Financial Management Report: GSQ Company Analysis and Techniques

VerifiedAdded on 2023/01/13

|14

|3465

|22

Report

AI Summary

This report provides a comprehensive analysis of financial management, focusing on the fictional company GSQ. It delves into the core concepts of management accounting, exploring the significance of management accounting systems, reports, and various techniques. The report examines different management accounting methods, including job costing, inventory management, and price optimization systems, and their benefits. It further analyzes management accounting reporting methods such as performance reports, budget reports, and cost accounting reports. The report also compares absorption costing and marginal costing techniques, including their advantages and disadvantages. Additionally, it explores different planning tools for budgetary control, like zero-based budgeting and capital budgeting. Overall, the report offers insights into how organizations can utilize management accounting systems effectively.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

Management accounting reporting methods................................................................................3

LO2 .................................................................................................................................................4

Management accounting costing techniques...............................................................................4

LO3..................................................................................................................................................8

Different types of planning tools.................................................................................................8

LO4..................................................................................................................................................9

Comparing ways organization can use management accounting system....................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

Management accounting reporting methods................................................................................3

LO2 .................................................................................................................................................4

Management accounting costing techniques...............................................................................4

LO3..................................................................................................................................................8

Different types of planning tools.................................................................................................8

LO4..................................................................................................................................................9

Comparing ways organization can use management accounting system....................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting can be defined as the process in which the reports of business

operations are prepared, these reports helps the business manager in making the short term or

long term decisions of company. It have the task of identifying, analysing, measuring,

communicating and interpreting the financial information to the users. Report is about GSQ and

it will be revealing the importance of management accounting systems, management accounting

reports, the different types of management accounting techniques. It will also be providing about

the planning tools in budgetary control. The study will also be revealing about the different

management accounting methods for responding to financial issues.

LO1

Management accounting

This is also known as cost accounting or managerial accounting. This is also defined as

the process used for analysing cost and operations for preparation of financial reports and

records. Management accounting is used by managers for translating the financial and costing

information into useful information for the effective decision making in the organisation.

Management accounting is for internal use by the managers and executives for achieving higher

efficiency and productivity at minimal costs (Maas, Schaltegger and Crutzen, 2016).

Management accounting systems

Management accounting systems are used by the organisation for keeping the business

over a defined structural path. This refers to the management techniques used in management

accounting for having proper record of all the financial data and information.

Cost Accounting

Cost accounting systems refers to the accounting system used for having proper record of

all the cost of company. This helps the business in analysing the incomes and expenditures of

the company that it will be earning in the given year. It involves applying range of costing

concepts and techniques over the business operation with the motive of keeping the costs under

control and achieving maximum productivity. It is used by GSQ in the production process for

calculating the costs of manufacturing a product.

Benefits

Cost accounting helps in keeping record of all the costs incurred by business.

This involves various tools and techniques for keeping the costs under control.

1

Management accounting can be defined as the process in which the reports of business

operations are prepared, these reports helps the business manager in making the short term or

long term decisions of company. It have the task of identifying, analysing, measuring,

communicating and interpreting the financial information to the users. Report is about GSQ and

it will be revealing the importance of management accounting systems, management accounting

reports, the different types of management accounting techniques. It will also be providing about

the planning tools in budgetary control. The study will also be revealing about the different

management accounting methods for responding to financial issues.

LO1

Management accounting

This is also known as cost accounting or managerial accounting. This is also defined as

the process used for analysing cost and operations for preparation of financial reports and

records. Management accounting is used by managers for translating the financial and costing

information into useful information for the effective decision making in the organisation.

Management accounting is for internal use by the managers and executives for achieving higher

efficiency and productivity at minimal costs (Maas, Schaltegger and Crutzen, 2016).

Management accounting systems

Management accounting systems are used by the organisation for keeping the business

over a defined structural path. This refers to the management techniques used in management

accounting for having proper record of all the financial data and information.

Cost Accounting

Cost accounting systems refers to the accounting system used for having proper record of

all the cost of company. This helps the business in analysing the incomes and expenditures of

the company that it will be earning in the given year. It involves applying range of costing

concepts and techniques over the business operation with the motive of keeping the costs under

control and achieving maximum productivity. It is used by GSQ in the production process for

calculating the costs of manufacturing a product.

Benefits

Cost accounting helps in keeping record of all the costs incurred by business.

This involves various tools and techniques for keeping the costs under control.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This helps business in assessing the variations between actual and budgeted outputs.

Inventory Management

Inventory management can be defined as combination of technology and software that is

helping organisations in keeping track of all the movements of inventory. Inventory management

is used for having record of company assets, raw materials and finished goods. Using this

management is able to analyse the consumption of raw materials frequency of movement in

finished goods. It provides important information for decision-making to management(Ameen,

Ahmed and Abd Hafez, 2018). Inventory management system is applied in warehouse and

production house of company for having a proper record over the inflow and outflow of

inventory.

Benefits

Inventory management is a useful that enable GSQ in having proper record of all the

movements of stocks.

This used by management in decision making and forecasting.

It also helps in placing purchase order on time so that the production process is not

interrupted.

Price Optimisation System

The management accounting system involves measuring the fluctuations in demand at

different price levels. This method is used by organisations for defining optimum prices for its

product that will be most favourable for it. Businesses uses this model as powerful lever for

earning profits by pricing its products. Companies decide prices depending how customers will

be responding to them at different prices. It also takes into considerations other factors

influencing the pricing models. GSQ applies this model for forecasting the demand of its

products at different price levels including the inflation factors.

Benefits

This is an efficient method involving mathematical programs that helps in accurate

forecasting.

Prices that will be most beneficial and acceptable are decided using the optimisation

model.

This is an effective tool used in decision-making by management.

2

Inventory Management

Inventory management can be defined as combination of technology and software that is

helping organisations in keeping track of all the movements of inventory. Inventory management

is used for having record of company assets, raw materials and finished goods. Using this

management is able to analyse the consumption of raw materials frequency of movement in

finished goods. It provides important information for decision-making to management(Ameen,

Ahmed and Abd Hafez, 2018). Inventory management system is applied in warehouse and

production house of company for having a proper record over the inflow and outflow of

inventory.

Benefits

Inventory management is a useful that enable GSQ in having proper record of all the

movements of stocks.

This used by management in decision making and forecasting.

It also helps in placing purchase order on time so that the production process is not

interrupted.

Price Optimisation System

The management accounting system involves measuring the fluctuations in demand at

different price levels. This method is used by organisations for defining optimum prices for its

product that will be most favourable for it. Businesses uses this model as powerful lever for

earning profits by pricing its products. Companies decide prices depending how customers will

be responding to them at different prices. It also takes into considerations other factors

influencing the pricing models. GSQ applies this model for forecasting the demand of its

products at different price levels including the inflation factors.

Benefits

This is an efficient method involving mathematical programs that helps in accurate

forecasting.

Prices that will be most beneficial and acceptable are decided using the optimisation

model.

This is an effective tool used in decision-making by management.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job Costing System

It is a accounting concept used for tracking the expenditures and revenues from a

particular job. This involves complete detail of all the costs incurred by organisation over a job

like raw materials, labour and overhead. Job could also be defined as specific job done for single

customer or related to single product line or batch of units with all the same products (Nitzl,

2016). The profitability of job is decided after properlyh assessing the costs of each operation.

This is applied by GSQ for assessing the costs on a particular order by customers.

Benefits

This is used by organisations for the business enterprise for assessing cost of each job

separately.

It enables company in deciding the profit margins for each job done by company.

Management accounting reporting methods

Management accounting reports provide important information to the users of financial

information in decision making processes. There are various accounting reports used by GSQ in

effective decisions

Performance Report

This report contains information related to the performance of activities and operations of

business. This provides management with analysis about the level of targets achieved by the

organisation in given time period. This contains details about the targets and the achievements.

This is essential for assessing the efficiency of its management in achieving the targets.

Performance report not only includes the operational performance but all also the performance of

individuals and employees of company. This helps the managers in identifying the employees

who are performing well so that they can be motivated with rewards and incentives for

maintaining their efforts.

Budget reports

These reports can be termed as the spending plan of the business. Budgets are prepared

by making forecasts about the future income and revenues. These forecasts are made by

companies after analysing both internal and external forces affecting the budgets. These are

prepared analysing the budgets of previous year and making adjustment according to the current

scenarios like demand and inflations. Budgets are very useful for organisations for having a

3

It is a accounting concept used for tracking the expenditures and revenues from a

particular job. This involves complete detail of all the costs incurred by organisation over a job

like raw materials, labour and overhead. Job could also be defined as specific job done for single

customer or related to single product line or batch of units with all the same products (Nitzl,

2016). The profitability of job is decided after properlyh assessing the costs of each operation.

This is applied by GSQ for assessing the costs on a particular order by customers.

Benefits

This is used by organisations for the business enterprise for assessing cost of each job

separately.

It enables company in deciding the profit margins for each job done by company.

Management accounting reporting methods

Management accounting reports provide important information to the users of financial

information in decision making processes. There are various accounting reports used by GSQ in

effective decisions

Performance Report

This report contains information related to the performance of activities and operations of

business. This provides management with analysis about the level of targets achieved by the

organisation in given time period. This contains details about the targets and the achievements.

This is essential for assessing the efficiency of its management in achieving the targets.

Performance report not only includes the operational performance but all also the performance of

individuals and employees of company. This helps the managers in identifying the employees

who are performing well so that they can be motivated with rewards and incentives for

maintaining their efforts.

Budget reports

These reports can be termed as the spending plan of the business. Budgets are prepared

by making forecasts about the future income and revenues. These forecasts are made by

companies after analysing both internal and external forces affecting the budgets. These are

prepared analysing the budgets of previous year and making adjustment according to the current

scenarios like demand and inflations. Budgets are very useful for organisations for having a

3

proper structure for its expenses. This helps GSQ in allocating its resources most appropriately

so that the costs decided do not go out of the budgeted levels (Averinа, Kolesnik and Makarova,

2016). Budgets are used by organisations for keeping the costs under control and taking

corrective measures for achieving the desired level of outputs.

Cost Accounting Report

Cost accounting reports contain the detailed analysis about the costs occurred for

manufacturing a product. It present all the variable and fixed cost separately that helps the

business in deciding the cost of product. Costing technique also involves making forecasts using

the information available with the business. Costing involves making comparisons about the

budgeted and actual level of outputs. This helps business in assessing the variances for which

company takes effective policies and procedures for reducing the variances and achieving the

required targeted objectives. Cost reports helps company in deciding the adequate profits

margins for the product so that it may attain the profitability and desired business objectives.

LO2

Management accounting costing techniques.

GSQ is a manufacturing concern that will be using different management accounting

techniques for reporting the business transactions. The different management accounting

techniques that will be used by the management accountants are marginal costing and absorption

costing. These are used for carrying out the profits from business operations.

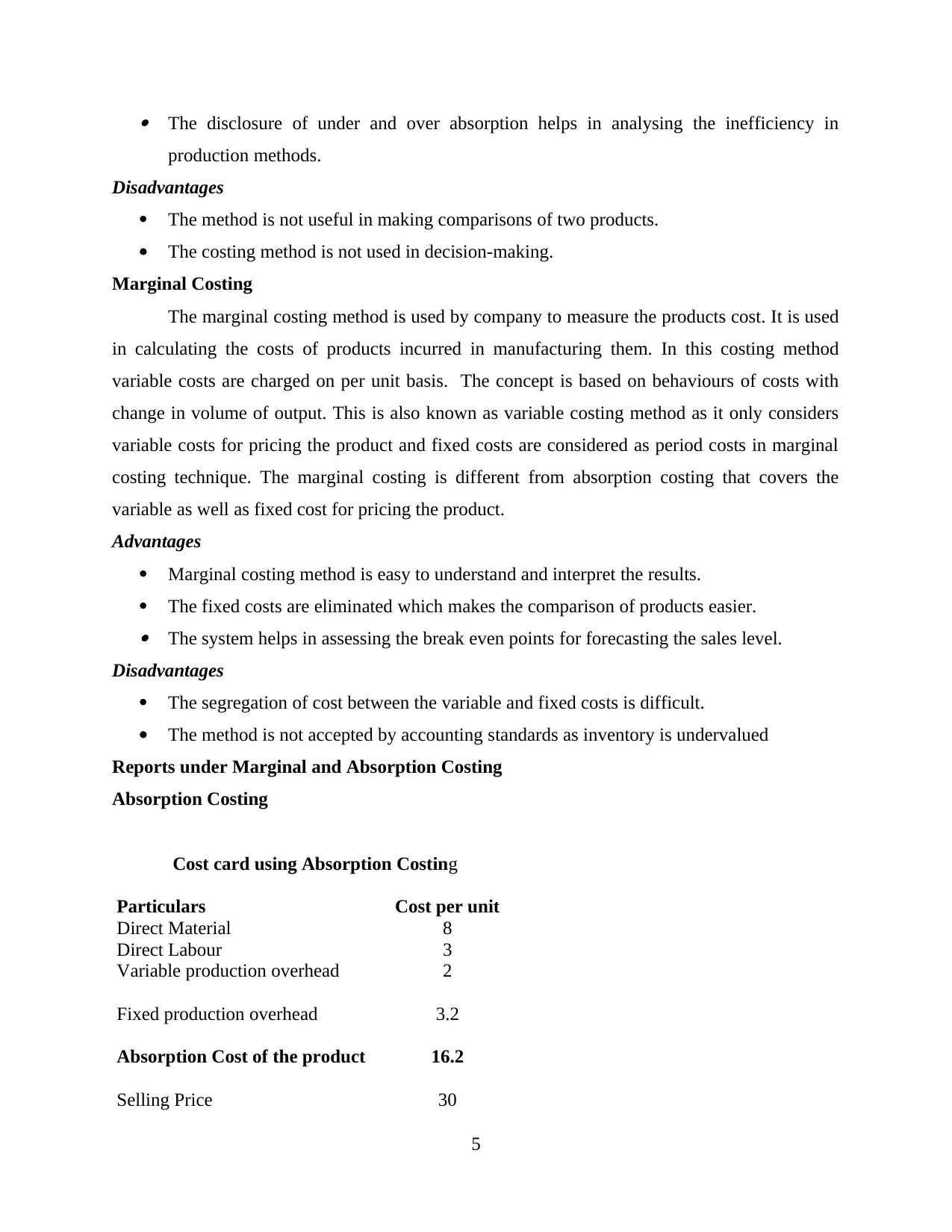

Absorption Costing

Absorption costing is also known as full costing method that are acceptable under the

accounting standards. The costing method is used for calculating the net income and for valuing

inventory. It is used by organisations for absorbing the manufacturing costs including both the

variable and fixed costs. The costing method includes both variable and fixed costs for

calculating the cost of product. Absorption costing is considered for analysing the accurate and

more comprehensive view for the business. As compared with the marginal costing method it

includes the fixed costs and variable costs in pricing the product.

Advantages

The methods is acceptable as per accounting standards for valuing the inventory.

It takes into account fixed costs incurred for manufacturing the product.

4

so that the costs decided do not go out of the budgeted levels (Averinа, Kolesnik and Makarova,

2016). Budgets are used by organisations for keeping the costs under control and taking

corrective measures for achieving the desired level of outputs.

Cost Accounting Report

Cost accounting reports contain the detailed analysis about the costs occurred for

manufacturing a product. It present all the variable and fixed cost separately that helps the

business in deciding the cost of product. Costing technique also involves making forecasts using

the information available with the business. Costing involves making comparisons about the

budgeted and actual level of outputs. This helps business in assessing the variances for which

company takes effective policies and procedures for reducing the variances and achieving the

required targeted objectives. Cost reports helps company in deciding the adequate profits

margins for the product so that it may attain the profitability and desired business objectives.

LO2

Management accounting costing techniques.

GSQ is a manufacturing concern that will be using different management accounting

techniques for reporting the business transactions. The different management accounting

techniques that will be used by the management accountants are marginal costing and absorption

costing. These are used for carrying out the profits from business operations.

Absorption Costing

Absorption costing is also known as full costing method that are acceptable under the

accounting standards. The costing method is used for calculating the net income and for valuing

inventory. It is used by organisations for absorbing the manufacturing costs including both the

variable and fixed costs. The costing method includes both variable and fixed costs for

calculating the cost of product. Absorption costing is considered for analysing the accurate and

more comprehensive view for the business. As compared with the marginal costing method it

includes the fixed costs and variable costs in pricing the product.

Advantages

The methods is acceptable as per accounting standards for valuing the inventory.

It takes into account fixed costs incurred for manufacturing the product.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The disclosure of under and over absorption helps in analysing the inefficiency in

production methods.

Disadvantages

The method is not useful in making comparisons of two products.

The costing method is not used in decision-making.

Marginal Costing

The marginal costing method is used by company to measure the products cost. It is used

in calculating the costs of products incurred in manufacturing them. In this costing method

variable costs are charged on per unit basis. The concept is based on behaviours of costs with

change in volume of output. This is also known as variable costing method as it only considers

variable costs for pricing the product and fixed costs are considered as period costs in marginal

costing technique. The marginal costing is different from absorption costing that covers the

variable as well as fixed cost for pricing the product.

Advantages

Marginal costing method is easy to understand and interpret the results.

The fixed costs are eliminated which makes the comparison of products easier. The system helps in assessing the break even points for forecasting the sales level.

Disadvantages

The segregation of cost between the variable and fixed costs is difficult.

The method is not accepted by accounting standards as inventory is undervalued

Reports under Marginal and Absorption Costing

Absorption Costing

Cost card using Absorption Costing

Particulars Cost per unit

Direct Material 8

Direct Labour 3

Variable production overhead 2

Fixed production overhead 3.2

Absorption Cost of the product 16.2

Selling Price 30

5

production methods.

Disadvantages

The method is not useful in making comparisons of two products.

The costing method is not used in decision-making.

Marginal Costing

The marginal costing method is used by company to measure the products cost. It is used

in calculating the costs of products incurred in manufacturing them. In this costing method

variable costs are charged on per unit basis. The concept is based on behaviours of costs with

change in volume of output. This is also known as variable costing method as it only considers

variable costs for pricing the product and fixed costs are considered as period costs in marginal

costing technique. The marginal costing is different from absorption costing that covers the

variable as well as fixed cost for pricing the product.

Advantages

Marginal costing method is easy to understand and interpret the results.

The fixed costs are eliminated which makes the comparison of products easier. The system helps in assessing the break even points for forecasting the sales level.

Disadvantages

The segregation of cost between the variable and fixed costs is difficult.

The method is not accepted by accounting standards as inventory is undervalued

Reports under Marginal and Absorption Costing

Absorption Costing

Cost card using Absorption Costing

Particulars Cost per unit

Direct Material 8

Direct Labour 3

Variable production overhead 2

Fixed production overhead 3.2

Absorption Cost of the product 16.2

Selling Price 30

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

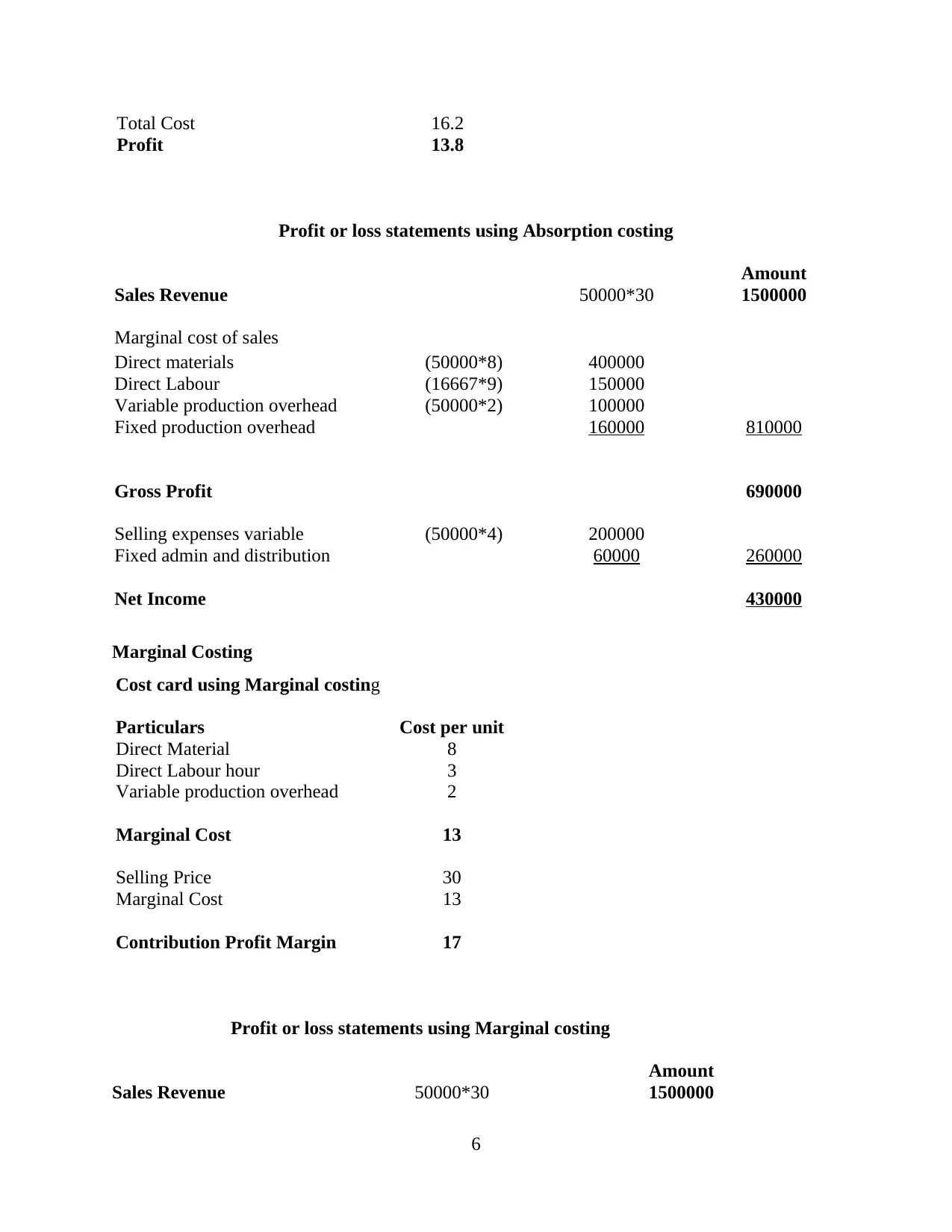

Total Cost 16.2

Profit 13.8

Profit or loss statements using Absorption costing

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials (50000*8) 400000

Direct Labour (16667*9) 150000

Variable production overhead (50000*2) 100000

Fixed production overhead 160000 810000

Gross Profit 690000

Selling expenses variable (50000*4) 200000

Fixed admin and distribution 60000 260000

Net Income 430000

Marginal Costing

Cost card using Marginal costing

Particulars Cost per unit

Direct Material 8

Direct Labour hour 3

Variable production overhead 2

Marginal Cost 13

Selling Price 30

Marginal Cost 13

Contribution Profit Margin 17

Profit or loss statements using Marginal costing

Amount

Sales Revenue 50000*30 1500000

6

Profit 13.8

Profit or loss statements using Absorption costing

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials (50000*8) 400000

Direct Labour (16667*9) 150000

Variable production overhead (50000*2) 100000

Fixed production overhead 160000 810000

Gross Profit 690000

Selling expenses variable (50000*4) 200000

Fixed admin and distribution 60000 260000

Net Income 430000

Marginal Costing

Cost card using Marginal costing

Particulars Cost per unit

Direct Material 8

Direct Labour hour 3

Variable production overhead 2

Marginal Cost 13

Selling Price 30

Marginal Cost 13

Contribution Profit Margin 17

Profit or loss statements using Marginal costing

Amount

Sales Revenue 50000*30 1500000

6

Marginal cost of sales

Direct materials (50000*8) 400000

Direct Labour hours (16667*9) 150000

Variable production overhead (50000*2) 100000 650000

Contribution 850000

Fixed production overhead 160000

Selling expenses variable (50000*4) 200000

Fixed admin and distribution 60000 420000

Net Income 430000

Working Note :

Wages per hour £9.00

Labour per unit 20 (Minutes)

Number of units 50000

Time for 50000 units (minutes) 1000000

(50000 units * 20 minutes)

Total Hours for production 16666.67

(1000000/60)

Direct wages £150,000.00

(16667 hours * 9)

7

Direct materials (50000*8) 400000

Direct Labour hours (16667*9) 150000

Variable production overhead (50000*2) 100000 650000

Contribution 850000

Fixed production overhead 160000

Selling expenses variable (50000*4) 200000

Fixed admin and distribution 60000 420000

Net Income 430000

Working Note :

Wages per hour £9.00

Labour per unit 20 (Minutes)

Number of units 50000

Time for 50000 units (minutes) 1000000

(50000 units * 20 minutes)

Total Hours for production 16666.67

(1000000/60)

Direct wages £150,000.00

(16667 hours * 9)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO3

Different types of planning tools

There are different types of planning tools available for budgetary control. A detailed

description is given below.

Zero based budgeting: It is a method of budgeting in which budget is prepared from the zero.

Every function or department within an organization is analysed based on its needs and cost. All

expenses are justified for each new period (Miller, 2018). It involves re-evaluating each item of

cash flow and justifying the expenditure that are required to be incurred by the department.

Advantages:

It justifies all operating expenses. It scraps the obsolete processes which helps in better costing and better profitability.

Disadvantages:

Process can be manipulated by managers to get more resources to their department.

It requires lot of time and efforts.

Capital budgeting: It is the formal business process for evaluating whether to invest in a

particular project and asset or not (Abor, 2017). It refers to the decision in relation to the

investment of the funds in addition, modification or replacement of fixed asset.

Advantages:

It helps in identifying the risk.

It provides complete report with respect to different projects. Helps in placing adequate control over expenditure.

Disadvantages:

Mostly decisions are taken for long term.

It requires professionals with high skills.

Introspective in nature due risk and discounting factor.

Cash budgeting: It is an estimation of cash flow for a specific period which includes expected

cash receipts and disbursements (DeFranco and Schmidgall, 2017). These cash inflows and

outflows include revenue collected, expenses paid, repayment of loan etc. This budget is usually

made after preparing sales, purchase and capital expenditure budget. It is prepared to assess

whether company is having sufficient cash to operate its business or not.

Advantages:

8

Different types of planning tools

There are different types of planning tools available for budgetary control. A detailed

description is given below.

Zero based budgeting: It is a method of budgeting in which budget is prepared from the zero.

Every function or department within an organization is analysed based on its needs and cost. All

expenses are justified for each new period (Miller, 2018). It involves re-evaluating each item of

cash flow and justifying the expenditure that are required to be incurred by the department.

Advantages:

It justifies all operating expenses. It scraps the obsolete processes which helps in better costing and better profitability.

Disadvantages:

Process can be manipulated by managers to get more resources to their department.

It requires lot of time and efforts.

Capital budgeting: It is the formal business process for evaluating whether to invest in a

particular project and asset or not (Abor, 2017). It refers to the decision in relation to the

investment of the funds in addition, modification or replacement of fixed asset.

Advantages:

It helps in identifying the risk.

It provides complete report with respect to different projects. Helps in placing adequate control over expenditure.

Disadvantages:

Mostly decisions are taken for long term.

It requires professionals with high skills.

Introspective in nature due risk and discounting factor.

Cash budgeting: It is an estimation of cash flow for a specific period which includes expected

cash receipts and disbursements (DeFranco and Schmidgall, 2017). These cash inflows and

outflows include revenue collected, expenses paid, repayment of loan etc. This budget is usually

made after preparing sales, purchase and capital expenditure budget. It is prepared to assess

whether company is having sufficient cash to operate its business or not.

Advantages:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It prevents over spending by the organization.

It helps in analysing the resources available to meet the operational needs. It also helps in analysing minimum liquidity and cash balance requirement.

Disadvantages:

It limits the spending power.

It does not reflect correct profit as it is based on assumptions and also it considers cash

flows from security deposits etc.

It is prepared based on the previous year cash allocation so there is no guarantee cash

flow will be similar in the future.

So, it can be said that planning tools are very essential for the GSQ Ltd. All these tools

have its own advantages and disadvantages. The application of these methods in an organization

will lead to increase its profitability and reduce risk and efficient management of the business.

LO4

Comparing ways organization can use management accounting system

Benchmarking: It is the process which helps in measuring the performance of the organization,

its products and processes. It is measured by comparing the company's performance to its

competitors. It helps in identifying the internal opportunities available to the organization for

further improvement (John and Eeckhout, 2018). For example by comparing the superior

performance and breaking down it to analyse what makes it superior and then comparing those

processes with the organization and then implement the changes as per the requirement. It helps

in improving the performance, productivity and profitability of the organization.

Key performance indicators: It is a performance measurement indicator which evaluates the

success of the organization based on certain indicators. It demonstrates how effectively

organization is achieving its objectives and goals. KPIs differ from organization to organization

and it is implemented at different levels to evaluate the success. Mostly, low KPIs are set for

processes in departments such as sales, marketing, HR etc. The high KPIs are focussed on the

overall performance of the organization. KPIs can be of different types such increase in sales

level, achieving the targeted outcome etc.

Balanced scorecard: It is a performance management metrics used by the organization to

identify and improve the business functions and their performance based on outcome. It allows

9

It helps in analysing the resources available to meet the operational needs. It also helps in analysing minimum liquidity and cash balance requirement.

Disadvantages:

It limits the spending power.

It does not reflect correct profit as it is based on assumptions and also it considers cash

flows from security deposits etc.

It is prepared based on the previous year cash allocation so there is no guarantee cash

flow will be similar in the future.

So, it can be said that planning tools are very essential for the GSQ Ltd. All these tools

have its own advantages and disadvantages. The application of these methods in an organization

will lead to increase its profitability and reduce risk and efficient management of the business.

LO4

Comparing ways organization can use management accounting system

Benchmarking: It is the process which helps in measuring the performance of the organization,

its products and processes. It is measured by comparing the company's performance to its

competitors. It helps in identifying the internal opportunities available to the organization for

further improvement (John and Eeckhout, 2018). For example by comparing the superior

performance and breaking down it to analyse what makes it superior and then comparing those

processes with the organization and then implement the changes as per the requirement. It helps

in improving the performance, productivity and profitability of the organization.

Key performance indicators: It is a performance measurement indicator which evaluates the

success of the organization based on certain indicators. It demonstrates how effectively

organization is achieving its objectives and goals. KPIs differ from organization to organization

and it is implemented at different levels to evaluate the success. Mostly, low KPIs are set for

processes in departments such as sales, marketing, HR etc. The high KPIs are focussed on the

overall performance of the organization. KPIs can be of different types such increase in sales

level, achieving the targeted outcome etc.

Balanced scorecard: It is a performance management metrics used by the organization to

identify and improve the business functions and their performance based on outcome. It allows

9

businesses to look at its business from different perspectives which includes financial and

customer perspective, internal business perspective and innovation and learning perspective. It is

used to measure and provide feedback to the organization. It links vision to strategic objectives,

targets and initiatives. It is a business performance measurement tool.

Variance analysis: It is analytical tool which is used for the analysis of difference between

actual performance and the standard performance. This analysis is used for exercising control

over the business. For example, budgeted sales is £10000 and the actual sales is £8000, in this

situation variance analysis will give a difference of £2000. It also helps in analysing the reason

for such difference and corrective actions are taken (Marzlin Marzuki and Ismail, 2019). The

detailed analysis of this allows management to identify the reason of fluctuation in its business

and the steps that can be taken. The variance analysis is of different types which includes

purchase price variance, selling price variance, labour efficiency variance, fixed and variable

overhead spending variance etc.

GSQ limited Sun Mark Limited

The GSQ limited uses variance analysis and

balanced scorecard system for measuring its

performance. The balanced score card help

GSQ Ltd in strategic planning, better analysing

management information accompanied with

improved and relevant performance reports.

Variance analysis helps the organization in

efficient and forward looking budgetary

decisions. It also acts as a control mechanism

in respect to cost.

Sun Mark Limited uses benchmarking and key

performance indicators. Benchmarking helps in

gaining perspective about the performance in

comparison to its competitors. It also helps in

setting performance expectations, monitor the

performance of the company and implement

changes. The key performance indicators

provides right information which helps in

informed decision making, allows users and

managers to measure target, establishes

transparency in the organization.

CONCLUSION

It can be concluded from the above that management accounting is very beneficial to

business organization. It helps in proper and complete analysis of the financial and non-financial

10

customer perspective, internal business perspective and innovation and learning perspective. It is

used to measure and provide feedback to the organization. It links vision to strategic objectives,

targets and initiatives. It is a business performance measurement tool.

Variance analysis: It is analytical tool which is used for the analysis of difference between

actual performance and the standard performance. This analysis is used for exercising control

over the business. For example, budgeted sales is £10000 and the actual sales is £8000, in this

situation variance analysis will give a difference of £2000. It also helps in analysing the reason

for such difference and corrective actions are taken (Marzlin Marzuki and Ismail, 2019). The

detailed analysis of this allows management to identify the reason of fluctuation in its business

and the steps that can be taken. The variance analysis is of different types which includes

purchase price variance, selling price variance, labour efficiency variance, fixed and variable

overhead spending variance etc.

GSQ limited Sun Mark Limited

The GSQ limited uses variance analysis and

balanced scorecard system for measuring its

performance. The balanced score card help

GSQ Ltd in strategic planning, better analysing

management information accompanied with

improved and relevant performance reports.

Variance analysis helps the organization in

efficient and forward looking budgetary

decisions. It also acts as a control mechanism

in respect to cost.

Sun Mark Limited uses benchmarking and key

performance indicators. Benchmarking helps in

gaining perspective about the performance in

comparison to its competitors. It also helps in

setting performance expectations, monitor the

performance of the company and implement

changes. The key performance indicators

provides right information which helps in

informed decision making, allows users and

managers to measure target, establishes

transparency in the organization.

CONCLUSION

It can be concluded from the above that management accounting is very beneficial to

business organization. It helps in proper and complete analysis of the financial and non-financial

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.