Financial Accounting Project: Sole Trader and Private Limited Company

VerifiedAdded on 2023/02/03

|16

|1557

|28

Project

AI Summary

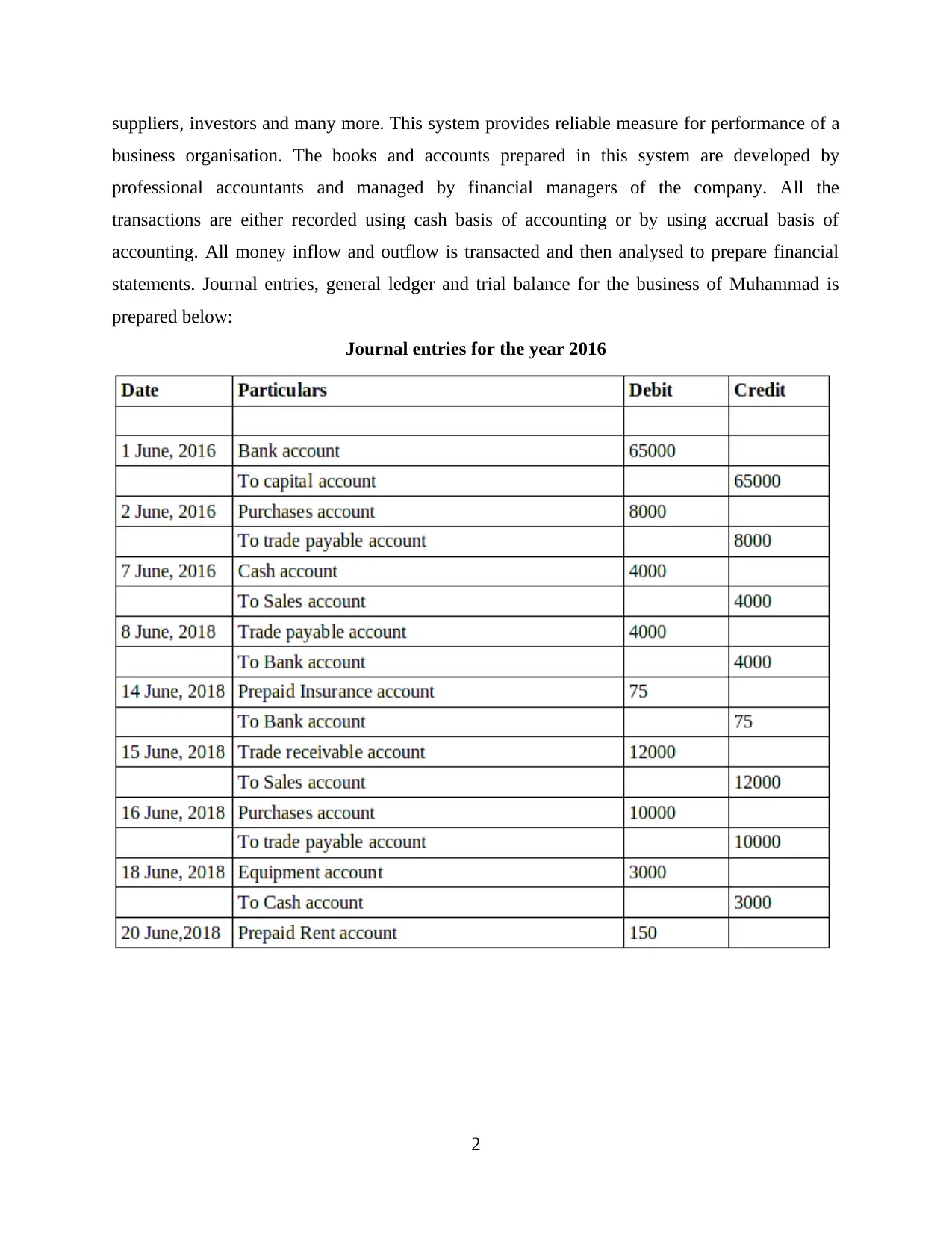

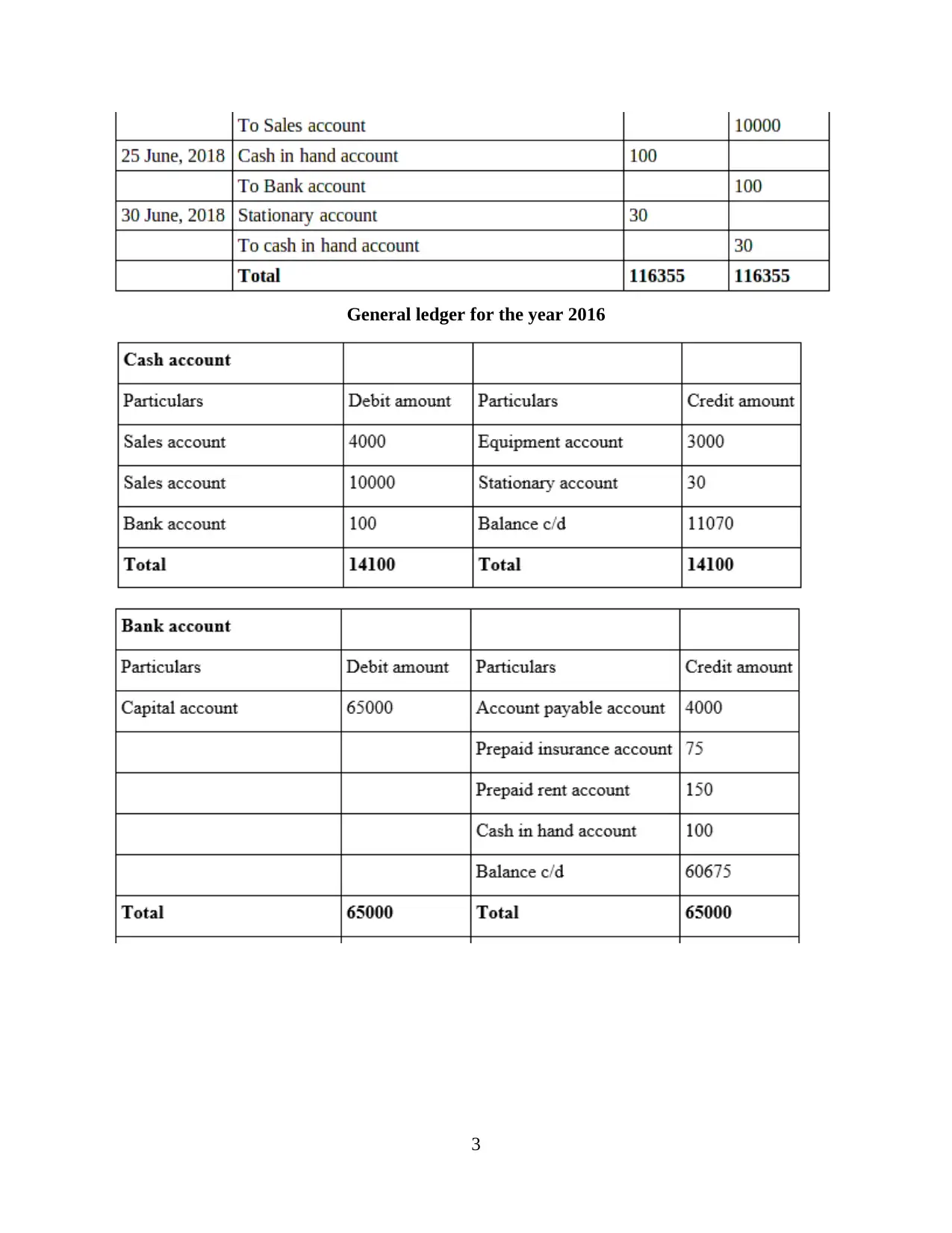

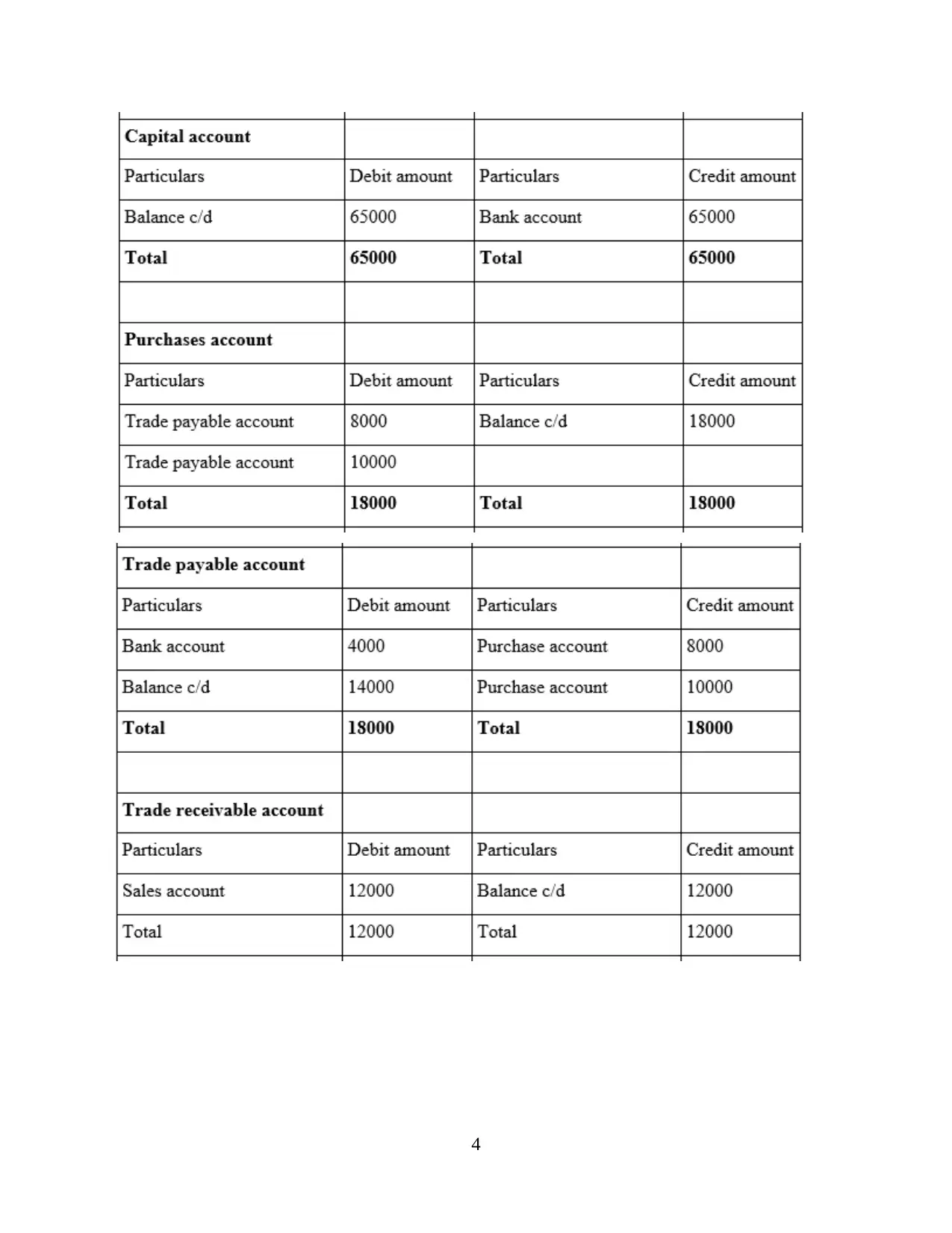

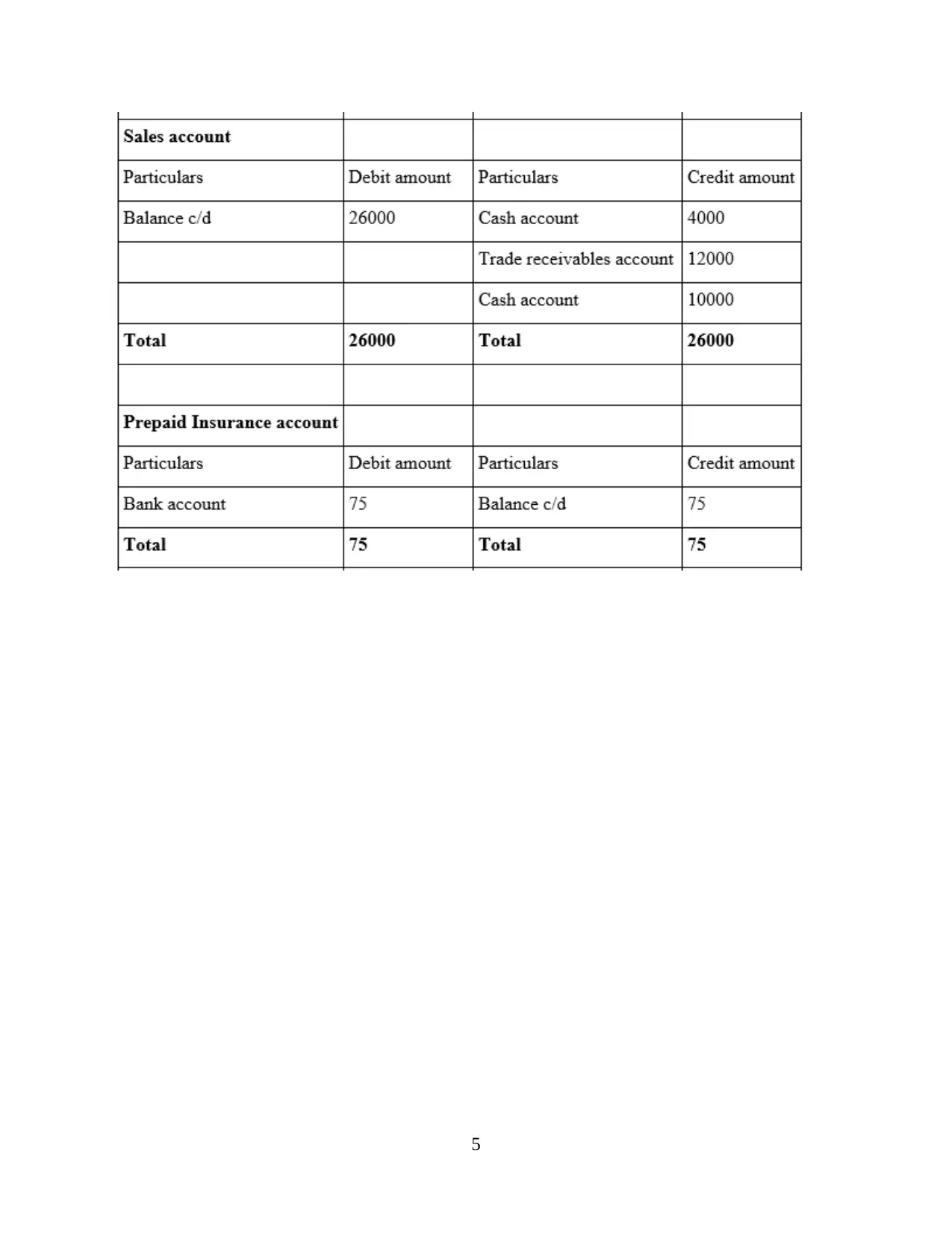

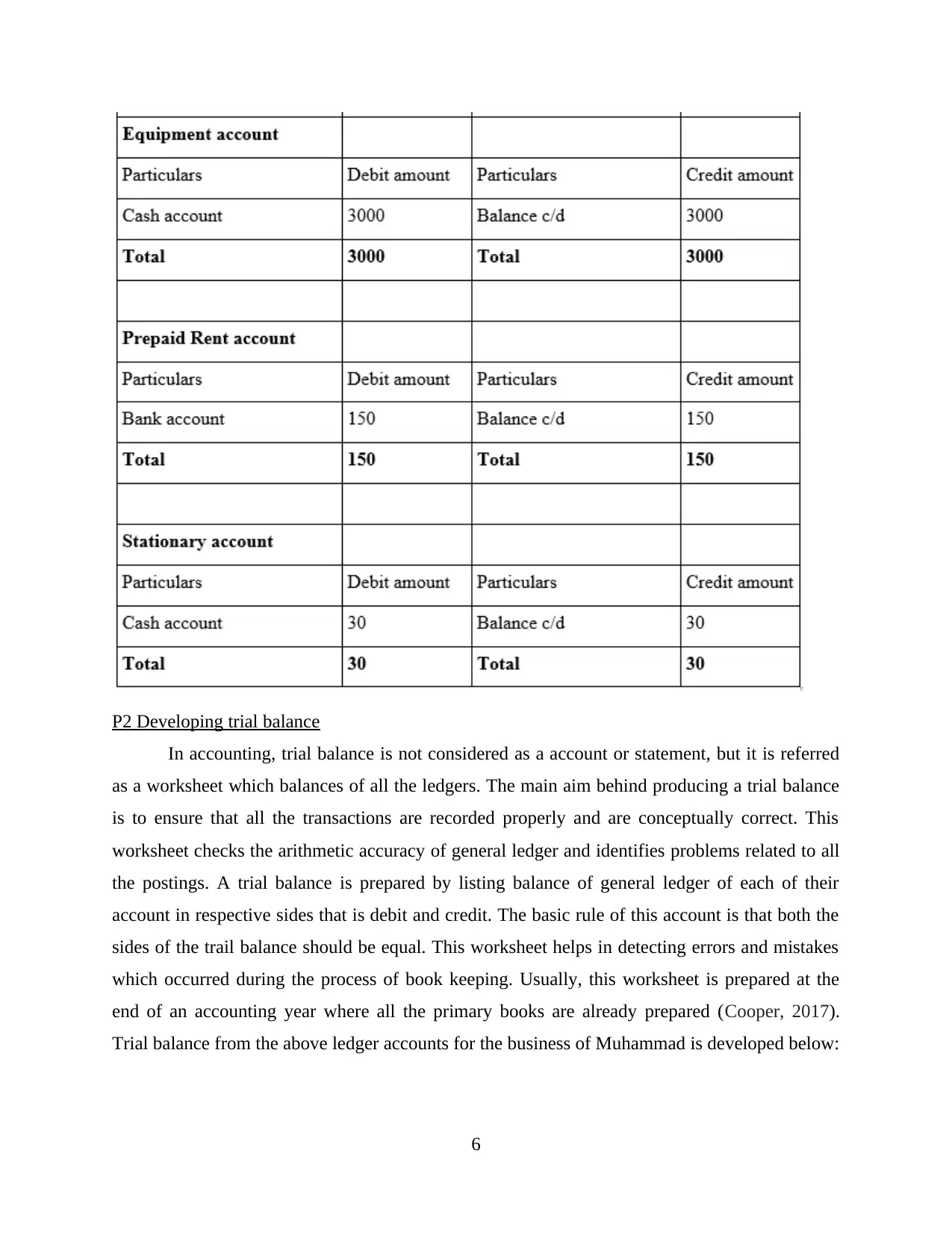

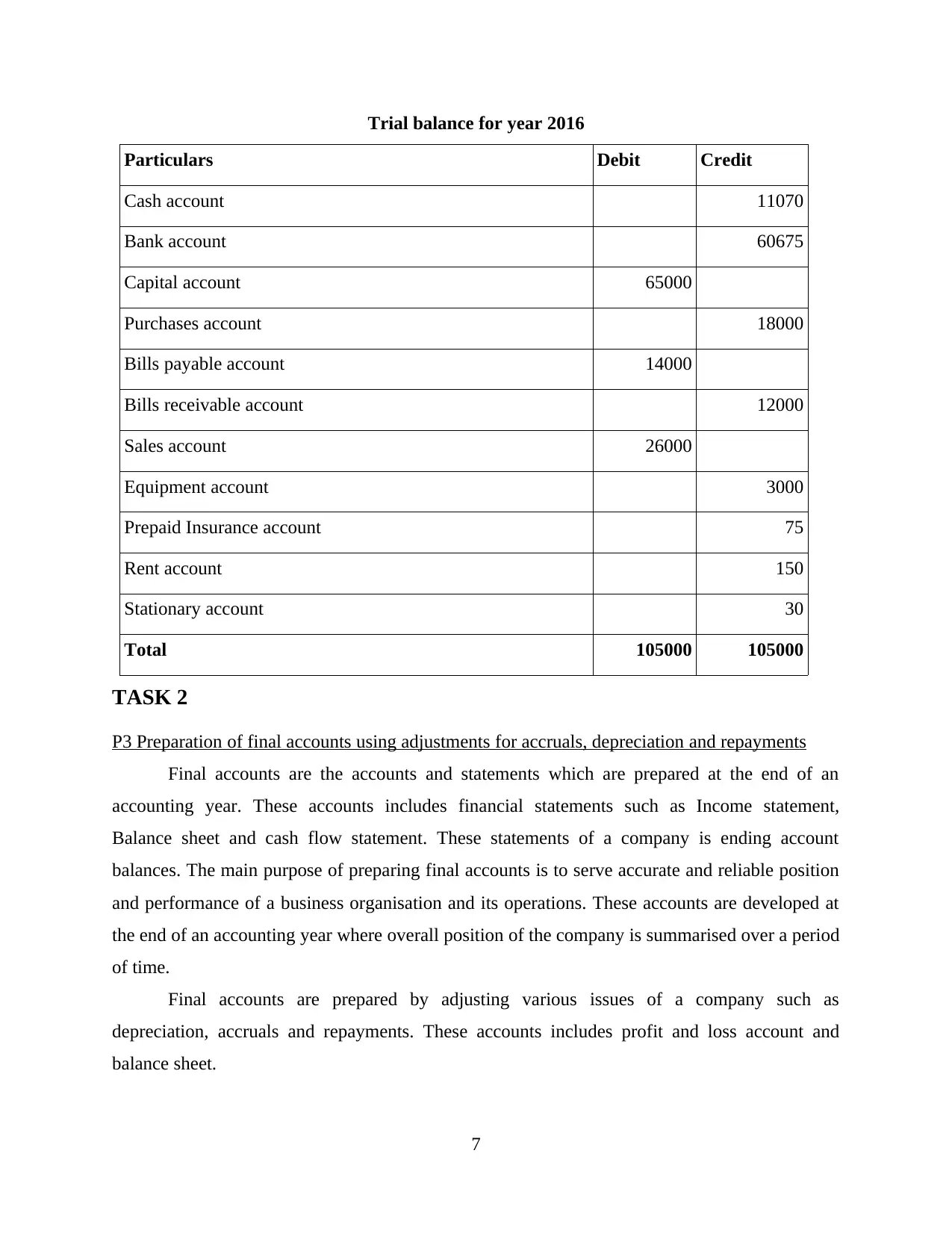

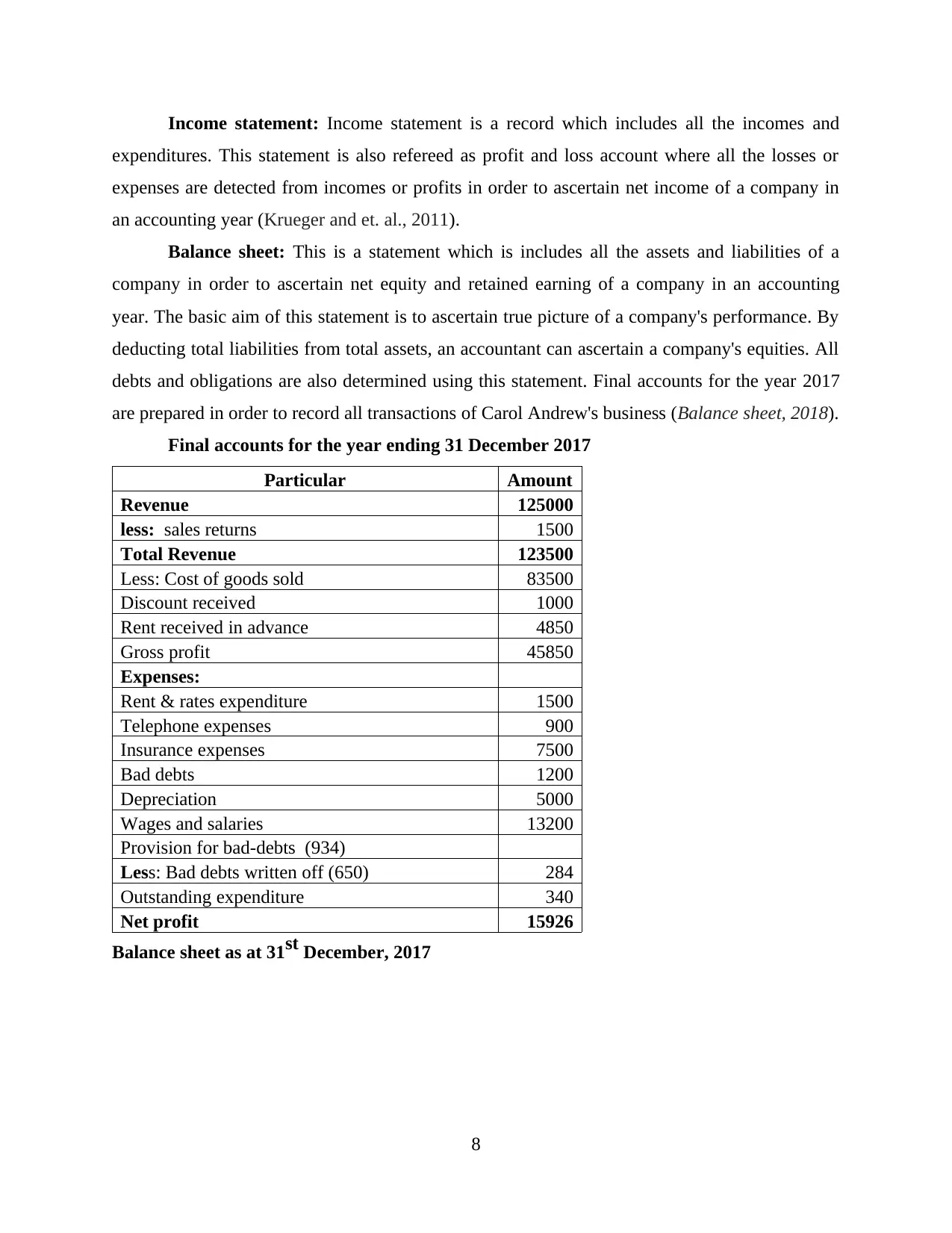

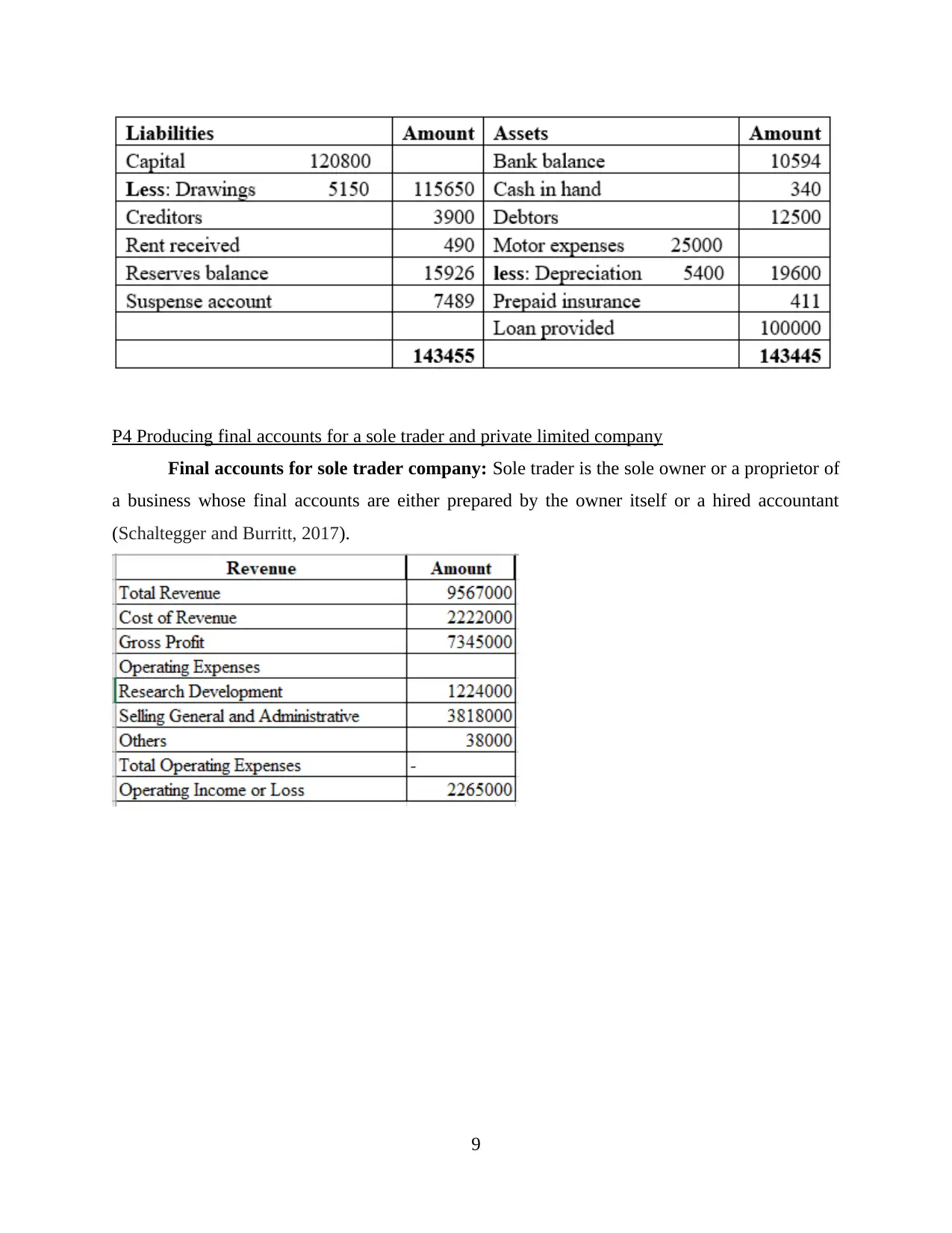

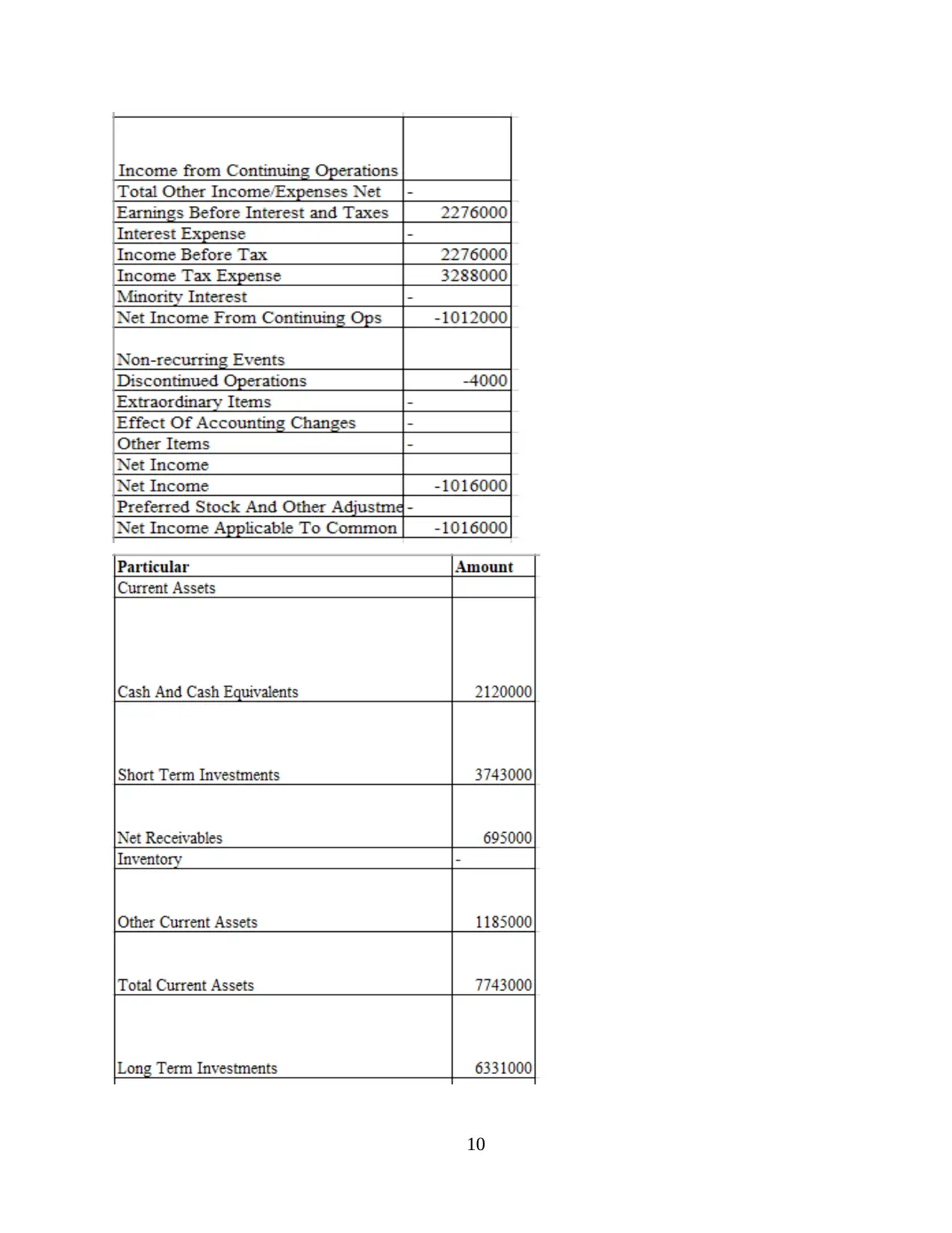

This project report provides a comprehensive overview of financial accounting principles and practices. It begins with an introduction to financial accounting and its significance in reflecting the financial position of a business. The project is divided into two main tasks. Task 1 focuses on the double-entry bookkeeping system, including the preparation of journal entries and a general ledger, followed by the development of a trial balance. Task 2 delves into the preparation of final accounts, including adjustments for accruals, depreciation, and repayments, and culminates in producing final accounts for both a sole trader and a private limited company. The report includes examples, journal entries, and financial statements, illustrating the practical application of accounting concepts. The conclusion summarizes the key learnings and emphasizes the importance of accurate financial statement preparation and analysis. References to relevant literature and online resources are also included.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.