Comprehensive Report: Recording and Analyzing Business Transactions

VerifiedAdded on 2022/12/28

|11

|1942

|43

Report

AI Summary

This report provides a comprehensive overview of financial accounting, beginning with an explanation of the decision-makers who utilize accounting information and the advantages and disadvantages of accounting practices. It then delves into practical application by preparing journal entries for David Wise in February 2020, followed by the creation of general ledgers and a trial balance for S. Keyes. The report continues with the preparation of an income statement for the year ending September 30, 2019, and concludes with an analysis of the impact of COVID-19 on a company's income statement, utilizing a PESTLE analysis to examine the various factors affecting business operations, including political, economic, social, technological, legal, and environmental considerations. The report also includes a list of references for further study.

Recording Business

Transactions

Transactions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1............................................................................................................................................3

(a) Decision makers of the accounting Information....................................................................3

(b) Advantages and Disadvantages of accounting.......................................................................4

PART 2............................................................................................................................................4

Preparing journal entries in the books of David Wise which occur in Feb 2020:.......................4

PART 3............................................................................................................................................6

a. Presenting general ledger of S. Keyes.....................................................................................6

Fixtures a/c.......................................................................................................................................7

b. Trial balance............................................................................................................................8

PART 4............................................................................................................................................8

a) Income statement for the year ending 30th September, 2019...................................................8

b) Impact of Covid-19 on company income statement................................................................9

REFERENCES................................................................................................................................1

PART 1............................................................................................................................................3

(a) Decision makers of the accounting Information....................................................................3

(b) Advantages and Disadvantages of accounting.......................................................................4

PART 2............................................................................................................................................4

Preparing journal entries in the books of David Wise which occur in Feb 2020:.......................4

PART 3............................................................................................................................................6

a. Presenting general ledger of S. Keyes.....................................................................................6

Fixtures a/c.......................................................................................................................................7

b. Trial balance............................................................................................................................8

PART 4............................................................................................................................................8

a) Income statement for the year ending 30th September, 2019...................................................8

b) Impact of Covid-19 on company income statement................................................................9

REFERENCES................................................................................................................................1

PART 1

(a) Decision makers of the accounting Information

Accounting is the process of recording financial transaction related to a business which

includes Summarising, analysing, and reporting those transactions in the books of accounts.

Financial accounts provide a wealth of information to its users, there are internal and external

users of financial accounting.

Internal users are the person who are inside in the organization

Management: These are real owner of the company who are using financial information

for decision making about their investments (B Romney 2018). In small businesses

sometimes there are management may include owners. Management of the company is

the first and foremost user of the financial statements, they are the ones who prepared the

financial statements. Employees: They have interest in the company's stability and profitability because they

want to know about their pay salaries and other employee’s benefits. They use financial

information for assess the performance of firm for their future career development.

External Users are the person who are outside the organisation.

Customers: They need to view financial statements of the company from which they are

purchasing goods and services. Customers always uses the product by seeing products

long term availability so sometimes they use financial statements.

Competitors: They would like to know about the financial status of the company for

maintain a competitive edge on their competitive firms (Chiu, Liu, Muehlmann and

Baldwin, A. 2019). They want to analyse the financial health of the other company so

uses this statements.

Government: Government agencies like income tax departments, sales departments

would like to know about the earning profits of the company for keep a check on that the

company is paying taxes on time or not.

Investors: These are the person who have interest in the company and they invest the

money in the business by analysing company’s financial performance and position.

(a) Decision makers of the accounting Information

Accounting is the process of recording financial transaction related to a business which

includes Summarising, analysing, and reporting those transactions in the books of accounts.

Financial accounts provide a wealth of information to its users, there are internal and external

users of financial accounting.

Internal users are the person who are inside in the organization

Management: These are real owner of the company who are using financial information

for decision making about their investments (B Romney 2018). In small businesses

sometimes there are management may include owners. Management of the company is

the first and foremost user of the financial statements, they are the ones who prepared the

financial statements. Employees: They have interest in the company's stability and profitability because they

want to know about their pay salaries and other employee’s benefits. They use financial

information for assess the performance of firm for their future career development.

External Users are the person who are outside the organisation.

Customers: They need to view financial statements of the company from which they are

purchasing goods and services. Customers always uses the product by seeing products

long term availability so sometimes they use financial statements.

Competitors: They would like to know about the financial status of the company for

maintain a competitive edge on their competitive firms (Chiu, Liu, Muehlmann and

Baldwin, A. 2019). They want to analyse the financial health of the other company so

uses this statements.

Government: Government agencies like income tax departments, sales departments

would like to know about the earning profits of the company for keep a check on that the

company is paying taxes on time or not.

Investors: These are the person who have interest in the company and they invest the

money in the business by analysing company’s financial performance and position.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b) Advantages and Disadvantages of accounting

Advantages of accounting

Helps in Decision making: Accounting helps in taking decision about financial position

and performance of a business. accounting information enables management to plan its future

activities, and helps in making budget.

Preparation of financial statements: Financial statements includes income statements,

balance sheets, cash flow statements are prepared easily if the proper recording of transaction is

done. these statements show true and correct financial position of a company.

Maintenance of business records: if recording of every transaction is done in journals

then it will show as records. f proper recording is done then financial statements also serve as an

evidence in court.

Disadvantages of accounting

Considered monetary Transactions: Financial accounting only considered monetary

transaction if any transaction who does not measurable in monetary terms then its impact is zero

in accounting.

Manipulation of accounts is possible: the accountant and mangers can manipulate or

misinterpret accounting profit which results in increase in frauds and scams in business

organisations.

Fixed Assets recorded at original cost only: There can be a difference between the

market value or book value of assets. Accounting only considered original cost of the asset not

market value so it sometimes balance sheet does not show true financial position.

PART 2

Preparing journal entries in the books of David Wise which occur in Feb 2020:

DATE PARTICULARS DEBIT £

CREDIT

£

01/02/2020 Asma Limited account dr. 350

To Office Fixtures account 350

Advantages of accounting

Helps in Decision making: Accounting helps in taking decision about financial position

and performance of a business. accounting information enables management to plan its future

activities, and helps in making budget.

Preparation of financial statements: Financial statements includes income statements,

balance sheets, cash flow statements are prepared easily if the proper recording of transaction is

done. these statements show true and correct financial position of a company.

Maintenance of business records: if recording of every transaction is done in journals

then it will show as records. f proper recording is done then financial statements also serve as an

evidence in court.

Disadvantages of accounting

Considered monetary Transactions: Financial accounting only considered monetary

transaction if any transaction who does not measurable in monetary terms then its impact is zero

in accounting.

Manipulation of accounts is possible: the accountant and mangers can manipulate or

misinterpret accounting profit which results in increase in frauds and scams in business

organisations.

Fixed Assets recorded at original cost only: There can be a difference between the

market value or book value of assets. Accounting only considered original cost of the asset not

market value so it sometimes balance sheet does not show true financial position.

PART 2

Preparing journal entries in the books of David Wise which occur in Feb 2020:

DATE PARTICULARS DEBIT £

CREDIT

£

01/02/2020 Asma Limited account dr. 350

To Office Fixtures account 350

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

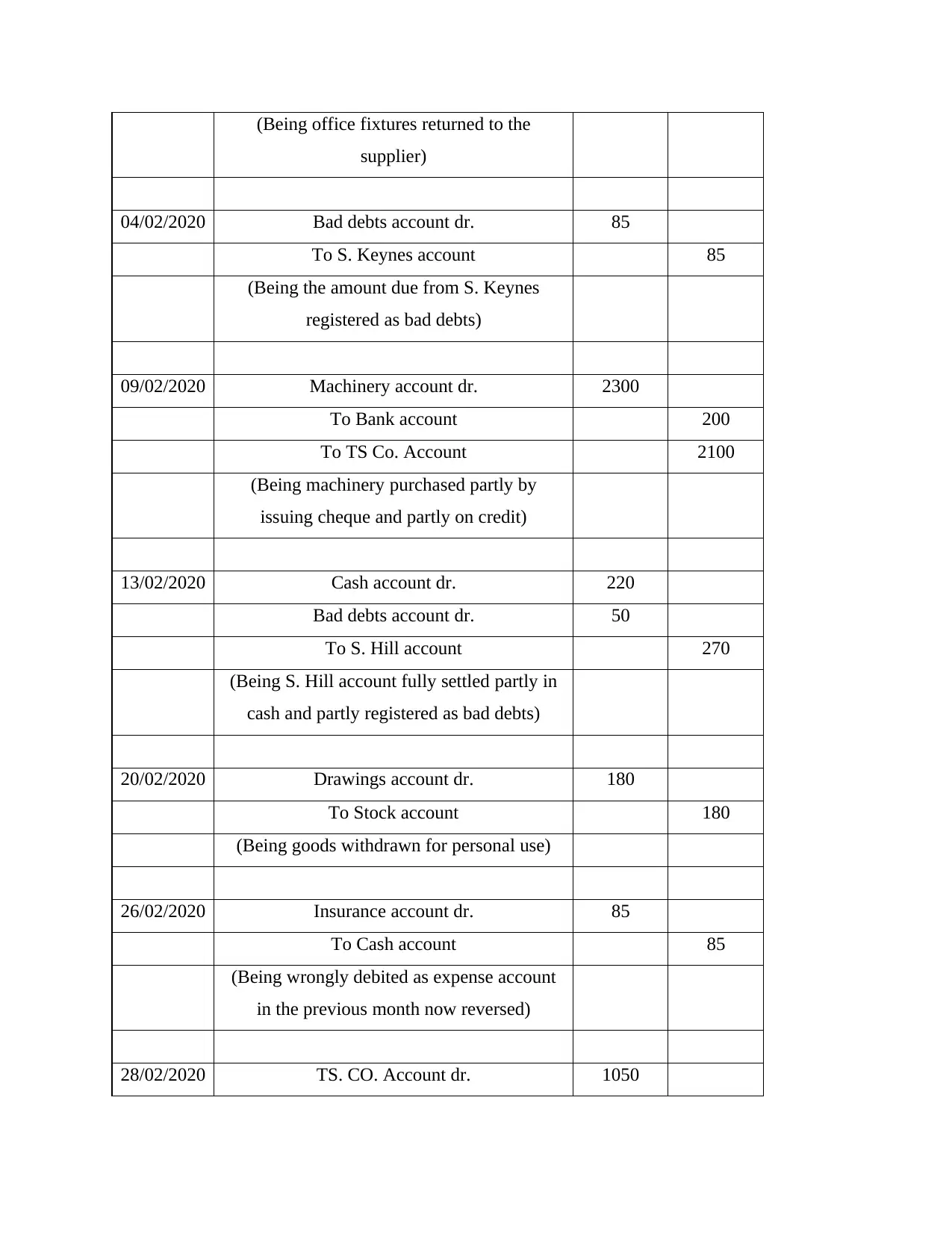

(Being office fixtures returned to the

supplier)

04/02/2020 Bad debts account dr. 85

To S. Keynes account 85

(Being the amount due from S. Keynes

registered as bad debts)

09/02/2020 Machinery account dr. 2300

To Bank account 200

To TS Co. Account 2100

(Being machinery purchased partly by

issuing cheque and partly on credit)

13/02/2020 Cash account dr. 220

Bad debts account dr. 50

To S. Hill account 270

(Being S. Hill account fully settled partly in

cash and partly registered as bad debts)

20/02/2020 Drawings account dr. 180

To Stock account 180

(Being goods withdrawn for personal use)

26/02/2020 Insurance account dr. 85

To Cash account 85

(Being wrongly debited as expense account

in the previous month now reversed)

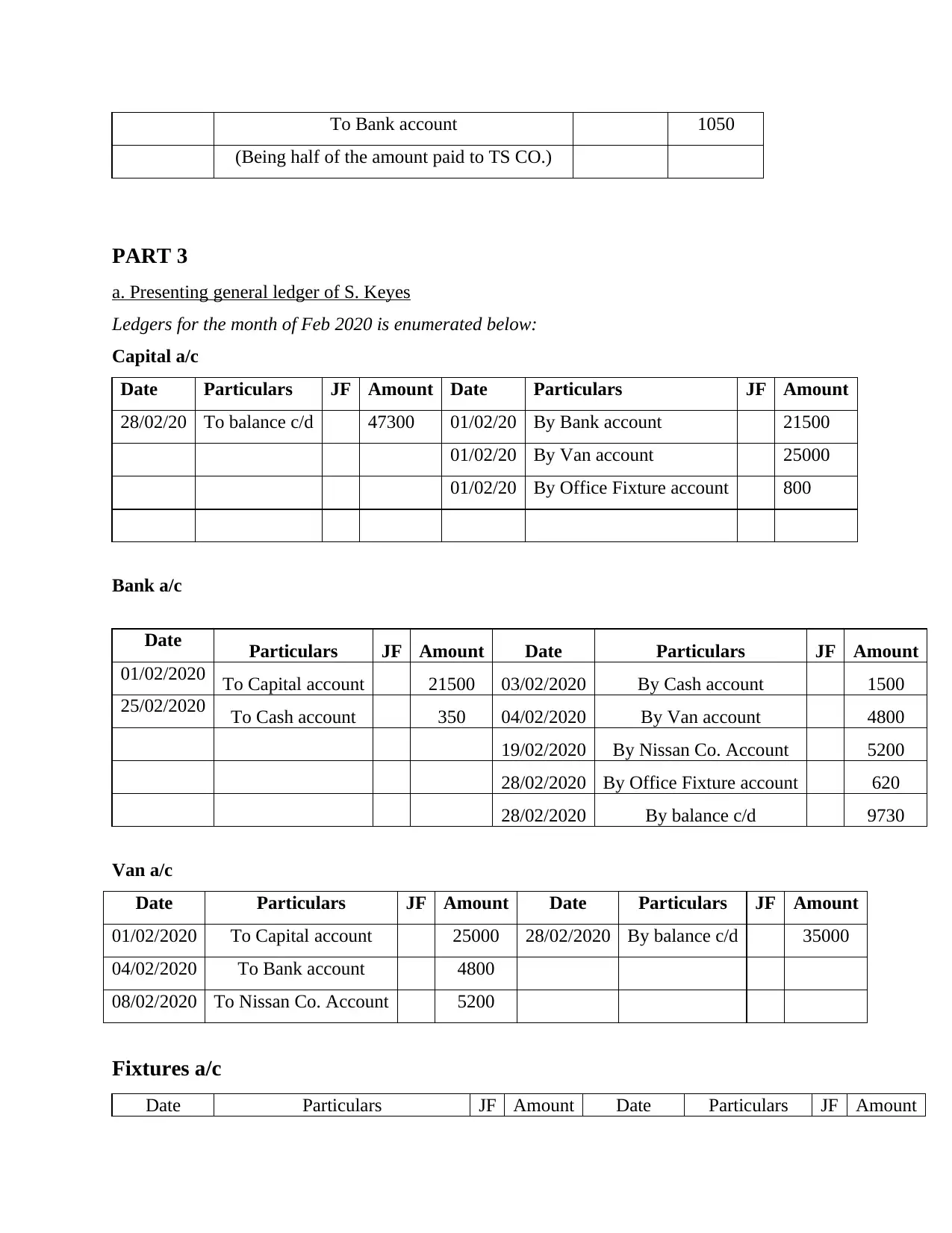

28/02/2020 TS. CO. Account dr. 1050

supplier)

04/02/2020 Bad debts account dr. 85

To S. Keynes account 85

(Being the amount due from S. Keynes

registered as bad debts)

09/02/2020 Machinery account dr. 2300

To Bank account 200

To TS Co. Account 2100

(Being machinery purchased partly by

issuing cheque and partly on credit)

13/02/2020 Cash account dr. 220

Bad debts account dr. 50

To S. Hill account 270

(Being S. Hill account fully settled partly in

cash and partly registered as bad debts)

20/02/2020 Drawings account dr. 180

To Stock account 180

(Being goods withdrawn for personal use)

26/02/2020 Insurance account dr. 85

To Cash account 85

(Being wrongly debited as expense account

in the previous month now reversed)

28/02/2020 TS. CO. Account dr. 1050

To Bank account 1050

(Being half of the amount paid to TS CO.)

PART 3

a. Presenting general ledger of S. Keyes

Ledgers for the month of Feb 2020 is enumerated below:

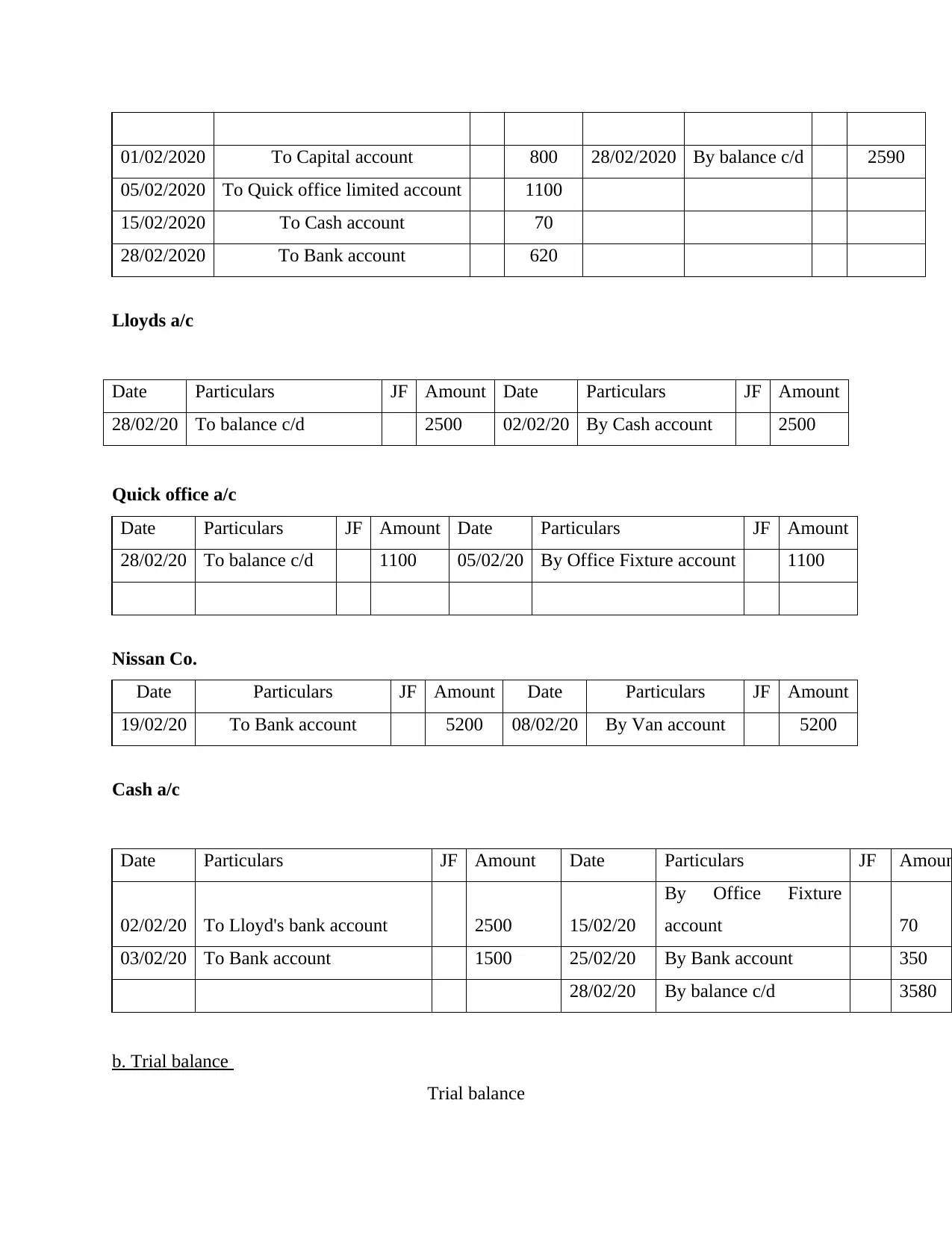

Capital a/c

Date Particulars JF Amount Date Particulars JF Amount

28/02/20 To balance c/d 47300 01/02/20 By Bank account 21500

01/02/20 By Van account 25000

01/02/20 By Office Fixture account 800

Bank a/c

Date Particulars JF Amount Date Particulars JF Amount

01/02/2020 To Capital account 21500 03/02/2020 By Cash account 1500

25/02/2020 To Cash account 350 04/02/2020 By Van account 4800

19/02/2020 By Nissan Co. Account 5200

28/02/2020 By Office Fixture account 620

28/02/2020 By balance c/d 9730

Van a/c

Date Particulars JF Amount Date Particulars JF Amount

01/02/2020 To Capital account 25000 28/02/2020 By balance c/d 35000

04/02/2020 To Bank account 4800

08/02/2020 To Nissan Co. Account 5200

Fixtures a/c

Date Particulars JF Amount Date Particulars JF Amount

(Being half of the amount paid to TS CO.)

PART 3

a. Presenting general ledger of S. Keyes

Ledgers for the month of Feb 2020 is enumerated below:

Capital a/c

Date Particulars JF Amount Date Particulars JF Amount

28/02/20 To balance c/d 47300 01/02/20 By Bank account 21500

01/02/20 By Van account 25000

01/02/20 By Office Fixture account 800

Bank a/c

Date Particulars JF Amount Date Particulars JF Amount

01/02/2020 To Capital account 21500 03/02/2020 By Cash account 1500

25/02/2020 To Cash account 350 04/02/2020 By Van account 4800

19/02/2020 By Nissan Co. Account 5200

28/02/2020 By Office Fixture account 620

28/02/2020 By balance c/d 9730

Van a/c

Date Particulars JF Amount Date Particulars JF Amount

01/02/2020 To Capital account 25000 28/02/2020 By balance c/d 35000

04/02/2020 To Bank account 4800

08/02/2020 To Nissan Co. Account 5200

Fixtures a/c

Date Particulars JF Amount Date Particulars JF Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

01/02/2020 To Capital account 800 28/02/2020 By balance c/d 2590

05/02/2020 To Quick office limited account 1100

15/02/2020 To Cash account 70

28/02/2020 To Bank account 620

Lloyds a/c

Date Particulars JF Amount Date Particulars JF Amount

28/02/20 To balance c/d 2500 02/02/20 By Cash account 2500

Quick office a/c

Date Particulars JF Amount Date Particulars JF Amount

28/02/20 To balance c/d 1100 05/02/20 By Office Fixture account 1100

Nissan Co.

Date Particulars JF Amount Date Particulars JF Amount

19/02/20 To Bank account 5200 08/02/20 By Van account 5200

Cash a/c

Date Particulars JF Amount Date Particulars JF Amoun

02/02/20 To Lloyd's bank account 2500 15/02/20

By Office Fixture

account 70

03/02/20 To Bank account 1500 25/02/20 By Bank account 350

28/02/20 By balance c/d 3580

b. Trial balance

Trial balance

05/02/2020 To Quick office limited account 1100

15/02/2020 To Cash account 70

28/02/2020 To Bank account 620

Lloyds a/c

Date Particulars JF Amount Date Particulars JF Amount

28/02/20 To balance c/d 2500 02/02/20 By Cash account 2500

Quick office a/c

Date Particulars JF Amount Date Particulars JF Amount

28/02/20 To balance c/d 1100 05/02/20 By Office Fixture account 1100

Nissan Co.

Date Particulars JF Amount Date Particulars JF Amount

19/02/20 To Bank account 5200 08/02/20 By Van account 5200

Cash a/c

Date Particulars JF Amount Date Particulars JF Amoun

02/02/20 To Lloyd's bank account 2500 15/02/20

By Office Fixture

account 70

03/02/20 To Bank account 1500 25/02/20 By Bank account 350

28/02/20 By balance c/d 3580

b. Trial balance

Trial balance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PARTICULARS DEBIT £

CREDIT

£

Capital 47300

Bank 9730

Van 35000

Office Fixtures 2590

Lloyd's Bank 2500

Quick office limited 1100

Cash in hand 3580

Total 50900 50900

PART 4

a) Income statement for the year ending 30th September, 2019

PARTICULARS £ £

Sales 80000 78000

Less Sales Return -2000

Opening Stock 36000

Add Purchase 150000

Less Purchase Return -600

Less Closing Stock -120000

Cost of goods sold 65400

Carriage Inward 720

Gross profit for the year 11880

Carriage Outward 400

Motor Expenses 1200

Rent 5000

CREDIT

£

Capital 47300

Bank 9730

Van 35000

Office Fixtures 2590

Lloyd's Bank 2500

Quick office limited 1100

Cash in hand 3580

Total 50900 50900

PART 4

a) Income statement for the year ending 30th September, 2019

PARTICULARS £ £

Sales 80000 78000

Less Sales Return -2000

Opening Stock 36000

Add Purchase 150000

Less Purchase Return -600

Less Closing Stock -120000

Cost of goods sold 65400

Carriage Inward 720

Gross profit for the year 11880

Carriage Outward 400

Motor Expenses 1200

Rent 5000

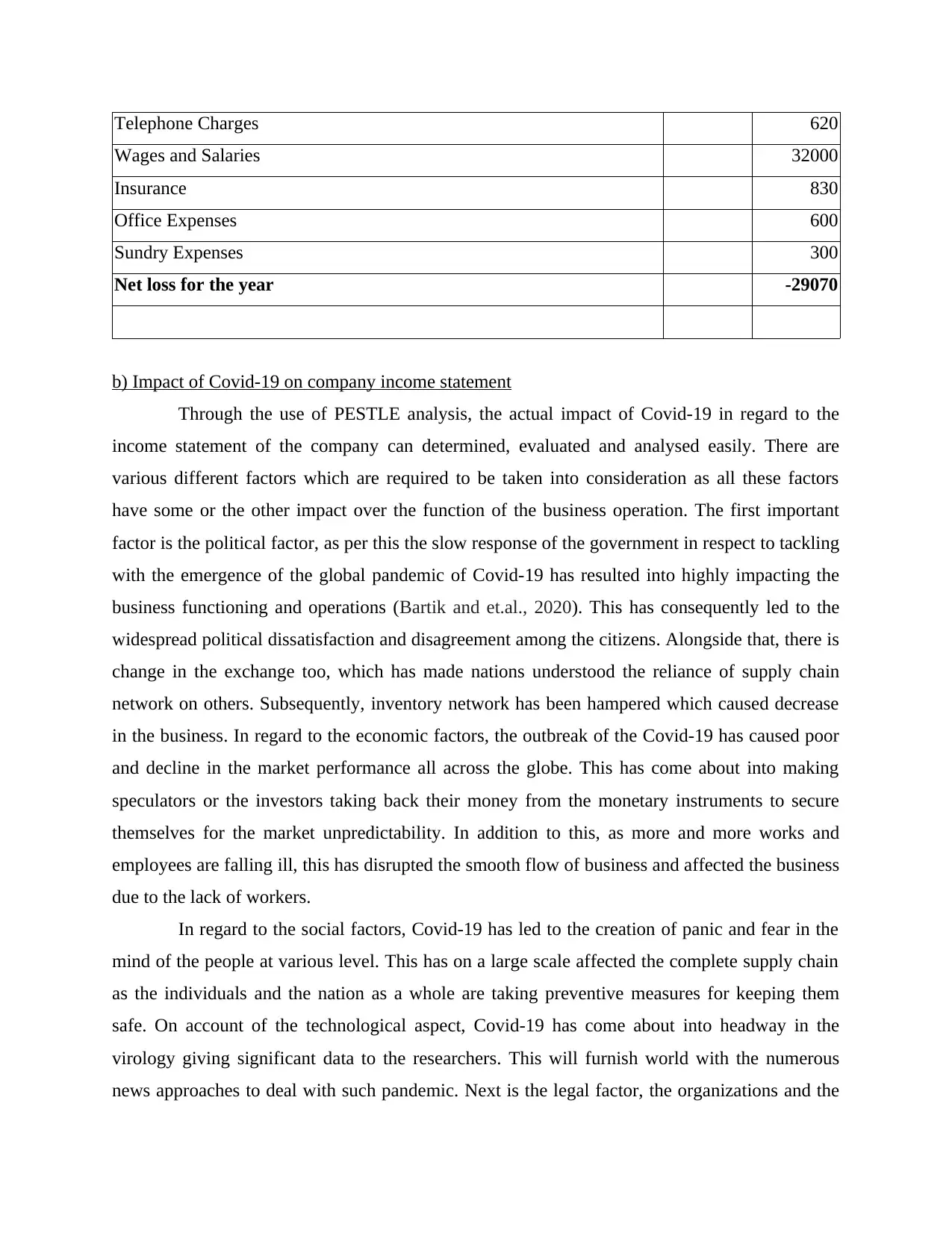

Telephone Charges 620

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Net loss for the year -29070

b) Impact of Covid-19 on company income statement

Through the use of PESTLE analysis, the actual impact of Covid-19 in regard to the

income statement of the company can determined, evaluated and analysed easily. There are

various different factors which are required to be taken into consideration as all these factors

have some or the other impact over the function of the business operation. The first important

factor is the political factor, as per this the slow response of the government in respect to tackling

with the emergence of the global pandemic of Covid-19 has resulted into highly impacting the

business functioning and operations (Bartik and et.al., 2020). This has consequently led to the

widespread political dissatisfaction and disagreement among the citizens. Alongside that, there is

change in the exchange too, which has made nations understood the reliance of supply chain

network on others. Subsequently, inventory network has been hampered which caused decrease

in the business. In regard to the economic factors, the outbreak of the Covid-19 has caused poor

and decline in the market performance all across the globe. This has come about into making

speculators or the investors taking back their money from the monetary instruments to secure

themselves for the market unpredictability. In addition to this, as more and more works and

employees are falling ill, this has disrupted the smooth flow of business and affected the business

due to the lack of workers.

In regard to the social factors, Covid-19 has led to the creation of panic and fear in the

mind of the people at various level. This has on a large scale affected the complete supply chain

as the individuals and the nation as a whole are taking preventive measures for keeping them

safe. On account of the technological aspect, Covid-19 has come about into headway in the

virology giving significant data to the researchers. This will furnish world with the numerous

news approaches to deal with such pandemic. Next is the legal factor, the organizations and the

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Net loss for the year -29070

b) Impact of Covid-19 on company income statement

Through the use of PESTLE analysis, the actual impact of Covid-19 in regard to the

income statement of the company can determined, evaluated and analysed easily. There are

various different factors which are required to be taken into consideration as all these factors

have some or the other impact over the function of the business operation. The first important

factor is the political factor, as per this the slow response of the government in respect to tackling

with the emergence of the global pandemic of Covid-19 has resulted into highly impacting the

business functioning and operations (Bartik and et.al., 2020). This has consequently led to the

widespread political dissatisfaction and disagreement among the citizens. Alongside that, there is

change in the exchange too, which has made nations understood the reliance of supply chain

network on others. Subsequently, inventory network has been hampered which caused decrease

in the business. In regard to the economic factors, the outbreak of the Covid-19 has caused poor

and decline in the market performance all across the globe. This has come about into making

speculators or the investors taking back their money from the monetary instruments to secure

themselves for the market unpredictability. In addition to this, as more and more works and

employees are falling ill, this has disrupted the smooth flow of business and affected the business

due to the lack of workers.

In regard to the social factors, Covid-19 has led to the creation of panic and fear in the

mind of the people at various level. This has on a large scale affected the complete supply chain

as the individuals and the nation as a whole are taking preventive measures for keeping them

safe. On account of the technological aspect, Covid-19 has come about into headway in the

virology giving significant data to the researchers. This will furnish world with the numerous

news approaches to deal with such pandemic. Next is the legal factor, the organizations and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

people are currently needed to keep the laws and principles set by the public authority under such

circumstance and rebelliousness of it will prompt inconvenience or punishment (Fairlie, 2020).

This factor has a huge impact over effectively and efficiently carrying out the business activities.

The last factor is environmental factor, the emergence of Covid-19 has caused travelling fear and

work from home or remote working condition which has come about into decrease in the

environmental pollution which is considered good for the people and the planet but on the other

hand, this has resulted into decline in the movement of people from one place to other. Hence, in

this way Covid-19 has affected the business as each of these factors ahs some influence or

impact over the items of income statement specially the revenue and cost. Coronavirus has

caused decline in revenue but the organizations were still required to meet with its fixed

expenses which cannot be ignored and thus, this has led to incurring losses for the businesses.

circumstance and rebelliousness of it will prompt inconvenience or punishment (Fairlie, 2020).

This factor has a huge impact over effectively and efficiently carrying out the business activities.

The last factor is environmental factor, the emergence of Covid-19 has caused travelling fear and

work from home or remote working condition which has come about into decrease in the

environmental pollution which is considered good for the people and the planet but on the other

hand, this has resulted into decline in the movement of people from one place to other. Hence, in

this way Covid-19 has affected the business as each of these factors ahs some influence or

impact over the items of income statement specially the revenue and cost. Coronavirus has

caused decline in revenue but the organizations were still required to meet with its fixed

expenses which cannot be ignored and thus, this has led to incurring losses for the businesses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

B Romney, M., 2018. Accounting information systems. Pearson Education Limited.

Bartik, A. W. and et.al., 2020. The impact of COVID-19 on small business outcomes and

expectations. Proceedings of the National Academy of Sciences. 117(30). pp.17656-

17666.

Chiu, V., Liu, Q., Muehlmann, B. and Baldwin, A. A., 2019. A bibliometric analysis of

accounting information systems journals and their emerging technologies

contributions. International Journal of Accounting Information Systems. 32 . pp.24-43.

Fairlie, R. W., 2020. The impact of COVID-19 on small business owners: Continued losses and

the partial rebound in May 2020 (No. w27462). National Bureau of Economic

Research.

1

Books and Journals

B Romney, M., 2018. Accounting information systems. Pearson Education Limited.

Bartik, A. W. and et.al., 2020. The impact of COVID-19 on small business outcomes and

expectations. Proceedings of the National Academy of Sciences. 117(30). pp.17656-

17666.

Chiu, V., Liu, Q., Muehlmann, B. and Baldwin, A. A., 2019. A bibliometric analysis of

accounting information systems journals and their emerging technologies

contributions. International Journal of Accounting Information Systems. 32 . pp.24-43.

Fairlie, R. W., 2020. The impact of COVID-19 on small business owners: Continued losses and

the partial rebound in May 2020 (No. w27462). National Bureau of Economic

Research.

1

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.