Financial Accounting Report on Tesco Plc: Ratio Analysis and Framework

VerifiedAdded on 2023/01/09

|9

|2163

|44

Report

AI Summary

This report delves into the core principles of financial accounting, starting with an overview of the conceptual framework, its purposes, and the objectives of financial reporting. It discusses globally accepted accounting standards, highlighting their benefits and limitations. The second part of the report focuses on a detailed analysis of Tesco PLC's financial performance, using ratio analysis to evaluate key aspects such as gross profit margin, return on equity, current ratio, quick ratio, debt-to-asset ratio, debt-to-equity ratio, and interest coverage. The analysis covers Tesco's performance over two recent years, comparing the ratios and offering critical evaluations and comments on the company's financial position and trends, considering both internal and external factors influencing the results. The conclusion summarizes the key findings and insights derived from the analysis, emphasizing the significance of financial accounting in providing stakeholders with the necessary information for informed decision-making.

FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a). Conceptual Framework and Its major purposes:...................................................................3

(b). Objectives of Financial Reporting:.......................................................................................3

(c). Globally accepted set of accounting standards and their benefits & limitations:.................5

TASK 2............................................................................................................................................6

Computation of Ratios of Tesco Plc for Two recent years and analysis of computed ratios:.....6

Critical Evaluation and Comments:.............................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a). Conceptual Framework and Its major purposes:...................................................................3

(b). Objectives of Financial Reporting:.......................................................................................3

(c). Globally accepted set of accounting standards and their benefits & limitations:.................5

TASK 2............................................................................................................................................6

Computation of Ratios of Tesco Plc for Two recent years and analysis of computed ratios:.....6

Critical Evaluation and Comments:.............................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Financial accounting term implies to specialise accounting division that maintains

records of the corporation 's financial activities. Using structured criteria, transactions are

documented, listed and reported in fiscal reports or financial statements, like P&L, balance sheet

etc (Schroeder, Clark and Cathey, 2019). The study consists of 2 major task, first covers

comprehensive discussion about conceptual-framework and its purposes, key aims of financial

reporting and, benefits & limitations of GAAP. While Second task covers thorough evaluation of

Ratios and comment on performance of Tesco Plc, UK based top supermarket-chain.

TASK 1

(a). Conceptual Framework and Its major purposes:

Conceptual framework in context of financial reporting relates to system of concepts and

goals which give rise to systematic consistent series of principles or standards for

effective financial reporting (Dennis, 2018).

Purpose of Conceptual Framework:

The vital purposes for the development of the accepted conceptual framework for

the financial reporting are that it establishes a mechanism for the interpretation of accounting

standards, basis for the settlement of accounting conflicts, basic concepts which further

shouldn't be replicated in specified accounting standards.

The another purpose of Framework is to support regulatory bodies and governing bodies

which are responsible for issuing accounting standards, in the formulation and revision of

accounting standard based on common concepts, to support preparers establish standardized

accounting policies with regards to areas not addressed by standards or where selection of

accounting policies is made, and to enable all relevant parties and entities to comprehend and

interpret standards.

(b). Objectives of Financial Reporting:

The primary objective or aim of the financial reporting process is to control , evaluate

and reporting or documenting the incomes/profits of a corporation. The aim of different reports

used in financial reporting is to evaluate key usage of capital-funds, cash flows, market results

and financial stability of corporations. This lets business and its investors to make informed

Financial accounting term implies to specialise accounting division that maintains

records of the corporation 's financial activities. Using structured criteria, transactions are

documented, listed and reported in fiscal reports or financial statements, like P&L, balance sheet

etc (Schroeder, Clark and Cathey, 2019). The study consists of 2 major task, first covers

comprehensive discussion about conceptual-framework and its purposes, key aims of financial

reporting and, benefits & limitations of GAAP. While Second task covers thorough evaluation of

Ratios and comment on performance of Tesco Plc, UK based top supermarket-chain.

TASK 1

(a). Conceptual Framework and Its major purposes:

Conceptual framework in context of financial reporting relates to system of concepts and

goals which give rise to systematic consistent series of principles or standards for

effective financial reporting (Dennis, 2018).

Purpose of Conceptual Framework:

The vital purposes for the development of the accepted conceptual framework for

the financial reporting are that it establishes a mechanism for the interpretation of accounting

standards, basis for the settlement of accounting conflicts, basic concepts which further

shouldn't be replicated in specified accounting standards.

The another purpose of Framework is to support regulatory bodies and governing bodies

which are responsible for issuing accounting standards, in the formulation and revision of

accounting standard based on common concepts, to support preparers establish standardized

accounting policies with regards to areas not addressed by standards or where selection of

accounting policies is made, and to enable all relevant parties and entities to comprehend and

interpret standards.

(b). Objectives of Financial Reporting:

The primary objective or aim of the financial reporting process is to control , evaluate

and reporting or documenting the incomes/profits of a corporation. The aim of different reports

used in financial reporting is to evaluate key usage of capital-funds, cash flows, market results

and financial stability of corporations. This lets business and its investors to make informed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

choices or options about how to handle business operations (Miller and Oldroyd, 2018).

Following are other key objectives of it, as described below:

Provide investors with relevant information and data: Investors always want to see how capital-

funds are being invested back within company and how money has been used effectively.

Financial reporting objective is to lets investors determine whether company is a effective or

reasonable place for making investment.

Thorough review of assets, liabilities and equity-funds: This major aim of financial reporting to

enable different stakeholders with quick and thorough evaluation of corporation's asstes and

liabilities to assess the actual performance and making comparison with other industry and

competitors.

Tracking cash flows: Where's the cash flowing from a business and Where is actually it heading

as well as whether organization making profits? Such answers are crucial to explore – then

financial reporting demonstrate how well a company is doing, and how it might pay its all debts

and keep on growing.

Nature of its different users:

External users: These are not so much involved in company's operations as well as not directly

affect to or affected by company's performance. Here are several major external users:

Government: They require company's information to assess the tax liability as taxes paid

by different corporation is key sources of income to government. Also rules and

legislations issued by government may influence companies' performance.

Creditors and Lenders: These users need the information of a company's performance

as to assess whether company is capable enough to payback loans and credits provided

by them. Also credit terms, support and policies of these users greatly impacts company's

performance.

Internal users: These users directly affect corporation's performance as they are part of a

business organisation. Here below are key internal users:

Employees: These users need company's information as to evaluate and assure that the

company 's performing well in market and jobs are effectively secure within company.

Also being a key resource of an organisation majorly affect business's performance.

Management: They are core responsible personnel towards performance and growth of

organisation. They need most sensitive and critical information of business to take

Following are other key objectives of it, as described below:

Provide investors with relevant information and data: Investors always want to see how capital-

funds are being invested back within company and how money has been used effectively.

Financial reporting objective is to lets investors determine whether company is a effective or

reasonable place for making investment.

Thorough review of assets, liabilities and equity-funds: This major aim of financial reporting to

enable different stakeholders with quick and thorough evaluation of corporation's asstes and

liabilities to assess the actual performance and making comparison with other industry and

competitors.

Tracking cash flows: Where's the cash flowing from a business and Where is actually it heading

as well as whether organization making profits? Such answers are crucial to explore – then

financial reporting demonstrate how well a company is doing, and how it might pay its all debts

and keep on growing.

Nature of its different users:

External users: These are not so much involved in company's operations as well as not directly

affect to or affected by company's performance. Here are several major external users:

Government: They require company's information to assess the tax liability as taxes paid

by different corporation is key sources of income to government. Also rules and

legislations issued by government may influence companies' performance.

Creditors and Lenders: These users need the information of a company's performance

as to assess whether company is capable enough to payback loans and credits provided

by them. Also credit terms, support and policies of these users greatly impacts company's

performance.

Internal users: These users directly affect corporation's performance as they are part of a

business organisation. Here below are key internal users:

Employees: These users need company's information as to evaluate and assure that the

company 's performing well in market and jobs are effectively secure within company.

Also being a key resource of an organisation majorly affect business's performance.

Management: They are core responsible personnel towards performance and growth of

organisation. They need most sensitive and critical information of business to take

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

managerial actions. Also they affects company's performance highly by their decisions,

policies and strategies.

(c). Globally accepted set of accounting standards and their benefits & limitations:

Globally accepted set of accounting standards imply to a collection of guidelines,

principles and procedures used by accounting sector to formulate and streamline annual financial

statements reported to different stakeholders (White, 2017). Here following are several key

benefit and limitations of globally accepted set of accounting standards:

Benefits:

These standards allow companies to ensure precision in their reporting of

annual financial data, reduce risks of misappropriation and eliminate frauds. For example

in a company by adopting such standards, prepare specific guideline for method of

valuation of inventories then there are less chances that staff or internal personnel can

commit any fraud or manipulation.

Such standards are mainly developed to protect the interests of multiple stakeholders ,

including owners. It keeps the businesses accountable for towards financial reporting

operations, thereby offering greater security to all stakeholders.

Through adoption of the these standard's guidelines, businesses have fair and equitable

presentation of its all financial and business information.

Limitations:

These standards attempt to pursue a "one-size-fits-all" concept instead of to consider the

enormous diversity which is often observed between businesses. As a consequence, it

may be challenging for enterprises in other sectors, and also for smaller firms, to follow

these concepts. For instance, a small enterprise that uses commonly accepted accounting

standards that finds GAAP too complicated and fail to integrate all the standards into its

standard/basic financial statements.

For global companies like Tesco Plc it is not possible to follow all globally accepted

accounting standards because in some countries these standards are not followed or

mandatory to follow countries' local standards, this lead to different reporting

complexities (Kourtis, Kourtis and Curtis, 2019).

policies and strategies.

(c). Globally accepted set of accounting standards and their benefits & limitations:

Globally accepted set of accounting standards imply to a collection of guidelines,

principles and procedures used by accounting sector to formulate and streamline annual financial

statements reported to different stakeholders (White, 2017). Here following are several key

benefit and limitations of globally accepted set of accounting standards:

Benefits:

These standards allow companies to ensure precision in their reporting of

annual financial data, reduce risks of misappropriation and eliminate frauds. For example

in a company by adopting such standards, prepare specific guideline for method of

valuation of inventories then there are less chances that staff or internal personnel can

commit any fraud or manipulation.

Such standards are mainly developed to protect the interests of multiple stakeholders ,

including owners. It keeps the businesses accountable for towards financial reporting

operations, thereby offering greater security to all stakeholders.

Through adoption of the these standard's guidelines, businesses have fair and equitable

presentation of its all financial and business information.

Limitations:

These standards attempt to pursue a "one-size-fits-all" concept instead of to consider the

enormous diversity which is often observed between businesses. As a consequence, it

may be challenging for enterprises in other sectors, and also for smaller firms, to follow

these concepts. For instance, a small enterprise that uses commonly accepted accounting

standards that finds GAAP too complicated and fail to integrate all the standards into its

standard/basic financial statements.

For global companies like Tesco Plc it is not possible to follow all globally accepted

accounting standards because in some countries these standards are not followed or

mandatory to follow countries' local standards, this lead to different reporting

complexities (Kourtis, Kourtis and Curtis, 2019).

TASK 2

Computation of Ratios of Tesco Plc for Two recent years and analysis of computed ratios:

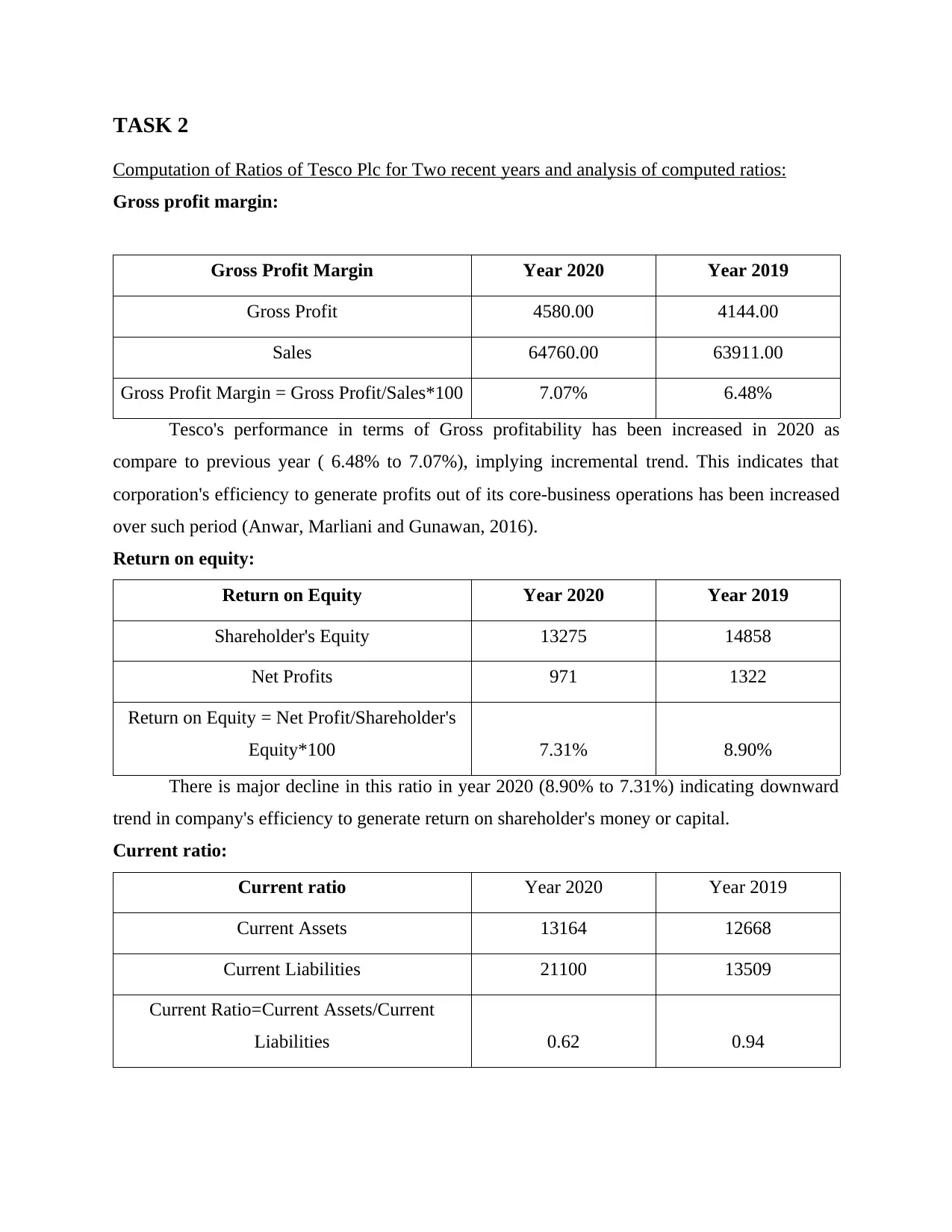

Gross profit margin:

Gross Profit Margin Year 2020 Year 2019

Gross Profit 4580.00 4144.00

Sales 64760.00 63911.00

Gross Profit Margin = Gross Profit/Sales*100 7.07% 6.48%

Tesco's performance in terms of Gross profitability has been increased in 2020 as

compare to previous year ( 6.48% to 7.07%), implying incremental trend. This indicates that

corporation's efficiency to generate profits out of its core-business operations has been increased

over such period (Anwar, Marliani and Gunawan, 2016).

Return on equity:

Return on Equity Year 2020 Year 2019

Shareholder's Equity 13275 14858

Net Profits 971 1322

Return on Equity = Net Profit/Shareholder's

Equity*100 7.31% 8.90%

There is major decline in this ratio in year 2020 (8.90% to 7.31%) indicating downward

trend in company's efficiency to generate return on shareholder's money or capital.

Current ratio:

Current ratio Year 2020 Year 2019

Current Assets 13164 12668

Current Liabilities 21100 13509

Current Ratio=Current Assets/Current

Liabilities 0.62 0.94

Computation of Ratios of Tesco Plc for Two recent years and analysis of computed ratios:

Gross profit margin:

Gross Profit Margin Year 2020 Year 2019

Gross Profit 4580.00 4144.00

Sales 64760.00 63911.00

Gross Profit Margin = Gross Profit/Sales*100 7.07% 6.48%

Tesco's performance in terms of Gross profitability has been increased in 2020 as

compare to previous year ( 6.48% to 7.07%), implying incremental trend. This indicates that

corporation's efficiency to generate profits out of its core-business operations has been increased

over such period (Anwar, Marliani and Gunawan, 2016).

Return on equity:

Return on Equity Year 2020 Year 2019

Shareholder's Equity 13275 14858

Net Profits 971 1322

Return on Equity = Net Profit/Shareholder's

Equity*100 7.31% 8.90%

There is major decline in this ratio in year 2020 (8.90% to 7.31%) indicating downward

trend in company's efficiency to generate return on shareholder's money or capital.

Current ratio:

Current ratio Year 2020 Year 2019

Current Assets 13164 12668

Current Liabilities 21100 13509

Current Ratio=Current Assets/Current

Liabilities 0.62 0.94

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

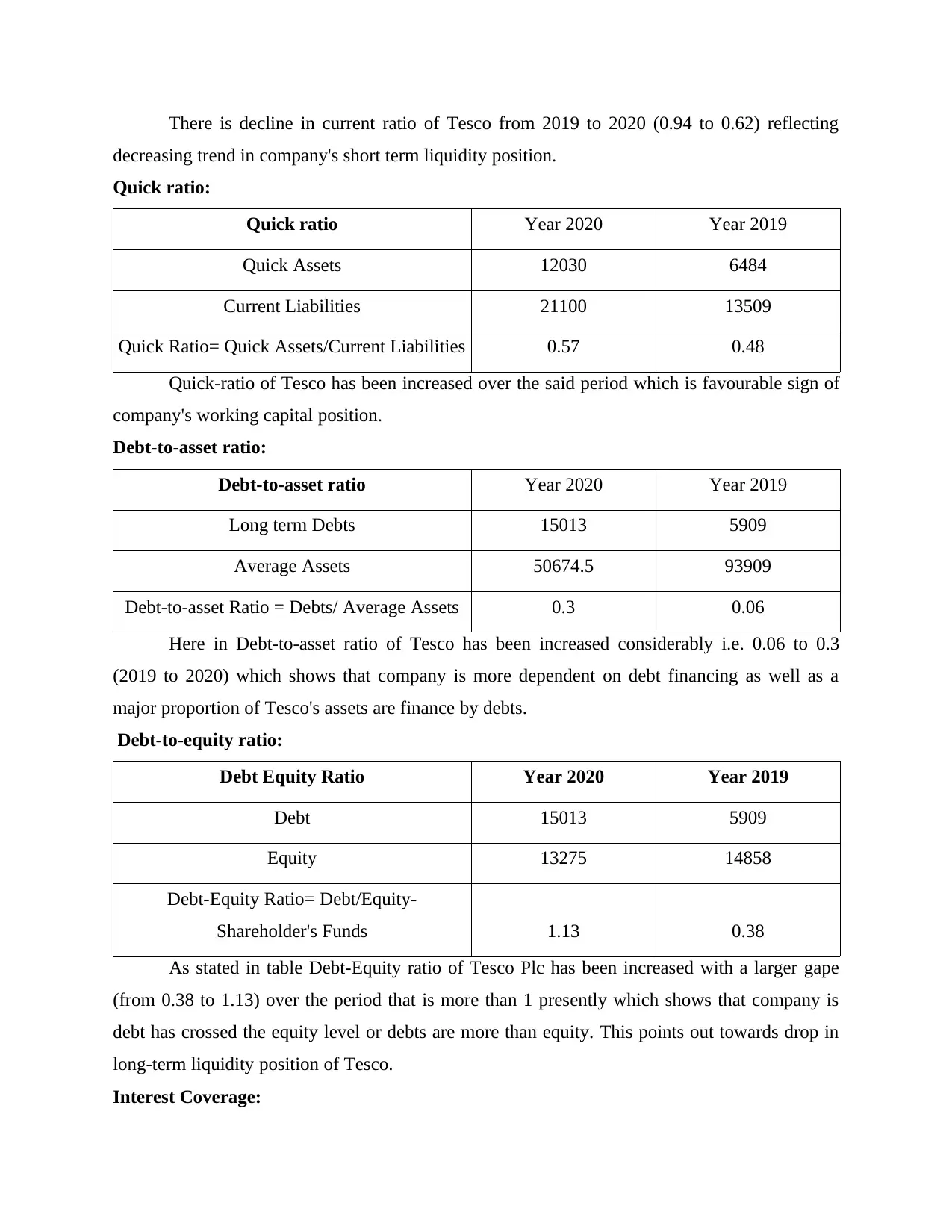

There is decline in current ratio of Tesco from 2019 to 2020 (0.94 to 0.62) reflecting

decreasing trend in company's short term liquidity position.

Quick ratio:

Quick ratio Year 2020 Year 2019

Quick Assets 12030 6484

Current Liabilities 21100 13509

Quick Ratio= Quick Assets/Current Liabilities 0.57 0.48

Quick-ratio of Tesco has been increased over the said period which is favourable sign of

company's working capital position.

Debt-to-asset ratio:

Debt-to-asset ratio Year 2020 Year 2019

Long term Debts 15013 5909

Average Assets 50674.5 93909

Debt-to-asset Ratio = Debts/ Average Assets 0.3 0.06

Here in Debt-to-asset ratio of Tesco has been increased considerably i.e. 0.06 to 0.3

(2019 to 2020) which shows that company is more dependent on debt financing as well as a

major proportion of Tesco's assets are finance by debts.

Debt-to-equity ratio:

Debt Equity Ratio Year 2020 Year 2019

Debt 15013 5909

Equity 13275 14858

Debt-Equity Ratio= Debt/Equity-

Shareholder's Funds 1.13 0.38

As stated in table Debt-Equity ratio of Tesco Plc has been increased with a larger gape

(from 0.38 to 1.13) over the period that is more than 1 presently which shows that company is

debt has crossed the equity level or debts are more than equity. This points out towards drop in

long-term liquidity position of Tesco.

Interest Coverage:

decreasing trend in company's short term liquidity position.

Quick ratio:

Quick ratio Year 2020 Year 2019

Quick Assets 12030 6484

Current Liabilities 21100 13509

Quick Ratio= Quick Assets/Current Liabilities 0.57 0.48

Quick-ratio of Tesco has been increased over the said period which is favourable sign of

company's working capital position.

Debt-to-asset ratio:

Debt-to-asset ratio Year 2020 Year 2019

Long term Debts 15013 5909

Average Assets 50674.5 93909

Debt-to-asset Ratio = Debts/ Average Assets 0.3 0.06

Here in Debt-to-asset ratio of Tesco has been increased considerably i.e. 0.06 to 0.3

(2019 to 2020) which shows that company is more dependent on debt financing as well as a

major proportion of Tesco's assets are finance by debts.

Debt-to-equity ratio:

Debt Equity Ratio Year 2020 Year 2019

Debt 15013 5909

Equity 13275 14858

Debt-Equity Ratio= Debt/Equity-

Shareholder's Funds 1.13 0.38

As stated in table Debt-Equity ratio of Tesco Plc has been increased with a larger gape

(from 0.38 to 1.13) over the period that is more than 1 presently which shows that company is

debt has crossed the equity level or debts are more than equity. This points out towards drop in

long-term liquidity position of Tesco.

Interest Coverage:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

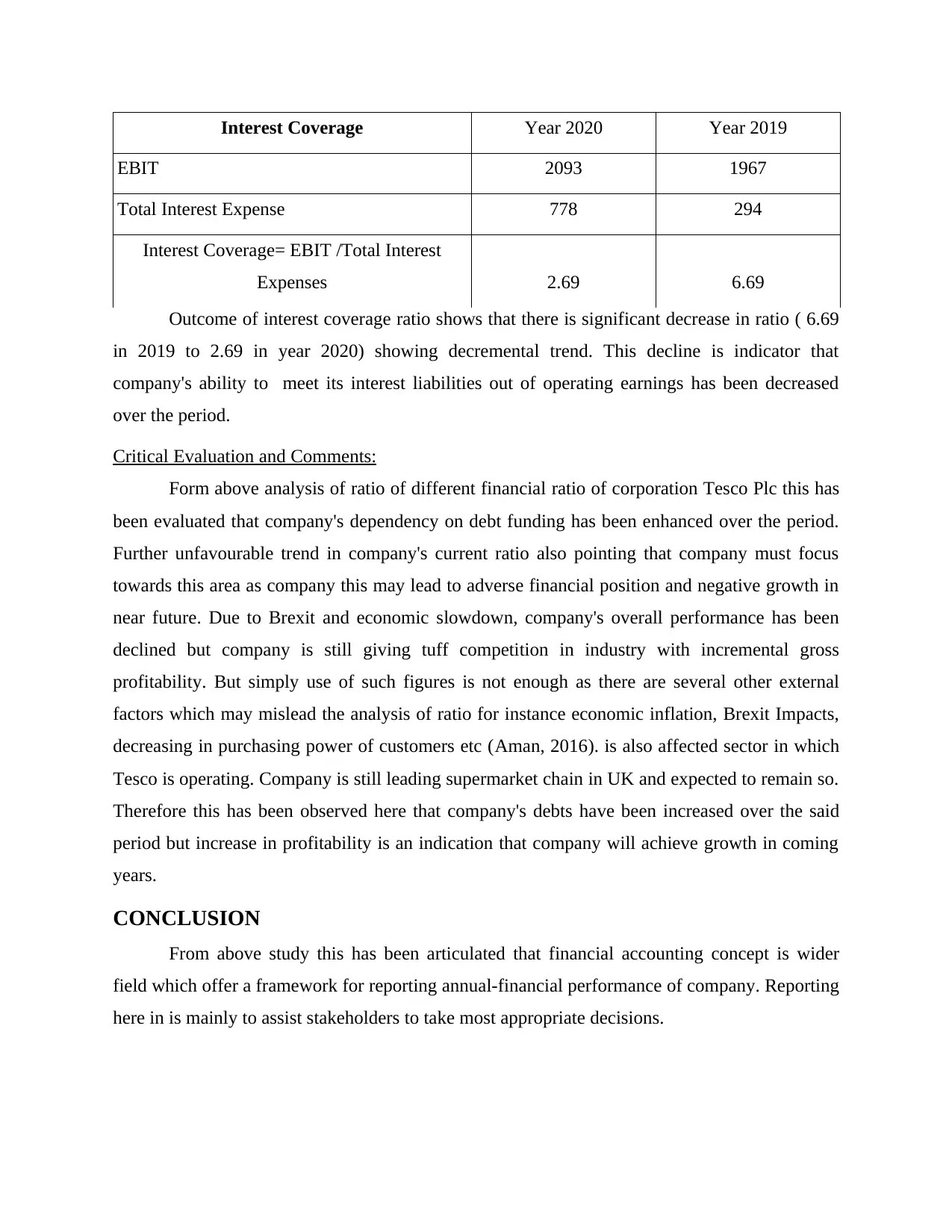

Interest Coverage Year 2020 Year 2019

EBIT 2093 1967

Total Interest Expense 778 294

Interest Coverage= EBIT /Total Interest

Expenses 2.69 6.69

Outcome of interest coverage ratio shows that there is significant decrease in ratio ( 6.69

in 2019 to 2.69 in year 2020) showing decremental trend. This decline is indicator that

company's ability to meet its interest liabilities out of operating earnings has been decreased

over the period.

Critical Evaluation and Comments:

Form above analysis of ratio of different financial ratio of corporation Tesco Plc this has

been evaluated that company's dependency on debt funding has been enhanced over the period.

Further unfavourable trend in company's current ratio also pointing that company must focus

towards this area as company this may lead to adverse financial position and negative growth in

near future. Due to Brexit and economic slowdown, company's overall performance has been

declined but company is still giving tuff competition in industry with incremental gross

profitability. But simply use of such figures is not enough as there are several other external

factors which may mislead the analysis of ratio for instance economic inflation, Brexit Impacts,

decreasing in purchasing power of customers etc (Aman, 2016). is also affected sector in which

Tesco is operating. Company is still leading supermarket chain in UK and expected to remain so.

Therefore this has been observed here that company's debts have been increased over the said

period but increase in profitability is an indication that company will achieve growth in coming

years.

CONCLUSION

From above study this has been articulated that financial accounting concept is wider

field which offer a framework for reporting annual-financial performance of company. Reporting

here in is mainly to assist stakeholders to take most appropriate decisions.

EBIT 2093 1967

Total Interest Expense 778 294

Interest Coverage= EBIT /Total Interest

Expenses 2.69 6.69

Outcome of interest coverage ratio shows that there is significant decrease in ratio ( 6.69

in 2019 to 2.69 in year 2020) showing decremental trend. This decline is indicator that

company's ability to meet its interest liabilities out of operating earnings has been decreased

over the period.

Critical Evaluation and Comments:

Form above analysis of ratio of different financial ratio of corporation Tesco Plc this has

been evaluated that company's dependency on debt funding has been enhanced over the period.

Further unfavourable trend in company's current ratio also pointing that company must focus

towards this area as company this may lead to adverse financial position and negative growth in

near future. Due to Brexit and economic slowdown, company's overall performance has been

declined but company is still giving tuff competition in industry with incremental gross

profitability. But simply use of such figures is not enough as there are several other external

factors which may mislead the analysis of ratio for instance economic inflation, Brexit Impacts,

decreasing in purchasing power of customers etc (Aman, 2016). is also affected sector in which

Tesco is operating. Company is still leading supermarket chain in UK and expected to remain so.

Therefore this has been observed here that company's debts have been increased over the said

period but increase in profitability is an indication that company will achieve growth in coming

years.

CONCLUSION

From above study this has been articulated that financial accounting concept is wider

field which offer a framework for reporting annual-financial performance of company. Reporting

here in is mainly to assist stakeholders to take most appropriate decisions.

REFERENCES

Books and Journals:

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Dennis, I., 2018. What is a conceptual framework for financial reporting?. Accounting in

Europe, 15(3), pp.374-401.

Miller, A.D. and Oldroyd, D., 2018. An economics perspective on financial reporting

objectives. Australian Accounting Review, 28(1), pp.104-108.

White, M.J., 2017. A US imperative: High-quality, globally accepted accounting

standards. Public Statement. Available at: https://www. sec. gov/news/statement/white-

2016-01-05. html (accessed 27 October 2018).

Kourtis, E., Kourtis, G. and Curtis, P., 2019. Αn Integrated Financial Ratio Analysis as a

Navigation Compass through the Fraudulent Reporting Conundrum: Α Case

Study. International Journal of Finance, Insurance and Risk Management, 9(1-2), pp.3-

20.

Anwar, K., Marliani, G. and Gunawan, C.I., 2016. Financial ratio analysis for increasing the

financial performance of the company at Bank Bukopin. IJSBAR, 29(2), p.231236.

Aman, S.M., 2016. Analysis of financial statements using ratio analysis for the last 5 years.

Books and Journals:

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Dennis, I., 2018. What is a conceptual framework for financial reporting?. Accounting in

Europe, 15(3), pp.374-401.

Miller, A.D. and Oldroyd, D., 2018. An economics perspective on financial reporting

objectives. Australian Accounting Review, 28(1), pp.104-108.

White, M.J., 2017. A US imperative: High-quality, globally accepted accounting

standards. Public Statement. Available at: https://www. sec. gov/news/statement/white-

2016-01-05. html (accessed 27 October 2018).

Kourtis, E., Kourtis, G. and Curtis, P., 2019. Αn Integrated Financial Ratio Analysis as a

Navigation Compass through the Fraudulent Reporting Conundrum: Α Case

Study. International Journal of Finance, Insurance and Risk Management, 9(1-2), pp.3-

20.

Anwar, K., Marliani, G. and Gunawan, C.I., 2016. Financial ratio analysis for increasing the

financial performance of the company at Bank Bukopin. IJSBAR, 29(2), p.231236.

Aman, S.M., 2016. Analysis of financial statements using ratio analysis for the last 5 years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.