Financial Accounting Report: Journal Entries, Ledgers, and Statements

VerifiedAdded on 2023/01/10

|23

|5021

|76

Report

AI Summary

This report delves into the core principles and practices of financial accounting. It begins by defining different types of business transactions, including cash, credit, internal, and external transactions, along with the contrasting systems of single and double-entry bookkeeping. The report then proceeds to illustrate the practical application of these concepts through journal entries, ledger accounts, and the creation of a trial balance. A key aspect of the report is the evaluation of the differences between financial reports and financial statements, highlighting their respective purposes and types. Further, the report examines fundamental accounting principles, such as economic entity assumptions, monetary unit assumptions, cost principles, and more. Finally, the report includes the preparation of a profitability statement, demonstrating the practical application of accounting knowledge to real-world financial scenarios.

Financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Scenario 1.........................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................4

Question 3...................................................................................................................................8

Question 4.................................................................................................................................10

Question 5.................................................................................................................................11

Scenario 2.......................................................................................................................................12

Question1..................................................................................................................................12

Question 2.................................................................................................................................13

Question 3.................................................................................................................................14

Question 4.................................................................................................................................15

Question 5.................................................................................................................................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................3

Scenario 1.........................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................4

Question 3...................................................................................................................................8

Question 4.................................................................................................................................10

Question 5.................................................................................................................................11

Scenario 2.......................................................................................................................................12

Question1..................................................................................................................................12

Question 2.................................................................................................................................13

Question 3.................................................................................................................................14

Question 4.................................................................................................................................15

Question 5.................................................................................................................................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION

Financial accounting is that branch of accounting which records all the transaction of the

company which are financial in nature and post them in ledger in order to summarize them and

prepare the financial statements like profit and loss account and balance sheet (Schroeder, Clark

and Cathey, 2019). The current report will discuss the different stages of financial accounting

through which the financial transaction has to go. Like in the report first some transaction will be

recorded with the help of journal entries and then these will be posted in the ledger accounts and

trial balance will be made from it. Further the difference between the financial statement and

reports will be outlined and principles of accounting as well. After that with the help of the given

trial balance the profit and loss and balance sheet will be prepared. Further the bank

reconciliation statement will be prepared and in the end some journal entries for the rectification

of some errors will be done.

Scenario 1

Question 1.

Different types of business transaction

In accounting, there are mainly two types of business transaction which are discussed

below.

Cash transactions and credit transactions

A transaction in which cash is involved that is either it is paid or received at the time

when the transaction took place is called cash transaction. For example, goods purchased for $50

and paid the amount immediately (Weygandt, Kimmel and Kieso, 2019). In credit transaction,

the cash is received or paid in the future date after the transaction occurs. For instance, the goods

are purchased worth $2000 for which payment will be made after 2 weeks even though goods

have been possessed. It is considered as credit transaction as the payment has not been made in

cash immediately.

Internal and external transactions

Internal transaction are those transactions which does not involve exchange of values

among the parties but it can be measured in financial terms and have an impact over the financial

position of the business. For example, recording depreciation, realizing the loss caused because

by fire and so forth. External transactions are those transactions in which business exchanges

values with the outsiders (Birt and et.al, 2020). These are those transactions which are usually

Financial accounting is that branch of accounting which records all the transaction of the

company which are financial in nature and post them in ledger in order to summarize them and

prepare the financial statements like profit and loss account and balance sheet (Schroeder, Clark

and Cathey, 2019). The current report will discuss the different stages of financial accounting

through which the financial transaction has to go. Like in the report first some transaction will be

recorded with the help of journal entries and then these will be posted in the ledger accounts and

trial balance will be made from it. Further the difference between the financial statement and

reports will be outlined and principles of accounting as well. After that with the help of the given

trial balance the profit and loss and balance sheet will be prepared. Further the bank

reconciliation statement will be prepared and in the end some journal entries for the rectification

of some errors will be done.

Scenario 1

Question 1.

Different types of business transaction

In accounting, there are mainly two types of business transaction which are discussed

below.

Cash transactions and credit transactions

A transaction in which cash is involved that is either it is paid or received at the time

when the transaction took place is called cash transaction. For example, goods purchased for $50

and paid the amount immediately (Weygandt, Kimmel and Kieso, 2019). In credit transaction,

the cash is received or paid in the future date after the transaction occurs. For instance, the goods

are purchased worth $2000 for which payment will be made after 2 weeks even though goods

have been possessed. It is considered as credit transaction as the payment has not been made in

cash immediately.

Internal and external transactions

Internal transaction are those transactions which does not involve exchange of values

among the parties but it can be measured in financial terms and have an impact over the financial

position of the business. For example, recording depreciation, realizing the loss caused because

by fire and so forth. External transactions are those transactions in which business exchanges

values with the outsiders (Birt and et.al, 2020). These are those transactions which are usually

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

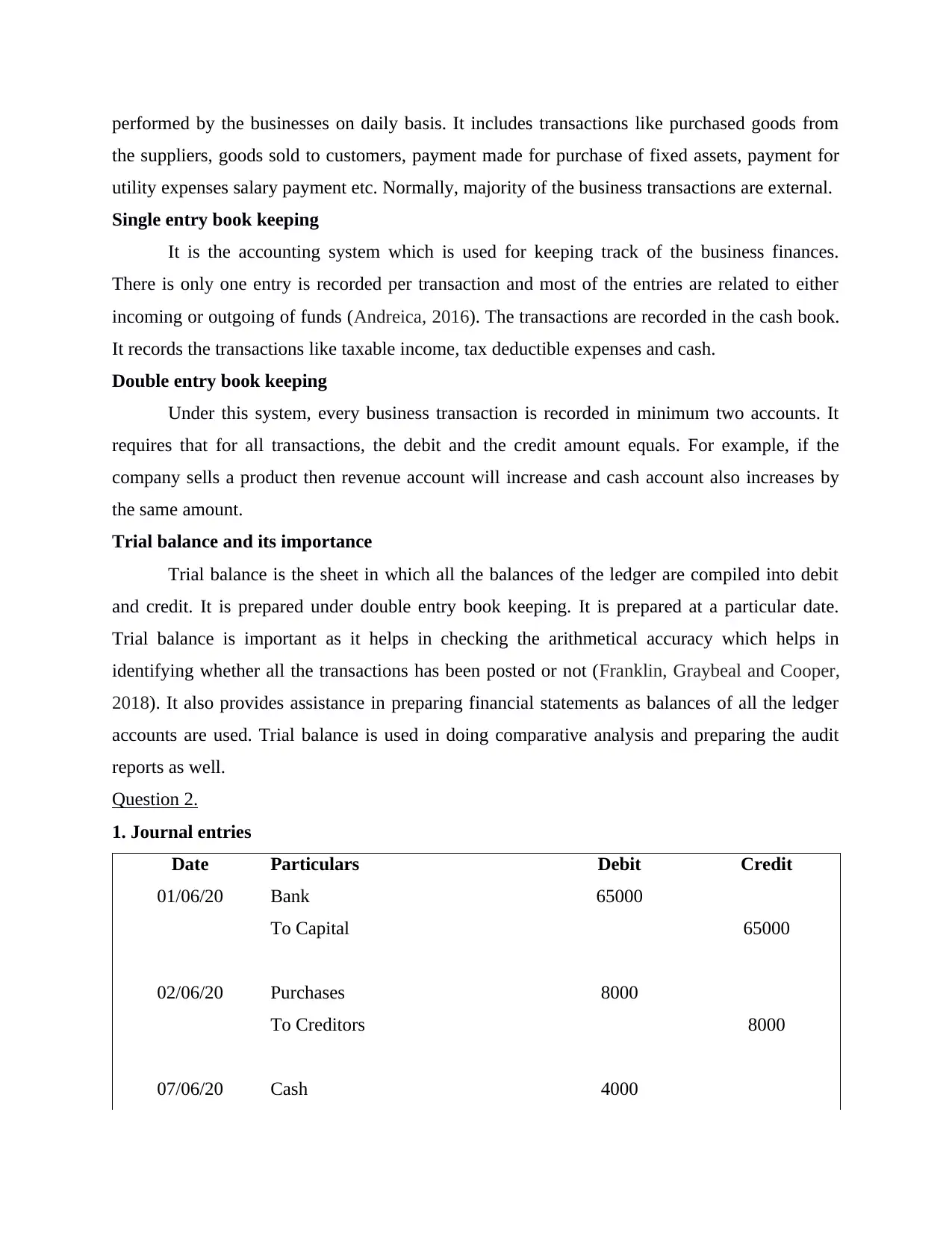

performed by the businesses on daily basis. It includes transactions like purchased goods from

the suppliers, goods sold to customers, payment made for purchase of fixed assets, payment for

utility expenses salary payment etc. Normally, majority of the business transactions are external.

Single entry book keeping

It is the accounting system which is used for keeping track of the business finances.

There is only one entry is recorded per transaction and most of the entries are related to either

incoming or outgoing of funds (Andreica, 2016). The transactions are recorded in the cash book.

It records the transactions like taxable income, tax deductible expenses and cash.

Double entry book keeping

Under this system, every business transaction is recorded in minimum two accounts. It

requires that for all transactions, the debit and the credit amount equals. For example, if the

company sells a product then revenue account will increase and cash account also increases by

the same amount.

Trial balance and its importance

Trial balance is the sheet in which all the balances of the ledger are compiled into debit

and credit. It is prepared under double entry book keeping. It is prepared at a particular date.

Trial balance is important as it helps in checking the arithmetical accuracy which helps in

identifying whether all the transactions has been posted or not (Franklin, Graybeal and Cooper,

2018). It also provides assistance in preparing financial statements as balances of all the ledger

accounts are used. Trial balance is used in doing comparative analysis and preparing the audit

reports as well.

Question 2.

1. Journal entries

Date Particulars Debit Credit

01/06/20 Bank 65000

To Capital 65000

02/06/20 Purchases 8000

To Creditors 8000

07/06/20 Cash 4000

the suppliers, goods sold to customers, payment made for purchase of fixed assets, payment for

utility expenses salary payment etc. Normally, majority of the business transactions are external.

Single entry book keeping

It is the accounting system which is used for keeping track of the business finances.

There is only one entry is recorded per transaction and most of the entries are related to either

incoming or outgoing of funds (Andreica, 2016). The transactions are recorded in the cash book.

It records the transactions like taxable income, tax deductible expenses and cash.

Double entry book keeping

Under this system, every business transaction is recorded in minimum two accounts. It

requires that for all transactions, the debit and the credit amount equals. For example, if the

company sells a product then revenue account will increase and cash account also increases by

the same amount.

Trial balance and its importance

Trial balance is the sheet in which all the balances of the ledger are compiled into debit

and credit. It is prepared under double entry book keeping. It is prepared at a particular date.

Trial balance is important as it helps in checking the arithmetical accuracy which helps in

identifying whether all the transactions has been posted or not (Franklin, Graybeal and Cooper,

2018). It also provides assistance in preparing financial statements as balances of all the ledger

accounts are used. Trial balance is used in doing comparative analysis and preparing the audit

reports as well.

Question 2.

1. Journal entries

Date Particulars Debit Credit

01/06/20 Bank 65000

To Capital 65000

02/06/20 Purchases 8000

To Creditors 8000

07/06/20 Cash 4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

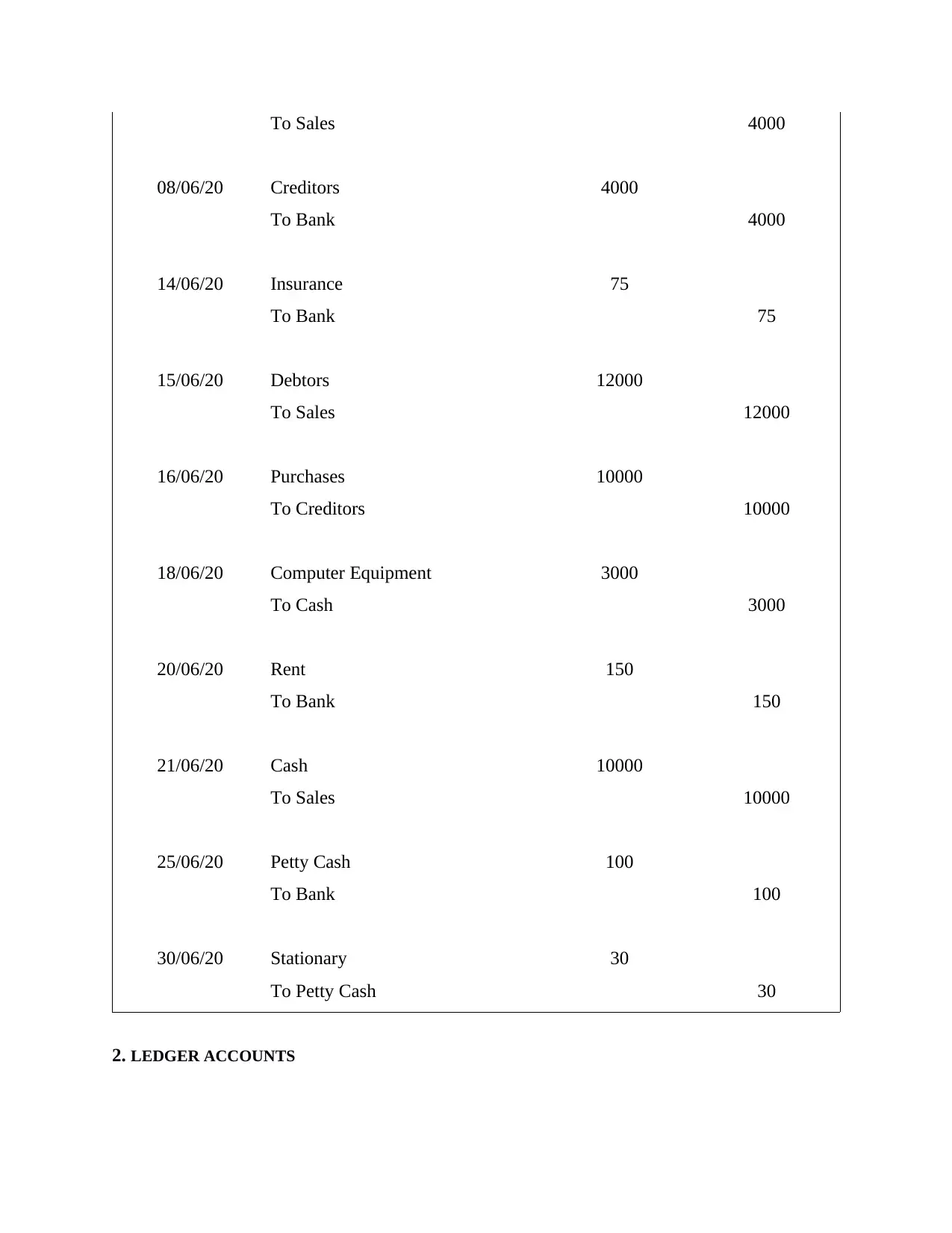

To Sales 4000

08/06/20 Creditors 4000

To Bank 4000

14/06/20 Insurance 75

To Bank 75

15/06/20 Debtors 12000

To Sales 12000

16/06/20 Purchases 10000

To Creditors 10000

18/06/20 Computer Equipment 3000

To Cash 3000

20/06/20 Rent 150

To Bank 150

21/06/20 Cash 10000

To Sales 10000

25/06/20 Petty Cash 100

To Bank 100

30/06/20 Stationary 30

To Petty Cash 30

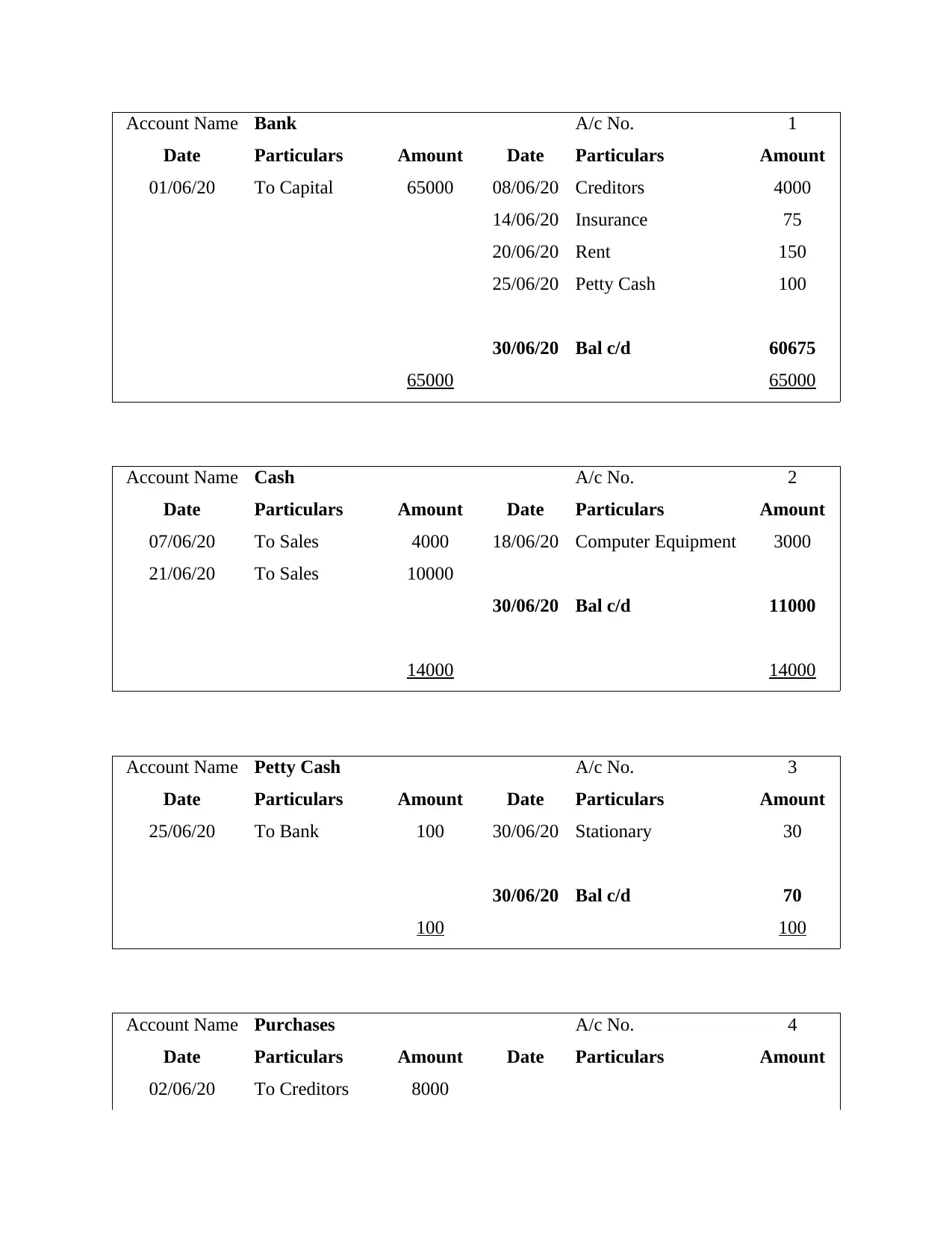

2. LEDGER ACCOUNTS

08/06/20 Creditors 4000

To Bank 4000

14/06/20 Insurance 75

To Bank 75

15/06/20 Debtors 12000

To Sales 12000

16/06/20 Purchases 10000

To Creditors 10000

18/06/20 Computer Equipment 3000

To Cash 3000

20/06/20 Rent 150

To Bank 150

21/06/20 Cash 10000

To Sales 10000

25/06/20 Petty Cash 100

To Bank 100

30/06/20 Stationary 30

To Petty Cash 30

2. LEDGER ACCOUNTS

Account Name Bank A/c No. 1

Date Particulars Amount Date Particulars Amount

01/06/20 To Capital 65000 08/06/20 Creditors 4000

14/06/20 Insurance 75

20/06/20 Rent 150

25/06/20 Petty Cash 100

30/06/20 Bal c/d 60675

65000 65000

Account Name Cash A/c No. 2

Date Particulars Amount Date Particulars Amount

07/06/20 To Sales 4000 18/06/20 Computer Equipment 3000

21/06/20 To Sales 10000

30/06/20 Bal c/d 11000

14000 14000

Account Name Petty Cash A/c No. 3

Date Particulars Amount Date Particulars Amount

25/06/20 To Bank 100 30/06/20 Stationary 30

30/06/20 Bal c/d 70

100 100

Account Name Purchases A/c No. 4

Date Particulars Amount Date Particulars Amount

02/06/20 To Creditors 8000

Date Particulars Amount Date Particulars Amount

01/06/20 To Capital 65000 08/06/20 Creditors 4000

14/06/20 Insurance 75

20/06/20 Rent 150

25/06/20 Petty Cash 100

30/06/20 Bal c/d 60675

65000 65000

Account Name Cash A/c No. 2

Date Particulars Amount Date Particulars Amount

07/06/20 To Sales 4000 18/06/20 Computer Equipment 3000

21/06/20 To Sales 10000

30/06/20 Bal c/d 11000

14000 14000

Account Name Petty Cash A/c No. 3

Date Particulars Amount Date Particulars Amount

25/06/20 To Bank 100 30/06/20 Stationary 30

30/06/20 Bal c/d 70

100 100

Account Name Purchases A/c No. 4

Date Particulars Amount Date Particulars Amount

02/06/20 To Creditors 8000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

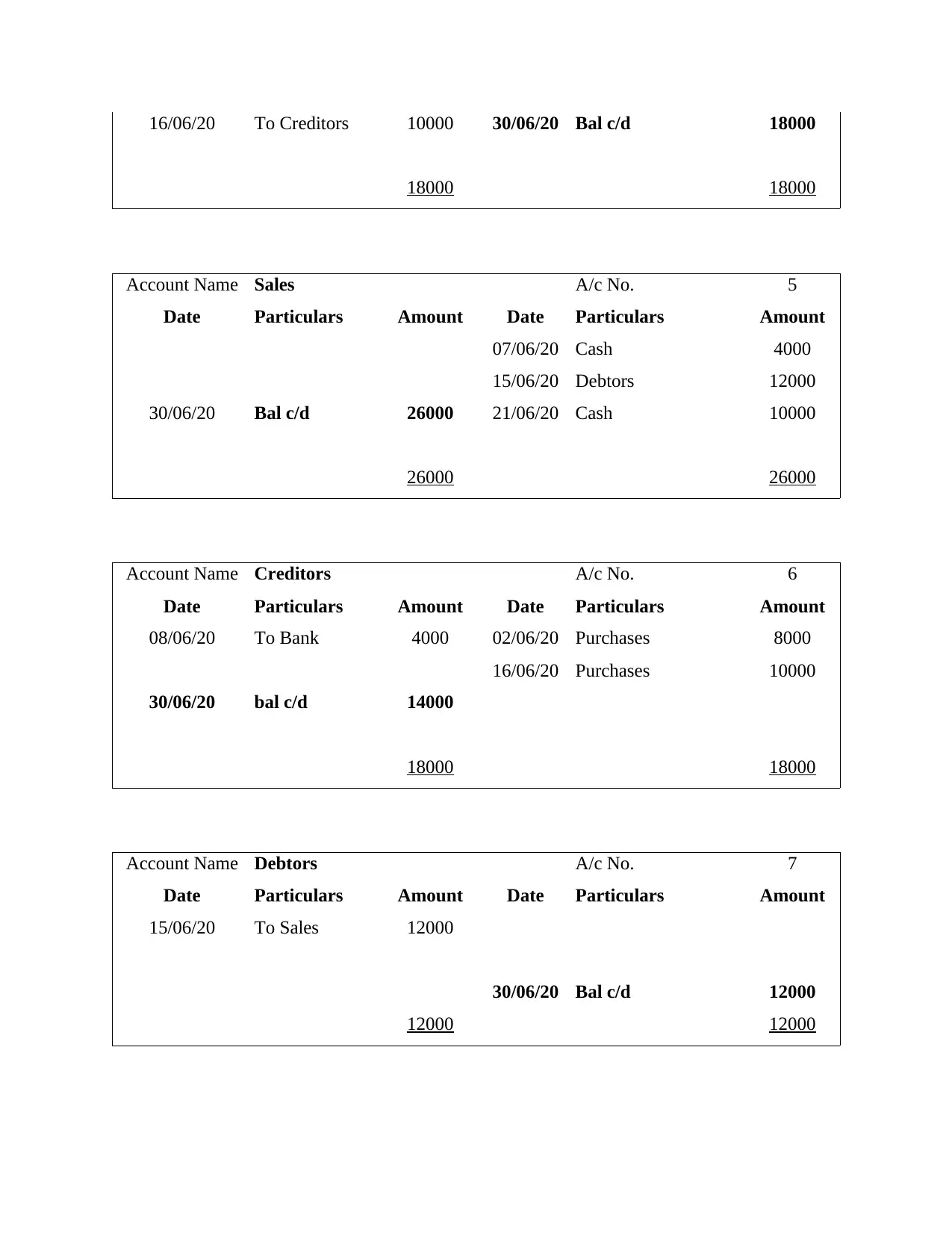

16/06/20 To Creditors 10000 30/06/20 Bal c/d 18000

18000 18000

Account Name Sales A/c No. 5

Date Particulars Amount Date Particulars Amount

07/06/20 Cash 4000

15/06/20 Debtors 12000

30/06/20 Bal c/d 26000 21/06/20 Cash 10000

26000 26000

Account Name Creditors A/c No. 6

Date Particulars Amount Date Particulars Amount

08/06/20 To Bank 4000 02/06/20 Purchases 8000

16/06/20 Purchases 10000

30/06/20 bal c/d 14000

18000 18000

Account Name Debtors A/c No. 7

Date Particulars Amount Date Particulars Amount

15/06/20 To Sales 12000

30/06/20 Bal c/d 12000

12000 12000

18000 18000

Account Name Sales A/c No. 5

Date Particulars Amount Date Particulars Amount

07/06/20 Cash 4000

15/06/20 Debtors 12000

30/06/20 Bal c/d 26000 21/06/20 Cash 10000

26000 26000

Account Name Creditors A/c No. 6

Date Particulars Amount Date Particulars Amount

08/06/20 To Bank 4000 02/06/20 Purchases 8000

16/06/20 Purchases 10000

30/06/20 bal c/d 14000

18000 18000

Account Name Debtors A/c No. 7

Date Particulars Amount Date Particulars Amount

15/06/20 To Sales 12000

30/06/20 Bal c/d 12000

12000 12000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

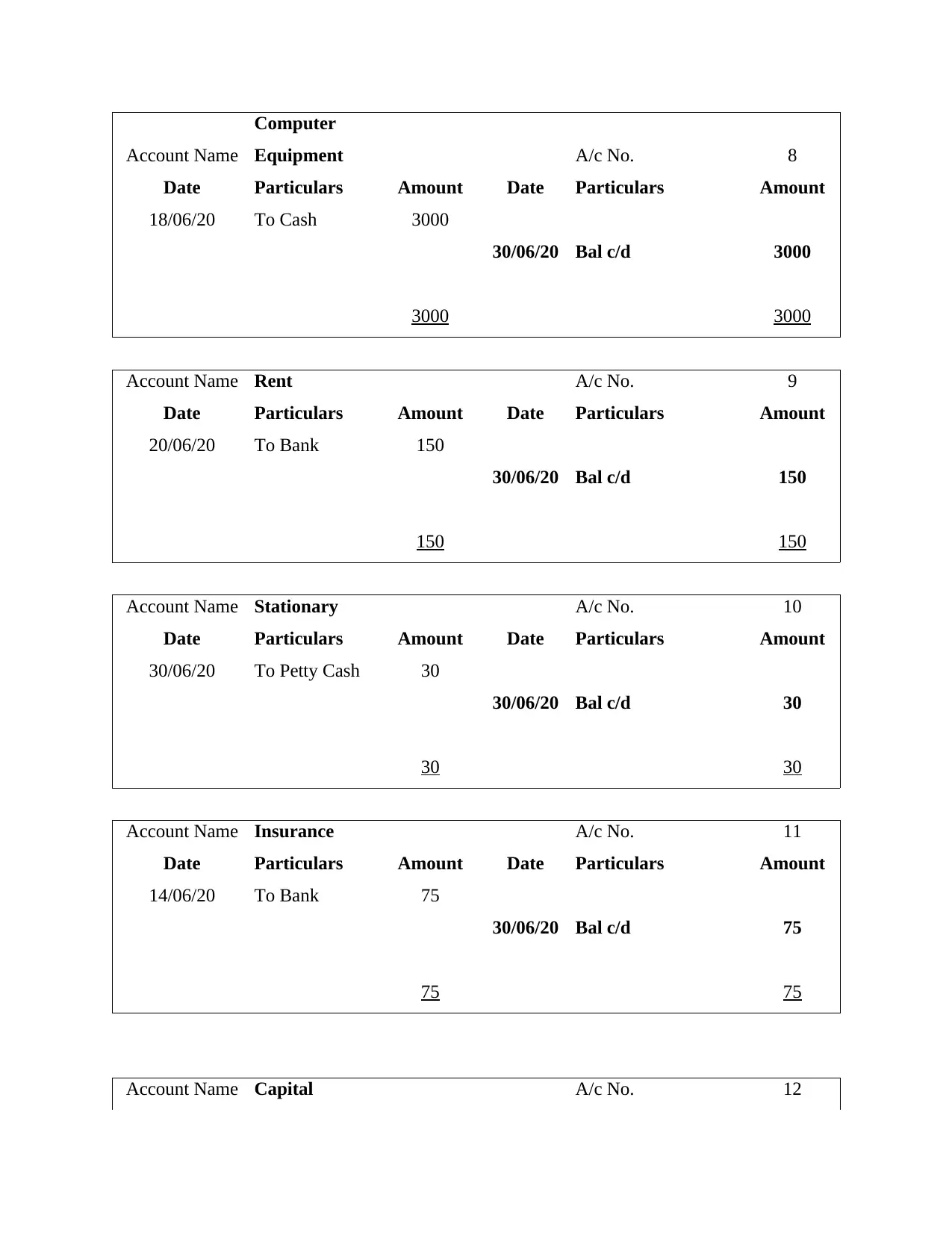

Account Name

Computer

Equipment A/c No. 8

Date Particulars Amount Date Particulars Amount

18/06/20 To Cash 3000

30/06/20 Bal c/d 3000

3000 3000

Account Name Rent A/c No. 9

Date Particulars Amount Date Particulars Amount

20/06/20 To Bank 150

30/06/20 Bal c/d 150

150 150

Account Name Stationary A/c No. 10

Date Particulars Amount Date Particulars Amount

30/06/20 To Petty Cash 30

30/06/20 Bal c/d 30

30 30

Account Name Insurance A/c No. 11

Date Particulars Amount Date Particulars Amount

14/06/20 To Bank 75

30/06/20 Bal c/d 75

75 75

Account Name Capital A/c No. 12

Computer

Equipment A/c No. 8

Date Particulars Amount Date Particulars Amount

18/06/20 To Cash 3000

30/06/20 Bal c/d 3000

3000 3000

Account Name Rent A/c No. 9

Date Particulars Amount Date Particulars Amount

20/06/20 To Bank 150

30/06/20 Bal c/d 150

150 150

Account Name Stationary A/c No. 10

Date Particulars Amount Date Particulars Amount

30/06/20 To Petty Cash 30

30/06/20 Bal c/d 30

30 30

Account Name Insurance A/c No. 11

Date Particulars Amount Date Particulars Amount

14/06/20 To Bank 75

30/06/20 Bal c/d 75

75 75

Account Name Capital A/c No. 12

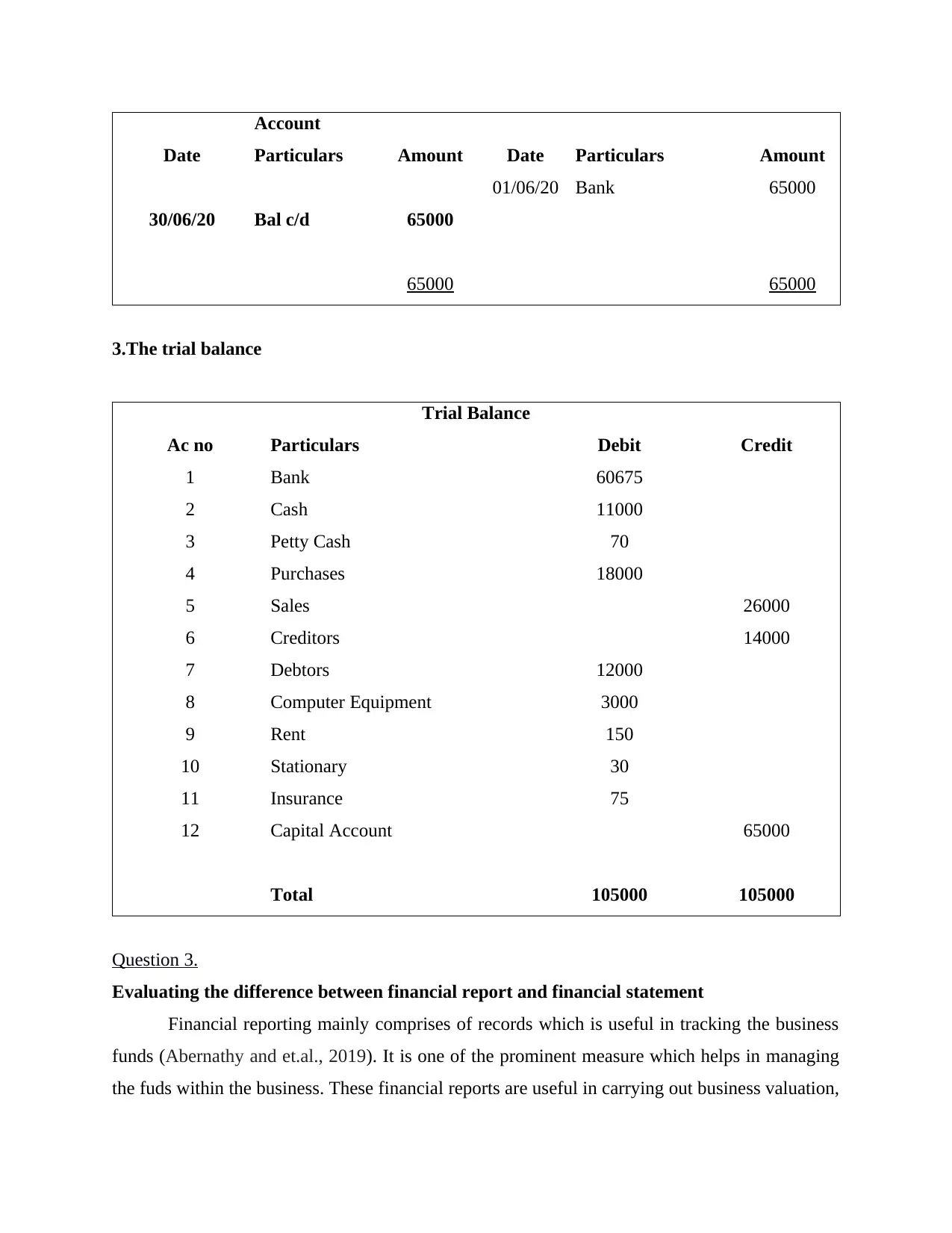

Account

Date Particulars Amount Date Particulars Amount

01/06/20 Bank 65000

30/06/20 Bal c/d 65000

65000 65000

3.The trial balance

Trial Balance

Ac no Particulars Debit Credit

1 Bank 60675

2 Cash 11000

3 Petty Cash 70

4 Purchases 18000

5 Sales 26000

6 Creditors 14000

7 Debtors 12000

8 Computer Equipment 3000

9 Rent 150

10 Stationary 30

11 Insurance 75

12 Capital Account 65000

Total 105000 105000

Question 3.

Evaluating the difference between financial report and financial statement

Financial reporting mainly comprises of records which is useful in tracking the business

funds (Abernathy and et.al., 2019). It is one of the prominent measure which helps in managing

the fuds within the business. These financial reports are useful in carrying out business valuation,

Date Particulars Amount Date Particulars Amount

01/06/20 Bank 65000

30/06/20 Bal c/d 65000

65000 65000

3.The trial balance

Trial Balance

Ac no Particulars Debit Credit

1 Bank 60675

2 Cash 11000

3 Petty Cash 70

4 Purchases 18000

5 Sales 26000

6 Creditors 14000

7 Debtors 12000

8 Computer Equipment 3000

9 Rent 150

10 Stationary 30

11 Insurance 75

12 Capital Account 65000

Total 105000 105000

Question 3.

Evaluating the difference between financial report and financial statement

Financial reporting mainly comprises of records which is useful in tracking the business

funds (Abernathy and et.al., 2019). It is one of the prominent measure which helps in managing

the fuds within the business. These financial reports are useful in carrying out business valuation,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

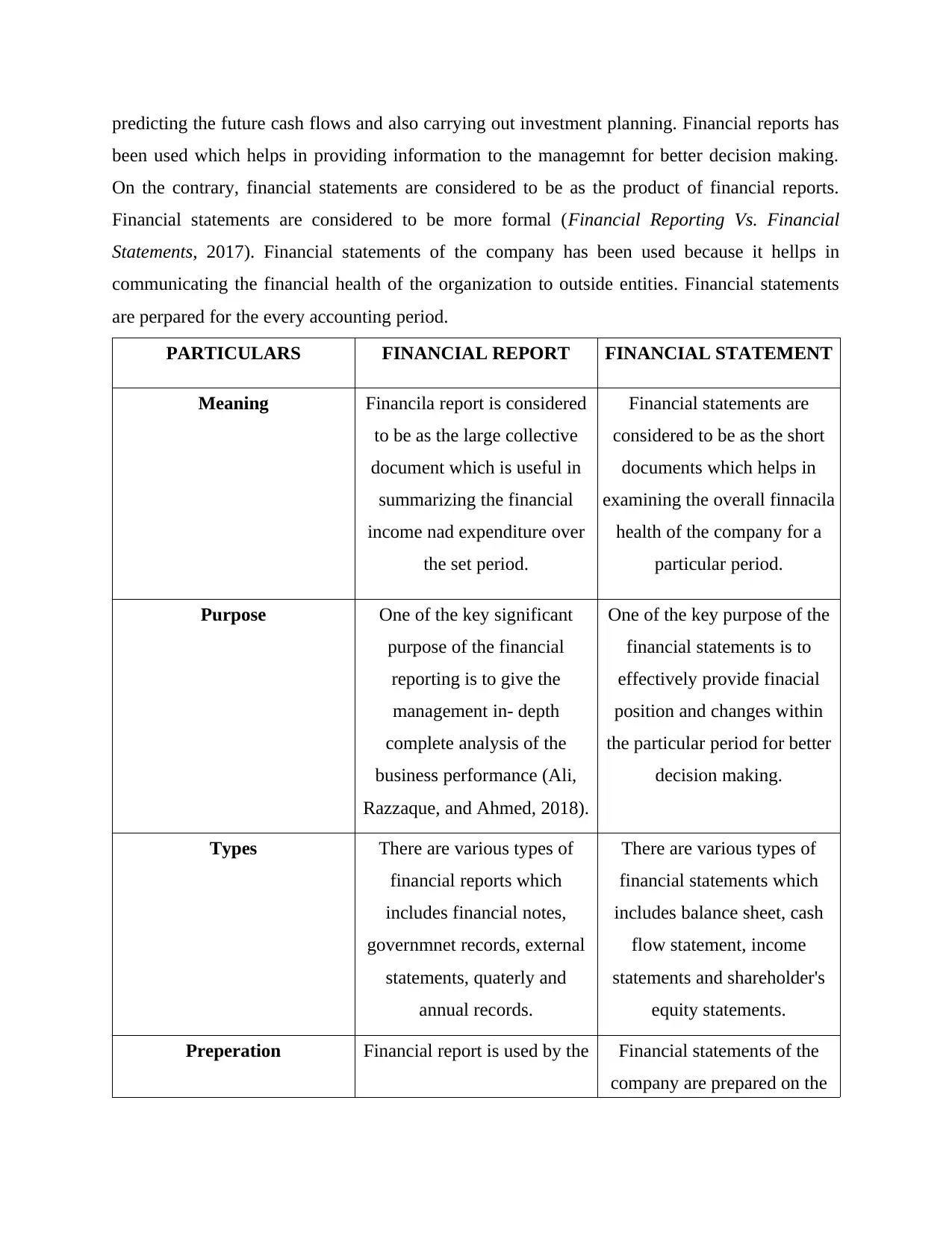

predicting the future cash flows and also carrying out investment planning. Financial reports has

been used which helps in providing information to the managemnt for better decision making.

On the contrary, financial statements are considered to be as the product of financial reports.

Financial statements are considered to be more formal (Financial Reporting Vs. Financial

Statements, 2017). Financial statements of the company has been used because it hellps in

communicating the financial health of the organization to outside entities. Financial statements

are perpared for the every accounting period.

PARTICULARS FINANCIAL REPORT FINANCIAL STATEMENT

Meaning Financila report is considered

to be as the large collective

document which is useful in

summarizing the financial

income nad expenditure over

the set period.

Financial statements are

considered to be as the short

documents which helps in

examining the overall finnacila

health of the company for a

particular period.

Purpose One of the key significant

purpose of the financial

reporting is to give the

management in- depth

complete analysis of the

business performance (Ali,

Razzaque, and Ahmed, 2018).

One of the key purpose of the

financial statements is to

effectively provide finacial

position and changes within

the particular period for better

decision making.

Types There are various types of

financial reports which

includes financial notes,

governmnet records, external

statements, quaterly and

annual records.

There are various types of

financial statements which

includes balance sheet, cash

flow statement, income

statements and shareholder's

equity statements.

Preperation Financial report is used by the Financial statements of the

company are prepared on the

been used which helps in providing information to the managemnt for better decision making.

On the contrary, financial statements are considered to be as the product of financial reports.

Financial statements are considered to be more formal (Financial Reporting Vs. Financial

Statements, 2017). Financial statements of the company has been used because it hellps in

communicating the financial health of the organization to outside entities. Financial statements

are perpared for the every accounting period.

PARTICULARS FINANCIAL REPORT FINANCIAL STATEMENT

Meaning Financila report is considered

to be as the large collective

document which is useful in

summarizing the financial

income nad expenditure over

the set period.

Financial statements are

considered to be as the short

documents which helps in

examining the overall finnacila

health of the company for a

particular period.

Purpose One of the key significant

purpose of the financial

reporting is to give the

management in- depth

complete analysis of the

business performance (Ali,

Razzaque, and Ahmed, 2018).

One of the key purpose of the

financial statements is to

effectively provide finacial

position and changes within

the particular period for better

decision making.

Types There are various types of

financial reports which

includes financial notes,

governmnet records, external

statements, quaterly and

annual records.

There are various types of

financial statements which

includes balance sheet, cash

flow statement, income

statements and shareholder's

equity statements.

Preperation Financial report is used by the Financial statements of the

company are prepared on the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

regular basis at an equal

intervals.

Financila reports play one of the key significant role in which helps in transmitting key

relevant information outise and inside of the company. It helps in providing the complete net

worth of the company by examining the expenses and spending. Financial statements are

prepared effectively for the specific accounting period (Agustiningsih, Murni and Putri, 2017).

This way it helps the management in properly taking decision by effectively managing the funds

of the company. It is useful in managing the dund flows and cash flows of the company.

Question 4.

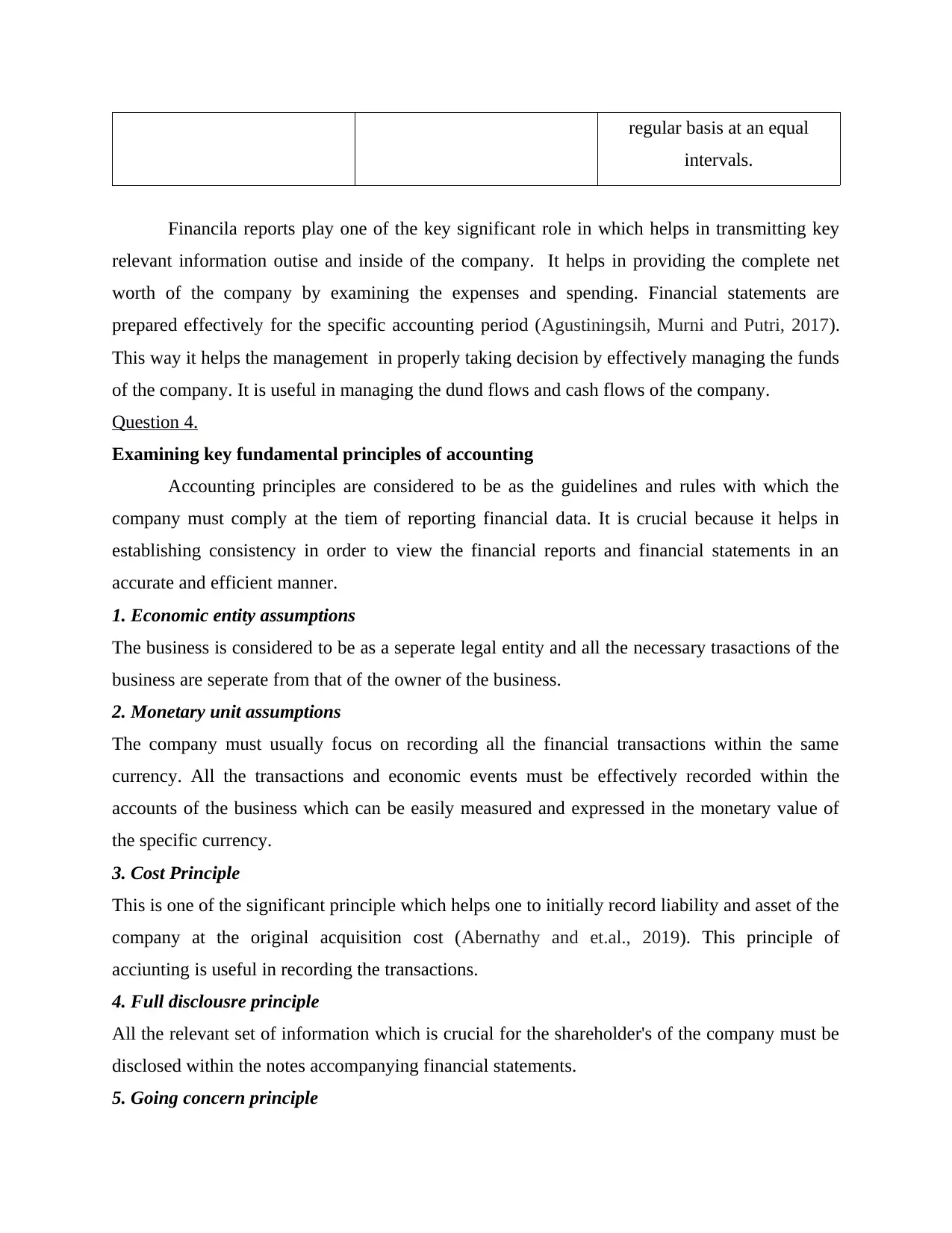

Examining key fundamental principles of accounting

Accounting principles are considered to be as the guidelines and rules with which the

company must comply at the tiem of reporting financial data. It is crucial because it helps in

establishing consistency in order to view the financial reports and financial statements in an

accurate and efficient manner.

1. Economic entity assumptions

The business is considered to be as a seperate legal entity and all the necessary trasactions of the

business are seperate from that of the owner of the business.

2. Monetary unit assumptions

The company must usually focus on recording all the financial transactions within the same

currency. All the transactions and economic events must be effectively recorded within the

accounts of the business which can be easily measured and expressed in the monetary value of

the specific currency.

3. Cost Principle

This is one of the significant principle which helps one to initially record liability and asset of the

company at the original acquisition cost (Abernathy and et.al., 2019). This principle of

acciunting is useful in recording the transactions.

4. Full disclousre principle

All the relevant set of information which is crucial for the shareholder's of the company must be

disclosed within the notes accompanying financial statements.

5. Going concern principle

intervals.

Financila reports play one of the key significant role in which helps in transmitting key

relevant information outise and inside of the company. It helps in providing the complete net

worth of the company by examining the expenses and spending. Financial statements are

prepared effectively for the specific accounting period (Agustiningsih, Murni and Putri, 2017).

This way it helps the management in properly taking decision by effectively managing the funds

of the company. It is useful in managing the dund flows and cash flows of the company.

Question 4.

Examining key fundamental principles of accounting

Accounting principles are considered to be as the guidelines and rules with which the

company must comply at the tiem of reporting financial data. It is crucial because it helps in

establishing consistency in order to view the financial reports and financial statements in an

accurate and efficient manner.

1. Economic entity assumptions

The business is considered to be as a seperate legal entity and all the necessary trasactions of the

business are seperate from that of the owner of the business.

2. Monetary unit assumptions

The company must usually focus on recording all the financial transactions within the same

currency. All the transactions and economic events must be effectively recorded within the

accounts of the business which can be easily measured and expressed in the monetary value of

the specific currency.

3. Cost Principle

This is one of the significant principle which helps one to initially record liability and asset of the

company at the original acquisition cost (Abernathy and et.al., 2019). This principle of

acciunting is useful in recording the transactions.

4. Full disclousre principle

All the relevant set of information which is crucial for the shareholder's of the company must be

disclosed within the notes accompanying financial statements.

5. Going concern principle

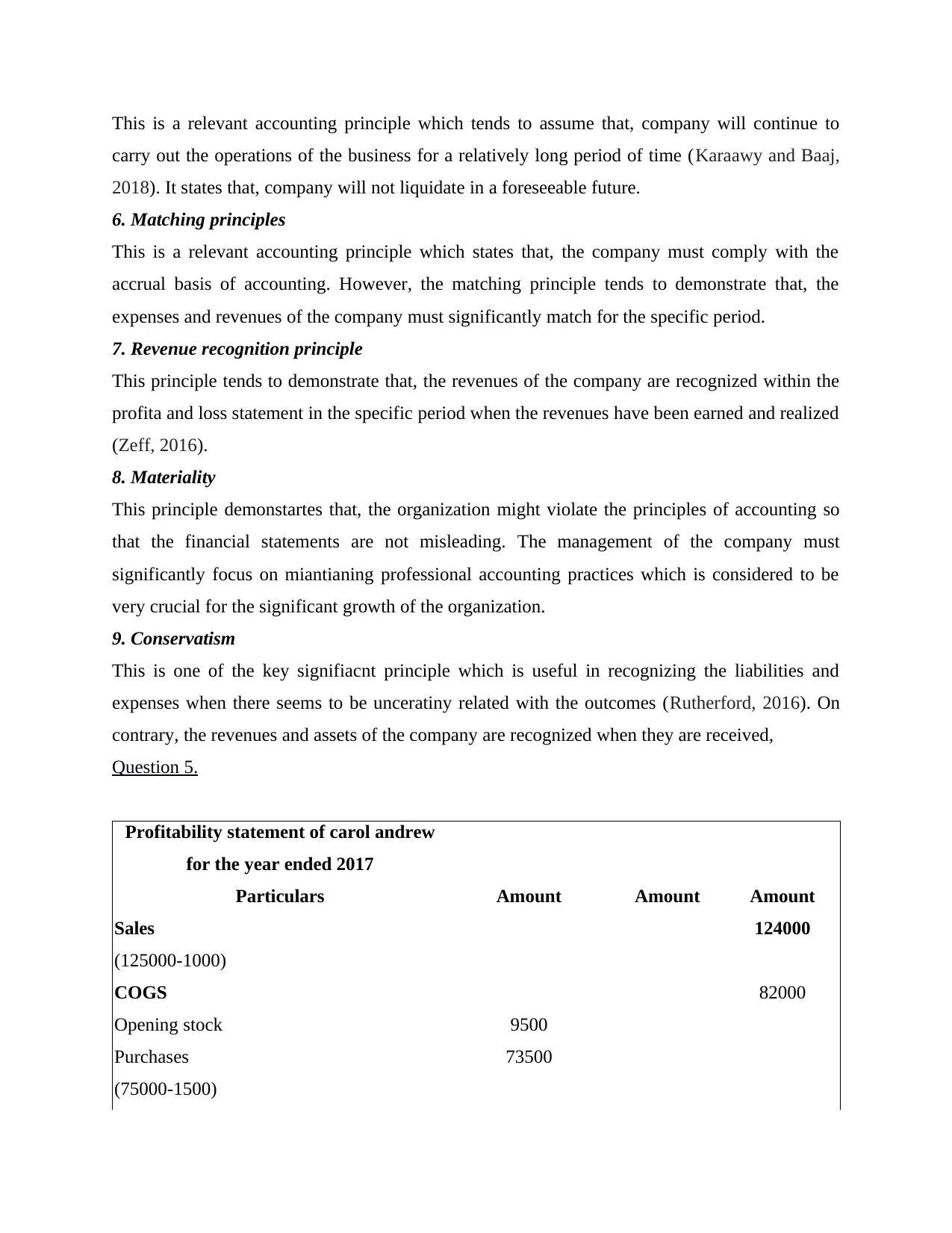

This is a relevant accounting principle which tends to assume that, company will continue to

carry out the operations of the business for a relatively long period of time (Karaawy and Baaj,

2018). It states that, company will not liquidate in a foreseeable future.

6. Matching principles

This is a relevant accounting principle which states that, the company must comply with the

accrual basis of accounting. However, the matching principle tends to demonstrate that, the

expenses and revenues of the company must significantly match for the specific period.

7. Revenue recognition principle

This principle tends to demonstrate that, the revenues of the company are recognized within the

profita and loss statement in the specific period when the revenues have been earned and realized

(Zeff, 2016).

8. Materiality

This principle demonstartes that, the organization might violate the principles of accounting so

that the financial statements are not misleading. The management of the company must

significantly focus on miantianing professional accounting practices which is considered to be

very crucial for the significant growth of the organization.

9. Conservatism

This is one of the key signifiacnt principle which is useful in recognizing the liabilities and

expenses when there seems to be unceratiny related with the outcomes (Rutherford, 2016). On

contrary, the revenues and assets of the company are recognized when they are received,

Question 5.

Profitability statement of carol andrew

for the year ended 2017

Particulars Amount Amount Amount

Sales 124000

(125000-1000)

COGS 82000

Opening stock 9500

Purchases 73500

(75000-1500)

carry out the operations of the business for a relatively long period of time (Karaawy and Baaj,

2018). It states that, company will not liquidate in a foreseeable future.

6. Matching principles

This is a relevant accounting principle which states that, the company must comply with the

accrual basis of accounting. However, the matching principle tends to demonstrate that, the

expenses and revenues of the company must significantly match for the specific period.

7. Revenue recognition principle

This principle tends to demonstrate that, the revenues of the company are recognized within the

profita and loss statement in the specific period when the revenues have been earned and realized

(Zeff, 2016).

8. Materiality

This principle demonstartes that, the organization might violate the principles of accounting so

that the financial statements are not misleading. The management of the company must

significantly focus on miantianing professional accounting practices which is considered to be

very crucial for the significant growth of the organization.

9. Conservatism

This is one of the key signifiacnt principle which is useful in recognizing the liabilities and

expenses when there seems to be unceratiny related with the outcomes (Rutherford, 2016). On

contrary, the revenues and assets of the company are recognized when they are received,

Question 5.

Profitability statement of carol andrew

for the year ended 2017

Particulars Amount Amount Amount

Sales 124000

(125000-1000)

COGS 82000

Opening stock 9500

Purchases 73500

(75000-1500)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.