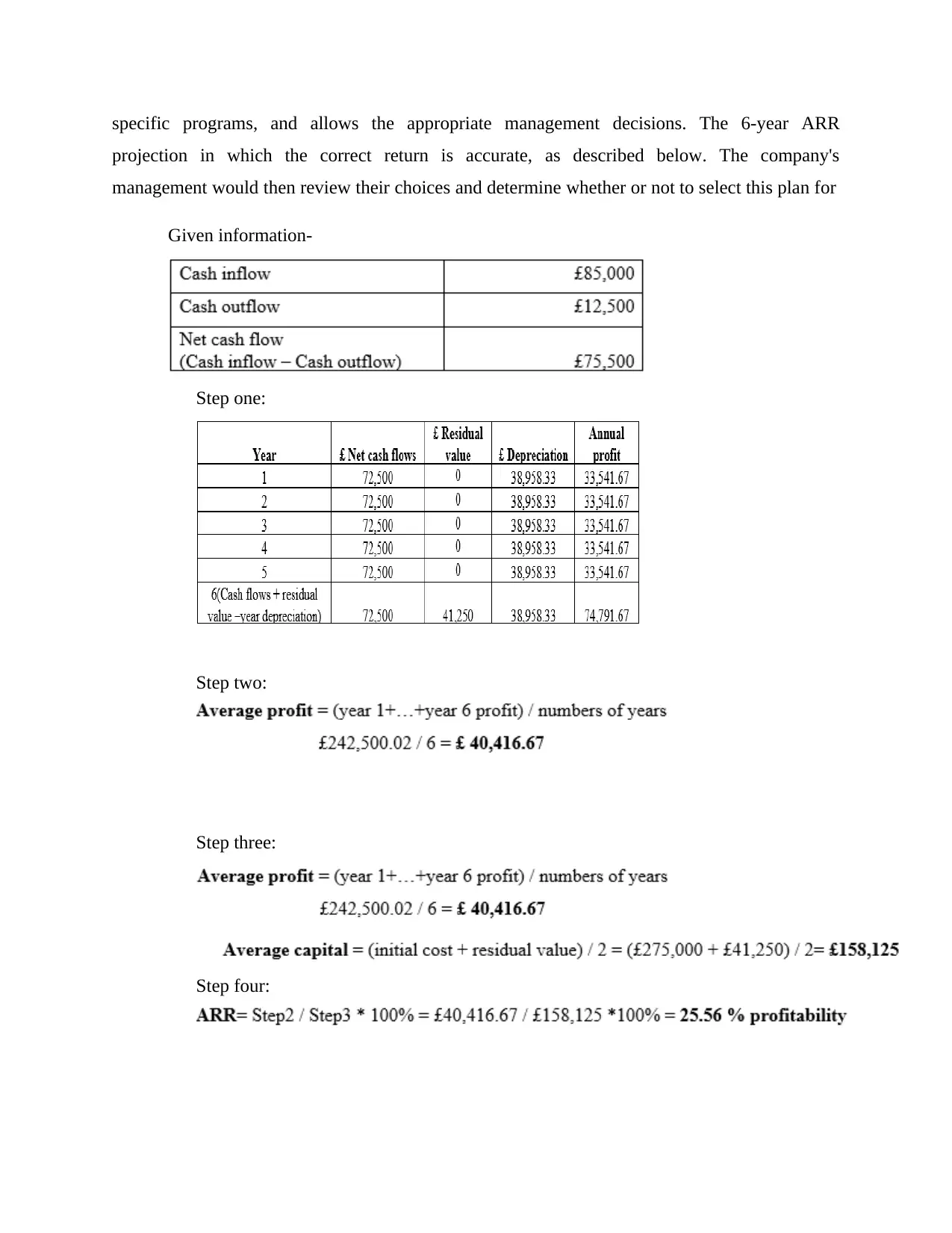

Accounting Rate of Return (ARR):

ARR used to compute estimated return probability on the acquisition or the sale of the company

in actual figures. It is one of the simple or shortest capital investment approaches employed by

the company during strategic thinking. The net earnings are derived from original investments.

ARR is the type of financial analysis that does not take all time and cash flows into

consideration. The better the customer profits yield, which implies, on the other side, that the

larger the sales, the narrower the revenue. Consequently, the company analyses the outcomes of

the maximization of the return. The firm's inveterate financial strategy executives should decide

favorably. The payback period for the device is calculated as follows:

Accounting Rate of Return (ARR):

ARR used to compute estimated return probability on the acquisition or the sale of the company

in actual figures. It is one of the simple or shortest capital investment approaches employed by

the company during strategic thinking. The net earnings are derived from original investments.

ARR is the type of financial analysis that does not take all time and cash flows into

consideration. The better the customer profits yield, which implies, on the other side, that the

larger the sales, the narrower the revenue. Consequently, the company analyses the outcomes of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

specific programs, and allows the appropriate management decisions. The 6-year ARR

projection in which the correct return is accurate, as described below. The company's

management would then review their choices and determine whether or not to select this plan for

Given information-

Step one:

Step two:

Step three:

Step four:

projection in which the correct return is accurate, as described below. The company's

management would then review their choices and determine whether or not to select this plan for

Given information-

Step one:

Step two:

Step three:

Step four:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

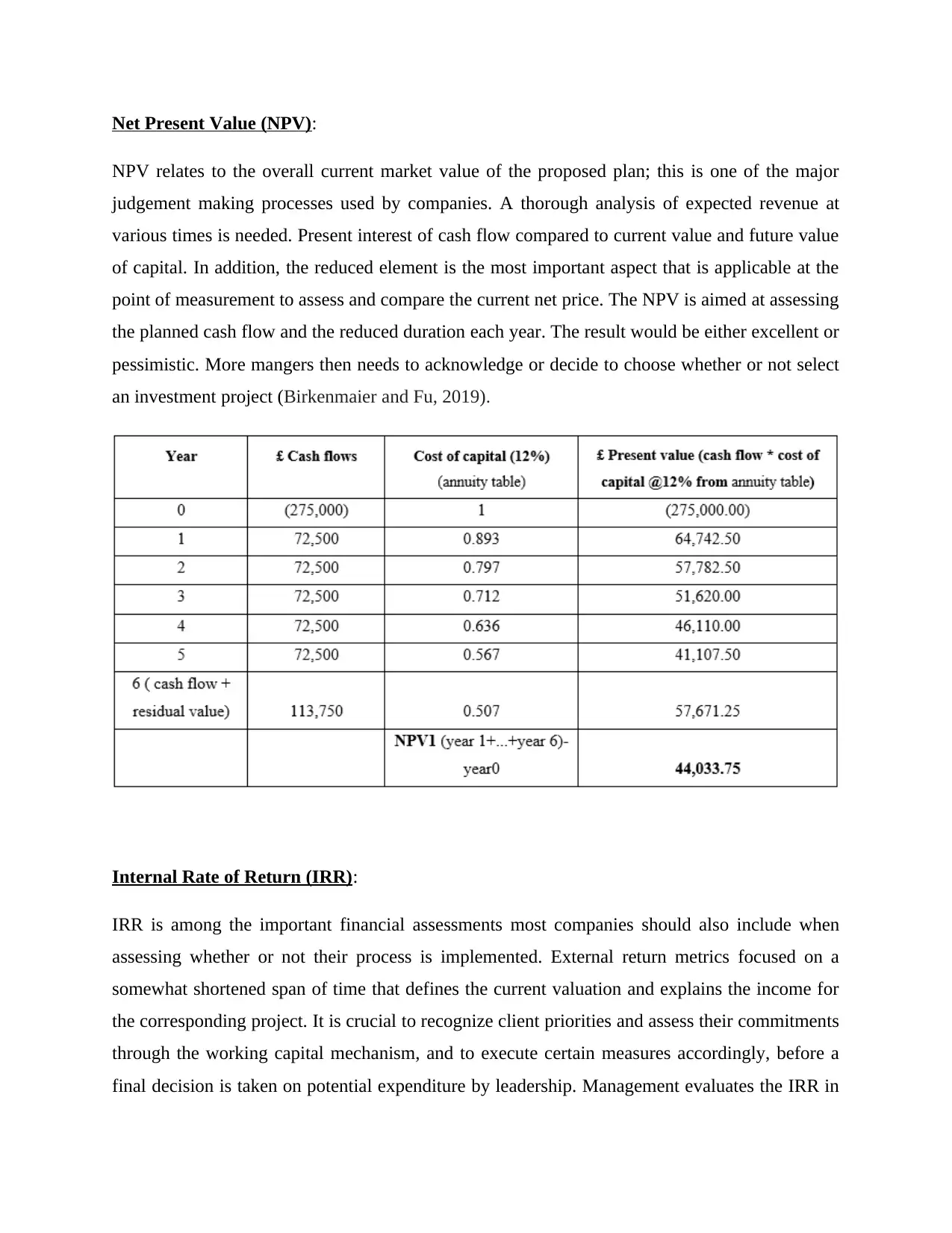

Net Present Value (NPV):

NPV relates to the overall current market value of the proposed plan; this is one of the major

judgement making processes used by companies. A thorough analysis of expected revenue at

various times is needed. Present interest of cash flow compared to current value and future value

of capital. In addition, the reduced element is the most important aspect that is applicable at the

point of measurement to assess and compare the current net price. The NPV is aimed at assessing

the planned cash flow and the reduced duration each year. The result would be either excellent or

pessimistic. More mangers then needs to acknowledge or decide to choose whether or not select

an investment project (Birkenmaier and Fu, 2019).

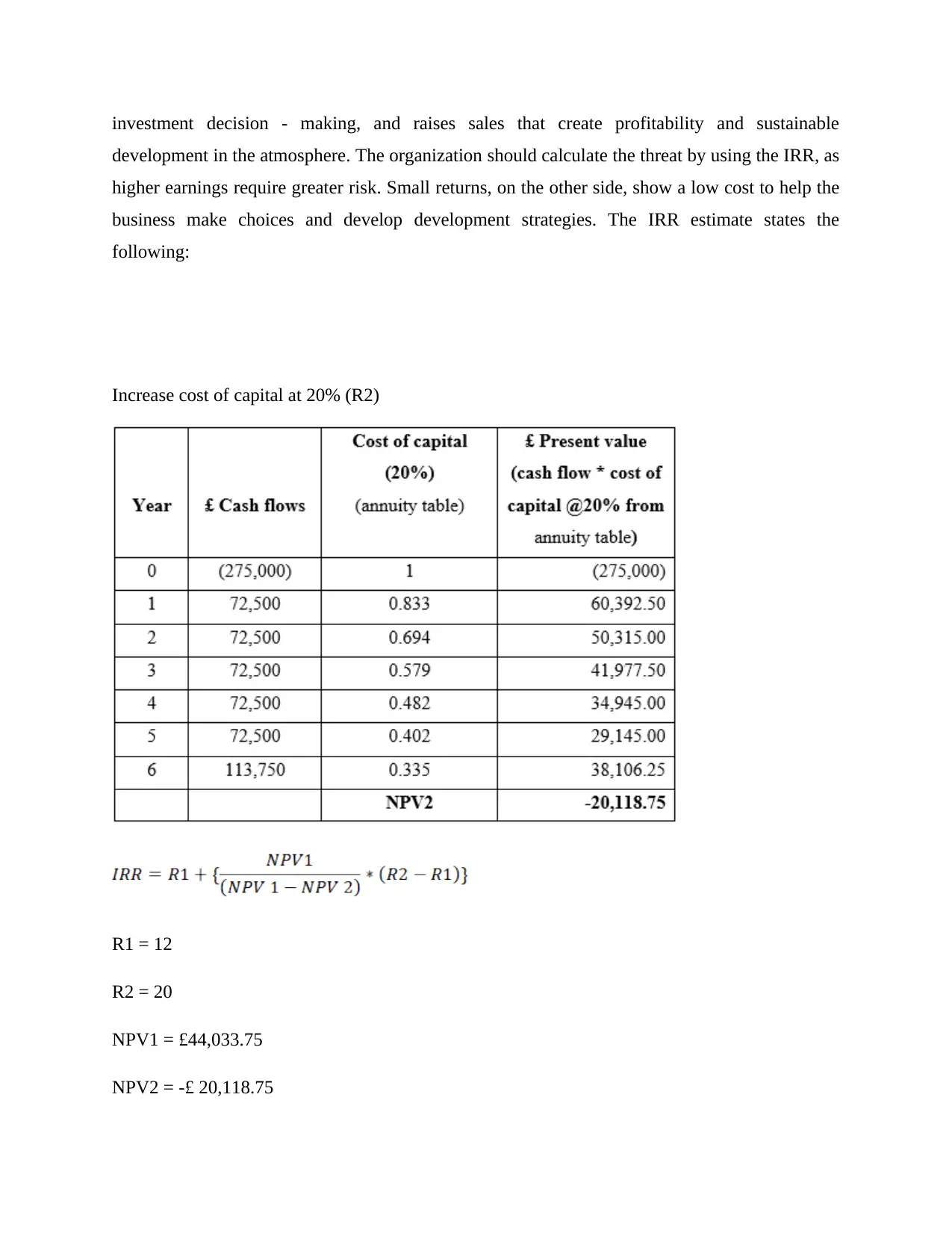

Internal Rate of Return (IRR):

IRR is among the important financial assessments most companies should also include when

assessing whether or not their process is implemented. External return metrics focused on a

somewhat shortened span of time that defines the current valuation and explains the income for

the corresponding project. It is crucial to recognize client priorities and assess their commitments

through the working capital mechanism, and to execute certain measures accordingly, before a

final decision is taken on potential expenditure by leadership. Management evaluates the IRR in

NPV relates to the overall current market value of the proposed plan; this is one of the major

judgement making processes used by companies. A thorough analysis of expected revenue at

various times is needed. Present interest of cash flow compared to current value and future value

of capital. In addition, the reduced element is the most important aspect that is applicable at the

point of measurement to assess and compare the current net price. The NPV is aimed at assessing

the planned cash flow and the reduced duration each year. The result would be either excellent or

pessimistic. More mangers then needs to acknowledge or decide to choose whether or not select

an investment project (Birkenmaier and Fu, 2019).

Internal Rate of Return (IRR):

IRR is among the important financial assessments most companies should also include when

assessing whether or not their process is implemented. External return metrics focused on a

somewhat shortened span of time that defines the current valuation and explains the income for

the corresponding project. It is crucial to recognize client priorities and assess their commitments

through the working capital mechanism, and to execute certain measures accordingly, before a

final decision is taken on potential expenditure by leadership. Management evaluates the IRR in

investment decision - making, and raises sales that create profitability and sustainable

development in the atmosphere. The organization should calculate the threat by using the IRR, as

higher earnings require greater risk. Small returns, on the other side, show a low cost to help the

business make choices and develop development strategies. The IRR estimate states the

following:

Increase cost of capital at 20% (R2)

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

development in the atmosphere. The organization should calculate the threat by using the IRR, as

higher earnings require greater risk. Small returns, on the other side, show a low cost to help the

business make choices and develop development strategies. The IRR estimate states the

following:

Increase cost of capital at 20% (R2)

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.