Financial Accounting Report: Revenue, Consolidation and Reporting

VerifiedAdded on 2022/12/27

|14

|2916

|416

Report

AI Summary

This financial accounting report, prepared by a student, addresses several key concepts in financial reporting. It begins with revenue recognition, discussing the criteria for recognizing income and the application of IAS 11 Construction Contracts. The report then moves on to consolidated financial statements, explaining their purpose, the concept of non-controlling interest, and the principles governing their preparation. It provides detailed working notes and a consolidated statement of financial position, along with a consolidated statement of profit or loss. The report further explores foreign currency translation, differentiating between local, functional, and presentation currencies and outlining various translation methods. Finally, it touches upon approaches to corporate reporting, including the integrated reporting framework, emphasizing its role in presenting financial information effectively. The report incorporates practical examples and references relevant accounting standards to illustrate the discussed concepts.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question 1................................................................................................................2

Answer to Question 2................................................................................................................2

Working Notes.......................................................................................................................2

Consolidated Financial Statement of P CO...........................................................................3

Answer to Question 3................................................................................................................4

Purpose of Preparing Consolidated Financial Statements.....................................................4

Non-Controlling Interest.......................................................................................................4

Principles of Consolidated Financial Statements..................................................................5

Consolidated Financial Statement.........................................................................................6

Answer to Question 4................................................................................................................6

Translation of Foreign Currency...........................................................................................7

Answer to Question 5................................................................................................................8

Approaches for Corporate Reporting....................................................................................8

Integrated Reporting Framework..........................................................................................9

Analysis of the Article.........................................................................................................10

Reference.................................................................................................................................12

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question 1................................................................................................................2

Answer to Question 2................................................................................................................2

Working Notes.......................................................................................................................2

Consolidated Financial Statement of P CO...........................................................................3

Answer to Question 3................................................................................................................4

Purpose of Preparing Consolidated Financial Statements.....................................................4

Non-Controlling Interest.......................................................................................................4

Principles of Consolidated Financial Statements..................................................................5

Consolidated Financial Statement.........................................................................................6

Answer to Question 4................................................................................................................6

Translation of Foreign Currency...........................................................................................7

Answer to Question 5................................................................................................................8

Approaches for Corporate Reporting....................................................................................8

Integrated Reporting Framework..........................................................................................9

Analysis of the Article.........................................................................................................10

Reference.................................................................................................................................12

2

FINANCIAL ACCOUNTING

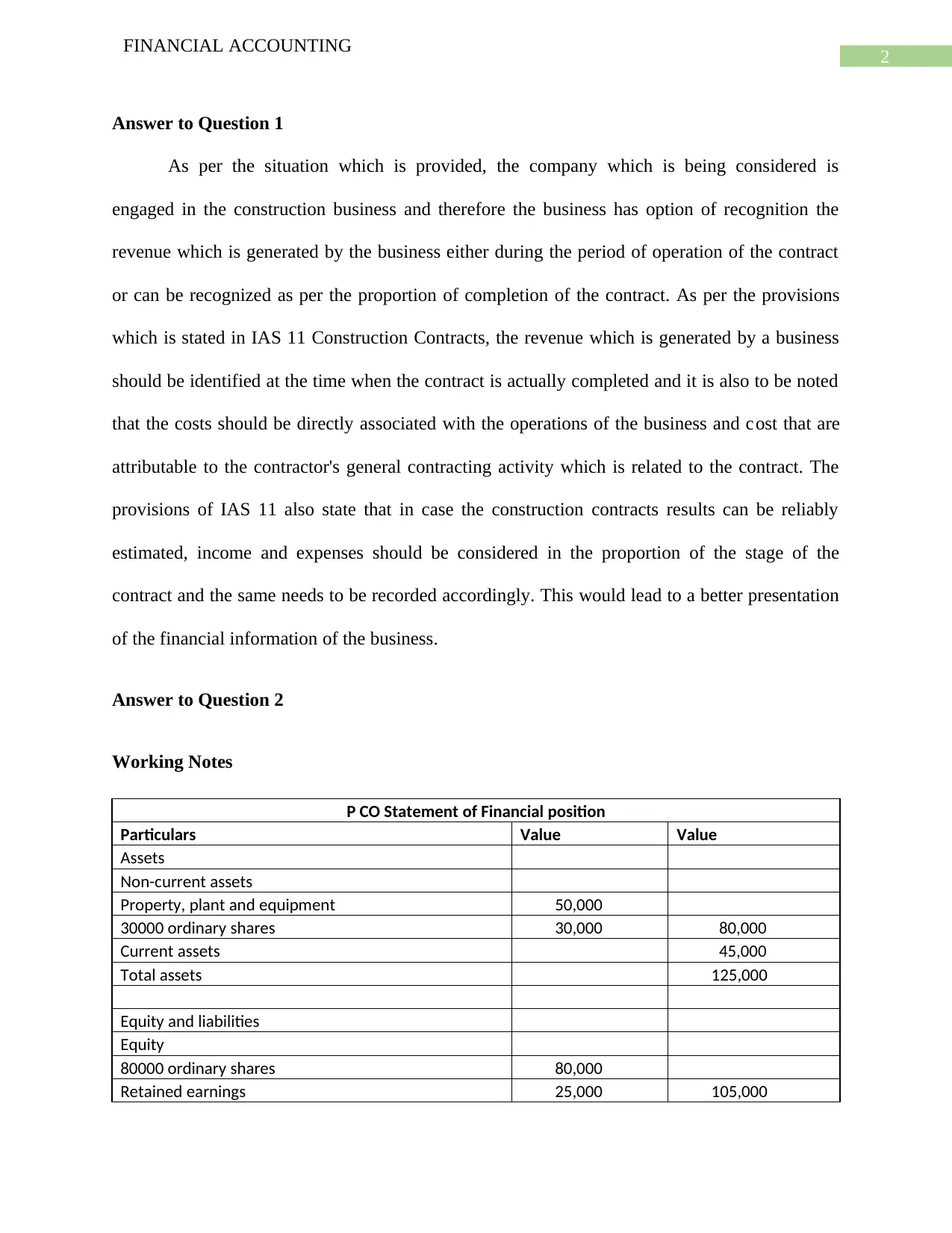

Answer to Question 1

As per the situation which is provided, the company which is being considered is

engaged in the construction business and therefore the business has option of recognition the

revenue which is generated by the business either during the period of operation of the contract

or can be recognized as per the proportion of completion of the contract. As per the provisions

which is stated in IAS 11 Construction Contracts, the revenue which is generated by a business

should be identified at the time when the contract is actually completed and it is also to be noted

that the costs should be directly associated with the operations of the business and cost that are

attributable to the contractor's general contracting activity which is related to the contract. The

provisions of IAS 11 also state that in case the construction contracts results can be reliably

estimated, income and expenses should be considered in the proportion of the stage of the

contract and the same needs to be recorded accordingly. This would lead to a better presentation

of the financial information of the business.

Answer to Question 2

Working Notes

P CO Statement of Financial position

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 50,000

30000 ordinary shares 30,000 80,000

Current assets 45,000

Total assets 125,000

Equity and liabilities

Equity

80000 ordinary shares 80,000

Retained earnings 25,000 105,000

FINANCIAL ACCOUNTING

Answer to Question 1

As per the situation which is provided, the company which is being considered is

engaged in the construction business and therefore the business has option of recognition the

revenue which is generated by the business either during the period of operation of the contract

or can be recognized as per the proportion of completion of the contract. As per the provisions

which is stated in IAS 11 Construction Contracts, the revenue which is generated by a business

should be identified at the time when the contract is actually completed and it is also to be noted

that the costs should be directly associated with the operations of the business and cost that are

attributable to the contractor's general contracting activity which is related to the contract. The

provisions of IAS 11 also state that in case the construction contracts results can be reliably

estimated, income and expenses should be considered in the proportion of the stage of the

contract and the same needs to be recorded accordingly. This would lead to a better presentation

of the financial information of the business.

Answer to Question 2

Working Notes

P CO Statement of Financial position

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 50,000

30000 ordinary shares 30,000 80,000

Current assets 45,000

Total assets 125,000

Equity and liabilities

Equity

80000 ordinary shares 80,000

Retained earnings 25,000 105,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL ACCOUNTING

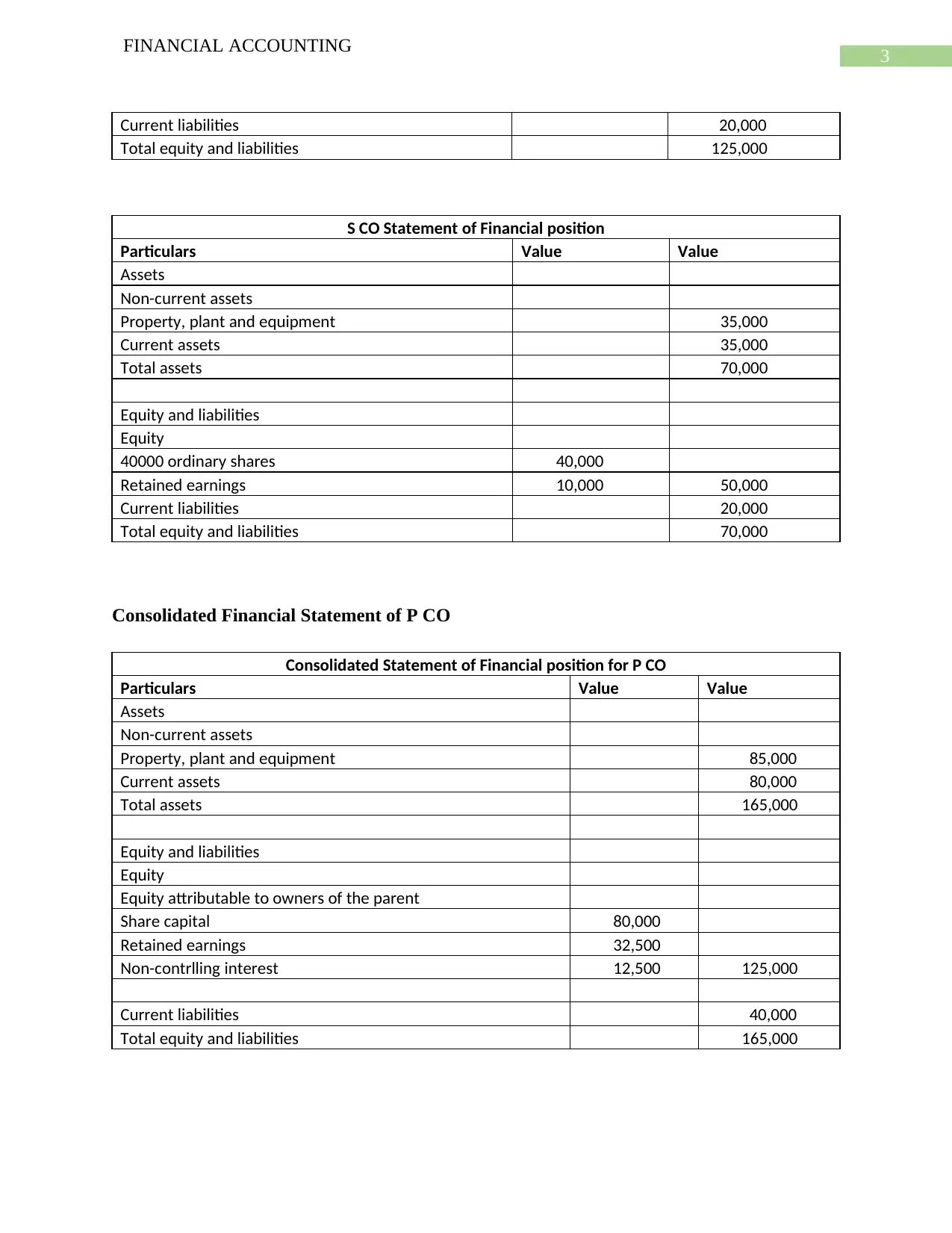

Current liabilities 20,000

Total equity and liabilities 125,000

S CO Statement of Financial position

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 35,000

Current assets 35,000

Total assets 70,000

Equity and liabilities

Equity

40000 ordinary shares 40,000

Retained earnings 10,000 50,000

Current liabilities 20,000

Total equity and liabilities 70,000

Consolidated Financial Statement of P CO

Consolidated Statement of Financial position for P CO

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 85,000

Current assets 80,000

Total assets 165,000

Equity and liabilities

Equity

Equity attributable to owners of the parent

Share capital 80,000

Retained earnings 32,500

Non-contrlling interest 12,500 125,000

Current liabilities 40,000

Total equity and liabilities 165,000

FINANCIAL ACCOUNTING

Current liabilities 20,000

Total equity and liabilities 125,000

S CO Statement of Financial position

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 35,000

Current assets 35,000

Total assets 70,000

Equity and liabilities

Equity

40000 ordinary shares 40,000

Retained earnings 10,000 50,000

Current liabilities 20,000

Total equity and liabilities 70,000

Consolidated Financial Statement of P CO

Consolidated Statement of Financial position for P CO

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 85,000

Current assets 80,000

Total assets 165,000

Equity and liabilities

Equity

Equity attributable to owners of the parent

Share capital 80,000

Retained earnings 32,500

Non-contrlling interest 12,500 125,000

Current liabilities 40,000

Total equity and liabilities 165,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL ACCOUNTING

Answer to Question 3

Purpose of Preparing Consolidated Financial Statements

The financial statements are considered to be important statements which reports about

the financial performance of a business during a period. The financial statement is prepared

following a generally accepted framework of reporting. It is on the basis of these reports that the

investors of a business decide whether or not to invest in a business. In certain cases, business

merge or is acquired by another business and for such entities in order to effectively represent the

financial position of the business a consolidated financial statement is prepared by the

management of a company. It is to be noted that business enter in a merger or acquisition process

in order to strengthen the process of the business and also for the purpose of acquiring synergy

effect in the business. The main purpose which can be identified for the preparation of the

consolidated financial statement is to effectively present the financial information of both the

companies in appropriate format and also demonstrate the financial position of the parent

company after the consolidation process is completed for the business (Müller 2014). Therefore,

it is imperative that management of the parent company effectively shows the financial position

of the parent company after merger or acquisition. The consolidated financial statements are

prepared and presented in order to provide full disclosures regarding how the business has

benefitted from merger or acquisition of another business. The consolidated financial statements

provide full information of both the companies and also shows the positive effects of merger or

acquisition on the company.

FINANCIAL ACCOUNTING

Answer to Question 3

Purpose of Preparing Consolidated Financial Statements

The financial statements are considered to be important statements which reports about

the financial performance of a business during a period. The financial statement is prepared

following a generally accepted framework of reporting. It is on the basis of these reports that the

investors of a business decide whether or not to invest in a business. In certain cases, business

merge or is acquired by another business and for such entities in order to effectively represent the

financial position of the business a consolidated financial statement is prepared by the

management of a company. It is to be noted that business enter in a merger or acquisition process

in order to strengthen the process of the business and also for the purpose of acquiring synergy

effect in the business. The main purpose which can be identified for the preparation of the

consolidated financial statement is to effectively present the financial information of both the

companies in appropriate format and also demonstrate the financial position of the parent

company after the consolidation process is completed for the business (Müller 2014). Therefore,

it is imperative that management of the parent company effectively shows the financial position

of the parent company after merger or acquisition. The consolidated financial statements are

prepared and presented in order to provide full disclosures regarding how the business has

benefitted from merger or acquisition of another business. The consolidated financial statements

provide full information of both the companies and also shows the positive effects of merger or

acquisition on the company.

5

FINANCIAL ACCOUNTING

Non-Controlling Interest

A non-controlling interest can be referred to as a minority position in a business which

generally occurs after a merger or acquisition takes place of a business. In other words, non-

controlling interest reflects that group of shareholders of a company which do not own more than

50% of the total capital of the business. A non-controlling interest of a business accounts for

lower level o shareholders of the business and such shareholders of the business do not have

voting rights in the company. The non-controlling interest of a business are measured at the net

asset value of entities.

Principles of Consolidated Financial Statements

Consolidated financial statements are formulated and presented by the management of a

company with the purpose of appropriately presenting the financial information of both the

companies effectively in a summative manner (Lombrano and Zanin 2013). The key purpose

which is identified for preparing consolidated financial statement is to shown appropriate the

revenue and expenses which is generated from the current level of operations of the business. In

addition to this, the consolidated financial statements also represent the assets and liabilities of

both the companies which are involved in merger or acquisition process. The principles of

consolidated financial statements are explained below in details:

A consolidated financial statement should effectively present the financial information of

both the businesses and therefore should present a true and fair view of the financial

situation of the business.

The consolidated financial statements are prepared by the management on the basis of the

reporting framework which is followed by parent company. It is also the responsibility of

the parent company to effective present the subsidiary companies in the annual reports

FINANCIAL ACCOUNTING

Non-Controlling Interest

A non-controlling interest can be referred to as a minority position in a business which

generally occurs after a merger or acquisition takes place of a business. In other words, non-

controlling interest reflects that group of shareholders of a company which do not own more than

50% of the total capital of the business. A non-controlling interest of a business accounts for

lower level o shareholders of the business and such shareholders of the business do not have

voting rights in the company. The non-controlling interest of a business are measured at the net

asset value of entities.

Principles of Consolidated Financial Statements

Consolidated financial statements are formulated and presented by the management of a

company with the purpose of appropriately presenting the financial information of both the

companies effectively in a summative manner (Lombrano and Zanin 2013). The key purpose

which is identified for preparing consolidated financial statement is to shown appropriate the

revenue and expenses which is generated from the current level of operations of the business. In

addition to this, the consolidated financial statements also represent the assets and liabilities of

both the companies which are involved in merger or acquisition process. The principles of

consolidated financial statements are explained below in details:

A consolidated financial statement should effectively present the financial information of

both the businesses and therefore should present a true and fair view of the financial

situation of the business.

The consolidated financial statements are prepared by the management on the basis of the

reporting framework which is followed by parent company. It is also the responsibility of

the parent company to effective present the subsidiary companies in the annual reports

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL ACCOUNTING

which needs to be prepared according to the principles of GAAP and showing

appropriate disclosures for the same (Aletkin 2014).

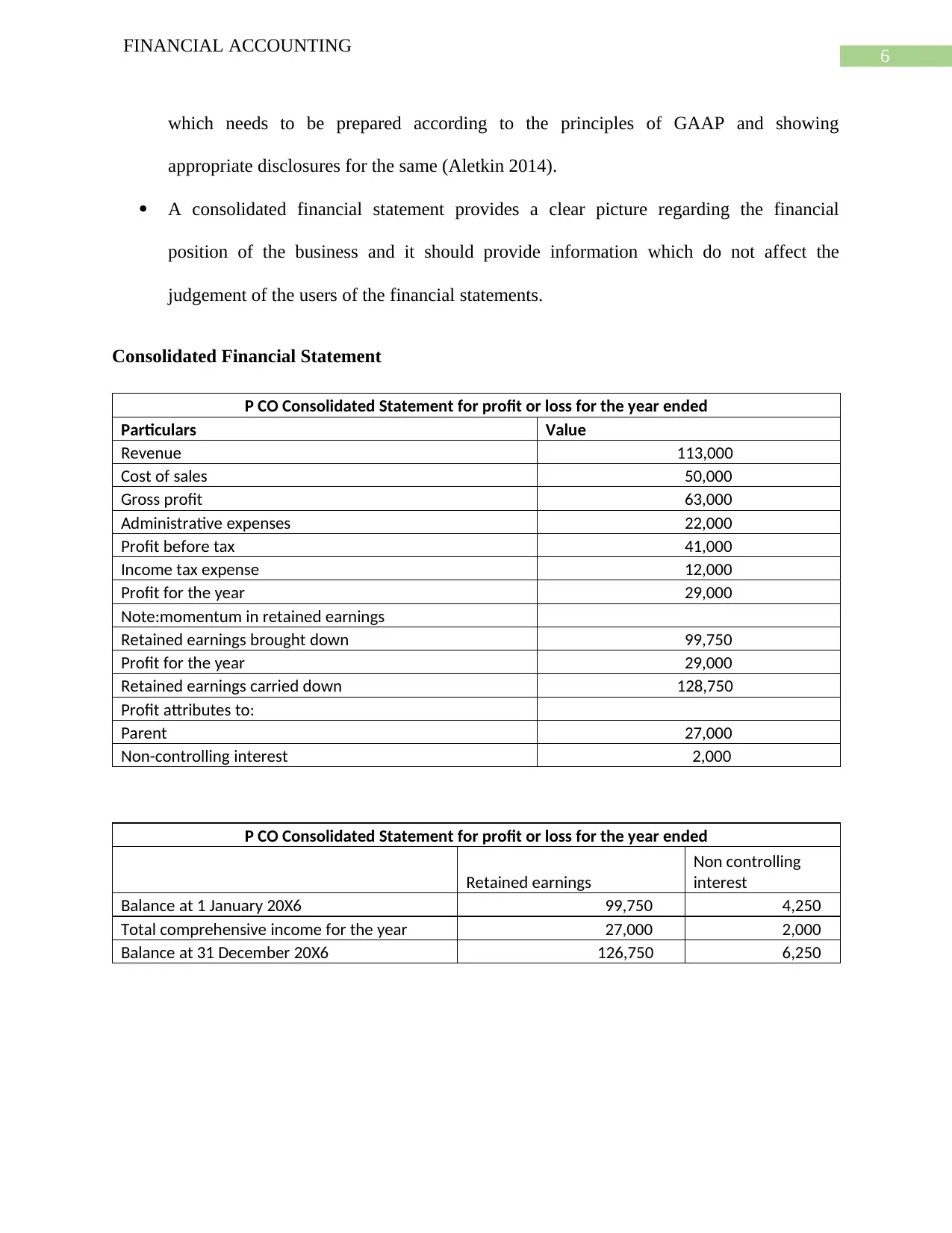

A consolidated financial statement provides a clear picture regarding the financial

position of the business and it should provide information which do not affect the

judgement of the users of the financial statements.

Consolidated Financial Statement

P CO Consolidated Statement for profit or loss for the year ended

Particulars Value

Revenue 113,000

Cost of sales 50,000

Gross profit 63,000

Administrative expenses 22,000

Profit before tax 41,000

Income tax expense 12,000

Profit for the year 29,000

Note:momentum in retained earnings

Retained earnings brought down 99,750

Profit for the year 29,000

Retained earnings carried down 128,750

Profit attributes to:

Parent 27,000

Non-controlling interest 2,000

P CO Consolidated Statement for profit or loss for the year ended

Retained earnings

Non controlling

interest

Balance at 1 January 20X6 99,750 4,250

Total comprehensive income for the year 27,000 2,000

Balance at 31 December 20X6 126,750 6,250

FINANCIAL ACCOUNTING

which needs to be prepared according to the principles of GAAP and showing

appropriate disclosures for the same (Aletkin 2014).

A consolidated financial statement provides a clear picture regarding the financial

position of the business and it should provide information which do not affect the

judgement of the users of the financial statements.

Consolidated Financial Statement

P CO Consolidated Statement for profit or loss for the year ended

Particulars Value

Revenue 113,000

Cost of sales 50,000

Gross profit 63,000

Administrative expenses 22,000

Profit before tax 41,000

Income tax expense 12,000

Profit for the year 29,000

Note:momentum in retained earnings

Retained earnings brought down 99,750

Profit for the year 29,000

Retained earnings carried down 128,750

Profit attributes to:

Parent 27,000

Non-controlling interest 2,000

P CO Consolidated Statement for profit or loss for the year ended

Retained earnings

Non controlling

interest

Balance at 1 January 20X6 99,750 4,250

Total comprehensive income for the year 27,000 2,000

Balance at 31 December 20X6 126,750 6,250

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ACCOUNTING

Answer to Question 4

Local currency may be defined as currency which effectively helps foreign subsidiaries to

executes its business transactions. The local currency may or may not be similar to functional

currencies of a business. On the other hand, function currency refers to the currency reflects the

primary economic climate of the subsidiary’s operations and this is a currency which is

commonly associated with the term of consolidation of a business. Presentation currency refers

to the currency which is used by the entity which is formed by acquisition or merger in

preparation of the financial statements of the business (Palea 2014). The presentation currency

reflects all the financial information of a business and is mostly same as the currency which is

used in the country in which the business is operating.

Translation of Foreign Currency

In most of the companies, there is a need to translate foreign currencies when the

business trade in those currencies and when they have foreign operations that use differing

currencies. It is important for parent company to translate the currency as per the requirement of

the country in which the business is operating. There are different methods which are available to

the management of a company for effective translation of the currency for the purpose of

presenting the financial information of a business (Evers, Meier and Spengel 2014). The methods

which are used for the purpose of translation of currency for the purpose of meeting the

requirements of consolidation are given below:

Current Rate Translation Method: This method uses the functional currency concept which

relies on the current rate when the functional currency is the same as the local currency. In

this method of translation, assets and liabilities of the business utilizes current or spot

exp=change rates which is present on the date of balance sheet.

FINANCIAL ACCOUNTING

Answer to Question 4

Local currency may be defined as currency which effectively helps foreign subsidiaries to

executes its business transactions. The local currency may or may not be similar to functional

currencies of a business. On the other hand, function currency refers to the currency reflects the

primary economic climate of the subsidiary’s operations and this is a currency which is

commonly associated with the term of consolidation of a business. Presentation currency refers

to the currency which is used by the entity which is formed by acquisition or merger in

preparation of the financial statements of the business (Palea 2014). The presentation currency

reflects all the financial information of a business and is mostly same as the currency which is

used in the country in which the business is operating.

Translation of Foreign Currency

In most of the companies, there is a need to translate foreign currencies when the

business trade in those currencies and when they have foreign operations that use differing

currencies. It is important for parent company to translate the currency as per the requirement of

the country in which the business is operating. There are different methods which are available to

the management of a company for effective translation of the currency for the purpose of

presenting the financial information of a business (Evers, Meier and Spengel 2014). The methods

which are used for the purpose of translation of currency for the purpose of meeting the

requirements of consolidation are given below:

Current Rate Translation Method: This method uses the functional currency concept which

relies on the current rate when the functional currency is the same as the local currency. In

this method of translation, assets and liabilities of the business utilizes current or spot

exp=change rates which is present on the date of balance sheet.

8

FINANCIAL ACCOUNTING

Temporal Rate Translation Method: This method requires the translation process to use

temporal or historical rate method for translation and it is also to be noted that the local

currency differs from that of functional currency (De Vlaminck and Sarens 2015). Income

generating assets can be adjusted when temporal rate is used for the purpose of translation.

Monetary-Nonmonetary Translation Method: This method of translation is utilized by a

business when a foreign business operation is highly integrated with a parent company which

operates in domestic country. This method is also used by businesses when the operations of

two businesses are related to each other in a manner.

Answer to Question 5

Approaches for Corporate Reporting

The purpose of corporate reporting is to effectively present the financial information of a

business so that the same can be used by the users of financial reports to take major decision.

The four-step model which is applied for the purpose of corporate reporting of a business

involves the following steps which are explained below in details:

Principle Based approach: This is a concept which is closely followed with integrated reporting

framework of a business and requires the management of a company to follow effectively all the

principles of accounting which needs to be followed while preparing the financial statements if a

business. The reporting framework of integrated reporting has significant advantage and is

developing rapidly in businesses (Weil, Schipper and Francis 2013). The integrated reporting

framework also ensures that the financial reports which is prepared by the management of the

company effectively presents the financial information of the business by using both qualitative

and quantitative approaches. In qualitative approaches more, theoretical information is provided

FINANCIAL ACCOUNTING

Temporal Rate Translation Method: This method requires the translation process to use

temporal or historical rate method for translation and it is also to be noted that the local

currency differs from that of functional currency (De Vlaminck and Sarens 2015). Income

generating assets can be adjusted when temporal rate is used for the purpose of translation.

Monetary-Nonmonetary Translation Method: This method of translation is utilized by a

business when a foreign business operation is highly integrated with a parent company which

operates in domestic country. This method is also used by businesses when the operations of

two businesses are related to each other in a manner.

Answer to Question 5

Approaches for Corporate Reporting

The purpose of corporate reporting is to effectively present the financial information of a

business so that the same can be used by the users of financial reports to take major decision.

The four-step model which is applied for the purpose of corporate reporting of a business

involves the following steps which are explained below in details:

Principle Based approach: This is a concept which is closely followed with integrated reporting

framework of a business and requires the management of a company to follow effectively all the

principles of accounting which needs to be followed while preparing the financial statements if a

business. The reporting framework of integrated reporting has significant advantage and is

developing rapidly in businesses (Weil, Schipper and Francis 2013). The integrated reporting

framework also ensures that the financial reports which is prepared by the management of the

company effectively presents the financial information of the business by using both qualitative

and quantitative approaches. In qualitative approaches more, theoretical information is provided

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL ACCOUNTING

by the business along with representation of the management of the company. The quantitative

approaches require the management of the company to present more of numerical information in

the financial statements which is prepared by the business (Robinson et al. 2015). The

quantitative approach of presenting more information requires better presentation of and use of

forecasting techniques for making comparisons.

Integrated Reporting Framework

Integrated reporting framework is used by the management of a company for effectively

presenting financial information in a concise manner which effectively represents the strategies

of the of the business along with performance and prospect of the business. The reporting

framework is consistent with the long term, medium term and long-term strategies of the

business. The management of a company must prepare an integrated report on the basis of this

framework (Nobes 2013). The method of integrated reporting framework is utilizing principle-

based approaches for maintaining appropriate balances between flexibility and prescription that

is related to wide variations in reporting framework of the business.

The integrated reporting framework has become excessively popular over the last few years

as it effectively presents the information of the business. In addition to this, a certain level of

quality can also be maintained by following integrated reporting framework. The objectives of

integrated reporting framework which can be identified are listed below in details:

The main purpose of integrated reporting framework is to ensure that the financial

statements are prepared by the management of the company following guiding principles

and content elements that governs the overall information which is presented in the

FINANCIAL ACCOUNTING

by the business along with representation of the management of the company. The quantitative

approaches require the management of the company to present more of numerical information in

the financial statements which is prepared by the business (Robinson et al. 2015). The

quantitative approach of presenting more information requires better presentation of and use of

forecasting techniques for making comparisons.

Integrated Reporting Framework

Integrated reporting framework is used by the management of a company for effectively

presenting financial information in a concise manner which effectively represents the strategies

of the of the business along with performance and prospect of the business. The reporting

framework is consistent with the long term, medium term and long-term strategies of the

business. The management of a company must prepare an integrated report on the basis of this

framework (Nobes 2013). The method of integrated reporting framework is utilizing principle-

based approaches for maintaining appropriate balances between flexibility and prescription that

is related to wide variations in reporting framework of the business.

The integrated reporting framework has become excessively popular over the last few years

as it effectively presents the information of the business. In addition to this, a certain level of

quality can also be maintained by following integrated reporting framework. The objectives of

integrated reporting framework which can be identified are listed below in details:

The main purpose of integrated reporting framework is to ensure that the financial

statements are prepared by the management of the company following guiding principles

and content elements that governs the overall information which is presented in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL ACCOUNTING

integrated reports of the business. It is also aimed at properly explaining the fundamental

concepts which are used for presenting the financial information of the business.

The framework is basically used by the management of the company for identifying areas

where the management of the company can create values for the business and it also

reflects the ability of the business for creating value in the operations of the business.

The integrated reporting framework which is used by businesses for complying with the

expectation of the shareholders of the business. This also reflect the ability of the

business to create value in a business and the stakeholders of the business includes

employees, customers and business partners and others.

Analysis of the Article

The analysis of the article effectively shows that business of Uniqlo which is engaged in

the business of retailing business and is considered to be quite successful in the market. The

management of the company needs to follow social accountability standards 8000 so that proper

social consideration is adopted in the business (Flower 2015). The business of retailing has

suffered significantly from ethical consideration and therefore the management of the company

needs to adopt appropriate strategies so that proper management of business can be implemented.

The management of the company needs to consider the safety issues in the business along with

proper working environment is available to the workers and proper shift time is maintained for

the workers operating in the business. The management of the company also needs to ensure that

no discrimination practices takes place in the business and every employee should be treated in

an equal manner. These policies would not only improve the business structure but also improve

the profit generation ability of the business. In addition to this, this will also improve the

confidence of the public in the business.

FINANCIAL ACCOUNTING

integrated reports of the business. It is also aimed at properly explaining the fundamental

concepts which are used for presenting the financial information of the business.

The framework is basically used by the management of the company for identifying areas

where the management of the company can create values for the business and it also

reflects the ability of the business for creating value in the operations of the business.

The integrated reporting framework which is used by businesses for complying with the

expectation of the shareholders of the business. This also reflect the ability of the

business to create value in a business and the stakeholders of the business includes

employees, customers and business partners and others.

Analysis of the Article

The analysis of the article effectively shows that business of Uniqlo which is engaged in

the business of retailing business and is considered to be quite successful in the market. The

management of the company needs to follow social accountability standards 8000 so that proper

social consideration is adopted in the business (Flower 2015). The business of retailing has

suffered significantly from ethical consideration and therefore the management of the company

needs to adopt appropriate strategies so that proper management of business can be implemented.

The management of the company needs to consider the safety issues in the business along with

proper working environment is available to the workers and proper shift time is maintained for

the workers operating in the business. The management of the company also needs to ensure that

no discrimination practices takes place in the business and every employee should be treated in

an equal manner. These policies would not only improve the business structure but also improve

the profit generation ability of the business. In addition to this, this will also improve the

confidence of the public in the business.

11

FINANCIAL ACCOUNTING

As per legitimacy theory, the management of a company is bound by social

considerations and therefore the management of company must take appropriate steps for making

improvements in social contributions of the business. The management of Uniqlo needs to

consider the well beings of the employees of the business and therefore introduce rewards

systems and processes so that the employees of the business are motivated towards achieving the

long term and short term objectives of the business.

FINANCIAL ACCOUNTING

As per legitimacy theory, the management of a company is bound by social

considerations and therefore the management of company must take appropriate steps for making

improvements in social contributions of the business. The management of Uniqlo needs to

consider the well beings of the employees of the business and therefore introduce rewards

systems and processes so that the employees of the business are motivated towards achieving the

long term and short term objectives of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.