Financial Accounting Report: International Manufacturers Ltd Analysis

VerifiedAdded on 2020/10/23

|9

|2005

|249

Report

AI Summary

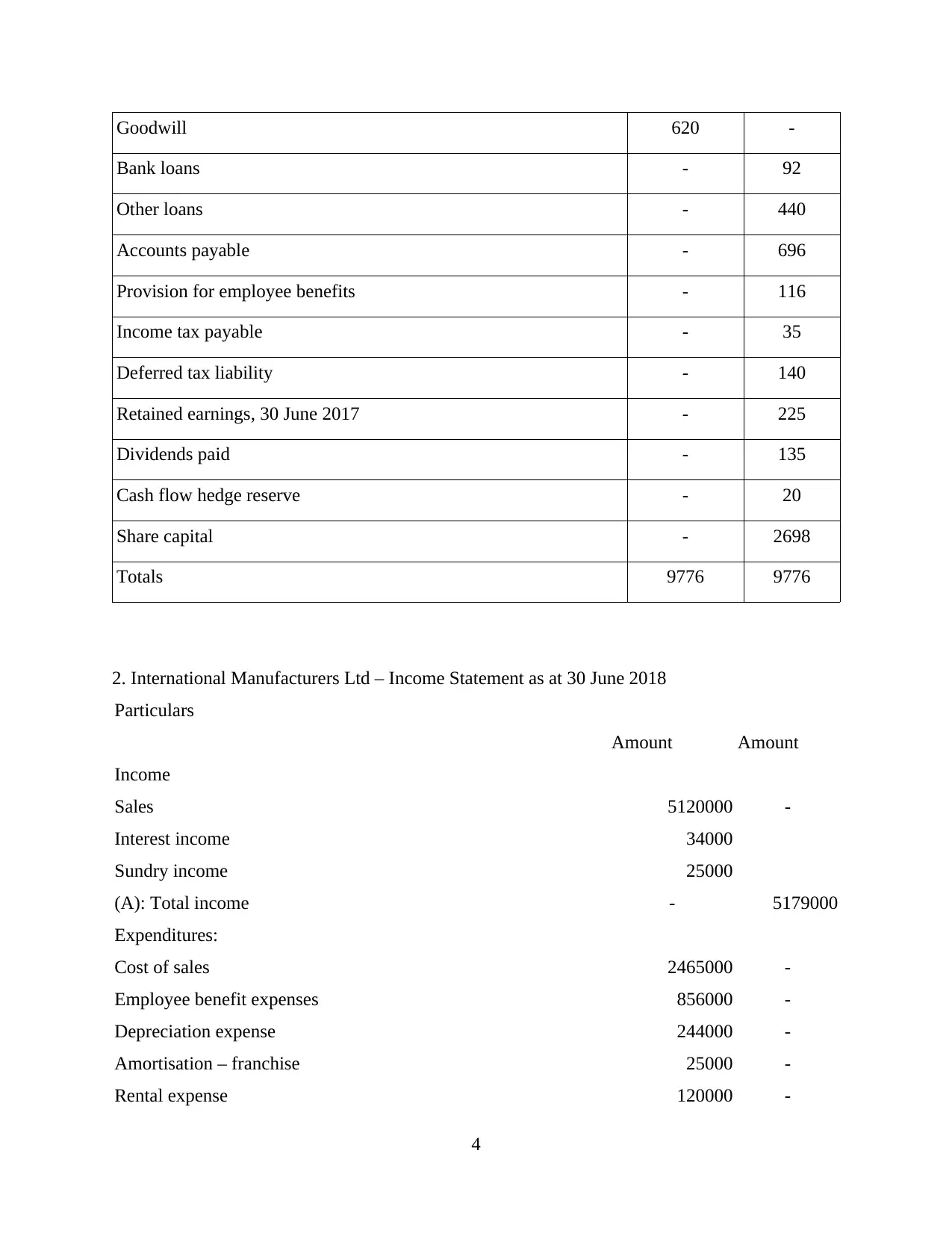

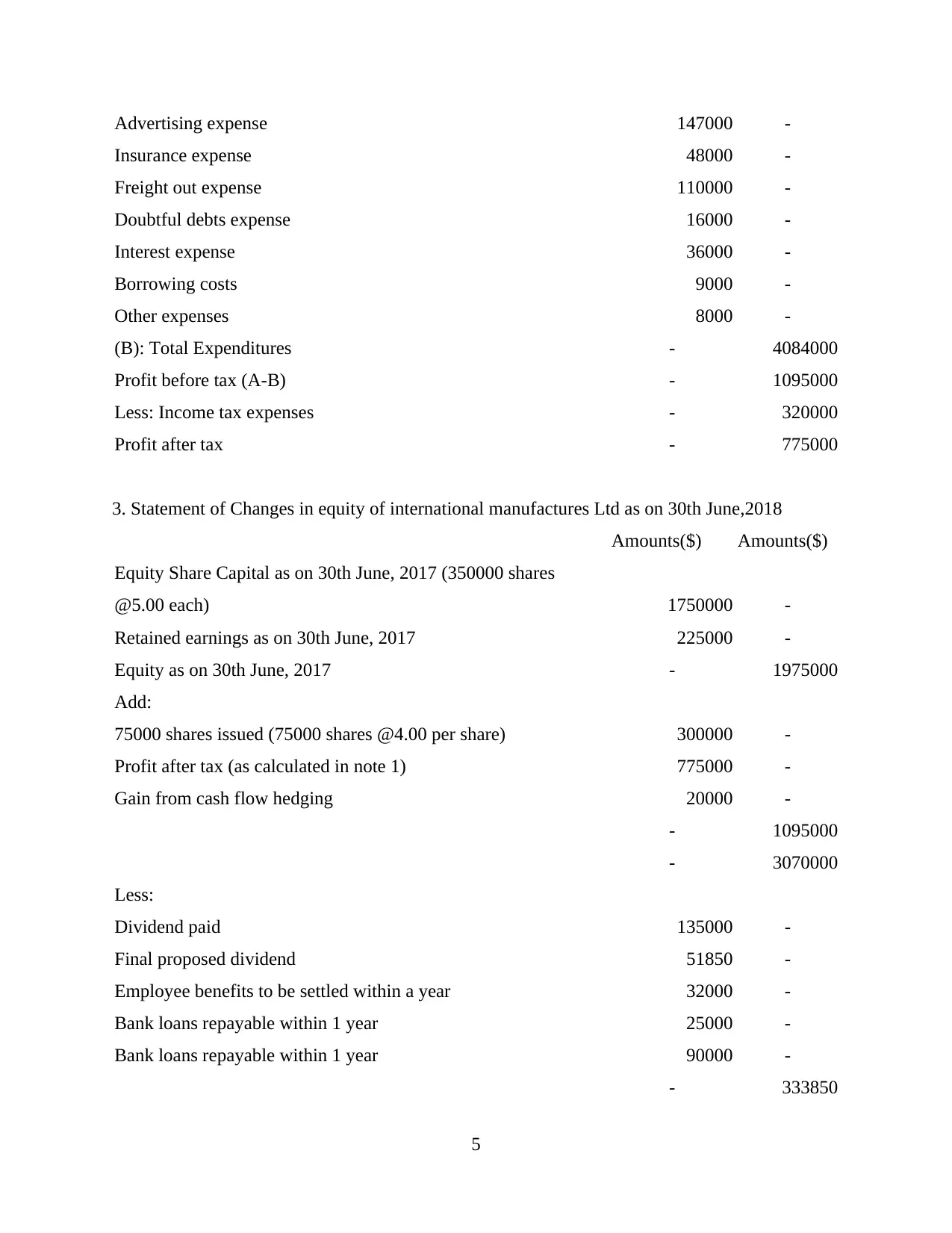

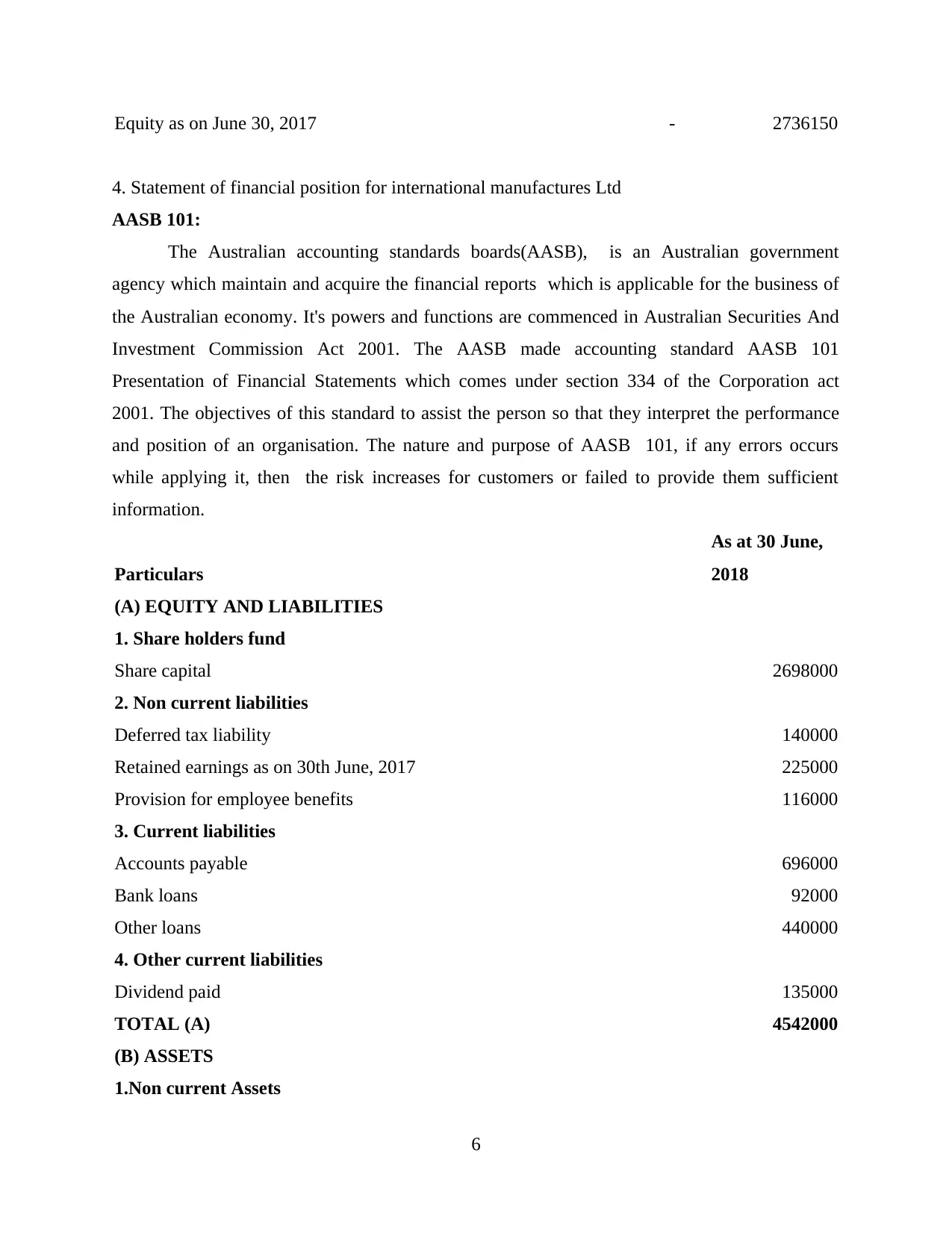

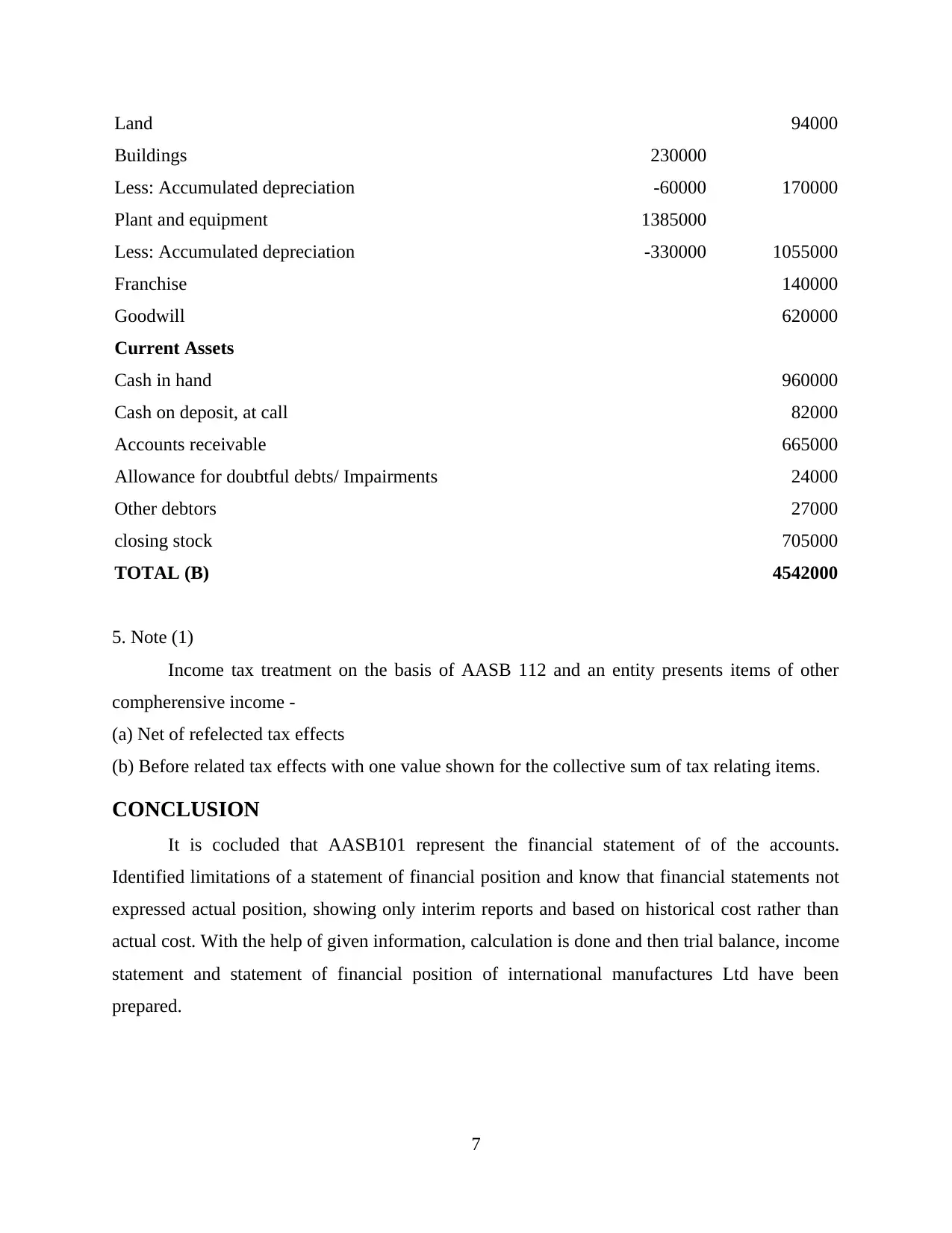

This report provides a comprehensive overview of financial accounting, focusing on the limitations of financial statements and the preparation of key financial reports. The report begins with an introduction to financial accounting and the purpose of financial statements, followed by a detailed discussion of the limitations inherent in these statements, such as the use of historical cost, the presentation of only interim reports, and the lack of exact financial positions. The main body of the report includes a trial balance, income statement, statement of changes in equity, and statement of financial position for International Manufacturers Ltd, all prepared in accordance with AASB 101. The report also includes detailed calculations and analyses of the financial data. The conclusion summarizes the key findings, emphasizing the importance of understanding the limitations of financial statements. The report is supported by relevant references, providing a solid foundation for understanding financial accounting principles and practices.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.