ACCT6003: Financial Accounting Processes Assignment 2 Report

VerifiedAdded on 2023/01/05

|11

|2230

|91

Report

AI Summary

This report presents a comprehensive case study on financial accounting, addressing key concepts such as accounting for debentures, impairment of assets, and asset revaluation. Part A of the report includes detailed general journal entries for debenture transactions, impairment loss calculations, and asset revaluation scenarios, demonstrating the application of accounting principles and standards. Part B offers an in-depth analysis of raising funds through share issues versus debentures, comparing their impacts on financial accounts and highlighting the advantages of each option for a company. The report concludes with a recommendation for the company on the most suitable method of fund raising, supported by thorough research and analysis. References to relevant accounting literature are also included.

Case study report

writing / accounting

writing / accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

MAIN BODY..............................................................................................................................................3

PART A...................................................................................................................................................3

Question 1 Accounting for Debentures....................................................................................................3

Question 2 Accounting for Impairment...................................................................................................3

Question 3 Asset Revaluation..................................................................................................................5

Part B.......................................................................................................................................................6

REFERENCES..........................................................................................................................................11

MAIN BODY..............................................................................................................................................3

PART A...................................................................................................................................................3

Question 1 Accounting for Debentures....................................................................................................3

Question 2 Accounting for Impairment...................................................................................................3

Question 3 Asset Revaluation..................................................................................................................5

Part B.......................................................................................................................................................6

REFERENCES..........................................................................................................................................11

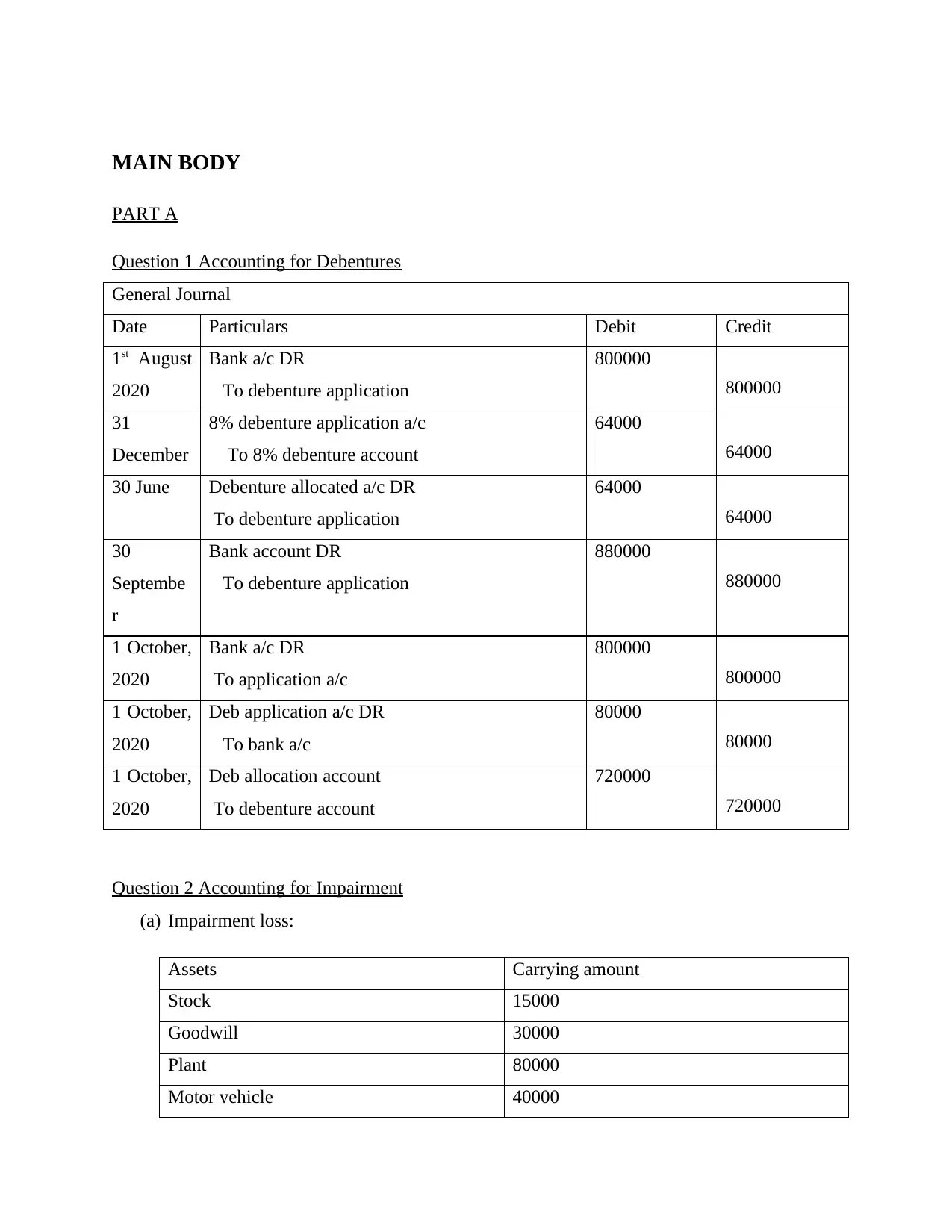

MAIN BODY

PART A

Question 1 Accounting for Debentures

General Journal

Date Particulars Debit Credit

1st August

2020

Bank a/c DR

To debenture application

800000

800000

31

December

8% debenture application a/c

To 8% debenture account

64000

64000

30 June Debenture allocated a/c DR

To debenture application

64000

64000

30

Septembe

r

Bank account DR

To debenture application

880000

880000

1 October,

2020

Bank a/c DR

To application a/c

800000

800000

1 October,

2020

Deb application a/c DR

To bank a/c

80000

80000

1 October,

2020

Deb allocation account

To debenture account

720000

720000

Question 2 Accounting for Impairment

(a) Impairment loss:

Assets Carrying amount

Stock 15000

Goodwill 30000

Plant 80000

Motor vehicle 40000

PART A

Question 1 Accounting for Debentures

General Journal

Date Particulars Debit Credit

1st August

2020

Bank a/c DR

To debenture application

800000

800000

31

December

8% debenture application a/c

To 8% debenture account

64000

64000

30 June Debenture allocated a/c DR

To debenture application

64000

64000

30

Septembe

r

Bank account DR

To debenture application

880000

880000

1 October,

2020

Bank a/c DR

To application a/c

800000

800000

1 October,

2020

Deb application a/c DR

To bank a/c

80000

80000

1 October,

2020

Deb allocation account

To debenture account

720000

720000

Question 2 Accounting for Impairment

(a) Impairment loss:

Assets Carrying amount

Stock 15000

Goodwill 30000

Plant 80000

Motor vehicle 40000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total 165000

Impairment loss: Unrecoverable amount-recoverable amount

= 165000-120000

= $45000

(b) Allocation of impairment loss:

Assets Carrying

amount

Proportion Loss allocated Adjusted

amount

Stock 15000 15/165 1363 13637

Goodwill 30000 30/165 5454 24546

Plant 80000 80/165 38787 41213

Motor vehicle 40000 40/165 9697 30303

Total 165000 55301

(c) Journal entry:

General Journal

Date Particulars Debit Credit

30 June

2020

Accumulated impairment loss a/c

To accumulated impairment loss a/c

55301

55301

30 June

2020

Accumulated impairment loss (stock) a/c

Stock a/c

To revaluation reserve (stock)

1363

13637

15000

30 June

2020

Accumulated impairment loss (vehicle) a/c

Vehicle a/c

To revaluation reserve (vehicle)

9697

30303

40000

Impairment loss: Unrecoverable amount-recoverable amount

= 165000-120000

= $45000

(b) Allocation of impairment loss:

Assets Carrying

amount

Proportion Loss allocated Adjusted

amount

Stock 15000 15/165 1363 13637

Goodwill 30000 30/165 5454 24546

Plant 80000 80/165 38787 41213

Motor vehicle 40000 40/165 9697 30303

Total 165000 55301

(c) Journal entry:

General Journal

Date Particulars Debit Credit

30 June

2020

Accumulated impairment loss a/c

To accumulated impairment loss a/c

55301

55301

30 June

2020

Accumulated impairment loss (stock) a/c

Stock a/c

To revaluation reserve (stock)

1363

13637

15000

30 June

2020

Accumulated impairment loss (vehicle) a/c

Vehicle a/c

To revaluation reserve (vehicle)

9697

30303

40000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

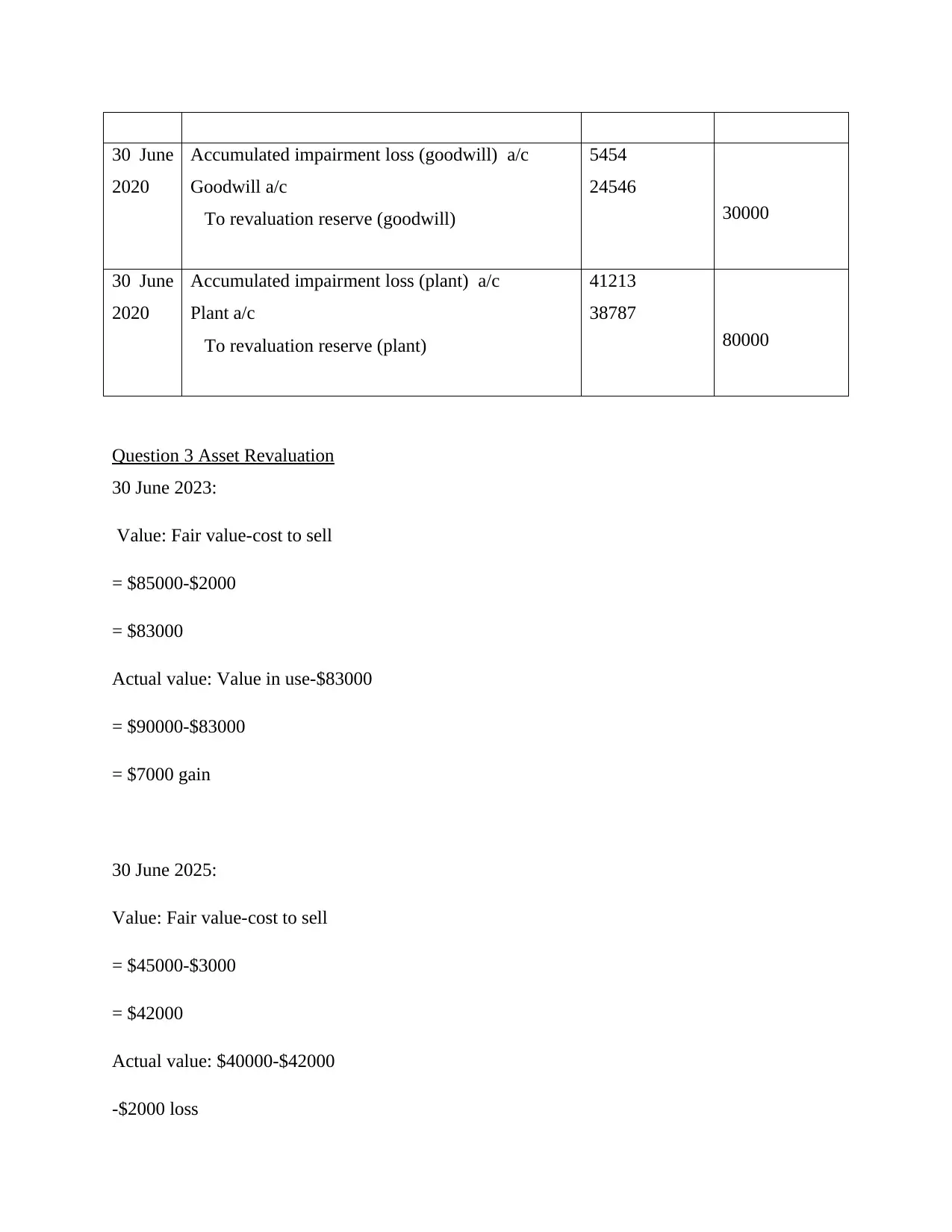

30 June

2020

Accumulated impairment loss (goodwill) a/c

Goodwill a/c

To revaluation reserve (goodwill)

5454

24546

30000

30 June

2020

Accumulated impairment loss (plant) a/c

Plant a/c

To revaluation reserve (plant)

41213

38787

80000

Question 3 Asset Revaluation

30 June 2023:

Value: Fair value-cost to sell

= $85000-$2000

= $83000

Actual value: Value in use-$83000

= $90000-$83000

= $7000 gain

30 June 2025:

Value: Fair value-cost to sell

= $45000-$3000

= $42000

Actual value: $40000-$42000

-$2000 loss

2020

Accumulated impairment loss (goodwill) a/c

Goodwill a/c

To revaluation reserve (goodwill)

5454

24546

30000

30 June

2020

Accumulated impairment loss (plant) a/c

Plant a/c

To revaluation reserve (plant)

41213

38787

80000

Question 3 Asset Revaluation

30 June 2023:

Value: Fair value-cost to sell

= $85000-$2000

= $83000

Actual value: Value in use-$83000

= $90000-$83000

= $7000 gain

30 June 2025:

Value: Fair value-cost to sell

= $45000-$3000

= $42000

Actual value: $40000-$42000

-$2000 loss

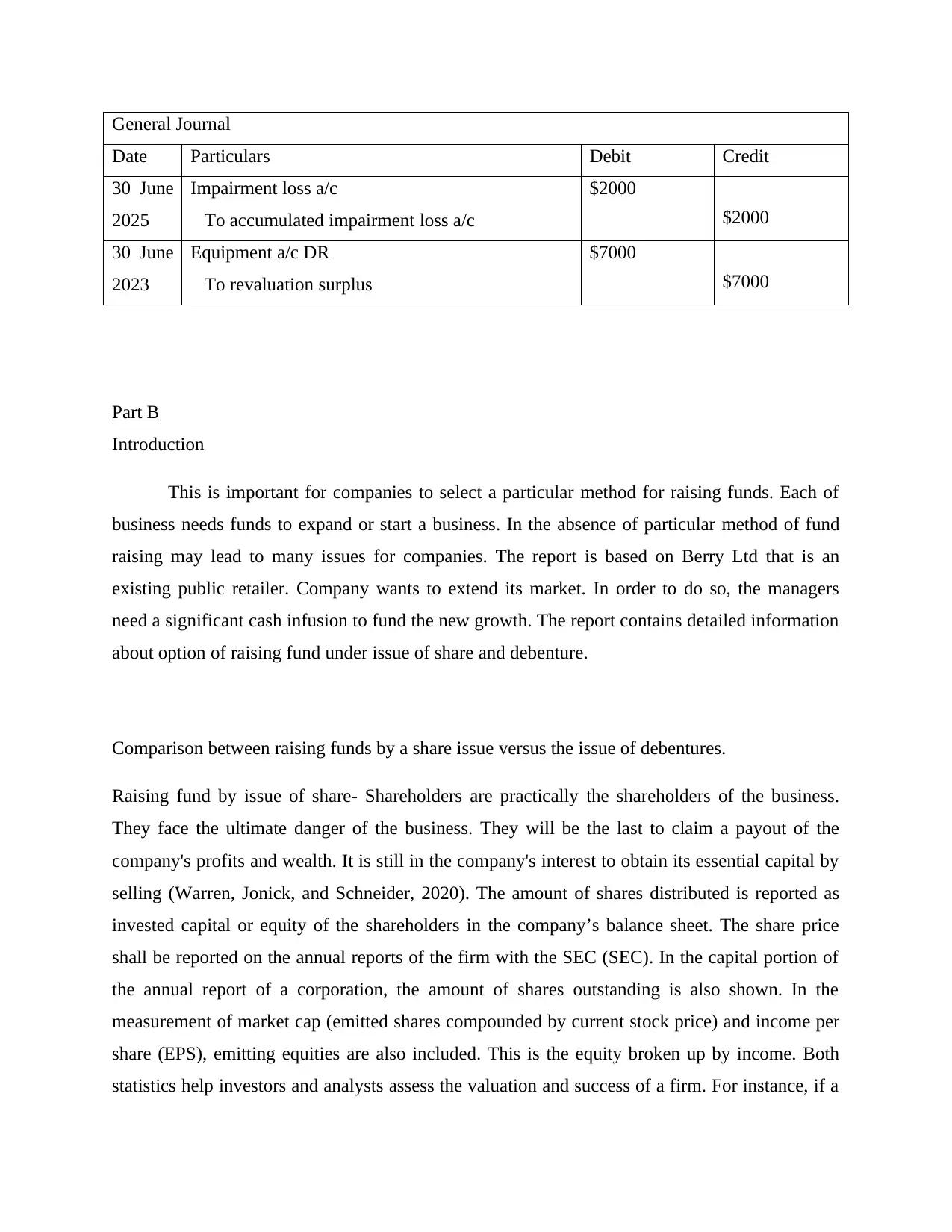

General Journal

Date Particulars Debit Credit

30 June

2025

Impairment loss a/c

To accumulated impairment loss a/c

$2000

$2000

30 June

2023

Equipment a/c DR

To revaluation surplus

$7000

$7000

Part B

Introduction

This is important for companies to select a particular method for raising funds. Each of

business needs funds to expand or start a business. In the absence of particular method of fund

raising may lead to many issues for companies. The report is based on Berry Ltd that is an

existing public retailer. Company wants to extend its market. In order to do so, the managers

need a significant cash infusion to fund the new growth. The report contains detailed information

about option of raising fund under issue of share and debenture.

Comparison between raising funds by a share issue versus the issue of debentures.

Raising fund by issue of share- Shareholders are practically the shareholders of the business.

They face the ultimate danger of the business. They will be the last to claim a payout of the

company's profits and wealth. It is still in the company's interest to obtain its essential capital by

selling (Warren, Jonick, and Schneider, 2020). The amount of shares distributed is reported as

invested capital or equity of the shareholders in the company’s balance sheet. The share price

shall be reported on the annual reports of the firm with the SEC (SEC). In the capital portion of

the annual report of a corporation, the amount of shares outstanding is also shown. In the

measurement of market cap (emitted shares compounded by current stock price) and income per

share (EPS), emitting equities are also included. This is the equity broken up by income. Both

statistics help investors and analysts assess the valuation and success of a firm. For instance, if a

Date Particulars Debit Credit

30 June

2025

Impairment loss a/c

To accumulated impairment loss a/c

$2000

$2000

30 June

2023

Equipment a/c DR

To revaluation surplus

$7000

$7000

Part B

Introduction

This is important for companies to select a particular method for raising funds. Each of

business needs funds to expand or start a business. In the absence of particular method of fund

raising may lead to many issues for companies. The report is based on Berry Ltd that is an

existing public retailer. Company wants to extend its market. In order to do so, the managers

need a significant cash infusion to fund the new growth. The report contains detailed information

about option of raising fund under issue of share and debenture.

Comparison between raising funds by a share issue versus the issue of debentures.

Raising fund by issue of share- Shareholders are practically the shareholders of the business.

They face the ultimate danger of the business. They will be the last to claim a payout of the

company's profits and wealth. It is still in the company's interest to obtain its essential capital by

selling (Warren, Jonick, and Schneider, 2020). The amount of shares distributed is reported as

invested capital or equity of the shareholders in the company’s balance sheet. The share price

shall be reported on the annual reports of the firm with the SEC (SEC). In the capital portion of

the annual report of a corporation, the amount of shares outstanding is also shown. In the

measurement of market cap (emitted shares compounded by current stock price) and income per

share (EPS), emitting equities are also included. This is the equity broken up by income. Both

statistics help investors and analysts assess the valuation and success of a firm. For instance, if a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

start - up company issues 10 million shares out of 20 million approved shares to an individual,

and the investor's stocks are really the only ones given, the proprietor has 100 percent of the

business. Boards usually use the completely filtered or required to work-model estimate for

preparing and forecasting. The Board of Directors, for instance: if the Board feels it should give

an activist two million more shares and gives high-performance staff three million shares, can

provide the founders with extra company shares so that their shareholding percentage cannot

decline dramatically.

Raising fund by issuing debenture- Debenture is a tool provided by the corporation that

acknowledges its loans to the holder. At some percent, debentures bear interest (Schroeder, Clark

and Cathey, 2019). The debt obtained by the corporation shall be reimbursed within a certain

time or at the discretion of the management in compliance with their terms of delivery. The price

where the debentures are sold does not have legal limits. Debentures may be sold at par, at a

discount or at an equity premium.

The corporation's creditors became Debenture holders. They routinely pay interest at a set rate on

their debt securities. It is standard practice to prefix the rate preceding debt securities, i.e. 12%.

In the event of the company dissolved against lenders, debenture holders have preference to pay

their debt and loans. Debenture holders don't worry about the company's equity. The ownership

and ownership of the organization are not concerned.

Comparison:

Basis Share Debenture

Meaning The stock is the corporation's own

funds.

The debt securities are the borrowing

resources of the firm.

What is it The shares comprise the company's

assets.

Debentures are the corporation's

liabilities.

Holders The investor is appointed

shareholders.

The debenture owner is called debenture

holder.

and the investor's stocks are really the only ones given, the proprietor has 100 percent of the

business. Boards usually use the completely filtered or required to work-model estimate for

preparing and forecasting. The Board of Directors, for instance: if the Board feels it should give

an activist two million more shares and gives high-performance staff three million shares, can

provide the founders with extra company shares so that their shareholding percentage cannot

decline dramatically.

Raising fund by issuing debenture- Debenture is a tool provided by the corporation that

acknowledges its loans to the holder. At some percent, debentures bear interest (Schroeder, Clark

and Cathey, 2019). The debt obtained by the corporation shall be reimbursed within a certain

time or at the discretion of the management in compliance with their terms of delivery. The price

where the debentures are sold does not have legal limits. Debentures may be sold at par, at a

discount or at an equity premium.

The corporation's creditors became Debenture holders. They routinely pay interest at a set rate on

their debt securities. It is standard practice to prefix the rate preceding debt securities, i.e. 12%.

In the event of the company dissolved against lenders, debenture holders have preference to pay

their debt and loans. Debenture holders don't worry about the company's equity. The ownership

and ownership of the organization are not concerned.

Comparison:

Basis Share Debenture

Meaning The stock is the corporation's own

funds.

The debt securities are the borrowing

resources of the firm.

What is it The shares comprise the company's

assets.

Debentures are the corporation's

liabilities.

Holders The investor is appointed

shareholders.

The debenture owner is called debenture

holder.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payment of

return

Mostly out of benefit will the

dividends be paid to the owners.

Profit can be charged even without

benefit to debenture holders.

Allowable

deduction

Dividend is tax expenditure and is

also not permitted as deductions.

Income is a cost in operation and is thus

authorized as a tax deduction

(Jiambalvo, 2019).

Trust deed In the event of shares, no

promissory note is performed.

In context of large debentures, trust

deeds shall be conducted.

Repayment When all debts have been paid,

shares shall be returned.

Debentures take precedence over stocks

and are thus refunded before shares.

Impact of each option on each option:

Impact of issue of share capital on financial accounts-

The first impact is on the balance sheet under the cash account. The sum the company

earns for the acquired stock raises the cash account. When receive amount is more than

par value capital, build two cash account entries that assign to each column the benefits

you earn. For example, if company issue an equity share of $20 with a par value of $1,

enter one item labeling the balance sheet cash account "common shares, Par-Value -$1"

and another item called "Capital over Par-Value-$ 19." The result of the inputs raises the

sum of the account to $20, and assets are distributed.

The influence of the issuing of shares on the shareholder's Equity Account is also

growing. The capital earned from the issuance of the stock raises the shareholders '

equity. Enterprises must enter the shareholder’s payment equity on the balance sheet

similarly to the company's cash records (Edwards, 2020). The first entry is called

"ordinary shares-Par Value $1." It can be included in the amount of shares sold in the

deal and the amount of shareholders left to be issued by the business. These numbers

must represent the drop in the amount of shares allowed. On the right hand section of the

balance sheet is the par value earned by the issued stock.

Impact of issue of debenture on financial accounts-

return

Mostly out of benefit will the

dividends be paid to the owners.

Profit can be charged even without

benefit to debenture holders.

Allowable

deduction

Dividend is tax expenditure and is

also not permitted as deductions.

Income is a cost in operation and is thus

authorized as a tax deduction

(Jiambalvo, 2019).

Trust deed In the event of shares, no

promissory note is performed.

In context of large debentures, trust

deeds shall be conducted.

Repayment When all debts have been paid,

shares shall be returned.

Debentures take precedence over stocks

and are thus refunded before shares.

Impact of each option on each option:

Impact of issue of share capital on financial accounts-

The first impact is on the balance sheet under the cash account. The sum the company

earns for the acquired stock raises the cash account. When receive amount is more than

par value capital, build two cash account entries that assign to each column the benefits

you earn. For example, if company issue an equity share of $20 with a par value of $1,

enter one item labeling the balance sheet cash account "common shares, Par-Value -$1"

and another item called "Capital over Par-Value-$ 19." The result of the inputs raises the

sum of the account to $20, and assets are distributed.

The influence of the issuing of shares on the shareholder's Equity Account is also

growing. The capital earned from the issuance of the stock raises the shareholders '

equity. Enterprises must enter the shareholder’s payment equity on the balance sheet

similarly to the company's cash records (Edwards, 2020). The first entry is called

"ordinary shares-Par Value $1." It can be included in the amount of shares sold in the

deal and the amount of shareholders left to be issued by the business. These numbers

must represent the drop in the amount of shares allowed. On the right hand section of the

balance sheet is the par value earned by the issued stock.

Impact of issue of debenture on financial accounts-

Debenture securities are a corporation's liabilities as they reflect potential assets to be

refunded. Present obligations or long-term liabilities exist in the balance sheet. Long-term

commitments are non-refundable loans of one year. Since debenture bonds fall under this

group, they are put in the long-term liability portion of the balance sheet.

When the Corporation has given and is to be charged one year after, it is reflected on the

Balance Sheet on non-current liabilities. If the corporation has given and is due in one

year, so the existing obligations are displayed in the financial statements. The debenture

value for the year (payable or non-payable) is a business cost and is included in the

declaration of income. Any gain in debenture which is extraordinary is also seen in the

Balance sheet in the total liabilities.

If the corporation has acquired debentures, they are known as expenditure and are seen in

the balance sheet under the reserves (Non-Current / Current securities). Debenture

interest is compensation that is reflected in the Declaration of Income. Interest is earned

or accumulated. Any convertible debt interest accrued is displayed in the financial

statements under cash flows.

Advantage of each option for company:

Issue of share capital:

The business does not promise the regular dividend on stock shares, thus, as with

debentures, the business has no defined liability. Dividend payments shall not be charged

out of loss in the event of combined preferred shares (Weygandt, Kieso and Aly, 2020).

Shares shall be distributed without protection or asset fee. Thus, the organization obtains

funds for its investments or also receives coverage without fee.

No refund is required for the funds collected by the issuance of securities. The owners

cannot claim restitution and thus the business has no obligation to reimburse share

capital.

Dividends are not pressured by the corporation. The dividend rate is not even defined on

the equity share. The organization holds adequate reserve in this situation and is

financially stable.

refunded. Present obligations or long-term liabilities exist in the balance sheet. Long-term

commitments are non-refundable loans of one year. Since debenture bonds fall under this

group, they are put in the long-term liability portion of the balance sheet.

When the Corporation has given and is to be charged one year after, it is reflected on the

Balance Sheet on non-current liabilities. If the corporation has given and is due in one

year, so the existing obligations are displayed in the financial statements. The debenture

value for the year (payable or non-payable) is a business cost and is included in the

declaration of income. Any gain in debenture which is extraordinary is also seen in the

Balance sheet in the total liabilities.

If the corporation has acquired debentures, they are known as expenditure and are seen in

the balance sheet under the reserves (Non-Current / Current securities). Debenture

interest is compensation that is reflected in the Declaration of Income. Interest is earned

or accumulated. Any convertible debt interest accrued is displayed in the financial

statements under cash flows.

Advantage of each option for company:

Issue of share capital:

The business does not promise the regular dividend on stock shares, thus, as with

debentures, the business has no defined liability. Dividend payments shall not be charged

out of loss in the event of combined preferred shares (Weygandt, Kieso and Aly, 2020).

Shares shall be distributed without protection or asset fee. Thus, the organization obtains

funds for its investments or also receives coverage without fee.

No refund is required for the funds collected by the issuance of securities. The owners

cannot claim restitution and thus the business has no obligation to reimburse share

capital.

Dividends are not pressured by the corporation. The dividend rate is not even defined on

the equity share. The organization holds adequate reserve in this situation and is

financially stable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Debenture:

Debentures enable higher role as a trustee in the 'pecking order.' The debt is not covered

otherwise-the uncertain role of borrowers at the base of the payment ladder is a far lower

ability to reclaim all cash.

Director's private funds are provided with important financial security and

encouragement.

The use of debt securities can support the development of a company in the long term. In

contrast to other modes of credit, it is also economical (Leone, Minutti-Meza and Wasley,

2019).

Debentures normally provide the issuer with a set interest rate which must be paid off

before the lenders earn any dividends.

Established owners do not minimize shares of the business, and the share of income stays

the same.

Conclusion

On the basis of above report this can be concluded that companies need to select the

appropriate fund raising method. In order to do so companies have to make proper research

related to types of options available, issues and benefits of each option. In the context of above

mentioned company, this can be suggested to owners and boards that they should raise funds

from issuing debentures. It is so because under this company does not need to pay any fixed

amount of interest to holders. As well as company does not need to share their ownership under

this option.

Debentures enable higher role as a trustee in the 'pecking order.' The debt is not covered

otherwise-the uncertain role of borrowers at the base of the payment ladder is a far lower

ability to reclaim all cash.

Director's private funds are provided with important financial security and

encouragement.

The use of debt securities can support the development of a company in the long term. In

contrast to other modes of credit, it is also economical (Leone, Minutti-Meza and Wasley,

2019).

Debentures normally provide the issuer with a set interest rate which must be paid off

before the lenders earn any dividends.

Established owners do not minimize shares of the business, and the share of income stays

the same.

Conclusion

On the basis of above report this can be concluded that companies need to select the

appropriate fund raising method. In order to do so companies have to make proper research

related to types of options available, issues and benefits of each option. In the context of above

mentioned company, this can be suggested to owners and boards that they should raise funds

from issuing debentures. It is so because under this company does not need to pay any fixed

amount of interest to holders. As well as company does not need to share their ownership under

this option.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Warren, C., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Edwards, J.D., 2020. History of public accounting in the United States (Vol. 28). Routledge.

Weygandt, J.J., Kimmel, P.D., Kieso, D.E. and Aly, I.M., 2020. Managerial Accounting: Tools

for Business Decision-Making. John Wiley & Sons.

Leone, A.J., Minutti-Meza, M. and Wasley, C.E., 2019. Influential observations and inference in

accounting research. The Accounting Review, 94(6), pp.337-364.

Warren, C., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Edwards, J.D., 2020. History of public accounting in the United States (Vol. 28). Routledge.

Weygandt, J.J., Kimmel, P.D., Kieso, D.E. and Aly, I.M., 2020. Managerial Accounting: Tools

for Business Decision-Making. John Wiley & Sons.

Leone, A.J., Minutti-Meza, M. and Wasley, C.E., 2019. Influential observations and inference in

accounting research. The Accounting Review, 94(6), pp.337-364.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.