Business Finance and Accounting: Differences and Users of Information

VerifiedAdded on 2023/01/12

|7

|1428

|69

Report

AI Summary

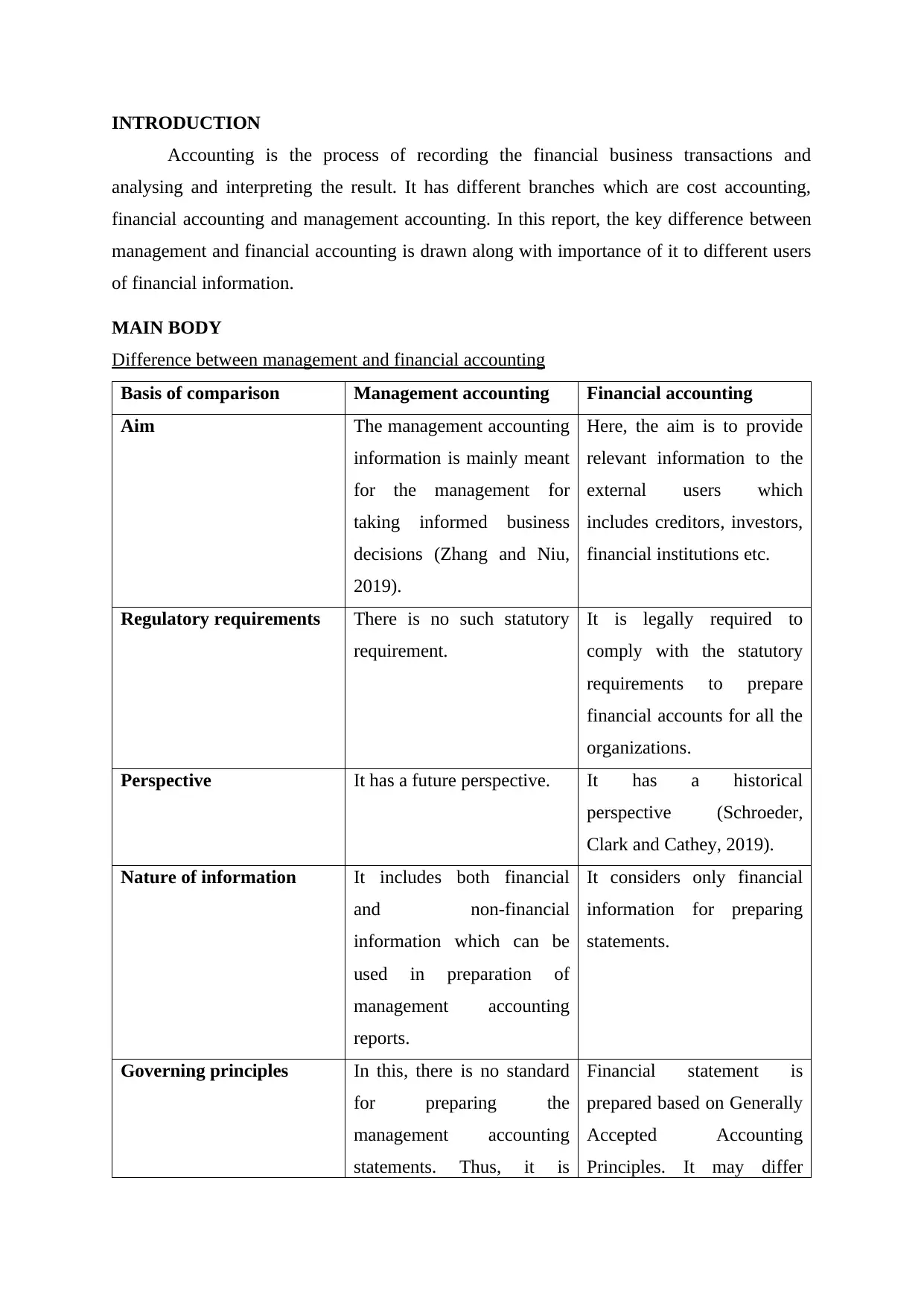

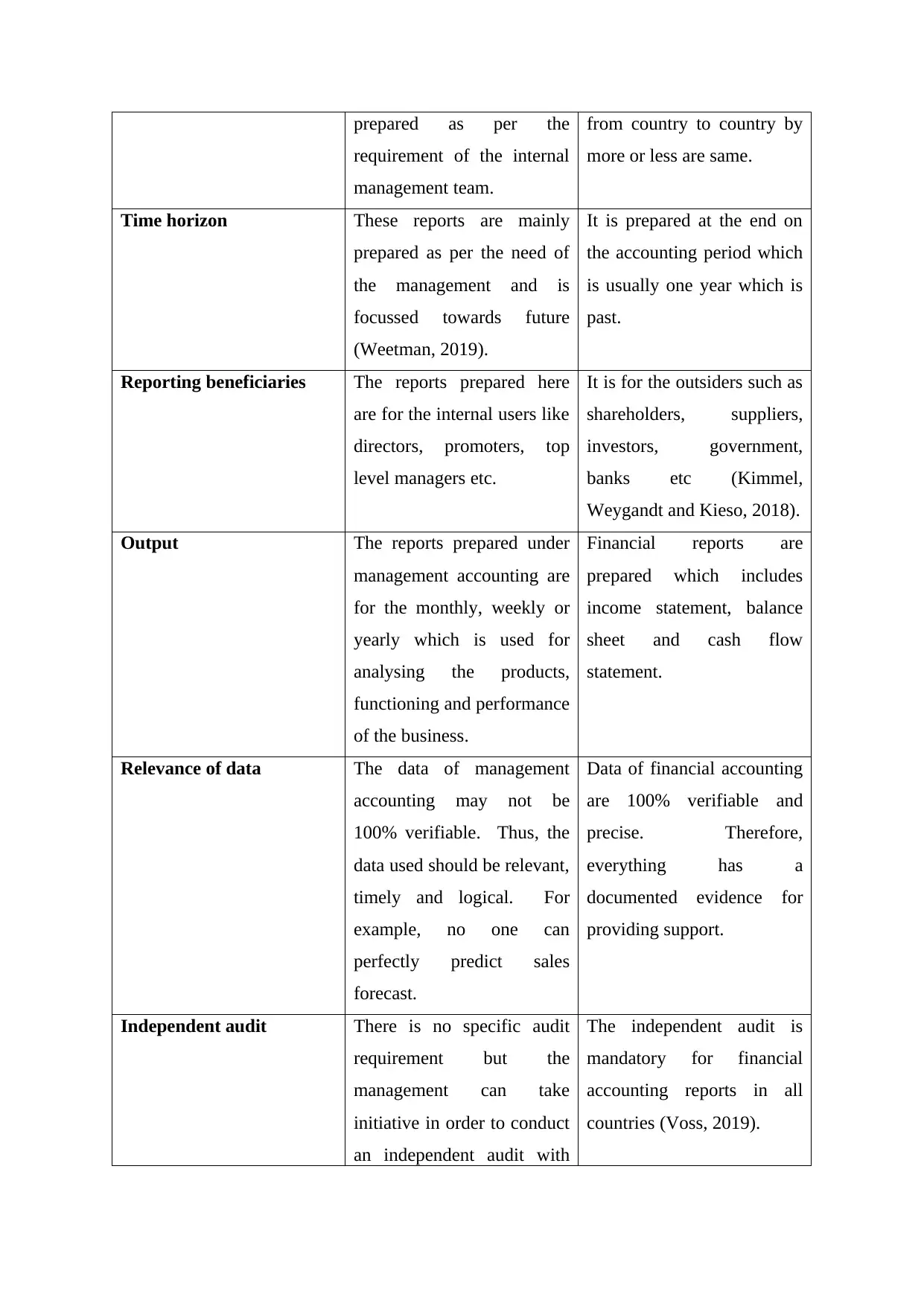

This report provides a comprehensive overview of financial and management accounting, outlining their fundamental differences, objectives, and target audiences. It begins by defining accounting and its various branches, emphasizing the distinctions between management and financial accounting. The report details the contrasting aims, regulatory requirements, perspectives, and nature of information used in each type of accounting. It also explores the different users of financial information, including investors, lenders, suppliers, customers, tax authorities, and government entities, highlighting how they utilize accounting data for decision-making. The report concludes by emphasizing the importance of both accounting systems in effectively managing a business and how they cater to diverse user needs. The report also includes a section on profit, cash flow, and working capital, explaining their differences and impacts on business operations.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.